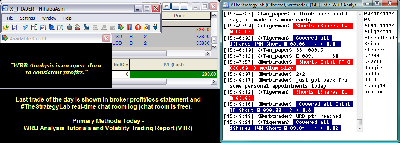

Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

091012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-280.png [ 78.06 KiB | Viewed 325 times ]

091012-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-280.png [ 78.06 KiB | Viewed 325 times ]

click on the above image to view today's performance verification Quote:

I had several personal appointments today that prevented me from trading most of key price movements. In fact, I was hoping the trading day would be very boring until I returned so that I wouldn't feel bad about missing price action that no trade opportunities.

Price Action Trade Performance for Today: +2.80 points or

$280 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the free

#TheStrategyLab chat room. You can read

today's #TheStrategyLab trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=108&t=1317.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

Price Action Analysis

Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=171&t=1594 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events via WRB Analysis from one trade to the next trade to give me the

market context before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day in the past involving key market events to help better understand my trading and reactions to the markets...something I can not get from my broker statements alone.

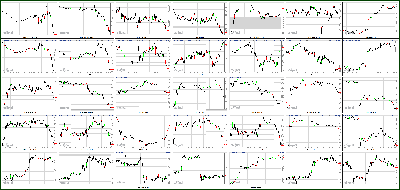

Attachment:

091012-Key-Price-Action-Markets.png [ 548.72 KiB | Viewed 329 times ]

091012-Key-Price-Action-Markets.png [ 548.72 KiB | Viewed 329 times ]

Market Update

Market Update 4:15 pm : Following a mostly uneventful, range-bound trading day, equities saw a late afternoon push to session lows. The major averages saw a notable divergence as the Dow slipped 0.4% while the S&P 500 and Nasdaq slid 0.6% and 1.0%, respectively.

The Dow Jones Transportation Average outperformed the broader market as most components posted gains. Airlines United Continental (UAL 20.06, +0.36) and Delta (DAL 9.38, +0.10) ended higher by 1.8% and 1.1%, respectively. Meanwhile, trucking stocks also showed strength. JB Hunt (JBHT 52.16, +0.51) and Con-way (CNW 29.98, +0.38) both gained near 1.0%.

Technology stocks lagged as major names within the space traded lower. Intel (INTC 23.26, -0.93) slid 3.8% as it remained under pressure after lowering its guidance on Friday. However, Intel's peer, AMD (AMD 3.47, +0.02) gained 0.6% after Goldman upgraded the shares from ‘sell' to ‘neutral.' In addition, major networking stocks showed weakness. F5 Networks (FFIV 96.63, -3.64) finished lower by 3.6%, while Cisco (CSCO 19.15, -0.41) slid 2.1%. Elsewhere, two tech giants traded near their respective all-time highs. Apple (AAPL 662.74, -17.70) marked a fresh all-time best at $683.29, but reversed into negative territory and ended down 2.6%. Meanwhile, Google (GOOG 700.77, -5.38) shed 0.8% as it nears its all-time high of $714.87.

Shares listed in the materials space advanced as names within the sector benefited from China's plan to increase infrastructure spending. Companies specializing in construction materials were led by Martin Marietta (MLM 84.18, +3.05) which added 3.8% after being upgraded from ‘equal weight' to ‘overweight' at Stephens. Meanwhile, Vulcan (VMC 41.44, +1.09) and Headwaters (HW 7.38, +0.43) advanced 2.7% and 6.2%, respectively.

Four paper and packaging producers slumped after receiving downgrades from Deutsche Bank. Rock-Tenn (RKT 66.97, -3.37), International Paper (IP 34.97, -1.51), Packaging Corp of America (PKG 32.44, -0.83), and KapStone (KS 20.75, -0.47) all lost between 2.0% and 5.0% on the news. The downgrade took place after the stocks went on a sharp rally in anticipation of a price increase in the fall. Deutsche Bank is skeptical as to the true ability of the producers to implement and maintain the said price hikes.

Casino and gaming stocks were mostly higher after Nevada Gaming Control Board reported July Las Vegas Strip revenues increased by 27.5% year-over-year. Boyd Gaming (BYD 6.32, +0.21), Isle of Capri Casinos (ISLE 6.42, +0.14), MGM Resorts (MGM 10.92, +0.22), and Wynn Resorts (WYNN 103.09, +0.35) added between 0.3% and 3.5%. Meanwhile, Caesars (CZR 7.10, -0.12), and Las Vegas Sands (LVS 43.41, -0.89) started the session in the black but ended lower by 1.7% and 2.0%, respectively.

According to the Federal Reserve, consumer credit decreased by $3.3 billion in July. This follows the prior month's reading of $6.5 billion, and is lower than the $10.0 billion that had been broadly expected among economists polled by Briefing.com.

Tomorrow's economic data is limited to July trade balance which will be reported at 8:30 ET.DJ30 -52.35 NASDAQ -32.40 SP500 -8.84 NASDAQ Adv/Vol/Dec 1006/1.53 bln/1448 NYSE Adv/Vol/Dec 1194/616.1 mln/1802

3:35 pm : Crude oil spent most of its pit trade chopping around in negative territory. The energy component slid to a session low of $95.34 per barrel in morning action. It then broke into positive territory but quickly fell back into the red. However, buyers stepped in as crude oil headed into the close and pushed prices up such that it closed 0.1% higher at $96.53 per barrel.

Natural gas came off its floor session low of $2.69 per MMBtu and inched higher for its entire session. A rally in the last half hour of pit trade took prices as high as $2.84 per MMBtu and had natural gas settle with a 4.9% gain at $2.81 per MMBtu. A stronger dollar and weak Chinese trade data put pressure on precious metals during today's pit session.

Gold spent its entire session in the red, dipping as low as $1729.20 per ounce. It settled slightly above that level at $1731.70 per ounce for a 0.5% loss. Silver came off its session low of $33.42 per ounce and briefly poked into positive territory where it touched a session high of $33.87 per ounce. Unable to hold on to the momentum, the metal fell back into the red and settled 0.3% lower at $33.63 per ounce.DJ30 -26.41 NASDAQ -27.87 SP500 -6.10 NASDAQ Adv/Vol/Dec 1083/1276.2 mln/1366 NYSE Adv/Vol/Dec 1314/403 mln/1648

3:00 pm : The S&P 500 and Nasdaq are pushing to fresh session lows, while the Dow is resisting the broader market pressure as it remains near its unchanged line.

According to recent reports, consumer credit decreased by $3.3 billion in July. This follows prior month's reading of $6.5 billion and is lower than the $10.0 billion that had been broadly expected among economists polled by Briefing.comDJ30 -16.83 NASDAQ -25.98 SP500 -4.26 NASDAQ Adv/Vol/Dec 1137/1.13 bln/1325 NYSE Adv/Vol/Dec 1442/356.9 mln/1507

2:30 pm : The Nasdaq continues pushing lower as it trails the broader market. The tech-heavy index is now off by 0.6%.

Casino and gaming stocks are mostly higher after Nevada Gaming Control Board reported July Las Vegas Strip revenues increased by 27.5% year-over-year. Boyd Gaming (BYD 6.36, +0.25), Isle of Capri Casinos (ISLE 6.45, +0.17), MGM Resorts (MGM 10.98, +0.28), and Wynn Resorts (WYNN 103.63, +0.89) are all up between 0.9% and 4.5% on the news. Meanwhile, Caesars (CZR 7.20, -0.02), and Las Vegas Sands (LVS 43.91, -0.39) started the session in the black but have slipped since. The two listings are down 0.3% and 0.9%, respectively.DJ30 -3.80 NASDAQ -18.97 SP500 -2.57 NASDAQ Adv/Vol/Dec 1153/1.03 bln/1284 NYSE Adv/Vol/Dec 1460/326.9 mln/1478

2:00 pm : The S&P 500 and Nasdaq have slipped to their session lows, while the Dow remains near its unchanged line.

Four paper and packaging producers are sliding after receiving downgrades from Deutsche Bank. Rock-Tenn (RKT 66.59, -3.74), International Paper (IP 35.00, -1.30), Packaging Corporation of America (PKG 32.45, -0.82), and KapStone (KS 20.80, -0.42) are all down between 1.9% and 5.2% on the news.The downgrade took place after the stocks went on a sharp rally in anticipation of a price increase in the fall. Deutsche Bank is skeptical as to the true ability of the producers to implement and maintain said price hikes.DJ30 -10.34 NASDAQ -19.12 SP500 -2.85 NASDAQ Adv/Vol/Dec 1150/954.2 mln/1280 NYSE Adv/Vol/Dec 1431/301.5 mln/1484

1:30 pm : The major averages continue to diverge as the S&P 500 and Dow approach session highs, while the Nasdaq trades just above its session low.

The Dow Jones Transportation Average is outperforming the broader market as most components make relatively significant advances. Airlines United Continental (UAL 20.34, +0.64) and Delta (DAL 9.46, +0.18) are higher by 3.1% and 1.9%, respectively. Meanwhile, trucking stocks are also showing strength, albeit not as robust. JB Hunt (JBHT 52.20, +0.55) and Con-way (CNW 29.95, +0.35) are both up near 1.0%.DJ30 +9.83 NASDAQ -11.71 SP500 -0.49 NASDAQ Adv/Vol/Dec 1264/878.7 mln/1140 NYSE Adv/Vol/Dec 1540/280.1 mln/1346

1:05 pm : Stocks began the session on a negative note and have maintained small losses throughout the day. The S&P 500 and Dow are hovering near their flat lines while the Nasdaq underperforms, down 0.5%.

The telecom sector is leading the way, up 0.8%. Within the group, Sprint (S 5.25, +0.22) is up 4.2% after Nomura upgraded the stock from ‘neutral' to ‘buy.' Other sector components seeing strength include Windstream (WIN 10.33, +0.13) and Verizon (VZ 44.14, +0.42), which are higher by 1.3% and 1.0%, respectively.

Technology stocks are underperforming as major names within the space trade lower. Intel (INTC 23.39, -0.79) is down 3.3% as it remains under pressure after lowering its guidance on Friday. However, Intel's peer, AMD (AMD 3.54, +0.09) is up 2.6% after Goldman upgraded the shares from ‘sell' to ‘neutral.' In addition, major networking stocks are showing weakness. F5 Networks (FFIV 98.09, -2.18) is lower by 2.2%, while Cisco (CSCO 19.16, -0.39) is sliding 2.0%. Elsewhere, two tech giants trade near their respective all-time highs. Apple (AAPL 672.88, -7.56) marked a fresh all-time best at $683.29, but has reversed into negative territory and is now down 1.1%. Meanwhile, Google (GOOG 705.58, -0.57) is off by 0.1% as it nears its all-time high of $714.87.

Shares listed in the materials space are rising as names within the sector benefit from China's plan to increase infrastructure spending. Companies specializing in construction materials are being led by Martin Marietta (MLM 84.95, +3.82) which is higher by 4.7% after being upgraded from ‘equal weight' to ‘overweight' at Stephens. Meanwhile, Vulcan (VMC 41.72, +1.37) and Headwaters (HW 7.34, +0.39) are up near 4.0% each. Coal stocks are also getting bid as James River Coal (JRCC 2.91, +0.15) and Arch Coal (ACI 6.83, +0.23) are advancing by 5.4% and 3.4%, respectively. Steel producers are also benefiting from the Chinese infrastructure plans. Cliffs Natural Resources (CLF 40.52, +0.61) is higher by 1.5% despite being downgraded from ‘buy' to ‘neutral' at Goldman. Other steel names are also higher as AK Steel (AKS 5.85, +0.08) and United States Steel (X 20.94, +0.05) are up 1.4% and 0.3%, respectively.

Titan Machinery (TITN 19.62, -5.74) is slumping 22.6% after delivering a mixed quarterly report. TITN missed on earnings, but beat on revenues. The company blamed the earnings miss on severe drought conditions in the Midwest, and lowered their full-year 2013 earnings expectations while leaving the revenue forecast unchanged.DJ30 +5.27 NASDAQ -13.74 SP500 -1.32 NASDAQ Adv/Vol/Dec 1175/816.2 mln/1211 NYSE Adv/Vol/Dec 1454/262.1 mln/1448

12:30 pm : The major averages continue to diverge as the Dow hovers near its unchanged line, while the Nasdaq has slipped back to its session low, down 0.5%.

Two names within the healthcare sector are showing considerable weakness after reporting disappointing research and development results. Geron (GERN 1.25, -1.65) is plunging 56.9% after announcing the discontinuation of its phase II study of a breast cancer drug, Imetelstat. The company also said it does not expect the drug to succeed in a second, separate study.

Zalicus (ZLCS 0.93, -0.46) is falling 33.0% after discontinuing its experimental rheumatoid arthritis treatment due to poor results. The company's drug, Synavive met the primary endpoints, but was unsuccessful with the second.

Elsewhere, Nordion (NDZ 6.98, -3.67) is slumping 34.5% after an arbitration panel rejected the company's claim against its supplier, Atomic Energy of Canada.DJ30 -0.18 NASDAQ -15.58 SP500 -1.98 NASDAQ Adv/Vol/Dec 1090/734.2 mln/1291 NYSE Adv/Vol/Dec 1362/240.1 mln/1518

12:00 pm : The major averages remain range bound as the S&P 500 and Dow hover near their respective unchanged lines.

Shares listed in the materials space are rising as names within the sector benefit from China's plan to increase infrastructure spending. Companies specializing in construction materials are being led by Martin Marietta (MLM 85.13, +4.00) which is higher by 5.0% after being upgraded from ‘equal weight' to ‘overweight' at Stephens. Meanwhile, Vulcan (VMC 41.93, +1.58) and Headwaters (HW 7.21, +0.26) are up near 4.0% each.

Coal stocks are also getting bid as James River Coal (JRCC 2.92, +0.16) and Arch Coal (ACI 6.71, +0.11) are advancing by 6.1% and 1.7%, respectively.DJ30 +6.23 NASDAQ -10.65 SP500 -0.76 NASDAQ Adv/Vol/Dec 1145/656.8 mln/1212 NYSE Adv/Vol/Dec 1455/218.2 mln/1401

11:30 am : The major averages are pushing higher as the Nasdaq continues to lag, down 0.4%.

Technology stocks are underperforming as major names within the space trade lower. Intel (INTC 23.49, -0.69) is down 2.9% as it remains under pressure after lowering its guidance on Friday. However, Intel's peer, AMD (AMD 3.53, +0.08) is up 2.5% after Goldman upgraded the shares from ‘sell' to ‘neutral.'

In addition, major networking stocks are showing weakness. F5 Networks (FFIV 97.78, -2.49) is lower by 2.5%, while Cisco (CSCO 19.23, -0.33) is sliding 1.7%.

Elsewhere, two tech giants trade near their respective all-time highs. Apple (AAPL 674.90, -5.54) marked a fresh all-time best at $683.29, but it reversed into negative territory and is now slipping 0.8%. Meanwhile, Google (GOOG 705.32, -0.82) is off by 0.1% as it nears its all-time high of $714.87.DJ30 +9.21 NASDAQ -13.39 SP500 -0.55 NASDAQ Adv/Vol/Dec 1062/572.1 mln/1268 NYSE Adv/Vol/Dec 1431/195.4 mln/1393

11:00 am : The major averages are showing some divergence as the Nasdaq underperforms, down 0.5%. Meanwhile, the Dow and S&P 500 trade near their respective unchanged lines.

The telecom sector is leading the way, up 0.8%. Within the group, Sprint (S 5.21, +0.18) is higher by 3.5% after Nomura upgraded the stock from ‘neutral' to ‘buy.' Other sector components seeing strength include Verizon (VZ 44.24, +0.52) and Windstream (WIN 10.25, +0.04), which are up by 1.1% and 0.5%, respectively.DJ30 -2.72 NASDAQ -15.32 SP500 -1.61 NASDAQ Adv/Vol/Dec 990/473.1 mln/1316 NYSE Adv/Vol/Dec 1349/168.5 mln/1461

10:35 am : Commodities are mixed today despite strength in the dollar index. Copper and natural gas are trading higher, while oil and precious metals are in the red.

Oct crude oil sold off earlier, around 8:45am ET, and pullback around $1.25 over the next 45 minutes to a new session low. Crude has since moved back above the $96 mark and is currently -0.2% at $96.19/barrel.

Oct natural gas was rallying sharply earlier and rose as high as $2.74. In current activity, nat gas is +1.0% at $2.71/MMBtu.

Precious metals have been trending lower during today's session and hit new session lows a short while ago (Gold $1729.20, Silver $33.41). However, silver is almost back to the unchanged line and is currently -0.1% at $33.65/oz, while gold is -0.4% at $1733.30/oz. Dec copper +1.3% at $3.69/lb.DJ30 -7.98 NASDAQ -13.52 SP500 -1.00 NASDAQ Adv/Vol/Dec 982/391.7 mln/1284 NYSE Adv/Vol/Dec 1394/145 mln/1388

10:00 am : Equities continue to hover near their opening levels as the S&P 500 is lower by 0.1%.

Steel producers continue to rally on stronger demand stemming from China's planned new infrastructure spending. Cliffs Natural Resources (CLF 41.59, +1.68) is higher by 4.2% despite being downgraded from ‘buy' to ‘neutral' at Goldman. Other steel names are also higher as AK Steel (AKS 6.02, +0.24) and United States Steel (X 21.26, +0.37) are up 4.3% and 1.8%, respectively.DJ30 -17.93 NASDAQ -9.23 SP500 -1.33 NASDAQ Adv/Vol/Dec 979/214.2 mln/1176 NYSE Adv/Vol/Dec 1326/93.5 mln/1384

09:45 am : Equities have turned lower since the open with the S&P 500 off by 0.2%.

Looking at the early sector performance, telecom leads the way, up 0.4%. Energy, materials, and discretionary stocks are also outperforming slightly as they hover near their unchanged lines. All other sectors are in the red with industrials and technology down 0.6% and 0.4%, respectively.DJ30 -30.99 NASDAQ -9.76 SP500 -2.66 NASDAQ Adv/Vol/Dec 861/142.4 mln/1231 NYSE Adv/Vol/Dec 1138/72.8 mln/1482

09:16 am : [BRIEFING.COM] S&P futures vs fair value: -2.60. Nasdaq futures vs fair value: -7.50. As the start of the U.S. session approaches, equity futures are pointing to a lower open by 0.3%.

Titan Machinery (TITN 21.63, -3.73) is slumping 14.7% after delivering a mixed quarterly report. TITN missed on earnings, but beat on revenues. The company blamed the earnings miss on severe drought conditions in the Midwest and lowered their full-year 2013 earnings expectations, while leaving the revenue forecast unchanged.

09:02 am : [BRIEFING.COM] S&P futures vs fair value: -2.60. Nasdaq futures vs fair value: -7.30. U.S. equity futures continue to point lower, with the S&P 500 futures down 0.3%.

The major Asian bourses saw a mixed session following the Chinese data dump. China's trade surplus expanded to $26.7 billion versus the expected $18.9 billion on both weaker-than-expected imports and exports. Pricing pressures were mixed as CPI printed an in-line 2.0% year-over-year, while PPI slowed to -3.5% on an annual basis. Meanwhile, industrial production rose 8.9% year-over-year and fixed asset investment expanded 20.2% since the start of the year. Elsewhere, Japan's Final GDP was revised down to reflect quarterly growth of 0.2% while 0.3% was expected, and current account readings both fell short of estimates. Australian home loans fell 1.0% month-over-month, while an increase of 0.1% was expected. Finally, Malaysian industrial production grew by 1.4% year-over-year when expectations called for 3.5% growth.

Japan's Nikkei closed unchanged as the strong yen weighed on exporters, and Intel's guidance cut hit chipmakers. Canon and Nissan Motor lost as much as 3.0% thanks to the continued strength in the yen while Advantest fell 4.4% in response to the Intel guidance. Construction names outperformed with Komatsu climbing 3.2% to lead the way.

In Hong Kong, the Hang Seng finished slightly higher by 0.1% despite weakness among Chinese banks. China Construction Bank and Industrial & Commercial Bank of China both shed 2.3% to limit the index's gains. Meanwhile, ZTE Corp. surged 6.1% after reports surfaced suggesting the co will be among those responsible for making a new line of phones for China Mobile Communications.

In China, the Shanghai Composite gained 0.3% as those names most sensitive to infrastructure spending led the way. Jiangxi Copper climbed 2.6% while Anhui Conch Cement and Xinjiang Tianshan Cement rallied 2.6% and 7.5% respectively.

European markets are quiet as the region's data was generally light. Both industrial and manufacturing production in France beat expectations. Italian second quarter GDP slipped a notch from its prior reading to reflect a contraction of 2.6% on a yearly basis. France also lowered its 2013 GDP forecast to an increase of 0.8% versus the prior expectation of 1.2%. French President Francois Hollande indicated he would initiate a EUR30 billion program, which includes new taxes and spending cuts in an effort to tighten the budget. Spain's 10-yr yield has declined to its lowest level since April, hitting 5.640%. Meanwhile, there are hints out of Greece suggesting talks between government officials and the Troika have a long way to go.

France's CAC is lower by 0.2% as financials continue to rally. Credit Agricole and BNP Paribas are up roughly 2.0% each. Industrial names are showing some weakness with Vallourec and Alstom down between 1.5% and 3.0%.

In the UK, the FTSE is flat as miners post broad gains. Kazakhmys leads the way, up 4.0%. Other mining stocks are also higher with Vedanta Resources, Rio Tinto, and Fresnillo all posting gains in excess of 2.5%. Meanwhile, consumer stocks trade lower with SabMiller and Associated British Foods down 2.1% each.

Germany's DAX is lower by 0.1% with drug makers lagging. Merck and Bayer are down 2.0% and 1.4%, respectively. German financials are extending their gains as Commerzbank and Deutsche Bank are higher by 3.3% and 2.5%, respectively.

08:28 am : [BRIEFING.COM] S&P futures vs fair value: -2.30. Nasdaq futures vs fair value: -6.80. U.S. equity futures are lower by 0.2%.

In M&A news, KSW (KSW 4.96, +0.89) is surging 21.9% after announcing the company will be acquired by privately-held Related Companies for $5.00 per share in cash. This represents a 23% premium to KSW's Friday closing price of $4.07 and the total transaction value is estimated at about $32.1 million.

08:00 am : S&P futures vs fair value: -1.80. Nasdaq futures vs fair value: -6.30. It is a quiet morning in the U.S. pre-market with equity futures pointing to a slightly lower open to start the week. The Federal Reserve's Thursday policy statement headlines the events of this week.

The world equity markets are mixed, with most indices hovering near their respective unchanged lines. China and Japan both released a flurry of economic data, which gave investors a mixed bag to digest. In China, trade balance was better than expected, but both imports and exports missed expectations. Industrial production came in slightly below projections while CPI and retail sales were reported in-line. The weaker-than-expected production data was most likely the key reading, and the miss suggests an ongoing slowdown, which investors took that as a greater likelihood the People's Bank of China would continue to add stimulus. Elsewhere, Japan's second quarter GDP was revised down a notch from its flash reading to indicate a 0.2% expansion on a quarterly basis.

In Europe, data was generally light. Both industrial and manufacturing production in France beat expectations. Italian second quarter GDP slipped a notch from its prior reading. France also lowered its 2013 GDP forecast to an increase of 0.8% versus 1.2% prior. French President Francois Hollande indicated he would initiate a EUR30 billion program, which includes new taxes and spending cuts in an effort to tighten the budget. Meanwhile, there are hints out of Greece suggesting talks between government officials and the Troika have a long way to go. At midday, key European indices are essentially flat.

Pre-market action this morning is limited to just a handful of names, and the moves are modest.

European financials continue to rally following the European Central Bank's announcement of the launch of an Outright Monetary Transactions program, or OMT. Deutsche Bank (DB 41.20, +1.02) and Royal Bank of Scotland (RBS 8.02, +0.16) are higher by 2.8% and 2.0%, respectively.

AIG (AIG 33.42, -0.57) is down 1.7% after the U.S. Treasury launched an offering of $18 billion of AIG common stock.

In economic news, consumer credit is the only notable data point, scheduled to be released at 15:00 ET.

06:23 am : [BRIEFING.COM] S&P futures vs fair value: -1.00. Nasdaq futures vs fair value: -6.00.

06:23 am : Nikkei...8869.37...-2.30...0.00. Hang Seng...19827.17...+25.00...+0.10%.

06:23 am : FTSE...5793.88...-0.90...0.00. DAX...7221.41...+6.90...+0.10%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader and

http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage