Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

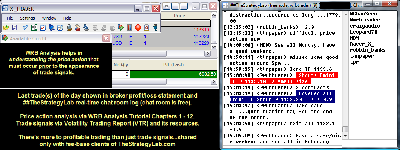

Attachment:

013114-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6082.50.png [ 173.6 KiB | Viewed 557 times ]

013114-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6082.50.png [ 173.6 KiB | Viewed 557 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,770.00 dollars or +17.70 points, Emini ES ($ES_F) futures @

$4,312.50 dollars or +86.25 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6,082.50 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=126&t=1710 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) my thought process from trade to trade so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell. If you join the chat room and then you do not ask any questions about WRB Analysis in your own trading or you do not document (journal) your own thoughts from trade to trade...the chat room will not be useful to you. Chat room access instructions @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=229&t=2165 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

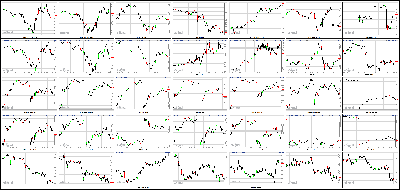

Stocks Fall, End Worst January In Years Attachment:

013114-Key-Price-Action-Markets.png [ 535.83 KiB | Viewed 535 times ]

013114-Key-Price-Action-Markets.png [ 535.83 KiB | Viewed 535 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Good riddance to a cold January, and we're not just talking about the weather.

Stocks dropped sharply during the first month of the year, with the Dow tumbling more than 5%. That was the Dow's worst January since 2009, when stocks were still in freefall in the aftermath of the financial crisis.

The S&P 500 slipped more than 3% this month, while the Nasdaq has shed nearly 2%.

Stocks have been hit particularly hard during the past two weeks due to emerging market worries and weak earnings.

Those factors also pressured the market on Friday. The Dow fell more than 150 points, or almost 1%, while the S&P 500 lost 0.7%, and Nasdaq declined 0.5%.

As stocks continued to lose ground, CNNMoney's Fear & Greed index, which measures seven indicators of market sentiment, fell further into "Extreme Fear" mode.

* Market volatility ahead. But don't panic!The market pullback hasn't been a total surprise though, given how well stocks did in 2013. Many experts believe stocks could continue to drop before resuming their upward trend.

"Frankly, we've been telling clients to expect a 5% to 10% decline," said Matt King, chief investment officer at Bell Investment Advisors. "We didn't think it would happen so early in the year, but it's been such a good run for markets that a meaningful correction is normal and healthy."

While stocks took a small step back last spring, they haven't experienced a correction, typically defined as a decline of 10% or more, in more than two years.

But King still thinks stocks will end the year with modest gains.

"We think the declines could spill over into February, but we're telling clients to buy into this weakness as well," said King. "We don't think this is anything more than a normal correction."

* No Terrible Twos for Facebook stockOn the earnings front Friday, Mattel (MAT, Fortune 500), Amazon (AMZN, Fortune 500), Chevron (CVX, Fortune 500) and MasterCard (MA, Fortune 500) were all big losers on Friday after reporting results that underwhelmed investors.

Mattel shares tumbled after the toy giant reported a surprise drop in its fourth-quarter revenue, as sales of its core brands Barbie and Fisher-Price fell sharply.

Amazon missed Wall Street's earnings forecasts, sending shares sharply lower. It was the worst performer in CNNMoney's Tech 30 index. Amazon also disclosed that it is considering doubling the membership price of Prime to $40 to cover rising fuel and shipping costs, a topic that generated plenty of chatter among traders on StockTwits.

"Explain again how raising Prime fees will increase growth?" asked SkepticalBull. "Oh yeah, that's right. It doesn't. It's a band-aid on a gunshot wound. $AMZN. Bearish."

But others came out in defense of the company.

"If Amazon is really losing money on Amazon Prime, of course it makes sense to raise the prices $AMZN," said ivanhoff.

Wal-Mart (WMT, Fortune 500)shares were flat after the discount retailer cut its guidance for the fourth quarter.

On the bright side, Google (GOOG, Fortune 500) and Chipotle (CMG) were all higher and hit new all-time highs following their earnings reports.

"$CMG $GOOG Have a Burrito while Googling for the next big thing!" joked StockTwits trader strick.

Facebook (FB, Fortune 500) shares also rose to new all-time highs. Shares of Facebook doubled in 2013 and have continued to rise this year, as the company continues to succeed with its mobile advertising strategy. Traders are hopeful that the stock will continue to gain ground.

"$FB Hope this become a more stable stock now with slow but continuous upwards movement...Bullish," said Heiko.

StockTwits trader vanhalenboss was also optimistic: "$FB Great company, great management team, great vision and executing in every category....BUY."

Zynga (ZNGA) was also higher, but the company also announced a new round of job cuts.

Microsoft (MSFT, Fortune 500) shares ticked up slightly following a Bloomberg report that the company is preparing to name executive vice president Satya Nadella as its next CEO.

* Worst is yet to come for 'Fragile Five'Emerging markets were in also in the limelight once again, with the Turkish lira and other currencies weakening further.

The volatility has been sparked by the fact that economic growth is slowing across developing economies and fears that China's shadow banking system could spark a credit crunch.

The Federal Reserve's decision to reduce the size of its monthly bond purchase program has also been weighing on emerging markets. The so-called tapering by the Fed is expected to leader to a stronger dollar, which should make emerging markets less attractive for investors.

In a statement Friday, the International Monetary Fund said "the turbulence also underscores the need for vigilance among central banks over liquidity conditions in international capital markets."

4:20 pm: [BRIEFING.COM] The stock market ended a disappointing month on a lower note as the S&P 500 lost 0.7%, extending its January decline to 3.6%. The Nasdaq outperformed, falling 0.5%, while the Dow Jones Industrial Average slid 1.0%.

Equities began the session sharply lower but a day-long rebound helped the major averages finish the trading day with more palatable losses. The S&P 500 made a very brief afternoon appearance in positive territory before retreating again in the final hour.

Today's cash session kicked off amid significant weakness in Europe where markets were flirting with losses close to 2.0%. The region-wide weakness was led by Germany after the country saw a 2.4% year-over-year drop in retail sales (+1.9% expected). A disappointing CPI reading for the eurozone (+0.7% versus 0.9% consensus) also played a part in the weakness.

Furthermore, the early selling once again coincided with yen strength as dollar/yen dropped as low as 102.00 before staging a modest recovery which accompanied the rebound in equities. Fittingly, the final hour retreat in stocks was accompanied another rally in the yen. Yen futures added 0.5% on Friday, extending their January gain to 3.0%.

Seven of ten sectors ended in the red with energy (-1.5%) seeing the largest decline. The sector was pressured by Dow component Chevron (CVX 111.63, -4.82), which tumbled 4.1% following disappointing earnings. The broader energy sector ended January behind the remaining nine groups with a loss of 6.3%.

Meanwhile, the second-weakest sector of the month, consumer discretionary, lost 1.3%, extending its January decline to 6.0%. The sector was a significant source of the morning weakness as Amazon.com (AMZN 358.69, -44.32) plunged 11.0% following its disappointing earnings and cautious guidance.

Despite the sharp loss in Amazon.com, the discretionary sector was able to climb off its lows with help from Chipotle Mexican Grill (CMG 551.96, +58.00) and homebuilders. Chipotle spiked 11.7% after reporting in-line earnings while iShares Dow Jones US Home Construction ETF (ITB 24.82, +0.43) added 1.8% as Treasury yields continued their retreat (10-yr yield -4 bps to 2.66%).

With regard to other cyclical groups, financials (-1.1%) lagged while industrials (-0.5%), materials (-0.6%), and technology (+0.2%) outperformed.

Notably, the tech sector drew strength from Google (GOOG 1180.97, +45.58), which jumped 4.0% after reporting earnings. Although the company missed its Capital IQ earnings estimate by $0.28, investors were pleased to see a 13% quarterly increase in click revenue.

On the countercyclical side, consumer staples (-0.4%), telecom services (+0.1%), and utilities (+0.8%) outperformed while health care (-0.8%) lagged.

Participation was well above average, which was likely related to month-end activity as 937 million shares traded at the NYSE.

Monday's data will be limited to the New Home Sales report for December, which will be released at 10:00 ET. It is also worth mentioning that China will release its Manufacturing PMI tonight at 20:00 ET, which is likely to generate a reaction in global markets on Monday. The general consensus expects the reading to slip from 51.0 to 50.5.

Related Stories

US STOCKS SNAPSHOT-S&P 500 ends at record closing high Reuters

U.S. stocks rally after retail sales top forecasts MarketWatch

How the Dow Jones industrial average did Thursday Associated Press

How the S&P 500 index fared Thursday Associated Press

Stocks Stage Big Comeback; NetSuite Turns Tail Investor's Business Daily

Nasdaq Composite -1.7% YTD

Russell 2000 -2.8% YTD

S&P 500 -3.6% YTD

Dow Jones Industrial Average -5.3% YTD

Week in Review: Stocks Endure Volatile Week

On Monday, the major averages followed the sharp losses of the prior week with another shaky performance. The Dow Jones Industrial Average and S&P 500 posted respective declines of 0.3% and 0.5% while the Nasdaq (-1.1%) and Russell 2000 (-1.5%) underperformed. Stocks displayed gains at the open but the early strength faded during the initial hour as the Nasdaq headed into the red. The other indices followed suit and the broad retreat continued until about 12:20 ET when stocks reversed, and spent the afternoon in a steady climb. Moderate selling pressure returned during the final hour, knocking the indices off their afternoon highs. Although there was no news responsible for the turn, the morning selling coincided with a strengthening yen while the session low in equities matched the high point for the Japanese currency. Once the yen began weakening again, a rally in equities ensued. Similarly, the selling observed during the last 30 minutes of action coincided with the yen gaining strength once again.

The stock market halted its three-day slide on Tuesday as the S&P 500 gained 0.6%. The tech-heavy Nasdaq (+0.4%) also finished in the green, but couldn't keep pace with the S&P 500 as Apple weighed following its quarterly report. Although the largest tech company beat on earnings and revenue, investors were not pleased by below-consensus iPhone sales. In addition, disappointing guidance for the second quarter also factored into the stock's 8.0% loss. The remainder of the technology sector (-0.7%) was a bit more mixed as large-cap names like Google, Oracle, and Intel posted solid gains while Seagate tumbled 11.3% after missing earnings estimates. Outside of technology, most other cyclical groups finished ahead of the broader market with financials (+1.3%) ending in the lead.

Selling pressure returned on Wednesday as equities ended broadly lower with small caps leading the weakness. The Russell 2000 lost 1.5% while the S&P 500 fell 1.0% as nine of ten sectors finished in the red. Although the session generated plenty of excitement, some of the events that played out over the course of the day were set in motion on Tuesday. Shortly after Tuesday's session on Wall Street ended, the Central Bank of Turkey shocked the market with a 445-basis point hike to 12.00% in an attempt to halt the rapidly weakening lira. The move worked...for 15 hours. The lira strengthened after the announcement, but spent the remainder of the overnight session in a steady retreat, giving up all of its gains. Interestingly, the news of out of Turkey also gave a boost to U.S. equity futures while weighing on the yen. The moves did not hold as futures spent the night in a steady retreat while the yen rallied. The materials sector (+0.5%) withstood the broad-based weakness with help from Dow Chemical, which rallied 4.1% after beating on earnings.

On Thursday, the major averages finished near their highs with the Nasdaq surging 1.8% while the S&P 500 gained 1.1% as all ten sectors ended in the green. Stocks jumped out of the gate and continued climbing steadily into the early afternoon. The S&P 500 notched a session high of 1798.77 just before 13:00 ET, and spent the rest of the trading day near that level. The upbeat start to the session was aided by overnight gains in index futures which rallied while the Japanese yen weakened. The futures market received an additional boost an hour before the cash open when it was reported that fourth quarter GDP rose 3.2%, per the advance estimate. The Nasdaq Composite spent the entire session in the lead with the likes of Amazon.com, Google, Facebook, and Qualcomm providing support. Amazon.com and Google rallied ahead of their earnings while Facebook and Qualcomm posted respective gains of 14.1% and 3.0% after reporting better-than-expected results.

