Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

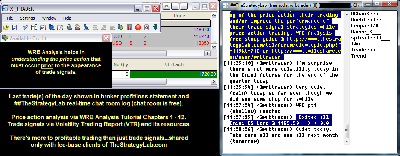

Attachment:

063014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1720.00.png [ 175.83 KiB | Viewed 490 times ]

063014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1720.00.png [ 175.83 KiB | Viewed 490 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,720.00 dollars or +17.20 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,720.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=131&t=1829 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=240&t=2365 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

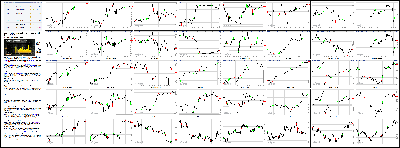

Stocks Up, Up, Up At Mid-Year Point Attachment:

063014-Key-Price-Action-Markets.png [ 1.24 MiB | Viewed 504 times ]

063014-Key-Price-Action-Markets.png [ 1.24 MiB | Viewed 504 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

That's a wrap! The first half of 2014 on Wall Street is officially in the books -- and performance was solid despite a lackluster finale on Monday.

Here's what you need to know:

1. By the numbers: Both the Dow Jones Industrial Average and S&P 500 lost ground slightly on Monday after flirting with record highs previously.

But the S&P 500 has already logged 22 record highs this year alone, ending the first half up 6%. While that first-half rally trailed last year's performance, it still easily bested the Dow's narrow gain of just 1.5%.

Interestingly, that's the biggest halftime lead by the S&P 500 over the Dow since 2009 and the seventh-biggest since 1929, according to Bespoke Investment Group.

Related: The 2014 half-time reportMeanwhile, the Nasdaq landed safely in the green on Monday, leaving it up a healthy 5.5% so far this year.

Tech stocks outperformed on Monday, as evidenced by the 0.5% gain for CNNMoney's Tech30. Standouts included Apple (AAPL, Tech30), SINA (SINA, Tech30) and BlackBerry (BBRY, Tech30). Then there was GoPro (GPRO), in a league of its own, continuing its red hot start as a public company. After zooming last week, the wearable camera maker popped another 13% today.

2. More housing hopes: Wall Street briefly cheered new signs of progress in the very important housing market. The National Association of Realtors said U.S. pending home sales jumped 6.1% in May, representing the biggest monthly increase since April 2010. Economists had been anticipating a more modest increase.

The bullish housing news lifted shares of home builders like Lennar (LEN) and PulteGroup (PHM).

3. Stock movers -- Yahoo, American Apparel, GoPro: Yahoo (YHOO, Tech30) enjoyed a 2.5% bump after the Internet company was upgraded to "overweight" by Piper Jaffray.

Related: Yahoo's Marissa Mayer loves AlibabaWhile Yahoo's core business remains "challenged," analyst Gene Munster said his bullish call is based on the belief that the company's stake in Alibaba is "undervalued." Last week, the Chinese e-commerce giant revealed plans to list its highly anticipated initial public offering on the New York Stock Exchange.

American Apparel (APP) dropped 6% after the company announced plans to adopt a shareholder rights plan in an effort to prevented ousted chairman (and founder) Dov Charney from seizing control. The sell-off follows a surge of nearly 30% on Friday.

Related: Founders in hot water at American Apparel, LululemonIt was truly a great leap for MannKind (MNKD). Shares soared nearly 10% after the company said the Food and Drug Administration approved a powder form of insulin that is inhaled. The stock is up 113% year to date.

PPG Industries (PPG) logged a 3% gain after unveiling plans to acquire a Mexican coatings company for about $2.3 billion.

Bank of New York Mellon (BK) advanced 3.5% as activist investor Nelson Peltz and his Trian Partners revealed a $1.05 billion stake in the financial company.

Related: Adrenaline rush! GoPro surges again4. Investors yawn at Facebook, BNP headlines: Facebook (FB, Tech30) is in hot water after it was revealed the social network conducted a 'mood' experiment on users without their knowledge or explicit consent. Facebook's terms of service give the company permission to conduct this kind of research, but many users have reacted with anger.

Wall Street, however, was unmoved by the drama. Facebook's stock closed down less than 0.5% after posting gains earlier in the day.

The U.S. Department of Justice is expected to announce a multi-billion dollar settlement with French banking giant BNP Paribas (BNPQY) on Monday. The bank has been subject to a long running criminal investigation over accusations that it breached U.S. sanctions on Iran, Sudan and other countries. Shares of BNP rose ever so slightly in Paris.

5. Dubai crumbles, Bulgaria booms: Investors continue to give Dubai's stock market a big thumbs down.

The DFM General Index plunged 4.4% on Monday due to worries about property stocks, especially contracting giant Arabtec Holdings. Dubai plummeted 22% in June, its worst month since 2008.

On the other hand, Bulgaria's stock market raced almost 6% higher after the European Union gave the green light to the country providing $2.3 billion in state aid for banks. The move follows a series of arrests of men accused of fueling bank runs.

Both European and Asian markets closed mixed. The main loser of the day was Australia's ASX All Ordinaries index, which dropped by 0.9%.

Argentina's markets fell just modestly even as the country faces a Monday deadline to pay two groups of bondholders. The way things unfold from here will determine Argentina's ability to move past its 2001 default and regain access to foreign funds.

4:10 pm: [BRIEFING.COM] The stock market finished the second quarter on a subdued note with the major averages ending near their flat lines. The Nasdaq Composite (+0.2%) outperformed throughout the session, while the S&P 500 (-0.04%) surrendered its slim gain into the close. For the quarter, the S&P 500 jumped 4.7%, while the Nasdaq advanced 5.0%.

Equity indices displayed losses at the start, but the Nasdaq and S&P 500 returned into the green after a better than expected Pending Home Sales report for June (6.1% versus 1.5% Briefing.com consensus) crossed the wires. Despite the early rebound, the S&P 500 ran into resistance in the 1964 area, which served as the high point for the day. Unlike the Nasdaq and S&P 500, the Dow Jones Industrial Average (-0.2%) could not make a sustained move into the green.

Five of ten sectors posted gains with this year's leader-utilities-setting the pace. The countercyclical sector advanced 0.8%, extending its year-to-date gain to 16.4%. Unlike utilities, the remaining defensively-oriented groups ended in the red with consumer staples, health care, and telecom services down 0.04%, 0.4%, and 0.4%, respectively.

Meanwhile, the six cyclical groups also ended on a mixed note. Consumer discretionary (-0.1%), energy (unch), financials (unch), and industrials (-0.4%) lagged, while technology (+0.2%) and materials (+0.5%) held gains throughout the day.

Notably, the technology sector fueled the outperformance of the Nasdaq Composite with chipmakers ending on their highs. Micron (MU 32.95, +1.44) surged 4.6% after being added to the Focus List at Credit Suisse, while the broader PHLX Semiconductor Index rose 1.1% to secure a quarterly advance of 8.4%. In addition, the top-weighted tech component-Apple (AAPL 92.93, +0.95)-also did some grunt work, rallying 1.0%.

Elsewhere, the materials sector was underpinned by miners and steelmakers. The Market Vectors Steel ETF (SLX 47.72, +0.28) added 0.6%, while Market Vectors Gold Miners ETF (GDX 26.45, +0.47) spiked 1.8%.

On the downside, industrials could not climb into the green amid weakness in defense contractors (PHLX Defense Index -0.5%). Transports, however, displayed relative strength. The Dow Jones Transportation Average tacked on 0.3% to secure a quarterly advance of 8.3%.

Treasuries retreated in the morning, but the brief slip was retraced in its entirety over the course of the session. The 10-yr note added five ticks with its yield slipping two basis points to 2.52%.

Despite the narrow ranges, participation was solidly above average with nearly 800 million shares changing hands at the NYSE.

Economic data was limited to Chicago PMI for June and May Pending Home Sales:

Related Stories

InPlay from Briefing.com Briefing.com

How the Dow Jones industrial average did Thursday Associated Press

Stocks pare losses; S&P bumps up to record close USA TODAY

S&P 500 on track for 6th straight quarterly gain MarketWatch

US STOCKS SNAPSHOT-S&P edges up at open to fresh record Reuters

Manufacturing activity decelerated in the Chicago region as the Chicago PMI fell to 62.6 in June from 65.5 in May. The Briefing.com consensus expected the index to fall to 61.0

The Chicago PMI has exceeded 60.0 for three consecutive months

Production strengthened in June as the related index increased to 70.1 from 64.4 on strong levels of backlogs

New orders growth faded in June as the related index fell to 65.1 from 70.2

Backlog levels dropped to 55.4 from 61.4

The Employment Index increased to 58.4 from 54.6

Pending home sales for May rose 6.1%, which was better than the 1.5% increase forecast by the Briefing.com consensus

The reading followed last month's revised increase of 0.5% (from 0.4%)

Tomorrow, the ISM Index for June (Briefing.com consensus 55.8) and May Construction Spending (consensus 0.4%) will be reported at 10:00 ET, while auto and truck makers will be reporting their June sales throughout the day.

S&P 500 +6.1% YTD

Nasdaq Composite +5.5% YTD

Dow Jones Industrial Average +1.5% YTD

Russell 2000 +2.6% YTD

3:35 pm: [BRIEFING.COM]

Grains including corn, soybeans and wheat sold off today following the USDA annual acreage report and quarterly grain stocks report results

July corn fell 25 cents (or -5.7%) to $4.17/bushel, July wheat fell 17 cents (or -2.9%) to $5.76/bushel, July soybeans fell 49 cents (or -3.6%) to $13.28/bushel

Crude oil futures extended losses last week, closing $0.43 today to $105.37/barrel

Gold and silver slowly climbed higher off of morning lows.

Aug gold ended the session $2.30 higher at $1322.30/oz. July silver fell $0.11 at $21.03/oz, but erased most losses

Natural gas rallied this morning and finished 3 cents higher at $4.47/MMBtu

Copper rallied this morning during pit trading, rising as high as $3.21/lb. Copper ended at $3.20, up $0.03.

2:55 pm: [BRIEFING.COM] The S&P 500 hovers right above its flat line with one hour remaining in the session.

During the past 30 minutes, General Motors (GM 36.11, -0.51) announced six new safety recalls that involve roughly 7.6 million vehicles manufactured between 1997 and 2014. The recalls are expected to result in a $1.20 billion charge, which already includes a $700 million charge from recalls announced earlier in the quarter. Shares of GM reversed from a gain of 0.6% to a loss of 1.4% following the news.

2:30 pm: [BRIEFING.COM] The S&P 500 has inched back its early high, while the Dow Jones Industrial Average has returned to its flat line.

The recent uptick has helped a handful of sectors return into the green, leaving just three groups in the red. The industrial sector (-0.3%) has lagged throughout the session amid weakness in defense stocks (PHLX Defense Index -0.3%), while transports have held gains since the opening bell. The Dow Jones Transportation Average trades up 0.6% with 15 of its 20 components in the green.

1:55 pm: [BRIEFING.COM] The S&P 500 (+0.1%) remains right above its flat line, while the Nasdaq Composite (+0.4%) has extended to a fresh session high thanks to the continued strength among some of the most influential tech components.

Shares of Apple (AAPL 93.25, +1.27) have been climbing steadily throughout the session and the top-weighted sector component is now higher by 1.4%. Elsewhere among top-weighted tech names, Oracle (ORCL 40.77, +0.24) and Cisco Systems (CSCO 24.86, +0.16) are both up near 0.6%, while Intel (INTC 30.89, -0.04) remains in the red even as the broader PHLX Semiconductor Index trades up 1.1%.

1:25 pm: [BRIEFING.COM] By and large, it has been a pretty uneventful day of trading. The major indices have chopped around, displaying a mostly bullish bias. That doesn't mean they are up big. Rather, it simply means that they have refused to give way to selling interest.

The resilience is fitting certainly as it relates to the market's disposition throughout the second quarter, which ends today. In that time, the Dow has gained 2.4%, the S&P 500 has jumped 4.8%, and the Nasdaq Composite has increased 5.1%.

Those are great, short-term returns to be sure, yet they still pale in comparison to the gains registered by the S&P 500 energy sector (+11.5%), the Philadelphia Semiconductor Index (+8.3%), the Dow Jones Transportation Average (+8.5%), the Dow Jones Utility Average (+8.0%), and the Nasdaq 100 (+7.3%).

Pretty remarkable for a period that included the flare-up of armed conflict in Ukraine and Iraq and the worst GDP reading (-2.9%) since the first quarter of 2009.

12:55 pm: [BRIEFING.COM] The major averages are little changed at midday with the S&P 500 trading less than a point above its flat line. The Dow Jones Industrial Average (-0.1%) has had a bit more difficulty keeping its head above water, while the Nasdaq Composite (+0.3%) displays relative strength.

Stocks kicked off the final session of the second quarter on a lower note, but a better than expected Pending Home Sales report for June (6.1% versus 1.5% Briefing.com consensus) helped the indices recover from their opening lows. Despite the early rebound, the S&P 500 has run into some resistance in the 1964 area.

Four of ten sectors display gains at this time with this year's top sector-utilities-in the lead. Including today's advance of 0.6%, the rate-sensitive sector is now up 16.1% for the year. Utilities notwithstanding, the consumer staples sector (+0.2%) is the only other countercyclical group trading in the green, while health care (-0.1%) and telecom services (-0.3%) lag after surrendering their early gains.

Interestingly, the underperformance of the health care sector has not been able to keep a lid on biotechnology with the iShares Nasdaq Biotechnology ETF (IBB 257.39, +0.66) creeping back to its opening high. Furthermore, the relative strength of biotech has given a measure of support to the Nasdaq Composite.

Fittingly, the tech-heavy Nasdaq has also drawn strength from the technology sector (+0.3%) and top-weighted components like Apple (AAPL 92.74, +0.77), Cisco Systems (CSCO 24.87, +0.17) and Oracle (ORCL 40.75, +0.22). The three names hold gains between 0.5% and 0.8%.

Chipmakers have also made a contribution to the sector's strength as the PHLX Semiconductor Index trades higher by 1.0% with Micron (MU 32.97, +1.46) up 4.7% after Credit Suisse added the stock to its Focus List.

On the fixed income side, Treasuries slumped ahead of the open, but they have since returned to their morning highs. The 10-yr note is higher by four ticks with its yield down two basis points at 2.52%.

Economic data was limited to Chicago PMI for June and May Pending Home Sales:

Manufacturing activity decelerated in the Chicago region as the Chicago PMI fell to 62.6 in June from 65.5 in May. The Briefing.com consensus expected the index to fall to 61.0

The Chicago PMI has exceeded 60.0 for three consecutive months

Production strengthened in June as the related index increased to 70.1 from 64.4 on strong levels of backlogs

New orders growth faded in June as the related index fell to 65.1 from 70.2

Backlog levels dropped to 55.4 from 61.4

The Employment Index increased to 58.4 from 54.6

Pending home sales for May rose 6.1%, which was better than the 1.5% increase forecast by the Briefing.com consensus

The reading followed last month's revised increase of 0.5% (from 0.4%)

12:30 pm: [BRIEFING.COM] Equity indices remain near their recent levels with the S&P 500 anchored to its flat line. At this juncture, four sectors display gains with utilities (+0.6%) holding the lead.

Outside of utilities, the consumer staples sector (+0.2%) is the only other countercyclical group trading in the green, while health care (-0.1%) and telecom services (-0.2%) lag after surrendering their early gains.

On the cyclical side, the top- and bottom-weighted sectors-technology (+0.3%) and materials (+0.1%)-hold modest gains, while the remaining four sectors display losses of no more than 0.2%.

Also of note, Treasuries have continued their advance with the 10-yr yield slipping to 2.52%.

12:00 pm: [BRIEFING.COM] The major averages continue respecting narrow trading ranges that were established during the past hour. The Nasdaq Composite (+0.2%) and S&P 500 hold modest gains, while the Dow Jones Industrial Average sits right below its flat line.

The price-weighted Dow is looking for direction with 15 listings up and 15 down. Boeing (BA 127.22, -1.32) is the weakest component, down 1.0%, while no other index member holds a loss of 1.0% or more. Meanwhile, the 15 advancers sport gains between 0.1% and 1.0% with Merck (MRK 58.09, +0.56) leading the way.

With June coming to an end, the Dow is on track to end the month behind the other indices with a monthly gain of 0.8%.

11:25 am: [BRIEFING.COM] Not much change in the major averages as the S&P 500 remains right near its flat line, while the Nasdaq (+0.2%) outperforms.

Nasdaq outperformance has been a common theme in June as the tech-heavy index sports a month-to-date advance of 3.9% versus a 2.0% gain for the S&P 500. Thanks to the resurgence of high-growth tech (and biotech) names, the Nasdaq is on pace to finish the second quarter just ahead of the S&P 500 with a 4.9% gain versus a 4.8% quarterly increase for the benchmark index.

Fittingly, with the Nasdaq staying ahead of the broader market, the technology sector (+0.3%) trades ahead of the remaining cyclical sectors. The top sector component-Apple (AAPL 92.64, +0.66)-is contributing to the outperformance with its 0.7% gain. Including the advance, the top-weighted tech stock has added nearly 21.0% since the end of the first quarter.

10:55 am: [BRIEFING.COM] The S&P 500 has slipped back to its flat line, while the Nasdaq Composite (+0.1%) continues holding a slim gain.

With the benchmark index hovering just below its flat line, only three sectors-consumer staples (+0.4%), technology (+0.2%), and utilities (+0.5%)-trade with gains at this time. The top performer of the three-utilities-is also the strongest sector so far in 2014. The rate-sensitive group has added 16.1% since the start of the year, while the second-best sector-energy-holds a year-to-date gain of 11.5%. Today, however, the energy sector is lower by 0.1%.

Elsewhere, Treasuries have returned into the green after notching their session lows shortly after the release of the Pending Home Sales report for May. The 10-yr note is higher by two ticks with its yield off one basis point at 2.53%.

10:35 am: [BRIEFING.COM]

Crude has also been in the red all day so far, before morning rally, which briefly put it back at the unchanged line

Aug crude oil is now -0.2% at $105.58/barrel

Gold and silver have been in the red all session so far

However, gold has been recovering off its LoD and is now -0.2% at $1317.30/oz

Silver has been more consolidated and is near its LoD, now -1.1% at $20.90/oz

Aug natural gas sold off in recent trade, hitting a new LoD of $4.38/MMBtu minutes ago. Nat gas is now -0.5% at $4.39/MMBtu

Copper put in a small rally, hitting a fresh HoD just a few min ago. Copper is currently +0.5% at $3.18/lb

Dollar index is currently -0.2% at 79.92, now sitting at a fresh LoD

10:00 am: [BRIEFING.COM] The S&P 500 has joined the Nasdaq Composite (+0.1%) in the green. The technology sector (+0.2%) continues showing relative strength, but it is worth mentioning that health care (+0.1%) has slipped from its early high.

Elsewhere, Treasuries have slumped to new lows for the session, sending the 10-yr yield to 2.54% after hovering near 2.52% less than an hour ago.

Just reported, pending home sales for May rose 6.1%, which was better than the 1.5% increase forecast by the Briefing.com consensus. Today's reading followed last month's revised increase of 0.5% (from 0.4%).

9:45 am: [BRIEFING.COM] Equity indices began the day on a lower note, but the Nasdaq (+0.1%) was quick to climb into the green. The index was able to rally off its opening level thanks to the early strength of the technology sector (+0.1%) as well as biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 257.64, +0.91) is higher by 0.4%. On a related note, the health care sector is higher by 0.2%.

On the flip side, the industrial sector (-0.4%) is the weakest performer amid weakness in defense contractors. The PHLX Defense Index trades down 0.7%.

Just released, the Chicago PMI for June slipped to 62.6 from 65.5, while the Briefing.com consensus expected a decrease to 61.0.

The Pending Home Sales report for May (consensus +1.5%) will cross the wires at 10:00 ET.

9:10 am: [BRIEFING.COM] S&P futures vs fair value: -1.50. Nasdaq futures vs fair value: -2.50. The major averages are on track for a quiet start to the trading week with the S&P 500 futures trading less than two points below fair value. Futures on the benchmark index have spent the bulk of the overnight session in the red, registering their pre-market lows during the past two hours.

Overseas action has not done much to change the overall sentiment as markets in Asia ended mostly higher, while most European indices trade with modest losses.

With regard to corporate news, General Motors (GM 36.50, -0.12) is expected to announce a victim compensation program today and Facebook (FB 67.51, -0.09) is seeing modest early pressure following reports the company manipulated its news feed as part of research in 2012.

The Chicago PMI report for June (Briefing.com consensus 61.0) will be released at 9:45 ET and the Pending Home Sales report for May (consensus +1.5%) will cross the wires at 10:00 ET.

Treasuries hold gains with the 10-yr yield down one basis point at 2.52%.

8:58 am: [BRIEFING.COM] S&P futures vs fair value: -1.60. Nasdaq futures vs fair value: -2.00. The S&P 500 futures trade less than two points below fair value.

Asian markets ended mostly higher with quarter-end window dressing taking hold.

In economic data:

Japan's preliminary industrial production (0.5% month-over-month versus expected 0.9%) missed estimates. Separately, Housing Starts fell 15.0% year-over-year (expected -10.6%, previous -3.3%)

Australia's HIA New Home Sales (-4.3% month-over-month) posted its biggest drop since August

------

Japan's Nikkei added 0.4%, bouncing off the psychologically important 15,000 level. Exporters gained despite the strength in the yen as Toyota Motor added 0.6% and Panasonic gained 0.7%.

Hong Kong's Hang Seng shed 0.1%, remaining near its best levels of 2014. Casino stocks gained in response to some positive 'tier 1' commentary on the space with Galaxy Entertainment climbing 3.6%.

China's Shanghai Composite rose 0.6%, posting its best close in nearly two weeks. Financials saw solid gains with Industrial Bank and Ping An Bank both adding 0.9%.

Major European indices trade mostly lower, while Germany's DAX (+0.3%) outperforms. In news, Bank of England Governor Mark Carney said the recent strength in the British pound is reflective of the strength of the economy. Currently, the pound (1.7050) trades right near its year-to-date high against the dollar.

Participants received several data points:

Eurozone M3 Money Supply rose 1.0% year-over-year (expected 0.8%, previous 0.7%), but Private Loans fell 2.0% year-over-year (consensus -1.6%, prior -1.8%). Separately, CPI rose 0.5% year-over-year, as expected, while Core CPI increased 0.8% (expected 0.7%, previous 0.7%)

Germany's Retail Sales slipped 0.6% month-over-month (expected 0.7%, previous -1.5%), while the year-over-year reading increased 1.9% (consensus 2.1%, prior 3.2%)

Great Britain's BoE Consumer Credit rose GBP740 million (expected GBP700 million, prior GBP650 million), while Net Lending to Individuals increased GBP2.70 billion (expected GBP2.50 billion, previous GBP2.40 billion)

Italy's CPI increased 0.1% month-over-month, while the year-over-year reading ticked up 0.3%

Spain's Business Confidence improved to -7 from -8, as expected

------

Germany's DAX trades higher by 0.3% with heavyweights Bayer and Siemens contributing to the advance. Both names are up near 0.5% apiece. Financials lag with Commerzbank and Deutsche Bank down 2.0% and 1.3%, respectively.

Great Britain's FTSE holds a loss of 0.2% with airlines on the defensive. EasyJet and International Consolidated Airlines are down 5.7% and 2.5% after EasyJet was downgraded at Bank of America.

In France, the CAC holds a loss of 0.2%. Credit Agricole is the weakest performer, down 2.6%. Chemical producer Solvay outperforms with a gain of 3.0%.

Spain's IBEX trades down 0.4% amid broad weakness. Banco Popular and Bankinter hold respective losses of 1.5% and 2.0%.

8:29 am: [BRIEFING.COM] S&P futures vs fair value: -0.70. Nasdaq futures vs fair value: -1.00. The stock market is on course for a flat start to the final session of the quarter. The S&P 500 and Nasdaq Composite will both enter the trading day with quarter-to-date gains of 4.7%, while the Dow Jones Industrial Average will look to maintain its 2.4% advance since the end of March.

The trading week will start on a quiet note following an Asian session that saw modest gains across most of the region. European indices, meanwhile, trade mostly lower, while Germany's DAX (+0.3%) outperforms.

Treasuries hover near their highs after inching up overnight. The 10-yr yield is lower by one basis point at 2.52%.

7:55 am: [BRIEFING.COM] S&P futures vs fair value: -3.00. Nasdaq futures vs fair value: -4.00. U.S. equity futures trade modestly lower amid cautious action overseas. The S&P 500 futures hover three points below fair value.

Reviewing overnight developments:

Asian markets ended mixed. Hong Kong's Hang Seng -0.1%, Japan's Nikkei +0.4%, and China's Shanghai Composite +0.6%.

In economic data:

Japan's Industrial Production rose 0.5% month-over-month (expected 0.9%, previous -2.8%) and Housing Starts fell 15.0% year-over-year (expected -10.6%, previous -3.3%)

Australia's HIA New Home Sales fell 4.3% month-over-month (previous 2.9%), while Private Sector Credit ticked up 0.4% month-over-month (expected 0.4%, prior 0.5%)

New Zealand's Building Consents fell 4.6% month-over-month (expected -2.5%, previous 1.9%), while ANZ Business Confidence slipped to 42.8% from 53.5%

In news:

Japan's Prime Minister Shinzo Abe published an op-ed in the Financial Times, discussing his growth strategy. The article indicated the cabinet will make changes to Japan's pension fund.

Major European indices trade lower across the board. Germany's DAX -0.1%, Great Britain's FTSE -0.3%, and France's CAC -0.5%. Elsewhere, Italy's MIB -0.7% and Spain's IBEX -0.8%.

Participants received several data points:

Eurozone M3 Money Supply rose 1.0% year-over-year (expected 0.8%, previous 0.7%), but Private Loans fell 2.0% year-over-year (consensus -1.6%, prior -1.8%). Separately, CPI rose 0.5% year-over-year, as expected, while Core CPI increased 0.8% (expected 0.7%, previous 0.7%)

Germany's Retail Sales slipped 0.6% month-over-month (expected 0.7%, previous -1.5%), while the year-over-year reading increased 1.9% (consensus 2.1%, prior 3.2%)

Great Britain's BoE Consumer Credit rose GBP740 million (expected GBP700 million, prior GBP650 million), while Net Lending to Individuals increased GBP2.70 billion (expected GBP2.50 billion, previous GBP2.40 billion)

Italy's CPI increased 0.1% month-over-month, while the year-over-year reading ticked up 0.3%

Spain's Business Confidence improved to -7 from -8, as expected

Among news of note:

Bank of England Governor Mark Carney said the recent strength in the British pound is reflective of the strength of the economy. Currently, the pound (1.7050) trades right near its year-to-date high against the dollar.

In U.S. corporate news:

Facebook (FB 67.30, -0.30): -0.5% amid reports the company manipulated its news feed as part of research in 2012.

Yahoo! (YHOO 34.85, +0.60): +1.8% after Piper Jaffray upgraded the stock to 'Overweight' from 'Neutral.'

The Chicago PMI report for June (Briefing.com consensus 61.0) will be released at 9:45 ET and the Pending Home Sales report for May (consensus +1.5%) will cross the wires at 10:00 ET.

6:29 am: [BRIEFING.COM] S&P futures vs fair value: -0.50. Nasdaq futures vs fair value: -2.00.

6:29 am: [BRIEFING.COM] Nikkei...15162.10...+67.10...+0.40%. Hang Seng...23190.72...-30.80...-0.10%.

6:29 am: [BRIEFING.COM] FTSE...6766.63...+8.80...+0.10%. DAX...9853.90...+38.40...+0.40%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage