Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

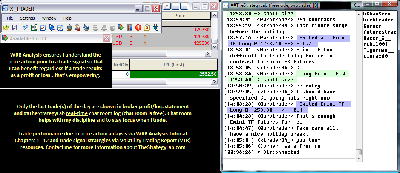

Attachment:

040215-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2562.50.png [ 87.39 KiB | Viewed 342 times ]

040215-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2562.50.png [ 87.39 KiB | Viewed 342 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

($1,500.00) dollars or -15.00 points, Emini ES ($ES_F) futures @

$4,062.50 dollars or +81.25 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $2562.50 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=142&t=2043 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=261&t=2728 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

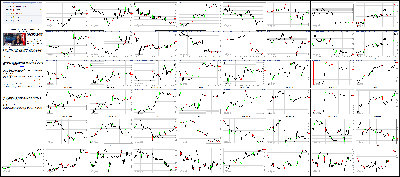

Attachment:

040215-Key-Price-Action-Markets.png [ 1.25 MiB | Viewed 349 times ]

040215-Key-Price-Action-Markets.png [ 1.25 MiB | Viewed 349 times ]

click on the above image to view today's price action of key markets 4:15 pm: [BRIEFING.COM] The major averages eked out modest gains on Thursday after spending the day inside narrow ranges. The S&P 500 gained 0.4% while the Nasdaq Composite (+0.1%) underperformed. The market ended the abbreviated week on a mixed note with the S&P 500 adding 0.3% while the Nasdaq shed 0.1% for the week.

Today's session was very quiet with the S&P 500 bouncing between its 100- (2,060) and 50-day moving averages (2,073). The index settled in the top half of its trading range, but it is worth noting that many participants chose to forego the session, evidenced by light trading volume. To that point, fewer than 700 million shares changed hands at the NYSE floor.

Still, nine of ten sectors registered gains with telecom services (+0.9%) spending the day ahead of its peers. Meanwhile, the remaining three countercyclical groups posted slimmer gains. Notably, the health care sector (+0.2%) registered a modest gain despite intraday weakness in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 339.70, -0.38) shed 0.1%.

The relative weakness in biotechnology kept the Nasdaq Composite behind the S&P 500 while high-beta chipmakers also lagged. Micron (MU 26.72, -0.41) lost 1.5% after reporting a bottom-line beat and issuing below-consensus revenue guidance while the broader PHLX Semiconductor Index slipped 0.3%.

Conversely, chipmakers also pressured the technology sector (-0.1%), which was the only group ending in the red. The modest loss was not entirely due to weakness among microchip names as several large cap components like Google (GOOGL 541.31, -8.18), Microsoft (MSFT 40.29, -0.43), and Qualcomm (QCOM 67.97, -1.46) dropped between 1.1% and 2.1%.

Elsewhere among cyclical groups, the energy sector (+0.2%) settled just above its flat line while crude oil endured a volatile session before ending lower by 1.8% at $49.10/bbl. On a related note, leaders from six countries and Iran agreed on a general framework for a deal that will require Iran to reduce its uranium stockpiles in exchange for the removal of sanctions that are currently in place. The deadline for the final agreement has been pushed back to June 30.

Also of note, the consumer discretionary sector (+0.9%) finished ahead of other cyclical groups thanks to broad strength. Homebuilders rallied with the iShares Dow Jones US Home Construction ETF (ITB 28.61, +0.48) climbing 1.7% while media names like CBS (CBS 61.16, +1.54), Comcast (CMCSA 57.94, +0.88), and Time Warner (TWX 85.00, +2.20) also posted solid gains.

Treasuries spent the day in a steady slide from their early morning highs, sending the 10-yr yield higher by five basis points to 1.91%.

Economic data included ISM Index, Construction Spending, ADP Employment, and MBA Mortgage Index:

Barrons.com

Wall St. ends four-day skid on late tech rally Reuters

The ADP National Employment Report revealed that employment in the nonfarm private business sector rose by 189K in March while the Briefing.com consensus expected an increase of 225K

The February reading was revised up to 214,000 from 212,000

The ISM Manufacturing Index declined to 51.5 in March from 52.9 in February while the Briefing.com consensus expected a decrease to 52.5

Nearly all of the regional manufacturing surveys pointed toward a sharp deceleration in the national manufacturing index so the drop in the ISM Index shouldn't have been much of a surprise

Production levels actually improved, albeit by a very small margin, as the related index increased to 53.8 in March from 53.7 in February

Construction spending declined 0.1% in February after declining a downwardly revised 1.7% (from -1.1%) in January while the Briefing.com consensus expected a decline of 0.3%

The unseasonably harsh winter weather conditions, which were blamed for a significant downturn in new housing starts, had little to no effect on overall construction levels

Total private construction increased 0.2% in February after declining 1.1% in January

The weekly MBA Mortgage Index rose 4.6% to follow last week's 9.5% spike

Tomorrow, the Nonfarm Payrolls report for March (Briefing.com consensus 250K) will be released at 8:30 ET even though the stock market will be closed.

Nasdaq Composite +3.2% YTD

Russell 2000 +4.1% YTD

S&P 500 +0.4% YTD

Dow Jones Industrial Average -0.3% YTD

Week in Review: Technical Levels in Focus

The major averages rallied throughout the Monday session with the Dow Jones Industrial Average (+1.5%) ending in the lead while the S&P 500 (+1.2%) and Nasdaq (1.2%) followed not far behind. The key indices began the week on an upbeat note, aided by overnight news indicating China has loosened its lending requirements for purchases of second homes. In addition, Friday's dovish remarks from Fed Chair Janet Yellen, who said the Fed will move cautiously when raising rates, provided another measure of support. All ten sectors ended the day with solid gains while the S&P 500 surged above its 50-day moving average (2,070). Overall, cyclical sectors had the best showing, but countercyclical groups held their own. Health care and telecom services ended at the bottom of the leaderboard, but both groups still gained close to 1.0% apiece.

The stock market extended its March decline on Tuesday, but was able to end the first quarter in the green. The S&P 500 (-0.9%) lost 1.7% for the month, but added 0.4% during the first quarter. The tech-heavy Nasdaq (-0.9%) outperformed, losing 1.3% in March to narrow its Q1 gain to 3.5%. For its part, the Dow Jones Industrial Average (-1.1%) lost 2.0% in March and shed 0.3% in Q1. Equity indices started the day amid broad pressure while the Dollar Index (98.31, +0.33) added to yesterday's gain. The S&P 500 tried climbing off its opening low, but daylong weakness among heavily-weighted sectors like health care (-1.5%), industrials (-1.0%), and energy (-0.9%) prevented the index from turning positive. On the flip side, the consumer discretionary sector (-0.5%) held a modest gain into the afternoon, but slipped into the red during the final hour. Still, the discretionary sector ended ahead of its peers with homebuilders contributing to the relative strength after DR Horton (DHI) was upgraded to 'Positive' from 'Neutral' at Susquehanna. Shares of DHI gained 1.7% while the iShares Dow Jones US Home Construction ETF (ITB) surrendered its gain ahead of the close. As for the broader market, the S&P 500 slipped back below its 50-day moving average (2,071).

The major averages kicked off April with a retreat that sent the S&P 500 lower by 0.4%. The benchmark index settled in-line with the Dow Jones Industrial Average and the Nasdaq Composite, with the latter catching up during the final hour. Equity indices spent the entire day in the red and could not rally following upbeat economic data from overseas. Strangely, S&P 500 futures tumbled nearly 20 points overnight after China reported its first expansionary Manufacturing PMI (50.1; expected 49.7) in three months. Similar to China, most Manufacturing PMI readings from Europe also surpassed estimates with the region-wide reading rising to 52.2 (expected 51.9). Interestingly, S&P 500 futures rallied off their overnight lows, but could not climb above the spot where the overnight selling commenced. Once the cash session began, the S&P 500 quickly returned into the neighborhood of its overnight low and settled on its 100-day moving average (2,060).

3:45 pm: [BRIEFING.COM]

WTI crude futures rise following agreement of initial framework with Iran

WTI crude oil futures have been climbing since and are now -1.1% at $49.52/barrel, well off its LoD of $48.11/barrel

May crude finished floor trading at $49.10/barrel, down $0.91/barrel

May nat gas rallied $0.11 to $2.71/MMBtu

June gold fell $7.50 to $1201/oz today, while May silver lost $0.34 to $16.72/oz

2:55 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.3% with one hour remaining in the final session of the week. If the benchmark index holds its ground into the close, it will end the week higher by 0.2%. The Dow Jones Industrial Average (+0.3%) trades in-line with the S&P 500 and is on track to register a comparable gain. However, the Nasdaq (-0.1%) is currently indicated to shed 0.2% for the week.

Trading volume remains relatively light going into the home stretch, but that's not surprising considering the stock market will be closed tomorrow. That being said, the futures market will be open tomorrow between 8:30 ET and 9:15 ET, thus allowing participants to respond to the Nonfarm Payrolls report for March. The Briefing.com consensus expected the reading to reveal the addition of 250,000 payrolls.

2:30 pm: [BRIEFING.COM] Recent action saw the S&P 500 (+0.4%) return near its session high, but the index remains inside a narrow range.

The telecom services sector (+1.0%) continues holding the lead, but more notably, the discretionary sector (+0.9%) is the top performer among influential groups. Homebuilders display broad strength with the iShares Dow Jones US Home Construction ETF (ITB 28.51, +0.38) higher by 1.4%. Similarly, large media names like Comcast (CMCSA 57.89, +0.83), CBS (CBS 61.11, +1.49), Time Warner (TWX 85.09, +2.29) also sport solid gains.

Elsewhere, Treasuries remain near their lows with the 10-yr yield higher by four basis points at 1.90%.

1:55 pm: [BRIEFING.COM] Equity indices remain in the middle of their ranges.

Today's economic data came in at some of the strongest levels in months.

Motor vehicle sales increased to 17.1 mln SAAR in March from 16.2 mln SAAR in February.

That was the first time that sales topped 17.0 mln SAAR since reaching 17.2 mln SAAR in November 2014.

The U.S. trade deficit declined to $35.4 bln in February from an upwardly revised $42.7 bln (from $41.8 bln) in January. The Briefing.com Consensus pegged the trade deficit at $42.0 bln.

The February trade deficit was the lowest deficit since November 2009.

The initial claims level declined to 268,000 for the week ending March 28 from an upwardly revised 288,000 (from 282,000) for the week ending March 21. The Briefing.com Consensus pegged the initial claims level at 285,000.

That is the lowest initial claims level since the end of January.

Factory orders increased 0.2% in February after declining a downwardly revised 0.7% (from -0.2%) in January. The Briefing.com Consensus expected factory orders to decline 0.5%.

1:35 pm: [BRIEFING.COM] The major U.S. indices continue to trade in a very tight range on limited volume ahead of the holiday weekend.

In commodities, WTI crude oil futures (-4% to $48.15/bbl) have been volatile in today's session, seeing noteworthy weakness in recent trade following reports that the U.S. and Iran have laid the foundation for an agreement in their nuclear talks, with drafting expected to complete by June 30th. In separate news, Baker Hughes (BHI 64.06, +0.23) released their weekly rig count report at the top of the hour, which the total number of active U.S. rigs declined by 20, the 17th consecutive week of declines. Worth noting, however, the rate of decline has slowed notably over the last few weeks since the company reported a weekly decline of 75 rigs in its weekly report a month ago.

In equities, shares in TrueCar (TRUE 15.52, -1.48) fell to a 7-month low after the company was initiated with a Sell rating at B. Riley & Co.

With the recent uptick in the broad market, all ten S&P sectors are posting gains on the day.

12:55 pm: [BRIEFING.COM] The major averages hold slim gains at midday with the S&P 500 (+0.3%) trading a step ahead of the Nasdaq Composite (+0.1%). Equity indices have spent the first half inside narrow ranges with many participants likely getting a head start on their extended weekend.

The S&P 500 began the day on its 100-day moving average (2,060) and spiked off that level; however, the opening rally stalled during the first hour, just beneath the 50-day moving average (2,073). Since then, the benchmark index has returned into the middle of its trading range.

Nine of ten sectors sport midday gains, but two of the four top-weighted groups-health care (+0.1%) and technology (-0.1%)-have struggled to keep pace with the broader market. The technology sector has been pressured by large cap components like Google (GOOGL 542.79, -6.76), Microsoft (MSFT 40.18, -0.54), and Oracle (ORCL 42.57, -0.22) while biotechnology has contributed to relative weakness in health care. The iShares Nasdaq Biotechnology ETF (IBB 339.56, -0.52) is lower by 0.2%. Furthermore, the combined softness in biotechnology and technology helps explain the underperformance of the Nasdaq.

On the flip side, two other influential sectors-consumer discretionary (+0.6%) and financials (+0.5%)-have shown relative strength while the remaining cyclical groups sit closer to their flat lines.

Elsewhere, Treasuries sit on their lows after sliding throughout the morning. The 10-yr yield is higher by three basis points at 1.89%.

Economic data included Initial Claims, Trade Balance, and Factory Orders:

The weekly initial claims level declined to 268,000 from an upwardly revised 288,000 (from 282,000) while the Briefing.com consensus expected a reading of 285,000

That is the lowest initial claims level since the end of January

According to the Department of Labor, there were no special factors that impacted the claims level. The drop in claims seems to be signal of improved labor market conditions

The U.S. trade deficit declined to $35.40 billion in February from an upwardly revised $42.70 billion (from $41.80 billion) in January while the Briefing.com consensus expected a deficit of $42.00 billion

The February trade deficit was the lowest deficit since November 2009. The goods deficit fell by $7.40 billion to $55.20 billion and the services surplus decreased by $0.10 billion to $19.70 billion

A steep decline in the petroleum-based trade deficit was the main catalyst for sharp drop. Currently, the U.S. is experiencing a significant supply glut, which lowered demand for crude imports, causing the petroleum-based deficit to shrink by $2.60 billion

Factory orders increased 0.2% in February after declining a downwardly revised 0.7% (from -0.2%) in January while the Briefing.com consensus expected a decline of 0.5%

The unexpected increase in factory orders was a direct result of higher petroleum prices. Orders at petroleum refineries increased 11.3% in February after declining 11.2% in January. The gains in petroleum pushed up nondurable goods orders up 1.8% after declining 3.2% in January

12:25 pm: [BRIEFING.COM] Recent action saw the S&P 500 (+0.2%) slip into the neighborhood of its opening range while the Nasdaq has returned to its flat line.

The Nasdaq has trailed the broader market since the opening bell and a recent downtick in the technology sector (-0.2%) has pressured the index back to unchanged. In addition, biotech names have added to their losses with the iShares Nasdaq Biotechnology ETF (IBB 338.70, -1.38) widening its decline to 0.4%. As a result, the health care sector is now back near its flat line.

With technology and health care struggling to stay positive, other heavily-weighted sectors have had to pick up the slack. To that point, financials (+0.4%) and consumer discretionary (+0.6%) continue showing relative strength.

11:55 am: [BRIEFING.COM] Equity indices continue drifting inside narrow ranges with the S&P 500 having spent the past 90 minutes inside a three-point band.

The range-bound action is not all that surprising considering many participants likely started their extended weekend early and chose to forego today's session. To that point, only 244 million shares have changed hands at the NYSE floor.

Meanwhile, market breadth continues favoring the bulls with two names trading in the green for each decliner.

11:25 am: [BRIEFING.COM] The major averages remain near their recent levels with the S&P 500 trading higher by 0.4%. The benchmark index opened right above its 100-day moving average (2,060) and rallied through the first hour until hitting its 50-day moving average (2,073), which has served as resistance for the time being.

Meanwhile, the Nasdaq Composite (+0.2%) trails due to losses among several large cap tech sector components (+0.1%). In addition, biotechnology lags with the iShares Nasdaq Biotechnology ETF (IBB 339.44, -0.64) lower by 0.1%. However, the health care sector (+0.3%) has been able to stay in the green.

10:55 am: [BRIEFING.COM] Equity indices have ticked down from their highs with the S&P 500 narrowing its gain to 0.4%. That being said, all ten sectors trade in the green with consumer discretionary (+0.7%) and energy (+0.6%) in the lead.

Meanwhile, the top-weighted technology sector sits on its flat line as several large cap components weigh. To that point, Google (GOOGL 541.08, -8.40), Microsoft (MSFT 40.40, -0.32), and Qualcomm (QCOM 68.74, -0.69) weigh while chipmakers have held up relatively well. The PHLX Semiconductor Index is higher by 0.2% with Micron (MU 27.22, +0.09) up 0.4% after reporting a bottom-line beat and issuing below-consensus revenue guidance.

Elsewhere, Treasuries have slid to new lows, sending the 10-yr yield to 1.90% (+4 bps).

10:45 am: [BRIEFING.COM]

Crude oil futures saw heavy selling in early AM trade, but has recovered moderately and is now at a current price of $49.40/barrel, down 1.4%

The price action is most likely driven by continued talks regarding Iran's nuclear activities.

Natural gas futures have been trading consistently and moderately higher throughout the session.

May natural gas futures spiked to a new session high of $2.70/MMBtu following the weekly storage data

Current price action has the commodity up +2.7% at $2.67/MMBtu

Precious metals have been in the red all day so far despite weakness in the dollar index (-0.6% at 97.54)

June gold futures are down -1% at $1196.70/oz, while May silver futures have been under heavy pressure and are currently quoted down 2.8% at $16.59/oz

May copper is down 0.7% to $2.73/lb

10:00 am: [BRIEFING.COM] The S&P 500 has extended its gain to 0.5%.

The just-released Factory Orders report for February indicated orders increased 0.2%, which was better than the Briefing.com consensus estimate that called for a decrease of 0.5%.

9:40 am: [BRIEFING.COM] As expected, the major averages began the day near their flat lines. The S&P 500 hovers just above its unchanged level while the Nasdaq Composite sits below its flat line.

Seven of ten sectors trade in the green, but their gains have been limited to no more than 0.2% so far. The consumer staples sector (+0.2%) leads while energy (-0.1%) sits in the red amid weakness in crude oil. The energy component trades lower by 2.3% at $48.93/bbl. Similarly, the top-weighted technology sector (-0.1%) also hovers in the red.

Treasuries remain on their lows with the 10-yr yield up one basis point at 1.87%.

9:14 am: [BRIEFING.COM] S&P futures vs fair value: -1.30. Nasdaq futures vs fair value: +5.60. The stock market is on track for flat open as futures on the S&P 500 trade within a point of fair value. Index futures have spent the night in negative territory, but they began climbing off their lows once markets in Europe opened for action.

Yesterday, the benchmark index surrendered its week-to-date gain and will enter today's session down 0.1% since last Friday. Keep in mind that the stock market will be closed tomorrow for Good Friday; however, the Nonfarm Payrolls report for March will still be released at 8:30 ET (Briefing.com consensus 250K).

As for today's data, weekly initial claims dropped to 268,000 from 288,000 while the Briefing.com consensus expected a reading of 285,000. Meanwhile, the trade deficit for February narrowed to $35.40 billion from $42.70 billion (expected deficit of $42.00 billion).

Treasuries hold slim losses with the 10-yr yield higher by a basis point at 1.87%.

The Factory Orders report for February (consensus -0.5%) will be released at 10:00 ET.

8:54 am: [BRIEFING.COM] S&P futures vs fair value: -2.20. Nasdaq futures vs fair value: +4.20. The S&P 500 futures hover two points below fair value.

Asian equity markets closed mostly higher this morning. The stand out among all the indices was the Nikkei, which was as much as 2% on the day. The catalyst was the prospects of more stimulus from the BOJ, after the Tankan Quarterly Report indicated large companies are forecasting inflation of +1.4% within 12 months and just +1.6% in the next 3 years (far below the 2% inflation target objective that the BOJ has set for FY16). In China, a similar theme helped to push stocks higher, with the Shanghai inching closer to 7 year highs again. Several analysts called for a fresh round of easing by the PBOC after a note from Fitch indicated that latest stimulus to help the property market may have a limited impact considering the glut of supply in the housing market.

In economic data:

Hong Kong's Manufacturing PMI fell to 49.6 from 50.7

India's HSBC Markit Manufacturing PMI rose to 52.1 from 51.2 (expected 51.0)

South Korea's Current Account surplus narrowed to KRW6.44 billion from KRW6.58 billion

Australia's Trade Deficit widened to AUD1.26 billion from AUD1.00 billion (expected deficit of AUD1.30 billion) while March MI Inflation Gauge ticked up 0.4% month-over-month (prior 0.0%)

------

Japan's Nikkei gained 1.5%. All sectors finished in positive territory with Financials and Consumer Discretionary both leading the way, up +1.8%. Notably, Mizuho traded higher by 1.8%, while Toshiba posted a 2.3% gain.

Hong Kong's Hang Seng ended +0.8% higher. Financials were on the move higher again with Bank of China and China Construction Bank both advancing by 1.1%

China's Shanghai Composite rose 0.4%. The volume was lighter than some of the most recent days, but shipbuilders saw some profit taking with the likes of China Shipbuilding Ind Co finishing 1% lower on the day.

Major European indices trade near their flat lines amid light volume. European Central Bank member Sabine Lautenschlager voiced concerns over the QE program, saying low interest rates can lead to price bubbles among other assets.

Economic data was limited:

UK's Construction PMI fell to 57.8 from 60.1 (expected 59.5)

Italy's Q4 Public Deficit came in at 2.3% (prior 3.0%)

------

Germany's DAX is lower by 0.1% with heavyweights Bayer, Daimler, and Deutsche Lufthansa down between 1.2% and 3.0%. Select basic materials names outperform with K+S and ThyssenKrupp higher by 2.2% and 0.7%, respectively.

UK's FTSE has added 0.1%. Mining names like Anglo American, Antofagasta, BHP Billiton, and Glencore down between 1.2% and 2.3% while consumer names outperform. Marks & Spencer Group has jumped 5.6% after reporting strong quarterly sales.

In France, the CAC trades up 0.1%. Financials and discretionary names lead with L'Oreal, Danone, and BNP Paribas holding gains between 0.2% and 0.6%.

8:31 am: [BRIEFING.COM] S&P futures vs fair value: -2.40. Nasdaq futures vs fair value: +4.30. The S&P 500 futures trade two points below fair value.

The latest weekly initial jobless claims count totaled 268,000 while the Briefing.com consensus expected a reading of 285,000. Today's tally was below the revised prior week count of 288,000 (from 282,000). As for continuing claims, they fell to 2.325 million from 2.413 million.

Separately, the February trade deficit narrowed to $35.40 billion from $42.70 billion while the Briefing.com consensus expected the deficit to come in at $42.00 billion.

7:57 am: [BRIEFING.COM] S&P futures vs fair value: -2.60. Nasdaq futures vs fair value: +2.70. U.S. equity futures trade modestly lower amid mixed action overseas. The S&P 500 futures have spent the entire night in the red and they currently hover three points below fair value.

Equity futures have not been able to draw support from modest dollar weakness that has the Dollar Index (97.83, -0.36) trading lower by 0.4%.

The recently-released Challenger Job Cuts report pointed to a 6.4% year-over-year increase in March.

Weekly Initial Claims (Briefing.com consensus 285K) and the February Trade Balance report (consensus -$42.00 billion) will cross the wires at 8:30 ET and the day's data will be topped off with the Factory Orders report for February (consensus -0.5%).

Treasuries have built on yesterday's gains with the 10-yr yield lower by a basis point at 1.85%.

In U.S. corporate news of note:

Carmax (KMX 70.75, +2.36): +3.5% after beating earnings estimates.

Micron (MU 27.00, -0.13): -0.5% after reporting a bottom-line beat and issuing below-consensus revenue guidance.

Procter & Gamble (PG 81.94, -0.38): -0.5% after BMO Capital downgraded the stock to 'Market Perform.'

Reviewing overnight developments:

Asian markets ended higher. China's Shanghai Composite +0.4%, Hong Kong's Hang Seng +0.8%, and Japan's Nikkei +1.5%

In economic data:

Hong Kong's Manufacturing PMI fell to 49.6 from 50.7

India's HSBC Markit Manufacturing PMI rose to 52.1 from 51.2 (expected 51.0)

South Korea's Current Account surplus narrowed to KRW6.44 billion from KRW6.58 billion

Australia's Trade Deficit widened to AUD1.26 billion from AUD1.00 billion (expected deficit of AUD1.30 billion) while March MI Inflation Gauge ticked up 0.4% month-over-month (prior 0.0%)

In news:

Hong Kong's PMI fell into contraction, fueled by a decline in the employment component

Major European indices trade near their flat lines. Germany's DAX -0.1%, UK's FTSE -0.1%, and France's CAC +0.1%. Elsewhere, Italy's MIB -0.2% and Spain's IBEX +0.2%

Economic data was limited:

UK's Construction PMI fell to 57.8 from 60.1 (expected 59.5)

Italy's Q4 Public Deficit came in at 2.3% (prior 3.0%)

Among news of note:

European Central Bank member Sabine Lautenschlager voiced concerns over the QE program, saying low interest rates can lead to asset price bubbles among other assets

5:53 am: [BRIEFING.COM] S&P futures vs fair value: -6.30. Nasdaq futures vs fair value: -9.30.

5:53 am: [BRIEFING.COM] Nikkei...19312.79...+278.00...+1.50%. Hang Seng...25275.64...+192.90...+0.80%.

5:53 am: [BRIEFING.COM] FTSE...6812.05...+2.60...+0.00%. DAX...11992.19...-9.20...-0.10%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage