Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=73&t=502.

Quote:

Today's results are 11 wins : 8 losses : 2 breakevens. I struggle today in my trading. Usually I get about 5 trading days like this per month and it is something that's normal for me as a trader that trades for a living. No excuses...just a tough trading day.

Trading Tip: Don't trade your bias. Instead, use it to manage your position size.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

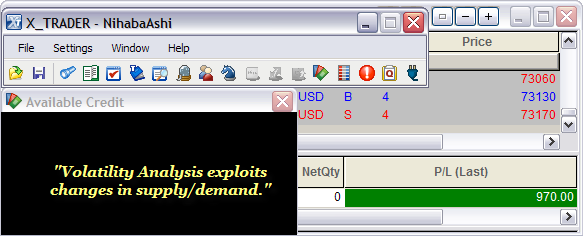

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

+9.70 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

042210_wrbtrader_PnLBlotterProfit.png [ 32.94 KiB | Viewed 1543 times ]

042210_wrbtrader_PnLBlotterProfit.png [ 32.94 KiB | Viewed 1543 times ]

------------------------------

Stocks Make A ComebackBy Alexandra Twin, senior writer

April 22, 2010: 6:44 PM ET

NEW YORK (CNNMoney.com) -- Stocks ended higher Thursday, erasing a steep morning selloff sparked by Greek debt default worries, a spike in the dollar versus the euro and a plunge in commodity prices.

Also in focus: President Obama's speech on financial reform, a better-than-expected housing market report, a mixed reading on weekly jobless claims, a rise in wholesale inflation and the latest round of corporate profit results.

The Dow Jones industrial average (INDU) gained 9 points, or 0.1%, having been down as much as 108 points in the morning. The S&P 500 index (SPX) rose 3 points, or 0.3%. The Nasdaq composite (COMP) rose 14 points, or 0.6%.

Fears that Greece's fiscal problems are even worse than expected sent global markets lower Thursday, lifting the dollar against the euro and pummeling the commodity sector.

But U.S. stocks managed to fight off the selling pressure as the session wore on, with commodity and financial shares erasing losses.

Rather than driven by a specific event, the recovery was a function of all the cross currents in the market, said John Wilson, chief technical strategist at Morgan Keegan.

"We started with worries about Greece, and you would have thought Obama's speech might have riled up markets, but stocks seem to be resistant to a big decline right now," he said.

"Earnings have been better than expected, but the response hasn't been much," he said. "We seem to be stalling here."

He said that he doesn't expect a big selloff in the coming weeks, but that stocks look to be moving into a more extended consolidation phase.

Stocks have risen over the last few months, with the Dow and Nasdaq rising in 8 of the last 9 weeks and the S&P 500 climbing in 7 of the last 9 weeks.

After the close, Microsoft (MSFT, Fortune 500) posted a higher quarterly profit that surpassed forecasts, due to a continued strong response to it Windows 7 operating system, introduced six months ago, as well as its Bing search engine.

Also after the close, Amazon.com (AMZN, Fortune 500) reported earnings that jumped 68% from a year ago, surpassing forecasts, on higher sales that also beat expectations.

Bond investors are chasing the past

Greece: Worries that the nation might default on its debt have dragged on stocks for the last few months, countering improved earnings and signs of stability in the global economy. Investors fear that a Greek default could trigger a bigger debt crisis in other strapped euro zone nations, destabilizing the euro and threatening the strength of the global economic recovery.

Fears were tempered last week when the European Union (EU) and the International Monetary Fund agreed to make billions in loans available to Greece at below market rates.

However, concerns were reignited Thursday after an EU report suggested that Greece's 2009 deficit was bigger than the government reported. The credit rating agency Moody's downgraded Greece's debt to a lower investment grade, and initiated a further review.

The dollar and commodities: The dollar gained versus the euro on Greece worries. The greenback also rose versus the yen after falling in the morning.

Commodity prices slumped, but were off the worst levels of the day. COMEX gold for June delivery fell $5.90 to settle at $1,142.90 per ounce.

U.S. light crude oil for June delivery rose 2 cents to settle at $83.70 a barrel on the New York Mercantile Exchange.

Company news: CenturyTel (CTL) said it would buy fellow local phone company Qwest Communications (Q, Fortune 500) in a stock swap worth $10.6 billion.

US Airways said it has ended merger talks with United Airlines, owned by UAL Corp. (UAUA, Fortune 500), amid talk that United was considering pursuing a merger with Continental (CAL, Fortune 500).

Starbucks (SBUX, Fortune 500) reported higher quarterly profit that beat estimates and boosted its 2010 outlook late Wednesday. Shares rallied 7.3% Thursday.

Market breadth was positive. On the New York Stock Exchange, winners topped losers by two to one on volume of 1.25 billion shares. On the Nasdaq, advancers beat decliners eight to five on volume of 2.68 billion shares.

Wall Street reform: President Obama made a push for financial reform Thursday, urging industry leaders to "join us, instead of

us in this effort."

Speaking at Cooper Union in New York, near Wall Street, Obama addressed an audience of students, union leaders and some of the financial industry's most prominent executives, including Goldman Sachs CEO Lloyd Blankfein.

Last week Goldman Sachs was accused by the Securities and Exchange Commission of defrauding investors in a subprime mortgage deal during the crisis.

Obama's speech occurred as Congress is debating a financial reform package that Democrats say would enable the U.S. to avoid another financial crisis. However, debate has been contentious amid differences of opinion over how to avoid further taxpayer-funded bailouts and ultimately prevent another crisis.

Economy: The National Association of Realtors said existing home sales rose to a 5.35 million unit annual rate in March from a 5.01 million unit rate in February. Economists surveyed by Briefing.com thought sales would rise to 5.29 million units.

The Producer Price Index (PPI), a measure of wholesale inflation, rose 0.7% in March after falling 0.6% in February, due to a big spike in food and fuel costs. Economists thought it would rise 0.5%. Prices excluding food and energy rose 0.1%, in line with forecasts and matching February's rise.

The number of Americans filing new claims for unemployment fell to 456,000 last week from a revised 480,000 in the previous week. Economists thought claims would fall to 450,000.

Continuing claims, a measure of Americans who have been receiving benefits for a week or more, fell to 4,646,000 from 4,686,000 in the previous week. Economists forecast 4,600,000 continuing claims.

World markets: In overseas trading, European markets fell, with London's FTSE down 1%, France's CAC 40 down 1.3% and Germany's DAX down 1%. Asian markets were mixed, with Hong Kong's Hang Seng index down 0.3% and Japan's Nikkei down 1.3%.

Bonds: Treasury prices fell, raising the yield on the 10-year note to 3.77% from 3.74% late Wednesday. Treasury prices and yields move in opposite directions.

Yahoo! Finance

Yahoo! Finance 4:35 pm : Blue chips managed modest gains amid a bevy of better-than-expected earnings, but the results acted as a positive catalyst for the broader market, which settled with a strong gain.

The S&P 500 extended its rebound from the prior session so that it is now less than 1% below the 52-week high that it tumbled from late last week. Its strength in the latest session was broad based with all 10 major sectors booking gains.

Broader market strength coupled with a 0.9% increase in crude oil prices to $83.91 per barrel to take energy stocks to a 1.9% gain. That was the best of the major indices.

Financials were next in line. The sector settled 1.3% higher with regional banks up 3.5% following better-than-expected bottom line results from Marshal & Isley (MI 9.31, +0.90), Regions Financial (RF 8.80, +0.47), and Zions Bank (ZION 27.42, +1.99).

Goldman Sachs (GS 159.98, -3.34) reported an upside earnings surprise of its own on the heels of fraud charges by the SEC. As for the latter matter, Britain's financial regulator started a formal enforcement investigation into the firm.

IBM (IBM 129.69, -2.54) and Johnson & Johnson (JNJ 65.99, -0.04) also bested Wall Street's expectations for the latest quarter, but a lowered forecast from Johnson & Johnson and dissatisfaction with IBM's margins dampened enthusiasm over the reports.

Market participants also showed little interest in upbeat earnings from Coca-Cola (KO 54.47, -0.85) and a dividend hike from Procter & Gamble (PG 63.19, -0.03). Their subsequent weakness hampered the consumer staples sector, which closed just 0.1% for the better.

Still, buying in the broader market was impressive as stocks climbed for the eighth time in nine sessions and the Volatility Index dropped by 9.3%. The VIX is now just 3% above the multiyear low that it hit last week.

Advancing Sectors: Energy (+1.9%), Financials (+1.3%), Utilities (+1.1%), Consumer Discretionary (+1.1%), Industrials (+0.7%), Telecom (+0.7%), Tech (+0.4%), Health Care (+0.3%), Materials (+0.2%), Consumer Staples (+0.1%)

Declining Sectors: (None) DJ30 +25.01 NASDAQ +20.20 NQ100 +0.5% R2K +1.4% SP400 +1.3% SP500 +9.65 NASDAQ Adv/Vol/Dec 2045/2.08 bln/651 NYSE Adv/Vol/Dec 2499/1.13 bln/556

3:30 pm : Commodities advanced nearly 1% this session.

The move to the upside was led by grains. July wheat futures rose 4%. July Corn futures rose over 2%.

Meanwhile, the energy complex traded about 1% higher this session. June crude oil closed 0.9% higher at $83.91 per barrel. June natural gas futures closed 0.8% higher at $3.97 per MMBtu. June gasoline and heating oil futures closed about 1% higher.

Gold and silver futures ended higher this session despite the mild strength in the dollar index. June gold closed 0.3% higher at $1139.20 per ounce; May silver closed 0.5% higher at $17.82 per ounce. DJ30 +30.38 NASDAQ +17.98 SP500 +9.19 NASDAQ Adv/Vol/Dec 1874/1.72 bln/778 NYSE Adv/Vol/Dec 2387/837 mln/629

3:00 pm : Stocks head into the final hour of this session with solid, broad-based gains. Both the Nasdaq and the S&P 500 have even attempted to make a move back toward their session highs.

As for the Dow, it is also up, but less impressively than its counterparts. It has lagged for most of the session despite better-than-expected earnings from a bevy of blue chips. DJ30 +39.30 NASDAQ +19.91 SP500 +10.04 NASDAQ Adv/Vol/Dec 1898/1.56 bln/773 NYSE Adv/Vol/Dec 2414/767 mln/613

2:30 pm : Stocks continue to drift sideways in a narrow trading range. Though that has made for rather lackluster action, gains remain healthy as stocks head toward their second straight gain since they slumped this past Friday.

Amid the steady gains, Treasuries have remained flat. In turn, the yield on the benchmark 10-year Note stands at 3.80%.

The greenback has also had a relatively quiet session, though it has gradually made its way to a 0.2% gain against competing currencies. DJ30 +28.72 NASDAQ +17.59 SP500 +8.81 NASDAQ Adv/Vol/Dec 1889/1.44 bln/764 NYSE Adv/Vol/Dec 2400/712 mln/610

2:00 pm : Large-cap tech outfits Apple (AAPL 245.62, -1.45) and Yahoo! (YHOO 18.49, +0.10) are on deck to report earnings after the closing bell, but in contrast to recent sessions the pair hasn't found the same type of support that participants had shown for other stocks ahead of their announcements. Instead, AAPL and YHOO are caught up in some rather lackluster action, which has actually weighed a bit on the Nasdaq 100 (+0.5%).

The consensus forecast for Apple calls for earnings of $2.45 per share, which is up considerably from the $1.33 per share that the company earned during the same period one year ago. Apple's quarterly earnings per share one year ago exceeded the consensus forecast by $0.24.

As for Yahoo!, it is expected to post a profit of $0.09 per share for its latest quarter. That would actually be down from the $0.15 per share that was brought in during the same period one year ago, when it beat the consensus estimate by $0.07 per share. DJ30 +35.06 NASDAQ +18.65 SP500 +9.24 NASDAQ Adv/Vol/Dec 1862/1.33 bln/771 NYSE Adv/Vol/Dec 2411/655 mln/602

1:30 pm : Volatility has dropped even more in recent trade, such that the Volatility Index is now down 7.2% this session.

Meanwhile, stocks recently eased back a bit and entered into a sideways drift. However, gains remain broad with all 10 major sectors still in positive territory.

Gains also remain healthy among commodities. As such, the CRB Commodity Index is up 1.0%, DJ30 +38.39 NASDAQ +18.10 SP500 +9.42 NASDAQ Adv/Vol/Dec 1873/1.21 bln/755 NYSE Adv/Vol/Dec 2427/613 mln/579

1:00 pm : Better-than-expected earnings continue to keep buyers in the market, such that stocks currently trade with broad-based gains and have almost recovered completely from the selloff that hit late last week.

Goldman Sachs (GS 161.36, -1.96) triggered a selloff last week when it was learned that the firm was charged with fraud by the SEC, but the company came back into focus this morning. Though the company bested earnings expectations with ease, concern about fallout from fraud charges was stoked by news that Britain's financial regulator started a formal enforcement investigation into the firm.

There were a bevy of other blue chips out with better-than-expected results, too, including IBM (IBM 129.57, -2.66) and Johnson & Johnson (JNJ 65.80, -0.23) were among them, but a lowered forecast from Johnson & Johnson and dissatisfaction with IBM's margins and have acted as an overhang on the pair and caused the health care sector (+0.2%) and tech sector (+0.5%) to lag the broader market.

Among other widely-held names, Coca-Cola (KO 54.48, -0.84) topped the consensus earnings estimate and Procter & Gamble (PG 63.26, +0.04) hiked its dividend.

While blue chips have found mixed interest among market participants, their results continue to support a picture of an improved earnings environment. That has helped to inspire buyers in the broader market and drive higher some 80% of the components in the S&P 500.

Though this session's broad-based move has brought the stock market back toward its 52-week high and may be suggestive of a resilience among stocks, many market pundits caution that resistance stands at existing highs and at technical levels closer to 1225. DJ30 +38.09 NASDAQ +17.98 SP500 +9.51 NASDAQ Adv/Vol/Dec 1881/1.14 bln/742 NYSE Adv/Vol/Dec 2418/572 mln/563

12:30 pm : Financials have come into sharper focus as they extend their advance to sport a 1.1% gain. The sector is currently led by regional lender Marshal & Isley (MI 9.13, +0.72), which posted this morning earnings results that exceeded Wall Street's expectations. Regions Financial (RF 8.46, +0.13) also bested expectations, as did Zions Bank (ZION 26.29, +0.86). The upside surprises have helped the group assemble a collective gain of 1.8%.

The financial sector has also gained amid strength in government-owned financial entities Freddie Mac (FRE 1.50, +0.07), and AIG (AIG 41.06, +1.97), which are both up in excess of 4%. Fannie Mae (FNM 1.24, +0.03) had been up with a similar gain, but it has since pulled back. DJ30 +43.68 NASDAQ +17.42 SP500 +9.80 NASDAQ Adv/Vol/Dec 1848/1.03 bln/755 NYSE Adv/Vol/Dec 2398/524 mln/559

12:00 pm : The S&P 500 recently set a fractionally improved session high. The move has put the stock market less than 1% below the 52-week high that it set last week.

Consumer staples stocks (unch.) and health care stocks (+0.2%), traditionally defensive oriented, are acting as laggards this session. Within the two sectors, consumer staples giant Procter & Gamble (PG 63.16, -0.06) has failed to inspire even though it announced a 9.5% increase to its quarterly dividend ahead of its end-of-month earnings release. Meanwhile, Johnson & Johnson (JNJ 65.88, -0.15) fell out of favor when its lowered earnings forecast overshadowed its better-than-expected bottom line results. DJ30 +33.78 NASDAQ +14.37 SP500 +8.36 NASDAQ Adv/Vol/Dec 1760/906 mln/806 NYSE Adv/Vol/Dec 2348/469 mln/594

11:30 am : The broader market has extended its midmorning rebound, but the move has stalled a bit near this morning's highs. Energy remains a primary source of strength; the sector is now up 1.8%.

As for other natural resource plays, materials stocks are up 0.6%, in-line with the broader market. Steel plays are mixed, though, following comments from Steel Dynamics (STLD 17.29, -0.23) that current consensus estimates are too high. Meanwhile, AK Steel (AKS 19.76, -1.07) is down sharply for the fourth straight session, despite in-line quarterly earnings. DJ30 +26.45 NASDAQ +12.05 SP500 +7.24 NASDAQ Adv/Vol/Dec 1690/785 mln/834 NYSE Adv/Vol/Dec 2265/414 mln/640

11:00 am : The Dow recently dipped into negative territory and the Nasdaq came in contact with the unchanged market, but stocks have since made a modest rebound to trade with varied gains.

Energy stocks continue to outperform. The sector is up 1.6% as oil and gas drillers (+2.9%) and oil and gas equipment plays (+3.4%) attract the attention of buyers. Their strength comes as oil extends its rebound from three straight losses; oil prices are now up 2.2% to $83.20 per barrel.

Treasuries are a bit mixed at the moment. Accordingly, the benchmark 10-year Note is down just a couple of ticks, but the 30-year Bond is up five ticks. DJ30 +15.26 NASDAQ +7.40 SP500 +5.90 NASDAQ Adv/Vol/Dec 1605/628 mln/881 NYSE Adv/Vol/Dec 2150/354 mln/686

10:30 am : Crude and precious metals hit new session highs in recent trade, with little help from the dollar index, which is sitting just above the unchanged line.

May crude oil has been in positive territory all session. After pulling back a little after the open, crude rallied to fresh session highs of $83.04 per barrel. Currently, it's trading at $82.85 per barrel, up 1.8%.

May natural gas fell in the red for the first time in today's session just before 8:00ET. The energy component has chopped around since then in and out of negative territory. It hit session lows of $3.91 per MMBtu an hour ago and is currently down 0.6%, at $3.92 per MMBtu.

June gold began gaining momentum in the middle of the overnight session. Gold set morning highs at $1146.80 per ounce around 30 minutes ago and is currently just under that level at $1142.5 per ounce, up 0.6%. May silver has been in positive territory all session. Silver hit its own new session high of $18.04 per ounce around the same time gold did. Currently, silver is up 1.3% at $17.97 per ounce. DJ30 -1.06 NASDAQ +4.31 SP500 +4.45 NASDAQ Adv/Vol/Dec 1518/456.4 mln/897 NYSE Adv/Vol/Dec 2011/277.2 mln/793

10:00 am : Stocks recently steadied their slide from the open, but tech has lagged a bit during the early going. The sector is presently up just 0.1% as shares of IBM (IBM 128.56, -3.67) drag along. The stock had actually traded with strength ahead of its quarterly earnings report, which was released after the prior session's close, but it has since succumbed to a bout of selling pressure that has stemmed partly from disappointment over the company's margins.

Volatility has taken an early tumble. That has the Volatility Index (VIX) down 3.5%. The VIX is now up roughly 10% from its multiyear low, which was reached last week.

Early movers: Trading up -- ARRY +34.1%, CPY +17.9%, UNIS +13.6%, ACUR +12.7%, INTT +10.6%, ASTE +9.3%, SMTX +8.9%, CPBY +8.9%; Trading down -- BDSI -11.4%, ENCO -10.1%, ATAX -9.3%, RBPAA -9.1%, BIOC -8.9%, MTG -8.4%, FALC -8%, PRAN -7.5%, NIV -7.2%

Advancing Sectors: Energy (+1.3%), Industrials (+0.9%), Consumer Discretionary (+0.9%), Financials (+0.8%), Utilities (+0.6%), Materials (+0.4%), Telecom (+0.2%), Consumer Staples (+0.2%), Health Care (+0.2%), Tech (+0.1%)

Declining Sectors: (None) DJ30 +23.20 NASDAQ +10.22 SP500 +6.80 NASDAQ Adv/Vol/Dec 1628/260 mln/677 NYSE Adv/Vol/Dec 2160/185 mln/555

09:45 am : Stocks have given up a small portion of their opening gains, but the early tone to trade remains broadly positive as all 10 major sectors in the S&P 500 continue to sport gains.

The best gains this morning come from the energy sector and industrials sector. Both are up 1.0%. Energy's gain has been underpinned by a rebound in oil prices, which were last quoted at $82.30 per barrel, up 1.1%. As for industrials, they are currently led by Illinois Tool Works (ITW 50.50, +1.69), which posted an upside earnings surprise for its latest quarter. DJ30 +21.01 NASDAQ +11.1 SP500 +6.38 NASDAQ Adv/Vol/Dec 1613/165 mln/632 NYSE Adv/Vol/Dec 2121/135 mln/532

09:15 am : S&P futures vs fair value: +6.20. Nasdaq futures vs fair value: +7.80. Earnings have dominated newswires. Results have been generally strong since, on average, only 1 in 4 of the companies that Briefing.com has covered since the prior session's close came short of the consensus estimate. Better-than-expected results were led by a battery of blue chips, including IBM (IBM), Coca-Cola (KO), Johnson & Johnson (JNJ), and Goldman Sachs (GS). Meanwhile, Procter & Gamble (PG) declared a 9.5% increase to its quarterly dividend, though the company doesn't report until the end of the month. In addition to the broad range of upbeat announcements, sentiment has been helped by strong gains among Europe's major bourses, which have rallied amid news of a jump in investor confidence in Germany and a healthy appetite for short-term Greek debt. As for other catalysts, the dollar is quiet and there's no data on deck.

09:00 am : S&P futures vs fair value: +5.70. Nasdaq futures vs fair value: +6.50. Stock futures are off of their premarket highs, but they continue to point to a strong start for the session.

Commodities have also attracted the interest of buyers. That has helped the CRB Commodity Index rebound to a 0.5% gain after broad losses in the prior session. At the moment, oil prices are up a strong 1.2% to $82.40 per barrel in early pit trade. Meanwhile, gold was last quoted with a 0.6% gain at $1141.90 per ounce and silver was last seen 1.0% higher at $17.91 per ounce.

Those gains come even though the dollar recently made a slight advance against competing currencies so that the Dollar Index is now up 0.1%.

08:35 am : S&P futures vs fair value: +5.20. Nasdaq futures vs fair value: +6.30. U.S. stock futures continue to trade with moderate strength. Meanwhile, Europe's bourses are up with strong gains amid news that Greece successfully sold nearly 2 billion euros worth of three-month bills in an auction that garnered strong demand and an interest rate that was below some of the more pessimistic expectations. News of a stronger-than-expected German investor confidence reading for April has also helped sentiment. Germany's DAX is up 1.3% at the moment. Of its 30 members, only Henkel AG I is in the red, while Daimler (DAI) is up nearly 8% in its best single-session percentage advance in months following strong earnings for its latest quarter. In France, the CAC is up 1.2%. Its gains have also been broad based. Dexia SA and Lagardere are the only two names in the 40-member index that have failed to find higher ground; they are down fractionally. With help from an upgrade by analysts at Citigroup, Total (TOT) currently sports one of the most impressive gains. In Britain, the FTSE is up 0.9%. Natural resource plays BP PLC (BP) and Rio Tinto (RTP) are leaders, but SABMiller is also strong after reports suggested that the company said its financial performance for the year remains in-line with expectations. As for data, the UK inflation rate for March climbed 3.4%, which was sharper than expected.

In Asia, Japan's Nikkei slipped 0.1% as strength in DAI Nippon Print and Fast Retailing was undermined by Softbank, which was a primary source of weakness. Hong Kong's Hang Seng finished 1.0% higher as banking issues of HSBC (HBC), China Construction Bank, and Industrial & Commercial Bank showed leadership. Li & Fung was a bit of a drag, however. Meanwhile, mainland China's Shanghai Composite finished flat.

08:00 am : S&P futures vs fair value: +6.10. Nasdaq futures vs fair value: +7.80. Participants have picked up where the prior session left off to give stock futures an upward push. The effort has been helped by a raft of strong quarterly reports, which have included better-than-expected earnings from IBM (IBM), Coca-Cola (KO), and Johnson & Johnson (JNJ). Though those particular names are mixed in premarket trade, their results support a positive earnings picture for the quarter.

Goldman Sachs (GS) also surpassed expectations for the latest quarter, but a Reuters report that indicated Britain's financial regulator started a formal enforcement investigation into the firm has acted as a reminder that there is some near-term uncertainty in the stock.

There is no official economic data scheduled for release today, but Fed Chairman Bernanke and Treasury Secretary Geithner will appear before the House Financial Services Committee to testify about the bankruptcy of Lehman Brothers at 11:00 AM ET. Prepared comments from the speech have already been released.

06:20 am : S&P futures vs fair value: +6.10. Nasdaq futures vs fair value: +7.50.

06:20 am : Nikkei...10900.68...-8.10...-0.10%. Hang Seng...21623.28...+218.20...+1.00%.

06:20 am : FTSE...5756.31...+28.40...+0.50%. DAX...6200.10...+37.80...+0.60%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage