Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htmBusiness Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

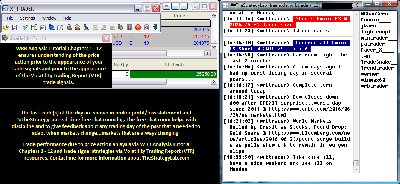

Attachment:

062416-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+25250.00.png [ 93.51 KiB | Viewed 435 times ]

062416-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+25250.00.png [ 93.51 KiB | Viewed 435 times ]

click on the above image to view today's performance verification Quote:

A few days ago I had my biggest losing trading day in many years due to unfamiliar and strange price action reacting to BREXIT. In contrast, today I had my biggest profitable trading day due to the same reasons but I needed to adapt (make some changes). Contact me if you want to know what the difference was between the two trading days while both trading days was under the market context of BREXIT if you're unable to determine it from the chat logs. Also, my WRB Analysis statistics showed an unusual high percentage price reaction to WRB Hidden GAP intervals soon after the formation of the WRB Hidden GAP intervals that I can only attribute to algorithms footprint.

Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

25,250.00 dollars or +505.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $25,250.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. Also, the free chat room is

not a signal calling chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=157&t=2394 The free chat room is

not a signal calling chat room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of the free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use the free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. The free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I keep the peace between members and I keep out the trouble makers so that members can peacefully post their observations about the markets, trades and WRB Analysis commentary.

Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=294&t=3166 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

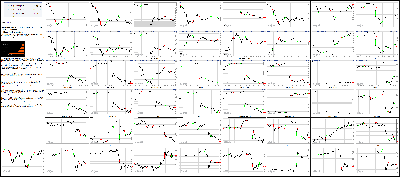

Attachment:

062416-Key-Price-Action-Markets.png [ 1016.78 KiB | Viewed 374 times ]

062416-Key-Price-Action-Markets.png [ 1016.78 KiB | Viewed 374 times ]

click on the above image to view today's price action of key markets 4:15 pm: [BRIEFING.COM] The major averages ended a tumultuous session on a sharply lower note, selling off after the United Kingdom surprised markets by voting to leave the European Union. The move had widespread implications throughout capital markets as the S&P 500 (-3.4%) tumbled 75 points, losing the most points since September 1, 2015. Today's trade featured a flight from risk assets, a bid in safe havens, and the underperformance of the heavily-weighted financial (-5.4%), technology (-4.3%), industrial (-4.0%), and consumer discretionary (-3.6%) sectors. The Nasdaq Composite (-4.1%) ended its day behind the S&P 500 (-3.6%) and the Dow Jones Industrial Average (-3.4%).

Global equity markets tumbled overnight as participants reacted to a surprise result from yesterday's Brexit vote. The "Leave" camp carried the referendum after receiving 51.9% of last night's vote. In response, European indices paced the retreat as investors looked ahead to the multi-year legal process of withdrawing the UK from the EU. Additionally, foreign exchange markets were in focus as the pound sank to a three-decade low (1.3231) against the dollar.

The major U.S. averages gapped lower at the beginning of the session as the heavyweight financial (-5.4%), technology (-4.3%), and industrial (-4.0%) sectors dragged on the broader market. To be fair though, all six cyclical sectors experienced heavy selling pressure as a flight from risk assets resulted in losses between 3.5% (energy) and 5.4% (financials). A downturn in crude oil added to the negative tenor as a rally in the buck weighed on the dollar-denominated commodity. For its part, WTI crude ended its pit session lower by 5.0% ($47.60/bbl; -$2.52). The S&P 500 (-3.6%) ended off its worst level of the day, but below prior technical support at the 2050 price level.

The economically-sensitive financial sector (-5.4%) moved lower in sympathy with European banking names as Deutsche Bank (DB 14.72, -3.12) experienced its largest daily point loss since 2008. Elsewhere, Lloyds Banking (LYG 3.33, -1.01) and Royal Bank of Scotland (RBS 5.43, -2.06) lost 23.3% and 27.5%, respectively. On the home front, Dow component Goldman Sachs (GS 141.86, -10.80) ended its day at the bottom of the price-weighted index. The broader sector fell 5.4% today, extending its yearly loss to 7.4%.

The high-beta chipmakers demonstrated relative weakness, evidenced by the 5.8% decline in the PHLX Semiconductor Index. The growth-sensitive group experienced pressure as Skyworks (SWKS 61.61, -5.60) plunged 8.3%. In the broader technology sector (-4.3%), large cap component Microsoft (MSFT 49.86, -2.05) fell 4.0%.

In the consumer discretionary space (-3.6%), retail names ended ahead of the broader sector as the SPDR S&P Retail ETF (XRT 41.10, -0.90) declined 2.1%. On the flipside, PVH (PVH 93.55, 9.19) fell 8.9% after the company reported that net revenue generated from inside the United Kingdom constituted 3.0% of its total net revenues. Separately, travel names weighed as large cap component Priceline (PCLN 1232.14) fell 11.4%.

The U.S. Dollar Index (95.48, +1.95) ended broadly higher as the euro and the pound finished with substantial losses against the buck. The euro/dollar pair declined 2.4% (1.1111) while sterling plunged 8.1% against the dollar (1.3676).

The Treasury complex settled off its session high as the yield on the 10-yr note finished lower by 17 basis points at 1.57%.

Today's participation was above the recent average as more than 1.1 billion shares changed hands on the NYSE floor. The Russell 2000 (-3.7%) likely contributed to the increased volume ahead of this evening's annual rebalancing.

Today's economic data was limited to Durable Orders for May and the final reading of Michigan Consumer Sentiment for May:

The advance report on durable goods disappointed as new orders declined 2.2% month-over-month (Briefing.com consensus -0.6%) while orders excluding transportation declined 0.3% (Briefing.com consensus +0.1%).

The disappointment is deep-seated for several reasons.

First, orders declined in almost every category.

Secondly, business investment continued to flag, evidenced by a 0.7% decline in new orders for nondefense capital goods excluding aircraft, which followed a 0.4% decline in April.

Third, shipments of nondefense capital goods excluding aircraft, which factor into the GDP report, were down 0.5%, reversing most of a 0.6% increase in April.

On a year-over-year basis, new orders excluding transportation are down 0.5% while orders for nondefense capital goods excluding aircraft are down 3.5%.

The decline in May featured a 34.1% drop in orders for defense aircraft and parts. Overall, though, new orders for transportation equipment declined 5.6%, led by a 2.8% drop in orders for motor vehicles and parts.

Some other prominent order declines were seen in primary metals (-1.4% after a 0.7% decline in April), fabricated metal products (-0.3% after a 3.6% increase in April), machinery (-0.2% after a 2.0% decline in April), electrical equipment, appliances, and components (-0.1% after a 0.2% decline in April).

The final reading for the University of Michigan Consumer Sentiment Survey revealed a dip to 93.5 from the preliminary reading of 94.3. The Briefing.com consensus estimate was pegged at 94.0.

The final reading for June was below the final reading of 94.7 for May and below the 96.1 reading seen for June 2015.

It was said in the release that consumers were a bit less optimistic in late June due to rising concerns about prospects for the U.S. economy.

Those concerns showed up in the Index of Consumer Expectations, which slipped to 82.4 from 84.9 in May.

The Current Economic Conditions Index actually ticked up to 110.8 from 109.9. That is the highest reading for this index since January 2007.

Separately, consumers' inflation expectations for the next 12 months were left unchanged at 2.4%.

Monday's economic data will be limited to the International Trade in Goods Report for May, which will be released at 8:30 ET.

Week in Review: Brexit Spoils Bull Party

The stock market gallivanted higher though the first fourdays of the week, but the upbeat attitude dissipated on Thursday evening afterit became clear that the British referendum on membership in the European Unionended with a 51.9% victory for the 'Leave' camp. The resulting Fridayselloff sent the S&P 500 lower by 3.6%. The index slid below its 50-daymoving average (2080), surrendering 1.6% for the week.

Although the weekly decline in the S&P 500 did not lookparticularly concerning, the moves that unfolded in the foreign exchange marketcaught the attention of many.

The final set of polls released ahead of the referendumpointed to a growing edge for the 'Remain' camp, which lulled some marketparticipants into a false sense of security. The pound notched a freshsix-month high against the dollar at 1.5018, but reversed in a flash afteractual results began pouring in.

The first signs of an impending reversal in the foreignexchange market began appearing around 18:00 ET on Thursday when the pound startedbacking away from its high. This took place after it was reported that the 'Remain'camp secured just a slight victory in Newcastle, where status quo was expectedto prevail by a large margin. Subsequent vote counts hinted at a much closerresult than it was first expected, which invited risk-off positioning into capitalmarkets.

At its lowest point, the pound was down nearly 11.0% againstthe dollar, but that decline was narrowed to 8.0% by the end of Friday. The volatilityleft the pound down more than 1,000 pips versus the dollar for the day, which isa move that would be expected to unfold over a few weeks under typicalconditions.

U.S. Treasuries surged in reaction to the developments, pressuringthe 10-yr yield to 1.40%--its lowest level since mid-2012.

The defensive finish to the week weighed on rate hikeexpectations, and the fed funds futures market now sees a higher chance of a ratecut in July (7.2%), September (7.2%), or November (7.0%) than that of a hike inNovember (1.9%). Looking farther out, the likelihood of a hike in February 2017sits at a lowly 22.3%.

3:30 pm: [BRIEFING.COM]

The dollar index holds onto this mornings surge, up +2% around the 95.43 level, putting downward pressure on commodities

Commodities, as measured by the Bloomberg Commodity Index, are down -1.6% at the 86.97 level

Crude oil plummets well below the $50/barrel handle support as the dollar gains momentum post-Brexit

August crude Oil futures fell $2.52 (-5.0%) to $47.60/barrel

Baker Hughes total U.S. rig count down 3 to 421 following last week's increase of 10

Monthly IEA data is scheduled to be released on July 13

Natural gas futures give up all of the previous session's gains and more as the dollar rallies after the UK voted to leave the EU

August natural gas closed $0.05 lower (-1.8%) at $2.69/MMBtu

Natural gas futures have changed their front month to August from July based on the active amount of volume of the contracts

In precious metals, gold breaks above $1300/oz resistance level, closing near fresh highs of 2016

August gold ended today's session up $59.40 (+4.7%) to $1322.50/oz

Silver moves in tandem with gold, opening notably higher and holding onto its gains into the close

July silver closed today's session $0.43 higher (+2.5%) at $17.78/oz

Base metal copper falls sharply in afternoon pit trading

July copper closed $0.05 lower (-2.3%) at $2.11/lb

3:00 pm:

[BRIEFING.COM] The major indices hover above new session lows as the Nasdaq Composite (-3.9%) trails the S&P 500 (-3.2%) and the Dow Jones Industrial Average (-3.1%). The move lower corresponded with the benchmark index violating technical support near the 2050 price level and oil ending its pit session with a 5.0% decline ($47.60/bbl; -$2.52).

Nine sectors trade in the red with economically-sensitive financials (-5.1%) trailing materials (-4.3%), technology (-4.0%), and industrials (-3.8%). Conversely, countercyclical sectors outperform with health care (-2.6%), consumer staples (-1.5%), telecom services (-0.6%), and utilities (+0.2%) leading.

In the consumer discretionary space (-3.6%), retailers trade ahead of the broader sector, evidenced by the 2.1% decline in the SPDR S&P Retail ETF (XRT 41.10, -0.90). In the group, Finish Line (FINL 20.54, +3.75) has surged 22.4% after reporting above-consensus results for the quarter. Conversely, PVH (PVH 93.98, -8.76) has stumbled 8.5% after reporting that 3.0% of its total net revenues are generated inside the United Kingdom.

The U.S. Dollar Index (95.40, +1.87) has drifted higher in recent action as the euro and commodity currencies lose ground to the greenback. The euro/dollar pair trades lower by 2.3% (1.1119) after slipping from the 1.1180 price level. Separately, the dollar has gained 1.4% against the Canadian dollar (1.2959).

2:30 pm:

[BRIEFING.COM] The major averages have ticked lower since our last update as the S&P 500 (-3.2%) violates technical support near the 2050 price level.

The energy (-3.2%) sector trades in-line with the broader market, succumbing to today's risk-off posture. Furthermore, oil has been pressured as a rebound in the greenback weighs on dollar-denominated commodities. Currently, WTI crude trades lower by 5.1% ($47.59/bbl; -$2.52) ahead of its pit session close at 14:30 ET.

In the sector, independent oil and gas names underperform as the group faces steeper downside risks from a prolonged downturn in crude oil. On the flipside, Dow components Chevron (CVX 102.35, -2.10) and Exxon Mobil (XOM 89.74, -2.06) show slimmer losses, trading ahead of the price-weighted index.

The U.S. Dollar Index (95.19, +1.67) has floated higher in recent action as the pound extends its loss against the greenback. Sterling trades lower by 7.9% against the dollar (1.3696).

The Treasury complex continues to back away from its high as equities float near their recent levels. The yield on the 10-yr note has slipped 16 basis points to 1.58%

2:00 pm:

[BRIEFING.COM] The S&P 500 (-2.8%) trades seven points off its worst level of the day, climbing back above the key 2050 price level. For the week, the benchmark index shows a loss of 0.9%.

In the front of the pack, countercyclical utilities (+0.9%), telecom services (+0.4%), and consumer staples (-1.1%) outperform.

In the consumer staples space (-1.1%), U.S. tobacco names demonstrate relative strength as Reynolds American (RAI 51.90, +1.06) and Altria (MO 67.86, +1.55) jump 2.1% and 2.4%, respectively. Conversely, Philip Morris International (PM 98.73, -3.17) underperforms as investors weigh the overseas exposure of some of its brands. Food names also lead in the sector as Tyson Foods (TSN 63.91, +0.55) and Hormel (HRL 35.34, +0.75) gain a respective 0.8% and 2.2%. The broader sector trades neck-and-neck with energy (-2.8%; week-to-date: +0.1%) on the weekly leaderboard. The two groups trail only utilities (+0.9%; week-to-date: +0.5%) and telecom services (-0.4%; week-to-date: +1.9%) over that time.

On the commodities front, gold ended its pit session higher by 4.7% ($1,322.50/ozt; +$59.40), extending its monthly gain to 8.6%.

1:35 pm:

[BRIEFING.COM] The major U.S. indices continue to trade under significant pressure following the shock EU referendum vote, with the Dow Jones Industrial Average down 2.9%.

A look inside the Dow shows that Goldman Sachs (GS 143.01, -9.65), JPMorgan (JPM 60.20, -3.85), and Caterpillar (CAT 73.56, -4.66) are underperforming. Following the surprising support for Britain to leave the EU, JPMorgan and Goldman are leading the Dow lower as the entire financial sector slumps on implications the decision could have on the industry.

Conversely, Wal-Mart (WMT 72.29, +0.19) is the Dow's best performing, and lone component in positive territory.

With global equities in free-fall today, the DJIA has now dropped into negative territory for June, currently down 1.6% this month.

1:10 pm:

[BRIEFING.COM] The stock market trades on a broadly lower note at midday, responding to Britain's surprising decision to leave the European Union. The move has reverberated through capital markets, pressuring risk assets and prompting a flight to safe havens. The extent of the downturn has been accentuated by weakness from the heavily-weighted financial (-4.7%), technology (-3.7%), industrial (-3.4%), and consumer discretionary (-3.3%) sectors. At midday, the Nasdaq Composite (-3.7%) trades behind the S&P 500 (-3.1%) and the Dow Jones Industrial Average (-2.9%).

European indices led the retreat overnight as participants weighed the potential implications a Brexit holds for the United Kingdom, the European Union, and global financial markets. The country surprised investors overnight when the "Leave" camp received 51.9% of yesterday's vote. Immediate repercussions for the decision were seen in the foreign exchange market as the pound tumbled to a level it last traded at in 1985 (1.3231). However, equity markets also experienced heavy selling pressure as Germany's DAX and France's CAC lost 6.8% and 8.0%, respectively.

The major U.S. averages opened under heavy selling pressure as heavyweight financials (-4.7%) and technology (-3.7%) weighed on the broader market. Furthermore, a downturn in crude oil also contributed to the negative bias. The S&P 500 (-3.1%) floated above its opening level throughout the morning. However, the benchmark index recently slipped to a new low after testing and violating technical support at the 2050 price level. At this juncture, nine sectors trade in the red with heavily-weighted financials (-4.7%), materials (-3.9%), technology (-3.7%), and industrials (-3.4%) rounding out the leaderboard.

The economically-sensitive financial sector (-4.7%) demonstrates broad-based weakness as the sector moves lower with European banking names. On that note, Deutsche Bank (DB 14.95, -2.88) trades lower by 16.2%, experiencing its largest daily point loss since 2008. In the sector, Dow component Goldman Sachs (GS 143.04, -9.62) has sunk 6.3%, rounding out the price-weighted index. The broader sector has extended its monthly decline to 6.1%, trailing the remaining groups over that time.

In the technology space (-3.7%), Dow components Microsoft (MSFT 49.87, -2.04) and IBM (IBM 148.15, -7.20) underperform, sliding 4.0% and 4.7%, respectively. Elsewhere, the high-beta chipmakers remain pressured, evidenced by the 5.0% decline in the PHLX Semiconductor Index. The index erased a weekly gain of 3.8% and currently shows a loss of 1.2% over that time.

The Dow Jones Transportation Average (-4.0%) trades behind the benchmark index as airline names lag. On that note, the U.S. Global Jets ETF (JETS 20.96, -1.13) has lost 5.1%. In the broader industrial sector, Boeing (BA 127.03, -6.52) underperforms, losing 5.0%.

Travel and leisure names weigh on the consumer discretionary space (-3.3%) as large cap component Priceline (PCLN 1237.00, -1.53) falls 11.0%. Conversely, fast food names outperform as McDonald's (MCD 119.67, -1.54) trades ahead of the broader sector and index.

The U.S. Dollar Index (95.17, +1.65) trades broadly higher as commodity currencies, the euro, and the pound lose ground to the greenback. The single currency has lost 2.0% against the buck (1.1158) while the pound has plunged 7.8% against the dollar (1.3713). Elsewhere, the dollar has lost 3.7% against the yen (102.23).

The Treasury complex trades off its session high as the yield on the 10-yr note remains lower by 17 basis points at 1.57%.

Today's economic data was limited to Durable Orders for May and the final reading of Michigan Consumer Sentiment for May:

The advance report on durable goods disappointed as new orders declined 2.2% month-over-month (Briefing.com consensus -0.6%) while orders excluding transportation declined 0.3% (Briefing.com consensus +0.1%).

The disappointment is deep-seated for several reasons.

First, orders declined in almost every category.

Secondly, business investment continued to flag, evidenced by a 0.7% decline in new orders for nondefense capital goods excluding aircraft, which followed a 0.4% decline in April.

Third, shipments of nondefense capital goods excluding aircraft, which factor into the GDP report, were down 0.5%, reversing most of a 0.6% increase in April.

On a year-over-year basis, new orders excluding transportation are down 0.5% while orders for nondefense capital goods excluding aircraft are down 3.5%.

The decline in May featured a 34.1% drop in orders for defense aircraft and parts. Overall, though, new orders for transportation equipment declined 5.6%, led by a 2.8% drop in orders for motor vehicles and parts.

Some other prominent order declines were seen in primary metals (-1.4% after a 0.7% decline in April), fabricated metal products (-0.3% after a 3.6% increase in April), machinery (-0.2% after a 2.0% decline in April), electrical equipment, appliances, and components (-0.1% after a 0.2% decline in April).

The final reading for the University of Michigan Consumer Sentiment Survey revealed a dip to 93.5 from the preliminary reading of 94.3. The Briefing.com consensus estimate was pegged at 94.0.

The final reading for June was below the final reading of 94.7 for May and below the 96.1 reading seen for June 2015.

It was said in the release that consumers were a bit less optimistic in late June due to rising concerns about prospects for the U.S. economy.

Those concerns showed up in the Index of Consumer Expectations, which slipped to 82.4 from 84.9 in May.

The Current Economic Conditions Index actually ticked up to 110.8 from 109.9. That is the highest reading for this index since January 2007.

Separately, consumers' inflation expectations for the next 12 months were left unchanged at 2.4%.

12:30 pm:

[BRIEFING.COM] The S&P 500 (-2.8%) has inched off a new low, testing support near the 2050 price level. Elsewhere, the Nasdaq Composite (-3.4%) paces the retreat amid weakness in technology and biotechnology.

In front of the pack, utilities (+0.5%) sport the only gain while countercyclical telecom services (-0.7%) show the slimmest loss. However, telecom services lead the remaining sectors on a weekly (+1.7%), monthly (+6.1%), and yearly (+18.2%) basis. Safe-haven gold has ticked up as equities hover near their respective lows. The precious metal has gained 4.7% ($1322.00/ozt, +$58.90), extending its June advance to 8.6%.

The U.S. Dollar Index (95.32, +1.79) continues to trade broadly higher as commodity currencies, the euro, and the pound lose ground to the greenback. The single currency has lost 2.3% against the buck (1.1123) while the pound has plunged 8.8% against the dollar (1.3585). Elsewhere, the dollar has lost 3.7% against the yen (102.28), sliding 7.6% since its May settlement at 110.71. For the week, the Dollar Index shows a gain of 1.0%.

12:00 pm:

[BRIEFING.COM] The S&P 500 (-2.7%) hovers five points off its worst level of the day, trading lower by 0.7% on a weekly basis. Separately, the domestically-oriented Russell 2000 has declined by 3.0% ahead of this evening's annual rebalancing.

The high-beta chipmakers demonstrate relative weakness, evidenced by the 4.1% decline in the PHLX Semiconductor Index. In the group, Skyworks (SWKS 63.15, -4.06) underperforms, losing 6.0%. The broader price-weighted index erased a monthly gain of 3.9% and is now down 0.2% since last Friday.

In the technology space (-3.2%), Dow components Microsoft (MSFT 50.04, -1.87) and IBM (IBM 147.84, -7.51) underperform. On the flipside, Facebook (FB 113.35, -1.73) and Apple (AAPL 94.11, -1.99) trade ahead of the broader sector, but still sport respective losses of 1.5% and 2.1%.

The CBOE Volatility Index (22.22, +4.97) has gained 28.8% today, responding to added volatility following yesterday's Brexit decision and the end of the quarter. For the week, the near-term volatility barometer has gained 14.5%.

11:30 am:

[BRIEFING.COM] The major averages have notched fresh session lows with the Nasdaq Composite (-3.12) and the S&P 500 (-2.7%) trading behind the Dow Jones Industrial Average (-2.6%). The leg lower in equities corresponded with a downtick in the pound and the close of trade in Europe.

The leaderboard remains little changed as financials (-4.2%) trade behind materials (-3.4%), technology (-3.2%), and industrials (-3.1%).

In the consumer discretionary space (-2.9%) travel and leisure names underperform as TripAdvisor (TRIP 62.59, -3.39) and Expedia (EXPE 103.30, -6.58) show losses of 4.5% and 5.9%, respectively. Elsewhere, cruise ship operators are pressured with Carnival (CCL 46.53, -2.83) losing 5.8%. Conversely, fast casual restaurant names outperform as Dow component McDonald's (MCD 120.43, -0.77) trades ahead of the broader sector and the price-weighted index.

On the commodities front, WTI crude trades lower by 4.1% ($48.06/bbl; -$2.07) while gold trades off its session high ($1,362.45), remaining higher by 4.3% ($1,317.60/ozt; +$54.50).

11:00 am:

[BRIEFING.COM] The S&P 500 (-2.3%) has traded sideways since our last update as the index floats nine points off its worst level of the day. For the week, the benchmark index shows a loss of 0.4%.

The economically-sensitive financial sector (-3.9%) demonstrates broad-based weakness, responding to a downturn in European banking names, global equities, and sovereign bond yields. Barclays (BCS 8.75, -2.42) and Lloyds Banking (LYG 3.22, -1.11) have declined 21.7% and 25.7%, respectively. Elsewhere, Deutsche Bank (DB 15.05, -2.79) has experienced its largest daily point loss since the 2008 financial crisis.

On the home front, losses have been restrained by comparison, with Bank of America (BAC 13.23, -0.83) and Citigroup (C 41.02, -3.44) losing a respective 5.9% and 7.7%. The broader sector has tumbled on the weekly leaderboard, erasing a 3.0% gain to trade lower by 0.9% over that period.

The Treasury complex trades off its session high as the yield on the 10-yr note remains lower by 17-basis points at 1.57%. The yield on the 10-yr note notched a low of 1.41% early in the night, falling near a record low of 1.38%.

10:30 am: [BRIEFING.COM]

The dollar index surges as the UK votes in favor of leaving the EU, the index is up +2% around the 95.38 level

Commodities, as measured by the Bloomberg Commodity Index, are down -1.4% around the 87.08 level

Crude oil plummets well below $50/barrel level reached last session, finding support near the $47 handle

July crude oil futures are currently down $1.79 (-3.6%) at $48.32/barrel

Baker Hughes rig data is scheduled to be released tomorrow at 12:00 pm ET

Monthly IEA data is scheduled to be released on July 13

Natural gas gives up the gains it locked in yesterday after EIA data, as industrial commodities see sharp declines across the board

July natural gas futures are down $0.04 (-1.5%) at $2.66/MMBtu

In precious metals, gold breaks above the $1300.00/oz resistance level, up as much as +5% in early morning trading

August gold futures are currently up $52.20 (+4.1%) at $1315.30/oz

Silver opens morning pit trading with notable gains, currently trading in tandem with gold as market participants continue to digest Brexit

July silver futures are currently up $0.41 (+2.4%) at $17.76/oz

Base metal copper declines as the dollar sees a large boost post-Brexit

July copper futures are down $0.04 (-2.0%) at $2.12/lb

10:00 am:

[BRIEFING.COM] The major averages have drifted higher in recent action as the S&P 500 (-2.4%) trades ten points off its opening low.

Just released, the University of Michigan Consumer Sentiment report for June was revised lower to 93.5 from 94.3 while the Briefing.com consensus expected a reading of 94.0.

Nine sectors trade in the red as the heavily-weighted financial (-3.7%) sector trails technology (-2.7%), industrials (-2.7%), and materials (-2.6%). On the flipside, countercyclical utilities (+0.4%) sports the only gain.

The U.S. Dollar Index (95.53, +2.00) has trimmed its gain to 2.1% as the euro regains some ground against the buck. The single currency trades lower by 2.5% against the dollar (1.1091) after ticking off the 1.1040 level earlier in the session. Separately, the dollar/yen pair trades lower by 3.6% (102.37) as the currency maintains its safe haven bid.

9:50 am:

[BRIEFING.COM] As expected, the stock market opened its day under heavy selling pressure as the Nasdaq Composite (-2.7%) trades behind the Dow Jones Industrial Average (-2.3%) and the S&P 500 (-2.3%).

All ten sectors opened in the red as heavily-weighted financials (-4.1%), technology (-2.8%), industrials (-2.8%), and consumer discretionary (-2.8%) round out the leaderboard. The remaining decliners show losses between 0.5% (utilities) and 2.3% (materials).

In the financial sector (-4.1%), money center banks demonstrate relative weakness, trading lower with European banking names. On that note, JPMorgan Chase (JPM 61.02, -3.03) rounds out the price-weighted index, declining 4.7%.

The consumer discretionary space (-2.8%) trades behind the broader market as travel names weigh on the group. Priceline (PCLN 1296.00, -94.20) has declined by 6.8%.

Separately, the Dow Jones Transportation Average (-3.3%) underperforms as airline names drag on the broader market. The U.S. Global Jets ETF (JETS 20.94, -1.14) has lost 5.2%.

On the commodities front, WTI crude trades lower by 4.1% ($48.07/bbl; -$2.04) while safe haven gold has climbed 4.6% to $1,320.40/ozt.

9:19 am: [BRIEFING.COM] S&P futures vs fair value: -73.00. Nasdaq futures vs fair value: -155.90.

The stock market is on track for steep opening losses as the S&P 500 futures trade 73 points below fair value.

Global equity markets are under pressure this morning as participants react to a surprising outcome in the United Kingdom's referendum on membership in the European Union. The "Leave" camp received 51.9% of lasts night's vote as markets and bookmakers were caught offsides by the high-turnout affair. European indices have paced the retreat with Germany's DAX and France's CAC trading lower by 6.6% and 8.1%, respectively. Additionally, foreign exchange markets were awash in added volatility as the pound sank to a level last seen in 1985 (1.3231). Currently, sterling trades lower by 7.9% (1.3698) against the buck.

The broader market has experienced a flight from risk as financials and energy names show some of the largest losses. Credit Suisse (CS 11.53, -2.19) and Deutsche Bank (DB 14.55, -3.29) have declined a respective 16.0% and 18.4% as investors weigh commentary from the Bank of England and the European Central Bank. On the flipside, safe havens received a bid overnight, bolstering the yen, Treasuries, and gold. The dollar/yen pair trades lower by 3.7% (102.25) after bouncing off the 99.00 price level. Treasuries have rallied as the yield on the 10-yr note tumbles 19-basis points to 1.55%. On the commodities front, gold trades higher by 5.4% ($1,331.60/ozt; +$68.50).

Today's economic data will be capped off with the Michigan Consumer Sentiment for May (Briefing.com consensus 94.0), which will cross the wires at 10:00 ET.

8:57 am: [BRIEFING.COM] S&P futures vs fair value: -69.20. Nasdaq futures vs fair value: -144.20.

Global markets continue to show steep losses with the S&P 500 futures trading 69 points below fair value.

Equity indices across Asia fell victim to intensive selling pressure after Britain voted to leave the European Union. The 'leave' camp received 51.9% of total votes, which contrasted heavily with polls that were conducted just before the referendum. The results of the vote invited caution into the foreign exchange market, sending the dollar/yen pair lower by nearly 3.7% to 102.29 after setting an overnight low near 99.00. For its part, the pound/yen pair is down 1,800 pips (-11.3%) at 140.09 after falling as low as 133.37 in overnight action. The retreat has pressured the currency pair to levels not seen since early 2013. Also of note, the overnight fluctuations resulted in the dollar rallying to a 5-year high against the Chinese yuan (6.6221).

In economic data:

Japan's Corporate Services Price Index +0.2% year-over-year (consensus 0.1%; last 0.3%)

Singapore's May Industrial Production -0.4% month-over-month (expected -1.7%; last 4.4%); +0.9% year-over-year (consensus 1.0%; previous 3.0%)

---Equity Markets---

Japan's Nikkei fell 7.9%, ending the week lower by 4.2%. The index dropped into the neighborhood of this year's low with sectors like financials (-9.8%), consumer discretionary (-9.0%), and technology (-8.5%) pacing the retreat. Dentsu, Mitsubishi Electric, Mazda Motor, Alps Electric, JTEKT, Fast Retailing, and TDK lost between 10.1% and 12.5%.

Hong Kong's Hang Seng surrendered 2.9%, but added 0.4% for the week. Financials and energy-related names faced the most aggressive selling with HSBC, CNOOC, Bank of East Asia, China Petroleum & Chemical, and ICBC falling between 3.2% and 6.6%.

China's Shanghai Composite settled lower by 1.3%, surrendering 1.1% for the week. AVIC Capital, Changyuan Group, and Shanghai Pudong Development Bank lost between 2.7% and 4.6%.

Major European indices trade lower across the board after the 'Leave' camp came away victorious from the referendum on British membership in the European Union. Foreign exchange markets pointed to a risk-on posture as the voting wound down, but early results showed just a slight lead for the 'Remain' side, which eventually devolved into a victory for the other side. The British pound fell as low as 1.3231 against the dollar before narrowing its decline to 7.9%, leaving the pair near 1.3701. European markets have faced broad-based selling with Spain's IBEX (-12.3%) pacing the decline.

In economic data:

Germany's June Ifo Business Climate Index 108.7 (expected 107.5; last 107.8). June Current Assessment 114.5 (expected 114.0; last 114.2) and June Business Expectations 103.1 (consensus 101.2; last 101.7)

UK's BBA Mortgage Approvals 42,200 (expected 37,900; last 40,000)

Italy's April Retail Sales +0.1% month-over-month (expected 0.2%; last -0.6%); -0.5% year-over-year (consensus 2.0%; last 2.1%)

Spain's PPI -5.5% year-over-year (last -6.1%)

---Equity Markets---

UK's FTSE is lower by 3.7% with homebuilders and financials under heavy pressure. Persimmon, Taylor Wimpey, Barratt Developments, Lloyds Banking, Barclays, and RBS are down between 17.5% and 23.0%. Select miners have shown strength with Randgold Resources spiking 20.6% and Fresnillo surging 12.8%.

Germany's DAX has tumbled 6.7% with Deutsche Bank and Commerzbank both down near 13.0%. Exporters BMW, Volkswagen, and Daimler are down between 8.7% and 9.3%.

France's CAC trades down 8.2% amid significant weakness in financials. Societe Generale, BNP Paribas, Credit Agricole, and AXA are down between 14.3% and 20.2%. Heavyweights Renault and Peugeot are both down near 15.0%.

Spain's IBEX has plunged 12.3% with financials like Santander, Banco Sabadell, Caixabank, Banco Popular, BBVA, and Bankia down between 17.7% and 22.0%.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: -68.00. Nasdaq futures vs fair value: -145.00.

Futures have floated higher in recent action as the S&P 500 futures trade 68 points below fair value.

Just released, May durable goods orders decreased 2.2% while the Briefing.com consensus expected a downtick of 0.6%. This comes after the prior month's revised reading of 3.3% (from 3.4%). Excluding transportation, durable orders declined 0.3% (Briefing.com consensus +0.1%) to follow the prior month's revised reading +0.5% (from +0.4%).

The U.S. Dollar Index (95.59, +2.06) has inched lower in recent action, but remains broadly higher on the day. The dollar/Canadian dollar pair trades higher by 1.7% (1.2994) after recently slipping from the 1.3050 price level. Separately, sterling trades lower by 7.7% (1.3732), moving off an overnight and multi-year low of 1.3231.

8:05 am: [BRIEFING.COM] S&P futures vs fair value: -77.70. Nasdaq futures vs fair value: -158.20.

U.S. equity futures plunged overnight after the United Kingdom surprised market participants by voting to leave the European Union. S&P 500 futures trade 78-points below fair value after futures on the benchmark index triggered limit down provisions earlier in the night. The "Leave" camp (52.0%) edged out the "Remain" faction (48.0%), prompting the multi-year legal process of unwinding the UK from the EU. In Britain, Prime Minister David Cameron has announced that he will be stepping down while the Bank of England and the ECB have stated that they will take steps towards boosting liquidity.

Global bourses trade broadly lower as Japan's Nikkei (-7.9%) was pressured by strengthening in the yen. Currently, the dollar trades lower by 3.5% against the safe haven currency (102.43). European bourses are experiencing sharper losses as participants weigh the long-standing implications this decision may hold for the UK and the EU. For its part, sterling has tumbled 8.2% against the dollar (1.3660) after returning to levels previously seen in 1985.

Today's trading volume is expected to be above the recent average while rebalancing in the Russell 2000 is also expected to add to higher participation.

The Treasury complex has surged with the yield on the 10-yr note tumbling 21-basis points to 1.53%.

On the economic front, Durable Orders for May (Briefing.com consensus -0.6%) and the final reading of Michigan Consumer Sentiment for May (Briefing.com consensus 94.0), which will cross the wires at 8:30 ET and 10:00 ET, respectively.

In U.S. corporate news of note:

Finish Line (FINL 17.90, +1.11): +6.6% after beating analysts' estimates for the quarter and reaffirming its FY17 earnings guidance

Sonic (SONC 27.87, -2.48): -8.2% following the company reporting a bottom-line beat and lowering its comparable store sales guidance for FY16

Financial Sector SPDR ETF (XLF 22.01, -1.32): -5.6% amid broad-based weakness in global banking names

Reviewing overnight developments:

Asia-Pacific indices tumbled after Britain voted to leave the European Union. Japan's Nikkei (-7.9%) led the retreat while Hong Kong's Hang Seng -2.9% and China's Shanghai Composite -1.3% followed.

In economic data:

Japan's Corporate Services Price Index +0.2% year-over-year (consensus 0.1%; last 0.3%)

Singapore's May Industrial Production -0.4% month-over-month (expected -1.7%; last 4.4%); +0.9% year-over-year (consensus 1.0%; previous 3.0%)

In news:

In the U.K. referendum, the 'leave' camp received 52.0% of total votes, which contrasted heavily with preliminary polling

The dollar/yen pair fell 3.5% to 102.43 after setting an overnight low at 99.00

For its part, the pound/yen pair is down 1,800 pips (-11.1%) at 140.50 after falling as low as 133.37 in overnight action

Also of note, the dollar rallied to a 5-year high against the Chinese yuan (6.6221).

European indices trade lower across the board with France's CAC -8.6%, Germany's DAX -7.1%, and the U.K.'s FTSE -4.3%. Elsewhere, Spain's IBEX (-12.6%) has paced the decline.

In economic data:

Germany's June Ifo Business Climate Index 108.7 (expected 107.5; last 107.8). June Current Assessment 114.5 (expected 114.0; last 114.2) and June Business Expectations 103.1 (consensus 101.2; last 101.7)

UK's BBA Mortgage Approvals 42,200 (expected 37,900; last 40,000)

Italy's April Retail Sales +0.1% month-over-month (expected 0.2%; last -0.6%); -0.5% year-over-year (consensus 2.0%; last 2.1%)

Spain's PPI -5.5% year-over-year (last -6.1%)

In news:

Foreign exchange markets pointed to a risk-on posture as the voting wound down,

However, early results showed just a slight lead for the 'Remain' side, which eventually devolved into a victory for the other side.

European average have been pressured after the 'Leave' camp came away victorious from the referendum on British membership in the European Union.

The British pound fell as low as 1.3231 against the dollar before narrowing its decline to 8.2%, leaving the pair near 1.3660.

5:57 am: [BRIEFING.COM] S&P futures vs fair value: -75.50. Nasdaq futures vs fair value: -153.10.

5:57 am: [BRIEFING.COM] Nikkei...14952...-1286.30...-7.90%. Hang Seng...20259...-609.20...-2.90%.

5:57 am: [BRIEFING.COM] FTSE...6048.17...-289.90...-4.60%. DAX...9643.35...-613.70...-6.00%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com