Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

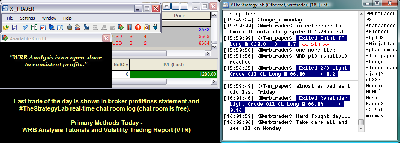

Attachment:

120712-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1280.00.png [ 75.8 KiB | Viewed 349 times ]

120712-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1280.00.png [ 75.8 KiB | Viewed 349 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, EuroFX 6E futures @

$800.00 dollars or +0.0064 ticks and Light Crude Oil CL (WTI) futures @

$480.00 dollars or +0.48 points.

Total Profit @ $1280.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with

price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=111&t=1387 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=197&t=1686 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

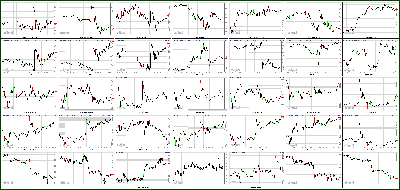

Stocks Finish Mixed As Apple Drags Down Techs Attachment:

120712-Key-Price-Action-Markets.png [ 540.39 KiB | Viewed 360 times ]

120712-Key-Price-Action-Markets.png [ 540.39 KiB | Viewed 360 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney)

The Nasdaq snapped a two-week winning streak Friday, dragged down by a nearly 9% sell-off in Apple shares. But the S&P and Dow managed to eke out a third straight week of modest gains.

U.S. stocks ended Friday in mixed territory as euphoria from better-than-expected jobs numbers faded in the wake of a report showed waning consumer confidence.

The Dow Jones industrial average gained 0.6%, helped by shares of JPMorgan Chase (JPM, Fortune 500) and Bank of America (BAC, Fortune 500), while the S&P 500 moved up 0.3%. The Nasdaq dropped by 0.4%, after Apple (AAPL, Fortune 500) fell 2.5%.

Investors learned ahead of the opening bell that the U.S. economy added more jobs than expected in November, and the unemployment rate fell to a four-year low.

But the latest consumer sentiment reading from Thomson Reuters/University of Michigan served as a stark reminder that consumers still are nervous The index unexpectedly fell to 74.5 in December, coming in way below forecasts and down from 82.7 in November.

On top of that, worries about the fiscal cliff and ongoing back-and-forth wrangling in Washington continue to keep investors on edge. If lawmakers fail to strike a deal before the end of the year to avert scheduled tax increases and spending cuts, they risk pushing the U.S. economy into recession.

* China's top 10 brandsLooking at individual stocks, Netflix (NFLX) CEO Reed Hastings is under investigation by the Securities and Exchange Commission for posting information about the company on his Facebook page that he hadn't disclosed to the SEC. Shares dipped slightly.

* Video - SEC: Don't you have better things to do?Shares of Smith & Wesson Holding Corp. (SWHC) dropped nearly 9% even though the gun maker reported strong quarterly earnings and boosted its full-year outlook.

Shares of publisher McGraw-Hill (MHP, Fortune 500) rose nearly 4% after the company announced that it would pay a one-time special dividend before year-end.

Western Gas Equity Partners (WGP) rose nearly 28% in its IPO Friday.

* Fear & Greed IndexEuropean markets were mixed after Germany's Bundesbank cut its growth forecasts and warned there was a risk of Europe's biggest economy dipping into recession in early 2013.

Asian markets also ended mixed. The Shanghai Composite performed best, adding 1.6%.

The dollar was firmer against the euro, the British pound and the Japanese yen.

Oil prices for January delivery rose slightly to $85.93 a barrel. Gold prices for February delivery edged up to $1,704.00.

The price on the 10-year Treasury fell, pushing the yield up to 1.63% from 1.58% late Thursday.

Market Update

Market Update 4:15 pm : Equities started the day in the black following the release of November nonfarm payrolls, which revealed an addition of 146,000 jobs. However, the optimism was short-lived and stocks surrendered their early gains after the preliminary reading of the December Michigan Sentiment fell short of estimates. The remainder of the session was relatively quiet as the S&P 500 traded near its unchanged line, the Nasdaq hovered near its lows, while the Dow spent the day climbing back to its highs. As a result, the benchmark S&P 500 index finished higher by 0.3%.

This morning, House Speaker Boehner and Minority Leader Pelosi both spoke before the media in Washington, but their message remained the same. During his remarks, Speaker Boehner said that no progress has been made in negotiations and the White House "has wasted another week." Meanwhile, Representative Pelosi reiterated that Democrats stand ready to extend Bush-era tax cuts for all but top 2% of earners.

Financials have outperformed after Wednesday's announcement from Citigroup (C 37.64, +0.62) indicated the company will dismiss more than 11,000 employees. Citigroup advanced 1.7% today and most majors saw comparable gains. However, Goldman Sachs (GS 116.57, -0.63) and Wells Fargo (WFC 33.23, +0.09) missed out on the sector-wide rally. Earlier, the Commodity Futures Trading Commission ordered Goldman Sachs to pay a $1.5 million civil monetary penalty to settle charges stemming from failure to diligently supervise its employees in late 2007.

Although domestic financials advanced, their European counterparts were relatively weaker. Spain's Banco Santander (SAN 7.59, -0.05) and Germany's Deutsche Bank (DB 44.82, -0.67) settled lower by 0.7% and 1.5%, respectively.

The tech sector was the biggest laggard and Apple (AAPL 533.25, -13.99) continued its weakness. The largest tech component lost 2.6% during today's session, and is down nearly 10.0% since Monday.

Elsewhere in technology, networking stocks were generally lower and Cisco Systems (CSCO 19.33, -0.14) shed 0.7%. Earlier, the company held its Analyst Day where Chief Executive Officer said Cisco has "gone too long" without making an acquisition.

Major hard drive manufacturers have enjoyed a strong week. Since Monday, Seagate (STX 28.34, -0.19) has added over 12.0% while Western Digital (WDC 37.60, +0.50) has rallied more than 11.0%. Today, the two headed in opposite directions. Seagate slipped 0.7% while Western Digital gained 1.4%.

In notable analyst action, 3D Systems (DDD 45.61, +1.07) advanced 2.4% after BB&T Capital Markets initiated coverage with a ‘Buy' rating and a $60 price target.

The GEO Group (GEO 32.00, +2.56) was the second-best S&P 500 component. The correctional facility operator surged 8.7% after the company authorized a special dividend of $350 million, and announced it has taken critical steps towards its planned conversion to a Real Estate Investment Trust. As a REIT, the company is expected to generate between $215 and $225 million in 2013 funds from operations. Peer Corrections Corporation of America (CXW 35.48, +1.37) gained 4.0%.

Last evening, Smith & Wesson (SWHC 9.92, -0.93) reported earnings in-line with the November preannouncement. The company's strong quarter was punctuated by upside third quarter and full-year earnings and revenue guidance. In addition, the Board of Directors has approved a $20 billion share repurchase program which is scheduled to run through June 30, 2013. The stock was up as much as 3.0% in pre-market trade, but settled lower by 8.6% Meanwhile, peer Sturm, Ruger (RGR 51.44, -2.00) lost 3.7%.

Nonfarm payrolls came in at 146K versus the 90K expected by the Briefing.com consensus. The prior reading was revised down to 138K from 171K. Nonfarm private payrolls added 147K against the 120K consensus. The unemployment rate was reported at 7.7%, ahead of the Briefing.com consensus which called for the figure to come in at 8.0%.

Hourly earnings rose by 0.2% while the expectations called for an uptick of 0.1%. Lastly, average workweek was reported at 34.4, which was in-line with the Briefing.com consensus.

The preliminary University of Michigan Survey for December came in at 74.5, which is lower than the 82.7 that was posted in the prior month, and worse than the reading of 82.4 that had been expected by the Briefing.com consensus.

According to the Federal Reserve, consumer credit increased by $14.2 billion in October. This follows prior month's reading of a $11.4 billion increase, and is higher than the $9.9 billion that had been broadly expected among economists polled by Briefing.com.

Week in Review: Stocks Drift as Fiscal Cliff Looms

Monday's session began on a positive note as upbeat European trade contributed to the bullish sentiment. However, the strength was temporary and the S&P 500 turned lower once the November ISM Index of 49.5 missed expectations. After sliding to its lows shortly after midday, the S&P 500 remained in the red and settled lower by 0.5%. The materials sector was the biggest laggard as chemical producers saw broad weakness. In addition, utility and industrial stocks underperformed as well.

Tuesday's trade was confined to a narrow range as the S&P 500 opened near its flat line, and spent the entire day within points of the unchanged level. At midday, Bloomberg TV aired an interview with President Obama, but his remarks were in-line with recent statements. The market did not receive notable economic data and sentiment-driving headlines were limited as well. As such, the benchmark index ended the choppy day with a loss of 0.2%. Netflix (NFLX 85.98, -0.19) surged 8.3% after the company announced a multi-year premium pay-TV window agreement with Walt Disney (DIS 49.24, +0.18).

On Wednesday, stocks finished the session on a higher note, but gave up a large portion of their gains in the final half-hour. The major averages showed notable divergence as the Dow led with a gain of 0.6% while Nasdaq lost 0.8%. The tech-heavy index lagged the broader market due to considerable weakness in shares of Apple (AAPL 533.25, -13.99), which fell 6.4% and saw their largest one-day drop in four years. Meanwhile, the S&P 500 held near its session high for the majority of the afternoon before late-day selling trimmed its gain to 0.2%.

Thursday opened with initial uncertainty before the major averages staged a climb to their respective highs. Overseas, Standard & Poor's lowered Greece's long term credit rating to ‘Select Default' from ‘CCC.' Meanwhile, Germany's DAX closed at its highest level in nearly five years. Domestically, trade was confined to a narrow range, but late-day buying lifted the S&P 500 to a slim gain of 0.3%. Deutsche Bank (DB 44.82, -0.67) slid 1.3% after reports from Reuters indicated the bank may have hid up to $12 billion in losses in order to avoid having to accept a government bailout.DJ30 +81.09 NASDAQ -11.23 SP500 +4.13 NASDAQ Adv/Vol/Dec 1142/1.57 bln/1300 NYSE Adv/Vol/Dec 1649/606.3 mln/1358

3:30 pm : Crude oil retreated from its overnight electronic session high of $86.92 per barrel and trended lower during today's pit trade. The energy component lost the earlier momentum as concerns over the "fiscal cliff" overshadowed better-than-expected jobs data. It closed lower for a fourth consecutive session, bringing the week's losses to 3.4% as it settled at $85.88 per barrel.

Natural gas brushed a session high of $3.69 per MMBtu in morning pit action but pulled-back into the red. It trended lower for the remainder of the session and booked a 0.3% loss for the week as it closed at $3.55 per MMBtu.

Precious metals tumbled to their pit session lows in early floor action following the jobs reports released earlier this morning. Gold slid to a one-month low of $1684.10 per ounce while silver fell as low as $32.68 per ounce. However, the move quickly reversed and both metals recovered back into positive territory. Despite erasing earlier losses and settling slightly above the unchanged line at $1705.10 per ounce, gold booked a 0.5% loss for the week. Silver closed the session flat at $33.13 per ounce, bringing the week's losses to 0.5%.DJ30 +52.86 NASDAQ -16.61 SP500 +1.19 NASDAQ Adv/Vol/Dec 1052/1.28 bln/1375 NYSE Adv/Vol/Dec 1444/411.1 mln/1537

3:00 pm : Equities are holding their recent levels and the S&P 500 is firmer by 0.2%.

According to the Federal Reserve, consumer credit increased by $14.2 billion in October. This follows prior month's reading of a $11.4 billion increase, and is higher than the $9.9 billion that had been broadly expected among economists polled by Briefing.com.DJ30 +57.72 NASDAQ -11.95 SP500 +2.33 NASDAQ Adv/Vol/Dec 1102/1.16 bln/1329 NYSE Adv/Vol/Dec 1435/379.1 mln/1535

2:30 pm : Equities are maintaining their recent levels and the S&P 500 is adding 0.2%.

Less than 30 companies covered by Briefing.com will report their quarterly results next week. Adobe Systems (ADBE 35.45, +0.31), Dollar General (DG 46.98, +0.55), and Costco (COST 98.82, +0.35) are the most notable names among those scheduled to report.

On Tuesday morning, Dollar General is expected to report earnings of $0.60. Meanwhile, the Capital IQ consensus expects the company to report quarterly revenue of $3.96 billion.

Costco will report its results ahead of Wednesday's open. Forecasts call for the wholesale retailer to announce earnings of $0.93 on revenue of $23.54 billion.

Notable earnings will be rounded out on Thursday afternoon when Adobe reports. The software company is expected to reveal earnings of $0.57 on $1.10 billion in revenue.DJ30 +54.10 NASDAQ -12.49 SP500 +1.99 NASDAQ Adv/Vol/Dec 1069/1.07 bln/1362 NYSE Adv/Vol/Dec 1430/349.8 mln/1536

2:00 pm : The major indices continue to hover near their recent levels and the S&P 500 is flat.

Financials have seen relative strength after Wednesday's announcement from Citigroup (C 37.47, +0.45) indicated the company will dismiss more than 11,000 employees. Citigroup is advancing 1.2% today and most majors are seeing comparable gains. However, Goldman Sachs (GS 116.50, -0.70) and Wells Fargo (WFC 33.15, +0.01) are missing out on the sector-wide rally.

Although domestic financials are outperforming, their European counterparts are relatively weaker. Spain's Banco Santander (SAN 7.54, -0.09) and Germany's Deutsche Bank (DB 44.74, -0.75) are down 1.3% and 1.6%, respectively.DJ30 +45.81 NASDAQ -18.05 SP500 +0.47 NASDAQ Adv/Vol/Dec 977/966.1 mln/1427 NYSE Adv/Vol/Dec 1384/318.9 mln/1569

1:30 pm : The Dow is higher by 0.5% as it nears its session high.

The Dow Jones Transportation Average is underperforming the industrials, up 0.1%. Trucking stocks were pressured over the course of the week, and major carriers are seeing weakness once again. JB Hunt (JBHT 58.36, -0.35) is down 0.6% and Con-way (CNW 27.39, -0.12) is shedding 0.5%.

Elsewhere, railroads are mixed. CSX (CSX 19.93, -0.31) is sliding 1.5% while Kansas City Southern (KSU 79.71, +1.11) is higher by 1.4%.DJ30 +59.09 NASDAQ -14.11 SP500 +1.77 NASDAQ Adv/Vol/Dec 1010/890.5 mln/1389 NYSE Adv/Vol/Dec 1428/299.6 mln/1506

1:00 pm : Equities began the day on a higher note after November nonfarm payrolls were reported at 146,000, which was well ahead of the 90,000 expected by the Briefing.com consensus. However, the strength did not hold as the major indices began slipping off their respective highs shortly after the open. The key averages slid further after the preliminary December Michigan Consumer Sentiment Survey missed expectations. At midday, the S&P 500 is flat.

The tech sector is the biggest laggard as Apple (AAPL 533.31, -13.93) trades lower by 2.6% and weighs on the space.

Networking stocks are seeing relative weakness as well. Cisco Systems (CSCO 19.31, -0.17) and F5 Networks (FFIV 91.66, -0.85) are both down near 0.9%. Earlier, Cisco management held its Analyst Day where Chief Executive Officer said the company has "gone too long" without making an acquisition.

Major hard drive manufacturers have enjoyed a strong week. Since Monday, Seagate (STX 28.36, -0.17) has added 12.3% while Western Digital (WDC 36.98, -0.11) has rallied 10.6%. Today, the two stocks are registering slight losses. STX is off by 0.5%, while WDC is shedding 0.2%.

In notable analyst action, 3D Systems (DDD 45.55, +1.01) is higher by 2.3% after BB&T Capital Markets initiated coverage with a ‘Buy' rating and a $60 price target.

The GEO Group (GEO 31.53, +2.09) is the best performing S&P 500 component. The correctional facility operator is surging 7.1% after the company authorized a special dividend of $350 million and announced it has taken critical steps towards its planned conversion to a Real Estate Investment Trust. As a REIT, the company is expected to generate between $215 and $225 million in 2013 funds from operations. Peer Corrections Corporation of America (CXW 35.07, +0.96) is advancing 2.8%.

Last evening, Smith & Wesson (SWHC 10.07, -0.77) reported earnings in-line with the November preannouncement. The company's strong quarter was punctuated by upside third quarter and full-year earnings and revenue guidance. In addition, the Board of Directors has approved a $20 billion share repurchase program which is scheduled to run through June 30, 2013. The stock was up as much as 3.0% in pre-market trade, but it currently trades lower by 7.1% Meanwhile, peer Sturm, Ruger (RGR 51.40, -2.04) is off by 3.8%.

Nonfarm private payrolls added 147K against the 120K consensus. The unemployment rate was reported at 7.7%, ahead of the Briefing.com consensus which called for the figure to come in at 8.0%.

Hourly earnings rose by 0.2% while the expectations called for an uptick of 0.1%. Lastly, average workweek was reported at 34.4, which was in-line with the Briefing.com consensus.

The preliminary University of Michigan Survey for December came in at 74.5, which is lower than the 82.7 that was posted in the prior month, and worse than the reading of 82.4 that had been expected by the Briefing.com consensus.

Today's economic data will be topped-off with the consumer credit report scheduled for a 15:00 ET release.DJ30 +53.55 NASDAQ -13.80 SP500 +0.33 NASDAQ Adv/Vol/Dec 1015/824.5 mln/1370 NYSE Adv/Vol/Dec 1240/278.1 mln/1512

12:30 pm : Equities are holding their recent levels and the S&P 500 is flat.

The GEO Group (GEO 31.47, +2.03) is the best performing S&P 500 component. The correctional facility operator is surging 6.9% after the company authorized a special dividend of $350 million and announced it has taken critical steps towards its planned conversion to a Real Estate Investment Trust. As a REIT, the company is expected to generate between $215 and $225 million in 2013 funds from operations. Peer Corrections Corporation of America (CXW 35.05, +0.94) is advancing 2.8%.DJ30 +44.60 NASDAQ -16.60 SP500 +0.31 NASDAQ Adv/Vol/Dec 977/740.6 mln/1389 NYSE Adv/Vol/Dec 1356/250.5 mln/1543

12:00 pm : The major averages are holding their recent levels and the Nasdaq is the weakest index, down 0.6%.

The tech sector is the biggest laggard as Apple (AAPL 534.16, -13.07) trades lower by 2.4% and weighs on the space.

Meanwhile, networking stocks are generally lower. Cisco Systems (CSCO 19.20, -0.27) and F5 Networks (FFIV 91.22, -1.29) are both down near 1.4%. Cisco is currently holding its Analyst Day where Chief Executive Officer said the company has "gone too long" without making an acquisition.

Major hard drive manufacturers have enjoyed a strong week. Since Monday, Seagate (STX 28.49, -0.04) has added 12.3% while Western Digital (WDC 37.15, +0.05) has rallied 10.6%. Today, the two stocks are showing little change. STX is off by 0.2%, while WDC is adding 0.1%.

In notable analyst action, 3D Systems (DDD 45.40, +0.86) is higher by 1.9% after BB&T Capital Markets initiated coverage with a ‘Buy' rating and a $60 price target.DJ30 +27.64 NASDAQ -18.86 SP500 -1.28 NASDAQ Adv/Vol/Dec 945/676.7 mln/1397 NYSE Adv/Vol/Dec 1300/230.2 mln/1575

11:30 am : The S&P 500 marked fresh session lows after House Speaker John Boehner addressed the media in Washington. During his remarks, the Speaker said no progress has been made in negotiations and the White House "has wasted another week." Following the Speaker's comments, the benchmark index is flat.

Last evening, Smith & Wesson (SWHC 10.24, -0.61) reported earnings in-line with the November preannouncement. The company's strong quarter was punctuated by upside third quarter and full-year earnings and revenue guidance. In addition, the Board of Directors has approved a $20 billion share repurchase program which is scheduled to run through June 30, 2013. The stock was up as much as 3.0% in pre-market trade, but it currently trades lower by 5.5% Meanwhile, peer Sturm, Ruger (RGR 51.52, -1.91) is off by 3.6%.DJ30 +31.91 NASDAQ -11.93 SP500 +0.45 NASDAQ Adv/Vol/Dec 1010/566.6 mln/1276 NYSE Adv/Vol/Dec 1393/200.5 mln/1457

11:00 am : The major averages have slipped to their respective lows and the S&P 500 is off by 0.1%.

The materials sector is outperforming on the strength of metal producers. The Market Vectors Steel ETF (SLX 45.12, +0.27) is higher by 0.6% and Cliffs Natural Resources (CLF 29.56, +0.37) is one of the top individual performers.

Elsewhere, miner Freeport-McMoRan (FCX 32.18, +1.37) is higher by 4.5% as it attempts to rebound from recent weakness. On Wednesday, Freeport slumped 16.0% after the company confirmed it will acquire Plains Exploration & Production (PXP 44.62, +1.44) and McMoRan Exploration (MMR 15.29, +0.27) in transactions totaling $20 billion.DJ30 +27.15 NASDAQ -11.56 SP500 -0.75 NASDAQ Adv/Vol/Dec 986/454.6 mln/1281 NYSE Adv/Vol/Dec 1328/169.9 mln/1452

10:30 am : Precious metals tumbled to pit session lows in volatile trade on strong jobs data released earlier this morning. Feb gold slid to $1684.10 while Mar silver fell as low as $32.68. Buyers quickly stepped in and took prices back into the black and to new session highs. Gold is currently up 0.2% at $1705.00, and silver is at $33.22, or up 0.3%.

Jan crude oil popped to an overnight session high of $86.92 following the jobs report despite a stronger dollar index. However, the energy component erased the gain shortly after floor trade opened. Prices fell back into negative territory and are currently down 0.2% at $86.11.

Jan natural gas came off its session low of $3.62 and has been inching higher since pit trade opened. It broke above the break-even level in recent action and is now up 0.2% at $3.68.DJ30 +32.94 NASDAQ -9.83 SP500 -0.23 NASDAQ Adv/Vol/Dec 1034/349.5 mln/1162 NYSE Adv/Vol/Dec 1393/141.2 mln/1364

10:00 am : The major averages ticked lower following the release of the preliminary Michigan Sentiment Survey. The S&P 500 is adding 0.1%.

The preliminary University of Michigan Survey for December came in at 74.5, which is lower than the 82.7 that was posted in the prior month, and worse than the reading of 82.4 that had been expected by the Briefing.com consensus.DJ30 +34.84 NASDAQ -6.53 SP500 +1.22 NASDAQ Adv/Vol/Dec 1034/201.1 mln/1075 NYSE Adv/Vol/Dec 1467/95.4 mln/1214

09:45 am : After retreating off their early highs, the major averages continue to register gains. The S&P 500 is higher by 0.3%.

High-beta financial stocks appear to be the biggest beneficiaries of the strong jobs report as the sector leads the broader market. Among individual names, Citigroup (C 37.61, +0.59) and Morgan Stanley (MS 16.96, +0.22) are both up near 1.5%.

Meanwhile, telecoms are underperforming as the sector trades lower by 0.3%.

Today's economic data will be topped off by the December Michigan Sentiment and October consumer credit reports. The two readings will be released at 9:55 ET and 15:00 ET, respectively.DJ30 +53.19 NASDAQ +5.10 SP500 +4.20 NASDAQ Adv/Vol/Dec 1141/136.2 mln/894 NYSE Adv/Vol/Dec 1669/74.4 mln/967

09:17 am : [BRIEFING.COM] S&P futures vs fair value: +4.70. Nasdaq futures vs fair value: +11.00. As the open nears, equity futures continue pointing to a higher start to the session. The S&P 500 futures are adding 0.3% following the upbeat November jobs report.

The risk-on sentiment appears to be taking hold going into the open as high-beta names advance. Bank of America (BAC 10.55, +0.10) and Citigroup (C 37.37, +0.35) are both up near 1.0%.

In addition, steelmakers are seeing pre-market strength. AK Steel (AKS 4.16, +0.06) and United States Steel (X 22.11, +0.11) are up 1.5% and 0.5%, respectively.

Today's economic data will be topped off by the December Michigan Sentiment and October consumer credit reports. The two readings will be released at 9:55 ET and 15:00 ET, respectively.

09:03 am : [BRIEFING.COM] S&P futures vs fair value: +5.70. Nasdaq futures vs fair value: +12.30. U.S. equity futures continue to trade near their pre-market highs following the positive November jobs report. The S&P 500 futures are adding 0.4%.

European bourses traded broadly lower until November U.S. nonfarm payrolls beat expectations. The early weakness came after the growth forecast released by Germany's Bundesbank sent shockwaves through the markets. The central bank expects Germany's 2013 real GDP growth of just 0.4%, which is down from the June projection of 1.6%. The bank also warned about the possibility of a recession, potentially as early as the first quarter, with activity picking up in the back half of the year. In addition to regional indices, the euro is trading lower as well. In other economic data, France posted a wider-than-expected government budget balance while British industrial and manufacturing production both missed expectations. Lastly, German industrial production slid 2.6% month-over-month on expectations of a milder decrease of 0.5%.

In the United Kingdom, the FTSE is higher by 0.2% and Centrica is leading the index. The energy supplier is higher by 2.3% after UBS added the stock to its most-preferred list. On the downside, miners are seeing relative weakness. Antofagasta, Eurasian Natural Resources, and Xstrata are all down between 0.4% and 0.7%.

Germany's DAX is firmer by 0.2% and producers of basic materials are advancing. K+S and Linde are both up near 0.5%. On the downside, Deutsche Telekom is off by 1.9% after cutting its dividend.

In France, the CAC is adding by 0.3%. Advertiser Publicis Groupe is leading the way, up 1.0%. Meanwhile, industrial stocks are under pressure. ArcelorMittal and Vallourec are seeing respective losses of 1.2% and 0.8%. In addition, Alcatel-Lucent is sliding 3.1% after the stock was removed from the index.

The major Asian averages finished mixed ahead of today's U.S. nonfarm payroll data. China's Shanghai Composite (+1.6%) outperformed after Shanghai Securities suggested Sichuan province will invest CNY2 trillion in urbanization in 2013. Other reports suggest November CPI will come out at 2.2%, retail sales will grow over 14%, and industrial production will increase 10%. Elsewhere in the region, a 7.3 magnitude earthquake shook northeastern Japan following the Nikkei's close, but there are no reports of any major damage. Meanwhile, the cleanup continues in the Philippines after a deadly typhoon swept across the country in the middle part of the week. Data out overnight saw Australia's trade deficit best forecasts but widen to AUD2.09 billion (AUD2.15 billion expected, AUD1.42 billion previous), Taiwan's trade surplus grow to $3.4 billion ($3.2 billion expected, $3.26 billion previous), and Malaysia's trade surplus climb to $9.60 billion ($7.20 billion expected, $6.5 billion previous).

In Japan, the Nikkei shed 0.2% as trade slipped off a seven-month high. Telecom providers Softbank and KDDI slumped 2.1% and 3.0% respectively on word rival NTT DoCoMo may soon begin selling iPhones. Meanwhile, Sharp surged 8.5% as shares continue to rally on the reported Qualcomm investment in the company.

In Hong Kong, the Hang Seng finished lower by 0.3% as the largest IPO in two years came to market. People's Insurance Co. raised $3.1 billion in its IPO, and shares jumped 6.9% in their debut. Elsewhere, luxury retailer Prada closed limit up, 10%, following its strong earnings.

China's Shanghai Composite gained 1.6% as cement stocks rallied on continued talk of urbanization. Huaxin Cement was the top performer in the group, ending up 5.9%. Meanwhile, spirit markers snapped their five-day losing streak with Wuliangye Yibin rallying 3.4%.

08:33 am : [BRIEFING.COM] S&P futures vs fair value: +6.90. Nasdaq futures vs fair value: +13.80. Equity futures have seen a positive initial reaction to the November employment data. The S&P 500 futures are higher by 0.5%.

Nonfarm payrolls came in at 146K versus the 90K expected by the Briefing.com consensus. The prior reading was revised down to 138K from 171K. Nonfarm private payrolls added 147K against the 120K consensus. The unemployment rate was reported at 7.7%, ahead of the Briefing.com consensus which called for the figure to come in at 8.0%.

Hourly earnings rose by 0.2% while the expectations called for an uptick of 0.1%. Lastly, average workweek was reported at 34.4, which was in-line with the Briefing.com consensus.

08:02 am : [BRIEFING.COM] S&P futures vs fair value: -3.40. Nasdaq futures vs fair value: -5.00. U.S. equity futures are modestly lower as market participants await the November nonfarm payrolls report. The Briefing.com consensus expects the figure to be reported at 90,000. Meanwhile, the unemployment rate is expected to tick up to 8.0%.

Overnight, a handful of Asian indices advanced, while major European bourses are trading lower. In Asia, China's Shanghai Composite was the top performer, gaining 1.6%. There were no economic releases of significance. Instead, the index was supported by positive commentary. A former People's Bank of China advisor expects 2013 GDP to reach 8.0%, and sees CPI at around 2.7%. Meanwhile, the Chinese press sees November CPI of 2.2%, retail sales growing over 14.0% and industrial production rising over 10.0%. Further, Shanghai Securities expects China's Sichuan province to invest CNY2 trillion in urbanization efforts. In Japan, the Nikkei shed 0.2%, but the biggest news hit after the close when a 7.3 magnitude earthquake struck near Tokyo. There are no early reports of any damage, but a tsunami warning of was issued, before officials cancelled the alert. Elsewhere, Hong Kong's Hang Seng slipped 0.3%.

European bourses are broadly lower after the growth forecast released by Germany's Bundesbank sent shockwaves through the markets. The central bank expects Germany's 2013 real GDP growth of just 0.4%, which is down from the June projection of 1.6%. The bank also warned about the possibility of a recession, potentially as early as the first quarter, with activity picking up in the back half of the year. In addition to regional indices, the euro is trading lower as well. In other economic data, France posted a wider-than-expected government budget balance while British industrial and manufacturing production both missed expectations. Lastly, German industrial production slid 2.6% month-over-month on expectations of a milder decrease of 0.5%. Looking at regional indices as they near midday, UK's FTSE is off by 0.1% while France's CAC and Germany's DAX are both lower by 0.2%.

In U.S. corporate news, Netflix (NFLX 85.13, -1.03) is lower by 1.2% after the company and its Chief Executive Officer, Reed Hastings, both received a "Wells Notice" from the Securities and Exchange Commission. The inquiry comes after the CEO published a social media comment which discussed the company's June metrics without submitting them to the SEC.

Smith & Wesson (SWHC 11.13, +0.28) is advancing 2.6% after reporting earnings in-line with the November preannouncement. The company's strong quarter was punctuated by upside third quarter and full-year earnings and revenue guidance. In addition, the Board of Directors has approved a $20 billion share repurchase program which is scheduled to run through June 30, 2013.

In addition to the previously mentioned November nonfarm payrolls, nonfarm private payrolls, unemployment rate, hourly earnings, and average workweek will all be reported at 8:30 ET. In addition, December Michigan Sentiment and October consumer credit will be released at 9:55 ET and 15:00 ET, respectively.

06:21 am : [BRIEFING.COM] S&P futures vs fair value: -1.50. Nasdaq futures vs fair value: -4.00.

06:21 am : Nikkei...9527.39...-17.80...-0.20%. Hang Seng...22191.17...-58.60...-0.30%.

06:21 am : FTSE...5896.39...-5.00...-0.10%. DAX...7524.07...-10.50...-0.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage