Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

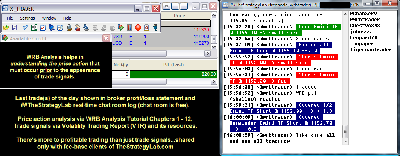

Attachment:

010314-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+820.00.png [ 175.59 KiB | Viewed 299 times ]

010314-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+820.00.png [ 175.59 KiB | Viewed 299 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$800.00 dollars or +8.00 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$20.00 dollars or +0.20 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $820.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1690 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

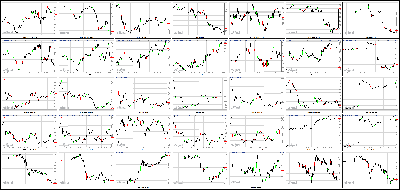

Stocks Off To A Lackluster Start In 2014 Attachment:

010314-Key-Price-Action-Markets.png [ 521.39 KiB | Viewed 334 times ]

010314-Key-Price-Action-Markets.png [ 521.39 KiB | Viewed 334 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

It's only two days into 2014 for investors. But so far, it's looking nothing like 2013. After kicking off the new year with a loss, stocks ended Friday mixed.

The Dow rose slightly while the S&P 500 and Nasdaq finished lower again, adding to Thursday's 1% declines.

Volume remained low Friday, as a major snowstorm in the Northeast kept traders away at the end of the holiday-shortened week.

Though the broader market's moves were relatively muted, Twitter (TWTR) shares continued to surge. The social media company's stock was up more than 2%, following a 6% jump on Thursday.

With the significant run-up, some traders on StockTwits wondered if Twitter shares may be due for a pullback soon.

"$TWTR Is it time to short this yet?" asked Howyodoing. "My goodness what a run."

"$TWTR If this makes it to 70 its going to get slammed," predicted MTPennybags.

* Video - Twitter is halfway to $140 While Twitter was soaring, tech giant Apple (AAPL, Fortune 500) continued to lose ground for a second day. Some traders speculated that activist investor Carl Icahn, who took a position in the company last year and has been pushing for a big buyback, may be unloading some shares.

"$AAPL I hope that was Icahn selling," said afernandez321. "Lets get rid of him. Now lets move on."

StockTwits user StrayTrader said it certainly smells like a large institutional investors is selling shares of Apple, but even if that's the case, he stressed that "there are plenty of us who believe in it."

"$AAPL Patience is the key, everybody knows Apple is the #1 smartphone maker in the world," added OwensInvestmentgroup. "Care less about a down day. Bullish."

Shares of T-Mobile (TMUS) were sharply lower after rival AT&T (T, Fortune 500) said it would offer up to $450 to customers who switch from T-Mobile.

Car makers were also in focus as they announced sales figures for December.

Shares of General Motors (GM, Fortune 500) and Toyota (TM) were lower after they all reported weaker December sales than expected. But Ford (F, Fortune 500) shares rose a bit.

Chrysler reported strong sales for December, and a full-year sales increase of 9%.

Sales have been strong across the auto industry in 2013, with automakers selling more than 15 million vehicles in the U.S. -- their best year since 2007.

European markets were higher while major Asian markets ended in the red, with Hong Kong's Hang Seng dropping by 2.2%. Markets in Shanghai and Tokyo were closed for an extended new year break.

4:10 pm: [BRIEFING.COM] The major averages wrapped up the week on a mixed note as the Dow Jones Industrial Average added 0.2% while the Nasdaq shed 0.3%. For its part, the S&P 500 ended flat.

Today's mixed finish was an appropriate reflection of a session that featured some mixed signals. On that note, seven of ten sectors ended in the red but market breadth remained positive throughout the trading day. In all likelihood, light volume played a part as some participants were kept away by the winter storm that has encompassed the Northeast. At the end of the day, only 533 million shares changed hands on the NYSE floor.

Stocks began the session on an upbeat note, but the Nasdaq was quick to slip from its early high. The index was pressured by its largest component, Apple (AAPL 540.98, -12.15), which lost 2.2%. Biotechnology also weighed on the Nasdaq as the iShares Nasdaq Biotechnology ETF (IBB 226.03, -1.06) shed 0.5%. The health care sector; however, outperformed with a gain of 0.2%.

The S&P 500 followed in the footsteps of the Nasdaq in the early afternoon, but the indices diverged once again during the final hour when the S&P 500 made an unsuccessful run at its opening high.

Seven sectors posted losses while financials (+0.6%), health care (+0.2%), and industrials (+0.3%) spent the entire session in the green.

Notably, the financial sector was underpinned by large banks as Bank of America (BAC 16.41, +0.31), Citigroup (C 53.40, +1.13), and JPMorgan Chase (JPM 58.66, +0.45) all gained between 0.8% and 2.2%.

Elsewhere, gains in the industrial sector were paced by airlines. Delta Air Lines (DAL 29.23, +1.53) and United Continental (UAL 39.95, +2.22) soared 5.5% and 5.9%, respectively, while the broader Dow Jones Transportation Average added 0.5%.

Switching gears, the commodity market saw a replay of Thursday as oil fell while gold rallied. Crude oil slid 1.6% to $93.96/bbl while gold futures advanced 1.1% to $1238.40/ozt.

Treasuries ended little changed with the 10-yr yield at 2.99%.

On Monday, November Factory Orders and the December ISM Services Index will both be reported at 10:00 ET.

Related Stories

Stocks Mostly Little Changed; China Lodging Gains Investor's Business Daily

Stocks Hold Near Session Highs; NQ Mobile Adds To Gains Investor's Business Daily

How the Dow Jones industrial average did Thursday Associated Press

Stocks Open Mostly Lower; 3M Rises, Herbalife Pares Gains Investor's Business Daily

U.S. stocks rise; Dow aims for 51st record close MarketWatch

Russell 2000 -0.6% YTD

DJIA -0.6% YTD

S&P 500 -0.9% YTD

Nasdaq -1.1% YTD

Week in Review: Shaky Start to 2014

Monday's session did not generate much excitement as the S&P 500 ended flat after spending the entire trading day inside of a four-point range. Interestingly, while the S&P 500 was challenged by its flat line throughout the session, the Dow Jones Industrial Average held just above its unchanged level for the duration of the day. The price-weighted Dow saw 19 of its 30 components finish in the green, but shares of Disney (DIS 76.11, -0.16) stood out with a 2.5% gain. The noteworthy strength ensued after Guggenheim upgraded the stock to 'Buy' from 'Neutral.'

On Tuesday, the major averages wrapped up a memorable year with a forgettable final session. The S&P 500 added 0.4%, extending its 2013 price return to 29.6%. Given its banner year, it was appropriate for the index to end 2013 at a fresh all-time high of 1848.35. The Dow Jones Industrial Average soared 26.5% in 2013 and ended at a record high of its own. Although the Dow (+0.4%) and S&P 500 (+0.4%) saw comparable gains on Tuesday, the Nasdaq (+0.5%) fared a bit better. That was the theme throughout the year as the tech-heavy index rallied 38.3%.

Bond and equity markets were closed on Wednesday for New Year's Day.

On Thursday, the S&P 500 exhibited a bit of a hangover in its first session of 2014. The benchmark index fell 0.9% as all ten sectors registered losses. Stocks were pressured from the opening bell as cautious action in Europe weighed on the early sentiment. In all likelihood, the slide caught a number of participants off guard given the understanding that the first few days of a new year are known to have a favorable bias with inflows into IRA accounts, bonus money being put to work, and new money coming off the sidelines. That did not happen today as sellers maintained control throughout the trading day. Energy (-1.3%), industrials (-1.3%), and technology (-1.1%)-slipped behind the broader market at the open and their underperformance weighed for the remainder of the session.

3:30 pm: [BRIEFING.COM] Feb crude oil fell below the $94 level, extending losses for a fourth consecutive session, as inventory data and a slightly stronger dollar index weighed on prices. Although crude oil inventories fell by 7 mln barrels when a smaller draw of 2.9 mln was expected, distillate inventories showed a build of 5 mln, which was much higher than the anticipated build of 0.8-1.2 mln. The energy component retreated from its session high of $95.40 per barrel and eventually settled 1.6% lower at $93.96 per barrel.

Feb natural gas slipped to a session low of $4.21 per MMBtu following inventory data that showed a draw of 97 bcf vs expectations for a draw of 115-126 bcf. It gained momentum and rose into positive territory by late morning pit trade. It touched a session high of $4.39 per MMBtu but reversed back into negative territory in the last half hour of pit trade and settled with a 0.5% loss at $4.30 per MMBtu.

Feb gold extended yesterday's gains despite the slightly stronger dollar index. The yellow metal trended higher after lifting from its session low of $1226.00 per ounce set just after floor trade opened. It brushed a session high of $1239.60 per ounce and settled at $1238.40 per ounce, or 1.1% higher.

Mar silver opened today's session in the red, with prices falling to a session low of $20.00 per ounce. However, it found buying support and broke into positive territory not long after equity markets opened. Silver eventually settled 0.3% higher at $20.20 per ounce.

3:00 pm: [BRIEFING.COM] The S&P 500 (+0.2%) has climbed to a fresh afternoon high as the last session of the week enters its final hour. Should the current standing hold, the S&P 500 will finish the abbreviated week with a loss of 0.4%. The tech-heavy Nasdaq is also on track to register a weekly loss (-0.4%) while the Dow has held up a bit better. The price-weighted index is higher by 0.1% this week.

Elsewhere, Treasuries have inched their way back into positive territory. The 10-yr note is higher by one tick with its yield hovering at 2.99%. For the week, the benchmark yield is on pace to register a loss of two basis points.

2:30 pm: [BRIEFING.COM] The major averages remain near their flat lines as the quiet afternoon continues. Investors did not receive any economic data today, but a handful of noteworthy reports will cross the wires next week.

On Monday, November Factory orders and the December ISM Services Index will both be released at 10:00 ET, but neither data point is expected to be met with a significant reaction in equities. Tuesday's data will be limited to the November Trade Balance while the FOMC Minutes from the December meeting will be released at 14:00 ET.

Finally, on Friday morning, everyone's attention will be turned to the December nonfarm payrolls report, which will be released at 8:30 ET.

2:00 pm: [BRIEFING.COM] Not much has changed since our last update as the Nasdaq (-0.3%) and S&P 500 (-0.1%) remain near their lows. Meanwhile, the Dow Jones Industrial Average (+0.1%) continues to outperform, but it too hovers near its session low.

The broader market is sending some mixed signals as seven of ten sectors sit in the red yet market breadth remains tilted to the upside with advancing issues on the NYSE outpacing decliners by a 1.3:1 ratio.

Trading volume; however, is sending a clear signal of limited participation. With two hours left in today's session only 273 million shares have changed hands on the NYSE floor.

1:25 pm: [BRIEFING.COM] Some mixed action in the broader market as neither buyers nor sellers have shown much conviction. That is owed in part to the relatively low participation stemming from the Northeast snowstorm and what we would call a wait-and-see stance in front of Monday's session when trading desks should be fully staffed again following the holidays.

Today marks the end of the "so-called "Santa Claus rally" period, which covers the last five trading days of the prior year and the first two of the new year. Entering today's session, the S&P 500 is up 0.2% in that span.

Trading lore penned in the Stock Trader's Almanac suggests Santa's failure to call (i.e. a negative return over the period) tends to precede bear markets or times stocks could be purchased at much lower prices later in the year. No two years are alike of course, yet that idea will get some added press over the weekend and early next week if we have another dip today that leads Santa astray.

1:00 pm: [BRIEFING.COM] At midday, equity indices trade in mixed fashion. The Nasdaq (-0.2%) holds a modest loss while the Dow Jones Industrial Average outperforms with a slight gain of 0.2%. For its part, the S&P 500 trades flat.

Generally speaking, today's session has been quiet with only 234 million shares traded at the New York Stock Exchange through the first half of action. The light participation is understandable considering some used the Wednesday closure to extend their weekends while others were kept away by the major snowstorm on the East Coast.

Equities began the session on an upbeat note, but the Nasdaq slipped behind the S&P 500 during the first hour. The tech-heavy index then slipped into the red while the broader market followed the slide with a retreat of its own.

The Nasdaq has been pressured by Apple (AAPL 543.55, -9.58), which trades lower by 1.7%. The largest tech component is registering its second consecutive loss as it nears its 50-day moving average (540.36). Due to Apple's weakness, the technology sector (-0.4%) is the weakest performer among cyclical groups.

In addition, the Nasdaq has to contend with underperformance among biotechnology as the iShares Nasdaq Biotechnology ETF (IBB 225.82, -1.27) trades lower by 0.6%. Despite biotech's weakness, the health care sector (+0.3%) sports a modest gain.

Outside of health care, only two groups-financials (+0.6%) and industrials (+0.3%)-continue to hold gains. The industrial sector has received significant support from airlines as Delta Air Lines (DAL 29.19, +1.49), JetBlue (JBLU 9.03, +0.43), and United Continental (UAL 38.40, +1.67) hold gains between 4.4% and 5.3% while the broader Dow Jones Transportation Average trades higher by 0.5%.

12:30 pm: [BRIEFING.COM] The major averages remain near their lows as the quiet session continues. On that note, only 218 million shares have changed hands on the floor of the New York Stock Exchange so far, which is understandable considering the East Coast has had to contend with a major snowstorm.

Interestingly, today's equity weakness has coincided with dollar strength as the Dollar Index (+0.2% at 80.78) looks to post its third advance in a row. The greenback has shown noteworthy strength against the euro, gaining nearly 200 pips versus the single currency since yesterday. Currently, the euro/dollar pair sits near its session low at 1.3600.

Despite today's gains in the dollar, dollar-denominated gold futures hover near their highs, up 1.0% at $1237.10/ozt.

12:00 pm: [BRIEFING.COM] The Nasdaq (-0.4%) and S&P 500 (-0.1%) remain in the red while the Dow Jones Industrial Average outperforms with a slight gain of 0.1%. Thirteen index components trade in positive territory with Goldman Sachs (GS 177.77, +0.88), IBM (IBM 186.19, +0.66), Johnson & Johnson (JNJ 91.66, +0.63), and United Technologies (UTX 112.94, +0.45) contributing to the relative strength of the price-weighted index.

On the downside, only two index components, Microsoft (MSFT 36.76, -0.40) and Verizon (VZ 48.36, -0.65) display losses larger than 1.0%.

Elsewhere, Treasuries remain confined to a narrow range as the 10-yr yield trades higher by one basis point at 3.00%.

11:30 am: [BRIEFING.COM] Recent action saw the S&P 500 return to its flat line while the Nasdaq (-0.2%) slipped to a fresh session low. As a result of the recent move, only four sectors continue to trade in positive territory.

Outside of energy (-0.2%) and technology (-0.4%), the remaining cyclical groups continue to hold up relatively well as financials and industrials display respective gains of 0.5% and 0.3%. Notably, the industrial sector is receiving considerable support from airlines. Delta Air Lines (DAL 28.77, +1.07), JetBlue (JBLU 8.83, +0.23), and United Continental (UAL 38.87, +1.14) hold gains between 2.7% and 3.8% while the broader Dow Jones Transportation Average trades higher by 0.5%.

10:55 am: [BRIEFING.COM] The S&P 500 (+0.2%) remains just below its session high, but the Nasdaq (-0.1%) has now slipped into the red. The tech-heavy index has lagged since the open with shares of Apple (AAPL 545.93, -7.20) contributing to the weakness.

The Nasdaq has also had to contend with a reversal in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 226.39, -0.70) is lower by 0.3% after starting the session on an upbeat note. Despite the weakness in biotech, the health care sector (+0.4%) continues to outperform. The remaining countercyclical groups are mixed as consumer staples (+0.2%) trade in-line with the S&P 500 while telecom services (-0.5%) and utilities (-0.2%) lag.

10:35 am: [BRIEFING.COM] Commodities are mixed this morning while the dollar index trades slightly higher.

Feb gold has been in positive territory so far, rising to a pit session high of $1234.90 in recent action. It is currently up 0.7% at $1234.00.

Mar silver lifted from its session low of $20.00 set in early morning floor action and recently broke into positive territory. It is now unchanged at $20.13.

Feb crude oil continues to chop around in negative territory. It managed to brush a session high of $95.40 moments after floor trade opened but dipped below the $95 level in recent action. It is currently trading at $94.81, or 0.7% lower ahead of inventory data to be released at 11:00am ET.

Feb natural gas sold off further into the red and to a new session low of $4.21 following a smaller-than-anticipated draw in inventories. It is now down 2.3% at $4.22.

9:55 am: [BRIEFING.COM] The S&P 500 (+0.3%) has padded its opening gain, but the tech-heavy Nasdaq (+0.1%) has slipped behind the benchmark index as Apple (AAPL 547.81, -5.32) weighs. The largest Nasdaq component trades lower by 1.0%, which marks its second consecutive decline.

Elsewhere, the broader technology sector (-0.1%) is also feeling Apple's weight. Chipmakers have not done much to offset Apple's losses as the PHLX Semiconductor Index trades lower by 0.2%. Index component Micron (MU 21.14, -0.52) trades lower by 2.4% after RBC Capital Markets downgraded the stock to 'Sector Perform' from 'Outperform.'

Outside of technology, only two other groups-telecom services (-0.8%) and utilities (-0.4%)-hover in the red. Notably, the utilities sector is being pressured by Exelon (EXC 26.52, -0.65) and FirstEnergy (FE 31.80, -0.58). The two stocks hold respective losses of 2.4% and 1.7% after both received downgrades.

9:45 am: [BRIEFING.COM] Equities registered opening gains with the Russell 2000 (+0.5%) leading the early charge. Meanwhile, the S&P 500 trades higher by 0.3% with nine of ten sectors displaying early gains.

Cyclical energy (+0.4%) and industrials (+0.6%) have climbed into an early lead after pacing yesterday's retreat. In addition, health care (+0.4%) has also played a part in the opening advance.

There hasn't been much movement in the Treasury market so far as the 10-yr note holds a slim loss with its yield up one basis point at 3.00%.

9:13 am: [BRIEFING.COM] S&P futures vs fair value: +2.60. Nasdaq futures vs fair value: +0.70. The major averages are expected to register modest opening gains as index futures hover near their pre-market highs. The S&P 500 futures trade three points above fair value as the benchmark index will look to rebound from yesterday's 0.9% decline that saw all ten sectors finish in negative territory.

Today's participation is expected to be on the light side due to the winter storm that has paralyzed much of the Northeast. However, low volume should not be surprising to participants that have taken part in the past several sessions. So far this week, trading volume has ranged from 452 million (Monday) to 612 million (Thursday), with each total coming in well below the 200-day average of 716 million.

Treasuries hold modest losses with the 10-yr yield up one basis point at 3.00%.

8:54 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +1.70. The S&P 500 futures continue to hover near their pre-market highs.

Markets across Asia ended lower as trade piggybacked the action on Wall Street. A disappointing Chinese Non-Manufacturing PMI number (54.6 actual versus 56.0 previous) led to underperformance both in Hong Kong and in Shanghai.

In other news of note, Indian Prime Minister Manmohan Singh announced he would relinquish his leadership role if his Congress Party wins this summer's election. Separately, Reserve Bank of India Governor Raghuram Rajan suggested interest rates will remain elevated as long as inflation crimps growth.

Japan's Nikkei was closed.

Hong Kong's Hang Seng fell 2.2%, posting its biggest drop in six months. Coal-related names remained under pressure due to the elevated pollution levels in major cities. China Shenhua Energy lost another 4.4% after analysts warned on the space.

China's Shanghai Composite lost 1.2%, pushing lower for a second session with shares ending just off four-month lows. Financials lagged with Bank of China giving up 1.9%.

Major European indices hover near their best levels of the session with Italy's MIB (+1.1%) paving the way. Investors received several economic data points this morning. Eurozone private loans declined 2.3% year-over-year (-2.1% expected, -2.2% prior) while M3 money supply grew 1.5% year-over-year, as expected (1.4% prior). Great Britain's BoE Consumer Credit expanded to GBP630 million from GBP450 million (GBP700 million expected) while mortgage approvals increased by 71,000 (69,000 expected, 68,000 previous). Separately, Construction PMI fell to 62.1 from 62.6 (62.0 forecast) while Nationwide HPI increased 1.4% month-over-month (0.7% expected, 0.7% prior). Elsewhere, Italy's CPI ticked up 0.2% month-over-month (0.3% expected, -0.3% prior) while the year-over-year reading rose 0.7% (0.8% consensus, 0.7% previous). Also of note, Spain's number of unemployed fell by 107,600 (+20,000 expected, -2,500 last).

Among news of note, according to the draft of the German annual economic report, the government does not plan to increase taxes at this time.

Great Britain's FTSE is higher by 0.3% with consumer names in the lead. Next trades up 9.2% after issuing an upbeat profit forecast. Peer Marks & Spencer Group is higher by 4.4%. On the downside, miners Antofagasta and Glencore Xstrata trade lower by 0.4% and 1.1%, respectively.

In Germany, the DAX holds an advance of 0.4%. ThyssenKrupp and K+S lead with both names displaying gains close to 2.0% apiece. Software company SAP underperforms with a loss of 0.5%.

France's CAC trades higher by 0.6% as defensive names lead. Electricite de France and Veolia Environnement hold respective gains of 1.6% and 1.5%.

In Italy, the MIB trades up 1.1%. Telecom Italia leads with a gain of 6.3% amid reports the company's largest owner plans to sell its Brazilian subdivision.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: +3.80. Nasdaq futures vs fair value: +3.70. U.S. equity futures continue to hover near their pre-market highs with the S&P 500 futures up four points against fair value. A subdued session is expected to finish out the holiday-shortened week with many participants kept away by the winter storm that has blanketed the Northeast.

There isn't much in the way of economic or company-specific news this morning. With that in mind, a handful of names are moving in reaction to analyst comments. Utility providers Exelon (EXC 26.83, -0.34) and FirstEnergy (FE 32.00, -0.38) are both down near 1.2% after receiving downgrades. Citigroup downgraded both Exelon and FirstEnergy while Exelon was also downgraded to 'Underperform' at Bank of America/Merrill Lynch.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +2.30. Nasdaq futures vs fair value: +3.70. U.S. equity futures hover near their pre-market highs. The S&P 500 futures trade two points above fair value.

Reviewing overnight developments:

Asian markets ended lower. China's Shanghai Composite -1.2%, Hong Kong's Hang Seng -2.2%, and Japan's Nikkei was closed.

Economic data was limited:

China's Non-manufacturing PMI fell to 54.6 from 56.0.

In news:

The decline in China's Non-manufacturing PMI came one day after the Manufacturing PMI also pointed to a slowdown in growth as the reading fell to 51.0 from 51.4 (51.2 expected).

According to a survey conducted by Kyodo News, less than 20% of large Japanese companies plan to raise wages in 2014.

Major European indices hover near their best levels of the session. Great Britain's FTSE +0.1%, Germany's DAX +0.4%, and France's CAC +0.6%. Elsewhere, Spain's IBEX +0.5% and Italy's MIB +1.1%.

Investors received several economic data points:

Eurozone private loans declined 2.3% year-over-year (-2.1% expected, -2.2% prior) while M3 money supply grew 1.5% year-over-year, as expected (1.4% prior).

Great Britain's BoE Consumer Credit expanded to GBP630 million from GBP450 million (GBP700 million expected) while mortgage approvals increased by 71,000 (69,000 expected, 68,000 previous). Also of note, Construction PMI fell to 62.1 from 62.6 (62.0 forecast) while Nationwide HPI increased 1.4% month-over-month (0.7% expected, 0.7% prior).

Italy's CPI ticked up 0.2% month-over-month (0.3% expected, -0.3% prior) while the year-over-year reading rose 0.7% (0.8% consensus, 0.7% previous).

In Spain, the number of unemployed fell by 107,600 (+20,000 expected, -2,500 last).

Among news of note:

According to the draft of the German annual economic report, the government does not plan to increase taxes at this time.

In U.S. corporate news:

Exelon (EXC 26.70, -0.47): -1.7% following downgrades at Bank of America/Merrill Lynch and Citigroup.

Micron (MU 21.30, -0.36): -1.7% after RBC Capital Markets downgraded the stock to 'Sector Perform' from 'Outperform.'

7:13 am: [BRIEFING.COM] S&P futures vs fair value: +0.70. Nasdaq futures vs fair value: +0.20.

7:13 am: [BRIEFING.COM] Nikkei...Holiday......... Hang Seng...22817.28...-522.80...-2.20%.

7:13 am: [BRIEFING.COM] FTSE...6721.37...+3.50...+0.10%. DAX...9425.36...+25.30...+0.30%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage