Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=73&t=498.

Quote:

Today's results are 16 wins : 4 losses. A lot of beginner or inexperience traders believes that the market is not impacted by news. Simply, they believe the market price action is strictly technical. That's just one of the many reasons why most traders are not profitable...they believe these myths and allow such to dictate their trading. Today we had volcanic ash grounding most European flights, consumer sentiment report and GS (Goldman Sachs) fraud allegations...that's a volatility eruption especially after a few low volatility tight trading range trading days. Anyways, I was more than twice my average number of trades today but the explosion in the volatility is too good to ignore. Thus, I was aggressive and wanted to be active to exploit very good price action. In fact, I only missed one trade signal that would have added another 10 point profit to my total for the day.

Trading Tip: To determine how sensitive your trade method is to changing volatility...overlap a VXX chart with a chart of your daily trade results. If your method is sensitive to volatility....contact me and I'll give you a few trading tips to exploit what you've observed after overlapping the charts.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

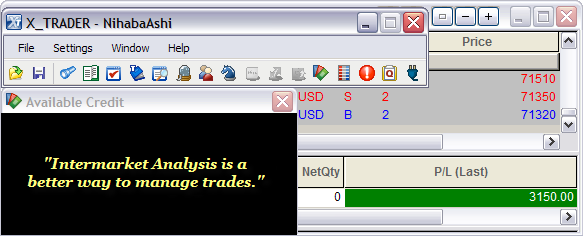

+31.50 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

041610_wrbtrader_PnLBlotterProfit.png [ 31.99 KiB | Viewed 1763 times ]

041610_wrbtrader_PnLBlotterProfit.png [ 31.99 KiB | Viewed 1763 times ]

------------------------------

Dow Tumbles 126, But Clings To 11,000 By Alexandra Twin, senior writer

April 16, 2010: 6:05 PM ET

NEW YORK (CNNMoney.com) -- Stocks tumbled Friday, with the Dow industrials skidding to end just above 11,000, as financial shares retreated after U.S. regulators charged Goldman Sachs with defrauding investors.

The news overshadowed strong quarterly results from Google, General Electric and Bank of America.

The Dow Jones industrial average (INDU) lost 126 points, or 1.1%, to finish at 11,018. The indicator fell as much as 170 points earlier, dropping below 11,000, a key psychological level. The Dow ended at an 18-month high on Thursday.

The S&P 500 index (SPX) lost 19 points, or 1.6%, and the Nasdaq composite (COMP) lost 34 points, or 1.4%. The S&P 500 ended at an 18-month high Thursday, while the Nasdaq composite ended at a 22-month high.

Despite Friday's losses, the Dow and Nasdaq ended up for the week. The S&P was slightly lower.

News that the Securities and Exchange Commission (SEC) has charged Goldman Sachs (GS, Fortune 500) with fraud involving mortgage-backed securities sent the firm's shares down 12.8% and also dragged on the broader financial sector. The KBW Bank (BKX) sector index lost 3.5%. Citigroup (C, Fortune 500), Morgan Stanley (MS, Fortune 500) and JPMorgan Chase (JPM, Fortune 500) all declined.

"The news is introducing an unknown into the market, and so you're seeing a strong reaction to it," said Steven Goldman, market strategist at Weeden & Co.

He said investors are trying to understand if Goldman is just the tip of the iceberg and if more companies are involved. They also want to know whether more agencies than just the SEC will become involved and what this is going to mean for the financial sector going forward.

"The Street is worried about more regulation and thinks that something like this is going to cause it," said Tom Schrader, managing director at Stifel Nicolaus. "There's also the fact that Goldman could be facing some punitive damage and it's a pretty widely held stock."

However, stocks have also not seen a notable selloff in nearly two months and were perhaps primed for a retreat, the strategist said. Goldman Sachs provided the catalyst.

The Dow, Nasdaq and S&P 500 rose for seven of the prior eight weeks.

Treasury prices rallied Friday, sending the corresponding yields lower, as investors sought safety in government debt. The dollar gained versus the euro and fell against the yen. Oil and gold prices plunged.

The VIX (VIX), Wall Street's so-called fear gauge, spiked as much as 18% in the afternoon, the biggest runup in two months. By the close, it was up 15%.

0:00 /4:55SEC shows teeth in Goldman suit

Goldman Sachs: The SEC charged Goldman and a vice president, Fabrice Tourre, with failing to disclose conflicts of interest related to a sale of mortgage-related securities that caused two European banks to lose almost $1 billion.

Goldman client Paulson & Co. helped put together an investment offering of mortgage-related securities the hedge fund thought would lose value. Separately, Paulson took out a type of insurance that let it reap huge profits when those securities tanked as the housing market collapsed. But Goldman didn't tell other clients that Paulson was betting on the offering falling apart.

Stocks seem to cut losses after the SEC said it was not pursuing charges against Paulson, Schrader said, as this seemed to reduce fears of a broader crackdown.

The charges came as lawmakers investigate practices and complex investments that helped cause the financial crisis.

SEC charges Goldman Sachs with fraud

Quarterly results: Investors had a sour response to improved quarterly results from a trio of top-tier companies.

General Electric (GE, Fortune 500) reported first-quarter earnings that fell from a year earlier, but topped estimates, on revenue that fell from the prior year and missed estimates. GE said it is expecting earnings growth for the rest of the year, but that more cost-cutting measures may be needed to drive further growth.

Shares of the Dow component fell 2.7%.

Bank of America (BAC, Fortune 500) reported a quarterly profit of $3.2 billion, up from a year ago and easily beating analysts' forecasts. But shares fell 5.5%, with the stock falling in tune with the broader financial market.

Late Thursday, Google (GOOG, Fortune 500) reported higher quarterly earnings and revenue that easily beat expectations, thanks to a recovering advertising market. But investors took a "sell the news" approach and Google's stock fell 7.6% Friday.

Economy: The University of Michigan's consumer sentiment index slipped to 69.5 in mid-April from 73.6 earlier in the month. The reading was a surprise to economists, who forecast it would rise to 75.

On a more positive note, the housing market showed new signs of stabilization in a Commerce Department report released before the opening bell.

Housing starts rose to a 626,000 annual unit rate in March from a 616,000 annual unit rate in February. That was the highest rate of housing starts since November 2008 and topped forecasts for an increase to 610,000. Starts also rose over 20% from a year ago.

Building permits, a measure of builder confidence, rose to a seasonally-adjusted annual rate of 685,000, the highest tally since October 2008. Results topped forecasts and also showed permits rose 34% versus March 2009.

World markets: In overseas trading, European markets fell, with London's FTSE down 1.4%, France's CAC 40 down 1.9% and Germany's DAX down 1.8%. Asian markets slipped too, with the Hong Kong Hang Seng down 1.3% and the Japanese Nikkei down 1.5%.

Bonds: Treasury prices rallied, lowering the yield on the 10-year note to 3.78% from 3.85% late Thursday. The 10-year had risen to as high as 4% a week ago, an 18-month peak. Treasury prices and yields move in opposite directions.

The dollar and commodities: The dollar gained versus the euro and fell against the yen.

COMEX gold for June delivery fell $23.40 to settle at $1,136.90 per ounce.

U.S. light crude oil for May delivery fell $2.27 to settle at $83.24 a barrel on the New York Mercantile Exchange.

Market breadth was negative. On the New York Stock Exchange, losers beat winners five to one on volume of 1.75 billion shares. On the Nasdaq, decliners beat advancers by over three to one on volume of 2.88 billion shares.

Yahoo! Finance

Yahoo! Finance 4:30 pm : The stock market's six-session streak of gains ended in dramatic fashion as the S&P 500 suffered its worst percentage loss in two months following news that the Securities Exchange Commission (SEC) has levied a charge against Goldman Sachs.

Moderate weakness in the early going became something much worse with midmorning news that the SEC has charged Goldman Sachs (GS 160.70, -23.57) and one of the company's vice presidents with fraud related to subprime securities. Goldman Sachs saw some $12 billion, or 13%, of its market cap evaporate. Concern that other investment banks and brokerages may be implicated led the group to a 9.4% loss. That undercut the broader financial sector, which fell 3.8% in its worst slide since February.

While selling was the worst among financials, more than 90% of the stocks in the S&P 500 retreated into the red. Most market participants wanted to lock in profits after they had watched the S&P 500 climb nearly 4% over the course of the previous 10 sessions, 7 of which marked improved 52-week highs.

Not even better-than-expected earnings from blue chips Google (GOOG 550.15, -45.15), Bank of America (BAC 18.41, -1.07), and General Electric (GE 18.97, -0.53) could keep sellers at bay this session. Participants initially responded to reports from the trio with mixed interest as many believed plenty good news had already been built in to the share prices. Some wanted more in the way of improved outlooks.

Economic data was split between positive and negative. Housing starts for March hit an annualized rate of 626,000, which was more than the rate of 610,000 that had been expected and the highest rate in more than one year. Building permits for March came in at an annualized rate of 685,000, which was above the rate of 625,000 that had been expected and was also the highest rate in more than one year.

On the other side of things, the preliminary Consumer Sentiment Survey for April from the University of Michigan came in at 69.5, which was not only below the 75.0 that had been widely expected, but it was also the worst reading since November.

The drastically soured tone turned some to Treasuries. In turn, the benchmark 10-year Note saw its yield slip to 3.76%, which is roughly 25 basis points below where it sat about two weeks ago.

Volatility also spiked in response to this session's selling. The Volatility Index, often euphemistically dubbed the Fear Index, spiked approximately 15%. Amid such action, many have come to question whether the stage has been set for a larger correction or if money will start to move in from the sidelines.

Trading volume surged to its highest level in nearly one month, but it is unclear how much of that is owed to this session's negative headlines since this was an options expiration session.

Advancing Sectors: (None)

Declining Sectors: Financials (-3.8%), Materials (-1.8%), Industrials (-1.6%), Energy (-1.5%), Consumer Discretionary (-1.4%), Tech (-1.4%), Utilities (-1.1%), Telecom (-0.8%), Health Care (-0.6%), Consumer Staples (-0.3%) DJ30 -125.91 NASDAQ -34.43 NQ100 -1.3% R2K -1.3% SP400 -1.2% SP500 -19.54 NASDAQ Adv/Vol/Dec 726/2.85 bln/1962 NYSE Adv/Vol/Dec 571/1.75 bln/2465

3:30 pm : Market weakness and a stronger dollar pressured a broad range of commodities this session. The effort culminated in a 1.2% loss for the CRB Commodity Index.

News that the SEC has brought fraud charges against Goldman Sachs (GS 160.15, -24.12) led to a wave of selling in the broader market. Ensuing volatility helped the dollar secure its gain, such that the Dollar Index remains 0.4% higher.

Precious metals were under some of the stiffest pressure. Gold prices dropped 2.0% to $1137 per ounce, while silver slumped 4.1% to settle at $17.68 per ounce.

Oil prices were pushed 2.7% lower to $83.24 per barrel. It had been as low as $82.52 per barrel.

Natural gas was independent of the other primary commodities. Contract prices managed to make their way 1.6% higher to $4.05 per MMBtu. DJ30 -116.46 NASDAQ -34.86 SP500 -18.40 NASDAQ Adv/Vol/Dec 665/2.43 bln/2026 NYSE Adv/Vol/Dec 557/1.33 bln/2472

3:00 pm : Stocks enter the final hour of trade facing their worst single-session percentage loss in slightly more than two months. Given the extent of this session's slide, stocks are also facing their first weekly loss in seven weeks. Heading into this session, stocks had been up roughly 1.4% week-to-date, but are now down fractionally for the week.

Volatility has eased back, but it is still up a sharp 13%, according to the Volatility Index, which is often euphemistically dubbed the Fear Index. Its spike this session is the sharpest since February. DJ30 -117.52 NASDAQ -33.52 SP500 -18.18 NASDAQ Adv/Vol/Dec 634/2.25 bln/2052 NYSE Adv/Vol/Dec 541/1.24 bln/2503

2:30 pm : Some modest support has surfaced to take stocks up from their afternoon lows. Losses remain steep and broad based, though.

News flow has slowed considerably since word about charges by the SEC against Goldman Sachs (GS 162.29, -21.98) was released earlier this session. Despite the lack of new catalysts, trading volume continues to climb. In fact, more than 1 billion shares have already traded hands on the NYSE. However, market watchers shouldn't read too much into this session's surge in volume since this is an options expiration date. DJ30 -97.64 NASDAQ -30.21 SP500 -15.50 NASDAQ Adv/Vol/Dec 648/2.12 bln/2032 NYSE Adv/Vol/Dec 584/1.17 bln/2457

2:00 pm : The S&P 500 has spent the past hour drifting along just above the 1190 line. That puts the benchmark index down roughly 1.7% this session. Though such a slide has caused some skittishness among market participants, stocks had advanced for six straight sessions ahead of today and the S&P 500 is still up nearly 7% since the start of the year. DJ30 -129.68 NASDAQ -37.93 SP500 -19.67 NASDAQ Adv/Vol/Dec 539/1.98 bln/2130 NYSE Adv/Vol/Dec 465/1.11 bln/2577

1:30 pm : The stock market has made a modest move up from its session low, but weakness remains widespread as more than 90% of the stocks listed in the S&P 500 reside in the red. Should such pressure persist, the stock market will post its worst single-session loss by percent since a 3.1% drop in February.

With equities so weak, interest has been triggered for Treasuries. As such, the benchmark 10-year Note is up 15 ticks. That has puched its yield down to 3.77%. Less than two weeks ago the yield on the 10-year had pushed past 4.00% for the first time since summer 2009. DJ30 -147.52 NASDAQ -37.71 SP500 -20.74 NASDAQ Adv/Vol/Dec 542/1.87 bln/2131 NYSE Adv/Vol/Dec 469/1.05 bln/2564

1:00 pm : Better-than-expected earnings from a few blue chips and upbeat data was met with mixed interest, which made for moderate weakness in the early going. But participants quickly stepped in and sold into the weakness as word that the Securities Exchange Commission will make a case against Goldman Sachs provided an excuse to take profits.

Google (GOOG 557.26, -38.04), Bank of America (BAC 18.72, -0.77), and General Electric (GE 18.83, -0.67) bested Wall Street's earnings estimates for the latest quarter, but market participants weren't entirely enthused given that expectations had become built in to stock prices and that many now want more in the way of improved outlooks.

Not even news that monthly housing starts hit their best annualized rate in more than one year during March. The same can be said for monthly building rates.

The preliminary Consumer Sentiment Survey for April from the University of Michigan disappointed by coming in below expectations at a multimonth low. The survey triggered some pressure in the broader market, but technical support was able to limit losses.

However, near-term technical support was completely thrashed as news broke that the SEC will make a case against Goldman Sachs (GS 163.17, -21.10) and one of the company's vice presidents in regard to fraud related to subprime securities. Although the SEC case is currently limited to GS, the news has put other investment banks and brokerages under the microscope and dropped the broader financial sector to a 3.5% loss, which is its worst single-session percentage slide since February.

The news item has also given broader market participants an excuse to take profits after they watched the stock market climb more than 15% from its February low. Moreover, the pullback has led many to question whether money will now move in from the sidelines or if this sets the stage for a larger correction and a sustained increase in volatility, which is up 23% at the moment, according to the Volatility Index.

For the time, though, stocks have been mired near session lows. The slide has threatened to put an end to the stock market's recent six-session streak of gains and undo its weekly gain. DJ30 -136.94 NASDAQ -38.46 SP500 -19.99 NASDAQ Adv/Vol/Dec 519/1.74 bln/2132 NYSE Adv/Vol/Dec 469/997 mln/2547

12:30 pm : The stock market has stopped its slide as the S&P 500 comes into contact with the 1190 line. Losses remain deep and broad based, but financials continue to grapple with the worst of it. The sector is currently down 3.8%, which puts it on a path toward its worst single-session percentage slide since early February.

Consumer staples stocks have held up relatively well against the selling effort. The sector is down just 0.4% as Coca-Cola (KO 54.85, +0.59) and Kroger (KR 23.57, +0.17) trade with strength. DJ30 -136.49 NASDAQ -39.01 SP500 -21.28 NASDAQ Adv/Vol/Dec 508/1.57 bln/2131 NYSE Adv/Vol/Dec 436/918 mln/2569

12:00 pm : Stocks quietly drifted lower after the open, but selling quickly intensified with news that the SEC will make a case against Goldman Sachs (GS) and one of the company's vice presidents. Although the SEC case is currently limited to GS, the news has put banks and other financial plays under the microscope -- the financial sector is down 3.5%.

While the news item has given participants an excuse to take profits, it will be interesting to see whether this pullback provides an opportunity for the money on the sidelines to get to work or if this is a set up for a larger correction and a sustained increase in volatility. Volatility has already surged so that the Volatility Index is up 18.3%. DJ30 -146.10 NASDAQ -41.39 SP500 -22.44 NASDAQ Adv/Vol/Dec 501/1.43 bln/2127 NYSE Adv/Vol/Dec 431/840 mln/2566

11:30 am : Financials (-3.9%) continue to come under sharp selling pressure in the wake of word that the Securities Exchange Commission (SEC) has charged Goldman Sachs (GS 163.14, -21.13) with fraud. The SEC recently wrapped up a conference call regarding its charge against Goldman, but it had said in response to a question regarding whether Deutsche Bank (DB 75.64, -6.08) will be charged with anything that it will not say if other banks will be brought into the fray. However, the SEC did say that investigation continues into structured products and other instruments. DJ30 -104.29 NASDAQ -26.50 SP500 -17.67 NASDAQ Adv/Vol/Dec 689/1.19 bln/1877 NYSE Adv/Vol/Dec 603 /707 mln/2333

11:00 am : Stocks recently fell under renewed selling pressure amid headlines that Goldman Sachs (GS 165.40, -18.87) has been charged by the Securities Exchange Commission with fraud related to subprime securities. Shares of GS started to steady their slide as buyers stepped in to offer support, but the stock has relapsed to trade near session lows.

Shares of Morgan Stanley (MS 29.96, -0.92) have fallen in sympathy with Goldman Sachs. Investment banks and brokerages are down 7.6%, collectively. Their weakness has undercut the broader financial sector, which is down 3.1%.

Meanwhile, the broader market has been pushed below 1200. The line initially offered support, but now it is acting as a bit of a cieling. DJ30 -55.77 NASDAQ -19.23 SP500 -12.10 NASDAQ Adv/Vol/Dec 735/929 mln/1764 NYSE Adv/Vol/Dec 746/552 mln/2124

10:30 am : The US Dollar Index fell sharply in recent trade, which gave a boost to most commodities. However, the dollar index remains in positive territory, up 0.2%.

May crude oil has traded in negative territory all session. Crude hit lows of $83.65 per barrel shortly after the open of pit trading and has bounced almost $1 off those lows. Currently, crude is trading at $84.41 per barrel, down 1.1%.

May natural gas has been erratic in the last couple of hours of trading. The energy component has traded in positive territory all session and recently hit fresh session highs of $4.05 per MMBtu. the energy component is just below that high currently at $4.04 per MMBtu, up 1.3%.

Precious metals also hit fresh session lows in recent trade with June gold touching $1146.90 per ounce and May silver falling to $18.17 per ounce. Both metals are just above those lows in current trade with gold at $1154 per ounce, down 0.5%, and silver at $18.27 per ounce, down 0.9%. DJ30 -1.06 NASDAQ -7.75 SP500 -3.10 NASDAQ Adv/Vol/Dec 911/657.6 mln/1514 NYSE Adv/Vol/Dec 1098/417.4 mln/1677

10:00 am : Stocks have extended their recent slide amid news that the preliminary Consumer Sentiment Survey for April from the University of Michigan came in at 69.5, which is not only below the 75.0 that had been widely expected, but it is also the worst reading since November. The S&P 500 found support at 1204, however.

Volatility has spiked in recent trade. The Volatility Index is up 3.2% as a result.

Early movers: Gapping up -- PFWD +28.8%, ENCO +16.1%, MBHIP +9.8%, LGF +7.9%, STBC +7.7%, RBS +7.4%, RBPAA +7.3%, DRL +6.2%; Gapping down -- HNSN -16.2%, MSB -11.1%, KKD -11.1%, IDI -9.6%, CRDC -6.8%, PPHM -6.8%, LION -5.9%

Advancing Sectors: Consumer Staples (+0.3%)

Declining Sectors: Financials (-1.4%), Industrials (-1.1%), Tech (-0.6%), Consumer Discretionary (-0.6%), Materials (-0.6%), Energy (-0.5%), Utilities (-0.3%), Health Care (-0.2%)

Unchanged: Telecom DJ30 -33.02 NASDAQ -17.48 SP500 -7.28 NASDAQ Adv/Vol/Dec 660/458 mln/1700 NYSE Adv/Vol/Dec 757/340 mln/1963

09:45 am : Telecom (+0.3%), consumer staples (+0.2%), and health care (+0.1%), laggards in recent sessions, are the only major sectors in higher ground during the early going.

Pressure is most intense against the financial sector, which is down 0.7% as shares of diversified banks and diversified financial service plays are pressured in the wake of the latest report from Bank of America (BAC 19.28, -0.20). Bank of America actually beat the Street's earnings expectations, but many investors now want to see improved forecasts and more explicit signs of confidence in companies as well.

Trading volume is already up sharply. Market participants should keep in mind that today is an options expiration day, so they should not read too much into the high volume levels this session. DJ30 -15.42 NASDAQ -12.62 SP500 -4.61 NASDAQ Adv/Vol/Dec 791/300 mln/1486 NYSE Adv/Vol/Dec 891/276 mln/1730

09:15 am : S&P futures vs fair value: -5.00. Nasdaq futures vs fair value: -9.80. Stocks have strung together six straight sessions of gains and enter Friday with a 1.4% week-to-date gain. Though stock futures currently suggest that the recent string of consecutive gains may be interrupted, the opening loss currently presaged by stock futures is unlikely to snap the stock market's streak of weekly gains before it hits seven. The pressure this morning comes in the face of better-than-expected earnings from Google (GOOG), Bank of America (BAC), and General Electric (GE). Despite their accomplishment, many market participants now want more in the way of improved outlooks and higher quality earnings. Stronger-than-expected monthly housing starts and building permits have been disregarded as a result. The dollar has become a bit of a headwind; it is currently up 0.4% against competing currencies. Its gain comes primarily at the loss of the euro, which continues to get caught up in concerns related to how financial aid for Greece could be put in place.

09:05 am : S&P futures vs fair value: -4.30. Nasdaq futures vs fair value: -8.80. Action in Europe is lackluster for the second straight session. In Britain, the FTSE is down 0.2%. Miners like BHP Billiton (BHP), Rio Tinto (RTP), and Xstrata are down on weak metal prices. An earnings beat by Bank of America (BAC) has helped Barclays (BCS) and Lloyds Banking (LTG), though. Germany's DAX is currently down 0.1%. Lufthansa has been weak as flights are grounded due to a cloud of volcano ash from Iceland. The interruption to flights has also hurt Air France-KLM, which has helped take France's CAC down 0.3%. Carrefour is strong, however, amid reports of strong first quarter sales growth. Though Reuters reported that Greece will auction 1.5 billion euros of 13-week T-bills on April 20, there remain questions and concerns about how to provide financial aid to Greece. Uncertainty over the latter matter has kept aloft yields on Greece's debt. In the meantime, interest rates on bonds for Portugal have been rising as the country's fiscal health remains dubious. In Asia, the MSCI Asia Pacific Index retreated 0.7% and Japan's Nikkei fell 1.5% to its lowest close in nearly three weeks. A stronger yen has been cited as a source of weakness. Banking shares were particularly weak, though reports indicated that banks like of Mitsubishi UFJ Financial Group (MTU) are expected to swing to profit for the fiscal year ended March 31. Tokyo Electron was weak amid a report that stated the company will likely post a smaller-than-expected operating profit. In Hong Kong, the Hang Seng closed 1.3% lower as efforts continued to curtail rising real estate prices. The more stringent requirements for loans proved to be a particular burden for property stocks. Chinese banks were also weakened by the news. In mainland China, the Shanghai Composite closed with a 1.1% loss.

08:35 am : S&P futures vs fair value: -3.10. Nasdaq futures vs fair value: -7.50. Stock futures remain mired in moderate weakness despite an upbeat batch of data. Housing starts for March hit an annualized rate of 626,000, which is more than the rate of 610,000 that had been expected. Starts for the prior month were revised upward to reflect an annualized rate of 616,000, which means that annualized housing starts for March increased 1.6% month-over-month. Building permits for March came in at an annualized rate of 685,000, which is above the rate of 625,000 that had been expected. The March rate is up 7.5% month-over-month from the upwardly revised annual rate of 637,000 for the prior month. Still to come this morning is the preliminary April Consumer Sentiment Survey from the University of Michigan at 9:55 AM ET.

08:05 am : S&P futures vs fair value: -2.00. Nasdaq futures vs fair value: -7.00. Stock futures are down slightly even though earnings from blue chips continue to exceed expectations - during the latest round of reports industry leaders Google (GOOG), Bank of America (BAC), and General Electric (GE) all beat on the bottom line. Shares of BAC and GE have found support, but questions about the quality of Google's report have GOOG under pressure in premarket trade. Shares of GOOG were recently quoted 4.8% lower at $566.51 each. Trade in Europe is tepid amid ongoing questions about how to handle a potential financial bailout of Greece, while Asia was hit with considerable losses amid a higher yet and efforts to cool property speculation. That has only dampened the mood this morning. Housing starts and building permits for March are due at the bottom of the hour. The preliminary Consumer Sentiment Survey for April from the University of Michigan follows at 9:55 AM ET. Fed Governor Warsh is scheduled to hold a speech at 10:00 AM ET and Kansas City Fed President Hoenig will speak at 12:30 PM ET.

06:27 am : S&P futures vs fair value: -3.10. Nasdaq futures vs fair value: -8.00.

06:27 am : Nikkei...11102.18...-171.60...-1.50%. Hang Seng...21865.26...-292.60...-1.30%.

06:27 am : FTSE...5822.25...-2.70...-0.10%. DAX...6292.93...+1.40...0.00.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage