Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

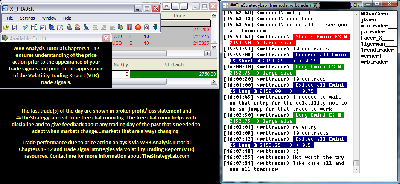

Attachment:

091216-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2750.00.png [ 95.11 KiB | Viewed 321 times ]

091216-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2750.00.png [ 95.11 KiB | Viewed 321 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$2,750.00 dollars or +55.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $2,750.00 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room for anyone to do a real-time review. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=160&t=2456  ##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. TheStrategyLab free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I

keep the peace between members via removing trouble makers so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell. TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Quote:

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=302&t=3259 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

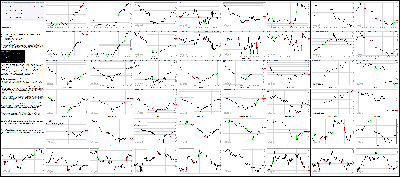

Attachment:

091216-Key-Price-Action-Markets.png [ 1.1 MiB | Viewed 275 times ]

091216-Key-Price-Action-Markets.png [ 1.1 MiB | Viewed 275 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market began the week on a sharply higher note as market participants dialed back rate hike expectations for the coming months. The major averages finished broadly higher, retracing the lion's share of Friday's losses. The Nasdaq Composite (+1.7%) settled slightly ahead of the S&P 500 (+1.5%) and the Dow Jones Industrial Average (+1.3%).

Interest rates remained in focus at the start of the session as participants mulled over a continued downturn in global bond markets. Early weakness was attributed to persistent uncertainty regarding the future path of global monetary policy. Recall that last week the European Central Bank disappointed investors by voting to leave its monetary policy stance unchanged. Furthermore, ECB President Mario Draghi indicated that the Governing Council did not discuss expanding the asset purchase program at the central bank's latest meeting.

Equity indices shook weakness in the opening hour of trade as Atlanta Fed President (non-FOMC voter) Dennis Lockhart and Minneapolis Fed President (non-FOMC voter) Neel Kashkari struck divergent tones on the future path of interest rate normalization. Mr. Lockhart signaled that recent data seriously warrants the discussion of raising rates. However, Mr. Kashkari stated that there's no urgency in raising rates at this time.

The major averages notched fresh session highs shortly after Fed Governor Lael Brainard reaffirmed her dovish stance. Governor Brainard stated that the case for preemptive tightening is less compelling given persistently low inflation and continued slack in the labor market. Ms. Brainard continues to advocate a cautious approach given the limited nature of the Fed's policy toolkit. In response, the implied probability of a rate hike at the September meeting fell to 15.0% from 24.0% in the prior session.

The benchmark index settled near its best level of the day, testing resistance near the 2160 price level. All ten sectors ended in the green with technology (+1.7%), utilities (+1.7%), consumer staples (+1.9%), and telecom services (+2.0%) leading the pack. On the flipside, the commodity-sensitive energy (+0.9%) and materials (+1.0%) sectors finished at the bottom of the leaderboard.

The defensively-oriented consumer staples sector (+1.9%) outperformed as the group recovered from last Friday's 2.1% decline. In the group, Dow component Wal-Mart (WMT 71.94, +1.64) demonstrated relative strength after being upgraded to "Outperform" from "Market Perform" at Cowen. Meanwhile, Philip Morris International (PM 100.64, +3.10) ended higher by 3.2% after Goldman added the stock to its conviction buy list. The broader sector trimmed its month-to-date loss to 1.4%.

In the technology sector (+1.7%), HP (HPQ 14.49, +0.54) gained 3.9% after announcing that it will acquire Samsung's (SSNLF 1250.00, 0.00) printer business for approximately $1.05 billion. Meanwhile, Apple (AAPL 105.44, +2.31) gained 2.2%, recovering from last week's 4.3% decline. The stock was under pressure after unveiling its iPhone 7 device last Thursday. The PHLX Semiconductor Index finished higher by 2.0%, narrowing its month-to-date loss to 2.2%.

Biotechnology outperformed in the health care space (+1.6%), evidenced by the 3.0% gain in the iShares Nasdaq Biotechnology ETF (IBB 287.11, +8.48). In the ETF, Mylan Labs (MYL 41.33, +1.44) rebounded 3.6%. The sub-group also benefited from reports that activist investor Starboard has taken a 4.6% stake in Perrigo (PRGO 95.23, +6.52).

The financial sector (+1.2%) ended behind the broader market as investors trimmed rate hike expectations and as Treasury yields pulled back. In the group, Wells Fargo (WFC 48.54, -0.18) underperformed as the stock continues to see weakness from last Thursday's settlement with the Consumer Financial Protection Bureau, the Office of the Comptroller of the Currency, and the Office of the LA City Attorney.

Treasuries ended modestly higher, recovering from relative weakness at the start of the session. The yield on the 2-yr note fell two basis points to 0.77% while the yield on the 10-yr note ticked down to 1.67% (-1 bps).

Today's participation was above the recent average as more than 992 million shares changed hands on the NYSE floor.

There was no economic data of note released today.

Tomorrow's economic data will be limited to the Treasury Budget for August, which will be released at 14:00 ET.

Russell 2000: +8.6% YTD

S&P 500: +5.6% YTD

Dow Jones: +5.2% YTD

Nasdaq: +4.1 % YTD

3:30 pm: [BRIEFING.COM]

The dollar index was down -0.2% around the 95.16 level

Commodities, as measured by the Bloomberg Commodity Index, were nearly flat (+0.07%) around the 84.08 level

Crude oil closed a volatile session near highs of the day ahead of tomorrow's monthly IEA report

October crude oil futures rose $0.41 (+0.9%) to $46.29/barrel

Monthly IEA data will be released tomorrow morning

API data will be released tomorrow after the bell

Weekly EIA data will be released Wed at 10:30 am ET

Rig count data will be released Friday at 1 pm ET

The next OPEC meeting will take place in Algiers, Algeria from Sept 26-28

Contributing factors affecting the price of oil include:

OPEC released its monthly market report this morning, revised FY17 non-OPEC supply estimates upward by 0.35 mb/d to 56.52 mb/d.

Non-OPEC oil supply in 2016 is now expected to contract by 0.61 mb/d, following an upward revision of 0.18 mb/d from the August MOMR to avg 56.32 mb/d. This has been mainly due to a lower-than-expected decline in US tight oil and a better-than-expected performance in Norway, as well as the early start-up of Kashagan field in Kazakhstan.

World oil demand growth in 2016 is now anticipated to increase by 1.23 mb/d after a marginal upward revision, mainly to reflect better-than-expected OECD data for the first half of the year. Oil demand in 2016 is expected to avg 94.27 mb/d.

Demand for OPEC crude in 2016 is estimated to stand at 31.7 mb/d, some 1.7 mb/d over last year. In 2017, demand for OPEC crude is forecast at 32.5 mb/d, an increase of 0.8 mb/d over the current year.

Natural gas erased all of Friday's losses, closed near 2-week highs

October natural gas closed $0.12 higher (+4.3%) at $2.91/MMBtu

Weekly EIA inventory data will be released Thursday at 10:30 am ET

In precious metals, gold & silver closed lower for the fourth consecutive session, despite the dollar index declining

December gold ended today's session down $9.00 (-0.7%) to $1325.60/oz

December silver closed today's session $0.36 lower (-1.9%) at $19.00/oz

3:00 pm:

[BRIEFING.COM] The major averages trade near recently-established session highs as the S&P 500 (+1.5%) retraces a good chunk of last Friday's 2.5% loss.

All ten sectors trade in the green with the defensively-oriented, and relatively high dividend-yielding, utilities (+1.7%), consumer staples (+1.8%), and telecom services (+2.1%) sectors leading the pack. The financials (+1.0%), energy (+1.0%), and materials (+1.0%) sectors trail behind, but are still sporting solid gains nonetheless.

The Dow Jones Transportation Average (+1.5%) trades neck-and-neck with the benchmark index as rail names outperform. CSX (CSX 28.81, +0.92) has rallied 3.3% after being upgraded to "Overweight" from "Equal Weight" at Barclays. On the flipside, American Airlines (AAL 38.34, -0.14) underperforms after reporting disappointing August traffic data. The airline also reaffirmed its third quarter unit revenue and margin guidance.

Treasuries trade on a mostly higher note, overcoming earlier losses to sport modest price gains across the curve. The yield on the 2-yr note has slipped two basis points to 0.77% while the yield on the 10-yr note has ticked lower by one basis point to 1.66%.

WTI crude ended its day higher by 0.9% ($46.29/bbl; +$0.41).

2:30 pm:

[BRIEFING.COM] The major averages trade at session highs with the Nasdaq Composite (+1.5%) leading the S&P 500 (+1.4%) and the Dow Jones Industrial Average (+1.2%).

The countercyclical health care sector (+1.5%) has marched higher lockstep with the broader market as biotechnology demonstrates relative strength. The iShares Nasdaq Biotechnology ETF (IBB 285.75, +7.12) has gained 2.6%, erasing a modest loss from the prior week. In the ETF, Regeneron Pharmaceuticals (REGN 397.63, +13.20) has jumped 3.5%. The industry group is also drafting higher alongside Perrigo (PRGO 95.55, +6.83). The specialty pharmaceutical name has rallied 7.7% after activist investor Starboard disclosed a 4.6% stake in the company. The broader sector has crossed into positive territory for the year and is now up 0.3% in 2016.

On the commodities front, WTI crude trades higher by 0.7% ($46.24/bbl; +$0.36) ahead of its pit session close at 14:30 ET. The energy component has received a boost in recent action, rising as the U.S. Dollar Index (95.06, -0.27, -0.29%) succumbs to falling U.S. rate hike expectations.

2:00 pm:

[BRIEFING.COM] The stock market has ticked higher in recent action as the S&P 500 climbs 0.9%.

The economically-sensitive financial sector (+0.4%) has recovered a portion of its post-Brainard losses. Governor Brainard recently struck a dovish note, advocating prudence when removing policy accommodations. The Federal Reserve Governor cited muted inflation expectations, persistent labor market slack, and a low neutral rate as reasons why the FOMC has favored a cautious approach. Furthermore, Governor Brainard indicated that the Fed's policy toolkit remains limited if the central bank were to face an unforeseen adverse shock.

The fed funds futures market trimmed rate hike expectations for the coming months. The implied probability of a rate hike at the September meeting fell to 15.0% from Friday's 24.0%. Meanwhile, the likelihood of a rate hike at the November meeting fell to 22.0% from 28.7% in the prior session.

The U.S. Dollar Index (95.06, -0.27, -0.29%) continues to trade modestly lower as the yen extends its gain against the greenback. The dollar has lost 1.0% against the safe-haven yen (101.66), carving out a new session low.

1:35 pm:

[BRIEFING.COM] The major U.S. indices have seen some volatility since our previous update, initially spiking, and then selling off amid the release of comments from Fed Governor Lael Brainard, who urged prudence in the removal of policy accommodation.

A look inside the Dow Jones Industrial Average shows that Wal-Mart (WMT 71.50, +1.20), Procter & Gamble (PG 87.61, +1.37), & Apple (AAPL 104.53, +1.40) are outperforming. Wal-Mart is leading the Dow after being upgraded to Outperform from Market Perform at Cowen.

Conversely, DuPont (DD 67.48, -0.95) is the worst-performing Dow component as materials sit out of the broad-market recovery.

Despite bouncing back from Friday's slump, the DJIA is still -1.3% this month.

Elsewhere, at the top of the hour, the Treasury's $24 bln 3-year auction drew a high yield of 0.947% on a bid to cover of 2.77, and its $20 bln 10-year reopening drew a high yield of 1.699% on a bid-to-cover of 2.35.

1:00 pm:

[BRIEFING.COM] The stock market trades on a higher note at midday, rebounding from heavy losses at the end of last week. Other focal points impacting today's trade have included a reversal in crude oil, a downtick in rate hike expectations, and strong sector leadership from the consumer discretionary (+0.8%), health care (+0.9%), and technology (+1.1%) sectors. At midday, the Nasdaq Composite (+1.0%) leads the S&P 500 (+0.8%) and the Dow Jones Industrial Average (+0.7%).

Today's session began on a lower note as participants responded to a downturn in global markets. Equities pulled back overnight, picking up where U.S. markets left off on Friday. The mover lower was facilitated by growing uncertainty regarding the path of global monetary policy and rising interest rates. Recall that Treasuries tumbled following Thursday's disappointing policy statement from the European Central Bank. The central bank opted to maintain its monetary policy stance, leaving interest rates and asset purchases unchanged.

The broader market trimmed losses in the first hour of trade as participants mulled recent commentary from Atlanta Fed President (non-FOMC voter) Dennis Lockhart and Minneapolis Fed President (non-FOMC voter) Neel Kashkari. President Lockhart indicated that incoming data warrants a serious discussion regarding a potential interest rate hike while President Kashkari believes there's no urgency in raising rates at this time. Both Fed officials took a somewhat standoffish approach, offering no real time table. In response, the implied probability of a rate hike at the September meeting fell to 21.0% from 24.0% in the prior session.

The benchmark index floats near its best level of the day, retracing a portion of Friday's loss. All ten sectors trade in the green with health care (+0.9%), technology (+1.0%), consumer staples (+1.2%), and telecom services (+1.2%) outperforming.

In the consumer staples sector (+1.2%), Dow component Wal-Mart (WMT 71.43, +1.13) outperforms after being upgraded to "Outperform" from "Market Perform" at Cowen. The stock has rallied 1.6%, leading the price-weighted index. Separately, Philip Morris International (PM 99.60, +2.06) has jumped 2.1% after being added to the conviction buy list at Goldman.

The influential technology sector (+1.0%) demonstrates relative strength as the high-beta chipmakers outperform. The PHXL Semiconductor Index has rebounded 1.4% following last week's 4.8% decline. Separately, top-weighted Apple (AAPL 104.81, +1.68) has rebounded 1.6% after last week's special event. The stock fell 4.3% in the prior week after unveiling the iPhone 7. Meanwhile, HP (HPQ 14.35, +0.40) has rallied 2.9% after announcing that it will acquire Samsung's (SSNLF 1250.00, 0.00) printer business for approximately $1.05 billion.

The financial sector (+0.6%) trades behind the broader market as investors trim rate hike expectations. On a side note, participants will also hear from Fed Governor Lael Brainard later in the session. Ms. Brainard will speak at the Chicago Council on Global Affairs. The timing of the speech has led to speculation that the dovish Fed official may attempt to signal a potential hike in the coming months. Governor Brainard is slated to speak at 1:15 p.m. ET.

Treasuries trade on a lower note with yields rising through the curve. The yield on the 10-yr note has gained one basis point (1.69%) while the yield on the 2-yr note is also higher by one basis point (0.79%).

There was no economic data of note released today.

12:25 pm:

[BRIEFING.COM] The broader market trades near its session high as the S&P sports a gain of 0.5%.

The commodity-sensitive energy sector (-0.1%) floats modestly beneath its flat line, shrugging off an uptick in crude oil futures. WTI crude trades higher by 0.1% ($45.93/bbl; +$0.05) amid continued softening in the U.S. Dollar Index (95.17, -0.17, -0.18%). The energy component has gained 2.7% so far in September.

In the group, ConocoPhillips (COP 42.80, +0.55) has rallied 1.3% after being upgraded to "Overweight' from "Neutral" at JP Morgan. Conversely, Occidental Petroleum (OXY 74.98, -1.13) has declined by 1.5% after the stock had its rating cut to "Underweight" at JP Morgan. Separately, Dow component Exxon Mobil (XOM 86.67, -0.17) has declined 0.2%, trading behind the price-weighted index. The broader sector sports a month-to-date gain of 1.1%, leading the remaining sectors over that period.

The U.S. Dollar Index (95.17, -0.17, -0.18%) has moved lower in recent action as the buck loses ground to the safe-haven yen. The dollar/yen pair trades lower by 0.8% (101.90) after sliding from 102.00 price level.

12:00 pm:

[BRIEFING.COM] The major averages trade near new session highs with the Nasdaq Composite (+0.9%) leading the S&P 500 (+0.6%).

All ten sectors trade in the green with technology (+0.9%) leading countercyclical telecom services (+0.8%) and health care (+0.8%) on top of the leaderboard.

The consumer discretionary space (+0.7%) trades ahead of the broader market as retail names outperform. The SPDR S&P Retail ETF (XRT 43.86, +0.34) has rebounded 0.9%, trimming last week's 2.2% decline. In the ETF, apparel retailers lead with L Brands (LB 72.40, +0.97) and Gap (GPS 23.71, +0.36) rising 1.4% and 1.6%, respectively. Meanwhile, Amazon (AMZN 768.14, +8.01) has jumped 1.1%. The ETF has declined 1.4% month-to-date, which compares to a loss of 2.1% in the broader sector.

Conversely, restaurant names underperform as Chipotle Mexican Grill (CMG 426.03, -0.52) and Starbucks (SBUX 54.18, -0.16) slip a respective 0.2% and 0.3%.

On the commodities front, WTI crude trades higher by 1.1% ($46.36/bbl; +$0.48) while gold has retreated 0.6% to $1,326.40/ozt.

11:30 am:

[BRIEFING.COM] The S&P 500 (+0.3%) floats near a fresh session high.

The economically-sensitive financial sector (-0.1%) has continued to pare its loss, rebounding from an opening decline of 0.9%. The group was under pressure following somewhat dovish remarks from Minneapolis Fed President, and non-FOMC voter, Neel Kashkari. The Fed President indicated that there doesn't appear to be any huge urgency in acting, but that he continues to pay close attention to incoming inflation data. The fed funds futures markets signals that the implied probability of a rate hike at the September meeting slipped to 21.0% from 24.0% earlier this morning.

Money center banks and life insurance names underperform in the space as JPMorgan (JPM 66.38, - 0.27) and Prudential (PRU 78.67, -0.50) decline 0.4% and 0.6%, respectively. Separately, Wells Fargo (WFC 48.24, -0.47) has lost 1.0%, seeing continued weakness from last Thursday's settlement with the Consumer Financial Protection Bureau, the Office of the Comptroller of the Currency, and the Office of the LA City Attorney.

Treasuries trade on a lower note with yields rising through the curve. The yield on the 10-yr note has gained one basis point (1.69%).

10:55 am:

[BRIEFING.COM] The broader market has pulled back from a recently-established session high, leaving the S&P 500 up 0.2%.

The influential technology sector (+0.5%) outperforms as top-weighted Apple (AAPL 104.46, +1.33) rebounds 1.3%. The stock declined 4.3% last week after unveiling the iPhone 7. Fellow tech heavyweights Facebook (FB 127.50, +0.40) and Alphabet (GOOG 763.35, +3.69) have gained 0.3% and 0.5%, respectively. Separately, the high-beta chipmakers demonstrate relative strength, evidenced by the 0.6% gain in the PHLX Semiconductor Index. The price-weighted index fell 4.8% last week, extending its monthly loss to 4.1%. The index currently shows a month-to-date loss of 3.6%, trailing the broader technology sector (+0.5%; month-to-date: -1.3%).

On the M&A front, HP (HPQ 14.17, +0.22) has rallied 1.6% after announcing that it will acquire Samsung's (SSNLF 1250.00, 0.00) printer business for approximately $1.05 billion.

Crude oil futures reversed in recent action, benefiting from some softening in the dollar. WTI crude trades higher by 1.0% ($46.33/bbl, +$0.45) after testing the $44.70 price level overnight.

10:30 am: [BRIEFING.COM]

Commodities, as measured by the Bloomberg Commodity Index, were -0.2% around the 83.91 level

Crude oil saw increased volatility, fell nearly 2% after the monthly OPEC report before recovering to trade nearly flat, extended Friday's losses

October crude oil futures were down $0.10 (-0.2%) around the $45.78/barrel level

Contributing factors affecting the price of oil include:

On Friday, Baker Hughes announced the total U.S. rig count was up 11 to 508 rigs, following last week's increase of 8 rigs.

The avg U.S. rig count for Aug 2016 was 481, up 32 from the 449 counted in July 2016, and down 402 from the 883 counted in Aug 2015.

The avg Canadian rig count for Aug 2016 was 129, up 35 from the 94 counted in July 2016, and down 77 from the 206 counted in Aug 2015.

The worldwide rig count for Aug 2016 was 1,547, up 66 from the 1,481 counted in July 2016, and down 679 from the 2,226 counted in Aug 2015.

OPEC released its monthly market report this morning, revised FY17 non-OPEC supply estimates upward by 0.35 mb/d to 56.52 mb/d.

Non-OPEC oil supply in 2016 is now expected to contract by 0.61 mb/d, following an upward revision of 0.18 mb/d from the August MOMR to avg 56.32 mb/d. This has been mainly due to a lower-than-expected decline in US tight oil and a better-than-expected performance in Norway, as well as the early start-up of Kashagan field in Kazakhstan.

World oil demand growth in 2016 is now anticipated to increase by 1.23 mb/d after a marginal upward revision, mainly to reflect better-than-expected OECD data for the first half of the year. Oil demand in 2016 is expected to avg 94.27 mb/d.

Demand for OPEC crude in 2016 is estimated to stand at 31.7 mb/d, some 1.7 mb/d over last year. In 2017, demand for OPEC crude is forecast at 32.5 mb/d, an increase of 0.8 mb/d over the current year.

Reminders:

Monthly IEA data will be released tomorrow

The next OPEC meeting will take place in Algiers, Algeria from Sept 26-28

API data will be released tomorrow after the bell

Weekly EIA petroleum data will be released at 10:30 am ET on Wed

Natural gas erased all of Friday's losses, rallied to fresh session highs in morning pit trading

October natural gas futures were up $0.10 (+3.7%) around the $2.90/MMBtu level

EIA natural gas inventory data will be released Thursday at 10:30 am ET

Silver futures decline for the fourth consecutive session as the dollar index traded nearly flat

December silver futures were down $0.36 (-1.9%) around the $19.01/oz level

10:00 am:

[BRIEFING.COM] The broader market floats near a session high with the Nasdaq Composite (+0.1%) and the S&P 500 (+0.1%) trading slightly ahead of the Dow Jones Industrial Average (UNCH).

The leaderboard remains little changed with countercyclical health care (+0.5%), consumer staples (+0.7%), utilities (+0.8%), and telecom services (+1.1%) leading the upside. Conversely, energy (-0.1%), and financials (-0.5%) underperform.

In the consumer staples sector (+0.7%), Dow component Wal-Mart (WMT 71.17, +0.87) leads after being upgraded to "Outperform" from "Market Perform" at Cowen. The stock tops the price-weighted index, gaining 1.2%. Conversely, Reynolds American (RAI 47.15, 0.00) trades flat after being downgraded to "Neutral" at Goldman.

The U.S. Dollar Index (95.37, +0.03, +0.04%) is modestly higher as the greenback trims its loss against the safe-haven yen. The dollar/yen pair trades lower by 0.7% (102.00) after moving off the 101.74 price level overnight. Separately, the dollar has gained 0.5% against the commodity-sensitive Canadian dollar (1.3117). The move has been spurred on by a 0.7% loss in crude oil futures ($45.55/bbl, -$0.33).

9:45 am:

[BRIEFING.COM] The stock market began the day on a mixed note with the Dow Jones Industrial Average (-0.2%) trailing the S&P 500 (UNCH) and the Nasdaq Composite (+0.1%).

Seven sectors trade in the green with defensively-oriented utilities (+0.4%), consumer staples (+0.4%), and telecom services (+0.6%) outperforming. Conversely, energy (-0.3%) and financials (-0.6%) lead to the downside.

The Dow Jones Transportation Average (-0.3%) demonstrates relative weakness as airline names underperform in the index. United Continental (UAL 51.59, -0.86) trades lower by 1.7% after reporting operational results for August. The company also reaffirmed revenue metrics for the third quarter. The U.S. Global Jets ETF (JETS 22.78, -0.39) has declined 1.7%.

In the health care space (+0.2%), biotechnology outperforms, evidenced by the 0.9% gain in the iShares Nasdaq Biotechnology ETF (IBB 281.04, +2.41). Celgene (CELG 105.68, +1.21) trades higher by 1.1% after receiving a bullish note from SunTrust.

On the commodities front, WTI crude trades lower by 1.1% ($45.36/bbl, -$0.52) while gold has slipped 0.6% to $1,326.30/ozt.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: -7.00. Nasdaq futures vs fair value: -18.90.

The stock market is on track for a lower start as the S&P 500 futures trade seven points below fair value.

Equity futures remain under pressure as participants continue to eye rising interest rates and potential shifts in global monetary policy. The ongoing angst comes on the heels of hawkish remarks from Federal Reserve officials and last week's disappointing policy statement from the European Central Bank. The ECB disappointed investors last Thursday, opting to keep its monetary policy stance unchanged. Furthermore, ECB President Mario Draghi startled investors by indicating that the Governing Council did not discuss extending the asset purchase program at the bank's latest meeting. However, the central bank did affirm plans to continue purchasing assets through March 2017 or beyond, if needed.

On the home front, Federal Reserve speakers remain in focus as participants look ahead to remarks from Fed Governor Lael Brainard. Ms. Brainard will speak at the Chicago Council on Global Affairs. The timing of the speech has caught participants slightly off guard, leading to speculation that the dovish Fed official may attempt to signal a potential hike in coming months. Governor Brainard is slated to speak at 1:15 ET. Separately, Atlanta Fed President, and non-FOMC voter, Dennis Lockhart stated earlier that economic data warrants a serious discussion regarding the speed and path of future rate hikes. However, Mr. Lockhart did not offer a timetable for policy moves.

WTI crude trades lower by 1.6% ($45.15/bbl, -$0.73), responding to general risk aversion and a mixed reading of OPEC's monthly oil market report. The oil cartel expects OPEC oil demand to come in at 31.7 million barrels per day in 2016, rising approximately 1.7 million barrels per day from last year. Demand in 2017 is expected to rise to 32.5 million barrels per day.

There is no economic data of note scheduled to be released today.

8:56 am: [BRIEFING.COM] S&P futures vs fair value: -9.50. Nasdaq futures vs fair value: -25.70.

The S&P 500 futures trade ten points below fair value.

Equity indices across the Asia-Pacific region ended Monday on a broadly lower note as cautious sentiment carried over from last week. Japan's Nikkei lost 1.7% amid a rally in the yen while equities in China (-1.9%) and Hong Kong (-3.4%) underperformed. The People's Bank of China set the yuan midpoint at 6.6908 against the dollar, which was the weakest fix since the end of August. There was some speculation that state-owned enterprises sold dollars in order to support the yuan.

In economic data:

Japan's August PPI -0.3% month-over-month (expected -0.2%; last -0.1%); -3.6% year-over-year (consensus -3.5%; last -3.9%). July Core Machinery Orders +4.9% month-over-month (expected -3.5%; last 8.3%); +5.2% year-over-year (consensus 0.3%; previous -0.9%). Machine Tool Orders -8.4% year-over-year (last -19.7%)

---Equity Markets---

Japan's Nikkei lost 1.7% with all ten sectors ending in the red. Materials (-2.7%), industrials (-2.1%), and technology (-1.8%) paced the retreat while utilities (-0.6%) outperformed. JTEKT, Alps Electric, Sumitomo Metal Mining, Canon, JFE Holdings, Nissan Chemical Industries, TDK, Softbank, and Fanuc lost between 3.0% and 5.0%.

Hong Kong's Hang Seng fell 3.4% with all 50 components registering losses. Financials and property-related names underperformed with China Resources Land, China Construction Bank, Hang Lung Properties, China Overseas, Bank of China, and ICBC losing between 4.7% and 5.7%.

China's Shanghai Composite climbed into the close, but still lost 1.9%. Shanghai Kai Kai Industrial, Tianjin Global Magnetic Card, Yanzhou Coal Mining, and Irico Display Devices lost between 6.6% and 7.2%.

Major European indices trade lower across the board, retreating alongside sovereign bonds. Reports out of Greece suggest differences between the country's government and International Monetary Fund officials could get in the way of the Greek bailout. This follows similar reports from last week. Italy's MIB (-2.5%) has paced today's retreat with bank shares leading the way.

Economic data was limited:

Italy's Quarterly Unemployment Rate ticked down to 11.5% from 11.6%

---Equity Markets---

UK's FTSE is down 1.6% with Associated British Foods falling 9.0% after cautious guidance for next year overshadowed above-consensus results. Miners and financials also lag with Anglo American, Glencore, Rio Tinto, RBS, Lloyds Banking, Standard Chartered, and Barclays down between 3.6% and 5.7%.

Germany's DAX has given up 1.8%. E.On has tumbled 14.6% after spinning off its traditional gas and coal operations. Commerzbank and Deutsche Bank are both down near 4.0% while exporters BMW, Daimler, and Volkswagen show losses between 2.3% and 2.6%.

France's CAC has retreated 1.8% amid broad weakness. ArcelorMittal is the weakest performer, down 5.0%, while Societe Generale, AXA, BNP Paribas, and Credit Agricole are down between 3.1% and 3.5%.

Italy's MIB has slid 2.5% with Unicredit, Banco Popolare, UBI Banca, Banca di Milano Scarl, Banca Pop Emilia Romagna, and Mediobanca are down between 3.4% and 4.8%.

8:31 am: [BRIEFING.COM] S&P futures vs fair value: -8.70. Nasdaq futures vs fair value: -26.10.

Index futures float above session lows with the S&P 500 futures remaining nine points below fair value.

On the central bank front, Atlanta Fed President, and non-FOMC voter, Dennis Lockhart recently stated that the U.S. economy continues to sustain sufficient momentum to substantially achieve the Fed's monetary policy objectives. President Lockhart also indicated that economic data warrants a serious discussion regarding rate hikes. However, Mr. Lockhart failed to offer a timetable for potential rate hikes. The fed funds futures market remains little changed after the comments. At this juncture, the implied probability of a rate hike at the September meeting sits at 24.0%, unchanged from Friday's likelihood.

The U.S. Dollar Index (95.32, -0.01, -0.01%) floats modestly lower as the pound and the yen hold gains against the greenback. The pound has ticked higher by 0.1% against the buck (1.3285) while the dollar/yen pair trades lower by 0.8% (101.92). The safe-haven currency has benefited from risk aversion in global markets.

8:06 am: [BRIEFING.COM] S&P futures vs fair value: -11.20. Nasdaq futures vs fair value: -30.40.

U.S. equity futures trade broadly lower as the S&P 500 futures trade eleven points below fair value. Index futures fell lockstep with global markets, extending last week's selloff. The move lower has been facilitated by growing uncertainty regarding the future path of global monetary policy and angst surrounding higher interest rates.

On the home front, the future path of interest rate normalization remains in focus as participants look ahead to commentary from Fed Governor Lael Brainard. Governor Brainard is one of the more dovish members of the FOMC, but speculation has arisen that Ms. Brainard will attempt to prepare markets for a potential September hike. The fed funds futures market currently estimates the implied probability of an interest rate hike at the September meeting at 24.0%. Governor Brainard is scheduled to speak at 1:15 p.m. ET.

Treasuries trade on a lower note as the long end of the curve demonstrates relative weakness. The yield on the 10-yr note is higher by two basis points (1.69%) while the yield on the 2-yr note has ticked higher by one basis point (0.79%).

There is no economic data of note scheduled to be released today.

In U.S. corporate news of note:

Potash (POT 17.30, +0.33): +1.9% after announcing a $36 billion merger of equals with Agrium (AGU 95.20, 0.00)

TrueCar (TRUE 8.37, -0.46): -5.2% following the company being downgraded to "Underweight" from "Equal-Weight" at Morgan Stanley

Perrigo (PRGO 92.07, +3.36): +3.8% after Starboard confirmed a 4.6% stake in the company

Praxair (PX 115.41, -2.00): -1.7% following the company announcing that it terminated potential merger talks with Linde (LNAGF 171.00, 0.00)

Reviewing overnight developments:

Asia-Pacific indices began the week on a broadly lower note with Hong Kong's Hang Seng (-3.4%), China's Shanghai Composite (-1.9%), and Japan's Nikkei (-1.7%).

In economic data:

Japan's August PPI -0.3% month-over-month (expected -0.2%; last -0.1%); -3.6% year-over-year (consensus -3.5%; last -3.9%). July Core Machinery Orders +4.9% month-over-month (expected -3.5%; last 8.3%); +5.2% year-over-year (consensus 0.3%; previous -0.9%). Machine Tool Orders -8.4% year-over-year (last -19.7%)

In news:

Indices began the week under pressure as cautious sentiment carried over from last week.

The People's Bank of China set the yuan midpoint at 6.6908 against the dollar, which was the weakest fix since the end of August.

There was some speculation that state-owned enterprises sold dollars in order to support the yuan.

European indices trade lower across the board with Germany's DAX (-1.8%), France's CAC (-1.8%), and the U.K.'s FTSE (-1.6%). Elsewhere, Italy's MIB has slid 2.6%.

Economic data was limited:

Italy's Quarterly Unemployment Rate ticked down to 11.5% from 11.6%

In news:

Reports out of Greece suggest differences between the country's government and International Monetary Fund officials could get in the way of the Greek bailout.

6:16 am: [BRIEFING.COM] S&P futures vs fair value: -18.00. Nasdaq futures vs fair

value: -47.00.

6:16 am: [BRIEFING.COM] Nikkei...16673...-292.80...-1.70%. Hang Seng...23291...-809.10...-3.40%.

6:16 am: [BRIEFING.COM] FTSE...6669.24...-107.70...-1.60%. DAX...10357.99...-215.50...-2.00%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

TheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com