Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

112312-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1090.00.png [ 74.65 KiB | Viewed 312 times ]

112312-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1090.00.png [ 74.65 KiB | Viewed 312 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$400.00 dollars or +4.00 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$690.00 dollars or +0.69 points.

Total Profit @ $1,090.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1375 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

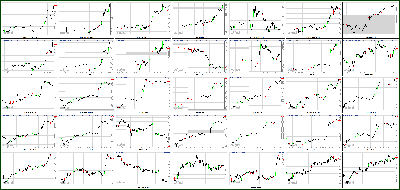

Dow Back Above 13,000 Attachment:

112312-Key-Price-Action-Markets.png [ 523.33 KiB | Viewed 273 times ]

112312-Key-Price-Action-Markets.png [ 523.33 KiB | Viewed 273 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- U.S. stocks wrapped up Black Friday more than 1%, inking the fifth straight day of gains.

The Dow Jones Industrial Average, the S&P 500, and the Nasdaq closed up between 1.3% and 1.4% on a post-Thanksgiving shortened trading day. All three indexes ended the week up more than 3%, racking up five straight days of gains. The Dow closed above 13,000 for the first time since Election Day.

Investors were cheered by the sight of busy shopping malls on the kickoff to the holiday shopping season. Leading retailers Wal-Mart (WMT, Fortune 500) and Target (TGT, Fortune 500) opened at 8 p.m. on Thanksgiving night, and large crowds were reported at those stores and others.

During a Friday morning interview with CNN, Toys "R" US CEO Jerry Storch said the long lines at stores were probably a sign that "people do feel a little more relaxed about the economy." Macy's CEO Terry Lundgren, also speaking on CNN, said he enjoyed watching the "stream of humanity" flow into his stores.

Shares of Macy's Inc (M, Fortune 500), Wal-Mart and Target were higher Friday, as were the stocks of other prominent retailers such Sears (SHLD, Fortune 500) and Best Buy (BBY, Fortune 500).

* Black Friday shoppers out in full forceBesides Black Friday retail sales, there was little else to move the markets Friday. But investors also stayed focused on Europe and the continued questions over Greece's finances.

European finance ministers failed to finalize the details of a debt-reduction package for Greece before the close of their meeting Wednesday. The officials had been expected to agree to release the funds for Greece so it would be able to make payments due in December.

U.S. markets were closed Thursday for Thanksgiving. Stocks finished higher Wednesday as investors focused on positive U.S. economic numbers.

* Fear & Greed IndexEuropean stocks and Asian markets both closed with gains.

Companies: Shares of BlackBerry maker Research in Motion (RIMM) moved up nearly 15% following a report by Canadian brokerage firm National Bank Financial that anticipates sales of the BlackBerry 10 smartphone, due to roll out early next year, will be better than expected.

Hostess Brands received approval from a bankruptcy judge Wednesday to shut down and begin selling off its assets.

Currencies and commodities: The dollar fell against the euro, British pound and Japanese yen.

Oil for January delivery rose 77 cents to $88.15 a barrel.

Gold futures for December delivery climbed $23.20 to $1,751.40 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury stayed put at 1.68%.

Market Update

Market Update1:15 pm : Equities began today's abbreviated session with a bullish bias. The sentiment was maintained into the close as the S&P 500 reached its high during the first hour of trade, and hovered near that area until the close. The markets were unfazed by headlines from overseas which indicated the Eurozone Summit has been postponed and will likely take place early next year. Today's volume was well below-average and trade was trapped in a narrow range. As a result, the S&P 500 advanced 1.3%.

Technology stocks led the broader market. Shares of Apple (AAPL 571.50, +9.80) added 1.7% as the stock attempts to halt its recent slide.

Semiconductor manufacturers outperformed and the PHLX Semiconductor index gained 1.8%. Among individual stocks which comprise the index, Taiwan Semiconductor (TSM 16.84, +0.58) advanced 3.6% after Taiwan's finance minister called on the government to begin purchasing individual equities.

Looking at other outperformers within the semiconductor average, Advanced Micro Devices (AMD 1.95, +0.08) and Lam Research (LRCX 35.34, +0.84) saw respective gains of 4.3% and 2.4%.

Also of note, OCZ Technology (OCZ 1.16, -0.03) slid 2.5% after the company received a Securities and Exchange Commission inquiry and a subpoena requesting certain company documents. The investigation pertains to financial reporting of customer incentive programs among other matters.

Elsewhere, Research in Motion (RIMM 11.66, +1.40) surged 13.7% after National Bank Financial raised its estimates for Blackberry 10 sales. In addition, National Bank Financial raised the price target to $15 from $12.

Utility stocks continued their recent slide. The space was the only decliner among S&P sectors as settled lower by 0.3%. The biggest relative weakness was observed among electricity providers as Exelon (EXC 28.57, -0.28), Edison International (EIX 43.49, -0.33), and Southern Company (SO 42.03, -0.25) all lost between 0.6% and 1.0%.

The extended weakness in utility stocks comes as investors prepare for the possibility of a dividend tax hike. In addition, electricity providers are expected to face tougher regulation after Superstorm Sandy caused considerable damage to east coast infrastructure. Earlier in the week, the investigative panel appointed by New York Governor Andrew Cuomo named Regina Calcaterra as the director. The newly-established panel will investigate utilities' preparation and response to Superstorm Sandy.

The Dow Jones Transportation Average advanced 1.1% and railroad stocks saw relative strength. Kansas City Southern (KSU 77.61, +1.28) gained 1.7% and Union Pacific (UNP 121.98, +1.94) advanced 1.6%.

There are no economic data points scheduled for a Monday release.

Week in Review: Stocks Register Gains During Abbreviated Week

On Monday, equities opened amid optimism regarding a potential fiscal cliff compromise. In addition, headlines out of Europe indicated the next tranche of Greek aid will likely come through before December 5. The positive sentiment supported the S&P 500 throughout the day and the benchmark average gained 2.0% after a final round of buying ran it to a session high close. Meanwhile, the Nasdaq outperformed with a gain of 2.2%. Apple (AAPL 571.50, +9.80) spiked 7.2% in an attempt to establish support and put a stop to its recent softness.

Tuesday began on a down note after Moody's cut France's sovereign rating to ‘Aa1' from ‘Aaa.' In addition, disappointing earnings from Hewlett-Packard (HPQ 12.44, +0.50) contributed to the cautious sentiment. The major averages managed to break into positive territory by midday, but tumbled to fresh lows as Federal Reserve Chairman Ben Bernanke spoke in front of the Economic Club of New York. During his remarks, Mr. Bernanke commented on the fiscal cliff by saying that if a resolution is not reached, the economy would slide into recession. In such case, the Federal Reserve would be powerless as the Chairman does not believe the Fed has the tools necessary to deal with that eventuality. The S&P 500 followed the early afternoon slide with another climb towards the unchanged level before ending with a gain of 0.1%. Hewlett-Packard slumped 12.0% after reporting mixed results. In addition to the results, investors were drawn to another point of interest in the quarterly report. The report included an $8.8 billion charge related to serious accounting improprieties and misrepresentations by Autonomy Corporation before it came under Hewlett-Packard's control. Following the earnings release, ISI Group downgraded HPQ to ‘neutral' from ‘buy.'

On Wednesday, the S&P 500 endured choppy trade during the first two hours of action. The index followed the early indecision with a run to session highs where it spent the majority of the afternoon. The market received some encouraging news from the Middle East where Israel and Hamas have reached a cease-fire agreement. However, the Eurozone remains a concern into the holiday as the next tranche of Greek aid was yet to be approved. The day's trade was confined to a tight range and volume was well below average. As a result, the S&P 500 ended higher by 0.2%. Salesforce.com (CRM 159.45, +0.67) spiked 8.8% after beating on the top and bottom lines. In addition to the quarterly beat, the cloud computing company issued in-line fourth quarter and full-year earnings and revenue guidance.

Equity and bond markets were closed on Thursday in observance of Thanksgiving.DJ30 +172.79 NASDAQ +40.30 SP500 +18.12 NASDAQ Adv/Vol/Dec 1776/745.0 mln/550 NYSE Adv/Vol/Dec 2438/328.9 mln/476

12:30 pm : The Dow is higher by 0.8% as trade enters the final thirty minutes of the session.

The Dow Jones Transportation Average is advancing 0.7% as it underperforms the remaining industrials. FedEx (FDX 87.49, -0.16) is the only decliner within the bellwether complex as it trades lower by 0.2%.

Meanwhile, railroad shares are seeing relative strength. Kansas City Southern (KSU 77.40, +1.07) is firmer by 1.4% and Union Pacific (UNP 121.50, +1.45) is rising by 1.2%.DJ30 +106.38 NASDAQ +27.32 SP500 +11.35 NASDAQ Adv/Vol/Dec 1526/573.2 mln/766 NYSE Adv/Vol/Dec 2212/207.5 mln/649

12:00 pm : Uneventful trade continues as the major averages hold their gains. The S&P 500 is firmer by 0.8%.

The materials sector is one of the top performers during today's low-volume session. Within the space, steel stocks are broadly higher. ArcelorMittal (MT 15.03, +0.21), Steel Dynamics (STLD 12.87, +0.20), and Mechel OAO (MTL 6.25, +0.15) are all adding between 1.4% and 2.6%. Earlier, Mechel reported temporary suspension of steelmaking operations at its plants in Romania and Ukraine. The halt comes due to unfavorable conditions on markets of raw materials and finished steel products.

Paper stocks are also outperforming. Neenah Paper (NP 26.55, +0.70) and Louisiana-Pacific (LPX 17.75, +0.52) are higher by 2.8% and 3.0%, respectively.DJ30 +99.98 NASDAQ +31.15 SP500 +11.16 NASDAQ Adv/Vol/Dec 1582/503.7 mln/693 NYSE Adv/Vol/Dec 2220/181.4 mln/632

11:30 am : The major averages are holding their recent levels and the S&P 500 is firmer by 0.9%.

Utility stocks are continuing their recent slide. The space is the only decliner among S&P sectors as it trades lower by 0.2%. The biggest relative weakness can be observed among electricity providers as Exelon (EXC 28.58, -0.27), Edison International (EIX 43.46, -0.36), and Southern Company (SO 41.98, -0.29) all see losses between 0.7% and 1.0%.

The extended slide in utility stocks comes as investors prepare for the possibility of a dividend tax hike. In addition, electricity providers are expected to face tougher regulation after Superstorm Sandy caused considerable damage to east coast infrastructure. Earlier in the week, the investigative panel appointed by New York Governor Andrew Cuomo named Regina Calcaterra as the director. The newly-established panel will investigate utilities' preparation and response to Superstorm Sandy.DJ30 +117.61 NASDAQ +31.92 SP500 +12.59 NASDAQ Adv/Vol/Dec 1578/428.9 mln/662 NYSE Adv/Vol/Dec 2267/157.5 mln/554

11:00 am : The major averages continue to trade near their respective highs and the S&P 500 is higher by 0.8%.

As crude oil adds 1.1%, the energy sector is seeing gains as well. Among major energy producers, Anadarko Petroleum (APC 73.60, +1.09) and Occidental Petroleum (OXY 76.02, +0.91) are both up near 1.3%.

Meanwhile, coal stocks which have been under pressure since the November 6 election are seeing strength and the Market Vectors Coal ETF (KOL 23.87, +0.37) is rising by 1.6%. Looking at individual coal stocks, Arch Coal (ACI 6.67, +0.16) trades higher by 2.5% while James River Coal (JRCC 2.49, +0.09) is adding 3.8%.DJ30 +112.29 NASDAQ +30.25 SP500 +11.59 NASDAQ Adv/Vol/Dec 1569/358.1 mln/637 NYSE Adv/Vol/Dec 2222/133.5 mln/556

10:35 am : The dollar index has been trending lower and is now down 0.8%, giving a boost to the commodities space.

Crude oil broke into positive territory moments after pit trade opened and has been trending higher. It recently rallied to a session high of $88.53 on no apparent news. It is currently trading just below that level at $88.43, or 1.2% higher.

Natural gas dipped to an overnight low of $3.83 just before floor trade opened and climbed to a pit session high of $3.90. It is now chopping around just below the unchanged level at $3.89, or 0.3% lower.

Gold and silver traded in a fairly consolidative pattern just above the break-even line in morning pit action. Gold also popped in recent action and is now at its new session hgih of $1749.50, or up 1.2%. Silver spiked to a session high of $33.92 moments ago and is now up 1.5% at $33.87.DJ30 +112.47 NASDAQ +30.32 SP500 +12.32 NASDAQ Adv/Vol/Dec 1607/286.9 mln/566 NYSE Adv/Vol/Dec 2331/111.92 mln/463

10:00 am : The major averages continue to trade near their respective highs. The S&P 500 is advancing 0.5%.

Technology stocks are seeing strength in the early going. Shares of Apple (AAPL 564.00, +2.30) are higher by 0.4% as the stock attempts to halt its recent slide.

Semiconductor manufacturers are seeing strength and the PHLX Semiconductor index is higher by 1.4%. Among individual stocks which comprise the index, Taiwan Semiconductor (TSM 16.86, +0.60) is advancing 3.7% after Taiwanese equities received a boost from the country's finance minister calling on the government to begin purchasing individual equities.

Looking at other outperformers within the semiconductor average, Advanced Micro Devices (AMD 1.93, +0.06) and Lam Research (LRCX 35.15, +0.65) are seeing respective gains of 3.2% and 1.9%.

Also of note, OCZ Technology (OCZ 1.13, -0.06) is sliding 5.0% after the company received a Securities and Exchange Commission inquiry and a subpoena requesting certain company documents. The investigation pertains to financial reporting of customer incentive programs among other matters.DJ30 +80.57 NASDAQ +19.32 SP500 +8.73 NASDAQ Adv/Vol/Dec 1460/185.2 mln/640 NYSE Adv/Vol/Dec 2094/76.1 mln/578

09:45 am : Equities have maintained their bullish pre-market bias. The S&P 500 is higher by 0.4% while Nasdaq is outperforming, up 0.5%.

Looking at the early sector performance, technology and consumer discretionary stocks are leading the advance. Meanwhile, utilities are continuing their recent weakness and the group is the only decliner among the ten S&P sectors.

Elsewhere, Petroquest Energy (PQ 5.27, +0.21) is the top early performer among all S&P 500 stocks. PQ is advancing 4.2% after Stifel Nicolaus upgraded the stock to ‘buy' from ‘hold.'DJ30 +58.84 NASDAQ +14.54 SP500 +5.69 NASDAQ Adv/Vol/Dec 1392/108.2 mln/614 NYSE Adv/Vol/Dec 2020/51.9 mln/588

09:15 am : [BRIEFING.COM] S&P futures vs fair value: +6.10. Nasdaq futures vs fair value: +11.00. As the start of the session nears, equity futures are pointing to a higher open.

Looking at pre-market movers, Alcatel-Lucent (ALU 1.19, +0.19) is advancing 19.0% after reports indicated the company is discussing financing with Goldman.

Elsewhere, OCZ Technology (OCZ 1.10, -0.09) is sliding 7.6% after the company received a Securities and Exchange Commission inquiry and a subpoena requesting certain company documents. The investigation pertains to financial reporting for customer incentive programs among other matters.

Also of note, major financials are seeing pre-market interest. Bank of America (BAC 9.84, +0.07), Morgan Stanley (MS 16.35, +0.10), and Wells Fargo (WFC 32.80, +0.21) are all up near 0.6%.

Today's volume is expected to be well below average and the session will come to an early close at 13:00 ET.

08:59 am : [BRIEFING.COM] S&P futures vs fair value: +3.50. Nasdaq futures vs fair value: +9.00. Equity futures continue to trade near their pre-market highs and the S&P 500 futures are firmer by 0.3%.

Taking a look at major currency pairs, the euro is adding 55 pips against the dollar. Today's advance brings the exchange rate in the most liquid currency pair up to 1.2930. Since the end of New York trade on Wednesday, the single currency has been in a steady uptrend, adding nearly 100 pips against the greenback.

The yen is seeing modest gains against the dollar as trade consolidates near the 82.35 area. Today's move in favor of the yen comes after the Japanese currency saw considerable weakness during recent sessions, rising from 80.20 on November 14 to its current 82.20.

Elsewhere, the Canadian dollar is seeing little change as the USDCAD pair trades just below parity, at 0.9973.

08:28 am : [BRIEFING.COM] S&P futures vs fair value: +4.10. Nasdaq futures vs fair value: +9.80. U.S. equity futures are near their pre-market highs, and the S&P 500 futures are adding 0.3%.

European markets are showing little change as the euro adds 30 pips against the dollar. The single currency currently trades near 1.2900 against the greenback. A moderate amount of economic data was released across Europe. On Thursday, France reported manufacturing and services PMI ahead of expectations. Meanwhile, Germany's manufacturing PMI of 46.8 beat forecasts while its services PMI of 48.0 fell short of expectations. Similarly, the two Eurozone PMI readings were mixed. The services component was reported at 45.7, below the expected 46.1. On the other hand, the region's manufacturing PMI of 46.2 was better-than-expected. This morning, Spanish PPI report indicated a 3.5% year-over-year increase while the consensus was expecting the indicator to rise by 4.0%. Elsewhere, German Ifo Business Climate Index of 101.4 was ahead of the expected 99.5. In regional news, the Eurozone leaders are at a standstill in their budget negotiations. Due to the lack of progress, German Chancellor Angela Merkel said she does not expect a deal to be made until the New Year. Also of note, reports from last Monday indicated Cyprus will receive a bailout package which should not exceed EUR10 billion. Yesterday, Cyprus Finance Minister said he expects up to EUR17.5 billion in aid.

In the United Kingdom, the FTSE is adding 0.2% as consumer stocks see strength. SABMiller and Kingfisher are seeing respective gains of 1.0% and 1.3%. On the downside, miners are underperforming. Evraz, Kazakhmys, and Polymetal are all down between 0.3% and 1.2%.

France's CAC is registering fractional gains. Electricite de France is the top gainer in the 40-stock index. The electricity supplier is rising by 4.3% after the British government said utility customers will face price increases by 2020 in order to cover the rising costs of a switch to renewable energy sources. Meanwhile, financials are lagging. Credit Agricole and Societe Generale are both down near 0.5%.

In Germany, the DAX is higher by 0.1% and chemical producers are outperforming. Lanxess and Linde are up 1.1% and 1.5%, respectively. Commerzbank is the biggest laggard as it trades lower by 2.3%.

The major Asian bourses ended mostly higher amid a quiet trade as the Thanksgiving holiday in the U.S. and a market closure in Japan produced light volumes. Taiwan's Taiex outperformed with a 3.1% gain after the country's finance minister suggested government controlled funds should buy equities. Data from the region was light as Taiwan's GDP saw an in-line 1.0% year-over-year while its industrial production posted a better than expected 4.6% year-over-year (2.2% expected) increase.

In Japan, the Nikkei was closed for Labor Thanksgiving Day.

In Hong Kong, the Hang Seng finished higher by 0.8% as property developers saw slight outperformance. Cheung Kong and Sun Hung Kai Properties both added 0.9% as residential real estate prices remain near record highs.

In China, the Shanghai Composite gained 0.6% as financials and coal names were firm with buyers emerging after their recent weakness. China Citic Bank and Yanzhou Coal Mining added 0.8% and 1.3% to finish among the top performers in their respective sectors.

08:05 am : S&P futures vs fair value: +3.30. Nasdaq futures vs fair value: +8.30. U.S. equity futures are modestly higher amid uneventful European trade. A low-volume session is expected and the New York Stock Exchange will close at 13:00 ET.

Overnight, the global equity markets endured a quiet session. In Asia, Japan's Nikkei was closed in observance of Labor Thanksgiving Day. Economic news in the region was limited, but on Thursday, the Chinese HSBC Manufacturing PMI was reported at 50.40, which was ahead of the prior month's reading of 49.50. Elsewhere, Hong Kong's CPI came in at 3.8% year-over-year, while a reading of 3.9% was generally expected. Taiwan's Taiex gained 3.1%, and was the best performer in the region after the country's finance minister said the government should purchase equities. Looking at other Asian indices, China's Shanghai Composite advanced 0.6% and Hong Kong's Hang Seng added 0.8%.

European markets are showing little change as the euro adds 30 pips against the dollar. The single currency currently trades near 1.2900 against the greenback. A moderate amount of economic data was released across Europe. On Thursday, France reported manufacturing and services PMI ahead of expectations. Meanwhile, Germany's manufacturing PMI of 46.8 beat forecasts while its services PMI of 48.0 fell short of expectations. Similarly, the two Eurozone PMI readings were mixed. The services component was reported at 45.7, below the expected 46.1. On the other hand, the region's manufacturing PMI of 46.2 was better-than-expected. This morning, Spanish PPI report indicated a 3.5% year-over-year increase while the consensus was expecting the indicator to rise by 4.0%. Elsewhere, German Ifo Business Climate Index of 101.4 was ahead of the expected 99.5. In regional news, the Eurozone leaders are at a standstill in their budget negotiations. Due to the lack of progress, German Chancellor Angela Merkel said she does not expect a deal to be made until the New Year. Also of note, reports from last Monday indicated Cyprus will receive a bailout package which should not exceed EUR10 billion. Yesterday, Cyprus Finance Minister said he expects up to EUR17.5 billion in aid. Major regional indices are little changed near midday. UK's FTSE is adding 0.1% while Germany's DAX and France's CAC are both flat.

In U.S. corporate news, Research in Motion (RIMM 11.71, +1.45) is higher by 14.1% after National Bank Financial raised its estimates for Blackberry 10 sales. In addition, National Financial Bank raised the price target to $15 from $12.

There is no economic data scheduled for today's release.

07:59 am : Nikkei...Holiday......... Hang Seng...21914...+171.00...+0.80%.

07:59 am : FTSE...5801...+10.00...+0.20%. DAX...3962...+2.00...0.00.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage