Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

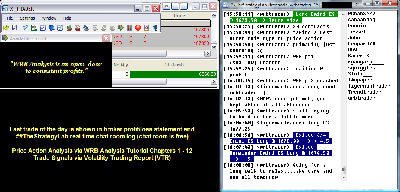

Attachment:

093013-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6560.00.png [ 88.4 KiB | Viewed 561 times ]

093013-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6560.00.png [ 88.4 KiB | Viewed 561 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$360.00 dollars or +3.60 points, Emini ES ($ES_F) futures @

$5750.00 dollars or +115.00 points, Light Crude Oil CL ($CL_F) futures @

$450.00 dollars or +0.45 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6560.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the chat room. You can read

today's chat room logs for details about each one of my trades via price action trading from

entry to exit (e.g. time, price, contract size) along with

price action commentary as the trade traversed to its completion...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=121&t=1613 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=219&t=1973 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

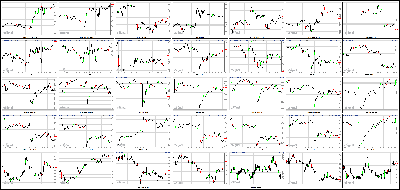

Dow Falls 128 Points As Washington Spooks Stocks Attachment:

093013-Key-Price-Action-Markets.png [ 525.96 KiB | Viewed 541 times ]

093013-Key-Price-Action-Markets.png [ 525.96 KiB | Viewed 541 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

Investors don't want to wait and see if lawmakers can reach a deal to avoid a government shutdown at midnight. They just sold.

The Dow Jones Industrial Average dropped more than 128 points, or nearly 1%, on Monday. The S&P 500 and the Nasdaq closed the day with losses as well.

October sell-off coming? Despite Monday's slide, the three major indexes are still up between 15% and 24% for the year. The Dow and S&P 500 are up between 2% and 3% in September alone, and hit record highs just two weeks ago. All three indexes are up for the quarter, led by the Nasdaq, which has risen 11%.

But some strategists are predicting that stocks could fall further if the government closes up shop -- even if it's only a brief shutdown.

* 8 things you need to know about the debt ceilingCitigroup analyst Tobias Levkovich said that the "rancorous debate in Washington" coupled with slowing economic growth could push the S&P 500 down to 1600, a drop of more than 5% from its current level.

Levkovich and several other analysts also expect companies to cut their 2014 profit forecasts when they report third quarter earnings over the next few weeks. That could be another wake up call for investors, who had been bullish all year despite some big risks.

The shutdown isn't the only thing in Washington that investors are worried about. Stocks have pulled back recently as the U.S. gets closer to hitting the debt ceiling. If Congress fails to increase the debt limit, the U.S. government won't be able to pay all of its bills later this month.

Fear and volatility spike: The Chicago Board Options Exchange's Volatility Index (VIX), a key gauge of market volatility more commonly known as the VIX, has risen nearly 10% in each of the past two trading sessions. But it's still a relatively low 17 -- far below the mid-40s range it traded at when Standard & Poor's downgraded the U.S.'s credit rating in 2011.

* Video - Fear returns as shutdown looms But investors do seem more nervous lately. CNNMoney's Fear & Greed Index has moved deeper into Fear mode and is getting close to Extreme Fear levels. The index was Neutral just a week ago.

* Obamacare and biotech boost health care stocksWhat's moving: Shares of Apple (AAPL, Fortune 500) dropped more than 1% as investors waited for details about CEO Tim Cook's reported lunch meeting with activist investor Carl Icahn. Traders weren't holding out hope for any good news though.

"$AAPL..if the traders" in the know" really thought there would be fireworks at their lunch meeting, many more calls would be trading," wrote StockTwits commenter christopherbrecher.

Investors also weren't wowed by news that Apple was named the "best global brand" by Interbrands.

J.C. Penney (JCP, Fortune 500) dipped nearly 3%. The retailer, which has been hemorrhaging money, announced last Friday that it had raised roughly $810 million through a public offering. Shares are trading near lows not hit since late 2000. Traders still have a bleak outlook for the company.

"$JCP imho if this Q4 is not good at all, $JCP would be def done. Even if Q4 were good, they would still be struggling for a long time," StockFan123 wrote.

Shares of Chipotle Mexican Grill (CMG) rose more than 2% following an analyst upgrade.

Noted short seller David Einhorn has said he's betting against the stock, and some traders continue to agree with Einhorn -- despite Chipotle's rally.

"$CMG at a multiple of 40 times earnings, this burrito maker is due for a substantial pullback," commented contrarianspeculator. "Waiting for Einhorn to pounce on this one again."

"$CMG there is more hedge $$ that sees this as an epic short than even a luke warm long...don't kid yourself," traderiver added.

* How the government will shut downGovernment shutdown fears hit world markets too: European markets and most Asian markets closed with losses, though the Shanghai Composite moved higher. China launched a free trade zone in Shanghai on Sunday, an experiment in promoting trade and expanding foreign investments in China.

4:15 pm : The S&P 500 fell 0.6% in the final session of the third quarter, trimming its quarterly advance to 4.7%.

Stocks stumbled out of the gate as political uncertainty in Washington and Italy caused participants to reduce their risk exposure.

In Washington, the federal government is on track to shut down at midnight following a game of political ping pong between the House of Representatives and the Senate. The two legislative bodies spent the day exchanging competing bill proposals with the House seeking to make changes to Obamacare while the Senate refused to engage in debate that would jeopardize funding for the health care law.

Overseas, the Italian government is on the ropes after five PDL ministers withdrew their support for the current legislature at the request of party leader Silvio Berlusconi. With the country's future in question, Prime Minister Enrico Letta is expected to appear in front of parliament on Wednesday to seek a new majority. Despite today's developments, Italian 10-yr yield ended little changed at 4.57% after increasing 20 basis points late last week in anticipation of the turmoil.

After notching their lows during the opening minutes, the major averages spent the first-half of the session in a steady climb with the Nasdaq (-0.3%) and Russell 2000 (-0.04%) pacing the rebound. The outperformance of the two indices was a recurring theme throughout the third quarter as the Nasdaq and Russell ended with respective gains of 10.8% and 9.9%.

All ten sectors settled in the red with consumer staples (-1.1%) leading to the downside. Meanwhile, other countercyclical groups ended mixed. Health care (-0.3%) and utilities (-0.1%) outperformed while telecom services (-0.6%) finished in-line.

The S&P 500 struggled with its 50-day moving average (1680) throughout the afternoon, but managed to close just above that level despite weakness among several cyclical sectors. Notably, energy, financials, and technology lost between 0.6% and 0.8% with energy leading to the downside as crude oil fell 0.5% to $102.32 per barrel.

Elsewhere, major financials lagged throughout the day. JPMorgan Chase (JPM 51.69, -0.55) was the weakest performer among the majors while the broader sector lost 0.7%.

Lastly, the technology sector saw some of its top components like Apple (AAPL 476.75, -6.00), Oracle (ORCL 33.17, -0.61), and Visa (V 191.10, -1.95) lose between 1.0% and 1.8%. Chipmakers withstood the bulk of the selling as the PHLX Semiconductor Index ended flat.

Treasuries ended little changed with the benchmark 10-yr yield down at 2.61%.

Trading volume surpassed the 200-day moving average of 728 million as 878 million shares changed hands on the floor of the New York Stock Exchange.

Economic data was limited to the September Chicago PMI report, which increased to 55.7 from 53.0 (Briefing.com consensus 53.7), representing the strongest reading since February. The Production Index improved to 58.0 from 53.0 with the increase completely due to continued strengthening in new orders.

The new orders index increased to 58.9 from 57.2. Another month of accelerating production gains may not be in the cards. Order backlogs have contracted each of the previous four months, putting the index at 46.7. Without a steady supply of backlogs, production gains will completely rely on new orders, and maintaining new orders at their current elevated levels may be difficult.

Tomorrow, August construction spending and the September ISM Index will both be reported at 10:00 ET.DJ30 -128.57 NASDAQ -10.12 SP500 -10.20 NASDAQ Adv/Vol/Dec 1166/1.77 bln/1395 NYSE Adv/Vol/Dec 1206/878.3 mln/1822

3:30 pm :

Precious metals and crude oil traded lower despite a weaker dollar index as the U.S. federal government is on track to shut down at midnight.

Dec gold slipped to a session low of $1322.00 per ounce in morning pit trade and eventually settled with a 0.9% loss at $1326.00 per ounce.

Dec silver pushed into positive territory and to a session high of $22.08 per ounce after brushing a session low of $21.43 in early morning floor action. However, it fell back into the red and settled 0.4% lower at $21.73 per ounce.

Nov crude oil extended Friday's losses, falling as low as $101.05 per barrel in morning pit action. It inched higher as the session progressed and settled with a 0.5% loss at $102.31 per barrel, just below its session high of $102.38 per barrel.

Nov natural gas also chopped around in negative territory, slipping to a session low of $3.51 per MMBtu. It settled with a 0.8% loss at $3.56 per MMBtu.

DJ30 -131.98 NASDAQ -13.43 SP500 -11.07 NASDAQ Adv/Vol/Dec 1066/1340.1 mln/1462 NYSE Adv/Vol/Dec 1009/406 mln/1989

3:00 pm : The S&P 500 trades lower by 0.6% as today's session enters its final hour. As noted earlier, small caps have traded ahead of the S&P throughout the day, and the Russell 2000 (+0.1%) has now climbed into positive territory.

In order for the S&P to join the Russell in the green, a handful of influential sectors will need to garner some late afternoon buying interest. Currently, the four top-weighted groups (consumer discretionary, financials, health care, and technology) hold losses ranging between 0.3% and 0.6%.DJ30 -119.21 NASDAQ -9.16 SP500 -9.46 NASDAQ Adv/Vol/Dec 1167/1.21 bln/1355 NYSE Adv/Vol/Dec 1120/368.2 mln/1864

2:30 pm : The S&P 500 (-0.5%) continues to trade near the middle of its range while small caps have erased almost all of their early losses. The Russell 2000 holds a slim loss of 0.1% and with the third quarter coming to an end today, the index is on track to post a quarterly gain of 9.8%.

Headlines from Washington have continued pouring in throughout the afternoon. According to the latest reports, the Senate has voted to reject the House spending bill that included a one-year delay of Obamacare. As such, the onus is now back on the House of Representatives to prevent a shutdown at midnight.DJ30 -104.50 NASDAQ -8.21 SP500 -8.13 NASDAQ Adv/Vol/Dec 1112/1.11 bln/1385 NYSE Adv/Vol/Dec 1086/335.5 mln/1881

2:00 pm : The major averages continue to hold their afternoon ranges with the Nasdaq (-0.2%) outperforming the remaining indices.

All ten sectors remain in negative territory with consumer staples (-0.9%) trailing behind the other nine groups. On the upside, health care (-0.3%), industrials (-0.4%), and materials (-0.3%) have been able to retrace a portion of their losses. Notably, the industrial sector has received support from transportation-related names as the Dow Jones Transportation Average trades little changed.

Also of note, a recent headline from Washington indicated Senate Majority Leader Harry Reid would not accept a one-week funding measure.DJ30 -107.61 NASDAQ -10.14 SP500 -8.75 NASDAQ Adv/Vol/Dec 1051/1.04 bln/1447 NYSE Adv/Vol/Dec 977/311.9 mln/1980

1:30 pm : It was a foregone conclusion that the wires would be festooned today with headlines pertaining to the latest dealings to keep the federal government running past midnight. To that end, Politico recently reported that House Republicans are talking about a one week stopgap funding bill.

The major indices caught a little tailwind on that headline, yet buyers have contained their enthusiasm knowing a one-week reprieve is not a real solution.

On a related note, Senator Reid will reportedly hold a press conference at 2:45 p.m. ET. Meanwhile, a Labor Department official has indicated the BLS will not release the September employment report on Friday if the government is shut down. The major indices subsequently ran into a headwind on that update.

Uncertainty is in the air today and the budget headlines are driving the market (crazy).DJ30 -90.71 NASDAQ -5.45 SP500 -6.73 NASDAQ Adv/Vol/Dec 1092/958 mln/1389 NYSE Adv/Vol/Dec 1032/284 mln/1916

1:00 pm : The S&P 500 holds a midday loss of 0.5% with all ten sectors hovering in the red.

Equities began the session sharply lower as global investors shied away from risk assets in reaction to the political turmoil in Italy and the United States.

European markets were rattled by five PDL ministers withdrawing their support for the coalition government. Their resignations came at the request of party leader Silvio Berlusconi, and Prime Minister Enrico Letta is expected to appear in front of parliament on Wednesday to seek a new majority.

In the U.S., the federal government is on track to shut down at midnight after lawmakers failed to agree on a funding bill. After the Senate passed a stopgap funding measure that did not call for defunding of Obamacare, the House of Representatives countered by adding a provision to delay health care reform for one year. Latest reports from Washington indicate Republican members of the House will meet at 14:00 ET.

The concerns associated with political uncertainty reflected on markets, but U.S. equities have been able to erase a good portion of their opening losses. The S&P trades near the middle of its range while the Nasdaq (-0.2%) hovers near its flat line.

Nasdaq outperformance has been a common theme as of late. With today's session marking the end of the third quarter, the tech-heavy index is on track to register a quarterly gain of 10.8%.

Today, the Nasdaq trades ahead of the S&P as biotechnology displays relative strength. The iShares Nasdaq Biotechnology ETF (IBB 210.16, -0.05) is lower by 0.3% while the traditional tech sector trades down 0.4%. The outperformance of biotech has placed the health care sector (-0.2%) atop today's leaderboard.

Meanwhile, the broader market remains pressured by a handful of influential sectors as consumer staples, energy, and financials hold losses between 0.7% and 0.8%. The energy space is the weakest performer among the three as crude oil trades down 1.0% at $101.81 per barrel.

With uncertainty abound, the CBOE Volatility Index (VIX 16.56, +1.10) is at its highest level since September 9 as participants adjust their near-term volatility expectations.

Today's economic data was limited to the September Chicago PMI report, which increased to 55.7 from 53.0 (Briefing.com consensus 53.7), representing the strongest reading since February. The Production Index improved to 58.0 from 53.0 with the increase completely due to continued strengthening in new orders. The new orders index increased to 58.9 from 57.2. Another month of accelerating production gains may not be in the cards. Order backlogs have contracted each of the previous four months, putting the index at 46.7. Without a steady supply of backlogs, production gains will completely rely on new orders, and maintaining new orders at their current elevated levels may be difficult.DJ30 -108.31 NASDAQ -9.38 SP500 -8.88 NASDAQ Adv/Vol/Dec 980/875.3 mln/1487 NYSE Adv/Vol/Dec 891/259.3 mln/2041

12:30 pm : After starting the session with losses close to 1.0% apiece, the major averages have been able to retrace a portion of their early decline. The opening weakness took place as participants grappled with political turmoil in Italy and the United States.

In Italy, Prime Minister Enrico Letta is expected to go before Parliament on Wednesday in hopes of securing a new majority after five PDL ministers withdrew their support for the government in allegiance with their leader Silvio Berlusconi.

In the U.S., the Senate is scheduled to vote on a stopgap funding measure to keep the government running. Similar to Friday, the measure is expected to pass after Senate takes out the changes made to the funding of Obamacare by the House of Representatives. Meanwhile, House Republicans are scheduled to meet at 14:00 ET in order to discuss the next step with a government shutdown looming at midnight.DJ30 -127.31 NASDAQ -12.33 SP500 -10.22 NASDAQ Adv/Vol/Dec 903/801.5 mln/1545 NYSE Adv/Vol/Dec 807/238.6 mln/2117

12:00 pm : The major averages continue to hold their recent levels with the Nasdaq (-0.1%) trading ahead of the other indices. The tech-heavy index has displayed strength throughout the month, and despite today's downtick, it holds a solid month-to-date gain of 5.2%.

Today's session marks the end of the month and the end of the quarter. The Nasdaq has had a strong showing over the past three months as it holds a quarter-to-date gain of 10.9%. This puts it well ahead of the Dow, which is on track to register just a 1.7% gain for the third quarter.

Even though equities have erased half of their early losses, the CBOE Volatility Index (VIX 16.71, +1.25) remains near its highest level of the day as participants adjust their near-term volatility expectations.DJ30 -91.15 NASDAQ -3.41 SP500 -6.84 NASDAQ Adv/Vol/Dec 990/729.2 mln/1455 NYSE Adv/Vol/Dec 915/219.7 mln/1999

11:35 am : The S&P 500 trades near the middle of its range after the rebound effort placed the index back above its 50-day moving average (1680). However, the S&P remains lower by 0.5% with influential sectors preventing the broader market from returning to its flat line.

At this juncture, only the energy sector trades with a loss of 1.0%. Meanwhile, the remaining cyclical groups hold losses between 0.4% and 0.7%. The materials sector (-0.4%) trades ahead of the other growth-sensitive groups as miners and steelmakers contribute to the outperformance. The Market Vectors Gold Miners ETF (GDX 25.20, +0.03) sports a gain of 0.1% and the Market Vectors Steel ETF (SLX 45.02,-0.04) is off 0.1%.DJ30 -93.11 NASDAQ -10.38 SP500 -8.27 NASDAQ Adv/Vol/Dec 586/653.9 mln/1581 NYSE Adv/Vol/Dec 852/200.2 mln/2048

11:00 am : The S&P 500 trades lower by 0.5% after spending the past hour climbing off its opening lows. The benchmark index has been able to halve its early losses, but all ten sectors continue to hover in the red.

Energy, financials, and technology began the session with losses close to 1.0%, but the subsequent rebound saw the three climb off their lows. Currently, the three cyclical sectors trade with losses ranging between 0.5% and 0.8%. Meanwhile, health care (-0.2%) and utilities (-0.2%) are the top performing sectors.

Elsewhere, Treasuries have surrendered their early gains and the benchmark 10-yr yield now trades higher by one basis point at 2.64%.DJ30 -104.21 NASDAQ -12.78 SP500 -8.53 NASDAQ Adv/Vol/Dec 744/526.8 mln/1639 NYSE Adv/Vol/Dec 754/168.2 mln/2116

10:30 am : All 10 S&P 500 sectors are in the red, energy and metals commodities are all lower (excl copper, which is flat), all despite the weakness in the dollar index.

Most agriculture commodities are higher this morning, however, despite weakness everywhere else.

Corn, wheat, oats, ethanol, coffee, orange juice, sugar, cotton and lumber futures are all trading higher this morning. Soybeans, rice and milk futures are all lower. But I think it's worth keeping this in mind... the gains is most commodities (mixed b/w both grains and soft commodities).

Back to energy, crude oil and natural gas have been in the red all day so far and are still near session lows. Nov crude fell as low as $101.05/barrel and is now -1.3% at $101.53/barrel. Nov nat gas is currently -2.0% at $3.52/MMbtu.

Precious metals are climbing higher in recent action. Dec gold is now -0.8% at $1328.20/oz, Dec silver is -0.8% at $21.66/oz.DJ30 -106.36 NASDAQ -17.79 SP500 -9.22 NASDAQ Adv/Vol/Dec 602/415.8 mln/1746 NYSE Adv/Vol/Dec 560/138 mln/2302

10:00 am : The major averages continue to hover near their opening lows with the S&P 500 down 0.8%. Today's lower open pressured the benchmark index below its 50-day average (1679/1680) for the first time since September 9.

All ten sectors continue to trade in negative territory with cyclical groups registering losses between 0.7% and 1.1%. Elsewhere, Treasuries continue to hold modest gains with the 10-yr yield down one basis point at 2.61%.

Given the uncertainty related to the looming government shutdown, the CBOE Volatility Index (VIX 17.29, +1.83) is at its highest level since September 3.DJ30 -142.21 NASDAQ -29.83 SP500 -13.01 NASDAQ Adv/Vol/Dec 427/254.3 mln/1876 NYSE Adv/Vol/Dec 361/93.9 mln/2473

09:45 am : The major averages opened the session in negative territory with all ten sectors trading lower. The S&P 500 holds a loss of 0.8% with energy (-1.1%), technology (-1.0%), and financials (-0.9%) pacing the early losses.

On the upside, the utilities sector (-0.1%) is the top early performer while remaining countercyclical sectors trade mixed. Consumer staples (-0.5%) and health care (-0.3%) outperform while the telecom services space (-0.9%) lags.

Just released, the September Chicago PMI rose to 55.7 from 53.0 while the Briefing.com consensus expected an uptick to 53.7.DJ30 -136.91 NASDAQ -34.00 SP500 -12.71 NASDAQ Adv/Vol/Dec 382/178.9 mln/1860 NYSE Adv/Vol/Dec 391/74.7 mln/2404

09:13 am : [BRIEFING.COM] S&P futures vs fair value: -13.70. Nasdaq futures vs fair value: -27.80. The major averages will begin today's session with notable losses as investors grapple with political turmoil around the world. In Europe, markets have been pressured by the resignation of five PDL ministers from the coalition government. Greece was not left out of the news flow with the leader of the Golden Dawn party Nikolaos Michaloliakos being placed under arrest and charged with belonging to a criminal organization.

Meanwhile, the political situation in the U.S. is little changed from Friday. After the Senate passed a stopgap funding bill without a provision to defund Obamacare, the House countered by adding a one-year Obamacare delay to the funding bill before sending it back to the Senate. With a midnight shutdown looming, investors should be on the lookout for headlines from Washington throughout the day.

Treasuries received a modest overnight bid, but retraced their gains in the past hour. The benchmark 10-yr yield is little changed at 2.63%.

The September Chicago PMI will be reported at 9:45 ET.

08:57 am : [BRIEFING.COM] S&P futures vs fair value: -14.00. Nasdaq futures vs fair value: -28.80. The S&P 500 futures trade lower by 0.9% amid political turmoil in Italy and the United States.

It was a sea of red across Asia as all of the major bourses, aside from China's Shanghai Composite (+0.7%), ended with losses. Fears of a U.S. Government shutdown weighed, but sellers were worried over the developments in Italy after Silvio Berlusconi withdrew five PDL ministers from the coalition government. Japan's Nikkei (-2.1%) led the major bourses lower, but emerging markets like the Philippines PSEi (-3.0%), Indonesia's Jakarta Composite (-2.4%), and Thailand's SET (-2.4%) were hit the hardest. China's Shanghai Composite (+0.7%) was the leader despite HSBC Flash Manufacturing PMI slipping to 50.2 (51.2 expected, 51.2 previous). Data from the rest of the region saw Japanese retail sales post an in-line increase of 1.1% year-over-year and preliminary industrial production miss estimates with a -0.7% month-over-month reading (-0.2% expected). Elsewhere, Australian private sector credit climbed a less than expected 0.3% month-over-month (0.4% expected) and India's current account deficit widened to $21.8 billion ($18.1 billion previous).

Japan's Nikkei closed lower by 2.1% as exporters lagged thanks to the strong yen. Toyota Motor shed 2.5% and Honda Motor gave up 3.0%. Elsewhere, financials were under pressure as Nomura Holdings fell 3.7%, leading the sector lower.

In Hong Kong, the Hang Seng lost 1.5% as trade broke down to a three-week low. Financials were weak as China Merchants Bank gave up 1.8%.

China's Shanghai Composite advanced 0.7% to post a second day of gains. Names tied to the recently announced free-trade zone in Shanghai outperformed as Shanghai Jinqiao Export and Shanghai Waigaoqiao both added close to 4.0%. The Shanghai Composite will be closed the remainder of the week for Golden Week.

Major European indices hover near their lows in reaction to the developments in Italy where PDL leader Silvio Berlusconi withdrew his ministers from the ruling coalition. Following the collapse of government, Prime Minister Enrico Letta is scheduled to face a confidence vote on Wednesday. Italy's MIB leads European indices to the downside with a loss of 1.9% and the benchmark 10-yr yield trades higher by nine basis points at 4.51%. Elsewhere, the head of the Greek Golden Dawn party Nikolaos Michaloliakos was arrested and charged with belonging to a criminal organization. Regional economic data was plentiful. Eurozone CPI increased 1.1% year-over-year (1.3% expected, 1.3% prior) and core CPI rose 1.0% year-over-year (1.1% expected, 1.1% last). Germany's retail sales rose 0.5% month-over-month (0.8% consensus, -0.2% prior) while the year-over-year reading ticked up 0.3% (0.4% forecast, 2.9% last). Great Britain's mortgage approvals came in at 62,000 (61,000 expected, 61,000 prior) and mortgage lending rose GBP1.00 billion (GBP0.90 billion forecast, GBP0.80 billion previous). Separately, net lending to individuals increased GBP1.60 billion, as expected. Italy's CPI slipped 0.3% month-over-month (-0.1% expected, 0.4% prior) while the year-over-year reading increased 0.9% (1.1% forecast, 1.2% previous). Separately, PPI fell 2.0% year-over-year (-1.6% expected, -1.3% prior) while the month-over-month reading ticked up 0.2%, as expected. French PPI rose 0.3% month-over-month (0.2% expected, 0.7% prior). Spain reported a current account surplus of EUR1.63 billion (EUR2.57 billion last) and saw its Business Confidence Index remain at -12 (-11 expected).

Great Britain's FTSE is lower by 0.9% as miners pace the decline. Anglo American, Antofagasta, Fresnillo, and Rio Tinto are all down between 2.8% and 3.7%. Homebuilder Persimmon outperforms with a gain of 2.2% after Prime Minister David Cameron said the scheme allowing people to take out 95% mortgages will be launched next week.

In Germany, the DAX sports a loss of 1.1% as 29 of 30 components trade lower. Commerzbank and Deutsche Bank are down 3.1% and 1.9%, respectively. On the upside, Fresenius Medical Care holds a slim gain of 0.4%.

France's CAC trades down 1.4% amid broad weakness. Credit Agricole and Societe Generale hold respective losses of 2.6% and 2.3%. Consumer names have displayed relative weakness as Danone Pernod Ricard trade little changed.

In Italy, the MIB is down 1.9% with bank shares broadly weaker. Intesa Sanpaolo trades lower by 4.4% after Chief Executive Officer Enrico Cucchiani resigned on Sunday. Silvio Berlusconi's Mediaset holds a loss of 3.9%.

08:28 am : [BRIEFING.COM] S&P futures vs fair value: -13.50. Nasdaq futures vs fair value: -25.00. U.S. equity futures trade near their lows with the S&P 500 futures down 0.9%. Equities are poised for a sharply lower open amid global political turmoil. In Europe, the Italian government has collapsed after PDL leader Silvio Berlusconi withdrew from the coalition along with some of his party's key ministers. While the near-term future of the country remains largely unknown, Prime Minister Enrico Letta will face a confidence vote in the Senate on Wednesday.

Domestically, the weekend came and went without an agreement to keep the government open into tomorrow. After the Senate approved a funding bill without the provision to defund Obamacare, the House of Representatives added a provision to delay health care funding for a year before sending the bill back to the Senate. Given the fluid situation, headlines from Washington are expected throughout the day.

Treasuries have received a modest bid and the benchmark 10-yr yield is lower by two basis points at 2.60%.

08:02 am : [BRIEFING.COM] S&P futures vs fair value: -13.80. Nasdaq futures vs fair value: -24.30. U.S. equity futures trade sharply lower with the S&P 500 futures down 0.9%. The notable weakness comes after the weekend failed to produce an agreement to keep the government open past October 1. In addition, global markets are reacting negatively to the developments in Italy where PDL leader Silvio Berlusconi withdrew his ministers from the coalition. Following the collapse of government, Prime Minister Enrico Letta is scheduled to face a confidence vote on Wednesday. Italy's MIB leads European indices to the downside with a loss of 1.9% and the benchmark 10-yr yield trades higher by nine basis points at 4.51%.

Reviewing overnight developments:

Asian markets ended mixed. Japan's Nikkei -2.1%, Hong Kong's Hang Seng -1.5%, and China's Shanghai Composite +0.7%.

In regional economic data:

China's HSBC Manufacturing PMI slipped to 50.2 from 51.2 (51.2 expected).

Japan's industrial production slipped 0.7% month-over-month (-0.4% expected, 3.4% prior), retail sales increased 1.1% year-over-year (1.0% forecast, -0.3% prior), and large retailers' sales ticked down 0.1% month-over-month (1.2% consensus, -1.6% last). Separately, Manufacturing PMI improved to 52.5 from 52.2 (52.2 expected). Also of note, construction orders increased 21.4% (13.7% last) and housing starts climbed 8.8% year-over-year (12.7% expected, 12.0% previous).

South Korea's industrial production rose 1.8% month-over-month (0.5% consensus, -0.3% prior) while the year-over-year reading increased 3.3% (2.4% expected, 0.9% previous). In addition, retail sales rose 0.4% month-over-month (0.0% expected, 1.2% prior) and the BSI Manufacturing Index rose to 82.0 from 78.0.

Looking at news:

China's Shanghai Composite outperformed other regional indices as the Shanghai Free Trade Zone opened for business. Markets in China will be closed for the remainder of the week for Golden Week.

Major European indices hover near their lows. Great Britain's FTSE -0.8%, Germany's DAX -1.1%, and France's CAC -1.3%. Elsewhere, Spain's IBEX -1.1% and Italy's MIB -1.9%.

Regional economic data was plentiful:

Eurozone CPI increased 1.1% year-over-year (1.3% expected, 1.3% prior) and core CPI rose 1.0% year-over-year (1.1% expected, 1.1% last).

Germany's retail sales rose 0.5% month-over-month (0.8% consensus, -0.2% prior) while the year-over-year reading ticked up 0.3% (0.4% forecast, 2.9% last).

Great Britain's mortgage approvals came in at 62,000 (61,000 expected, 61,000 prior) and mortgage lending rose GBP1.00 billion (GBP0.90 billion forecast, GBP0.80 billion previous). Separately, net lending to individuals increased GBP1.60 billion, as expected.

Italy's CPI slipped 0.3% month-over-month (-0.1% expected, 0.4% prior) while the year-over-year reading increased 0.9% (1.1% forecast, 1.2% previous). Separately, PPI fell 2.0% year-over-year (-1.6% expected, -1.3% prior) while the month-over-month reading ticked up 0.2%, as expected.

French PPI rose 0.3% month-over-month (0.2% expected, 0.7% prior).

Spain reported a current account surplus of EUR1.63 billion (EUR2.57 billion last) and saw its Business Confidence Index remain at -12 (-11 expected).

In news:

Italy's MIB is pacing the decline in Europe with bank shares displaying notable losses. Intesa Sanpaolo trades lower by 3.7% after Chief Executive Officer Enrico Cucchiani resigned on Sunday.

In Greece, the head of the Golden Dawn party Nikolaos Michaloliakos was arrested and charged with belonging to a criminal organization.

In U.S. corporate news:

Colgate-Palmolive (CL 60.15, +0.22) is +0.4% after Morgan Stanley upgraded the stock to 'Overweight' from 'Equal Weight.'

Major financials are among the early laggards with Bank of America (BAC 13.69, -0.21), Citigroup (C 48.18, -0.71), Goldman Sachs (GS 157.00, -2.85), and JPMorgan Chase (JPM 51.50, -0.74) down between 1.3% and 1.7%.

The September Chicago PMI will be reported at 9:45 ET.

07:04 am : [BRIEFING.COM] S&P futures vs fair value: -13.00. Nasdaq futures vs fair value: -23.00.

07:04 am : Nikkei...14455.80...-304.30...-2.10%. Hang Seng...22859.86...-347.20...-1.50%.

07:04 am : FTSE...6456.58...-56.10...-0.90%. DAX...8568.67...-92.80...-1.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com HomepageMarket Update