Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

011714-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+290.00.png [ 175.87 KiB | Viewed 389 times ]

011714-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+290.00.png [ 175.87 KiB | Viewed 389 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$290.00 dollars or +2.90 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $290.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1700 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

Stocks Finish The Week Mixed Attachment:

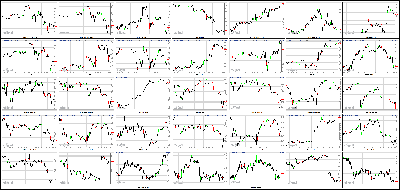

011714-Key-Price-Action-Markets.png [ 541.58 KiB | Viewed 315 times ]

011714-Key-Price-Action-Markets.png [ 541.58 KiB | Viewed 315 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

The major stock indexes moved in different directions Friday as investors analyzed a slew of corporate earnings and the latest figures on housing.

The Dow closed up slightly, while the S&P 500 and Nasdaq finished modestly lower. CNNMoney's Tech 30 index was flat. Stocks ended the week mixed. It seems that investors are searching for direction after some bigger market moves earlier in the week.

The U.S. markets will be closed Monday in observance of Martin Luther King, Jr. Day.

Corporate earnings have been hit and miss so far this quarter, providing little impetus for stocks to add to last year's impressive gains.

Shares of United Parcel Service (UPS, Fortune 500) fell after the shipping company lowered fourth quarter earnings estimates due to a surge of last minute holiday orders. UPS took some heat late last year for failing to make deliveries in time for Christmas. Shares of rival FedEx (FDX, Fortune 500) fell slightly on the news as well.

Morgan Stanley (MS, Fortune 500)shares rose after the investment bank's earnings beat Wall Street estimates. The firm was the last of the six largest U.S. banks to post earnings. The majority of those banks surpassed analysts' expectations, but Wells Fargo (WFC, Fortune 500), JPMorgan Chase (JPM, Fortune 500), Citigroup (C, Fortune 500) and Bank of America (BAC, Fortune 500) all reported a sharp drop in mortgage activity due to higher interest rates.

General Electric (GE, Fortune 500) fell despite reporting a boost in quarterly earnings.

"$GE So let me get this straight... They crush the quarter and price goes down?," said StockTwits trader Luv2Ski217, who noted that he was bullish on the stock.

American Express (AXP, Fortune 500) spiked over 3% to an all-time high even though earnings missed estimates. The results did show a jump in consumer spending.

The stock also benefited from some notable analyst upgrades and optimism from the company's management on its earnings call. .

"$AXP miss earnings, who cares, upgrade anyway," quipped Cjcgoss78 on StockTwits.

$AXP Conference call positive.. Keeping costs down while expanding biz ," said Ghost22.

Intel (INTC, Fortune 500) shares sank more than 2% following earnings that missed expectations. Intel was one of the worst performers in CNNMoney's Tech 30 index.

"Intel's numbers left investors feeling less than enthusiastic about the group's outlook as the group expects no revenue growth in 2014," explained Ishaq Siddiqi, a market strategist at ETX Capital in London.

Shares of Electronic Arts (EA) surged more than 11% after an analyst upgrade and a report that the company will beat out its competitors for holiday video game sales. The stock was the top gainer in the Tech 30.

But one trader on StockTwits didn't understand why the stock was up so sharply.

"$EA Someone walk me thru why this is up so much? What am I missing here," said PProtector.

* China's growth expected to beat official targetsShares of Nu Skin (NUS) continued to fall. The stock has plunged over 40% since Wednesday after Chinese state media accused the beauty products marketer of running a pyramid scheme.

Herbalife (HLF), another multi-level marketer that has been accused by critics -- most notably hedge fund manager Bill Ackman -- of running a pyramid scheme, has dropped more than 13% on the Nu Skin news.

On the economic front, the Census Bureau released reports that showed new housing construction and building permits fell in December. The robust housing market has been a main driver of the economic recovery.

The main European indexes closed higher, while Asian markets mostly ended with losses.

4:40 pm: [BRIEFING.COM] The broader market ended the week on a down note, undercut by a spate of uninspiring earnings results and guidance from some widely-held companies that put a damper on the bullish sentiment seen in the middle of the week.

There were some buying efforts on Friday that controlled the fallout, but generally speaking there wasn't a lot of conviction among buyers with the exception of some specific stocks. Those exceptions tended to reside in the price-weighted Dow Jones Industrial Average, which outperformed the other major indices on Friday.

American Express (AXP 90.97, +3.19), which came up shy of consensus earnings estimates but spotlighted encouraging card member spending, was instrumental in the Dow's outperformance. It joined with Visa (V 232.18, +10.41) -- the highest-priced stock in the Dow -- to effectively account for all of the Dow's gains. Remarkably, 21 out of the 30 Dow components ended lower on Friday.

Intel (INTC 25.85, -0.69) and General Electric (GE 26.58, -0.62) were among the Dow laggards. Both companies reported their results for the fourth quarter, yet neither wowed investors. Intel missed by a penny and said it expected FY14 revenues to be approximately flat. GE was in-line with expectations and said things were improving, albeit in a mixed environment.

Morgan Stanley (MS 33.40, +1.40), which beat by eight cents, and Schlumberger (SLB 90.21, +1.60), which beat by two cents, enjoyed positive outings that provided a measure of support for the broader market and their respective sectors.

Be that as it may, every S&P 500 sector closed in the red on Friday. The energy sector (-0.05%) was the relative strength leader while the consumer staples sector (-0.8%) was the biggest laggard. The latter was afflicted by a big earnings warning out of Elizabeth Arden (RDEN 27.96, -6.54).

Other notable companies warning they expect to fall short of earnings expectations included Con-way (CNW 40.59, -0.81), Royal Dutch Shell (RDS.a 70.57, -1.17), and UPS (UPS 99.91, -0.58). The warning from UPS drew a lot of attention, yet the company came back nicely from a loss of more than three points during the day as investors seemed to warm to the notion that its shortfall was tied to the bad weather and the operational challenges of meeting increased demand during the holiday selling period.

The earnings news was the focal point throughout the day. There were some early economic releases, but they didn't have much bearing on today's proceedings. Overall, the economic news was good enough not to create any newfound concerns about the economic recovery.

December housing starts slipped 9.8% to an annualized rate of 999,000 units, but the two-month average for starts was the highest since March 2008.

Industrial production jumped 0.3%, which was the fifth consecutive month industrial production increased.

The preliminary reading for the University of Michigan Consumer Sentiment report for January dipped to 80.4 from 82.5, but the downturn wasn't enough to cause any real concerns

Today was an options expiration day, so volume was heavier than usual with 880 mln shares having traded at the NYSE versus 641 mln on Thursday.

For the week, the S&P 500 declined 0.2%, the Dow Jones Industrial Average gained 0.1%, and the Nasdaq Composite increased 0.6%.

As a reminder, the stock and bond markets will be closed on Monday in observance of Martin Luther King, Jr. Day.

Dow Jones Industrial Average -0.7% YTD

S&P 500 -0.5% YTD

Nasdaq Composite +0.5% YTD

Russell 2000 +0.4% YTD

3:30 pm: [BRIEFING.COM]

Precious metals traded higher today despite an advance by the dollar index. Feb gold rose to a session high of $1254.60 per ounce after trading as low as $1242.70 per ounce in early morning pit trade. It settled 1.0% higher at $1251.80 per ounce, booking a 0.4% gain for the week.

Mar silver lifted from a session low of $20.12 per ounce and peaked at $20.42 per ounce by late morning action. It eventually settled 1.2% higher at $20.30 per ounce, gaining 0.3% over the week.

Feb crude oil also traded in positive territory. It pulled back from a session high of $94.94 per barrel set at pit trade open to a session low of $93.94 per barrel. However, it quickly recovered back above the $94 per barrel level and settled with a 0.4% gain at $94.33 per barrel. Today's advance brought gains for the week to 1.8%.

Feb natural gas, on the other hand, spent today's floor trade in the red. It rallied to a session high of $4.39 per MMBtu after trading as low as $4.30 per MMBbt but lost momentum heading into the close and closed 1.4% lower at $4.33 per MMBtu. Despite the loss, natural gas gained 6.7% over the week.

3:00 pm: [BRIEFING.COM] Moving into the final hour of a three-day weekend, the market continues in a state it has existed in throughout today's trading: mixed.

One area of strength has been the US Dollar Index (DXY 81.27, +0.35) has risen 0.4%, largely at the expense of the euro, which has taken a 0.6% tumble against the dollar.

Despite the dollar's strength, dollar-based commodities have fared reasonably well. Crude oil (94.18, +0.22) is up 0.2%, gold (1252.00, +11.80) has risen close to 1.0%, and silver (20.31, +0.25) has jumped 1.3%.

2:30 pm: [BRIEFING.COM] The Dow Jones Industrial Average is up 72 points today. That's not bad, but it is interesting when one stops to consider that those gains have been forged entirely on the back of just 10 components.

That's right. There are just 10 Dow components sporting a gain at this time. Fortunately for the price-weighted Dow, a number of the ones that are up happen to be among the Dow's highest-priced issues: Visa (V 230.28, +8.51), IBM (IBM 190.57, +1.81), Goldman Sachs (GS 176.71, +1.54), Chevron (CVX 120.20, +1.37), United Technologies (UTX 144.42, +0.20), ExxonMobil (XOM 100.06, +1.12), and American Express (AXP 91.90, +4.12) to name just about all of the winners.

Outside the Dow, the broader market seems to be just running in place.

2:00 pm: [BRIEFING.COM] The indices are settling in at lower ranges without a lot of fanfare to speak of. The Nasdaq has been the laggard today with the likes of Apple (AAPL 543.54, -10.71), Google (GOOG 1152.29, -3.93), Cisco (CSCO 22.70, -0.08), Intel (INTC 25.64, -0.90), and LinkedIn (LNKD 221.32, -9.24) all backtracking.

Today's weakness notwithstanding, the Nasdaq is still on track for a winning week as it is currently up 0.72%.

Separately, comments from Richmond Fed President Lacker are hitting the wires. Mr. Lacker is not a voting FOMC member this year, but his views remain aligned with those expressed by others this week (i.e. Lockhart, Plosser, and Fisher) in that he believes the tapering should continue. Mr. Lacker added that recent data is far from what would be needed to change his view.

1:30 pm: [BRIEFING.COM] The market hit a bit of an air pocket in the last 30 minutes that made for a noticeable dip on an intraday chart that was tracking a pretty narrow trading range (hence, the noticeable dip). In any event, the S&P 500 has been pushed back further into negative territory, as has the Nasdaq.

The struggle for the broader market today is that it has lacked a strong cohort of leadership groups like we saw in the Tuesday-Wednesday rally. The best-performing area today is the energy sector (+0.4%), which is helping but is not exactly carrying the day.

On the downside, the consumer staples sector (-0.7%) is the biggest laggard as the big warning from Elizabeth Arden (RDEN 29.19, -5.31), and subsequent fallout, has provoked some valuation concerns for other richly-valued consumer staples companies.

1:00 pm: [BRIEFING.COM] Thus far, it has been one of those days in the stock market in which there is no strong sense of where things are headed. The broader action has been mixed, sector leadership is wanting, and the earnings results since yesterday's close have been mixed at best.

The Dow Jones Industrial Average has been the relative strength leader since the opening bell, bolstered by the strength in American Express (AXP 91.86, +4.08), which came up four cents shy of the S&P Capital IQ consensus EPS estimate, yet still had some good credit trends shine through beneath that headline.

Other widely-held names reporting their results included Morgan Stanley (MS 33.47, +1.47), which beat by eight cents, Schlumberger (SLB 90.03, +1.42), which beat by two cents, General Electric (GE 26.52, -0.68), which was in-line, Intel (INTC 25.77, -0.77), which missed by a penny, and Capital One (COF 73.00, -3.44), which missed by twelve cents.

Separately, Royal Dutch Shell (RDS.A 70.94, -0.80), Con-way (CNW 40.16, -1.25), Elizabeth Arden (RDEN 29.24, -5.26), and UPS (UPS 99.01, -1.48) all issued profit warnings. UPS was down more than three dollars earlier, but has pared some of those losses as investors recognize its shortfall had to do with weather and the operational challenges of meeting increased demand.

The earnings news for the most part has overshadowed today's economic data, which includes the Housing Starts, Industrial Production, and University of Michigan Consumer Sentiment reports.

From an economic standpoint, there was nothing alarming in those reports.

Starts were down 9.8% in December to an annualized rate of 999,000 units, yet that left the two-month average at its highest since March 2008.

Industrial production increased 0.3%, which was in-line with expectations, and the fifth consecutive monthly increase

Consumer sentiment dipped to 80.4 (Briefing.com consensus 83.0) from 82.5, but the deviation wasn't enough to cause a stir

Today is an options expiration day, so volume has been heavier than usual. 408 mln shares have traded at the NYSE versus 285 mln shares at this point yesterday.

12:30 pm: [BRIEFING.COM] The S&P 500 peeked its head above the unchanged mark a short time ago. The recovery from today's lows has brought the S&P 500 back to positive territory for the week (+0.2%), but it still remains down for the year (-0.1%).

Apple (AAPL 548.30, -5.95) is throwing its weight around today, acting as a drag on the broader market. It would be remiss not to mention that shares of AAPL had increased as much as 5% this week, so we suspect today's weakness is rooted in a profit-taking effort more than anything else.

The pounding Best Buy (BBY 25.20, -1.63) took yesterday, though, and the weakness in Intel (INTC 25.71, -0.83) today is likely prompting tech investors to reassess risk-reward dynamics with their holdings. That might help explain why the Nasdaq, which has been a standout this week (+1.0%), is acting a little sluggish today.

12:00 pm: [BRIEFING.COM] Call the stock market what you will, just don't call it too exciting at this point. Stocks are plodding along after an opening rush of activity related to the monthly options expiration.

The performance trend remains intact. Big moves today have been reserved for individual issues like American Express (AXP 91.77, +3.99) and Nu Skin (NUS 77.95, -6.85); otherwise, there isn't much wave action on either the sell side or the buy side.

The same narrative applies for the Treasury market, which has held in a very tight range close to the unchanged area throughout the cash session. The benchmark 10-yr note is currently up two ticks, which places it near the high for the day. Its yield has dipped to 2.838% versus 3.02% at the end of 2013.

11:25 am: [BRIEFING.COM] The Dow Jones Industrial Average has led the other major indices all day and it is still leading now. The relative strength there is lessening the selling pressure elsewhere as larger losses in the other indices have all been trimmed in conjunction with the Dow's advance.

At the moment, there are five sectors trading higher and five sectors trading lower. No sector, however, is up, or down, more than 1.0%. That mixed showing helps explain in part the fairly flat nature of the S&P 500 at this juncture.

Riding the strength of Schlumberger's (SLB 89.96, +1.35) earnings report and 28% increase in its quarterly dividend, the oil services stocks are faring well today and are an integral reason why the energy sector (+0.6%) leads all sectors.

11:00 am: [BRIEFING.COM] The major averages are mixed, but today's gold star goes so far to the Dow Jones Industrial Average. It has supplanted the Nasdaq in the outperformance ranks thanks to the big gain in American Express (AXP 93.03, +5.25) following its earnings report, and gains in other high-priced stocks like Goldman Sachs (GS 177.06, +1.89), IBM (IBM 189.98, +1.22), Chevron (CVX 119.86, +1.03), and Visa (V 223.76, +1.99).

It is perhaps not surprising to see the Dow assume some leadership. The broader market has found it difficult to find its way in 2014 and recent earnings/guidance disappointments have clouded the picture a bit. Accordingly, there has been a rotation into some of the more liquid and typically less volatile Dow components.

The broader market isn't doing much at this juncture, but its is worth noting that the heavily-weighted energy (+0.5%) and financial (+0.2%) sectors are exhibiting some relative strength.

10:30 am: [BRIEFING.COM] Commodities are mixed this morning with energy and metals almost all higher and agriculture futures mostly lower.

WTI crude oil sold off sharply this morning, erasing its gains as it dropped from the $94.94 HoD to the currently LoD of $93.94. Feb crude is currently +0.4% at $94.32/barrel.

Natural gas futures have been in the red all session so far and are now -0.9% at $4.34/MMBtu (Feb contract).

Metals are all trading higher excluding iron ore futures, which are down 0.5% at $129.71/ton. Aluminum rose 0.3% overnight on the London Metals Exchange. Back to domestics markets, gold, silver, copper, platinum and palladium are all higher.

Gold and silver gained steam over three hours ago and remain trading near session highs. Feb gold is now +0.7% at $1249/ioz, while Mar silver is +1.2% at $20.30/oz.

10:00 am: [BRIEFING.COM] Pinned down by a batch of disappointing earnings results/guidance from some widely-held companies, the major indices are finding it difficult in the early-going to establish upside traction. There are some individual standouts like American Express (AXP 92.23, +4.45) and Morgan Stanley (MS 32.95, +0.95), but for the most part, sector leadership is lacking.

The preliminary reading for the January University of Michigan Consumer Sentiment survey revealed a dip in sentiment to 80.4 (Briefing.com consensus 83.0) from 82.5 in December.

The initial market reaction to the Michigan number has been pretty muted.

9:40 am: [BRIEFING.COM] The opening bell rang and the major indices turned lower as expected. Each, however, has already shown some resilience to selling efforts in what could be a choppy day of trading given the mixed batch of earnings news.

UPS (UPS 97.62, -2.87) is an early laggard following its earnings warnings for FY13 and FY14. Intel (INTC 25.46, -1.08) is another luminary getting clipped early following a fourth quarter earnings report and outlook that investors apparently didn't regard too highly.

Intel's weakness is a drag on the Dow, as is the weakness in General Electric (GE 26.62, -0.58), which delivered in-line earnings results. Conversely, American Express (AXP 91.61, +3.83) is acting as an offset and is getting a pass despite coming up four cents shy of the S&P Capital IQ consensus EPS estimate for the fourth quarter.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: -2.50. Nasdaq futures vs fair value: -9.50. Just reported, December industrial production increased 0.3% which was in-line with the Briefing.com consensus. Meanwhile, capacity utilization hit 79.2% while the Briefing.com consensus called for a reading of 79.1%.

8:58 am: [BRIEFING.COM] S&P futures vs fair value: -1.80. Nasdaq futures vs fair value: -8.00. Markets across Asia ended mostly lower as trade slipped following some disappointing earnings reports on Wall Street. News and data was mostly absent, limited to the Japanese government upped its economic assessment for the first time in four months.

Japan's Nikkei (-0.1%) slipped amid a lackluster trade. Mitsubishi Motors was a notable outperformer, surging 10.1% as traders covered their short bets.

Hong Kong's Hang Seng (+0.6%) outperformed despite selling off into the close. Casino stocks led the way as Galaxy Entertainment jumped 5.3% and Sands China rallied 3.5%. Recent outperformer Lenovo slumped 4.0% as traders booked profits.

China's Shanghai Composite (-0.9%) posted its lowest close in over five months as worries over the onslaught of IPOs set to hit the market persist. Neway Valve jumped 43.4% during today's debut.

The major European bourses hover little changed. A quiet day for data saw U.K. retail sales blow past estimates (2.6% MoM actual v. 0.5% MoM expected) while France's budget deficit widened to EUR87.0 bln (EUR80.0 bln expected, EUR86.1 bln previous). Making headlines were comments from French President Francois Hollande, suggesting the euro is too high.

Britain's FTSE trades flat as some recent selling has wiped away the early gains. Royal Dutch Shell trades down 2.2% after lowering its guidance.

Germany's DAX is up 0.1% amid a

y trade. Utilities lag as RWE and E.ON trade down 2.0% and 0.7%, respectively.

France's CAC is unchanged as trade has dipped back to the flat line. Automaker Renault sports a gain of 2.9% as momentum carries over from yesterday's strong monthly sales report.

8:35 am: [BRIEFING.COM] S&P futures vs fair value: -1.80. Nasdaq futures vs fair value: -7.80. Housing starts hit an annualized rate of 999,000 units during December, which is above the 986,000 expected by the Briefing.com consensus. November starts were revised up to reflect an annualized rate of 1,107,000 starts (from 1,091,000). As for building permits, they fell to 986,000 from the prior month's revised rate of 1,017,000 (from 1,007,000). That was below the pace of 1,000,000 that had been expected among economists polled by Briefing.com.

8:01 am: [BRIEFING.COM] S&P futures vs fair value: +0.20. Nasdaq futures vs fair value: -3.00. The S&P futures are up four points, which leaves them roughly in-line with fair value on this options expiration day. The indication follows a spate of earnings results from widely-held companies and a positive disposition seen currently in most European markets.

Reviewing overnight developments:

Asian markets were mostly weak, although losses were generally held under 1.0%. Japan's Nikkei -0.1%; China's Shanghai Composite -0.9%; Hong Kong's Hang Seng +0.6%; South Korea's Kospi -0.7%.

Economic data was limited:

Japan's Household Confidence declined to 41.3 from 42.5 (43.4 expected).

In news:

Reuters reports that the People's Bank of China said it will use various liquidity management tools in a flexible way and improve the system to appropriately adjust liquidity in order to maintain reasonable growth in credit and social financing

Major European indices are higher. Germany's DAX +0.2%; the UK's FTSE 100 +0.1%; France's CAC 40 +0.2%.

Participants received several economic data points:

Great Britain's Retail Sales surged 2.6% month-over-month (0.4% forecast, 0.1% prior) while the annualized reading pointed to an increase of 5.3% (2.6% forecast, 1.8% last). Also of note, core Retail Sales jumped 2.8% month-over-month (0.3% expected, 0.2% last) while the year-over-year reading indicated an increase of 6.1% (3.2% consensus, 2.1% prior).

French government budget deficit widened to EUR87.0 billion from EUR86.10 billion (EUR80.00 billion deficit expected).

Swiss PPI was unchanged month-over-month (0.1% consensus, -0.1% prior) while the year-over-year reading reflected a decrease of 0.4% (-0.5% forecast, -0.4% last).

Among news of note:

Bloomberg discusses that the EU is considering a ban on proprietary trading for the largest banks from 2018

Standard & Poor's revised its credit outlook for Portugal to Negative from CreditWatch Negative. Its current rating of 'BB' was affirmed.

In U.S. corporate news:

Intel (INTC 25.53, -1.01) is trading 3.8% after missing the fourth quarter S&P Capital IQ consensus EPS estimate by a penny and noting that it expects FY14 revenue to be approximately flat

American Express (AXP 88.99, +1.21) is up 1.4% despite coming up four cents shy of the S&P Capital IQ consensus EPS estimate for the fourth quarter

General Electric (GE 26.90, -0.30) is off slightly after the company posted an in-line fourth quarter profit and noted backlog of equipment and services is at a record high $244 bln

Morgan Stanley (MS 32.68, +0.68) is trading higher after beating the fourth quarter consensus EPS estimate by eight cents on a 12.4% jump in revenue

Schlumberger (SLB 89.35, +0.74) is getting a boost after topping the S&P Capital IQ consensus EPS estimate by two cents and announcing a 28% increase in its quarterly dividend

Sprint (S 9.27, +0.19) is moving up following reports it has gotten financing proposals from banks for a T-Mobile (TMUS) bid

December Housing Starts and Building Permits will be released at 8:30 ET while December Industrial Production and Capacity Utilization will be reported at 9:15 ET. The day's data will be topped off with the 9:55 ET release of the preliminary University of Michigan Sentiment survey for January.

6:15 am: [BRIEFING.COM] S&P futures vs fair value: +1.50. Nasdaq futures vs fair value: +1.00.

6:15 am: [BRIEFING.COM] Nikkei...15734.46...-12.70...-0.10%. Hang Seng...23133.35...+146.90...+0.60%.

6:15 am: [BRIEFING.COM] FTSE...6828.21...+12.80...+0.20%. DAX...9775.93...+59.50...+0.60%.

S&P 500 Falls as GE, Intel Earnings Disappoint Investors By Lu Wang and Callie Bost Jan 17, 2014 4:45 PM ET

Most U.S. stocks retreated, dragging the Standard & Poor’s 500 Index lower for the week, as earnings from companies including General Electric (GE) Co. to Intel Corp. disappointed investors.

General Electric lost 2.3 percent as margins at its manufacturing units fell short of projections. Intel dropped 2.6 percent as its revenue forecast raised concern the personal-computer market is struggling to grow. United Parcel Service Inc. slid 0.6 percent as it projected earnings below analysts’ estimates. American Express Co. climbed 3.6 percent after reporting fourth-quarter profit doubled.

The S&P 500 (SPX) fell 0.4 percent to 1,838.70 at 4 p.m. in New York. The Dow Jones Industrial Average rose 41.55 points, or 0.3 percent, to 16,458.56 as American Express and Visa Inc. surged. Markets will close on Jan. 20 for the Martin Luther King Jr. Day holiday.

“Investors are taking cues from earnings releases,” Jim Russell, who helps oversee $113 billion as a senior equity strategist for U.S. Bank Wealth Management, said by phone. “Just as important as fourth-quarter earnings are, many investors are watching for company guidance for signs on what early 2014 will bring. This year, we’ll see a tearing between winners and losers and we’ve seen that in this earnings season so far.”

Atlanta-based UPS expects to report an adjusted profit of $4.57 a share for 2013, below... Read More

U.S. stocks fell yesterday, dragging the S&P 500 from a record, as Best Buy Co. tumbled after holiday sales declined and earnings at companies from Citigroup Inc. to CSX Corp. disappointed investors. The benchmark gauge is down 0.5 percent this year after jumping 30 percent in 2013 for the biggest annual gain since 1997.

Five-Year RallyAbout 6.9 billion shares changed hands on U.S. exchanges today amid the expiration of options contracts, 13 percent higher than the three-month average. About three stocks fell for every two that rose.

A five-year rally that lifted the S&P 500 up more than 170 percent from a bear-market low has boosted equity valuations to near the highest level since 2009. The S&P 500 trades at 15.6 times the estimated earnings of its members, more than the five-year average multiple of 14.1, data compiled by Bloomberg show.

Seven companies in the S&P 500 including General Electric and Morgan Stanley (MS) reported financial results today. Per-share profit for companies in the benchmark probably climbed 6 percent in the fourth quarter, while sales increased 2 percent, according to analysts surveyed by Bloomberg.

“The market just can’t seem to get going this year,” Wayne Wilbanks, chief investment officer at Wilbanks, Smith & Thomas Asset Management LLC in Norfolk, Virginia, which oversees $2.4 billion, said in a phone interview. “Earnings are OK, but for the market to go much higher, earnings are going to have to be really good.”

Economic DataReports today showed mixed data on the economy, with industrial production rising for a fifth month in December while the Thomson Reuters/University of Michigan preliminary January index of consumer sentiment unexpectedly fell.

The pace of U.S. home construction dropped less than forecast in December, capping the best year for the industry since 2007.

The Chicago Board Options Exchange Volatility Index (VIX) dropped 0.7 percent today to 12.44. The gauge of S&P 500 options known as the VIX is down 9.3 percent this year.

All 10 industry groups in the S&P 500 slipped as consumer-staples, technology and industrial companies fell more than 0.5 percent to lead the retreat.

GE MarginsGeneral Electric slipped 2.3 percent to $26.58. The company reported operating earnings per share in line with analyst estimates. Profit margins at the manufacturing divisions expanded 60 basis points, according to a presentation posted on GE’s website. That fell short of guidance for 70 basis points of growth that Chief Executive Officer Jeffrey Immelt first laid out in December 2012 and affirmed as recently as last month.

Intel erased 2.6 percent to $25.85. The world’s largest maker of computer chips forecast first-quarter revenue that may fall short of some analysts’ estimates as corporate demand fails to reignite personal-computer sales. Consumer notebook demand is declining in Asia, Chief Executive Officer Brian Krzanich said.

UPS (UPS) dropped 0.6 percent to $99.91 after the shipping company projected fourth-quarter earnings that trailed analysts’ estimates. A surge of packages from online shopping just before Christmas forced the company to hire more temporary workers than planned and miss holiday deliveries.

SLM Corp. lost 9.8 percent, the most in the S&P 500, to $24.47. The student lender known as Sallie Mae reported a fourth-quarter profit decline of 22 percent.

Bank EarningsCapital One Financial Corp. fell 5.3 percent to $72.39. The credit-card lender said fourth-quarter profit missed some analysts’ estimates as expenses came in higher than estimated.

American Express (AXP) climbed 3.6 percent to a record $90.97. The biggest credit-card issuer by purchases benefited from a pickup in household wealth and consumer confidence that has propelled card purchases. Sanford C. Bernstein & Co. raised its profit estimates.

Visa, the world’s biggest bank-card network, jumped 4.7 percent to $232.18, also a record. AmEx and Visa added a combined 87 points to the Dow today.

Morgan Stanley added 4.4 percent to $33.40. The owner of the world’s largest brokerage reported profit that beat analysts’ estimates as equity-trading revenue increased and earnings from wealth management climbed to a record.

Electronic Arts Inc. jumped 12 percent to $24.10 for the biggest increase in the S&P 500. The second-largest U.S. video-game maker was rated buy in new coverage by CRT Capital Group LLC. Separately, U.S. spending on video-game hardware surged to its highest in three years in December, according to Port Washington, New York-based NPD Group Inc.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage