Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

112112-wrbtrader-Price-Action-Trading-PnL-Blotter-Loss-760.00.png [ 76.24 KiB | Viewed 286 times ]

112112-wrbtrader-Price-Action-Trading-PnL-Blotter-Loss-760.00.png [ 76.24 KiB | Viewed 286 times ]

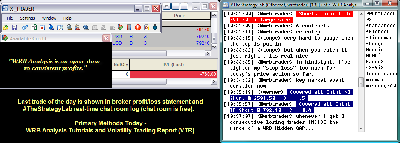

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

($760.00) dollars or -7.60 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$0 dollars or +0.00 points.

Total Profit @ ($760.00) dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1373 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events while using WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone.

U.S. Market Wrap Nov. 21 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. U.S. stocks rose, sending the Standard & Poor’s 500 Index higher a fourth day, as U.S. Secretary of State Hillary Clinton and Egyptian Foreign Minister Mohamed Amr announced a cease-fire between Israel and Hamas.

Attachment:

112112-Key-Price-Action-Markets.png [ 552.86 KiB | Viewed 280 times ]

112112-Key-Price-Action-Markets.png [ 552.86 KiB | Viewed 280 times ]

Market Update

Market Update 4:20 pm : The S&P 500 endured choppy trade during the first two hours of action. The index followed the early indecision with a run to session highs where it spent the majority of the afternoon. The market received some encouraging news from the Middle East where Israel and Hamas have reached a cease-fire agreement. However, the Eurozone remains a concern into the holiday as the next tranche of Greek aid is yet to be approved. Today's trade was confined to a tight range and volume was well below average. As a result, the S&P 500 ended higher by 0.2%.

The technology sector outperformed the broader market and the SPDR Technology Select Sector ETF (XLK 28.39, +0.09) settled higher by 0.3%. Apple (AAPL 561.70, +0.78) has been in focus recently due to the extended weakness observed in the stock during the past two months. Today, the biggest tech component tacked on 0.1% as the shares attempt to establish support in the $550 area.

In notable tech earnings, Salesforce.com (CRM 158.66, +12.76) spiked 8.8% after beating on the top and bottom lines. In addition to the quarterly beat, the cloud computing company issued in-line fourth quarter and full-year earnings and revenue guidance. Peer SAP (SAP 75.23, +0.87) added 1.2%.

Elsewhere, NCI (NCIT 4.58, +0.24) surged 5.5% after the company was awarded multiple task orders as part of its contract with the U.S. Army. The total value of the orders was reported at $27.1 million.

Also of note, Cirrus Logic (CRUS 31.16, +0.82) advanced 2.7% after the company's Board of Directors authorized the repurchase of up to $200 million of the company's common stock.

Industrial bellwether Deere (DE 82.83, -3.16) fell 3.7% after reporting mixed results. During the fourth quarter, the machinery manufacturer earned $1.75, which was $0.13 short of the Capital IQ consensus estimate. However, the company's revenue of $9.05 billion represented a 14.5% year-over-year increase, and beat expectations. Deere's outlook was mostly positive as the company expects full-year 2013 revenue above consensus and net income in-line with expectations.

The Dow Jones Transportation Average added 0.3%. Railroads saw relative weakness yesterday, but displayed strength today. Kansas City Southern (KSU 76.33, +0.69) and Norfolk Southern (NSC 57.03, +0.12) finished higher by 0.9% and 0.2%, respectively.

On the other hand, airlines which outperformed yesterday were among the biggest laggards. JetBlue Airways (JBLU 5.07, +0.05) and Southwest Airlines (LUV 9.24, +0.13) saw respective gains of 1.0% and 1.4%.

Today's choppy price action was reflected in the performance of individual sectors. However, utilities opened as the weakest performing group, and remained there for the duration of the session. Electrical companies have been pressured since Hurricane Sandy, and their shares felt the brunt of today's weakness. The SPDR Utilities Select Sector (XLU 34.18, -0.15) slid 0.4%. Among individual electricity producers, Duke Energy (DUK 60.23, -0.55) and NextEra Energy (NEE 67.25, -0.46) both lost near 0.7%.

The weekly MBA Mortgage Index pointed to a 2.2% decrease in mortgage applications during the past week. Today's reading followed prior week's increase of 12.6%.

The latest weekly initial jobless claims count totaled 410,000, which was lower than the 423,000 that had been expected by the Briefing.com consensus. The tally was below the revised prior week count of 451,000. As for continuing claims, they fell to 3.337 million from 3.367 million.

The University of Michigan's final Consumer Sentiment Survey for November fell to 82.7 from the 84.9 that was posted in the preliminary Survey. The Briefing.com consensus expected the reading to slip to 84.5.

Lastly, leading indicators for October increased by 0.2%, which was in-line with the forecast. Today's reading followed prior month's increase of 0.6%.

Note that equity and bond markets will be closed tomorrow in observance of Thanksgiving. Trading will resume on Friday, but the final session of the week will end at 13:00 ET.DJ30 +48.38 NASDAQ +9.87 SP500 +3.22 NASDAQ Adv/Vol/Dec 1556/1.36 bln/857 NYSE Adv/Vol/Dec 2016/521.9 mln/969

3:30 pm : Commodities displayed some notable volatility today, especially in the oil market. Inventory data came out for oil and for natural gas today. Oil data didn't cause the commodity to do much initially, but sellers began to step in later, cause the Dec contract to fall below the $86.50 mark. Crude recovers those losses with an afternoon rally, to end the day 0.7% higher at $87.41/barrel.

Natural gas futures spiked following inventory, which pushed the December contract as high as $3.91. At the end of today's floor trading session, nat gas closed 2.3% higher at $3.91/MMBtu.

Precious metals ended the day higher, while copper (base metal) slid modest lower. In morning action, gold and silver rallied higher, allowing Dec gold to ended the day up 0.3% at $1723.70/oz and Dec silver up 1% at $33.29. Dec copper lost 2 cents to finish at $3.50/lb.DJ30 +42.82 NASDAQ +7.67 SP500 +1.93 NASDAQ Adv/Vol/Dec 1402/1162.3 mln/994 NYSE Adv/Vol/Dec 1829/370 mln/1144

3:00 pm : The major averages are holding their recent levels as trade enters the final hour.

Last week, shares of Groupon (GRPN 3.90, +0.53) hit their all-time low of $2.60 after delivering another round of disappointing earnings. Since reaching its lows, the stock has been in a steady uptrend. Yesterday, GRPN gained nearly 2.0% after Tiger Global Management disclosed a 9.9% stake in the company. Today, the coupon provider is surging 15.7% to extend its recent strength.DJ30 +45.00 NASDAQ +9.58 SP500 +2.16 NASDAQ Adv/Vol/Dec 1380/1.06 bln/996 NYSE Adv/Vol/Dec 1779/330.2 mln/1166

2:30 pm : The S&P 500 is adding 0.1% as it trades one point away from its session high.

Casino stocks were pressured in the days following Hurricane Sandy. The storm impacted operations of casinos in Atlantic City and gaming stocks suffered accordingly. Today, Century Casinos (CNTY 2.77, +0.07), Melco Crown Entertainment (MPEL 15.05, +0.37), and MGM Resorts (MGM 9.84, +0.20) are all seeing gains near 2.5% as they attempt to break the recent trend.DJ30 +38.01 NASDAQ +8.58 SP500 +1.36 NASDAQ Adv/Vol/Dec 1400/963.3 mln/965 NYSE Adv/Vol/Dec 1760/305.7 mln/1183

2:00 pm : Quiet afternoon trade continues as the S&P 500 adds 0.2%.

Today's choppy price action is being reflected in the performance of individual sectors. However, the utility sector began the day as the biggest laggard, and has extended its losses since. The SPDR Utilities Select Sector (XLU 34.05, -0.28) is sliding 0.8% and nearly half of the decline occurred in recent minutes. Electrical companies have been pressured since Hurricane Sandy, and their stocks are feeling the brunt of today's weakness. Dominion Resources (D 49.91, -0.43), Duke Energy (DUK 60.23, -0.55), and NextEra Energy (NEE 66.81, -0.90) are all down near 1.0%.DJ30 +55.06 NASDAQ +9.48 SP500 +3.17 NASDAQ Adv/Vol/Dec 1428/890.2 mln/917 NYSE Adv/Vol/Dec 1857/284.6 mln/1078

1:30 pm : The major averages are holding their recent levels and the Dow is higher by 0.4%.

The Dow Jones Transportation Average is adding 0.2% as it trails the industrial average. Railroads saw relative weakness yesterday, but three of four rail operators are outperforming today. Kansas City Southern (KSU 76.34, +0.70), Norfolk Southern (NSC 57.14, +0.23), and Union Pacific (UNP 120.58, +0.55) are all up between 0.4% and 0.9%.

On the other hand, airlines which outperformed yesterday are seeing relative weakness. United Continental (UAL 19.59, -0.18) and JetBlue Airways (JBLU 4.98, -0.04) are both down near 0.9%.DJ30 +47.29 NASDAQ +7.75 SP500 +2.48 NASDAQ Adv/Vol/Dec 1392/827.8 mln/944 NYSE Adv/Vol/Dec 1792/261.4 mln/1119

1:00 pm : Equities registered gains in the opening minutes of today's session. However, the major indices saw some divergence as the S&P 500 and Nasdaq followed the early strength with a slide to their respective flat lines before climbing to session highs. Meanwhile, the Dow has been climbing steadily since the open and is currently higher by 0.4%. Midday volume is well below average and trade has been confined to a tight range ahead of tomorrow's Thanksgiving holiday.

The technology sector is leading the way as the SPDR Technology Select Sector ETF (XLK 28.42, +0.12) trades higher by 0.4%. Apple (AAPL 562.60, +1.68) has been in focus due to the extended weakness observed in the stock during the past two months. Today, the biggest tech component is adding 0.3% as the stock attempts to establish support in the $550 area.

In notable tech earnings, Salesforce.com (CRM 156.89, +10.99) is spiking 7.5% after beating on the top and bottom lines. In addition to the quarterly beat, the cloud computing company issued in-line fourth quarter and full-year earnings and revenue guidance. Peer SAP (SAP 75.30, +0.94) is adding 1.3%.

Elsewhere, NCI (NCIT 4.76, +0.42) is surging 9.7% after the company was awarded multiple task orders as part of its contract with the U.S. Army. The total value of the orders was reported at $27.1 million.

Financial stocks are among the biggest laggards and the SPDR Financial Select Sector ETF (XLF 15.63, -0.01) is lower by 0.1%. Wells Fargo (WFC 32.63, -0.29) is a notable decliner among the majors, shedding 0.9%. Elsewhere, JPMorgan Chase (JPM 40.58, -0.11) and Citigroup (C 35.72, -0.28) are seeing respective losses of 0.3% and 0.8%. Meanwhile, Bank of America (BAC 9.73, +0.10) is adding 0.9% as it outperforms its peers.

With domestic financials seeing weakness, their European counterparts are mixed. Discussions over the next tranche of Greek aid are expected to carry over into next week. Deutsche Bank (DB 42.29, -0.30) is off by 0.7% while Banco Bilbao Vizcaya Argentaria (BBVA 8.11, +0.10) is higher by 1.3%.

Also of note, Deere (DE 82.17, -3.80) is down 4.4% after reporting mixed results. During the fourth quarter, the producer of industrial machinery earned $1.75, which was $0.13 short of the Capital IQ consensus estimate. However, the company's revenue of $9.05 billion represented a 14.5% year-over-year increase, and beat expectations. Deere's outlook was mostly positive as the company expects full-year 2013 revenue above consensus and net income in-line with expectations.

In today's economic data, the weekly MBA Mortgage Index pointed to a 2.2% decrease in mortgage applications during the past week. Today's reading followed prior week's increase of 12.6%.

The latest weekly initial jobless claims count totaled 410,000, which was lower than the 423,000 that had been expected by the Briefing.com consensus. The tally was below the revised prior week count of 451,000. As for continuing claims, they fell to 3.337 million from 3.367 million.

The University of Michigan final Consumer Sentiment Survey for November fell to 82.7 from the 84.9 that was posted in the preliminary Survey. The Briefing.com consensus expected the reading to slip to 84.5.

Lastly, leading indicators for October increased by 0.2%, which was in-line with the forecast. Today's reading followed prior month's increase of 0.6%.DJ30 +48.97 NASDAQ +8.19 SP500 +2.59 NASDAQ Adv/Vol/Dec 1407/763.6 mln/915 NYSE Adv/Vol/Dec 1821/241.8 mln/1096

12:30 pm : The S&P 500 has ticked up near its session high in the past few minutes. Nine out of ten S&P 500 sectors saw corresponding upticks, but utility stocks bucked the trend and held their levels.

Earlier, Zale (ZLC 5.30, -2.14) reported quarterly earnings and revenue below consensus estimates. Additionally, the company reiterated its plans to achieve positive net income during fiscal year 2013. Zale is plunging 28.8% in the wake of disappointing earnings, but the weakness does not appear to be spilling over to its peers. Blue Nile (NILE 37.79, +0.86) and Tiffany (TIF 61.59, +0.75) are up 2.3% and 1.2%, respectively.DJ30 +41.35 NASDAQ +6.88 SP500 +2.16 NASDAQ Adv/Vol/Dec 1375/695.5 mln/921 NYSE Adv/Vol/Dec 1803/221.8 mln/1091

12:00 pm : The major averages are holding their recent levels and the S&P 500 is flat.

Financial stocks are among the weakest performers and the SPDR Financial Select Sector ETF (XLF 15.58, -0.07) is lower by 0.5%. Wells Fargo (WFC 32.51, -0.41) is a notable decliner among the majors as it trades lower by 1.3%. Elsewhere, JPMorgan Chase (JPM 40.39, -0.30) and Citigroup (C 35.66, -0.34) are both down near 1.0%.

Meanwhile, Bank of America (BAC 9.69, +0.06) is outperforming. The financial giant was up as much as 1.0%, and is currently adding 0.5%.

With domestic financials seeing weakness, their European counterparts are mixed as the Eurogroup continues discussing terms for the the next tranche of Greek aid. Today, Deutsche Bank (DB 42.10, -0.49) is sliding 1.2% while Banco Bilbao Vizcaya Argentaria (BBVA 8.11, +0.10) is rising by 1.3%.DJ30 +29.16 NASDAQ +2.73 SP500 +0.06 NASDAQ Adv/Vol/Dec 1293/608.5 mln/1000 NYSE Adv/Vol/Dec 1647/201.1 mln/1227

11:30 am : The major averages are holding their recent levels and the S&P 500 is registering marginal gains.

The technology sector is outperforming the broader market as the SPDR Technology Select Sector ETF (XLK 28.37, +0.07) trades higher by 0.3%. Apple (AAPL 560.30, -0.61) has been in focus recently due to the extended weakness observed in the stock during the past two months. Today, the biggest tech component is off by 0.1% as the stock attempts to establish support in the 550 area.

In notable tech earnings, Salesforce.com (CRM 157.18, +11.28) is spiking 7.7% after beating on the top and bottom lines. In addition to the quarterly beat, the cloud computing company issued in-line fourth quarter and full-year earnings and revenue guidance. Peer SAP (SAP 75.30, +0.94) is adding 1.2%.

Elsewhere, NCI (NCIT 4.71, +0.37) is surging 8.6% after the company was awarded multiple task orders as part of its contract with the U.S. Army. The total value of the orders was reported at $27.1 million.

Also of note, Cirrus Logic (CRUS 31.14, +0.80) is advancing 2.6% after the company's Board of Directors authorized the repurchase of up to $200 million of the company's common stock.DJ30 +28.92 NASDAQ +3.59 SP500 +0.44 NASDAQ Adv/Vol/Dec 1259/515.1 mln/986 NYSE Adv/Vol/Dec 1654/172.9 mln/1189

11:00 am : The S&P 500 and Nasdaq have slipped to their respective unchanged levels. However, the Dow remains in the black and trades higher by 0.2%.

After falling nearly 3.0% yesterday, crude oil is adding 0.9%. With the energy component registering gains, energy stocks are advancing as well. Refinery operator Tesoro (TSO 41.21, +1.13) is a notable outperformer. The stock is rising by 2.8% to extend its recent strength.

Among the major energy names, Anadarko Petroleum (APC 72.81, +0.92) is advancing 1.3% while Exxon Mobil (XOM 87.76, +0.26) and Schlumberger Limited (SLB 70.38, +0.36) are both up near 0.4%.

Meanwhile, coal stocks are attempting to shake off their recent weakness. The group has been pressured since the election and today the Market Vectors Coal ETF (KOL 23.44, 0.00) trades flat.DJ30 +26.88 NASDAQ -0.04 SP500 +0.29 NASDAQ Adv/Vol/Dec 1192/422.2 mln/1012 NYSE Adv/Vol/Dec 1582/144.9 mln/1242

10:30 am : Commodities are mixed this morning, while the dollar index is near the unchanged line. The index has steadily inched lower all session, from its overnight high.

Jan crude oil has shown nice strength this morning and rose as high as $87.87. Ahead of inventory data, crude was up 0.9% at $87.51. Following the data, crude fell a little and is now +0.8% at $87.46/barrel.

Dec natural gas futures were in the red almost all session, but rallied in recent trade. In current action, nat gas is flat at $3.83/MMBtu.

Precious metals sold off in recent activity, basically erasing all of today's gains. Dec gold is now +0.04% at $1724.30/oz, while Dec silver is +0.1% at $32.97/oz. Dec copper sold off a short while ago and fell to a new LoD of $3.47/lb.DJ30 +21.78 NASDAQ -1.62 SP500 -0.26 NASDAQ Adv/Vol/Dec 1080/316.8 mln/1040 NYSE Adv/Vol/Dec 1457/114 mln/1295

10:00 am : The major averages are holding their slim gains and the S&P 500 is adding 0.1%.

The University of Michigan's final Consumer Sentiment Survey for November fell to 82.7 from the 84.9 that was posted in the preliminary Survey. The Briefing.com consensus expected the reading to slip to 84.5.

Separately, leading indicators for October increased by 0.2%, which is in-line with the forecast. Today's reading follows prior month's increase of 0.6%.DJ30 +34.87 NASDAQ +6.54 SP500 +1.92 NASDAQ Adv/Vol/Dec 1175/198.1 mln/857 NYSE Adv/Vol/Dec 1533/79.8 mln/1159

09:45 am : The opening minutes saw an extension of the bullish pre-market bias. The S&P 500 is adding 0.2% while the Nasdaq trades higher by 0.4%.

Looking at the early sector alignment, technology and energy stocks are pacing the early gains. Meanwhile, utilities are the most notable underperformer as the sector trades lower by 0.2%.

In notable earnings, Deere (DE 82.76, -3.23) is shedding 3.6% after reporting mixed results. During the fourth quarter, the producer of industrial machinery earned $1.75, which was $0.13 short of the Capital IQ consensus estimate. However, the company's revenue of $9.05 billion represented a 14.5% year-over-year increase, and beat expectations. Deere's outlook was mostly positive as the company expects full-year 2013 revenue above consensus and net income in-line with expectations.

Final November Michigan Sentiment and October leading indicators will be reported at 9:55 ET and 10:00 ET, respectively.DJ30 +24.88 NASDAQ +10.29 SP500 +2.49 NASDAQ Adv/Vol/Dec 1240/103.1 mln/700 NYSE Adv/Vol/Dec 1645/53.9 mln/980

09:17 am : [BRIEFING.COM] S&P futures vs fair value: +2.30. Nasdaq futures vs fair value: +2.50. With the U.S. markets set to begin the final full session of the week, equity futures are pointing to a slightly higher open.

Taking a final look at pre-market movers, Cirrus Logic (CRUS 32.34, +2.00) is rising by 6.6% after the company announced that its Board of Directors has authorized the repurchase of up to $200 million of the company's common stock.

Flowers Foods (FLO 23.10, +0.99) is advancing 4.5% after Reuters reported the company is likely to be interested in parts of the Hostess brand.

Scholastic (SCHL 24.30, -7.54) is slumping 23.7% after the publisher lowered its full-year 2013 earnings guidance below consensus.

Final November Michigan Sentiment and October leading indicators will be reported at 9:55 ET and 10:00 ET, respectively.

09:00 am : [BRIEFING.COM] S&P futures vs fair value: +2.80. Nasdaq futures vs fair value: +4.00. U.S. equity futures have inched higher and the S&P 500 futures are adding 0.1%.

European indices opened lower after reports indicated the Eurogroup will continue discussing the next tranche of Greek aid into next week. The euro shed more than 50 pips against the dollar in immediate reaction, but has since retraced those losses. Similarly, the key regional indices opened lower in the wake of the report, but have rallied back to their respective unchanged levels since. The markets were able to shake off the early weakness as International Monetary Fund Managing Director Christine Lagarde indicated progress is being made and a deal may be close. Economic data in the region was limited. In Great Britain, public sector net borrowing was reported at GBP6.5 billion while a month-over-month increase of GBP4.0 billion was broadly expected. Elsewhere, Spain saw its trade deficit narrow to EUR3.10 billion from the previous deficit of EUR3.14 billion.

In the United Kingdom, the FTSE is adding 0.1%. Chemical producer Johnson Matthey is sliding 6.4% after reporting a decrease in its first half profit. Utility stocks are among the top advancers as Severn Trent, National Grid, and United Utilities all see gains between 0.9% and 2.5%.

France's CAC is up 0.3% as industrials pace the advance. Vallourec is advancing 5.4% and Cie de St-Gobain is firmer by 2.1%. Meanwhile, non-cyclical consumer stocks are seeing weakness. Drug maker Sanofi is slipping 0.8%.

Germany's DAX is rising by 0.1% as technology companies attempt to keep the index in the black. Software company SAP is advancing 1.5% after rival Salesforce.com reported strong earnings. Semiconductor manufacturer Infineon Technologies is also seeing strength as the stock trades higher by 2.7%. On the downside, producers of basic materials are under pressure. K+S and ThyssenKrupp are down 2.8% and 1.3%, respectively.

The major Asian bourses ended mixed as many were able to shrug off the inability of European finance ministers to reach a Greek accord with the IMF. Japan's Nikkei rallied as a weak trade balance reading (-JPY0.62 trillion actual v. --JPY0.46 trillion expected) brought about further yen weakness. Data from the rest of the region was light with Australia's MI Leading Index climbing 0.7% month-over-month (0.4% previous).

Japan's Nikkei added 0.9% as exporters outperformed on yen weakness. Automakers Honda Motor and Toyota Motor benefitted with respective gains of 3.2% and 2.2%. Elsewhere, heavyweight Softbank jumped 2.3% after JP Morgan raised its price target.

In Hong Kong, the Hang Seng gained 1.4% as insurer Ping An climbed 0.8% after seeing two days of losses on reports HSBC was looking to sell its 15.6% stake in the company.

China's Shanghai Composite settled higher by 1.1% after early selling dropped the index to its lowest level since February 2009. Brokerage firms outperformed as Sinolink Securities surged 4.0% and Hong Yuan Securities rallied 5.1% to lead the space higher. Coal names were also firm with Yanzhou Coal and China Shenhua Energy tacking on 2.3% and 1.5% respectively.

08:32 am : [BRIEFING.COM] S&P futures vs fair value: +1.50. Nasdaq futures vs fair value: +1.50. Equity futures have shown little reaction to the latest unemployment claims data. The S&P 500 futures are flat while Dow futures are marginally lower.

The latest weekly initial jobless claims count totaled 410,000, which is lower than the 423,000 that had been expected by the Briefing.com consensus. The tally is below the revised prior week count of 451,000. As for continuing claims, they fell to 3.337 million from 3.367 million.

08:03 am : [BRIEFING.COM] S&P futures vs fair value: +1.10. Nasdaq futures vs fair value: +1.00. U.S. equity futures are mixed amid quiet European trade.

Overnight, the markets received reports indicating the Eurogroup has not yet reached agreement on approving the next tranche of Greek aid. The euro shed more than 50 pips against the dollar in immediate reaction, but has since retraced those losses. Asian indices also turned lower in the wake of the reports, and they too staged a rebound following the initial weakness. Japan's trade balance report showed a deficit of JPY62 trillion and missed expectations. The export component also missed forecasts after falling 6.5%. Specifically, exports to Asia fell 4.9%, to China -11.6%, and to Europe -20.1%. The negative data resulted in the now familiar "bad news is good news" reaction as investors speculated the data might encourage further fiscal stimulus from the Japanese government or monetary easing from the Bank of Japan. Looking at regional indices, Japan's Nikkei added 0.9%, China's Shanghai Composite rose by 1.1%, and Hong Kong's Hang Seng gained 1.4%.

European indices opened lower after the reports of a delay in Greek aid talks. Of the major averages, France's CAC and Germany's DAX are being the most resilient as the two trade higher by 0.1%. However, United Kingdom's FTSE is off by 0.1% as it continues trading in the red. The markets were able to shake off the early weakness as International Monetary Fund Managing Director Christine Lagarde indicated progress is being made and a deal may be close. Regarding the unrest in the Middle East, yesterday's reports of a cease-fire proved to be premature as

between Israel and Hamas continues. Earlier today, a bus bomb injured at least 21 people in downtown Tel Aviv. While Hamas officials did not claim responsibility for the attack, they did praise it.

In U.S. corporate news, Deere (DE 84.00, -1.99) is lower by 2.3% after reporting mixed earnings. During the fourth quarter, the producer of industrial machinery earned $1.75, which was $0.13 short of the Capital IQ consensus estimate. However, the company's revenue of $9.05 billion represented a 14.5% year-over-year increase, and beat expectations. Deere's outlook was mostly positive as the company expects full-year 2013 revenue above consensus and net income in-line with expectations.

Salesforce.com (CRM 148.10, +2.20) is adding 1.5% after beating on the top and bottom lines. In addition to the quarterly beat, the cloud computing company issued in-line fourth quarter and full-year earnings and revenue guidance.

Zale (ZLC 6.50, -0.94) is sliding 12.6% after missing on earnings and revenue. Additionally, the company reiterated its plans to achieve positive net income during fiscal year 2013. The Capital IQ consensus expects this line item to come in at $0.35.

The weekly MBA Mortgage Index pointed to a 2.2% decrease in mortgage applications during the past week. Today's reading follows prior week's increase of 12.6%.

In upcoming economic data, weekly initial and continuing claims will be announced at 8:30 ET. In addition, final November Michigan Sentiment and October leading indicators will be reported at 9:55 ET and 10:00 ET, respectively.

06:33 am : [BRIEFING.COM] S&P futures vs fair value: +1.00. Nasdaq futures vs fair value: -1.50.

06:33 am : Nikkei...9222.52...+79.90...+0.90%. Hang Seng...21524.36...+296.10...+1.40%.

06:33 am : FTSE...5744.77...-3.30...-0.10%. DAX...7176.94...+3.90...+0.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage