Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=73&t=503.

Quote:

Today's results are 5 wins : 3 losses : 1 breakeven. A lot better than yesterday due to the fact I had 2 well manage profitable trades that I was able to get much more than their profit target. In fact, I usually need about 2 winners per day that go beyond a WRB pt1 level to ensure my trading day will result as a profitable day.

Trading Tip: Stop loss protections are for the worst case scenario in a trade. However, you must learn to understand the price action to minimize losses prior to letting a stop get hit.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

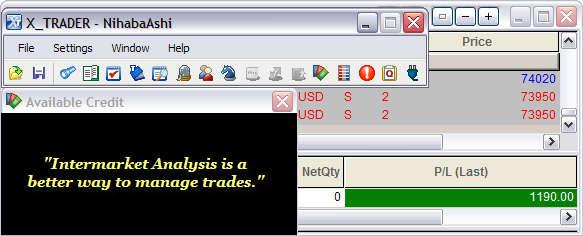

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

+11.90 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

042310_wrbtrader_PnLBlotterProfit.png [ 31.77 KiB | Viewed 1582 times ]

042310_wrbtrader_PnLBlotterProfit.png [ 31.77 KiB | Viewed 1582 times ]

------------------------------

Dow, S&P End At 19-Month Highs By Alexandra Twin, senior writer

April 23, 2010: 10:33 PM ET

NEW YORK (CNNMoney.com) -- Stocks rallied Friday, with the Dow, Nasdaq and S&P 500 all ending at fresh 2010 highs, after a surprisingly strong new-home sales report, a surge in commodities and improved earnings from American Express.

The Dow Jones industrial average (INDU) rose 70 points, or 0.6%, ending at 11,204.28, the highest close since Sept. 19, 2008.

The S&P 500 index (SPX) rose 8 points, or 0.7%, ending at 1217.28, also the highest point since Sept. 19, 2008.

The Nasdaq composite (COMP) gained 11 points, or 0.4%, closing at 2530.15, the highest point since June 5, 2008.

"Today it was about the new-home sales and the earnings, but we've also been seeing some real resilience in the market, with the Dow up for the longest winning streak in six years," said Paul Brigandi, vice president of trading at Direxion Funds.

The Dow has now risen for eight weeks straight, its longest positive streak since January 2004. The Nasdaq has also risen for eight consecutive weeks. The S&P 500 ended lower last week and has risen for seven of the last eight weeks.

"Everyone's anticipating a pullback, but we're just not seeing it, even with the overhang of Greece and other sovereign debt issues and financial regulatory reform," he said.

Stocks seesawed through the morning as investors considered a variety of economic, corporate and geopolitical news. But the tone turned positive by the close, with the Dow and S&P 500 ending at fresh 18-month highs and the Nasdaq closing at a new 22-month high.

A surprisingly weak durable-goods orders report raised worries about the economy that were later tempered by a strong new home sales report. The dollar fluctuated, putting some pressure on corresponding commodity prices and stocks. Investors also sorted through the ramifications of Greece's decision to access emergency funds.

Better-than-expected earnings from American Express and others were also in the mix. A variety of homebuilder stocks jumped.

Greece: Worries about the nation defaulting on its debt eased Friday after Greece's prime minister requested up to $53 billion in aid from the European Union and International Monetary Fund.

Greece's bond yields had hit record highs Friday before the debt-plagued nation asked to access the loans made available to it earlier this month. The European Union (EU) pledged to provide as much as $40 billion at a 5% interest rate, well below market rate. The IMF said it would lend Greece $13 billion.

Worries that Greece wouldn't make its May 19 deadline for refinancing more than $11 billion were exacerbated Thursday after ratings agency Moody's cut its bond rating on the country. An EU report showed that Greece's budget deficit last year was worse than the nation has admitted, adding to the worries.

Economy: Orders for durable goods fell 1.3% in March, the Commerce Department reported Friday. Orders rose 1.1% in February and were expected to rise 0.1% in March, according to a consensus of economists surveyed by Briefing.com.

The weak report raised some worries about the pace of the recovery, but the fears were tempered by a strong housing market report.

In the housing report, new home sales rose to a 411,000-unit annual rate in March from a 324,000-unit annual rate in February, a 27% increase that was the fastest rate of gain in 47 years. Economists had expected sales of 330,000.

Bond investors are chasing the past

Quarterly results: Roughly 83% of S&P 500 company earnings have topped estimates, with growth currently forecast to have risen 50% from a year earlier, according to the latest from Thomson Reuters. Revenue growth is expected to have risen 11% from a year ago.

American Express (AXP, Fortune 500) reported higher quarterly earnings late Thursday that topped estimates. The Dow component also said its customers spent more in the first quarter than a year earlier and that it set aside less money for loan losses. Shares gained 2% Friday.

Fellow credit card distributor Capitol One Financial (COF, Fortune 500) also posted earnings that improved from a year earlier and topped estimates, and also set aside less for loan losses than in previous quarters. However, the company said customer loan demand is still weak. Shares gained 2.5%.

Microsoft (MSFT, Fortune 500) posted a higher quarterly profit that surpassed forecasts late Thursday. The results were due to a continued strong response to it Windows 7 operating system, introduced six months ago, as well as its Bing search engine. Shares fell 2% Friday.

Also after the close Thursday, Amazon.com (AMZN, Fortune 500) reported earnings that jumped 68% from a year ago, surpassing forecasts, on higher sales that also beat expectations. Amazon shares fell 4.5%.

Merck (MRK, Fortune 500) rallied 5% and was one of the Dow's biggest gainers after it forecast charges related to healthcare reform that are lower than its rivals. Merck expects to take around $170 million in charges this year and between $300 million and $350 million in charges next year.

Market breadth was positive. On the New York Stock Exchange, winners beat losers two to one on volume of 880 million shares. On the Nasdaq, advancers topped decliners five to four on volume of 2 billion shares.

The dollar and commodities: The dollar fell versus the euro, giving up morning gains. The greenback advanced versus the yen.

U.S. light crude oil for June delivery rose $1.42 to $85.12 a barrel on the New York Mercantile Exchange.

COMEX gold for June delivery rose $10.80 to settle at $1,153.70 per ounce.

World markets: In overseas trading, European markets rallied, with London's FTSE up 1%, France's CAC 40 up 0.7% and Germany's DAX up 1.5%. Asian markets fell, with Hong Kong's Hang Seng index down 1% and Japan's Nikkei down 0.3%.

Bonds: Treasury prices fell, raising the yield on the 10-year note to 3.82% from 3.77% late Thursday. Treasury prices and yields move in opposite directions.

Yahoo! Finance

Yahoo! Finance 4:30 pm : The Dow closed on its highs for the year, and finished higher for its eighth consecutive week, closing on its 200-week moving average. U.S. equities initially took their cue from Europe as investors responded positively to Greece seeking aid from the IMF and European Union.

News that Greece requested $55 billion from the EU and IMF helped improve the mood of investors following last night's after-hours session, when it had appeared several companies would be weaker this morning. Traders sold the news of better-than expected earnings from market heavyweights Microsoft (MSFT 30.96, -0.43) and Amazon (AMZN 143.63, -6.46), investors gained confidence as the selling stayed contained, and stocks started rallying around midday to close at both session highs and 19-month highs.

Energy shares were the best performers, gaining 2.3%. Schlumberger (SLB 72.68, +4.50) led the sector showing gains of almost 7%. Higher oil prices helped as crude closed near $85.10 in electronic trading.

Meanwhile, telecom shares continued to lag the broader market and closed down 0.2%. A downgrade of Verizon (VZ 29.05, -0.23) put pressure on shares in the telecom space.

Volume on the NYSE closed above its 200-day average for the third straight session.

Economic data released today had little sustainable impact on the direction of the market in early trading. A surprise spike in new home sales for March of 26.9% month-over-month to an annualized rate of 411,000 units led to a short rally in stocks, but they later pulled back.

Durable goods orders for March also had little influence on the market's initial direction. Total orders fell 1.3%, which is a negative surprise since the consensus had called for a 0.2% increase. Excluding transportation, durable goods orders for March spiked 2.8%, which was considerably stronger than the 0.7% increase that had been widely forecast. Orders less transportation for February were revised higher to reflect a 1.7% increase.

Advancing Sectors: Energy (+2.3%), Materials (+1.3%), Health Care (+1.1%), Utilities (+0.8%), Industrials (+0.7%), Consumer Discretionary (+0.5%), Tech (+0.5%), Financials (+0.4%)

Declining Sectors: Telecom (-0.2%), Consumer Staples (-0.1%) DJ30 +69.99 NASDAQ +11.08 NQ100 +0.5% R2K +1.0% SP400 +1.0% SP500 +8.61 NASDAQ Adv/Vol/Dec 1702/2.43 bln/991 NYSE Adv/Vol/Dec 2161/1.21 bln/869

3:30 pm : Commodities had a relatively solid session as the CRB Commodity Index put together a 0.7% gain, which made for its fourth straight advance and left it 1.0% higher for the week.

Natural gas booked some of the best gains this session as its price climbed 3.1% to $4.26 per MMBtu. Oil prices were also strong as crude prices climbed 1.7% to $85.12 per barrel, a closing high for the week.

As for precious metals, gold prices gained 0.9% to settle pit trade at $1153.30 per ounce. Silver prices advanced 1.1% to $18.20 per ounce. DJ30 +53.21 NASDAQ +5.71 SP500 +6.61 NASDAQ Adv/Vol/Dec 1566/2.01 bln/1121 NYSE Adv/Vol/Dec 2041/882 mln/971

3:00 pm : Stocks have pushed to new highs as investors look ahead to next week. The S&P 500 is up 0.5%, while the Dow is up 0.4% and the Nasdaq trails with a gain of 0.3%.

Briefing.com will cover more than 20 earnings announcement before the opening bell on Monday. Investors will be particularly focused on Catapillar's (CAT 68.55, +1.05) announcement as it will give a glimpse into the strength of the economies of both the United States and China. Wall Street's estimates call for earnings of $0.39 per share. Other companies that may be impacted by the release are CNH (CNH 31.56, +0.44) which beat estimates on Wednesday, and Joy Global (JOYG 61.07, -0.47) which doesn't report until early June. DJ30 +45.35 NASDAQ +6.36 SP500 +5.79 NASDAQ Adv/Vol/Dec 1529/1.82 bln/1135 NYSE Adv/Vol/Dec 1981/798 mln/1023

2:30 pm : The S&P 500 sits just below its its best level of the day as stocks continue to grind higher. The S&P 500 and Dow Jones Industrial Average are up 0.3% while the Nasdaq has just crossed back into positive terriotory.

Telecom, which has lagged the broader market over the course of the year, continues to underperform, and is down 0.7%. The broker downgrade of Verizon (VZ 28.92 -0.36) caused selling in other companies within the space. AT&T (T 26.12, -0.15) and Qwest (Q 5.25, -0.12) sold off on the news.

In contrast, energy shares are up 1.7%, the strongest performers of the day, as crude oil looks to close its session above $85.00 per barrel, near session highs. DJ30 +29.55 NASDAQ +0.92 SP500 +3.84 NASDAQ Adv/Vol/Dec 1452/1.67 bln/1209 NYSE Adv/Vol/Dec 1874/728 mln/1100

2:00 pm : The major market indices remain mixed as investors look ahead to next week's Fed announcement. No change in rates are expected, but investors will be looking for any change in the wording of the Fed's statement and hints about when the Fed will begin to raise rates.

Also next week, the government will announce first quarter GDP. The report will give traders their first look at the strength of the economy's recovery as it progresses in 2010. The consensus is looking for the economy to expand 3.5% following last quarter's gain of 5.6%.

DJ30 +28.27 NASDAQ -0.87 SP500 +3.04 NASDAQ Adv/Vol/Dec 1424/1.58 bln/1218 NYSE Adv/Vol/Dec 1824/684 mln/1147

1:30 pm : Stocks have retraced most of this morning's gains following a pop in health care stocks, and the sector is now up 0.8%. Health care stocks found a bid around noon after Merck (MRK 35.36, +1.61) announced its revenues would fall by $170 millon, less than expected. Competitors Pfizer (PFE 16.86, +0.38), and Bristol-Meyers Squibb (BMY 24.73, +0.30) followed suit. The moves comes after the sector had fallen 3% over the past two sessions.

DJ30 +19.35 NASDAQ -3.19 SP500 +1.66 NASDAQ Adv/Vol/Dec 1404/1.45 bln/1218 NYSE Adv/Vol/Dec 1805/630 mln/1151

1:00 pm : Another batch of better-than-expected earnings and a dose of strong data have been met with a collective yawn. Market participants are also unenthused by news that Greece has finally asked for financial aid.

Trade in the broader market has been confined to a sideways chop this session. That has made for rather lackluster action in the face of upside earnings surprises from Microsoft (MSFT 30.88, -0.51), Amazon.com (AMZN 144.08, -6.01), and Honeywell (HON 47.01, -0.43). The three have succumbed to selling as the better-than-expected results bring about a sell-the-news reaction as strong results become the norm.

Consumer finance plays American Express (AXP 48.65, +1.88) and Capital One (COF 46.32, +0.77) have been an exception, though. The two stocks traded with strength ahead of their announcements and have successfully extended their gains.

While AXP has been a source of strength for the Dow, Travelers (TRV 53.23, -0.56) has been one of the weaker blue chips. The company was one of the few to miss the consensus earnings estimate.

Despite a lack of support from the broader market, homebuilders have put together their second straight session of strong gains. The group's 4.6% gain is largely the result of a near 27% surge in new home sales for March. The spike precedes the expiration of a homebuyer tax credit.

In other economic news, durable goods orders for March unexpectedly fell 1.3%, but orders less transportation spiked a stronger-than-expected 2.8%.

A pullback by the greenback hasn't done much for stocks either. The Dollar Index is currently down 0.1% as the euro is whipsawed to a strong gain. The action in the euro follows news that Greece has requested financial aid from both the European Union and International Monetary Fund. Though such a request would seemingly remove an overhang from the stock market, concerns persist over the fiscal health of Portugal, Italy, Ireland, and Spain. DJ30 +24.26 NASDAQ +0.31 SP500 +2.35 NASDAQ Adv/Vol/Dec 1408/1.35 bln/1203 NYSE Adv/Vol/Dec 1787/589 mln/1141

12:30 pm : The broader market action remains choppy as stocks continue to drift near unchanged. However, the NASDAQ is beginning to show some signs of weakness, down 0.2%.

Shares of technology giant Microsoft (MSFT 30.88, -0.48) are lower on the day after releasing earnings following yesterday's close. The weakness has spread throughout much of the software space to companies like Salesforce.com (CRM 87.89, -0.81) and Red Hat (RHT 31.14, -0.15).

Despite weakness among software companies, Apple (AAPL 269.50, +3.03) soared to a new all-time high above $272 earlier this morning, but has since drifted back below $270 per share. DJ30 +13.91 NASDAQ -5.32 SP500 +0.42 NASDAQ Adv/Vol/Dec 1327/1.23 bln/1267 NYSE Adv/Vol/Dec 1727/531 mln/1206

12:00 pm : The broader market continues to move sideways in a relatively quiet trade today with the major indices near the flat line.

Oil equipment, services, and distribution are outperforming the broader indices showing gains of 0.9%. Buoyed by 6% gains from Schlumberger (SLB 72.31, +4.09), as well as strong performance in Halliburton (HAL 34.40, +0.67), and Baker Hughes (BHI 53.44, +1.64) the sector is the largest gainer on the day.

The energy complex has also benefited from a 1% jump in the price of crude oil. Crude oil is now trading near $84.50 per barrel. DJ30 -2.49 NASDAQ -7.18 SP500 -1.41 NASDAQ Adv/Vol/Dec 1209/1.13 bln/1366 NYSE Adv/Vol/Dec 1596/483 mln/1312

11:30 am : The equity indices remain mixed on the session with the Dow Jones Industrial Average up fractionally, and the NASDAQ and S&P 500 slightly lower.

The Volatility Index, the VIX, is down another 0.8% today after running into resistance at its 50-day moving average yesterday. The VIX is trading near its lowest levels of the year, and shows investors are comfortable with equities at these levels.

Gold has pushed above $1150 to its highest level of the session after selling showed up in the dollar. Some of the smaller miners, El Dorado Gold (EGO 14.15, +0.23) and Yamana Gold (AUY 10.33, +0.15), have led the group higher.

DJ30 2.57 NASDAQ -6.31 SP500 -0.66 NASDAQ Adv/Vol/Dec 1195/985 mln/1335 NYSE Adv/Vol/Dec 1602/429 mln/1286

11:00 am : The greenback has given up its morning gain, such that the Dollar Index is now down 0.1% after it was up as much as 0.4% just two hours ago. The dollar's downturn has helped provide a boon for commodity prices, which are now up a collective 0.4%, as measured by the CRB Commodity Index.

Natural resource plays have benefited most from the greenback's pullback. In turn, energy has extended its gain to 0.9% and materials stocks are now up 0.7% -- materials stocks had been mixed in the early going.

Steel stocks are among the strongest plays within the materials sector. The group is up 1.6% at the moment. Its gain follows a 0.8% advance in the prior session and puts them up roughly 0.9% week-to-date. DJ30 +4.84 NASDAQ -6.46 SP500 -0.48 NASDAQ Adv/Vol/Dec 1124/800 mln/1367 NYSE Adv/Vol/Dec 1550/356 mln/1292

10:30 am : The Dollar Index pulled back in recent trade, which gave a boost to commodities.

Both June crude oil and May natural gas traded in negative territory during most of today's session. Crude and natural gas hit morning lows of $82.92 per barrel and natural gas hit lows of $4.07 per MMBtu around 9:00ET. However, June crude oil and May natural gas spiked off those lows, pushing into positive territory on the weakness in the dollar index. Crude is currently $84.07 per barrel, up 0.4% and natural gas is $4.14 per MMBtu, up 0.3%.

Precious metals also spiked sharply in recent trade, moving into positive territory due to weakness in the dollar index. Gold bounced off recent lows of $1135.20 per ounce and silver spiked off its lows of $18.35 per ounce. Gold is currently $1147.40 per ounce, up 0.4%, while silver is at $18.08 per ounce, up 0.4%.

DJ30 +31.14 NASDAQ +2.52 SP500 +2.76 NASDAQ Adv/Vol/Dec 1250/595.6 mln/1192 NYSE Adv/Vol/Dec 1711/267.5 mln/1059

10:00 am : New home sales for March surged 26.9% month-over-month to an annualized rate of 411,000 units, which is the highest rate since July 2009. The consensus estimate had called for a 5.5% monthly increase to an annualized rate of 325,000 units.

The news has sent shares of homebuilders up to a 7.9% gain. That comes on top of the group's prior session surge, which was underpinned by better-than-expected existing home sales for March. Homebuilders are now up 14.5% since the close of trade Wednesday.

The broader market has also responded positively to the headline, such that all three major indices are at session highs in positive territory.

Advancing Sectors: Energy (+0.6%), Materials (+0.6%), Financials (+0.5%), Industrials (+0.5%), Consumer Discretionary (+0.4%), Tech (+0.4%), Health Care (+0.1%)

Declining Sectors: Telecom (-0.5%), Consumer Staples (-0.5%), Utilities (-0.3%) DJ30 +33.48 NASDAQ +3.07 SP500 +1.99 NASDAQ Adv/Vol/Dec 1155/410 mln/1174 NYSE Adv/Vol/Dec 1581/186 mln/1120

09:45 am : The broader market opened in mixed fashion, but it has since slipped amid a sudden flurry of selling. The slide has been broad based, but defensive-oriented plays are under the most pressure at the moment. As such, consumer staples stocks and utilities are down 0.6%, telecom stocks are down 0.5%, while health care stocks have shed a collective 0.4%.

However, better-than-expected earnings from Schlumberger (SLB 71.84, +3.66) have attracted buyers into oil and gas equipment plays (+3.2%), which have helped keep the energy sector in positive territory with a 0.2% gain even though oil prices are down 0.8% to $83 per barrel in the early going. DJ30 -19.04 NASDAQ -4.33 SP500 -2.36 NASDAQ Adv/Vol/Dec 812/240 mln/1416 NYSE Adv/Vol/Dec 1002/120 mln/1627

09:15 am : S&P futures vs fair value: flat. Nasdaq futures vs fair value: +0.30. Stock futures have eased off of their morning highs, but they continue to point to a higher start for the session. Such a move would help the S&P 500 add to its current 1.4% week-to-date gain after it settled last week a tepid 0.2% lower. Last week's loss was the first weekly decline for the stock market since February. The generally positive tone this morning stems from news that Greece has requested financial aid from both the European Union and International Monetary Fund. While the request has addressed an overhang on the stock market, concerns persist over the fiscal health of Portugal, Italy, Ireland, and Spain. Such concern has had a hand in the undoing of the euro's earlier strength. As a consequence the greenback has gained ground so that the Dollar Index now sports a 0.4% gain. In corporate news, upside surprises continue to portray an improved operating picture for companies, but excitement over the better-than-expected earnings has dwindled in recent sessions as strong results become the norm. Economic data this morning showed a stronger-than-expected spike in March durable goods orders less transportation, but the headline orders number slipped unexpectedly. New home sales numbers are due at 10:00 AM ET.

09:05 am : S&P futures vs fair value: -0.60. Nasdaq futures vs fair value: -0.30. Europe's major bourses are up on news that Greece has requested financial aid from the EU and IMF. The request is said to be for some $55 billion and could remove an overhang from the market. While the announcement has helped narrow Greece's credit default spreads and yields, those of Portugal, Spain, Ireland, and Italy have seen limited movement. Greece's ASE 20 Index has pared its gain, though; it was up 3.0%, but is now up just 0.2%. Meanwhile, Germany's DAX is up 1.3% with only four of its 30 members in the red. RWE, one of the country's biggest electricity generators, is the worst performer with its 5.0% drop this session. France's CAC is up 0.4% as it sports a broad-based gain of its own. Saint Gobain is a primary leader, while Danone is a laggard. Roughly 90% of the names in Britain's FTSE are in higher ground. That has helped underpin a 0.7% gain for the British index. HSBC (HBC) currently leads the climb, but Prudential PLC (PUK) is under pressure. Uninspired by Wall Street's rally in the prior session, Asia's major markets moved lower over night. In turn, Japan's Nikkei fell 0.3%. Kyocera (KYO) and Fast Retailing led the list of falling issues. Hong Kong's Hang Seng shed 1.0% as financial issues fell under a stiff bout of selling pressure. HSBC, China Construction Bank, and Industrial & Commercial Bank were the primary sources of weakness. Meanwhile, energy plays PetroChina (PTR) and China Petroleum & Chemical (SNP) weakened the Shanghai Composite, which settled with a 0.5% loss.

08:35 am : S&P futures vs fair value: +1.30. Nasdaq futures vs fair value: +4.80. Durable goods orders for March fell 1.3%, which is a negative surprise since the consensus had called for a 0.2% increase, while orders for the prior month were revised upward to reflect a 1.1% increase. However, when excluding transportation, durable goods orders for March spiked 2.8%, which was considerably stronger than the 0.7% increase that had been widely forecast. Orders less transportation for February were revised higher to reflect a 1.7% increase.

Separately, the dollar has gained ground against competing currencies in recent action, such that the Dollar Index is now up 0.3% to its highest level since overnight trade.

08:05 am : S&P futures vs fair value: +1.10. Nasdaq futures vs fair value: -0.50. Earnings continue to come in above consensus estimates with Microsoft (MSFT), Amazon.com (AMZN), American Express (AXP), Honeywell (HON), and Johnson Controls (JCI) posting some of the more noteworthy upside surprises since the prior session's close. Still, their announcements have been met with a mixed reaction. A more positive impact was made on premarket trade by news that after weeks of speculation and concern Greece has made a request for financial aid from the European Union and International Monetary Fund. The news has also helped prop up the euro, which has kept the dollar in check, and aided Europe's primary bourses in a rally from their losses in the prior session. Asia's major market averages moved lower overnight, though. Monthly durable goods orders are due at the bottom of the hour. New home sales numbers follow at 10:00 AM ET.

06:32 am : S&P futures vs fair value: +0.30. Nasdaq futures vs fair value: flat.

06:32 am : Nikkei...10914.4...-34.60...-0.30%. Hang Seng...21244.5...-210.00...-1.00%.

06:32 am : FTSE...5702...+37.00...+0.60%. DAX...6235.3...+66.80...+1.00%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage