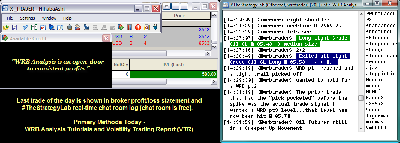

Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

110512-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+580.00.png [ 77.4 KiB | Viewed 284 times ]

110512-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+580.00.png [ 77.4 KiB | Viewed 284 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$100.00 dollars or +1.00 points, EuroFX 6E futures @

$0.00 dollars or +0.0000 ticks and Light Crude Oil CL (WTI) futures @

$480.00 dollars or +0.48 points.

Total Profit @ $580.00 dollars.

Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroupCME EuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroupS&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=110&t=1361 Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade or position trade.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=195&t=1654 -----------------------------

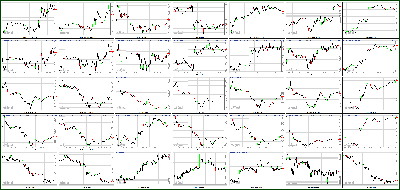

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading (day trading, swing trading, position trading) and reactions to the markets...something I can

not get from my broker statements alone.

Attachment:

110512-Key-Price-Action-Markets.png [ 534.05 KiB | Viewed 304 times ]

110512-Key-Price-Action-Markets.png [ 534.05 KiB | Viewed 304 times ]

Market Update

Market Update 4:25 pm : Today's session began on a mixed note. The S&P 500 spent the majority of the day in negative territory as cautious trade took place ahead of tomorrow's Presidential election. However, late afternoon buying drove the benchmark average to a higher finish by 0.2%.

The technology sector outperformed the broader market. The biggest tech component, Apple (AAPL 584.62, +7.82), gained 1.4% after reporting that sales of its iPad 4 and iPad mini have reached three million units during the first three days of sales. Also of note, shortly before the close reports indicated that the company may be considering a switch from Intel (INTC 21.84, +0.01) processors. Following the news, Intel shares surrendered their gains, while AMD (AMD 2.10, 0.00) and ARM Holdings (ARMH 34.08, +0.88) spiked higher.

Netflix (NFLX 78.24, +1.34) added 1.7% after announcing it will issue one right for each current share of outstanding common stock at the close of business on November 2, 2012. The rights will not be exercisable immediately. However, if they do become exercisable, each right will entitle shareholders to buy one one-thousandth of a share of a new series of participating preferred stock at an exercise price of $350 per right. The plan is intended to protect Netflix and its stockholders from efforts to obtain control of company.

In technology earnings, Rogers Corporation (ROG 41.90, +2.67) spiked 6.8% after reporting mixed results. The supplier of communications equipment reported earnings of $0.69, which was $0.05 ahead of the Capital IQ consensus estimate. Meanwhile, the company's revenue of $130.20 million was slightly lower than estimated. However, the strength in the stock is likely related to upbeat guidance as the company expects fourth quarter earnings above analyst estimates while revenue is expected to be in-line with expectations.

On the downside, Ebix (EBIX 19.26, -3.15) fell 14.1% after Bloomberg reports indicated the software company is facing a Securities and Exchange Commission probe focused on its accounting practices. Since the initial report, company officials have issued the following statement: "The Ebix senior management team has not been advised of nor is it aware of any SEC investigation regarding the Company's previous filings. We stand behind the accuracy of our public filings. The Bloomberg article is inaccurate and misleading in many respects and we intend to evaluate all avenues of recourse."

Looking at the financial sector, The SPDR Financial Select Sector ETF (XLF 15.97, -0.03) underperformed the broader market as it settled lower by 0.2%.

Among the majors, Goldman Sachs (GS 124.08, +0.83) and Wells Fargo (WFC 34.02, +0.28) outperformed as the two stocks settled higher by 0.7% and 0.8%, respectively. Meanwhile, Bank of America (BAC 9.75, -0.10) and Citigroup (37.32, -0.28) were the notable laggards as the pair saw respective losses of 1.0% and 0.7%.

Elsewhere, KBW (KBW 17.47, +1.17) announced a merger with Stifel Financial (SF 32.58, +0.67). Per the agreement, KBW shareholders will receive $17.50 per share, which represents a 7.4% premium to KBW's Friday closing price. In addition, Stifel Financial reported its earnings this morning. During the third quarter, the investment brokerage earned $0.60 on $420.08 million in revenue. Both figures were ahead of the Capital IQ consensus estimates.

Also of note, MetLife (MET 34.69, -0.01) has agreed to sell its $70 billion mortgage servicing portfolio to JPMorgan Chase (JPM 42.27, -0.15). The move is aimed at expanding JPMorgan's footprint in the mortgage servicing business, while banks were expected to reduce their exposure in this area. As a result, companies which concentrate on mortgage investment were pressured. Nationstar Mortgage Holdings (NSM 30.20, -2.91) fell 8.8% and Ocwen Financial (OCN 32.95, -2.06) slid 5.9%.

The Dow Jones Transportation Average outperformed the broader market and settled higher by 0.3%. Alaska Air (ALK 40.13, +1.09) was the top performer within the complex after the carrier reported an 8.5% increase in traffic on the back of a 5.1% increase in capacity as compared to October 2011. In addition, Hurricane Sandy did not have a material impact on the company's capacity as 38 flights to and from the East Coast were cancelled. The stock rose by 2.8% following the positive report, and traded at its all-time high. Rival United Continental (UAL 20.25, +0.52) advanced 2.6% after the company's first Dreamliner 787 supplied by Boeing (BA 70.41, +0.36) took flight over the weekend.

Two automakers reported their quarterly results before today's open. Tesla Motors (TSLA 31.50, +2.58) surged 8.9% after reporting mixed earnings. During the third quarter, the automaker registered a loss of $0.92, which was $0.01 below the Capital IQ consensus estimates. Meanwhile, the company's revenue of $50.1 million represents a 13.2% year-over-year decline, but the figure came in ahead of analyst expectations. Lastly, Tesla reaffirmed its full-year 2012 guidance as well as its full-year 2013 gross margin projections and delivery targets. Note that today's buying has lifted the stock to levels not seen since late September.

Elsewhere, Toyota Motor (TM 81.35, +3.55) finished higher by 4.6% after its bottom line exceeded the Capital IQ consensus estimates. The Japanese carmaker reported earnings of JPY81.44, which was JPY8.47 ahead of expectations. Meanwhile, the company's revenue was in-line with analyst estimates. Regarding future outlook, the company raised its full-year 2013 net income guidance and lowered the full-year 2013 revenue expectations.

The October ISM Services index was reported at 54.2, which is below the 55.0 Briefing.com consensus, and down from September's reading of 55.1.

There is no economic data scheduled for tomorrow. However, the U.S. Treasury will auction off $32 billion in 3-yr notes.DJ30 +19.28 NASDAQ +17.53 SP500 +3.06 NASDAQ Adv/Vol/Dec 1481/1.44 bln/973 NYSE Adv/Vol/Dec 1538/600.7 mln/1448

3:00 pm : The S&P 500 continues to hold its recent levels, and trades higher by 0.1%.

This week brings the final heavy dose of third quarter earnings. After today's close, Express Scripts (ESRX 62.98, +0.96) is one of the names scheduled to report. The Capital IQ consensus expects the provider of pharmacy benefit management services to earn $0.99 on $27.46 billion in revenue.

Zillow (Z 34.14, -2.13) is also set to announce its quarterly results. The online real estate information service is expected to report earnings of $0.07 on revenue of $31.85 million.

Other after-hours results will come from Broadsoft (BSFT 36.17, +0.11), EOG Resources (EOG 116.21, +1.01), and Live Nation (LYV 9.16, -0.08).

Ahead of tomorrow's open, CVS Caremark (CVS 46.66, +0.10), Fossil (FOSL 93.44, +0.34), Office Depot (ODP 2.51, -0.01), and OfficeMax (OMX 7.46, -0.04) are some of the notable names which will report their earnings.DJ30 +3.80 NASDAQ +13.40 SP500 +1.36 NASDAQ Adv/Vol/Dec 1447/1.06 bln/984 NYSE Adv/Vol/Dec 1491/367.6 mln/1485

2:30 pm : The S&P 500 has broken through its flat line and the index now trades higher by 0.1%.

Two for-profit education stocks are headed in opposite directions after reporting their quarterly results. Bridgepoint Education (BPI 9.66, -0.44) is sliding 4.4% after its third quarter earnings of $0.56 were $0.13 below the Capital IQ consensus estimate. BPI's revenue of $252.10 million also fell short of analyst expectations. In addition, the company reported a 7.0% year-over-year decline in its third quarter new enrollment.

On the upside, Lincoln Educational Services (LINC 3.85, +0.15) is higher by 4.1% after its third quarter revenue of $104.10 million exceeded the Capital IQ consensus forecast. Regarding the fourth quarter outlook, the company expects revenues to come in below consensus.

Elsewhere, Corinthian Colleges (COCO 2.47, -0.27) is down 9.9% after disclosing a letter from the United States Department of Education which disputes the company's calculations of its composite score for the fiscal year ended June 30,2011. The two parties have agreed to meet and discuss the issues.DJ30 +0.82 NASDAQ +11.86 SP500 +0.99 NASDAQ Adv/Vol/Dec 1429/975.3 mln/992 NYSE Adv/Vol/Dec 1451/340.1 mln/1510

2:05 pm : The major averages are holding their recent levels and the S&P 500 is off by 0.1%.

Looking at the financial sector, The SPDR Financial Select Sector ETF (XLF 15.92, -0.08) is underperforming the broader market as it trades lower by 0.5%.

Among the majors, Goldman Sachs (GS 123.57, +0.32) and Wells Fargo (WFC 33.88, +0.14) are outperforming as the two stocks trade higher by 0.3% and 0.4%, respectively. Meanwhile, Bank of America (BAC 9.71, -0.14) and Citigroup (37.18, -0.42) are the notable laggards as the two see respective losses of 1.4% and 1.1%.

Elsewhere, KBW (KBW 17.46, +1.16) announced a merger with Stifel Financial (SF 32.55, +0.64). Per the agreement, KBW shareholders will receive $17.50 per share, which represents a 7.4% premium to KBW's Friday closing price. In addition, Stifel Financial reported its earnings this morning. During the third quarter, the investment brokerage earned $0.60 on $420.08 million in revenue. Both figures were ahead of the Capital IQ consensus estimates.

Also of note, MetLife (MET 34.54, -0.16) has agreed to sell its $70 billion mortgage servicing portfolio to JPMorgan Chase (JPM 42.10, -0.32). The move is aimed at expanding JPMorgan's footprint in the mortgage servicing business, while banks were expected to reduce their exposure in this area. As a result, companies which concentrate on mortgage investment are seeing weakness. Nationstar Mortgage Holdings (NSM 30.98, -2.13) and Ocwen Financial (OCN 33.13, -1.87) are down 6.4% and 5.4%, respectively.DJ30 -12.00 NASDAQ +4.70 SP500 -1.00 NASDAQ Adv/Vol/Dec 1395/894.1 mln/1030 NYSE Adv/Vol/Dec 1402/313.1 mln/1571

1:35 pm : The S&P 500 has recovered a portion of its losses and it now trades lower by 0.1%.

The Dow Jones Transportation Average is higher by 0.1% as it outperforms the remaining industrials.

Alaska Air (ALK 39.93, +0.90) is the top performer within the complex after the carrier reported an 8.5% increase in traffic on the back of a 5.1% increase in capacity as compared to October 2011. In addition, Hurricane Sandy did not have a material impact on the company's capacity as 38 flights to and from the East Coast were cancelled. The stock is adding 2.3% following the positive report, and is now trading at its all-time high. Rival United Continental (UAL 20.01, +0.28) is advancing 1.4% after the company's first Dreamliner 787 supplied by Boeing (BA 70.31, +0.26) took flight over the weekend.

Meanwhile, shipper Matson (MATX 20.97, -0.38) is the biggest laggard among the group, and trades lower by 1.8%. Peer Kirby Corporation (KEX 56.79, -0.30) is off by 0.5%.DJ30 -13.09 NASDAQ +5.73 SP500 -1.18 NASDAQ Adv/Vol/Dec 1356/825.1 mln/1038 NYSE Adv/Vol/Dec 1393/290.2 mln/1562

1:05 pm : Stocks began today's session on a mixed note. The tech-heavy Nasdaq is outperforming, but the index has given up the bulk of its gains and trades flat at midday. As market participants show caution ahead of tomorrow's Presidential election, the S&P 500 is off by 0.3%.

The materials sector is one of the top performers today. Within the sector, steel stocks are outperforming, while paper stocks are showing weakness. Among steel producers, AK Steel (AKS 5.28, +0.03) and Cliffs Natural Resources (CLF 36.80, +0.53) are higher by 0.8% and 1.5%, respectively.

In paper and packaging stocks, Rock-Tenn (RKT 66.05, -1.44) is down 2.1% after JP Morgan downgraded the stock to neutral. Meanwhile, International Paper (IP 35.16, -0.77) and KapStone Paper and Packaging (KS 21.43, -0.17) are seeing respective losses of 2.1% and 0.8%. However, peer Wasau Paper (WPP 8.42, +0.23) is a notable outlier. The stock is advancing 2.8% after 10.0% stakeholder, Starboard Value Funds, bought 75,000 shares.

The technology sector is also trading ahead of the broader market. The biggest tech component, Apple (AAPL 579.65, +2.85), is higher by 0.5% after reporting that sales of its iPad 4 and iPad mini have reached three million units during the first three days of sales.

QUALCOMM (QCOM 60.12, +0.82) is adding 1.4% after Nomura upgraded the stock to ‘buy' from ‘neutral.'

In technology earnings, Rogers Corporation (ROG 41.89, +2.66) is spiking 6.8% after reporting mixed results. The supplier of communications equipment reported earnings of $0.69, which was $0.05 ahead of the Capital IQ consensus estimate. Meanwhile, the company's revenue of $130.20 million was slightly lower than estimated. However, the strength in the stock is likely related to upbeat guidance as the company expects fourth quarter earnings above analyst estimates while revenue is expected to be in-line with expectations.

On the downside, Ebix (EBIX 17.57, -4.84) is plunging 21.6% after Bloomberg reports indicated the software company is facing a Securities and Exchange Commission probe focused on its accounting practices.

Two automakers reported their quarterly results before today's open. Tesla Motors (TSLA 30.14, +2.22) is advancing 7.7% after reporting mixed earnings. During the third quarter, the automaker registered a loss of $0.92, which was $0.01 below the Capital IQ consensus estimates. Meanwhile, the company's revenue of $50.1 million represents a 13.2% year-over-year decline, but the figure came in ahead of analyst expectations. Lastly, Tesla reaffirmed its full-year 2012 guidance as well as its full-year 2013 gross margin projections and delivery targets. Note that today's buying has lifted the stock to levels not seen since late September.

Elsewhere, Toyota Motor (TM 80.25, +2.45) is higher by 3.2% after its bottom line exceeded the Capital IQ consensus estimates. The Japanese carmaker reported earnings of JPY81.44, which was JPY8.47 ahead of expectations. Meanwhile, the company's revenue was in-line with analyst estimates. Regarding future outlook, the company raised its full-year 2013 net income guidance and lowered the full-year 2013 revenue expectations.

The October ISM Services index was reported at 54.2, which is below the 55.0 Briefing.com consensus, and down from September's reading of 55.1.DJ30 -30.10 NASDAQ +0.21 SP500 -3.59 NASDAQ Adv/Vol/Dec 1323/753.2 mln/1069 NYSE Adv/Vol/Dec 1309/267.2 mln/1621

12:35 pm : The S&P 500 has slipped further during the past 30 minutes, and the benchmark index now trades lower by 0.2%.

A handful of apparel stocks are among the top performers in the S&P 500. Aeropostale (ARO 13.93, +0.65) is advancing 4.9% after FBR Capital upgraded the stock to ‘outperform' from ‘market perform' with a $16 price target.

Meanwhile, Quiksilver (ZQK 3.67, +0.27) is rising by 7.9% after Stifel Nicolaus upgraded the stock to ‘buy' from ‘hold' with a $6 price target.

Elsewhere, Deckers Outdoor (DECK 31.39, +1.10) and K-Swiss (KSWS 3.35, +0.24) are also seeing strength. The two footwear stocks are trading higher by 3.7% and 7.7%, respectively.DJ30 -25.09 NASDAQ -0.66 SP500 -3.04 NASDAQ Adv/Vol/Dec 1354/681.8 mln/1026 NYSE Adv/Vol/Dec 1317/243.9 mln/1596

12:00 pm : The major averages are slipping lower and the S&P 500 is off by 0.1%.

Two automakers reported their quarterly results before today's open. Tesla Motors (TSLA 30.26, +1.35) is advancing 4.7% after reporting mixed earnings. During the third quarter, the automaker registered a loss of $0.92, which was $0.01 below the Capital IQ consensus estimates. Meanwhile, the company's revenue of $50.1 million represents a 13.2% year-over-year decline, but the figure came in ahead of analyst expectations. Lastly, Tesla reaffirmed its full-year 2012 guidance as well as its full-year 2013 gross margin projections and delivery targets.

Elsewhere, Toyota Motor (TM 79.69, +1.89) is higher by 2.4% after its bottom line exceeded the Capital IQ consensus estimates. The Japanese carmaker reported earnings of JPY81.44, which was JPY8.47 ahead of expectations. Meanwhile, the company's revenue was in-line with analyst estimates. Regarding future outlook, the company raised its full-year 2013 net income guidance and lowered the full-year 2013 revenue expectations.DJ30 -16.57 NASDAQ +5.41 SP500 -1.63 NASDAQ Adv/Vol/Dec 1354/595.1 mln/999 NYSE Adv/Vol/Dec 1355/216.8 mln/1555

11:30 am : The S&P 500 continues to chop around its unchanged line while Nasdaq is higher by 0.3%.

The materials sector is one of the top performers today. Within the sector, mining and steel stocks are outperforming, while paper stocks are showing weakness. Among steel producers, AK Steel (AKS 5.38, +0.13) and Cliffs Natural Resources (CLF 37.27, +1.00) are higher by 2.5% and 2.8%, respectively.

In paper and packaging stocks, Rock-Tenn (RKT 66.09, -1.40) is down 2.1% after JP Morgan downgraded the stock to neutral.

Meanwhile, International Paper (IP 35.33, -0.60) and KapStone Paper and Packaging (KS 21.41, -0.19) are seeing respective losses of 1.6% and 0.9%. However, peer Wasau Paper (WPP 8.43, +0.24) is a notable outlier. The stock is advancing 3.1% after 10.0% stakeholder, Starboard Value Funds, bought 75,000 shares.DJ30 -6.13 NASDAQ +8.95 SP500 -0.34 NASDAQ Adv/Vol/Dec 1395/526.2 mln/921 NYSE Adv/Vol/Dec 1407/193.9 mln/1480

11:00 am : The key indices have lifted off their early lows and the S&P 500 is currently flat. The Nasdaq, however, is higher by 0.4% as it outperforms.

The technology sector is showing relative strength. The biggest tech component, Apple (AAPL 585.71, +8.91), is higher by 1.5% after reporting that sales of its iPad 4 and iPad mini have reached three million units during the first three days of sales.

Netflix (NFLX 77.94, +1.04) is adding 1.5% after announcing it will issue one right for each current share of outstanding common stock at the close of business on November 2, 2012. The rights will not be exercisable immediately. However, if they do become exercisable, each right will entitle shareholders to buy one one-thousandth of a share of a new series of participating preferred stock at an exercise price of $350 per right. The plan is intended to protect Netflix and its stockholders from efforts to obtain control of company.

QUALCOMM (QCOM 60.16, +0.86) is advancing 1.4% after Nomura upgraded the stock to ‘buy' from ‘neutral.'

In technology earnings, Rogers Corporation (ROG 42.09, +2.86) is spiking 7.3% after reporting mixed results. The supplier of communications equipment reported earnings of $0.69, which was $0.05 ahead of the Capital IQ consensus estimate. Meanwhile, the company's revenue of $130.20 million was slightly lower than estimated. However, the strength in the stock is likely related to upbeat guidance as the company expects fourth quarter earnings above analyst estimates while revenue is expected to be in-line with expectations.

On the downside, Ebix (EBIX 16.09, -6.32) is plunging 28.2% after Bloomberg reports indicated the company is facing a Securities and Exchange Commission probe focused on its accounting practices.DJ30 -4.11 NASDAQ +11.08 SP500 +0.32 NASDAQ Adv/Vol/Dec 1350/432.1 mln/920 NYSE Adv/Vol/Dec 1407/164.7 mln/1455

10:30 am : Many commodities are showing strength this morning even though the dollar index is near its session high.

Dec crude oil has been chopping around just above the unchanged line and rose as high as $85.37 about 30 min ahead of floor trading. Currently, crude is +0.3% at $85.11/barrel.

Dec natural gas has been in the red for most of the session, but moved into positive territory in recent trade after it rallied off its $3.51 LoD, hitting a new HoD of $3.58/MMBtu a short while ago. Nat gas is now +0.5% at $3.57/MMBtu.

Precious metals are higher as well with Dec gold +0.5% at $1683.50/oz and Dec silver +0.4% at $30.98/oz. Dec copper is currently -0.7% at $3.46/lb.DJ30 -36.95 NASDAQ +0.20 SP500 -4.18 NASDAQ Adv/Vol/Dec 1206/315.4 mln/1030 NYSE Adv/Vol/Dec 1162/130 mln/1639

10:00 am : Stocks have shown mixed reaction the latest ISM Services data. The S&P 500 is off by 0.3%, while Nasdaq ticked up and is now flat.

The October ISM Services index was reported at 54.2, which is below the 55.0 Briefing.com consensus, and down from September's reading of 55.1.DJ30 -41.85 NASDAQ -1.04 SP500 -5.16 NASDAQ Adv/Vol/Dec 1089/200.9 mln/1109 NYSE Adv/Vol/Dec 1072/92.7 mln/1697

09:45 am : After trading higher in pre-market, the major averages have slipped lower. Currently, the S&P 500 is off by 0.3% while Nasdaq is lower by 0.1%.

Looking at the early sector alignment, utilities are a notable laggard as the sector trades lower by 1.2%. Financials are also seeing early weakness. Only technology stocks are currently positive while industrials and energy stocks trade near their respective flat lines.

Apple (AAPL 585.76, +8.96) is gaining 1.6% after announcing that it sold three million tablets since Friday's launch. This figure includes iPad 4 and iPad mini tablets.

The October ISM Services Index will be released at 10:00 ET. The Briefing.com consensus expects the reading to come in at 55.0.DJ30 -34.10 NASDAQ -1.47 SP500 -4.44 NASDAQ Adv/Vol/Dec 944/121.5 mln/1177 NYSE Adv/Vol/Dec 974/67.6 mln/1713

09:17 am : [BRIEFING.COM] S&P futures vs fair value: -2.90. Nasdaq futures vs fair value: -2.00. Heading into the open, equity futures remain modestly higher. The S&P 500 futures are adding 0.1% while Nasdaq futures are higher by 0.3%.

Netflix (NFLX 74.50, -2.40) is shedding 3.1% after announcing it will issue one right for each current share of outstanding common stock at the close of business on November 2, 2012. The rights will not be exercisable immediately. However, if they do become exercisable, each right will entitle shareholders to buy one one-thousandth of a share of a new series of participating preferred stock at an exercise price of $350 per right. The plan is intended to protect Netflix and its stockholders from efforts to obtain control of company.

Elsewhere, Apple (AAPL 584.70, +7.90) is advancing 1.4% after announcing that it sold three million tablets since Friday's launch. This figure includes iPad 4 and iPad mini tablets.

The October ISM Services Index will be reported at 10:00 ET. The Briefing.com consensus expects the reading to come in at 55.0.

09:05 am : S&P futures vs fair value: -2.70. Nasdaq futures vs fair value: -0.50. U.S. equity futures have reversed off pre-market lows and the S&P 500 futures are currently higher by 0.1%. The move higher took place after Apple (AAPL 584.34, +7.54) reported selling three million tablets since Friday's launch.

The major Asian averages ended mostly lower as traders remained cautious ahead of Tuesday's U.S. presidential election and Thursday's leadership handoff in China. Over the weekend, China released its latest Nonmanufacturing PMI number which climbed off a seven-month low to 55.5 (53.7 previous). Elsewhere, Australian data was heavy as retail sales climbed 0.5% month-over-month (0.4% expected) and the trade deficit narrowed to A$1.46 billion (A$1.60 billion expected, A$1.88 billion previous) while ANZ Job Advertisements fell 4.6% month-over-month. Finally, India's trade deficit widened to $18.08 billion from $13.19 billion as exports fell 10.8% and imports rose 5.1%.

In Japan, the Nikkei closed lower by 0.5% as electronics names remained under pressure. Sharp plunged 6.7% after receiving a six-notch downgrade from Fitch following Friday's warning suggesting the company's viability to survive is in question. Competitor Panasonic tumbled 5.6% as it piggybacked the move. Elsewhere, Toyota Motor gained 2.2% on reports the co would announce an improved outlook.

Hong Kong's Hang Seng slipped 0.5% as financials underperformed. Industrial and Commercial Bank of China fell 1.3% and Bank of China lost 0.9%. Growth sensitive names were also week with Angang Steel and Anhui Conch Cement off 1.6% and 0.2%, respectively.

In China, the Shanghai Composite shed 0.1% as transportation names saw a mixed session. FAW Car lost 2.5% as traders priced in expectations of disappointing October sales while train maker China CNR Corp. rallied 1.7% after announcing a CNY7.24 billion worth of contracts.

European markets are seeing broad weakness and Spain's IBEX is a notable laggard as it trades lower by 1.7%. Economic data was light as the Eurozone Sentix Investor Confidence was reported at -18.8, which was ahead of expectations. Another notable data point was reported in the United Kingdom where the Services PMI was reported at 50.6, which fell short of the expected reading of 52.0. Over the weekend, German Chancellor, Angela Merkel, suggested the euro-crisis could still be another 5 years from full resolution. In addition, the European Central Bank is checking whether it broke its own collateral rules when lending to Spanish banks. Meanwhile, the International Monetary Fund is reportedly urging Greek debt holders to take a haircut to help Greece return to sustainable debt levels. Peripheral yields are worth noting this morning, as Spain's benchmark 10-yr yield is adding nine basis points, to 5.751% while Italy's 10-yr debt is higher by six basis points, to 5.003%.

In the United Kingdom, the FTSE is lower by 0.6% and miners are underperforming. Eurasian Natural Resources and Vedanta Resources are seeing respective losses of 2.8% and 3.8%. On the upside, provider of mining equipment Weir Group is leading the FTSE with a 5.5% gain after issuing upbeat guidance.

In France, the CAC is down 1.0% as 38 out of 40 index components trade in the red. Construction company Vinci is sliding 1.9% after projecting a lower full-year net income due to new taxes. Alcatel-Lucent is the top advancer as it trades higher by 1.8%. The stock has been under heavy pressure in recent months as it trades near its all-time low.

Germany's DAX is shedding 0.6% and chemical producers are seeing weakness. BASF and Lanxess are both down near 1.0%. On the upside, Deutsche Boerse is adding 2.5%.

08:00 am : S&P futures vs fair value: -4.20. Nasdaq futures vs fair value: -10.30. U.S. equity futures are modestly lower amid quiet pre-market trade.

As the U.S. presidential election nears, China is preparing to hand-off power to the 18th National Congress. Both events are contributing to cautious market sentiment, and a shift away from risk assets appears to be continuing. Meanwhile, China's HSBC's Non-manufacturing PMI data came in better than expected, but couldn't keep the Shanghai Composite from finishing lower by 0.1%. Elsewhere, Japan reiterated its concerns of the strong yen at the G-20 conference. The Japanese press suggested Japan is setting the stage for even more stimulus, which could reach as much as JPY2.7 trillion. Korean KOSPI slipped 0.6%, and was an underperformer in the region following reports over the weekend that Hyundai Motors misrepresented some of its latest fuel economy statistics on recent models. Looking at other Asian indices, Japan's Nikkei and Hong Kong Hang Seng both slid 0.5%.

In Europe, German Chancellor, Angela Merkel, suggested the euro-crisis could still be another 5 years from full resolution. In addition, the European Central Bank is checking whether it broke its own collateral rules when lending to Spanish banks. Meanwhile, the International Monetary Fund is reportedly urging Greek debt holders to take a haircut to help Greece return to sustainable debt levels. Peripheral yields are worth noting this morning, as Spain's benchmark 10-yr yield is adding nine basis points, to 5.751% while Italy's 10-yr debt is higher by six basis points, to 5.003%. European indices are in the red as France's CAC is down 0.9% while Germany's DAX and UK's FTSE are both lower by 0.6%.

In U.S. corporate news, KBW (KBW 19.15, +2.85) announced a merger with Stifel Financial (SF 32.04, +0.13). Per the agreement, KBW shareholders will receive $17.50 per share, which represents a 7.4% premium to KBW's Friday closing price. In addition, Stifel Financial reported its earnings this morning. During the third quarter, the investment brokerage earned $0.60 on $420.08 million in revenue. Both figures were ahead of the Capital IQ consensus estimates.

Humana (HUM 75.21, 0.00) reported third quarter earnings of $2.62 on $9.65 billion in revenue. The report was mixed as the insurer's earnings beat the Capital IQ consensus estimates by $0.57 while the revenue fell short of expectations. In addition, the company raised its full-year 2012 earnings guidance above consensus and guided full-year 2013 earnings below analyst expectations. Lastly, the company acquired Metropolitan Health Networks (MDF 11.20, +0.35) for $11.25 per share, which represents a 3.7% premium to MDF's Friday closing price.

Today's economic data is limited to the October ISM Services Index, which will be released at 10:00 ET. The Briefing.com consensus expects the reading to come in at 55.0.

06:46 am : [BRIEFING.COM] S&P futures vs fair value: -3.50. Nasdaq futures vs fair value: -7.00.

06:46 am : Nikkei...9007.44...-43.80...-0.50%. Hang Seng...22006.40...-104.90...-0.50%.

06:46 am : FTSE...5834.22...-34.30...-0.60%. DAX...7324.41...-39.40...-0.50%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage