Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

091316-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5187.50.png [ 92.81 KiB | Viewed 569 times ]

091316-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5187.50.png [ 92.81 KiB | Viewed 569 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$5,187.50 dollars or +103.75 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $5,187.50 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room for anyone to do a real-time review. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=160&t=2457  ##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. TheStrategyLab free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I

keep the peace between members via removing trouble makers so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell. TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Quote:

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=302&t=3259 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

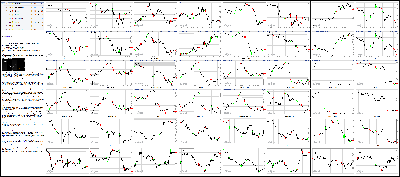

Attachment:

091316-Key-Price-Action-Markets.png [ 1.12 MiB | Viewed 494 times ]

091316-Key-Price-Action-Markets.png [ 1.12 MiB | Viewed 494 times ]

click on the above image to view today's price action of key markets 4:15 pm: [BRIEFING.COM] The major averages ended the Tuesday affair sharply lower as rising long-term interest rates pressured the broader market. The upswing in interest rates was led by growing uncertainty surrounding the future path and effectiveness of global central bank policy. The S&P 500 (-1.5%) settled behind the Dow Jones Industrial Average (-1.4%) and the Nasdaq Composite (-1.1%).

Equity indices began the session under pressure as investors continued to mull over central bank policy here at home and from overseas. Fed Governor Lael Brainard reaffirmed a dovish stance in the prior session, stating that the case for preemptive tightening has become less compelling. In response, the implied probability of a rate hike at the September meeting fell to 15.0% from 24.0% at the start of the week.

The dovish posture failed to carry over buying interest into today's session as participants responded to mixed performances from global markets and a downturn in crude oil. The energy component was under pressure after the International Energy Agency's monthly report struck a bearish tone. The IEA cut its global demand growth forecast for 2016 to 1.3 million barrels per day (previous: 1.4 million barrels) while the group also trimmed its 2017 growth estimate to 1.2 million barrels (previous: 1.4 million barrels). The negative revisions cast doubt on the potential timetable for an oil market rebalancing.

The benchmark index notched a session low (2120.27) shortly after midday, finishing narrowly above that level. All ten sectors ended in the red with financials (-1.8%), materials (-1.9%), telecom services (-2.0%), and energy (-2.9%) acting as notable laggards. Conversely, technology (-0.6%) and consumer staples (-1.4%) ended with the narrowest losses.

The commodity-sensitive energy sector (-2.9%) ended broadly lower amid a sustained downturn in crude oil. WTI crude finished lower by 3.0% ($44.92/bbl; -$1.37). In the group, oilfield service names underperformed with Baker Hughes (BHI 48.34, -1.36) and Halliburton (HAL 41.11, -1.29) losing 2.8% and 3.0%, respectively. On a side note, the American Petroleum Institute is slated to release its weekly inventory report this evening while the Department of Energy is scheduled to release its more influential inventory report tomorrow at 10:30 ET.

The economically-sensitive financial sector (-1.8%) was under pressure as participants reassessed rate hike expectations for the year. In the group, Wells Fargo (WFC 46.96, -1.58) declined 3.7%. The name has been under pressure since announcing a settlement with the Consumer Financial Protection Bureau last Thursday. The broader sector has declined 2.8% this month and currently sports a year-to-date loss of 0.2%.

Biotechnology underperformed in the health care space (-1.5%), evidenced by the 1.6% loss in the iShares Nasdaq Biotechnology ETF (IBB 282.62, -4.49). The ETF was under pressure after rallying 3.0% in the prior session. In the ETF, Vertex Pharmaceuticals (VRTX 95.27, -2.59) underperformed after Raymond James issued a "Market Perform" designation on the stock.

The influential technology space (-0.6%) finished ahead of the benchmark index as top-weighted component Apple (AAPL 108.12, +2.68) led. The Dow component rallied 2.6% after T-Mobile (TMUS 45.34, -0.59) and Sprint (S 6.56, -0.36) reported bullish pre-order data for the iPhone 7. The PHLX Semiconductor Index (-0.9%) also finished ahead of the broader market as iPhone suppliers drafted higher on the news. Broadcom (AVGO 165.24, +0.76) and Skyworks (SWKS69.36, +1.02) ended higher by 0.5% and 1.5%, respectively.

Treasuries ended sharply lower with the long end of the curve demonstrating relative weakness. The yield on the 2-yr note rose two basis points to 0.79% while the yield on the 10-yr note jumped six basis points to 1.72%.

Today's participation was above the recent average as more than one billion shares changed hands on the NYSE floo

Today's economic data was limited to the Treasury Budget for August:

The Treasury Budget for August showed a deficit of $107.1 billion versus a deficit of $64.4 billion in August 2015. The Treasury Budget data is not seasonally adjusted, so the August deficit cannot be compared to the $112.8 billion deficit registered in July.

Total receipts in August were $231.3 billion while total outlays were $338.4 billion.

Receipts were $20.5 billion more than receipts in August 2015. Total outlays, meanwhile, were $63.2 billion more than the same period a year ago.

The 12-month deficit widened to $529.9 billion from $487.2 billion in July.

Tomorrow's economic data will include the 7:00 ET release of the weekly MBA Mortgage Index. Meanwhile, Import/Export Prices for August will each cross the wires at 8:30 ET.

Russell 2000: +6.8% YTD

S&P 500: +4.1% YTD

Dow Jones: +3.7% YTD

Nasdaq: +3.0% YTD

3:30 pm: [BRIEFING.COM]

The dollar index was up +0.5% around the 95.61 level, weighing on commodities overall

Commodities, as measured by the Bloomberg Commodity Index, were -1.3% around the 83.02 level

Crude oil erased yesterday's gains, closed near session lows below the $45.00/barrel handle support ahead of tonight's API data

October crude oil futures fell $1.37 (-3.0%) to $44.92/barrel

IEA data highlights:

The IEA lowered global demand forecasts for FY16 by ~100k barrels per day for FY16 to +1.3 mln barrels a day. The IEA also lowered FY17 demand growth forecasts to +1.2 mln barrels per day, about 200k less than previous estimates.

Decline in oil demand in China and Europe were also cited by the IEA as factors influencing the updated forecast.

Saudi Arabia takes the top spot from US shale as the world's largest producer.

IEA estimated that the U.S. had shut in 460k barrels a day of production, while Saudi Arabia pumped out an extra 400k barrels a day.

OPEC producer United Arab Emirates increased oil production by 20k barrels per day to 3.09 mln barrels, its highest output level ever.

Data reminders:

The next OPEC meeting will take place in Algiers, Algeria from Sept 26-28

API data will be released today after the bell

Weekly EIA petroleum data will be released Wed at 10:30 am ET

Rig count data will be released Friday at 1 pm ET

Natural gas ended afternoon pit trading unchanged ahead of Thursday's EIA inventory data

October natural gas closed flat at $2.91/MMBtu

Weekly EIA data will be released Thursday at 10:30 am ET

In precious metals, gold & silver traded modestly lower & in tandem with each other as the dollar index surged

December gold ended today's session down $1.60 (-0.1%) to $1324.00/oz

December silver closed today's session $0.02 lower (-0.1%) at $18.98/oz

3:00 pm:

[BRIEFING.COM] As the stock market enters its final hour of trade, the S&P 500 (-1.4%) trades behind the Dow Jones Industrial Average (-1.3%) and the Nasdaq Composite (-1.1%).

All ten sectors trade in the red with telecom services (-1.9%), materials (-2.0%), and energy (-2.7%) rounding out the leaderboard. The remaining decliners sport losses between 0.7% (technology) and 1.7% (financials).

The PHLX Semiconductor Index (-1.0%) trades ahead of the broader market as iPhone suppliers Qorvo (QRVO 53.87, +0.11), Broadcom (AVGO 16.18, +0.70), and Skyworks (SWKS 69.17, +0.3) gain between 0.2% and 1.0%. The group is drafting higher alongside Apple (AAPL 108.00, +2.56) following the release of positive iPhone 7 pre-order data from service providers. The price-weighted index has gained 1.0% this week, leading the benchmark index (-1.4%; week-to-date: UNCH) over that time.

Treasuries trade near session lows as the long end of the curve continues to show relative weakness. The yield on the 30-yr bond has risen eight basis points (2.47%) while the yield on the 2-yr note is higher by four basis points (0.81%).

2:30 pm:

[BRIEFING.COM] The S&P 500 (-1.6%) has inched lower in recent trade, floating four points above its session low.

The Dow Jones Transportation Average (-1.9%) trades behind the broader market as airlines weigh on the index. The U.S. Global Jets ETF (JETS 22.90, -0.44) has declined 1.9%. Conversely, low-cost carrier JetBlue Airways (JBLU 17.26, +0.48) has jumped 2.8% after reporting that August traffic increased 6.2% year-over-year. The company also reported that revenue per available seat mile fell 5.5% year-over-year in August while third-quarter revenue per available seat mile is estimated to fall 3.0% to 4.0% year-over-year.

In the broader industrial sector (-1.5%), Eaton (ETN 63.27, -1.72) underperforms, slipping 2.7%. The stock has declined 4.3% since being downgraded to "Sector Weight" at KeyBanc on September 9. This compares to a loss of 3.0% in the Industrial Select Sector SPDR ETF (XLI 57.04, -0.81) over that same time.

WTI crude is trading lower by 2.7% ($45.01/bbl; -$1.28) ahead of its pit session close at 14:30 ET. The American Petroleum Institute is scheduled to release its weekly inventory report this evening. Separately, the Department of Energy will release its more influential inventory report tomorrow at 10:30 ET.

2:00 pm:

[BRIEFING.COM] The major averages have pulled back in recent action as the S&P 500 trades lower by 1.5%.

The leaderboard remains little changed with health care (-1.6%), financials (-1.8%), telecom services (-2.4%), and energy (-2.7%) rounding out the board.

The U.S. Dollar Index (95.52, +0.42, +0.44%) trades near a fresh session high as the greenback extends its lead over the safe-haven yen. The move in the currency pair was facilitated by reports speculating that the Bank of Japan may seek to expand its foray into negative interest rates when its meets on September 21. Recall that the central bank disappointed investors with its latest policy statement, opting to maintain its key interest rate. The dollar has gained 0.8% against the yen (102.62), jumping off the 102.20 price level earlier in the session.

On the economic front, the Treasury Budget statement for August showed a deficit of $107.1 billion. The Treasury data is not seasonally adjusted so the August deficit cannot be compared to the $112.80 billion deficit in July.

1:35 pm:

[BRIEFING.COM] The major U.S. indices have pared some of their losses in recent action, but still show heavy losses in afternoon trading.

A look inside the Dow Jones Industrial Average shows that Chevron (CVX 99.72, -2.53), American Express (AXP 64.36, -1.54), & Verizon (VZ 51.35, -1.22) are underperforming. Chevron is leading the Dow lower as energy stocks slump following this morning's International Energy Agency (IEA) report. The organization trimmed its FY16 & FY17 demand growth estimates, sending crude futures lowers.

Conversely, Apple (AAPL 108.25, +2.81) is the best-performing, and lone Dow component in positive territory following confirmations from phone carriers T-Mobile & Sprint of strong orders thus far for the iPhone 7 & iPhone 7 Plus. Sprint said orders were up nearly 400% in the first three days compared to last year, while T-Mobile stated that pre-orders 'shattered' the previous record, setting a single day sales record for any smartphone the carrier has ever sold.

Erasing a large portion of yesterday's gains, the DJIA is now down 1.6% this month.

Elsewhere, at the top of the hour, the Treasury's $12 bln 30-year auction was met with soft demand, drawing a high yield of 2.475% on a bid-to-cover of 2.13.

1:05 pm:

[BRIEFING.COM] The stock market is under pressure at midday as the major averages pull back after yesterday's rebound. Focal points impacting today's trade have included a downturn in crude oil futures, a rebound in the dollar, and a spike in Treasury rates. At midday, the S&P 500 (-1.7%) trades behind the Dow Jones Industrial Average (-1.5%) and the Nasdaq Composite (-1.4%).

Today's session began on a lower note as a lack of carry over buying interest and a downturn in crude oil weighed on index futures. Global bourses finished on a mixed note, shrugging off the positive bias from yesterday's rebound here at home. China's Shanghai Composite (+0.1%) finished little changed despite a string of stronger-than-expected economic data. Meanwhile, European markets finished with losses, carving out lows during the U.S. session.

A bearish reading of the International Energy Agency's monthly report also contributed to early weakness. The IEA lowered its global demand growth forecast for 2016 to 1.3 million barrels per day (previous: 1.4 million barrels) while also cutting its 2017 estimates to 1.2 million barrels (previous: 1.4 million barrels). The disappointing outlook has called into question the potential timetable for an oil market rebalancing. At this juncture, WTI crude trades lower by 2.7% ($45.02/bbl; -$1.29).

The major averages extended early losses through the first half of trade as heavily-weighted health care (-1.8%) and financials (-2.1%) weigh on the broader market. The benchmark index trades at a session low, attempting to find support near the 2120 price level. All ten sectors trade in negative territory with financials (-2.1%), materials (-2.4%), telecom services (-2.4%), and energy (-2.8%) rounding out the board. Conversely, heavily-weighted technology (-0.9%) and consumer staples (-1.4%) show the narrowest losses.

In the commodity-sensitive energy sector (-2.8%), oilfield service names demonstrate relative weakness as Baker Hughes (BHI 48.38, -1.32) and Halliburton (HAL 40.96, -1.44) decline 2.9% and 3.4%, respectively. Meanwhile, Anadarko Petroleum (APC 57.45, -0.34) outperforms after announcing the acquisition of deep water assets from Freeport McMoRan (FCX 10.07, -1.01). Anadarko has received several upgrades and price target increases following the news.

The economically-sensitive financial sector (-2.1%) has been under pressure as participants continue to reassess rate hike expectations for the year. Fed Governor Lael Brainard dialed back expectations yesterday, indicating that preemptive tightening has become less compelling given the persistently low inflation trend, slack in the labor market, and fragility in the global markets. The fed funds futures market currently estimates the odds of a September rate hike at 15.0% falling from 24.0% at the start of yesterday's session.

Biotechnology underperforms in the health care space (-1.8%), evidenced by the 2.6% loss in the iShares Nasdaq Biotechnology ETF (IBB 279.73, -7.38). The ETF is under pressure after rising 3.0% in the prior session. In the group, Vertex Pharmaceuticals (VRTX 93.80, -4.05) displays relative weakness after the company received a "Market Perform" designation from Raymond James.

The influential technology space (-0.9%) trades ahead of the benchmark index as top-weighted component Apple (AAPL 108.07, +2.63) outperforms. The Dow component has rallied 2.6% after T-Mobile (TMUS 44.76,- 1.17) and Sprint (S 6.50, -0.42) released bullish pre-order data for the iPhone 7. T-Mobile reported that pre-orders have surpassed all previous iPhone models while Sprint indicated that pre-orders are up more than 375.0% from the same three day period a year ago.

The Treasury curve has steepened in the first half of trade. The yield on the benchmark 10-yr note has risen eight basis points to 1.74% while the yield on the 2-yr note is higher by four basis points (0.81%). The move was aided by bearish commentary from Bill Miller, Chief Investment Officer of Legg Mason. Mr. Milled advocated shorting the 10-yr Treasury note at the 2016 Delivering Alpha Conference.

Today's economic data will be limited to the Treasury Budget for August, which will be released at 14:00 ET.

12:30 pm:

[BRIEFING.COM] The major averages hover above session lows as the S&P 500 (-1.5%) trades slightly behind the Dow Jones Industrial Average (-1.3%).

The countercyclical health care sector (-1.6%) trades behind the broader market as biotechnology underperforms. The iShares Nasdaq Biotechnology ETF (IBB 281.53, -5.58) has declined by 1.9%, pulling back from yesterday's 3.0% gain.

In the group, Vertex Pharmaceuticals (VRTX 95.08, -2.78) displays relative weakness after the company received a "Market Perform" designation from Raymond James. The biotechnology ETF has inched higher by 0.2% in September, which matches a 0.2% gain in the broader health care sector over that time.

Treasuries have accelerated their retreat in recent action, leading to steepening in the yield curve. The yield on the benchmark 10-yr note has risen six basis points to 1.72% while the yield on the 2-yr note is higher by three basis points (0.80%). On a related note, Bill Miller, Chief Investment Officer of Legg Mason, recently advocated shorting the 10-yr Treasury note. The comments were offered at the 2016 Delivering Alpha Conference.

12:00 pm:

[BRIEFING.COM] The broader market continues to float near its session low as the S&P 500 declines 1.6%.

The commodity-sensitive energy space (-2.8%) demonstrates relative weakness amid a downturn in crude oil futures. The energy component has declined 2.8% ($44.97/bbl; -$1.32) following a bearish reading of the International Energy Agency's monthly report. The IEA lowered its global demand growth outlook for 2016 and 2017. The agency sees global demand growth for 2016 coming in at 1.3 million barrels per day (prior: 1.4 million barrels) while 2017 demand growth is expected to come in at 1.2 million barrels per day (prior: 1.4 million barrels).

In the sector, oil field service names underperform with Baker Hughes (BHI 48.38, -1.32) and Halliburton (HAL 40.96, -1.44) falling 2.9% and 3.4%, respectively. Meanwhile, Dow component Chevron (CVX 100.02, -2.23) trades behind the price-weighted index.

The American Petroleum Institute is scheduled to release its weekly inventory report this evening. Separately, the Department of Energy is slated to release its more influential inventory report tomorrow at 10:30 ET.

11:30 am:

[BRIEFING.COM] The major averages have traded in sideways fashion as the S&P 500 (-1.4%) trails the Nasdaq Composite (-1.2%). Elsewhere, the domestically-oriented Russell 2000 (-1.7%) displays relative weakness.

The consumer discretionary space (-1.4%) trades in-line with the broader market while influential Netflix (NFLX 95.57, -3.48) underperforms. The stock has declined 3.6% after being downgraded to "Underperform" from "Neutral" at Macquarie. The firm cited increased competition and increasing content cost for the downgrade. Separately, Dow component Home Depot (HD 126.32, -2.27) shows a loss of 1.8%.

On the central bank front, Atlanta Federal Reserve President, and non-FOMC voter, Dennis Lockhart recently announced that he will be stepping down as President of the Atlanta Fed on February 28, 2017. Mr. Lockhart has been a centrist on the committee and the next Atlanta Fed chief is scheduled to become a voting member of the FOMC in 2017.

The Treasury curve has steepened in recent action as the long end of the curve underperforms. The yield on the 2-yr note is higher by two basis points (0.79%) while the yield on the 10-yr note has risen four basis points (1.70%).

11:00 am:

[BRIEFING.COM] The broader market trades near a recently-established session low as the S&P 500 declines 1.3%.

The heavily-weighted financial sector (-1.9%) has continued to pull back in recent action, extending its week-to-date loss to 0.8%. In the group, Wells Fargo (WFC 47.15, -1.39) underperforms among money center banks. The bank recently announced that it would eliminate sales goals associated with its retail banking division. The decision comes on the heels of last Thursday's settlement with the Consumer Financial Protection Bureau. Wells Fargo has declined 5.5% since announcing the settlement on August 8. This compares to a loss of 2.5% in the broader Financial Select Sector SPDR ETF (XLF 23.90, -0.41).

The broader sector is under pressure as participants continue to dial back rate hike expectations for the year. The fed funds futures markets indicates that the implied probability of a rate hike at the September meeting is 15.0%, falling from 24.0% at the start of the week.

Treasuries trade on a mostly lower note with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note is higher by one basis point (1.68%) while the yield on the 2-yr note is unchanged at 0.77%.

10:30 am: [BRIEFING.COM]

The dollar index was up +0.3% around the 95.37 level, weighing on the commodities complex overall

Commodities, as measured by the Bloomberg Commodity Index, were down -0.9% around the 83.32 level

Crude oil futures dropped below the $45.00/barrel handle of support after monthly IEA data revised FY16 & FY17 global oil demand growth est. downward

October crude oil futures were down $1.33 (-2.9%) around the $44.96/barrel level

Monthly IEA data highlights:

The IEA lowered global demand forecasts for FY16 by ~100k barrels per day for FY16 to +1.3 mln barrels a day. The IEA also lowered FY17 demand growth forecasts to +1.2 mln barrels per day, about 200k less than previous estimates.

Decline in oil demand in China and Europe were also cited by the IEA as factors influencing the updated forecast.

Saudi Arabia takes the top spot from US shale as the world's largest producer.

IEA estimated that the U.S. had shut in 460k barrels a day of production, while Saudi Arabia pumped out an extra 400k barrels a day.

OPEC producer United Arab Emirates increased oil production by 20k barrels per day to 3.09 mln barrels, its highest output level ever.

Data reminders:

API data will be released after the bell today

Weekly EIA data will be released tomorrow at 10:30 am ET

Rig count data will be released Friday at 1 pm ET

The next OPEC meeting will take place in Algiers, Algeria from Sept 26-28

Natural gas traded nearly flat in morning pit trading after yesterday's +4.3% surge

October natural gas futures were down $0.02 (-0.7%) around the $2.89/MMBtu level

Weekly EIA data will be released Thursday at 10:30 am ET

In precious metals, gold & silver snapped their 4-day losing streak, gold inched off 3-week lows hit yesterday despite a rally in the dollar index

December gold futures were up $2.30 (+0.2%) around the $1327.90/oz level

December silver futures were up $0.04 (+0.2%) around the $19.04/oz level

10:00 am:

[BRIEFING.COM] The broader market has notched a fresh session low as the S&P 500 declines 1.0%.

The leaderboard remains little changed with health care (-1.3%), financials (-1.5%), telecom services (-1.7%), and energy (-2.1%) leading to the downside. Conversely, technology (-0.3%) shows the narrowest loss.

In the health care space (-1.3%), biotechnology underperforms, evidenced by the 2.0% decline in the iShares Nasdaq Biotechnology ETF (IBB 281.41, -5.70). In the ETF, Vertex Pharmaceuticals (VRTX 95.08, -2.78) trades lower by 2.9% after Raymond James initiated coverage on the name, issuing a Market Perform designation. The broader sector has gained 0.2% week-to-date, which compares to an uptick of 0.4% in the benchmark index.

The U.S. Dollar Index (95.40, +0.31, +0.32%) floats above its flat line as the buck holds gains against the yen and pound. The dollar has gained 0.4% against the safe-haven yen (102.26) while the pound has declined 1.0% against the greenback (1.3200). Separately, the dollar has jumped 0.9% against the commodity-sensitive Canadian dollar (1.3159).

9:45 am:

[BRIEFING.COM] The stock market opened on a lower note as the S&P 500 (-0.7%) and the Dow Jones Industrial Average (-0.7%) each trail the tech-heavy Nasdaq (-0.4%).

Nine sectors trade in the red with telecom services (-1.4%) and energy (-1.4%) leading to the downside. The remaining decliners sport losses between 0.4% (utilities) and 1.1% (financials). On the flipside, the technology (UNCH) sector trades narrowly in the green.

The influential technology space (UNCH) trades ahead of the broader market as top-weighted component Apple (AAPL 108.47, +3.02) outperforms. The name has jumped 2.9% after T-Mobile (TMUS 45.48, -0.45) and Sprint (S 6.85, -0.07) each reported bullish pre-order data for the iPhone 7.

In the financial sector (-1.1%), life insurance names underperform as MetLife (MET 43.66, -0.63) and Prudential (PRU 78.70, -1.04) trade lower by 1.1% and 1.3%, respectively. The broader sector has extended its month-to-date loss to 2.2%, leading only materials (-0.9%; month-to-date: -2.5%) over that time.

On the commodities front, WTI crude trades lower by 1.5% ($45.58/bbl; -$0.71) while gold has ticked higher by 0.3% to $1,329.50/ozt.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: -16.70. Nasdaq futures vs fair value: -25.90.

The stock market is on track for a lower open as the S&P 500 futures trade 17 points below fair value.

Index futures were unable to gain traction overnight, sliding lockstep with crude oil. The energy component was under pressure after the International Energy Agency lowered its global demand growth estimates for 2016 and 2017. The IEA sees demand at 1.3 million barrels per day in 2016, falling approximately 100,000 barrels per day from the previous estimate. Separately, the global demand estimate for 2017 fell to 1.2 million barrels per day (from 1.4 million). The somewhat bearish outlook has called into question existing timelines for a potential rebalancing in the oil market. At this juncture, WTI crude trades lower by 2.1% ($45.32/bbl; -$0.97).

The U.S. Dollar Index (95.45, +0.34, +0.37%) has also acted as a headwind for the dollar-denominated commodity. The index is rebounding after falling 0.3% yesterday. The greenback was under pressure following dovish commentary from Fed Governor Lael Brainard. Governor Brainard stated that the case for preemptive tightening is less compelling given the persistently low inflation trend, continued slack in the labor market, and fragility in the global markets. Participants dialed back rate hike expectations in response. The fed funds futures market currently estimates the odds of a September rate hike at 15.0% falling from 24.0% at the start of yesterday's session.

On the corporate front, Anadarko Petroleum (APC 56.15, -1.64) has declined by 2.8% in pre-market action after announcing a public offering of 35.25 million shares. The independent oil and gas name also announced that it would acquire deep water assets in the Gulf of Mexico from Freeport McMoRan (FCX 10.75, -0.33). Anadarko Petroleum will pay $2.00 billion for the assets.

Today's economic data will be limited to the Treasury Budget for August, which will be released at 14:00 ET.

8:57 am: [BRIEFING.COM] S&P futures vs fair value: -16.50. Nasdaq futures vs fair value: -26.40.

Equity futures trade at fresh session lows as the S&P 500 futures trade 17 points below fair value.

Equity indices across Asia ended Tuesday on a mixed note with Japan's Nikkei (+0.3%) showing relative strength. The yen (102.27) climbed at the start of the overnight session, but a subsequent reversal has the currency down 0.4% against the dollar. Overnight headlines indicate the Bank of Japan is looking to change or do away with maturity limits on JGB purchases. Separately, data from China surprised to the upside.

In economic data:

China's August Retail Sales +10.6% year-over-year (consensus 10.3%; last 10.2%), August Industrial Production +6.3% year-over-year (expected 6.1%; last 6.0%), and August Fixed Asset Investment +8.1% year-over-year (consensus 8.0%; previous 8.1%)

Australia's NAB Business Confidence ticked up to 6 from 4 and NAB Business Survey ticked down to 7 from 8

New Zealand's August FPI +1.3% month-over-month (last -0.2%)

South Korea's August Unemployment Rate held at 3.6%, as expected. August Import Price Index -8.5% year-over-year and Export Price Index -9.7% year-over-year (last -7.4%)

---Equity Markets---

Japan's Nikkei added 0.3% with seven sectors posting gains. Health care (+1.2%), consumer staples (+0.6%), and industrials (+0.5%) outperformed while financials (-1.4%) and utilities (-0.8%) lagged. JGC, Kubota, Shiongi, Suzuki Motor, Sony, Fanuc, and Bridgestone gained between 1.3% and 2.1%.

Hong Kong's Hang Seng shed 0.3% with property names and select financials showing weakness. China Resources Land, Hang Lung Properties, Cheung Kong Properties, Bank of China, and Ping An Insurance lost between 0.8% and 1.9%. Want Want China was the top performer, climbing 1.9%.

China's Shanghai Composite settled just above its flat line. Routon Electronic, Shenzhen Geoway, Keda Group, and China Security & Fire gained between 7.0% and 8.0%.

Major European indices trade near their flat lines with Germany's DAX (+0.3%) showing relative strength. Demand for Germany's 10-yr bund has driven its yield back down to 0.02% after briefly creeping above 0.05% yesterday. The euro (1.1235) is little changed against the dollar while the pound has slid 0.8% to 1.3226.

In economic data:

Eurozone September ZEW Economic Sentiment 5.4 (expected 6.7; previous 4.6) and Q2 Employment Change +1.4% year-over-year, as expected (previous 1.4%)

Germany's September ZEW Economic Sentiment 0.5 (expected 2.5; last 0.5) and ZEW Current Conditions 55.1 (expected 56.0; last 57.6). August CPI 0.0% month-over-month, as expected (last 0.0%); +0.4% year-over-year, as expected (last 0.4%). August WPI -0.7% month-over-month (expected 0.1%; last 0.2%)

UK's August CPI +0.3% month-over-month (expected 0.4%; last -0.1%); +0.6% year-over-year (consensus 0.7%; last 0.6%). Core CPI +1.3% year-over-year (consensus 1.4%; last 1.3%) and Input PPI +0.2% month-over-month (expected 0.6%; last 3.1%). House Price Index +8.3% year-over-year (expected 8.5%; last 8.7%)

Italy's July Industrial Production +0.4% month-over-month (expected 0.2%; last -0.3%); -0.3% year-over-year (consensus -1.0%; last -0.9%)

Swiss August PPI -0.3% month-over-month (expected -0.2%; last -0.1%); -0.4% year-over-year (consensus -0.3%; last -0.8%)

---Equity Markets---

France's CAC is lower by 0.1%. Air Liquide has jumped 4.6% while other growth-sensitive names like Lafarge, Schneider Electric, Peugeot, and Essilor International are up between 0.5% and 2.0%. Financials are mixed with Credit Agricole down 0.2%, BNP Paribas flat, and Societe Generale adding 0.3%.

UK's FTSE trades up 0.1% amid strength in consumer and health care names. Burberry, Carnival, Coca Cola HBC, Shire, Hikma Pharmaceuticals, and GlaxoSmithKline display gains between 1.3% and 2.1%.

Germany's DAX has added 0.3%. Infineon, Linde, and Adidas are up between 2.2% and 2.5% while exporters BMW, Volkswagen, and Daimler have gained between 0.5% and 0.8%. Financials trade in mixed fashion with Deutsche Bank adding 0.4% while Commerzbank is down 0.5% and Deutsche Boerse retreats 1.1%.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: -13.70. Nasdaq futures vs fair value: -22.10.

Equity futures trade little changed since the last update with S&P 500 futures floating 14 points below fair value.

In company specific news, Blue Buffalo (BUFF 24.67, -1.42) trades lower by 5.4% after filing for a 14.3 million share common stock offering for a selling stakeholder. Chesapeake Energy (CHK 7.93, -0.12) has declined 1.5% after the name received an "Underperform" designation at FBR Capital. Dow component Chevron (CVX 101.84, -0.41) has ticked lower by 0.4% despite BMO Capital issuing an "Outperform" rating on the stock. To be fair though, the energy sector has been under pressure amid a downturn in crude oil futures. WTI crude trades lower by 2.3% ($45.20/bbl; -$1.09).

The U.S. Dollar Index (95.23, +0.14, +0.15%) trades off its best level as the euro erases its loss against the greenback. The euro has gained 0.1% against the buck (1.1248) after moving off the 1.1220 price level overnight. Separately, the dollar/yen pair trades higher by 0.4% (102.27) while sterling has declined 0.6% against the dollar (1.3251).

8:05 am: [BRIEFING.COM] S&P futures vs fair value: -13.70. Nasdaq futures vs fair value: -19.90.

U.S. equity futures trade on a lower note with the S&P 500 futures floating 14 points below fair value. A downturn in crude oil weighs on index futures as participants respond to a bearish reading of the International Energy Agency's monthly report. Specifically, the report featured a negative revision for demand growth in 2016 and 2017. Global demand forecasts for full-year 2016 fell by nearly 100,000 barrels per day to 1.3 million barrels. Forecasts for global demand growth in 2017 came in at 1.2 million barrels per day, falling 200,000 barrels from the previous estimate. At this juncture, WTI crude trades lower by 2.2% ($45.28/bbl; -$1.01).

Global bourses trade on a flat note, shrugging off yesterday's strong performance from U.S. equity markets. European bourses lead the advance as sovereign bonds rebound. The yield on the 10-yr bund has slipped three basis points to 0.01%. Meanwhile, China's Shanghai Composite (+0.1%) finished little changed despite stronger-than-expected readings of China's August Retail Sales (+10.6% year-over-year; consensus: 10.3%), August Industrial Production (+6.3% year-over-year; expected: 6.1%), and August Fixed Asset Investment (+8.1% year-over-year; consensus 8.0%).

Treasuries trade on a mixed note with the long end of the curve demonstrating relative strength. The yield on the 2-yr note is unchanged (0.77%) while the yield on the benchmark 10-yr note is lower by one basis point (1.66%).

Today's data will be limited to the Treasury Budget for August, which will be released at 14:00 ET.

In U.S. corporate news of note:

Intersil (ISIL 21.50, +1.74): +8.8% after announcing that the company would be acquired by Renesas Electronics (RNECF 5.65, 0.00) for $22.50 per share or approximately $3.2 billion

Netflix (NFLX 97.39, -1.66): -1.7% following the stock being downgraded to "Underperform" from "Neutral" at Macquarie

Anadarko Petroleum (APC 55.50, -2.29): -4.0% after pricing an offering of 35.25 million shares of common stock

Western Digital (WDC 52.58, +0.27): +0.5% following the stock being upgraded to "Buy" from "Neutral" at Longbow

Reviewing overnight developments:

Asia-Pacific indices ended Tuesday on a mixed note with Japan's Nikkei (+0.3%) leading China's Shanghai Composite (+0.1%), and Hong Kong's Hang Seng (-0.3%).

In economic data:

China's August Retail Sales +10.6% year-over-year (consensus 10.3%; last 10.2%), August Industrial Production +6.3% year-over-year (expected 6.1%; last 6.0%), and August Fixed Asset Investment +8.1% year-over-year (consensus 8.0%; previous 8.1%)

Australia's NAB Business Confidence ticked up to 6 from 4 and NAB Business Survey ticked down to 7 from 8

New Zealand's August FPI +1.3% month-over-month (last -0.2%)

South Korea's August Unemployment Rate held at 3.6%, as expected. August Import Price Index -8.5% year-over-year and Export Price Index -9.7% year-over-year (last -7.4%)

In news:

The yen (102.28) climbed at the start of the overnight session, but a subsequent reversal has the currency down 0.4% against the dollar.

Bank of Japan is looking to change or do away with maturity limits on JGB purchases.

Meanwhile, data from China surprised to the upside.

European indices trade on a flat note with Germany's DAX (+0.5%) leading the U.K.'s FTSE (+0.2%) and France's CAC (+0.1%).

In economic data:

Eurozone September ZEW Economic Sentiment 5.4 (expected 6.7; previous 4.6) and Q2 Employment Change +1.4% year-over-year, as expected (previous 1.4%)

Germany's September ZEW Economic Sentiment 0.5 (expected 2.5; last 0.5) and ZEW Current Conditions 55.1 (expected 56.0; last 57.6). August CPI 0.0% month-over-month, as expected (last 0.0%); +0.4% year-over-year, as expected (last 0.4%). August WPI -0.7% month-over-month (expected 0.1%; last 0.2%)

UK's August CPI +0.3% month-over-month (expected 0.4%; last -0.1%); +0.6% year-over-year (consensus 0.7%; last 0.6%). Core CPI +1.3% year-over-year (consensus 1.4%; last 1.3%) and Input PPI +0.2% month-over-month (expected 0.6%; last 3.1%). House Price Index +8.3% year-over-year (expected 8.5%; last 8.7%)

Italy's July Industrial Production +0.4% month-over-month (expected 0.2%; last -0.3%); -0.3% year-over-year (consensus -1.0%; last -0.9%)

Swiss August PPI -0.3% month-over-month (expected -0.2%; last -0.1%); -0.4% year-over-year (consensus -0.3%; last -0.8%)

In news:

Demand for Germany's 10-yr bund has driven its yield back down to 0.01% after briefly creeping above 0.05% yesterday.

The euro (1.1237) is little changed against the dollar while the pound has slid 0.6% to 1.3255.

6:23 am: [BRIEFING.COM] S&P futures vs fair value: -12.50. Nasdaq futures vs fair value: -24.00.

6:23 am: [BRIEFING.COM] Nikkei...16,729.04...+56.10...+0.30%. Hang Seng...23,215.76...-74.80...-0.30%.

6:23 am: [BRIEFING.COM] FTSE...6,705.41...+4.50...+0.10%. DAX...10,470.89...+39.00...+0.40%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

TheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com