3:30 pm: [BRIEFING.COM] Apr gold and Mar silver surrendered morning gains as they reversed from their respective session highs of $1254.80 per ounce and $19.47 per ounce set moments after pit trade opened. Gold slipped into the red in afternoon action and settled 0.2% lower at $1239.80 per ounce. The yellow metal fell 2.0% over the week as investors reacted to the FOMC taper announcement and strong U.S. GDP data. Silver, unable to regain momentum, settled unchanged at $19.13 per ounce, booking a 3.2% loss for the week.

Mar crude oil traded in negative territory as the dollar index posted modest gains. It came off its session low of $97.23 per barrel set at pit trade open and trended higher until late afternoon action. It then lost steam after touching a session high of $98.39 per barrel and settled with a 0.7% loss at $97.53 per barrel. Despite today's weakness, crude oil gained 0.9% over the week.

Mar natural gas extended yesterday's losses, falling as low as $4.72 per MMBtu in late morning action on forecasts for milder weather. It gained some steam in the last hour of floor trade and settled at $4.94 per MMBtu, or 1.6% lower. Despite trading at 4 year highs earlier this week, natural gas booked a weekly loss of 1.8%.

3:00 pm: [BRIEFING.COM] The S&P 500 hovers right below its flat line with one hour remaining in today's session. Although the index began the day with a 22 point loss, it was able to notch a session low shortly after the open, and head higher from there.

It would be remiss not to mention that the entire rebound has been accompanied by a rally in dollar/yen after the pair notched a session low just under the 102.00 level. Similarly, the recent downtick from highs corresponded with dollar/yen slipping from its best level of the afternoon.

Interestingly, both the S&P 500 and futures on the yen are currently flat for the week. With today's session marking the end of January, the S&P 500 is on pace to post a 3.1% loss while yen futures are on track to add 2.9% this month.

2:35 pm: [BRIEFING.COM] Following a continuation of the rebound, the S&P 500 finds itself less than three points below its flat line. Furthermore, thanks to the recovery, the index is now unchanged for the week.

Market participants received a full slate of economic data this week and the tail end of next week shapes up to be equally busy in terms of the amount of reports on the schedule. However, most of the reports are not expected to move the market with the exception of Friday's nonfarm payrolls for January.

2:00 pm: [BRIEFING.COM] The S&P 500 has inched to a fresh rebound high in a broad-based move that saw all sectors tick up from their recent levels. The consumer staples sector has joined technology (+0.4%), telecom services (+0.9%), and utilities (+0.9%) in the green, but so far its gain has been limited to less than 0.1%.

Elsewhere, industrials and materials are looking to regain their flat lines while consumer discretionary (-0.7%), financials (-0.6%), and health care (-0.5%) continue to weigh.

Also of note, Treasuries have been slipping since stocks notched their lows. The 10-yr yield now sits at 2.67% after notching a session low just below 2.65%.

Related Stories

Dow, S&P 500 Break Support As Stocks Sell Off Again Investor's Business Daily

Market Hustle: Futures Fall Amid Soft Corporate Results TheStreet.com

Relative Strength Charts For S&P 500 Sectors Seeking Alpha

Buy, Sell, Hold? Chart Shows Analyst Ratings on S&P 500 Stocks by Sector Minyanville

S&P 500 Analyst Ratings By Sector Seeking Alpha

1:30 pm: [BRIEFING.COM] The major indices are still mired in negative territory. The consolation of that standing is that they were much deeper in negative territory shortly after the opening bell. The ability of the S&P 500 to hold above support at its 100-day moving average and an afternoon recovery effort in the European markets helped stem the steady flow of sell orders.

Still, participants are picking their spots today when it comes to making purchases, which is why the broader market has had some difficulty extending the recovery try.

The Treasury market continues to benefit in the face of the continued stock market weakness both here and abroad. The 10-yr note is up 9 ticks today, bringing its yield down to 2.66%. That is ultimately a supportive move for mortgage rates, which is perhaps why the homebuilders are a standout group today. The iShares US Home Construction ETF (ITB 24.90, +0.51) is up 2.1% at this juncture.

Another beneficiary of the drop in long-term rates is the utilities sector (+0.6%), which has outperformed all month (+2.6%) as the yield on the 10-yr note has come down from 3.02% at the end of 2013.

1:00 pm: [BRIEFING.COM] Equity indices trade broadly lower at midday with the Dow Jones Industrial Average (-0.7%) leading the weakness. The S&P 500 displays a more modest loss of 0.4% as seven of ten sectors hover in the red.

Stocks began the session with sharp losses that saw the S&P 500 trade just three points above its 100-day moving average. The early weakness resulted from a handful of factors at home and abroad.

Overseas, markets across Europe were down as much as 2.0% after Germany reported a 2.4% year-over-year drop in retail sales (+1.9% expected). In addition, a disappointing CPI reading for the eurozone (+0.7% versus 0.9% consensus) also played a part in the weakness.

Furthermore, the early selling once again coincided with yen strength as dollar/yen dropped as low as 102.00 before staging a modest recovery. Interestingly, once the currency pair began climbing off its lows, stocks began heading higher as well.

At this juncture, the consumer discretionary (-1.0%) sector trails the remaining groups with Amazon.com (AMZN 364.94, -38.03) responsible for a significant portion of the weakness. The online retail giant trades lower by 9.5% after reporting below-consensus earnings and issuing cautious guidance. The company reported its results after yesterday's close and factored into the sharply lower start to the session.

From one consumer sector to another, the staples sector (-0.1%) outperforms even after Wal-Mart (WMT 74.86, +0.11) was the latest retailer to warn of an expected fourth quarter earnings shortfall on account of the weather. Wal-Mart, though, was also impacted by the reduction in food stamp benefits that went into effect November 1.

On the upside, technology (+0.3%) has received significant support from Google (GOOG 1180.30, +44.91), which trades higher by 4.0%. Although the company missed on earnings, investors were pleased by a 13% quarterly increase in click revenue.

Even though the S&P 500 has put a significant dent in its losses, influential sectors like consumer discretionary (-1.0%), financials (-0.8%), and health care (-0.6%) continue to lag, suggesting their underperformance could pressure the market once again before today's session ends.

Treasuries hold modest gains with the 10-yr yield down three basis points at 2.66%.

Today's economic data included a handful of reports:

Personal income was flat in December after increasing 0.2% in November. Spending increased 0.4%, down from an upwardly revised 0.6% (from 0.5%) in November. The Briefing.com consensus expected both personal income and spending to increase 0.2% in December.

The Employment Cost Index increased 0.5% in the fourth quarter to follow a 0.4% gain in Q3 2013. The Briefing.com consensus expected an increase 0.4%.

The Chicago PMI fell slightly in January, from 60.8 to 59.6. The Briefing.com consensus expected the reading to fall to 58.0. While the PMI has fallen for three consecutive months, the October peak of 66.6 was never sustainable. It is very difficult for the reading to remain above 60.0 for any extended period of time.

The January University of Michigan Consumer Sentiment Index was revised up to 81.2 in the final reading from 80.4. That is still down from a reading of 82.5 in December but above the Briefing.com consensus expectation of 80.4. The present conditions index was revised higher (to 96.8 from 95.2), as was the outlook index (to 71.2 from 70.9). Despite the revisions, both indices are still lower than they were in December.

12:30 pm: [BRIEFING.COM] Equities have continued their steady climb off morning lows, but it should be noted the S&P 500 (-0.4%) has passed a handful of influential sectors. Consumer discretionary (-1.0%), financials (-0.8%), and health care (-0.6%) continue to lag, which matters to the broader market considering the three account for 40% of the entire S&P 500. If these sectors remain weak into the second half of the session, the broader market will be likely to follow suit.

Meanwhile, the largest sector, technology, has climbed into the green. The group trades higher by 0.2% thanks in part to the relative strength of Google (GOOG 1179.00, +43.61). The stock is higher by 3.9% despite its bottom-line miss. However, investors found solace in the company's click revenue, which rose 13% over the prior quarter.

12:00 pm: [BRIEFING.COM] The S&P 500 hovers near the middle of its range as it looks to continue its rebound off lows in the 1772 area. At its lowest point of the session, the benchmark index was just three points away from its 100-day average (1769), which hasn't been tested since early October.

Including today's decline, the S&P 500 is on track to post a January loss of 3.3%. This would put the index in the middle of its peers as the Dow holds a month-to-date loss of 5.0% while the Nasdaq has given up 1.6% in January.

After finishing 2013 ahead of other sectors, the discretionary group is on pace to end the month with a loss of 5.7%. This would place the sector at the bottom of this month's leaderboard, right alongside the energy space.

11:30 am: [BRIEFING.COM] Recent action saw the major averages trim another portion of their losses with the S&P 500 narrowing its decline to 0.5%.

Two countercyclical sectors-telecom services (+0.1%) and utilities (+0.7%)-are back in the green while the other two-consumer staples (-0.4%) and health care (-0.8%)-remain in the red.

On the cyclical side, technology (-0.1%) and materials (-0.1%) outperform while the remaining four groups display losses between 0.5% and 1.1%. The discretionary sector is the weakest performer as Amazon.com (AMZN 365.88, -37.06) weighs following its disappointing report and guidance. The online retail giant holds a loss of 9.2%.

It should be noted that once again today's price action has been mirroring the performance of the dollar/yen pair. Currently, the pair trades at 102.15 after notching a session low just below the 102.00 level at 11:00 ET.

11:00 am: [BRIEFING.COM] Equity indices continue to hold the bulk of their losses with the Dow Jones Industrial Average (-1.1%) looking to narrow the gap between itself and other indices. The price-weighted index lags as all but three components trade in the red. The three advancers-Caterpillar (CAT 94.00, +0.80), Microsoft (MSFT 36.93, +0.07), and Verizon (VZ 47.79, +0.16)-display gains between 0.2% and 0.8%.

On the downside, eleven index members sport losses of 1.0% or more with Chevron (CVX 111.94, -4.50) seeing the largest loss. The stock trades down 3.9% after missing earnings estimates by one cent on below-consensus revenue. On a related note, the energy sector (-1.2%) is the weakest group at this juncture.

Including today's decline, the Dow is on track to end January with a loss of 5.4%.

10:35 am: [BRIEFING.COM] Commodities are mixed this morning with energy and metals mostly lower and agriculture futures mostly higher.

Gold and silver futures have been selling off and are now back near the flat line. Apr gold is now +0.3% as $1246.10/oz, Mar silver is +0.4% at $19.20/oz.

Crude oil and natural gas have been in the red all day. In recent action, natural rallied and hit $4.99/MMBtu, but quickly reversed and has been selling off.

Mar natural gas is now -4.7% at $4.78/MMBtu, while Mar crude oil is -0.5% at $97.75/barrel.

10:00 am: [BRIEFING.COM] Equity indices have inched off their worst levels of the session, but they remain sharply lower. The S&P 500 has trimmed its decline to 1.0%.

It should be noted influential sectors continue to trail the broader market with consumer discretionary, financials, and health care down between 1.0% and 1.4%.

The University of Michigan Consumer Sentiment report for January was revised up to 81.2 in the final reading while the Briefing.com consensus expected the index to hold at 80.4.

9:45 am: [BRIEFING.COM] As expected, the major averages began the session sharply lower with the Dow Jones Industrial Average (-1.3%) seeing the largest early loss. Meanwhile, the S&P 500 trades lower by 1.1% with all ten sectors registering losses.

Technology (-0.6%) and utilities (-0.3%) are holding in relatively well while consumer discretionary (-1.7%), energy (-1.8%), and financials (-1.3%) lag. Notably, the technology sector owes its outperformance to Google (GOOG 1156.00, +20.61) while the discretionary space is being pressured by Amazon.com (AMZN 367.50, -35.51).

Just released, the January Chicago PMI slipped to 59.6 from 60.8 while the Briefing.com consensus expected a decline to 58.0.

The final reading of the University of Michigan Consumer Survey for January will be released at 9:55 ET.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: -22.60. Nasdaq futures vs fair value: -36.50. The stock market is on track for a sharply lower open as the S&P 500 futures trade almost 23 points below fair value. Futures on the benchmark index began slumping from yesterday's closing levels after Amazon.com (AMZN 371.00, -32.01) reported disappointing quarterly results, sending shares lower. Google (GOOG 1180.66, +45.27) also reported an earnings miss, but the stock headed higher as investors were pleased by an increase in click revenue.

Although futures climbed back into positive territory during the Asian session, the weakness returned once Europe opened for action. At this juncture, European indices sit near their lows with Germany's DAX (-1.9%) seeing the largest loss. Contributing to the weakness were disappointing German retail sales figures (-2.4% year-over-year actual versus +1.9% expected) and eurozone CPI (+0.7% actual, +0.9% expected).

With futures near lows, Treasuries hover on their highs with the 10-yr yield down almost five basis points at 2.65%.

The Chicago PMI report for January and the final reading of the University of Michigan Consumer Survey for January will be reported at 9:45 ET and 9:55 ET.

8:58 am: [BRIEFING.COM] S&P futures vs fair value: -25.00. Nasdaq futures vs fair value: -39.50. The S&P 500 futures trade 25 points below fair value.

Markets across Asia ended mixed amid a lackluster trade. Much of the region was closed in observance of the Lunar New Year, with closures set to continue into next week. Japanese data was heavy as National Core CPI (1.3% year-over-year versus 1.2% expected), Tokyo Core CPI (0.7% year-over-year versus 0.7% expected), household spending (0.7% year-over-year versus 1.2% expected), and preliminary industrial production (1.1% month-over-month versus 1.3% expected) were released.

Elsewhere, Australia saw a tame PPI print (0.2% quarter-over-quarter actual versus 0.7% expected), keeping a potential Reserve Bank of Australia rate cut on the table at next week's meeting. Also of note, Thailand's trade deficit narrowed to $285 million from $560 million while its current account surplus grew to $2.53 billion from $2.29 billion.

Japan's Nikkei fell 0.6%, posting its lowest close since the middle of November. Automakers were pressured as a result of the strong yen as Toyota Motor lost 1.3% and Nissan Motor sank 0.8%.

China's Shanghai Composite and Hong Kong's Hang Seng were closed for the Lunar New Year.

Major European indices have spent the first half of the session in a steady decline with Germany's DAX (-2.1%) in the lead. The weakness comes after the country reported a 2.5% month-over-month decline in retail sales (0.2% expected, 0.9% prior) while the year-over-year reading tumbled 2.4% (1.9% forecast, 1.1% last). Adding to the weakness was inflation data from the eurozone as CPI increased 0.7% year-over-year while an uptick of 0.9% was broadly expected. Core CPI, however, rose an in-line 0.8% (0.7% prior). Separately, the unemployment rate held steady at 12.0% (12.1% forecast).

Elsewhere, French PPI ticked up 0.2% month-over-month (0.1% consensus, 0.5% last) while consumer spending ticked down 0.1% month-over-month (-0.4% expected, 1.4% last). Italy's PPI slipped 0.1% month-over-month (0.2% consensus, -0.1% previous) while the year-over-year reading declined 1.8% (-1.9% forecast, -1.8% last). Separately, the monthly unemployment rate ticked down to 12.7% from 12.8%, as expected. Also of note, Spain's current account surplus narrowed to EUR870 million from EUR1.71 billion.

Germany's DAX is lower by 2.1% as all but one component register losses. Financials are leading the weakness with Commerzbank and Deutsche Bank down 4.3% and 4.0%, respectively. On the upside, utility company E.ON hovers just above its flat line.

In France, the CAC trades down 1.8% with banks also pacing the retreat. BNP Paribas, Credit Agricole, and Societe Generale are down between 3.0% and 3.5%. On the upside, LVMH Moet Hennessy Louis Vuitton sports an advance of 5.4% after reporting upbeat results.

Great Britain's FTSE holds a loss of 1.7% amid broad weakness. Royal Bank of Scotland is lower by 2.3% while consumer names like Coca-Cola HBC and Diageo display respective losses of 4.4% and 2.1%.

8:33 am: [BRIEFING.COM] S&P futures vs fair value: -24.40. Nasdaq futures vs fair value: -39.00. The S&P 500 futures trade 24 points below fair value.

December personal income was unchanged while the Briefing.com consensus expected an increase of 0.2%. Meanwhile, personal spending rose 0.4% while the consensus expected an uptick of 0.2%.

Separately, core PCE prices ticked up 0.1%, as expected.

Lastly, the fourth quarter employment cost index increased 0.5% while the Briefing.com consensus expected an uptick of 0.4%.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -20.40. Nasdaq futures vs fair value: -34.30. U.S. equity futures hover near their pre-market lows amid cautious overseas action. The S&P 500 futures trade 20 points below fair value.

Reviewing overnight developments:

In Asia, Japan's Nikkei lost 0.6% while China's Shanghai Composite and Hong Kong's Hang Seng were closed for the Lunar New Year.

In economic data:

Japan's National CPI rose 1.6% year-over-year (1.5% last) while Tokyo CPI increased 0.7% year-over-year (0.9% prior). National Core CPI increased 1.3% (1.2% forecast, 1.2% last) while Tokyo Core CPI rose an in-line 0.7% (0.7% previous). Also of note, Manufacturing PMI increased to 56.6 from 55.2, industrial production ticked up 1.1% month-over-month (1.2% consensus, -0.1% last), and the unemployment rate fell to 3.7% from 4.0% (3.9% forecast). Separately, housing starts rose 18.0% year-over-year (13.5% expected, 14.1% last) while construction orders increased 4.9% year-over-year (2.2% last).

Australia's PPI increased 0.2% quarter-over-quarter (0.9% consensus, 1.3% prior) while Private Sector Credit increased 0.5% month-over-month (0.4% forecast, 0.3% last).

Among news of note:

Japan's Prime Minister Shinzo Abe said a tax panel may implement a corporate tax cut in February.

Major European indices have spent the first half of the session in a steady decline. Great Britain's FTSE -1.1%, France's CAC -1.2%, and Germany's DAX -1.5%. Elsewhere, Italy's MIB -1.0% and Spain's IBEX -1.1%.

Looking at economic data:

Eurozone CPI increased 0.7% year-over-year (0.9% forecast, 0.8% prior) while Core CPI rose an in-line 0.8% (0.7% prior). Separately, the unemployment rate held steady at 12.0% (12.1% forecast).

Germany's retail sales fell 2.5% month-over-month (0.2% forecast, 0.9% last) while the year-over-year reading declined 2.4% (1.9% expected, 1.1% prior).

French PPI ticked up 0.2% month-over-month (0.1% consensus, 0.5% last) while consumer spending ticked down 0.1% month-over-month (-0.4% expected, 1.4% last).

Italy's PPI slipped 0.1% month-over-month (0.2% consensus, -0.1% previous) while the year-over-year reading declined 1.8% (-1.9% forecast, -1.8% last). Separately, the monthly unemployment rate ticked down to 12.7% from 12.8%, as expected.

Spain's current account surplus narrowed to EUR870 million from EUR1.71 billion.

In news:

Regional markets have been hit with a one-two punch of selling interest following a sharp decline in German retail sales and yet another below-consensus CPI reading from the Eurozone.

In U.S. corporate news:

Amazon.com (AMZN 372.52, -30.49) -7.6% after reporting fourth quarter earnings $0.18 below the Capital IQ consensus estimate. Additionally, the company issued cautious first-quarter guidance.

Broadcom (BRCM 29.50, +0.29): +1.0% after announcing above-consensus results and increasing its quarterly dividend to $0.12.

Chipotle Mexican Grill (CMG 555.97, +62.01): +12.6% after reporting in-line earnings on better-than-expected revenue.

Google (GOOG 1176.00, +40.61): +3.6% after missing the Capital IQ consensus estimate by $0.28 on in-line revenue. However, "click revenue" rose 31% year-over-year and 13% over the prior quarter.

LyondellBasell (LYB 80.25, +2.19): +2.8% following its better-than-expected earnings.

Mattel (MAT 40.20, -2.81): -6.5% after missing on earnings and revenue.

Wynn Resorts (WYNN 207.25, +5.74): +2.9% after beating on earnings and revenue.

December Personal Income, Personal Spending, Core PCE Prices, and the fourth quarter Employment Cost Index will all be released at 8:30 ET while the final reading of the University of Michigan Consumer Survey for January will be reported at 9:55 ET.

6:20 am: [BRIEFING.COM] S&P futures vs fair value: -17.50. Nasdaq futures vs fair value: -32.00.

6:20 am: [BRIEFING.COM] Nikkei...14914.53...-92.50...-0.60%. Hang Seng...Holiday.........

6:20 am: [BRIEFING.COM] FTSE...6487.84...-50.50...-0.70%. DAX...9249.42...-125.10...-1.30%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage