Price Action Trade Results of M.A. Perry

Price Action Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htm &

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Users Reviews, Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htm Review of TheStrategyLab: http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 &

http://www.thestrategylab.com/thestrategylab-reviews.htmPrice Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Telephone: +1 708 572-4885

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

Attachment:

040418-wrbtrader-Price-Action-Trading-Broker-PnL-Statement-Profit+3837.50.png [ 76.82 KiB | Viewed 346 times ]

040418-wrbtrader-Price-Action-Trading-Broker-PnL-Statement-Profit+3837.50.png [ 76.82 KiB | Viewed 346 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini RTY ($RTY_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$3,837.50 dollars or +76.75 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,837.50 dollars Russell 2000 Emini RTY Futures: 1 tick or 0.10 = $5.00 dollars and there's more contract information @

CMEGroup (formerly as TF @

The ICE)

S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log & Price Action Analysis is archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=179&t=2791 All of my trades are posted

real-time at the above link for today's archive chat log in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader for anyone to do a real-time review (you must be a member of the chat room for a real-time review). Although the trades and price action analysis are posted by me and other users of WRB Analysis in real-time...review of TheStrategyLab is that this is

not a signal calling chat room

nor is this a live trading room that has a head trader telling you what to do. I'm the moderator (I keep the peace between members) and my own live trades are posted within 3.2 seconds on average

after the trade confirmation in my broker trade execution platform via an

auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility...all key concepts from the WRB Analysis free study guide even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room

nor is it a live trading room with a head trader even though members of the chat room are posting their trades & market analysis in real-time. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the

primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback about

your own trading and for members to help each other...as in more eyes on the market. In addition, we

highly recommend that you use the free chat room with a professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they can provide you with the

quantitative statistical analysis of your trading. You can then download your results and post them in your private thread at the forum.

Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your quantitative statistical analysis, brokerage statements in the free chat room. Instead, its highly recommended that you only post that particular information in your private thread for

security reasons. Yet, if you want to post that type of information at another website, blog or chat room...that's your choice.

TheStrategyLab free chat room is on IRC via

users request because the IRC servers are located in many different countries, software in many different languages, many different mobile apps, many different types of social media software can be used to log in along with IRC being easier to moderate via

script codes when trouble makers, spammers and trolls show up. I'm the

moderator of the free chat room via the user name

wrbtrader. Thus, I

keep the peace between members without hesitation in removing problematic traders so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets without being

trolled or harassed.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell nor do we allow the free chat room to be used for mentoring because we do

not offer a mentoring service. The

purpose of TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. If you join the free chat room and then you decide to

not post any WRB Analysis about the price action or you decide to not post your trades or you decide to be silent (lurk without saying a word about today's markets)...you're not using the free chat room properly to help improve your trading.

In fact, we do

not want silent (lurkers) traders to join the free chat room unless they are actively posting at the forum about their trading after the markets close.

Access instructions for the free chat room

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Quote:

All of my real-time posted trades involves price action concepts from

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always backtesting new concepts of WRB Analysis, new trade entry rules, new trade management rules, new position size management rules before application in real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades or sharing the new concepts with fee-base clients...living up to the name of my website.

TheStrategyLab.

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=350&t=3706 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini RTY futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

Attachment:

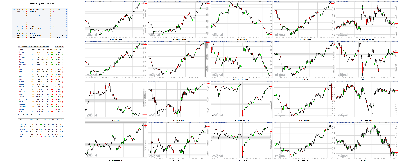

040418-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.99 MiB | Viewed 337 times ]

040418-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.99 MiB | Viewed 337 times ]

click on the above image to view today's price action of key markets discussed by members of TheStrategyLab chat room or private thread discussions The Market at 04:30PM ETDow: +230.94… | Nasdaq: +100.83… | S&P: +30.24…

NASDAQ Vol: 2.2 bln… Adv: 2183… Dec: 738…

NYSE Vol: 855.3 mln… Adv: 2014… Dec: 917…

Moving the Market

China retaliates against Trump administration's tariffs by announcing duties on U.S. imports worth around $50 billion in total

NEC Director Larry Kudlow tells reporters that there is a chance the China tariffs do not go into effect; says President Trump wants to painlessly solve China trade issue

The industrials and energy sectors underperform, while the consumer discretionary and consumer staples groups show relative strength

Sector Watch

Strong: Consumer Discretionary, Technology, Consumer Staples, Health Care

Weak: Industrials, Energy, Materials, Utilities

04:30PM ET

[BRIEFING.COM] Stocks fought through trade war fears on Wednesday to advance for the second session in a row. The S&P 500, which opened Wednesday with a loss of around 1.5%, finished higher by 1.2% at 2644.69. The Nasdaq and the Dow also opened solidly lower, but ended with gains of 1.5% and 1.0%, respectively, advancing to 7042.11 and 24264.30.

Newly unveiled tariff plans between the world's two largest economies left investors feeling a bit uneasy on Wednesday morning; the Trump administration announced a plan to impose tariffs of 25% on Chinese imports across 1,300 product categories worth $50 billion in total, and China retaliated by announcing a similar plan, calling for duties of 25% on American imports across 106 product categories -- including soybeans, planes, cars, and chemicals -- also worth approximately $50 billion in total. However, the realization that the tariffs have yet to be put in force provided some comfort to investors.

The specific turnaround point for the market came mid-morning when NEC Director Larry Kudlow told reporters that there is a chance that the China tariffs do not go into effect, emphasizing that President Trump wants to solve the China trade issue with the least amount of pain possible. Stocks began trimming losses immediately after the opening bell, eventually triggering some short-covering activity that further accelerated the upward move. The major averages finished near their best marks of the day.

10 of 11 S&P sectors closed Wednesday's session in positive territory, with seven adding more than 1.0%. The consumer discretionary sector (+1.8%) was the best-performing group, with just about all of its components finishing in the green. Amazon (AMZN 1410.57, +18.52) rallied 1.3%, while homebuilders showed particular strength after Lennar (LEN 62.82, +5.73) reported better-than-expected earnings for its fiscal first quarter; LEN shares jumped 10.0%, and the iShares U.S. Home Construction ETF (ITB 40.52, +1.80) added 4.7%.

The top-weighted technology (+1.4%) and financials (+1.1%) sectors performed in-line with, or slightly better than, the broader market, but the industrial space (+0.4%) underperformed, as names with a large exposure to China, including Dow component Boeing (BA 327.44, -3.38), struggled; BA shares lost 1.0%. The utilities space (+0.2%) also lagged, and the energy sector was the only group to finish in negative territory, shedding 0.1%.

U.S. Treasuries finished Wednesday on a mostly lower note, pushing yields a tick higher; the benchmark 10-yr yield climbed one basis point to 2.79%. Elsewhere, West Texas Intermediate crude futures declined 0.2% to $63.37/bbl, gold futures advanced 0.3% to $1340.60/oz, and the U.S. Dollar Index ticked down 0.1% to 89.80.

Reviewing Wednesday's economic data, which included the ADP Employment Report for March, the ISM Services Index for March, and Factory Orders for February:

The ADP National Employment Report showed an increase of 241,000 in March (Briefing.com consensus 203,000). The January reading was revised to 246,000 from 235,000.

This report should solidify expectations for another strong nonfarm payrolls number when the government releases the Employment Situation Report on Friday.

The ISM Services Index for March dipped to 58.8 (Briefing.com consensus 59.0) from an unrevised reading of 59.5 in February.

The key takeaway from the report is that the services sector is still growing nicely, albeit at a slightly slower pace than February.

The Factory Orders report for February showed an increase of 1.2% (Briefing.com consensus +1.8%). The January reading was revised to -1.3% from -1.4%.

The key takeaway from the report is that it revealed a rebound in business spending, evidenced by the 1.4% increase in orders for nondefense capital goods excluding aircraft.

On Thursday, investors will receive the Trade Balance for February (Briefing.com consensus -$56.7 billion) and weekly Initial Claims (Briefing.com consensus 255K).

Nasdaq Composite: +2.0% YTD

S&P 500: -1.1% YTD

Dow Jones Industrial Average: -1.8% YTD

Russell 2000: -0.3% YTD

Dow: +230.94… | Nasdaq: +100.83… | S&P: +30.24…

NASDAQ Adv/Dec 2183/738. …NYSE Adv/Dec 2014/917.

03:45PM ET

[BRIEFING.COM]

Commodities ending the day lower

Overall, commodities, as measured by the Bloomberg Commodity Index, are -0.4% at 86.6218

The dollar index is -0.1% at 89.79

Energy:

Mar WTI crude oil futures settled -$0.09 at $63.35/barrel on the day

In other energy, Mar natural gas settled +$0.02 at $2.72/MMBtu

Metals:

Apr gold settled +$2.80 at $1340.10/oz, while Mar silver settled -$0.13 to $16.26/oz

Mar copper settled -$0.05 at $3.01/lb

Dow: +222.67… | Nasdaq: +95.12… | S&P: +29.03…

NASDAQ Adv/Dec 2172/768. …NYSE Adv/Dec 1946/981.

02:55PM ET

[BRIEFING.COM] Stocks have shot to new session highs in recent trade, with the S&P 500 doubling its gain to 0.7%.

Retailers are rallying, evidenced by the 2.3% increase in the SPDR S&P Retail ETF (XRT 44.70, +1.01), with names like Target (TGT 71.39, +1.86), Ross Stores (ROST 78.11, +1.91), Best Buy (BBY 72.87, +2.53), and Macy's (M 29.96, +0.97) showing particular strength; the four companies are up between 2.5% and 3.5%.

Meanwhile, in the bond market, U.S. Treasuries are mixed; the 10-yr yield is up one basis point at 2.79%, while the 2-yr yield is down one basis point at 2.28%.

Dow: +108.33… | Nasdaq: +54.37… | S&P: +17.48…

NASDAQ Adv/Dec 1622/480. …NYSE Adv/Dec 1792/1114.

02:30PM ET

[BRIEFING.COM] The major averages have now all turned higher in afternoon action, sporting gains between 0.1% and 0.6% apiece.

Checking in on the S&P sectors, six of eleven trade in negative territory on Wednesday; the worst losses come out of the energy (-1.3%) sector where bellwether names Exxon Mobil (XOM 74.51, -0.50), Schlumberger (SLB 64.39, -0.40), and ConocoPhillips (COP 59.23, -0.79) each sport losses of worse than 1.0%. The sector is weaker in part due to the earlier released Energy Information Administration data, which revealed a draw on crude inventories vs an expected build.

Leading action higher today, the consumer staples (+1.2%) sector is enjoying solid moves in beverage names like Coca-Cola (KO 44.18, +0.80, +1.9%) and PepsiCo (PEP 110.34, +2.15, +2.0%), with a decent performance out of consumer goods company Procter & Gamble (PG 79.24, +0.78, +1.0%) to boot. Also adding a lift are food names like Hormel Foods (HRL 36.26, +2.04, +6.0%), Campbell Soup (CPB 43.51, +1.23, +2.9%), and Kellogg (K 65.22, +1.85, +2.9%).

Dow: +12.26… | Nasdaq: +39.91… | S&P: +2.27…

NASDAQ Adv/Dec 1615/602. …NYSE Adv/Dec 1625/1272.

02:00PM ET

[BRIEFING.COM] The broader market has held steady since our last update, albeit in a losing fashion.

Gold futures for June delivery settled Wednesday up 0.2% to about $1340.20/oz, propped up by ongoing trade war fears which stemmed from China's new tariff plan which came in retaliation to U.S. tariffs on Chinese goods.

As a reminder, the Trump administration on Tuesday revealed a plan to impose tariffs of 25% on Chinese imports across 1,300 product categories worth $50 billion in total; China responded by announcing a similar plan, calling for duties of 25% on American imports across 106 product categories worth about $50 billion in total.

The US Dollar Index shows losses around 0.1% to 90.10 in recent action, also aiding the advance in gold.

Dow: -102.00… | Nasdaq: -7.51… | S&P: -3.28…

NASDAQ Adv/Dec 1366/915. …NYSE Adv/Dec 1255/1643.

01:30PM ET

[BRIEFING.COM] The major U.S. indices remain lower in today's trade, but are showing just fractional losses at this time after stocks staged a meaningful recovery off of this morning's 'trade-war' fear lows.

A look inside the Dow Jones Industrial Average shows that Boeing (BA 321.69, -2.13), Caterpillar (CAT 142.28, -2.78), & Intel (INTC 49.02, -0.73) are underperforming after China announced a new 25% tariff on certain imported products from the U.S..

Conversely, Nike (NKE 67.76, +1.06) is the best-performing Dow component as consumer discretionary names display relative strength after being excluded from China's retaliatory tariff on US goods.

At current levels, the DJIA is down 0.88% this week.

Dow: -93.03… | Nasdaq: -4.17… | S&P: -4.86…

NASDAQ Adv/Dec 1367/934. …NYSE Adv/Dec 1213/1670.

01:05PM ET

[BRIEFING.COM] The U.S. equity market got off to a poor start this morning, but has made up for it since. The S&P 500 is currently up 0.1%, hovering at its best mark of the day, after opening with a loss of around 1.5%. Meanwhile, the Nasdaq Composite is up 0.2%, and the Dow Jones Industrial Average is down 0.2%.

Trade war fears were dialed up this morning after China unveiled a new tariff plan in retaliation to U.S. tariffs on Chinese goods. The Trump administration on Tuesday revealed a plan to impose tariffs of 25% on Chinese imports across 1,300 product categories worth $50 billion in total; China responded by announcing a similar plan, calling for duties of 25% on American imports across 106 product categories worth approximately $50 billion in total. The U.S. plan is subject to a comment period before going into effect, and the Chinese plan is also not yet official.

Investors have taken solace in the fact that there is still hope for negotiation between the U.S. and China, a realization that has helped dull the initial knee-jerk reaction. The industrial (-0.9%) and energy (-1.1%) sectors are still solidly lower this afternoon, but most other groups are trading in the green. The consumer discretionary (+0.6%) and consumer staples (+1.2%) sectors are the top performers, while the top-weighted technology (-0.1%) and financials (+0.1%) sectors are flat.

In the bond market, U.S. Treasuries have retraced their opening gains as the equity market has grown stronger, pushing yields into the green; the benchmark 10-yr yield is up one basis point at 2.79% after hovering around 2.76% earlier. Gold -- another safe-haven asset -- is still higher, but only modestly so, up 0.2% at 1340.20.

Reviewing Wednesday's economic data, which included the ADP National Employment Report for March, the ISM Services Index for March, and Factory Orders for February:

The ADP National Employment Report showed an increase of 241,000 in March (Briefing.com consensus 203,000). The January reading was revised to 246,000 from 235,000.

This report should solidify expectations for another strong nonfarm payrolls number when the government releases the Employment Situation Report on Friday.

The ISM Services Index for March dipped to 58.8 (Briefing.com consensus 59.0) from an unrevised reading of 59.5 in February.

The key takeaway from the report is that the services sector is still growing nicely, albeit at a slightly slower pace than February.

The Factory Orders report for February showed an increase of 1.2% (Briefing.com consensus +1.8%). The January reading was revised to -1.3% from -1.4%.

The key takeaway from the report is that it revealed a rebound in business spending, evidenced by the 1.4% increase in orders for nondefense capital goods excluding aircraft.

Dow: -75.50… | Nasdaq: +4.71… | S&P: -1.42…

NASDAQ Adv/Dec 1591/780. …NYSE Adv/Dec 1399/1465.

12:30PM ET

[BRIEFING.COM] The S&P 500 has made it to its flat line, overcoming a loss of more than 1.0% earlier in the session.

More than half of the S&P sectors are now trading in the green, with consumer discretionary (+0.5%) and consumer staples (+1.0%) leading the charge. The industrials and energy groups are still solidly lower, however, down around 1.0% apiece. Dow components Boeing (BA 322.58, -8.24, -2.5%) and Caterpillar (CAT 143.10, -1.96, -1.4%) are still struggling due to fears of a trade war between the U.S. and China.

In Europe, the major stock indices finished Wednesday relatively flat, with the UK's FTSE adding 0.1% while France's CAC and Germany's DAX lost 0.2% and 0.4%, respectively.

Dow: -50.77… | Nasdaq: +21.42… | S&P: +0.89…

NASDAQ Adv/Dec 1584/819. …NYSE Adv/Dec 1346/1508.

11:55AM ET

[BRIEFING.COM] The market hasn't moved much since the last update; the S&P 500 is still down 0.3%, while the Nasdaq and the Dow hold losses of 0.1% and 0.6%, respectively.

Homebuilders are rallying today, pushing the iShares U.S. Home Construction ETF (ITB 39.46, +0.73) higher by 1.9%, after Miami-based home construction giant Lennar (LEN 60.80, +3.68) reported better-than-expected earnings for its fiscal first quarter this morning; LEN shares have spiked 6.4%.

In the U.S. Treasury market, issues are flat moving into the afternoon session, giving back all of their early gains. The benchmark 10-yr yield, which moves inversely to the price of the 10-yr Treasury note, is unchanged at 2.78% after being down two basis points this morning.

Dow: -156.07… | Nasdaq: -8.91… | S&P: -9.83…

NASDAQ Adv/Dec 1475/986. …NYSE Adv/Dec 1096/1733.

11:30AM ET

[BRIEFING.COM] Equities have continued ticking higher this morning, pushing the S&P 500 within 0.3% of its unchanged mark.

The consumer discretionary sector (+0.2%) has jumped into positive territory for the first time today in recent trading. Most names within the group are higher, including Dow components Home Depot (HD 174.16, +0.40) and Nike (NKE 67.34, +0.64), but a 0.7% decline in shares of Amazon (AMZN 1380.85, -11.20) has kept the sector in check.

Meanwhile, the consumer staples sector (+0.8%) is trading atop today's leaderboard. Almost all of the sector's components are in the green, with drug retailers CVS Health (CVS 64.76, +2.18) and Walgreens Boot Alliance (WBA 65.08, +1.91) showing particular strength, adding around 3.0% apiece.

Dow: -166.42… | Nasdaq: -17.53… | S&P: -10.28…

NASDAQ Adv/Dec 1562/969. …NYSE Adv/Dec 1131/1693.

10:55AM ET

[BRIEFING.COM] Stocks have cut their opening losses in half this morning, but the major averages are still solidly lower. The S&P 500 and the Nasdaq Composite are down 0.6% apiece, while the Dow Jones Industrial Average is lower by 0.9%.

Eight S&P groups are down -- including financials (-0.6%), consumer discretionary (-0.2%), industrials (-1.2%), energy (-1.0%), materials (-0.8%), technology (-1.3%), health care (-0.4%), and utilities (-0.1%) -- while three are trading in the green -- including consumer staples (+0.8%), telecom services (+0.6%), and real estate (+0.5%).

On a separate note, the Department of Energy reported that U.S. crude inventories declined by 4.6 million barrels last week, while the consensus estimate was expecting a build of 1.4 million barrels. WTI crude futures were down around 2.0% ahead of the release, but now trade lower by 1.1% at $62.85 per barrel.

Dow: -222.04… | Nasdaq: -45.78… | S&P: -15.36…

NASDAQ Adv/Dec 1377/1159. …NYSE Adv/Dec 1080/1706.

10:35AM ET

[BRIEFING.COM]

Commodities are beginning the day lower

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently -0.8% at 86.2813

Dollar index is currently -0.2% at 89.66

Looking at energy...

Mar WTI crude oil futures are now -$0.89 at $62.62/barrel

Oil just recovered some losses following post-EIA data rally

In other energy, Mar natural gas is +$0.04 at $2.74/MMBtu

Moving on to metals...

Apr gold is currently +$8.00 at $1345.30/oz, while Mar silver is -$0.07 at $16.32/oz

Mar copper is now -$0.06 (-2%) at $3.00/lb

Dow: -368.96… | Nasdaq: -84.64… | S&P: -28.50…

NASDAQ Adv/Dec 1030/1617. …NYSE Adv/Dec 825/1953.

10:00AM ET

[BRIEFING.COM] Equity indices continue hovering near their opening levels, with the S&P 500 showing a loss of 1.2%.

Just in, the ISM Services Index for March dipped to 58.8 (Briefing.com consensus 59.0) from an unrevised reading of 59.5 in February.

Separately, the Factory Orders report for February showed an increase of 1.2% (Briefing.com consensus +1.8%). The January reading was revised to -1.3% from -1.4%.

Dow: -348.14… | Nasdaq: -70.78… | S&P: -24.98…

NASDAQ Adv/Dec 1064/1587. …NYSE Adv/Dec 690/2036.

09:40AM ET

[BRIEFING.COM] The major averages are down between 1.1% and 1.7%, with the Dow showing relative weakness.

All 11 S&P sectors are trading in the red this morning. Industrials (-1.8%), materials (-1.8%), and energy (-1.8%) are the worst-performing groups, while the consumer staples (-0.3%), utilities (-0.6%), and real estate (-0.3%) spaces have held up relatively well.

As a reminder, both the ISM Services Index for March (Briefing.com consensus 59.0) and Factory Orders for February (Briefing.com consensus +1.8%) will be released at 10:00 AM ET.

Dow: -428.28… | Nasdaq: -88.66… | S&P: -33.13…

NASDAQ Adv/Dec 650/2011. …NYSE Adv/Dec 383/2338.

09:11AM ET

[BRIEFING.COM] S&P futures vs fair value: -37.50. Nasdaq futures vs fair value: -113.00.

The U.S. equity market is on course for a solidly lower open, as the S&P 500 futures are trading 38 points, or 1.4%, below fair value.

This morning's bearish disposition follows an announcement from China, which has proposed additional tariffs on 106 products imported from the U.S., including soybeans, planes, autos, and chemicals. This tariff announcement, which amounts to a total import value of around $50 billion, highlights for investors that China is going to take off the gloves if it has to in this trade fight. Shares of companies with large exposure to China, including Dow components Boeing (BA 315.49, -15.36, -4.6%) and Caterpillar (CAT 140.02, -5.01, -3.5%), are showing notable weakness in pre-market trading.

The ADP National Employment report for March crossed the wires earlier this morning, showing the addition of 241,000 nonfarm payrolls (Briefing.com consensus 203,000). The ADP reading is seen as a prelude to the BLS's nonfarm payroll figure, which will be released Friday, but isn't very reliable, often deviating sharply from the official number. Today's last economic reports -- ISM Services Index for March (Briefing.com consensus 59.0) and February Factory Orders (Briefing.com consensus +1.8%) -- will both be released at 10:00 AM ET.

U.S. Treasuries are higher this morning, pushing the benchmark 10-yr yield down two basis points to 2.76%. Meanwhile, WTI crude futures are down 1.8% at $62.35/bbl, the U.S. Dollar Index is down 0.2% at 89.68, and gold futures are up 1.0% at $1350.70/oz.

08:51AM ET

[BRIEFING.COM] S&P futures vs fair value: -37.00. Nasdaq futures vs fair value: -110.00.

The S&P 500 futures are trading 37 points, or 1.4%, below fair value.

Equity indices in the Asia-Pacific region ended Wednesday on a mixed note. China's Ministry of Commerce announced that a 25% tariff will be imposed on 106 products imported from the U.S. These imports are currently worth about $50 billion, and the announcement was made after the Trump administration threatened to impose tariffs on 1,300 categories of products from China. On the economic front, China's March Caixin Services PMI (52.3; expected 54.5) fell to a four-month low.

In economic data:

China's March Caixin Services PMI 52.3 (expected 54.5; last 54.2)

Australia's February Retail Sales +0.6% month-over-month (expected 0.3%; last 0.2%). February Building Approvals -6.2% month-over-month (expected -4.8%; last 17.2%) and Private House Approvals +1.9% (last -0.9%)

---Equity Markets---

Japan's Nikkei edged up 0.1%. Fast Retailing, Familymart, Takeda Pharmaceuticals, Isuzu Motors, KDDI, J Front Retailing, and Subaru advanced between 1.8% and 3.0%. On the downside, Dainippon Screen Manufacturing, Japan Steel Works, Furukawa Electric, and SUMCO lost between 3.0% and 4.0%.

Hong Kong's Hang Seng fell 2.2% amid broad weakness. Apple suppler AAC Technologies fell 5.9% while consumer names like China Mengniu Dairy and Want Want China lost 4.9% and 4.1%, respectively. Sunny Optical Tech, Geely Automobile, ICBC, and Bank of China surrendered between 1.9% and 4.0%.

China's Shanghai Composite shed 0.2%. Keda Group, Beijing AriTime Intelligent Control, Aisino, Hundsun Technologies, and Sinomach General Machinery Science & Technology fell between 4.2% and 6.2%.

India's Sensex slid 1.1%. Tata Steel lost 3.3% while AXIS Bank, IndusInd Bank, Kotak Mahindra Bank, Yes Bank, and HDFC Bank posted losses between 1.6% and 2.6%.

Major European indices trade lower across the board with Germany's DAX (-1.1%) leading the retreat. In Italy, Movimento 5 Stelle is reportedly opposed to forming a coalition with Silvio Berlusconi's Forza Italia. This means Matteo Salvini's Lega will have to decide between honoring its coalition commitment to Forza Italia and forming a new coalition with M5S.

In economic data:

Eurozone February Unemployment Rate 8.5%, as expected (last 8.6%). March CPI +1.4% year-over-year, as expected (last 1.1%) and core CPI +1.0% year-over-year (expected 1.1%; last 1.0%)

UK's March Construction PMI 47.0 (expected 50.9; last 51.4)

Italy's Q4 Public Deficit 1.6% (last 1.9%). February Unemployment Rate 10.9% (expected 11.0%; last 11.1%)

---Equity Markets---

UK's FTSE is lower by 0.4%. Miners and financials are among the laggards with Anglo American, Rio Tinto, BHP Billiton, Antofagasta, Glencore, Old Mutual, Standard Chartered, Provident Financial, HSBC, and Standard Life showing losses between 1.1% and 3.8%.

France's CAC is down 0.7% amid losses in all but seven components. STMicroelectronics has slid 3.8% while financials like Societe Generale, Credit Agricole, BNP Paribas, and AXA are down between 0.9% and 1.6%.

Germany's DAX has slumped 1.1%, revisiting this year's low. Infineon has given up 3.7% while heavyweights like Lufthansa, Volkswagen, Deutsche Bank, BMW, Siemens, Daimler, Allianz, BASF, and SAP are down between 0.9% and 3.3%.

08:25AM ET

[BRIEFING.COM] S&P futures vs fair value: -42.80. Nasdaq futures vs fair value: -128.00.

The S&P 500 futures are trading 43 points, or 1.6%, below fair value.

The ADP National Employment Report showed an increase of 241,000 in March (Briefing.com consensus 203,000). The January reading was revised to 246,000 from 235,000. The ADP reading is seen as a prelude to the BLS's nonfarm payrolls figure (Briefing.com consensus 175,000), which will be released on Friday.

07:57AM ET

[BRIEFING.COM] S&P futures vs fair value: -40.80. Nasdaq futures vs fair value: -124.80.

Futures are pointing towards a solidly lower open for the U.S. equity market this morning after China announced it will impose a 25% tariff on 106 products imported from the U.S., including soybeans, planes, and cars. The tariffs are worth about $50 billion in total and are a direct response to the Trump administration's duties on Chinese imports.

The S&P 500 futures are currently trading 41 points, or 1.6%, below fair value. Dow futures show relative weakness, down 2.0%, as Boeing (BA 314.99, -15.86) and Caterpillar (CAT 141.00, -4.03), which have significant exposure to China, are showing heavy losses in pre-market trading; the two names are down 4.8% and 2.8%, respectively. The tech-heavy Nasdaq futures are down 1.8%.

Safe-haven assets are in demand this morning, including U.S. Treasuries, gold, and the Japanese yen. The 10-yr yield, which moves inversely to the price of the benchmark 10-yr Treasury note, is down two basis points at 2.76%, while gold futures are up 0.8% at $1347.40/oz and the yen is up 0.4% against the U.S. dollar at 106.22.

Investors will receive several pieces of economic data this morning, including ADP Employment Change for March (Briefing.com consensus 203K) at 8:15 AM ET and both February Factory Orders (Briefing.com consensus +1.8%) and the ISM Services Index for March (Briefing.com consensus 59.0) at 10:00 AM ET. The ADP reading is seen as a prelude to the BLS's nonfarm payrolls figure, which will be released on Friday, but isn't very reliable, often deviating sharply from the official number.

Overseas, indices in the Asia-Pacific region ended Wednesday mixed, while the major bourses in Europe are lower across the board.

In U.S. corporate news:

Lennar (LEN 57.87, +0.78): +1.4% after beating quarterly profit estimates.

CarMax (KMX 56.84, -3.12): -5.2% after missing revenue estimates for the fourth quarter and reporting a 8.0% decline in same-store sales.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region ended Wednesday on a mixed note. Japan's Nikkei +0.1%, Hong Kong's Hang Seng -2.2%, China's Shanghai Composite -0.2%, India's Sensex -1.1%.

In economic data:

China's March Caixin Services PMI 52.3 (expected 54.5; last 54.2)

Australia's February Retail Sales +0.6% month-over-month (expected 0.3%; last 0.2%). February Building Approvals -6.2% month-over-month (expected -4.8%; last 17.2%) and Private House Approvals +1.9% (last -0.9%)

In news:

China's Ministry of Commerce announced that a 25% tariff will be imposed on 106 products imported from the U.S. These imports are currently worth about $50 billion, and the announcement was made after the Trump administration threatened to impose tariffs on 1,300 categories of products from China.

Major European indices trade lower across the board. UK's FTSE -0.6%, France's CAC -1.0%, Germany's DAX -1.5%.

In economic data:

Eurozone February Unemployment Rate 8.5%, as expected (last 8.6%). March CPI +1.4% year-over-year, as expected (last 1.1%) and core CPI +1.0% year-over-year (expected 1.1%; last 1.0%)

UK's March Construction PMI 47.0 (expected 50.9; last 51.4)

Italy's Q4 Public Deficit 1.6% (last 1.9%). February Unemployment Rate 10.9% (expected 11.0%; last 11.1%)

In news:

In Italy, Movimento 5 Stelle is reportedly opposed to forming a coalition with Silvio Berlusconi's Forza Italia. This means Matteo Salvini's Lega will have to decide between honoring its coalition commitment to Forza Italia and forming a new coalition with M5S.

07:31AM ET

[BRIEFING.COM] S&P futures vs fair value: -39.50. Nasdaq futures vs fair value: -113.00.

06:59AM ET

[BRIEFING.COM] S&P futures vs fair value: -45.50. Nasdaq futures vs fair value: -135.00.

06:59AM ET

[BRIEFING.COM] Nikkei...21319.55...+27.30...+0.10%. Hang Seng...29519...-661.40...-2.20%.

06:59AM ET

[BRIEFING.COM] FTSE...6980.45...-50.00...-0.70%. DAX...11816.87...-185.60...-1.60%.

04:30PM ET

[BRIEFING.COM] U.S. equities rebounded on Tuesday, reclaiming a little more than half of their Monday losses in a broad-based rally. The S&P 500 advanced 1.3% to 2614.45, the Dow Jones Industrial Average climbed 1.7% to 24033.36, and the Nasdaq Composite jumped 1.0% to 6941.28.

The major averages bounced around with modest gains for much of the session, but shot to new highs in the late afternoon following a headline that the White House doesn't have any specific plans for action against Amazon (AMZN 1392.05, +20.06). The news wasn't really new -- Press Secretary Sarah Huckabee Sanders made a similar statement last week -- but, nonetheless, it served to temper fears following critical comments from President Trump, who alleges the company is taking advantage of the U.S. Post Office and gets unfair tax treatment.

Amazon jumped following the headline, and the broader market came along with it -- thanks in part to some short-covering activity. AMZN shares, which were down as much as 1.2% on Tuesday, finished higher by 1.5%, while the S&P 500 finished near its session high and about 25 points above its 200-day simple moving average (2590). The benchmark index settled below the key technical level for the first time since June 2016 on Monday.

All 11 S&P sectors finished Tuesday in positive territory, with energy (+2.1%) being the top performer as WTI crude futures rebounded from a two-week low, climbing 0.7% to $63.45 per barrel. The financials (+1.4%), consumer discretionary (+1.2%), industrials (+1.4%), materials (+1.5%), health care (+1.5%), and consumer staples (+1.4%) sectors also finished with solid gains, while the lightly-weighted utilities (+0.4%) and real estate (+0.3%) sectors lagged.

The most influential group -- information technology -- finished higher by 1.0%, but struggled up until the late-afternoon rally, losing as much as 0.7% earlier in the session. The group's turnaround helped boost investor sentiment, which has suffered in recent weeks amid a lack of sector leadership; the technology group has underperformed as of late after pacing last year's rally and a once positive start to 2018. Likewise, the financial sector's upbeat performance was also a notable tailwind for investor sentiment.

Investors did not receive any economic data on Tuesday, but automakers did report sales figures for the month of March. General Motors (GM 36.94, +1.18), Ford Motor (F 11.15, +0.29), and Fiat Chrysler (FCAU 21.79, +1.84) advanced 3.3%, 2.7%, and 9.2%, respectively, after all three reported year-over-year increases in sales; Fiat Chrysler's sales increased 14.0%, while GM's and Ford's sales increased 16.0% and 3.4%, respectively. Electric automaker Tesla (TSLA 267.53, +15.05) also climbed, adding 6.0%, after reporting Model 3 production just below its target and reaffirming its production outlook.

In the bond market, U.S. Treasuries tumbled on Tuesday, pushing yields higher across the curve; the yield on the benchmark 10-yr Treasury note climbed five basis points to 2.78%, rebounding from an eight-week low, while the 2-yr yield also advanced five basis points, closing at 2.29%.

Looking ahead, investors will receive several reports on Wednesday, including the weekly MBA Mortgage Applications Index at 7:00 AM ET, the ADP Employment Change report for March (Briefing.com consensus 203K) at 8:15 AM ET, and both February Factory Orders (Briefing.com consensus +1.8%) and the ISM Services Index for March (Briefing.com consensus 59.0) at 10:00 AM ET.

Nasdaq Composite: +0.6% YTD

S&P 500: -2.2% YTD

Dow Jones Industrial Average: -2.8% YTD

Russell 2000: -1.5% YTD

Dow: +389.17… | Nasdaq: +71.16… | S&P: +32.57…

NASDAQ Adv/Dec 1912/1027. …NYSE Adv/Dec 2209/748.

Special thanks to

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links and data will be useful for you.

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Rebuttal to Emmett Moore via TheStrategyLab.com Review

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 The Strategy Lab: Valforex - The Manipulative Review Scam

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3676 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htm Advance WRB Analysis Tutorial Chapters 4 - 12

@ http://www.thestrategylab.com/WRBAnalysisTutorials.htmDisclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis. The risk of loss can be substantial. Therefore, you must carefully consider if trading is suitable for you within the context of your financial condition. TheStrategyLab.com is an education and research site. The resources on this site are provided for informational purposes only and should not be used to replace professional educational and professional research because we are retail traders only. TheStrategyLab.com does not accept liability for your use of the website and its resources.

We make no guarantees of success and your level of success is dependent upon other factors including your skill as a trader, knowledge, financial condition, market conditions and other factors. Trading is stressful and you should always consult a doctor in all matters relating to physical and mental health of you & your family because trading can impact beyond your financial condition regardless if you're a profitable or losing trader. Also, you can read our full disclaimer statement @ http://www.thestrategylab.com/Disclaimer.htmBest Regards,

M.A. Perry

Online user name

wrbtrader (more info about me)

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850 & http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading (no indicators)

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com