Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

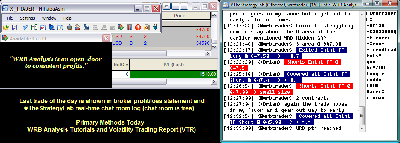

Attachment:

092012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-1510.png [ 78.12 KiB | Viewed 312 times ]

092012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-1510.png [ 78.12 KiB | Viewed 312 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +15.10 points or

$1510 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=108&t=1325.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis)...regardless if I'm day trading, swing trading or position trading.

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=171&t=1594 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading (day trading, swing trading, position trading) and reactions to the markets...something I can

not get from my broker statements alone.

U.S. Market Wrap Sept. 20 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. Most U.S. stocks fell, sending the Standard & Poor’s 500 Index lower for the third time in four days, as data from China to Japan and Europe increased concern that a global economic slowdown is worsening.

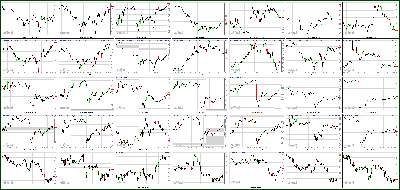

Attachment:

092012-Key-Price-Action-Markets.png [ 534.84 KiB | Viewed 281 times ]

092012-Key-Price-Action-Markets.png [ 534.84 KiB | Viewed 281 times ]

Market Update

Market Update 4:15 pm : Stocks got off to a slow start after bearish data from around the world overshadowed investor optimism. Japan reported a wider-than-expected trade deficit while the French and Eurozone PMI readings were well short of expectations. Domestically, the weekly initial claims exceeded expectations. After marking session lows thirty minutes into the trading day, the major averages set off on a day-long climb towards positive territory. As a result, the S&P 500 finished flat.

Healthcare stocks were generally higher as they benefited from the day's risk-off sentiment. Within the sector, Questcor (QCOR 30.33, +3.98) closed higher by 15.1% after losing nearly 49.0% during yesterday's sell-off which was sparked by doubts as to whether insurance companies will cover Questcor's Acthar gel.

Providers of health care equipment and supplies also saw strength within the defensive sector. CryoLife (CRY 5.90, +0.14), Meridian Bioscience (VIVO 18.84, +0.38), and Masimo (MASI 24.87, +0.39) all posted gains between 1.6% and 2.4%. On the downside, Horizon Pharmaceuticals (HZNP 3.48, -1.10) slumped 24.0% after pricing a $75 million public offering of common stock and warrants at $3.50 per unit.

The Dow Jones Transportation Average ended lower by 2.8% as it trailed the broader market. The bellwether group showed considerable weakness as railroads weighed on the complex. The four railroad components of the average were firmly lower after Norfolk Southern (NSC 66.11, -6.58) cut its guidance due to slumping demand, and decreasing revenues from fuel surcharges. Norfolk Southern slid 9.1% while CSX (CSX 21.49, -1.30), Kansas City Southern (KSU 76.90, -2.22), and Union Pacific (UNP 120.95, -4.10) all fell between 2.8% and 6.0%.

Only Overseas Shipholding Group (OSG 7.16, +0.15) managed to stay positive within the transportation average while CH Robinson (CHRW 57.55, +0.15) spent the session hovering around its flat line.

Looking at the industrial sector, CLARCOR (CLC 43.75, -5.82) slumped 11.7% after delivering a disappointing quarterly report. The company missed on earnings and revenues and the conference call contributed to the negative sentiment as management issued downside fourth quarter and full-year guidance.

Apogee Enterprises (APOG 19.50, +1.88) was a notable outlier among industrial stocks. The producer of building materials advanced 10.7% after beating on earnings and revenues. Management was upbeat in its conference call as upside guidance was issued for full-year 2013.

Green Mountain Coffee Roasters (GMCR 27.84, -2.97) shed 9.6% after Starbucks (SBUX 51.19, +1.07) announced it will begin selling a single-serve brewing machine for $199.00. The Verismo will first be sold online before becoming available at Starbucks cafes next month. In addition to the $199.00 model, the company will also sell a $399.00 version which contains a larger water tank and an LCD display. Starbucks' presence in the single-serve market is expected to take a chunk out of a market previously dominated by Green Mountain's Keurig machines.

Two names made their exchange debut today. Online real estate search service, Trulia (TRLA 24.00, +1.90) surged 41.2% in its public debut. Shares of the company began trading at $22.00 after the initial public offering was priced at $17.00. Trulia's peer, Zillow (Z 46.17, +0.62) has risen over 130.0% since the company went public in July of last year. Meanwhile, Susser Petroleum (SUSP 22.91, -0.49) added 11.8% to its initial public offering price of $20.50.

The latest weekly initial jobless claims count totaled 382,000, which is higher than the 375,000 that had been expected. The tally is above the revised prior week count of 385,000. As for continuing claims, they fell to about 3.272 million from 3.304 million.

Separately, the Philadelphia Fed Survey rose to -1.9 for September. The reading shows an improvement over last month's -7.1. Economists polled by Briefing.com had expected that the Survey would improve to a -4.0 reading.

Lastly, leading indicators for August decreased by 0.1%, which is worse than the unchanged reading that had been widely expected to follow the prior month's 0.4% increase.

There are no notable releases on tomorrow's economic calendar. However, it is important to note that quadruple witching occurs tomorrow. This means that stock index futures, stock index options, stock options, and single stock futures are all set to expire.DJ30 +18.97 NASDAQ -6.66 SP500 -0.79 NASDAQ Adv/Vol/Dec 909/1.76 bln/1524 NYSE Adv/Vol/Dec 1182/678.5 mln/1821

3:30 pm : Crude oil erased overnight losses as it inched higher into positive territory during morning pit trade. The energy component peaked at a session high of $92.69 per barrel and pulled-back slightly in afternoon action. Crude settled 0.1% higher at $92,35 per barrel, booking its first gain in four sessions.

Natural gas traded higher despite bearish inventory data that showed a build of 67 Bcf when a build of 65 Bcf was anticipated. It initially dropped to a session low of $2.77 per MMBtu but quickly recovered. After trading in a relatively consolidative pattern in afternoon floor trade, natural gas settled with a 1.1% gain at $2.80 per MMBtu.

Gold slid further into the red and to its pit session low of $1757.70 per ounce following the Philadelphia Fed and August Leading Indicators data. However, buyers stepped in and brought prices up to the unchanged line by afternoon action. The yellow metal settled just 0.1% lower at $1770.10 per ounce despite a stronger dollar index.

Silver also slid to its session low of $34.12 per ounce on the economic data but recovered into positive territory in late morning action. It brushed a session high of $34.76 per ounce and settled for a 0.3% gain at $34.69 per ounce.DJ30 +11.53 NASDAQ -6.25 SP500 -0.78 NASDAQ Adv/Vol/Dec 961/1487.4 mln/1438 NYSE Adv/Vol/Dec 1163/448 mln/1799

3:00 pm : The Dow continues to hover around its flat line, while the S&P 500 is off by 0.2%.

Two notable companies are scheduled to report their earnings after the close. Oracle (ORCL 32.38, -0.40) is expected to earn $0.53 on revenues of $8.416 billion. Oracle earnings are worth watching as the management's guidance may reflect the outlook for the remainder of the technology sector.

Meanwhile, analysts expect corporate uniform producer Cintas (CTAS 41.28, +0.02) to report earnings of $0.58 on revenues of $1.059 billion. Cintas guidance may provide an indirect glance into the labor market as higher uniform sales would likely be an indication of an uptick in hiring.DJ30 -5.14 NASDAQ -9.63 SP500 -2.85 NASDAQ Adv/Vol/Dec 923/1.32 bln/1483 NYSE Adv/Vol/Dec 1080/398.4 mln/1876

2:30 pm : The major averages have risen to fresh session highs, but the S&P 500 is off by 0.1%.

Green Mountain Coffee Roasters (GMCR 28.13, -2.68) is falling 8.7% after Starbucks (SBUX 50.98, +0.87) announced it will begin selling a single-serve brewing machine for $199.00. The Verismo will first be sold online before becoming available at Starbucks cafes next month. In addition to the $199.00 model, the company will also sell a $399.00 version which contains a larger water tank and an LCD display. Starbucks' presence in the single-serve market is expected to take a chunk out of a market previously dominated by GMCR's Keurig machines.DJ30 +9.33 NASDAQ -7.81 SP500 -1.90 NASDAQ Adv/Vol/Dec 935/1.23 bln/1448 NYSE Adv/Vol/Dec 1090/371.9 mln/1859

2:00 pm : The major averages are holding their afternoon levels. The Dow briefly crossed into positive territory, but has slipped back into the red since.

Healthcare stocks are generally higher as they benefit from the day's risk-off sentiment. Within the sector, Questcor (QCOR 29.39, +3.04) is higher by 11.4% as it rebounds after losing nearly 49.0% in yesterday's sell-off which was sparked by doubts as to whether insurance companies will cover Questcor's Acthar gel.

Providers of health care equipment and supplies are also seeing strength within the defensive sector. CryoLife (CRY 5.91, +0.15), Meridian Bioscience (VIVO 18.82, +0.36), and Masimo (MASI 25.23, +0.75) are all up between 2.0% and 3.0%.

On the downside, Horizon Pharmaceuticals (HZNP 3.50, -1.08) is slumping 23.6% after pricing a $75 million public offering of common stock and warrants at $3.50 per unit.DJ30 -5.92 NASDAQ -11.89 SP500 -3.59 NASDAQ Adv/Vol/Dec 852/1.13 bln/1518 NYSE Adv/Vol/Dec 1027/341.1 mln/1928

1:30 pm : After retracing half of their early losses, the major averages are holding their afternoon levels. The S&P 500 is down 0.3%.

The Dow Jones Transportation Average is sliding 2.8% as it underperforms the broader market. The bellwether group is showing considerable weakness as railroads weigh on the rest of transportation stocks. The four railroad components of the average are firmly lower after Norfolk Southern (NSC 66.15, -6.54) issued cautious guidance. CSX (CSX 21.62, -1.17), Kansas City Southern (KSU 76.62, -2.50), and Union Pacific (UNP 120.37, -4.68) are all down between 3.0% and 5.2%. Only Overseas Shipholding Group (OSG 7.18, +0.17) is managing to stay positive within the transportation average while CH Robinson (CHRW 57.37, -0.03) trades around its flat line.DJ30 -15.09 NASDAQ -12.15 SP500 -4.08 NASDAQ Adv/Vol/Dec 800/1.05 bln/1560 NYSE Adv/Vol/Dec 979/317.5 mln/1950

1:00 pm : Stocks began the session firmly in the red after a series of bearish data points crossed the wires. Japan reported a wider-than-expected trade deficit while the French PMI was well short of expectations. After reaching lows thirty minutes into the session, the major averages reversed in an attempt to reclaim their early losses. At midday, the S&P 500 is down 0.4%.

Consumer staples are outperforming the broader market as investors flock towards traditionally safe sectors. Beverage producers are generally higher with Monster Beverage (MNST 54.52, +0.77) leading the way, up 1.4%. The strength in the energy drink maker comes on the heels of renewed speculation of a possible takeover. Elsewhere, Constellation Brands (STZ 33.58, +0.42) and Pepsico (PEP 71.28, +0.43) are both up near 1.0%.

Cigarette makers are also on the rise. Altria (MO 33.49, +0.34), Lorillard (LO 120.29, +1.61), and Reynolds American (RAI 43.95, +0.34) are all up near 1.0%.

ConAgra Foods (CAG 27.38, +1.73) is surging 6.7% after beating on earnings and revenues. In addition, the management raised its full-year 2013 guidance and bumped up the dividend to $0.25.

Financial shares are lower across the board as banks give back some of their post-FOMC gains. The SPDR Financial Select Sector ETF (XLF 15.90, -0.14) is lower by 0.9%. Morgan Stanley (MS 17.15, -0.42) is sliding 2.6%, while Citigroup (C 33.72, -0.46) and Goldman Sachs (GS 116.94, -2.08) are both down near 1.5%. Earlier, UBS downgraded the three financials from ‘buy' to ‘neutral' in a move which resulted from the sector's 30.0% run-up since late July.

Two names are advancing as their shares begin trading publically. Online real estate search service, Trulia (TRLA 24.20, +2.13) is surging 42.4% in its public debut. Shares of the company began trading at $22.00 after the initial public offering was priced at $17.00. Trulia's peer, Zillow (Z 46.00, +0.45) has risen over 130.0% since the company went public in July of last year. Meanwhile, Susser Petroleum (SUSP 22.60, -0.80) is trading 10.2% above its initial public offering price of $20.50.

Industrial stocks are generally lower as the risk-off trade drives today's action. Rail stocks are posting the widest losses within the sector after Norfolk Southern (NSC 66.05, -6.64) cut its guidance due to slumping demand and decreasing revenues from fuel surcharges. Norfolk Southern is down 9.1% while Union Pacific (UNP 120.43, -4.61), CSX (CSX 21.61, -1.18), and Kansas City Southern (KSU 76.59, -2.53) are all sliding between 3.0% and 5.2%.

Among machinery producers, CLARCOR (CLC 44.77, -4.80) is down 9.7% after delivering a disappointing quarterly report. The company missed on earnings and revenues. The conference call contributed to the negative sentiment as management issued downside fourth quarter and full-year guidance.

Apogee Enterprises (APOG 20.28, +2.66) is a notable outlier within the industrial sector. The producer of building materials trades higher by 15.1% after beating on earnings and revenues. The management was upbeat in its conference call as upside guidance was issued for full-year 2013.

The latest weekly initial jobless claims count totaled 382,000, which is higher than the 375,000 that had been expected. The tally is above the revised prior week count of 385,000. As for continuing claims, they fell to about 3.272 million from 3.304 million.

Separately, the Philadelphia Fed Survey rose to -1.9 for September. The reading shows an improvement over last month's -7.1. Economists polled by Briefing.com had expected that the Survey would improve to a -4.0 reading.

Lastly, leading indicators for August decreased by 0.1%, which is worse than the unchanged reading that had been widely expected to follow the prior month's 0.4% increase.DJ30 -21.30 NASDAQ -15.61 SP500 -5.14 NASDAQ Adv/Vol/Dec 760/988.1 mln/1592 NYSE Adv/Vol/Dec 957/300.1 mln/1966

12:30 pm : Stocks are continuing their slow climb off session lows as the S&P 500 is off by 0.3%.

Two names are advancing as their shares begin trading publically. Online real estate search service, Trulia (TRLA 24.24, +2.14) is surging 42.6% in its public debut. Shares of the company began trading at $22.00 after the initial public offering was priced at $17.00. Trulia's peer, Zillow (Z 45.81, +0.26) has risen over 130.0% since the company went public in July of last year.

Meanwhile, Susser Petroleum (SUSP 22.77, -0.63) is trading 11.1% above its initial public offering price of $20.50.DJ30 -20.55 NASDAQ -14.57 SP500 -4.79 NASDAQ Adv/Vol/Dec 787/881.5 mln/1538 NYSE Adv/Vol/Dec 969/273.2 mln/1921

12:00 pm : The major averages are continuing their climb towards the unchanged line as the S&P 500 is down 0.2%.

Financial shares are lower across the board as banks give back some of their post-FOMC gains. The SPDR Financial Select Sector ETF (XLF 15.91, -0.13) is down 0.8%. Citigroup (C 33.80, -0.38), Goldman Sachs (GS 117.24, -1.78), and Morgan Stanley (MS 17.18, -0.39) are all down near 2.0% after UBS downgraded the three financials from ‘buy' to ‘neutral.' The downgrade comes after the sector rallied by more than 30.0% since late July.

Meanwhile, European financials are also lower. Banco Bilbao Vizcaya Argentaria (BBVA 8.17, -0.26) and Barclays (BCS 14.46, -0.27) are down 3.1% and 1.8%, respectively.DJ30 -10.00 NASDAQ -10.38 SP500 -3.25 NASDAQ Adv/Vol/Dec 850/785.1 mln/1457 NYSE Adv/Vol/Dec 1012/251.1 mln/1877

11:30 am : The major averages are near their session highs, but they remain in the red. The S&P 500 is down 0.3%.

Industrial stocks are generally lower as the risk-off trade drives today's action. Rail stocks are posting the widest losses within the sector after Norfolk Southern (NSC 66.00, -6.69) cut its guidance due to slumping demand and decreasing revenues from fuel surcharges. Norfolk Southern is down 9.2% while Union Pacific (UNP 120.74, -4.31), CSX (CSX 21.65, -1.13), and Kansas City Southern (KSU 76.89, -2.23) are all sliding between 2.5% and 5.0%.

Among machinery producers, CLARCOR (CLC 45.06, -4.51) is down 9.1% after delivering a disappointing quarterly report. The company missed on earnings and revenues. The conference call contributed to the negative sentiment as management issued downside fourth quarter and full-year guidance.

Apogee Enterprises (APOG 20.30, +2.68) is a notable outlier within the industrial sector. The producer of building materials trades higher by 15.2% after beating on earnings and revenues. The management was upbeat in its conference call as upside guidance was issued for full-year 2013.DJ30 -23.31 NASDAQ -12.83 SP500 -5.17 NASDAQ Adv/Vol/Dec 795/655.1 mln/1482 NYSE Adv/Vol/Dec 896/225.3 mln/1951

11:00 am : Equities have lifted off their early lows but the major averages remain in negative territory. The S&P 500 is down 0.3%.

Consumer staples are outperforming the broader market as investors flock towards traditionally safe sectors. Beverage producers are generally higher with Monster Beverage (MNST 55.18, +1.43) leading the way, up 2.6%. The strength in the energy drink maker comes on the heels of renewed speculation of a possible takeover. Constellation Brands (STZ 34.00, +0.84) and Pepsico (PEP 71.52, +0.67) are both up near 1.0%.

Cigarette makers are also on the rise. Altria (MO 33.60, +0.45), Lorillard (LO 120.44, +1.76), and Reynolds American (RAI 44.01, +0.40) are all up near 1.3%.

ConAgra Foods (CAG 27.42, +1.77) is surging 6.9% after beating on earnings and revenues. In addition, the management raised the full-year 2013 guidance and bumped up the dividend by a penny.DJ30 -21.99 NASDAQ -11.60 SP500 -4.28 NASDAQ Adv/Vol/Dec 770/520.3 mln/1449 NYSE Adv/Vol/Dec 875/189.1 mln/1944

10:35 am : The dollar index is trading near its session high, which is weighing on some commodities this morning.

Oct natural gas futures rallied this morning, trading to a new session high of $2.82/MMBtu. Just ahead of inventory, nat gas was +1.6% at $2.81/MMBtu, but following the data, which showed a build of 67 bcf vs the 65 bcf consensus, nat gas dropped a quick four cents to $2.77/MMBtu. Currently, nat gas is +1.3% at $2.80/MMBtu.

Nov crude oil has been in negative territory almost all session, but has been generally trending higher all morning. In recent trade, it's moved back near the unchanged line and is now -0.2% at $92.12/barrel.

Dec gold and Dec silver sold off a short while ago to new session lows (Gold $1757.70, Silver $34.12) and remain in the red in current activity. Gold is now -0.4% at $1764.90 and silver is -0.3% at $34.49/oz.DJ30 -42.94 NASDAQ -17.76 SP500 -7.01 NASDAQ Adv/Vol/Dec 557/369.4 mln/1628 NYSE Adv/Vol/Dec 681/151 mln/2121

10:00 am : The major averages continue to decline as the S&P 500 is down 0.6%.

The Philadelphia Fed Survey rose to -1.9 for September. That comes after August's reading of -7.1. Economists polled by Briefing.com had expected that the Survey would improve to a -4.0 reading for the month of September.

Separately, leading indicators for August decreased by 0.1%, which is worse than the unchanged reading that had been widely forecast to follow the 0.4% increase in the prior month.DJ30 -55.17 NASDAQ -21.90 SP500 -9.32 NASDAQ Adv/Vol/Dec 473/251.1 mln/1638 NYSE Adv/Vol/Dec 580/116.2 mln/2160

09:45 am : The major averages have maintained their early bearish sentiment as the S&P 500 trades lower by 0.5%.

Looking at the early sector alignment, consumer staples, utilities, and telecoms lead early. The three sectors are outperforming as the risk-off trade appears to be the theme of the day. Materials, industrials, and financials are all down near 1.0%.DJ30 -38.01 NASDAQ -18.47 SP500 -7.64 NASDAQ Adv/Vol/Dec 466/139.1 mln/1591 NYSE Adv/Vol/Dec 587/83.2 mln/2084

09:16 am : [BRIEFING.COM] S&P futures vs fair value: -6.80. Nasdaq futures vs fair value: -13.00. Heading into the open, equity futures remain near their pre-market lows, down 0.4%.

Transportation stocks bear watching today after Norfolk Southern (NSC 68.25, -4.44) lowered their third quarter earnings outlook due to slumping demand and decreasing revenues from fuel surcharges. Related names which may show related weakness include CSX (CSX 21.70, -1.09), Union Pacific (UNP 121.54, -3.51), and Kansas City Southern (KSU 79.12, 0.00).

The Philadelphia Fed Survey and leading indicators will be reported at 10:00 ET.

09:00 am : [BRIEFING.COM] S&P futures vs fair value: -6.70. Nasdaq futures vs fair value: -13.00. Equity futures continue pointing to a slightly lower open. The S&P 500 futures are down 0.4%.

It was a sea of red across Asia as all of the major averages finished in negative territory. China's Shanghai Composite fell 2.1%, and was the worst performer in the region after China's HSBC Flash Manufacturing PMI ticked up to 47.8 (47.6 previous) but remained in contraction. Elsewhere in the region, Japan's trade deficit widened to JPY0.47 trillion on expectations of a JPY0.37 reading.

Japan's Nikkei closed lower by 1.6% as companies with exposure to China were under pressure. Komatsu slid 3.1% and Nissan Motor fell 3.4% as the two names led their respective sector's lower. Elsewhere, Japan Airlines ended higher for a second day after Wednesday's initial public offering.

In Hong Kong, the Hang Seng slid 1.2% as shares were hit following the weak Chinese data. Commodity-related names were under pressure as Cnooc slipped 3.5% and Zijin Mining lost 3.8%. Meanwhile, a slowdown in the number of new subscribers weighed on mobile phone operator China Unicom as the stock tumbled 5.2% on news the company added 3.07 million subscribers in August after adding 3.09 million in July.

China's Shanghai Composite fell 2.1% as selling dropped the index to its lowest level since February 2009. Commodity names were weak as Chalco and China Shenhua Energy both fell 2.8%. Elsewhere, New China Life Insurance plunged 7.2% following a reported 6.1% decline in insurance premium income.

In Europe, markets are lower across the board after a handful of regional PMI readings missed expectations. The French PMI reading proved to be a disappointment as the service component was reported at 46.1 while expectations called for a reading of 49.4. Meanwhile, the manufacturing PMI showed a reading of 42.6 against the expectations of a 46.4 print. Equities and the euro both saw knee jerk moves lower in response to the weak data. Germany tried to save the day by exceeding expectations on both manufacturing and service PMIs. However, markets were largely unimpressed as the broader weakness appears to be too much for the European indices thus far. Lastly, the Eurozone services PMI also missed expectations as the actual reading of 46.0 fell short of the expected 47.4.

France's CAC is down 0.8% as financial names lag. Societe Generale, Credit Agricole, and BNP Paribas are all down near 2.5%. Hotel operator Accor leads the index, up 2.9%.

In the UK, the FTSE is lower by 0.7% as miners weigh on the index. Evraz is down 4.5%, while Anglo American, Vedanta Resources, and Kazakhmys are all down between 3.0% and 3.5%. On the upside, communication stocks British Sky Broadcasting Group and ITV are adding 1.1% and 1.5%, respectively.

Germany's DAX is off by 0.5% as the risk-off theme resonates throughout the region. Deutsche Bank is sliding 2.4% after agreeing to sell its BHF-Bank unit to RHJ International for EUR384 million. Peer Commerzbank is the biggest laggard of the session, down 4.2%. Airline Lufthansa is firmer by 1.6% after announcing it will combine short-distance flights with its discount Germanwings unit.

08:31 am : [BRIEFING.COM] S&P futures vs fair value: -6.20. Nasdaq futures vs fair value: -12.00. Equity futures remain lower by 0.3% after the release of the weekly initial and continuing claims.

The latest weekly initial jobless claims count totaled 382,000, which is higher than the 375,000 that had been expected. The tally is above the revised prior week count of 385,000. As for continuing claims, they fell to about 3.272 million from 3.304 million.

07:59 am : [BRIEFING.COM] S&P futures vs fair value: -4.80. Nasdaq futures vs fair value: -9.50. U.S. equity futures are lower by 0.3% amid relatively quiet pre-market trade.

Overnight, most of the major equity markets were trading in negative territory. After the latest round of quantitative easing, the focus is shifting back to data points which imply a continued struggle for business activity around the world. Japan's trade deficit declined, but markets seemed disappointed by exports falling for a third straight month. Autos and consumer electronics led the decline in the Nikkei. Elsewhere, the Shanghai Composite fell sharply following the HSBC Flash Manufacturing PMI which signaled another month of contraction. The reading was reported at 47.8, which was up slightly from last month's 47.6. The major Asian bourses finished firmly lower as China's Shanghai Composite fell 2.1%, while Japan's Nikkei slipped 1.6%, and Hong Kong's Hang Seng slumped 1.2%.

In Europe, markets took another leg down when French PMI largely missed expectations. The service component was reported at 46.1 while expectations called for a reading of 49.4. Meanwhile, the manufacturing PMI showed a reading of 42.6 against the expectations of a 46.4 print. Equities and the euro both saw knee jerk moves lower. Germany tried to save the day by exceeding expectations on both Manufacturing and Service PMIs. However, markets were largely unimpressed as the broader weakness appears to be too much for the European indices thus far. Lastly, the Eurozone services PMI also missed expectations as the actual reading of 46.0 fell short of the expected 47.4. Nearing midday, the major regional indices are all in the red. France's CAC is down 0.7%, UK's FTSE is lower by 0.6%, and Germany's DAX is off by 0.4%.

A handful of stocks are on the move in pre-market after reporting earnings and issuing guidance.

Adobe Systems (ADBE 33.35, +0.23) is higher by 0.7% despite reporting in-line earnings and missing revenue expectations. The company also issued downside guidance which serves as an ominous sign for third and fourth quarter earnings from other tech companies.

Bed Bath & Beyond (BBBY 65.54, -3.25) is down 4.7% after missing on earnings and reporting in-line revenues. In addition, the management issued in-line guidance as it expects earnings to be near the bottom of the estimate range.

Norfolk Southern (NSC 68.13, -4.56) is sliding 6.3% after lowering its third quarter earnings outlook due to declines in certain markets and lower revenues from fuel surcharges. Union Pacific (UNP 123.00, -2.05) is lower by 1.6% on related weakness.

Weekly initial and continuing claims will be reported at 8:30 ET, while the September Philadelphia Fed Survey and leading indicators will be released at 10:00 ET.

06:53 am : [BRIEFING.COM] S&P futures vs fair value: -4.50. Nasdaq futures vs fair value: -9.50.

06:52 am : Nikkei...9086.98...-145.20...-1.60%. Hang Seng...20590.92...-251.00...-1.20%.

06:52 am : FTSE...5855.20...-33.30...-0.60%. DAX...7361.17...-29.60...-0.40%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage