Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

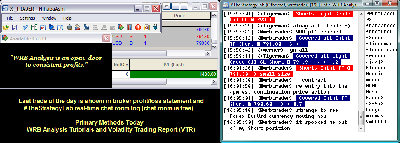

Attachment:

110812-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1430.00.png [ 78.57 KiB | Viewed 311 times ]

110812-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1430.00.png [ 78.57 KiB | Viewed 311 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$630.00 dollars or +6.30 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$800.00 dollars or +0.80 points.

Total Profit @ $1430.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1364 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading (day trading, swing trading, position trading) and reactions to the markets...something I can

not get from my broker statements alone.

U.S. Market Wrap Nov. 8 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. U.S. stocks declined, extending losses since the re-election of President Barack Obama and sending the Dow Jones Industrial Average to the lowest level since July, amid concern about Greece’s financial aid payment.

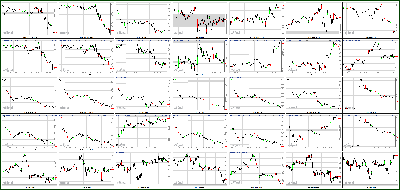

Attachment:

110812-Key-Price-Action-Markets.png [ 526.92 KiB | Viewed 270 times ]

110812-Key-Price-Action-Markets.png [ 526.92 KiB | Viewed 270 times ]

Market Update

Market Update 4:30 pm : Equities began today's session on a slightly higher note. However, the bullish bias was dispelled during the opening hour. After marking its session high at 1,401, the S&P 500 reversed and slid to its 200-day moving average near the 1,380 area. The index followed the move with a seven point bounce, before late-day selling drove the index back below the 200-day moving average. As a result, the benchmark average settled lower by 1.2%.

Crude oil gained 0.6%, but the energy sector was the biggest laggard of the day. The SPDR Energy Select Sector ETF (XLE 69.57, -1.28) lost 1.8%. Among oil and gas stocks, Carrizo (CRZO 21.71, -1.77) dropped 7.5%. Meanwhile, providers of energy equipment also saw broad weakness. Ensco (ESV 55.12, -2.61) slid 4.5% and Diamond Offshore (DO 65.37, -2.41) lost 3.6%.

Yesterday's sell-off in coal stocks saw the Market Vectors Coal ETF (KOL 24.29, -0.16) drop 5.5%. Today, the ETF shed 0.7%. Among individual coal producers, James River Coal (JRCC 3.36, +0.07) outperformed, and settled higher by 2.1%. On the downside, Alpha Natural Resources (ANR 8.15, -0.30) lost 3.6%.

Looking at technology stocks, Apple (AAPL 537.75, -20.25) continued its recent weakness. The biggest tech component ended lower by 3.6%.

In tech earnings, QUALCOMM (QCOM 60.67, +2.54) advanced 4.4% after beating on earnings and revenue. The company's bottom line of $0.89 beat the Capital IQ consensus estimate by $0.07. Meanwhile, the revenue of $4.87 billion was also ahead of expectations. It should be noted that the company guided first quarter and full-year 2013 earnings and revenue above consensus.

Universal Display (PANL 23.12, -5.05) fell 18.0% after reporting disappointing earnings. During the third quarter, the manufacturer of organic LEDs lost $0.12 on $12.5 million in revenue. The company's earnings were $0.17 below expectations, while its revenue also fell short of estimates. In addition, PANL issued downside full-year 2012 revenue guidance.

Utility stocks which have seen considerable weakness since Hurricane Sandy, saw relative strength. PPL (PPL 28.73, +0.43) was the top performer among electricity providers. The stock added 1.5% after the company reported earnings of $0.72, which was $0.05 better than the Capital IQ consensus estimate. However, the revenue of $2.4 billion was below expectations. In addition, the company issued in-line guidance.

Meanwhile, FirstEnergy (FE 42.91, +0.61) advanced 1.4% after beating on earnings. In addition, the company lowered its full-year 2012 earnings guidance in-line with expectations and also guided full-year 2013 earnings in-line with estimates.

Elsewhere, Southern Company (SO 43.26, +0.46) slid 1.1% after RBC Capital Markets upgraded the stock to ‘outperform' from ‘sector perform.'

Looking at the retail industry, the SPDR S&P Retail ETF (XRT 61.24, -1.36) underperformed the broader market and ended lower by 2.2%. Among individual retailers, Kohl's (KSS 51.55, -2.77) lost 5.1% after reporting third quarter earnings of $0.91 on $4.49 billion in revenue. The company's bottom line was $0.04 ahead of Capital IQ estimates, while the revenue was reported in-line with the November 1 preannouncement. However, the company's outlook was a point of concern as the retailer issued downside fourth quarter earnings guidance.

Elsewhere, American Eagle Outfitters (AEO 19.69, -0.90) finished lower by 4.4% and Aeropostale (ARO 12.69, -0.88) dropped 6.5% after Detweiler made cautious comments about the apparel retailer.

Also of note, McDonald's (MCD 85.13, -1.73) stumbled 2.0% after reporting a 1.8% decline in global same-store sales. The figure was below the expected decrease of 1.0%. In addition, this was the first time the fast food giant saw a monthly decline since 2003.

In today's economic data, the latest weekly initial jobless claims count totaled 355,000, which was lower than the 370,000 that had been expected. The tally was below the unrevised prior week count of 363,000. As for continuing claims, they fell to 3.127 million from 3.262 million.

The trade deficit narrowed to $41.5 billion during September after a downwardly revised prior month deficit of $43.8 billion. Economists polled by Briefing.com had expected that the deficit would come in at $45.4 billion.

Tomorrow, October export prices ex-agriculture and import prices ex-oil will be reported at 8:30 ET. In addition, the November Michigan Sentiment and September wholesale inventories will be announced at 9:55 ET and 10:00 ET, respectively.DJ30 -121.41 NASDAQ -41.71 SP500 -17.02 NASDAQ Adv/Vol/Dec 642/1.82 bln/1812 NYSE Adv/Vol/Dec 825/758.6 mln/2238

3:35 pm : Crude oil spent most of its floor session in positive territory despite a stronger dollar index. The energy component slid off its session high of $85.70 per barrel and brushed a session low of $84.22 per barrel. After very choppy action, crude settled 0.7% higher at $85.09 per barrel.

Natural gas came off its session low of $3.53 per MMBtu and popped into the black on bullish inventory data that showed a build of 21 bcf when a build of 25 bcf was expected. It continued to climb higher for the remainder of floor trade and closed at its session high of $3.61 per MMBtu for a 0.8% gain. Precious metals climbed higher in today's pit trade despite a stronger dollar index. The advance came on better-than-expected U.S. weekly initial jobless claims data and Eurozone debt concerns.

Gold came off its session low of $1712.60 per ounce and brushed a session high of $1726.90 per ounce moments before it settled with a 0.7% gain at $1726.00 per ounce. Silver fared even better as it settled 1.8% higher at $32.24 per ounce, or just below its session high of $32.25 per ounce.DJ30 -69.07 NASDAQ -32.48 SP500 -11.02 NASDAQ Adv/Vol/Dec 755/1507.6 mln/1681 NYSE Adv/Vol/Dec 957/513 mln/2059

3:00 pm : The S&P 500 continues to hover near its recent levels. The index is currently down 0.7%.

The third quarter earnings season is winding down as about 90.0% of the S&P 500 companies have already reported their earnings. The S&P 500 stocks which are set to announce their quarterly results after today's close include, Disney (DIS 50.27, +0.19), Nordstrom (JWN 55.98, -1.27), Microchip Technology (MCHP 32.04, -0.07), NVIDIA (NVDA 12.88, +0.27), and Public Storage (PSA 143.02, -0.32).DJ30 -61.41 NASDAQ -28.09 SP500 -9.77 NASDAQ Adv/Vol/Dec 789/1.35 bln/1651 NYSE Adv/Vol/Dec 985/454.5 mln/2017

2:30 pm : The S&P 500 is holding its recent levels as it trades lower by 0.7%.

Utility stocks, which have seen considerable weakness since Hurricane Sandy, are outperforming. The sector is the only space within the S&P 500 which is positive on the day. PPL (PPL 29.09, +0.79) is the top performer among electricity providers. The stock is higher by 2.8% after the company reported earnings of $0.72, which was $0.05 better than the Capital IQ consensus estimate. However, PPL revenue of $2.4 billion was below expectations. In addition, the company issued in-line guidance.

Meanwhile, FirstEnergy (FE 43.36, +1.06) is higher by 2.5% after beating on earnings. In addition, the company lowered its full-year 2012 earnings guidance in-line with expectations and also guided full-year 2013 earnings in-line with estimates.

Elsewhere, Southern Company (SO 43.62, +0.82) is higher by 1.9% after RBC Capital Markets upgraded the stock to ‘outperform' from ‘sector perform.'DJ30 -66.85 NASDAQ -28.47 SP500 -9.83 NASDAQ Adv/Vol/Dec 792/1.25 bln/1628 NYSE Adv/Vol/Dec 996/422.5 mln/2006

2:00 pm : After marking its session low at 1,381, the S&P 500 regained seven points. The index is currently lower by 0.5%.

The financial sector is outperforming the broader market and the SPDR Financial Select Sector ETF (XLF 15.59, -0.01) is off by 0.1%. Among the majors, Bank of America (BAC 9.47, +0.24) is rebounding from yesterday's 7.1% decline. Today the stock trades higher by 2.6% after being upgraded to ‘buy' from ‘hold' at ISI Group.

The sector outperformance is largely driven by the outperformance of insurance companies. Allstate (ALL 38.88, +0.21), Travelers (TRV 69.36, +0.65), and Progressive (PGR 22.24, +0.15) are all seeing gains between 0.5% and 1.0%.DJ30 -51.84 NASDAQ -21.29 SP500 -7.90 NASDAQ Adv/Vol/Dec 820/1.15 bln/1590 NYSE Adv/Vol/Dec 1019/390.9 mln/1971

1:35 pm : The major averages are continuing their steady decline and the Dow is off by 0.7%.

The Dow Jones Transportation Average is registering wider losses than the remaining industrials. The bellwether complex trades lower by 0.9%. Shipping stocks are headed in opposite directions. Kirby Corporation (KEX 54.93, -1.80) is the weakest transportation stock, down 3.2%. Meanwhile, Matson (MATX 22.70, +1.77) is surging 8.7% after reporting earnings and revenue above the Capital IQ consensus estimates.

Besides Matson, Airline Stocks listed in the transportation average are all trading in the black. JetBlu Airways (JBLU 5.35, +0.15) is the top performer, up 2.8%.DJ30 -88.00 NASDAQ -28.51 SP500 -11.94 NASDAQ Adv/Vol/Dec 760/1.06 bln/1639 NYSE Adv/Vol/Dec 950/358.3 mln/2033

1:05 pm : Stocks began the session on a higher note amid upbeat European trade. The S&P 500 briefly crossed above the 1,400 level, but the gains were short-lived as the S&P 500 dipped below its flat line 50 minutes into the session. Since then, the index has been declining steadily, and it currently trades lower by 0.5%.

Looking at technology stocks, Apple (AAPL 545.13, -12.73) is continuing its recent streak of underperformance. The biggest tech component is lower by 2.3%.

In tech earnings, QUALCOMM (QCOM 61.79, +3.66) is higher by 6.3% after beating on earnings and revenue. The company's bottom line of $0.89 beat the Capital IQ consensus estimate by $0.07. Meanwhile, the revenue of $4.87 billion was also ahead of expectations. It should be noted that the company guided first quarter and full-year 2013 earnings and revenue above consensus.

Universal Display (PANL 22.91, -5.27) is falling 18.7% after reporting disappointing earnings. During the third quarter, the manufacturer of organic LEDs lost $0.12 on $12.5 million in revenue. The company's earnings were $0.17 below expectations, while its revenue also fell short of estimates. In addition, PANL issued downside full-year 2012 revenue guidance.

Monster Worldwide (MWW 6.65, +0.94) is spiking 16.5% after reporting third quarter earnings of $0.09 on $221.7 million in revenue. The results may not be entirely comparable to the Capital IQ estimates of $0.05 on $235.43 billion in revenue due to company's ongoing restructuring.

Elsewhere, Ebix (EBIX 17.56, -0.83) is falling 4.8% despite beating on earnings and revenue.

Looking at the retail industry, the SPDR S&P Retail ETF (XRT 61.32, -1.28) is underperforming the broader market as it trades lower by 2.0%. Among individual retailers, Kohl's (KSS 52.20, -2.12) is down 3.9% after reporting third quarter earnings of $0.91 on $4.49 billion in revenue. The company's earnings were $0.04 ahead of Capital IQ estimates, while the revenue was reported in-line with the November 1 preannouncement. However, the company's outlook was a point of concern as the retailer issued downside fourth quarter earnings guidance. Elsewhere, American Eagle Outfitters (AEO 19.88, -0.71) is down 3.5% and Aeropostale (ARO 12.72, -0.85) is sliding 6.3% after Detweiler made cautious comments about the apparel retailer.

Homebuilder stocks are lagging the broader market and the SPDR S&P Homebuilders ETF (XHB 25.95, -0.48) is sliding 1.8%. Builder stocks outperformed yesterday, and managed to record limited losses. Today, however, major builders are seeing relative weakness. DR Horton (DHI 20.86, -0.56) and PulteGroup (PHM 17.20, -0.56) are both down near 2.8%. On the upside, Hovnanian (HOV 5.58, +0.08) is higher by 1.5%.

The latest weekly initial jobless claims count totaled 355,000, which was lower than the 370,000 that had been expected. The tally was below the unrevised prior week count of 363,000. As for continuing claims, they fell to 3.127 million from 3.262 million.

The trade deficit narrowed to $41.5 billion during September after a downwardly revised prior month deficit of $43.8 billion. Economists polled by Briefing.com had expected that the deficit would come in at $45.4 billion.DJ30 -48.94 NASDAQ -19.84 SP500 -6.51 NASDAQ Adv/Vol/Dec 825/954.1 mln/1548 NYSE Adv/Vol/Dec 1100/322.3 mln/1855

12:30 pm : Stocks have pushed further into the red and the S&P 500 is now below 1,390. The benchmark index is lower by 0.4%.

Homebuilder stocks are lagging the broader market and the SPDR S&P Homebuilders ETF (XHB 26.07, -0.36) is sliding 1.4%. Builder stocks outperformed yesterday, and managed to record limited losses. Today, however, major builders are seeing relative weakness. DR Horton (DHI 20.93, -0.49) and PulteGroup (PHM 17.33, -0.43) are both down near 2.3%. On the upside, Hovnanian (HOV 5.66, +0.16) is higher by 2.9%.DJ30 -32.86 NASDAQ -15.92 SP500 -5.04 NASDAQ Adv/Vol/Dec 906/857.3 mln/1448 NYSE Adv/Vol/Dec 1185/290.4 mln/1759

12:05 pm : The S&P 500 continues to hover around 1,390 as it trades lower by 0.2%.

Looking at the retail industry, the SPDR S&P Retail ETF (XRT 61.82, -0.78) is underperforming the broader market as it trades lower by 1.2%. Among individual retailers, Kohl's (KSS 51.99, -2.33) is down 4.3% after reporting third quarter earnings of $0.91 on $4.49 billion in revenue. The company's earnings were $0.04 ahead of Capital IQ estimates, while the revenue was reported in-line with the November 1 preannouncement. However, the company's outlook was a point of concern as the retailer issued downside fourth quarter earnings guidance.

Elsewhere, American Eagle Outfitters (AEO 20.05, -0.54) is down 2.7% and Aeropostale (ARO 12.88, -0.69) is sliding 5.1% after Detweiler made cautious comments about the apparel retailer.DJ30 -26.57 NASDAQ -11.62 SP500 -3.86 NASDAQ Adv/Vol/Dec 895/773.4 mln/1442 NYSE Adv/Vol/Dec 1193/265.9 mln/1729

11:35 am : The major averages have slipped further into the red and the S&P 500 is off by 0.3%.

Crude oil is higher by 0.5%, but energy stocks are among the biggest laggards of the day and the SPDR Energy Select Sector ETF (70.21, -0.64) is lower by 0.9%.

Among oil and gas stocks, Swift Energy (SFY 14.15, -0.76) and Carrizo (CRZO 22.12, -1.36) are both losing near 5.5%. Meanwhile, providers of energy equipment are also seeing broad weakness. Ensco (ESV 54.93, -2.79) is down 4.8% and Diamond Offshore (DO 65.34, -2.44) is sliding 3.6%.

Elsewhere, coal stocks are mixed after yesterday's sell-off which saw the Market Vectors Coal ETF (KOL 24.52, +0.07) drop 5.5%. Today, the ETF is adding 0.3%. Among individual coal producers, James River Coal (JRCC 3.47, +0.18) is outperforming as it trades higher by 5.5%. On the downside, Walter Energy (WLT 33.60, -0.66) is shedding 1.9%.DJ30 -36.75 NASDAQ -14.22 SP500 -4.97 NASDAQ Adv/Vol/Dec 963/675.1 mln/1349 NYSE Adv/Vol/Dec 1152/236.7 mln/1719

11:05 am : The major averages have slipped to fresh session lows after headlines out of Europe indicated the Eurozone ministers will delay the Greek aid call for weeks. The S&P 500 is off by 0.1%.

Looking at technology stocks, Apple (AAPL 548.45, -9.55) is continuing its recent streak of underperformance. The biggest tech component is lower by 1.7%.

In tech earnings, QUALCOMM (QCOM 62.05, +3.92) is higher by 6.7% after beating on earnings and revenue. The company's bottom line of $0.89 beat the Capital IQ consensus estimate by $0.07. Meanwhile, the revenue of $4.87 billion was also ahead of expectations. It should be noted that the company guided first quarter and full-year 2013 earnings and revenue above consensus.

Universal Display (PANL 23.78, -4.40) is falling 15.6% after reporting disappointing earnings. During the third quarter, the manufacturer of organic LEDs lost $0.12 on $12.5 million in revenue. The company's earnings were $0.17 below expectations, while its revenue also fell short of estimates. In addition, PANL issued downside full-year 2012 revenue guidance.

Monster Worldwide (MWW 6.69, +0.98) is spiking 17.7% after reporting third quarter earnings of $0.09 on $221.7 million in revenue. The results may not be entirely comparable to the Capital IQ estimates of $0.05 on $235.43 billion in revenue due to company's ongoing restructuring.

Elsewhere, Ebix (EBIX 16.60, -1.80) is falling 9.8% despite beating on earnings and revenue.DJ30 -34.78 NASDAQ -7.64 SP500 -4.01 NASDAQ Adv/Vol/Dec 1039/549.7 mln/1235 NYSE Adv/Vol/Dec 1192/198.4 mln/1639

10:35 am : Commodities have been mostly higher this morning, despite strength in the dollar index. Natural gas futures just spiked five cents, back to the unchanged line of $3.58/MMBtu after the EIA reported a smaller-than-expected build (21 bcf vs 25 bcf) and are now +0.3% at $3.59/MMBtu.

Dec crude oil has been in positive territory all session, but sold off sharply after hitting a new HoD of $85.70/barrel at 9am EST. Currently, crude is now +0.5% at $84.88/barrel.

Precious metals are trading higher as well with Dec gold +0.2% at $1717.20/oz and Dec silver +0.8% at $31.92/oz. Dec copper is +0.5% at $3.46/lb

Tomorrow morning at 8:30am EST, the USDA will release its monthly (November) WASDE crop report, which typically has a large impact on ag commodities such as corn, wheat and soybeans.DJ30 -4.33 NASDAQ 0.32 SP500 -0.14 NASDAQ Adv/Vol/Dec 1044/372.2 mln/1175 NYSE Adv/Vol/Dec 1376/155 mln/1420

10:00 am : The S&P 500 has slipped off its early highs near the 1,401 level. The benchmark index is currently higher by 0.3%.

Utility stocks are outperforming in the early going. The sector was under pressure after Hurricane Sandy caused major damage to East Coast electricity delivery systems. PPL (PPL 28.94, +0.64) is the top performer among electricity providers. Earlier, the company reported earnings of $0.72, which was $0.05 better than the Capital IQ consensus estimate. However, PPL revenue of $2.4 billion was below expectations. In addition, the company issued in-line guidance.

Looking at other electric utilities, Duke Energy (DUK 63.51, +0.57), Exelon (EXC 31.80, +0.36), and Southern (SO 43.36, -0.56) are all up between 0.9% and 1.4%.DJ30 +26.98 NASDAQ +9.16 SP500 +3.83 NASDAQ Adv/Vol/Dec 1202/233.5 mln/960 NYSE Adv/Vol/Dec 1539/98.8 mln/1168

09:45 am : The opening minutes saw an extension of the modest bullish pre-market sentiment. The S&P is adding 0.5%.

Financials and utilities are seeing early strength as the two sectors see gains in excess of 1.0%. Meanwhile, consumer staples, health care, and materials are showing little change in the early going.

Elsewhere, QUALCOMM (QCOM 62.43, +4.30) is higher by 7.4% after beating on earnings and revenue. The company's bottom line of $0.89 beat the Capital IQ consensus estimate by $0.07. Meanwhile, the revenue of $4.87 billion was also ahead of expectations. It should be noted that the company guided first quarter and full-year 2013 earnings and revenue above consensus.DJ30 +42.93 NASDAQ +11.63 SP500 +6.52 NASDAQ Adv/Vol/Dec 1173/142.7 mln/946 NYSE Adv/Vol/Dec 1584/72.1 mln/1049

09:17 am : [BRIEFING.COM] S&P futures vs fair value: +0.30. Nasdaq futures vs fair value: +7.00. Heading into the open, equity futures remain modestly higher. The S&P 500 futures are up 0.3%.

Major financials are showing pre-market strength after yesterday's sell-off had the biggest impact on the sector. Bank of America (BAC 9.48, +0.25) is higher by 2.8% after ISI Group upgraded the stock to ‘buy' from ‘hold.' Meanwhile, JPMorgan Chase (JPM 41.23, +0.75) after disclosing the Federal Reserve's approval of firm's resubmitted capital plan which includes the resumption of stock buybacks.

09:00 am : S&P futures vs fair value: +2.20. Nasdaq futures vs fair value: +9.30. U.S. equity futures are modestly higher, and the S&P 500 futures are up 0.3%.

Major Asian indices closed broadly lower and Hong Kong's Hang Seng was a notable laggard, down 2.4%. The markets played catch-up to the decline on Wall Street, with each of the major indices shedding at least 1.5%. The Chinese once-in-a-decade power hand-off is underway as president-in-waiting, Xi Jinping, and premier-in-waiting, Li Keqiang, are moving into the spotlight. Meanwhile, outgoing president, Hu Jintao, outlined many goals including an end to government corruption, and plans to double GDP by 2020 from its 2010 levels. Financial reform and decentralization of government were also highlighted as objectives. Be on the look-out for key data out of China tomorrow as CPI, industrial production and retail sales are set to be reported. Elsewhere, Japan's economic data disappointed as machine tool orders dropped 7.8% month-over-month, and widely missed expectations. Australia's better-than-expected employment data revealed an addition of 10.7K jobs, while the consensus called for an increase of 0.2K. This helped keep the unemployment rate steady at 5.4% while the figure was expected to increase to 5.5%. In addition, JPMorgan believes the Reserve Bank of Australia will cut rates in December despite better-than-expected figures. Looking at currencies, USDJPY dipped slightly, to 79.89. The Australian dollar slipped 0.1% against the U.S. dollar as the pair trades near 1.0406. USDCNY is at 6.2429.

In Japan, the Nikkei lost 1.5%. Oki Electric was the biggest laggard as the stock settled lower by 9.4% after the company said it expects a bigger half-year net loss forecast, resulting from an overstatement by its Spanish unit. Technology stocks also saw weakness. Sumco and Toshiba lost 4.8% and 3.5%, respectively. Isuzu gained 4.7% after the carmaker issued upside guidance which stemmed from cost cutting measures undertaken by the company.

In Hong Kong, the Hang Seng fell 2.4% and consumer stocks were broadly weaker. Esprit, Belle International, and Li & Fung all lost between 2.1% and 3.7%. Only two index components posted gains, and both were non-cyclical stocks. Hengan International gained 1.1% and Tingyi Cayman Islands Holding added 0.4%.

China's Shanghai Composite lost 1.6% and chemical companies saw weakness. HeiLongJiang HeiHua dropped 8.4% and Hubei Xingfa plunged 9.7%. Australia's ASX outperformed the region's indices and slipped 0.7%. Miners Lynas and South Boulder gained 11.8% and 10.2%, respectively. In Europe, the key austerity vote was passed in Greece yesterday, and it remains to be seen how quickly said reforms are implemented.

The European bourses are in positive territory, but off their highs. Sentiment grew sour when reports suggested—once again—that Spain would not seek a bail out prior to year's end. Also of note, the country auctioned off nearly EUR5 billion of debt and its benchmark 10-yr interest rate added 14 basis points, to 5.832%. In Germany, the trade balance was reported slightly ahead of expectations, but the export portion showed softness. The European Central Bank left its key interest rate unchanged at 0.75%. The policy meeting was followed by a press conference, during which, Central Bank President Mario Draghi said 2013 growth momentum will remain weak. In the United Kingdom, the Bank of England also left its interest rate and the asset purchasing program unchanged at their respective 0.5% and EUR375 billion.

In the United Kingdom, the FTSE is adding 0.3%. Burberry is the top performer as it trades higher by 2.8%. On the downside, security company, G4S, is down 5.5% after the company lost a Yorkshire prison contract.

France's CAC is higher by 0.5%. Vallourec is advancing 7.0% on strong earnings. Cap Gemini is the biggest laggard, down 5.5%.

In Germany, the DAX is advancing 0.3%. Commerzbank is the main underperformer, lower by 3.7%. Meanwhile, HeidelbergCement is advancing 3.7% after its cost cutting program resulted in a 10.0% debt reduction.

08:33 am : [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +10.00. Equity futures showed little change in response to the latest initial claims. The S&P 500 futures are up 0.4%.

The latest weekly initial jobless claims count totaled 355,000, which is lower than the 370,000 that had been expected. The tally is below the unrevised prior week count of 363,000. As for continuing claims, they fell to 3.127 million from 3.262 million.

The trade deficit narrowed to $41.5 billion during September after a downwardly revised prior month deficit of $43.8 billion. Economists polled by Briefing.com had expected that the deficit would come in at $45.4 billion.

08:00 am : S&P futures vs fair value: +3.40. Nasdaq futures vs fair value: +10.50. U.S. equity futures are higher by 0.4% following yesterday's sell-off which saw the major indices drop over 2.0%.

Overnight, the world equity markets were mixed. Asia played catch-up to the decline on Wall Street, with each of the major indices shedding at least 1.5%. In China, the power hand-off took place and outgoing president, Hu Jintao, outlined many goals including an end to government corruption, and plans to double GDP by 2020 from its 2010 levels. Financial reform and decentralization of government were also highlighted as objectives. Be on the look-out for key data out of China tomorrow as CPI, Industrial Production and Retail Sales are set to be reported. China's Shanghai Composite lost 1.6%. Meanwhile, Japan's economic data did not do the Nikkei any favors as Machine Tool Orders dropped 7.8% month-over-month, and widely missed expectations. The Nikkei slid 1.5%. In Australia, better-than-expected employment data revealed an addition of 10.7K jobs, while the consensus called for an increase of 0.2K. This helped keep the unemployment rate steady at 5.4% while the figure was expected to increase to 5.5%. In addition, JPMorgan thinks the Reserve Bank of Australia will cut rates in December despite better than expected figures. Australia's ASX outperformed the region's indices and slipped 0.7%. Elsewhere, Hong Kong's Hang Seng fell 2.4%.

In Europe, the key austerity vote was passed in Greece yesterday, and it remains to be seen how quickly said reforms are implemented. The European bourses are in positive territory, but off their highs. Sentiment grew sour when reports suggested—once again—that Spain would not seek a bail out prior to year's end. Also of note, the country auctioned off nearly EUR5 billion of debt and its benchmark 10-yr interest rate added 14 basis points, to 5.832%. In Germany, the trade balance was reported slightly ahead of expectations, but the export portion showed softness. The European Central Bank left its key interest rate unchanged at 0.75% and Central Bank President Mario Draghi will hold a press conference at 8:30 ET. In the United Kingdom, the Bank of England also left its interest rate and the asset purchasing program unchanged at their respective 0.5% and EUR375 billion. Looking at European indices, France's CAC is advancing 0.6%, Germany's DAX is higher by 0.5%, and UK's FTSE is adding 0.3%.

In U.S. corporate news, QUALCOMM (QCOM 62.50, +4.38) is higher by 7.5% after beating on earnings and revenue. The company's bottom line of $0.89 beat the Capital IQ consensus estimate by $0.07. Meanwhile, the revenue of $4.87 billion was also ahead of expectations. It should be noted that the company guided first quarter and full-year 2013 earnings and revenue above consensus.

Universal Display (PANL 19.72, -8.46) is falling 30.0% after reporting disappointing earnings. During the third quarter, the manufacturer of organic LEDs lost $0.12 on $12.5 million in revenue. The company's earnings were $0.17 below expectations, while its revenue also fell short of estimates. In addition, PANL issued downside full-year 2012 revenue guidance.

Dean Foods (DF 17.00, +0.92) is higher by 5.7% after beating on earnings and revenue. Meanwhile, the company's guidance was in-line with expectations. Dean also announced that two senior executives, Shaun Mara and Steve Kemps, will leave the company.

Weekly initial and continuing claims and the September trade balance will all be released at 8:30 ET.

The U.S. Treasury will auction off $16 billion in 30-yr bonds.

06:30 am : [BRIEFING.COM] S&P futures vs fair value: -1.00. Nasdaq futures vs fair value: +4.00.

06:30 am : Nikkei...8837.15...-137.70...-1.50%. Hang Seng...21566.91...-532.90...-2.40%.

06:30 am : FTSE...5806.12...+14.50...+0.30%. DAX...7269.33...+36.50...+0.50%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage