Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

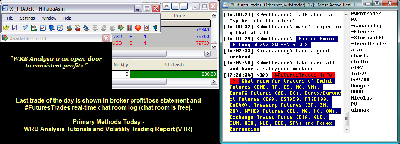

062912-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-830.png [ 76.16 KiB | Viewed 533 times ]

062912-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-830.png [ 76.16 KiB | Viewed 533 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +8.30 points or

$830 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. You can read

today's #FuturesTrades trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=105&t=1259.

To join our

free chat room...

log-in instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=162&t=1492 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

Stocks End First Half Of 2012 With A Bang Attachment:

062912-Key-Price-Action-Markets.png [ 519.35 KiB | Viewed 493 times ]

062912-Key-Price-Action-Markets.png [ 519.35 KiB | Viewed 493 times ]

click on the above image to view today's price action of key markets NEW YORK (CNNMoney) -- U.S. stocks soared Friday, and all three indexes closed out the first half of 2012 up more than 5%. The Nasdaq has etched double-digit gains.

A deal among European leaders to help struggling eurozone banks buoyed global markets Friday, at least temporarily erasing investors' looming fears over the viability of the eurozone.

While stocks have clocked broad gains for the year, all three indexes closed out the second quarter below first quarter highs. Fears over Europe pushed stocks down nearly 10% in early June.

Still, on Friday, investors looked solely at what was accomplished at the two-day European Union summit in Brussels. European leaders struck a "breakthrough" deal early Friday aimed at easing the recapitalization of banks.

Expectations were so low heading into the summit that the surprise announcement sparked widespread euphoria. Investors were relieved to see sky-high bond yields in Spain and Italy retreat from 7% -- the level that flashes bailout warning signals.

* Fear & Greed Index hits neutral"We're finally seeing a cause and effect," said Frank Davis, director of trading at LEK Securities. "It's a very positive sign that they can have a timely impact with some of the moves EU leaders make."

The Dow Jones industrial average (INDU) closed the day up 278 points, or 2.2%. The S&P 500 (SPX) gained 33 points, or 2.5%. The Nasdaq (COMP) added 86 points, or 3%.

Financial stocks led the broad worldwide rally.

In Paris, BNP Paribas (BNPQF) and Credit Agricole (CRARY) and Societe Generale (SCGLY) rose nearly 10%. In Frankfurt, Commerzbank (CRZBY) rose 5% and Deutsche Bank (DB) surged 7%. In Madrid, Banco Santander (SAN) jumped 7%.

In the United States, Bank of America (BAC, Fortune 500), Citigroup (C, Fortune 500), Morgan Stanley (MS, Fortune 500) and Goldman Sachs (GS, Fortune 500) all rose between 2% and 6%.

JPMorgan (JPM, Fortune 500), which is still reeling from news that its trading losses could jump as high as $9 billion, dipped slightly, and Barclays (BCS), which is under pressure for manipulating LIBOR rates, closed down 5%

U.S. stocks closed in negative territory Thursday, after clawing back in the final hour of trading from much steeper losses.

World markets: The EU deal includes a mechanism to inject capital directly into banks, which may reduce what Investec bond analyst Elisabeth Afseth called "the bank-sovereign negative feedback loop."

Afseth said the loop starts when a nation borrows to recapitalize its troubled banks, which then increases the country's debt, pushes up bond yields, reduces bond values and forces banks to require even more capital.

* European leaders reach key deal on banks"It's an important step," Afseth said, but she remains skeptical. "You have to be a little bit concerned where the funds are coming from. They could potentially run out quite quickly."

EU leaders are hoping for implementation of the bank agreement by July 9.

European stocks all closed higher. Britain's FTSE 100 (UKX) added 2%, the DAX (DAX) in Germany jumped 3.5% and France's CAC 40 (CAC40) rallied 3.8%.

Asian markets also ended higher. The Shanghai Composite (SHCOMP) closed just above breakeven, while the Hang Seng (HSI) in Hong Kong surged 3.1% and Japan's Nikkei (N225) gained 1.5%.

Economy: The Chicago Purchasing Managers' Index for June came in at 52.9, slightly below expectations of 53, but up from 52.7 last month. Any reading above 50 signifies expansion in the region's manufacturing sector.

The University of Michigan's Consumer Sentiment Index for June came in below expectations at 73.2, compared with 74.1 in May.

* Video - Stick a fork in it: BlackBerry's doneCompanies: Home builder KB Home (KBH) reported a second-quarter loss Friday that was smaller than expected, which pushed shares up 13%.

Nike (NKE, Fortune 500) shares tumbled 9%, a day after the company reported quarterly earnings that missed analyst estimates.

Shares of Research In Motion (RIMM) fell 19%, after the BlackBerry-maker reported a wider-than-expected loss Thursday, and another delay of its long-awaited BlackBerry 10 operating system.

Ford (F, Fortune 500) shares slid nearly 5%. On Thursday, the automaker lowered its guidance based on poor performance by its international divisions.

Shares of gun manufacturing company Smith & Wesson (SWHC) surged after the company's earnings beat profit expectations by a wide margin.

Currencies and commodities: The dollar fell against the euro, British pound and Japanese yen.

Oil for August delivery rose $7.27 to $84.96 a barrel.

Gold futures for August delivery jumped $53.80 to $1,604.20 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury fell, pushing the yield up to 1.65% from 1.58% late Thursday.

Market Update

Market Update 4:30 pm : The S&P 500 bounced 2.5% to score its best one-day percentage gain since December. The move helped fuel a strong weekly and monthly gain, but wasn’t enough to move stocks out of the red for the month.

A foray into stocks followed news that Eurozone officials have opened the door for Spain's banks to be directly recapitalized with bailout funds once Europe sets up a single banking supervisor. Moreover, Spain will not have to take on additional sovereign debt.

Market participants were also pleased to learn of a growth package worth 120 billion euros that will be aimed at boosting the European Investment Bank’s lending capacity.

The commitment of additional funds to address precarious conditions was taken as a positive rather than as a negative with implications for fiscal conditions. In turn, the euro rallied aggressively. By session’s end the euro was up 1.7% against the greenback.

Improved sentiment among market participants and a decidedly weaker dollar helped the case for commodities. In fact, the CRB Commodity Index rallied 4.6% for its best single-session spike in almost three years.

Crude oil was a primary driver of the CRB’s climb ahead of the EU's Iran oil sanctions set to begin on July 1. The energy component rallied 9.4% to settle at $85.02 per barrel, which translates into a 6.6% weekly gain.

With oil prices up and market participants willing to take on more risk, Energy stocks rallied to a collective gain of a little more than 3%. Still, they were slightly outperformed by Industrials and Tech plays; those two sectors each scored gains of 3.3%.

Utilities, which are decidedly defensive, encountered some selling after pushing higher in the early going. The sector was able to find support at the flat line before

to reclaim gains. It settled the session with a 0.6% gain, only a fraction of what the broad market scored.

Nike (NKE 87.78, -9.11) shares suffered a precipitous drop despite the decidedly positive tone to broad market trade. The stock’s slump came in response to a disappointing quarterly report. Ford (F 9.59, -0.50) shares also fell hard; the company’s latest profit forecast proved displeasing. A relatively soft forecast from Accenture (ACN 60.09, +3.46) was forgiven amid an upside earning surprise and broad market strength.

Personal income increased in May by 0.2%, which is slightly greater than the 0.1% increase that had been widely expected. However, personal spending stayed flat, instead of increasing by 0.1% as had been broadly anticipated. Core personal consumption expenditures were up 0.1% month over month. They had been generally expected to increase by 0.2%.

The June Chicago PMI reading of 52.9 came as little surprise since economists had generally expected a reading of 53.0 to follow the prior month reading of 52.7.

The only other item on the economic calendar was the University of Michigan's final Consumer Sentiment Survey for May. It eased down to 73.2 from the 74.1 that was posted in the preliminary Survey. Many had expected the reading to go unrevised.

In addition to encouraging news from Europe, participation picked up today as investment managers moved to rebalance and window dress their portfolios for the close of the quarter. For the second quarter the S&P 500 shed a little more than 3%. That was due to losses suffered in the past two months, offset partly by a 4.0% gain for June. The stock market’s 2.0% gain this week stands as its best performance since the first full week of the month. DJ30 +277.83 NASDAQ +85.56 NQ100 +3.1% R2K +2.9% SP400 +2.8% SP500 +33.12 NASDAQ Adv/Vol/Dec 2176/1.92 bln/378 NYSE Adv/Vol/Dec 2682/1.09 bln/393

3:30 pm : The CRB Commodity Index rallied 4.6% today, booking its best one-day bounce in almost three years.

Crude oil and precious metals surged in today's pit trade on stronger sentiment and a drop in the dollar following the agreement between EU leaders to provide relief fund access to sovereign debt and Spanish banks. The move also came ahead of the EU's Iran oil sanctions set to begin on July 1. Crude oil rose an impressive 9.4% in today's pit trade as it settled at $85.02 per barrel, just below its session high of $85.28 per barrel. Crude's rally pushed the energy component to settle the week 6.6% higher.

Natural gas also climbed higher in today's floor session. It finished the week 5.6% higher at $2.82 per MMBtu despite yesterday's drop amid a bigger-than-expected inventory build of 57 bcf.

Gold settled just below its session high of $1607.80 per ounce, closing the week 2.3% higher at $1603.50 per ounce. A rally in silver pushed prices as high as $27.92 per ounce and erased losses from its previous three sessions, such that the metal settled the week with a 3.6% gain at $27.67 per ounce. DJ30 +237.38 NASDAQ +77.34 SP500 +28.69 NASDAQ Adv/Vol/Dec 2145/1.35 bln/400 NYSE Adv/Vol/Dec 2635/545 mln/425

3:00 pm : Stocks enter the final hour of the session holding steady to their heady gains. The rally today stands as the best move for the S&P 500 in about three weeks. It also has the stock market on pace for a weekly gain of almost 2% and a monthly gain of almost 4%.DJ30 +240.33 NASDAQ +77.85 SP500 +29.22 NASDAQ Adv/Vol/Dec 430/1.25 bln/70 NYSE Adv/Vol/Dec 2130/500 mln/390

2:30 pm : The three major equity averages have inched up to new session highs. Their gains range from the Dow's 2% to a near 3% gain by the Nasdaq. Small-cap stocks and mid-cap stocks are also sporting gains on the order of almost 3%.DJ30 +244.83 NASDAQ +78.80 SP500 +28.62 NASDAQ Adv/Vol/Dec 2120/1.14 bln/400 NYSE Adv/Vol/Dec 2630/460 mln/415

2:00 pm : Stocks are drifting sideways in what is generally a rather unexciting crawl. However, the crawl comes with heady gains that have the broad market on pace for its best performance in about three weeks. The scope of the move has helped fuel the stock market's first monthly gain since March; losses in the last two months have left the stock market in the red for the second quarter.DJ30 +228.65 NASDAQ +74.52 SP500 +26.85 NASDAQ Adv/Vol/Dec 2105/1.04 bln/415 NYSE Adv/Vol/Dec 2635/425 mln/400

1:30 pm : Stocks have inched up to incrementally improved session highs that have resulted in a 2.0% gain for the S&P 500. The broad market measure hasn't had such a strong bounce since it rallied 2.3% earlier this month.DJ30 +233.69 NASDAQ +73.65 SP500 +27.40 NASDAQ Adv/Vol/Dec 2100/940 mln/405 NYSE Adv/Vol/Dec 2600/390 mln/415

1:00 pm : An increased appetite for risk following efforts by eurozone leaders to improve financial conditions in the region has the S&P 500 up almost 2%.

Stocks staged a strong gap higher at the open as participants responded to strong gains among the many major global averages and news that Eurozone countries opened the door for Spain's banks to be directly recapitalized with bailout funds once Europe sets up a single banking supervisor, so that Spain will not have to take on additional sovereign debt. Additionally, a 120 billion euro growth package was announced with the aim to boost lending capacity for the European Investment Bank. The positive response to Europe's efforts has also brought about aggressive buying interest in the euro, which is currently up 1.8% against the greenback.

Although ensuing gains have been broad, improved investor sentiment has been especially beneficial to cyclical stocks -- Materials, Industrials, Tech, Energy, and Financials are all up between 2% and 3%. Defensive in nature, Utilities have spent the past few hours descending steadily so that the sector is now at the flat line.

Amid improved investor sentiment and a dramatic drop by the dollar, commodities are on the climb. In fact, the 3.7% gain by the CRB Index today stands as its best one-day bounce since 2009. Oil has been a big driver of that move; it is now up to about $82 per barrel for a gain greater than 5%.

Share volume this session is relatively strong as efforts are made to partake in today's advance. End-of-quarter window-dressing by portfolio managers is also playing a large part.

Corporate news flow has been almost completely overshadowed by the headlines from Europe. Nike (NKE 89.54, -7.35) disappointed with its latest quarterly update, while Ford (F 9.61, -0.48) disappointed with its latest profit forecast. Accenture (ACN 59.59, +2.96) pleased with its latest quarterly report, though.

Economic data has had little sway with traders. There were no surprises to monthly personal spending and income numbers or the Chicago PMI. The final monthly reading on consumer sentiment from the University of Michigan was revised slightly lower, though. DJ30 +219.33 NASDAQ +71.45 SP500 +25.84 NASDAQ Adv/Vol/Dec 2065/880 mln/425 NYSE Adv/Vol/Dec 2555/365 mln/435

12:30 pm : The euro is up almost 2% against the greenback. Its bounce comes after Eurozone leaders dropped the requirement that taxpayers receive preferred creditor status on aid to Spain's banks, effectively opening the way to recapitalize the lenders directly with bailout funds once Europe sets up a single banking supervisor. That means Spain will not have to take on additional sovereign debt. The EU banking supervision will take time to form, however.

Leaders across the Atlantic also agreed that the bailout funds, through the European Central Bank, can buy sovereign bonds in both the primary and the secondary markets. A growth package of 120 billion euros was also announced; it will aim to boost lending capacity for the European Investment Bank and help small enterprises.DJ30 +211.23 NASDAQ +67.55 SP500 +25.12 NASDAQ Adv/Vol/Dec 2070/800 mln/400 NYSE Adv/Vol/Dec 2550/330 mln/430

12:00 pm : The stock market continues to trade with big gains. Volume has been strong, too. The increase in participation is partly a response to efforts by eurozone officials to improve financial conditions, but also because the end of the second quarter often results in asset rebalancing and "window dressing" by portfolio managers.DJ30 +220.16 NASDAQ +66.36 SP500 +25.58 NASDAQ Adv/Vol/Dec 2055/690 mln/395 NYSE Adv/Vol/Dec 2585/300 mln/385

11:30 am : With stocks holding steady to strong, broad gains Treasuries remain in the red. The benchmark 10-year Note is currently down a half of a point, which has been enough to lift its yield a few basis points back above 1.60% after it had traded down to its lowest point in about 10 days during the prior session.DJ30 +219.06 NASDAQ +66.77 SP500 +25.63 NASDAQ Adv/Vol/Dec 2020/590 mln/400 NYSE Adv/Vol/Dec 2605/255 mln/340

11:00 am : The S&P 500 has managed to move past the 1350 line after pausing at that point earlier this morning. Its climb comes on the back of a broad-based bid that has lifted all 10 major sectors to strong gains that range from the Utilities sector's 0.8% advance to the Industrials sector's 2.6% rally.DJ30 +209.30 NASDAQ +61.12 SP500 +23.99 NASDAQ Adv/Vol/Dec 2000/465 mln/380 NYSE Adv/Vol/Dec 2635/210 mln/285

10:30 am : Commodities continue to sport robust gains, keeping the CRB Index up with a gain of almost 3%. Their climb comes in conjunction with stronger sentiment, which has increased interest in risk assets, and a dramatic drop by the dollar.

Among the CRB's most closely tracked constituents, oil prices are up 5.7% to trade at $82.10 per barrel. Prices haven't been above $82 per barrel since last week. Fellow energy component natural gas is sporting a 2.0% gain at $2.79 per MMBtu.

Unable to extend its push past $1600 per ounce, gold prices are up 3.0% to $1596.10 per ounce. Meanwhile, silver is sporting a 4.4% gain at $27.44 per ounce. DJ30 +208.09 NASDAQ +62.71 SP500 +24.51 NASDAQ Adv/Vol/Dec 1995/360 mln/360 NYSE Adv/Vol/Dec 2615/170 mln/275

10:00 am : Stocks are holding strong to their gains. The action has the S&P 500 drifting along the 1350 line.

The June Chicago PMI reading of 52.9 came as little surprise since economists had generally expected a reading of 53.0 to follow the prior month reading of 52.7.

Separately, the University of Michigan's final Consumer Sentiment Survey for May eased down to 73.2 from the 74.1 that was posted in the preliminary Survey. Many had expected the reading to go unrevised. DJ30 +189.59 NASDAQ +49.60 SP500 +21.27 NASDAQ Adv/Vol/Dec 2005/120 mln/255 NYSE Adv/Vol/Dec 2535/85 mln/205

09:45 am : The final session of the week and of the second quarter has started on a strong note. In fact, this morning's bounce positions the broad market for its best one-day bounce in three weeks. That has the stock market headed for a 3.0% monthly gain -- its first monthly advance since March. However, the S&P 500 is still down more than 4% for the quarter. Of course, that comes after it rallied 12% in the first quarter.DJ30 +169.76 NASDAQ +1.64 SP500 +1.50 NASDAQ Adv/Vol/Dec NA/NA/NA NYSE Adv/Vol/Dec NA/NA/NA

09:15 am : S&P futures vs fair value: +23.50. Nasdaq futures vs fair value: +45.20. Efforts aimed at improving what have been persistently precarious conditions in Europe have helped global markets and domestic equity futures rally aggressively. The news has also stirred strong buying interest in the euro, which is now up 1.9% against the greenback after it had drifted down to a near three-week low of almost $1.240 just yesterday. With the dollar down sharply and market participants willing to accept more risk, commodity prices have bounded to big gains, such that the CRB Commodity Index is up 2.7% for its best single-session bounce in nine months. Neither a disappointing quarterly report from Nike (NKE 87.25, -9.64) nor in-line monthly personal income and spending numbers have undermined strengthened sentiment. Still on tap, though, is the latest Chicago PMI and the final monthly survey on consumer sentiment from the University of Michigan. They are due at 9:45 AM ET and 9:55 AM ET, respectively.

09:05 am : S&P futures vs fair value: +23.20. Nasdaq futures vs fair value: +45.20. Commodities are on the climb this morning, partly helped by the dollar's dramatic drop. Aggressive buying has oil prices up 5.4% to $81.90 per barrel, while natural gas sports a 1.4% gain at $2.77 per MMBtu. Precious metals have been pushed up after trading lower in recent sessions. Renewed interest has gold prices up 3.0% to $1598 per ounce, while silver sports a 5.3% gain at $27.68 per ounce. Collective strength in the space has the CRB Index up 2.7%, which stands as its strongest single-session spike in nine months.

08:35 am : S&P futures vs fair value: +21.00. Nasdaq futures vs fair value: +39.70. Personal income increased in May by 0.2%, which is slightly greater than the 0.1% increase that had been widely expected. However, personal spending stayed flat, instead of increasing by 0.1% as had been broadly anticipated. Core personal consumption expenditures were up 0.1% month over month. They had been generally expected to increase by 0.2%.

08:05 am : S&P futures vs fair value: +21.00. Nasdaq futures vs fair value: +39.70. A late rally helped stocks slash losses yesterday. Momentum from the move has extended into Friday's early action with help from headlines reporting that European leaders have agreed to measures aimed at reducing borrowing costs in Italy and Spain, where debt yields have retreated. The announcement was complemented by a growth package of 120 billion euros intended to boost lending capacity of the European Investment Bank was also announced. The news has helped drive the euro sharply higher; it was last quoted with a 1.6% gain against the greenback.

Relegated to secondary concern, a disappointing quarterly report from Nike (NKE 85.89, -11.00) has shares down sharply ahead of the open. Accenture (ACN 59.15, +2.52) has pleased investors with an upside earnings surprise, however. Note: ticker quotes reflect premarket prices.

As an aside, the economic calendar for today features monthly personal income and spending numbers, the latest Chicago PMI reading, and the final monthly survey on consumer sentiment from the University of Michigan.

06:30 am : [BRIEFING.COM] S&P futures vs fair value: +15.00. Nasdaq futures vs fair value: +28.00.

06:30 am : Nikkei...9006.78...+132.70...+1.50%. Hang Seng...19441.46...+29.60...+2.20%.

06:30 am : FTSE...5565.73...+72.70...+1.30%. DAX...6278.06...+128.20...+2.10%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader,

http://stocktwits.com/wrbtrader and

http://chart.ly/users/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage