Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

053112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-2150.png [ 75.62 KiB | Viewed 504 times ]

053112-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit-2150.png [ 75.62 KiB | Viewed 504 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: +21.50 points or

$2150 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. You can read

today's #FuturesTrades trading chat room logs for details (e.g. time, price, contract size) about each one of my trades from

entry to exit along with price action commentary as the trade traversed in comparison to what's shown in the above image...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=104&t=1235.

To join our

free chat room...

log-in instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=152&t=1459 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

U.S. Stock Market Wrap May 31 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. U.S. stocks fell, capping the biggest monthly decline for the Standard & Poor's 500 Index since September, as disappointment with American economic reports overshadowed optimism that Greece will stay in the euro.

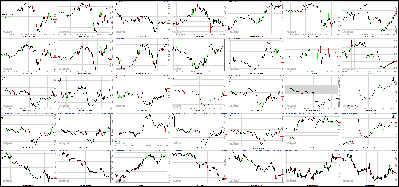

Attachment:

053112-Key-Price-Action-Markets.png [ 538.58 KiB | Viewed 502 times ]

053112-Key-Price-Action-Markets.png [ 538.58 KiB | Viewed 502 times ]

Market Update

Market Update 4:30 pm : Disappointing data played a part in dropping the S&P 500 to the 1300 line, which provided a floor for a rebound amid renewed interest in Financials, but the attempt to advance lost steam and left the stock market to suffer its second straight loss. During the course of May the broad market sank more than 6%, which makes it the worst month since September.

The major equity averages all dropped in excess of 1% in the prior session as attention returned to the troubles of Europe. Those concerns appeared to be tempered this morning as debt yields in the region retreated and the euro attracted a modest bid.

Those developments helped improve the mood among traders ahead of the open, but sentiment was undermined by a few economic reports that failed to meet expectations.

The latest ADP Employment Change report suggests that private payrolls increased during May by 133,000, which is less than the increase of 157,000 that had been expected, on average, among economists polled by Briefing.com. The report is often regarded as a preview of the official monthly payrolls report, which is due tomorrow.

Weekly initial jobless claims had remained near 370,000 for the past few weeks, but the latest tally increased to 383,000. It had been widely expected to come in at 368,000.

A revised reading of first quarter GDP also proved displeasing. It suggested that the economy expanded at a clip of 1.9%, down from the 2.2% increase that was featured in the preliminary reading, and less than the 2.0% pace that had been broadly anticipated.

The Chicago PMI reading made an unexpected pullback in May to 52.7 from 56.2 in April. Economists polled by Briefing.com had expected, on average, that it would improve to 57.0.

An absence if encouraging data and a midmorning pullback by the euro to a near two-year low of just $1.23 made it easy for stocks to slide to sizable losses. The S&P 500 was down about 1% to the 1300 line before it stabilized.

Technical support coincided with an upturn by Financials to help lift the broad market into afternoon trade. Financials were able to settle with a 0.7% gain amid help from bank stocks and shares of diversified financial services firms. Although Financials put on one of the better performances of the day, they fell more than 9% in May to suffer one of the worst monthly performances of any sector.

Telecom stocks were also strong today, but they have been performing well all month. The sector scored a 0.8% gain today, and a near 3% gain for the month. No other sector advanced in May. Many market participants have come to favor the sector’s defensive characteristics and relatively rich dividend yields. Some of those same features made Utilities the strongest performers of 2011.

While many stocks were able to slash their losses in afternoon action, the S&P 500 didn’t make a meaningful move into positive territory until the final 30 minutes. The effort came apart into the close, though, resulting in a return to negative territory by the closing bell.

For the second straight session Energy was the worst performing sector. It suffered a 0.9% loss; along the way it set a new seven-month low. Its descent has come in close correlation to a retreat by oil prices, which set new 2012 lows today at $85.86 per barrel before it settled pit trade at $86.51 per barrel for a 1.5% loss.

The end of the month brought about an increase in share volume, such that the number of shares traded on the NYSE surged above 1 billion to one of the highest tallies of 2012.

Advancing Sectors: Telecom +0.8%, Financials +0.7%, Utilities +0.6%

Declining Sectors: Consumer Discretionary -0.3%, Consumer Staples: -0.3%, Industrials -0.3%, Health Care -0.4%, Materials -0.5%, Tech -0.6%, Energy -0.9%DJ30 -26.41 NASDAQ -10.02 NQ100 -0.5% R2K +0.00% SP400 -0.3% SP500 -2.99 NASDAQ Adv/Vol/Dec 1195/2.11 bln/1350 NYSE Adv/Vol/Dec 1442/1.32 bln/1557

3:30 pm : Eurozone concerns and disappointing domestic data weighed on many commodities today, such that the CRB Index suffered a 0.8% loss. For the month of May it fell almost 11%, which stands as its worst monthly performance since this past September.

The CRB’s slide came as crude oil extended its slide for a third consecutive session. It set a new 2012 low of $85.86 per barrel in late morning action, but pushed up to a session high of $87.64 per barrel before it ultimately settled at $86.51 per barrel for a 1.5% loss. Inventory data that showed a build of 2.2 million barrels when a build of 1.0 million barrels had been anticipated didn’t help the case for crude.

Natural gas popped out of negative territory and traded up to a floor session high of $2.50 per MMBtu despite inventory data that showed a build of 71 bcf when a build of 70 bcf had been broadly expected. However, the energy component tumbled into the close and settled at $2.43 per MMBtu for a gain of just 0.4%.

Gold traded up to a pit session high of $1574.60 per ounce in morning action, but quickly slid into negative territory and touched a session low of $1553.00 per ounce. After some choppy action the yellow metal settled floor trade with a 0.1% loss at $1564.50 per ounce. For May it fell about 6%. As for silver, it began floor trade in negative territory and fell as low as $27.51 per ounce. Although it climbed into the black in afternoon action, silver ultimately settled at $27.80 per ounce, or 0.7% lower. Silver prices dropped about 10% this month. DJ30 +47.64 NASDAQ -0.68 SP500 +3.50 NASDAQ Adv/Vol/Dec 1075/1.32 bln/1420 NYSE Adv/Vol/Dec 1245/485 mln/1720

3:00 pm : The stock market is chopping along as participants prepare for the close, which is now only 60 minutes away. With the end of the session in sight, anticipation is building for the official monthly payrolls report due tomorrow morning -- earlier today participants were dealt a disappointing ADP Employment Change report that is usually regarded as a preview of the official nonfarm payrolls number. Tomorrow also brings the latest ISM Manufacturing reading and monthly construction spending numbers.DJ30 +1.89 NASDAQ -15.11 SP500 -2.95 NASDAQ Adv/Vol/Dec 1090/1.21 bln/1395 NYSE Adv/Vol/Dec 1255/450 mln/1715

2:30 pm : The major averages have stabilized since their recent slip. Despite the improved tone of trade, market participants continue to display a preference for defensive-oriented stocks. That has helped Telecom climb to a 0.8% gain. Up roughly 7% this year, Telecom stocks are among the strongest performers of 2012.

Utilities stocks were the strongest performers of 2011, but for 2012 they are flat. The sector is up 0.7% today. DJ30 +4.96 NASDAQ -13.11 SP500 -2.45 NASDAQ Adv/Vol/Dec 1035/1.11 bln/1425 NYSE Adv/Vol/Dec 1890/415 mln/1765

2:00 pm : The major equity averages have extended their backslide so that stocks are at their lowest level in about 90 minutes. Financials,

to maintain a modest gain, remain a source of support, but the sector's efforts are being undermined by weakness in the Energy sector and Tech sector, both of which are now down 0.8%.

The stock market's most recent leg lower has prompted the Volatility Index to rise a bit. That said, it remains down about 0.7% for the day after pulling back from an early session spike that sent it above 25 for a new multi-month high. DJ30 -23.04 NASDAQ -21.24 SP500 -5.42 NASDAQ Adv/Vol/Dec 1040/1.01 bln/1415 NYSE Adv/Vol/Dec 1170/380 mln/1760

1:30 pm : The S&P 500 recently came in contact with the flat line, but has been unable to extend its bounce off of session lows into positive territory. That struggle has prompted some participants to start paring their positions, forcing the broad market measure back into the red. The Dow has been implicated by the action so that it is now back near the unchanged mark after it had worked its way up to a modest gain. Meanwhile, the Nasdaq remains firmly in the red.DJ30 +7.04 NASDAQ -11.10 SP500 -1.79 NASDAQ Adv/Vol/Dec 1075/935 mln/1360 NYSE Adv/Vol/Dec 1250/350 mln/1670

1:00 pm : Disappointment stemming from a downward revision to first quarter GDP and an unexpected rise in weekly initial jobless claims prompted premarket participants to back off of an early morning bid that had come amid an upturn by the euro and a reduction in the yields of eurozone debt. The latest round of monthly retail sales, though generally solid, mattered little to most broad market traders.

The major equity averages all dropped to sizable losses in the early going. Selling intensified as the euro surrendered its early morning gain against the greenback. At its low the euro traded at just $1.23.

However, the S&P 500 was able to find support near the 1300 line. That provided a floor for stocks to stage a rebound, which was led by the Financial sector. Financials have bounded out of the red to a 0.4% gain with help from banking and diversified financial services plays. Still, the sector continues to trail Telecom, which is up 0.7% and outperforming for the second straight session.

Although the S&P 500 hasn't been able to fully rally out of the red just yet, the Dow has managed to push into positive territory. Its move has been helped by the likes of AT&T (T 34.18, +0.34), Wal-Mart (WMT 66.52, +1.08), and Chevron (CVX 98.57, +0.94). DJ30 +4.43 NASDAQ -13.05 SP500 -2.88 NASDAQ Adv/Vol/Dec 960/830 mln/1460 NYSE Adv/Vol/Dec 1115/315 mln/1800

12:30 pm : After a brief pause, stocks resumed their upward push so that the Dow poked into positive territory for a slight gain. It has since pulled back to the flat line. As for the S&P 500, it lost momentum as it came closer to the neutral line. Meanwhile, the Nasdaq remains in the red with a rather marked loss, although it is up from its session low, which made for a loss of more than 1% for the Nasdaq.DJ30 +1.55 NASDAQ -11.25 SP500 -2.62 NASDAQ Adv/Vol/Dec 900/750 mln/1530 NYSE Adv/Vol/Dec 960/280 mln/1945

12:00 pm : The stock market's recent rebound has encountered resistance. That has left the S&P 500 in the red with a sizable loss.

Financials had attempted to provide a broad market lift by running up to the neutral line, but the sector failed to to push into positive territory. That has caused the sector to slip back to a 0.2% loss.

Defensive-oriented stocks continue to trade with relative strength, though. Telecom, in particular, is up 0.4% today. The sector was also the prior session's top performing group. DJ30 -53.58 NASDAQ -24.84 SP500 -9.25 NASDAQ Adv/Vol/Dec 815/645 mln/1590 NYSE Adv/Vol/Dec 825/240 mln/2050

11:30 am : A recent bounce by the Financial sector has helped lift the broad market up from its session low, which is right near the 1300 line for the S&P 500. Banks and diversified financial services plays like JPMorgan Chase (JPM 33.19, +0.23) and Citigroup (C 26.34, +0.34) are helping to lead the effort.DJ30 -56.65 NASDAQ -25.73 SP500 -9.68 NASDAQ Adv/Vol/Dec 645/545 mln/1740 NYSE Adv/Vol/Dec 605/200 mln/2255

11:00 am : Stocks continue to lose ground. That has market participants pushing into Treasuries once again, resulting in a new record low yield for the benchmark 10-year Note of about 1.56%.DJ30 -83.70 NASDAQ -30.63 SP500 -11.87 NASDAQ Adv/Vol/Dec 630/430 mln/1680 NYSE Adv/Vol/Dec 685/160 mln/2145

10:35 am : Natural gas prices were recently flat at $2.42 per MMBtu, but have since fallen to $2.40 per MMBtu for a 0.7% loss in response to a weekly inventory report that showed a build of 71 bcf when a build of 70 bcf had been broadly expected.

Crude oil prices remain under heavy pressure. Futures prices currently price the commodity at $86.85 per barrel for a 1.1% loss. Prices set a new 2012 low of almost $86.50 per barrel earlier in the session. Weekly inventory numbers will be released at 11:00 AM ET.

Precious metals have come under pressure since moving in mixed fashion a couple of hours ago. In turn, gold prices are now grappling with a 0.3% loss at $1561 per ounce, while silver sits at $27.68 per ounce with a 1.1% loss. DJ30 -58.01 NASDAQ -28.70 SP500 -9.69 NASDAQ Adv/Vol/Dec 555/300 mln/1695 NYSE Adv/Vol/Dec 580/120 mln/2190

10:00 am : Stocks have extended their opening slide. Downside action has been more pronounced in the Nasdaq, which is contending with a loss that is now double that of the Dow due largely to weakness among large-cap Tech stocks like Google (GOOG 581.43, -6.80), Microsoft (MSFT 29.02, -0.32), and Apple (AAPL 573.18, -5.99).DJ30 -46.92 NASDAQ -23.65 SP500 -8.86 NASDAQ Adv/Vol/Dec 845/90 mln/1230 NYSE Adv/Vol/Dec 1150/55 mln/1420

09:45 am : Stocks have fallen into negative territory with the open of trading. The slide has been relatively broad based, but for the second straight session Energy stocks are experiencing some of the sharpest selling pressure. The sector is currently down about 0.8% after it sank about 3% yesterday. Another drop in crude oil futures, which currently price oil with a 0.9% loss at $87.05 per barrel, hasn't helped the sector's prospects.

Separately, the Chicago PMI reading fell from 56.2 in April to 52.7 in May. It had been widely expected to improve to 57.0. DJ30 -28.23 NASDAQ -14.98 SP500 -4.79 NASDAQ Adv/Vol/Dec NA/NA/NA NYSE Adv/Vol/Dec NA/NA/NA

09:15 am : S&P futures vs fair value: -0.30. Nasdaq futures vs fair value: -0.80. Stock futures remain relatively mixed after a modest bid that came amid an uptick by the euro and a downturn for yields in the eurozone was flattened by some disappointing data that featured a downward revision to first quarter GDP and an unexpected increase in weekly initial jobless claims. On the corporate front, many retailers are out with same-store sales results for May. Of the names covered by Briefing.com, those that exceeded expectations outnumber those that came short by about 2-to-1. Saks (SKS 9.97, +0.00), Target (TGT 58.50, +0.71), and TJX Co's (TJX 41.33, +0.00) were among those that exceeded expectations, but both Gap (GPS 26.26, -0.41) and Kohl's (KSS 46.65, -2.17) missed what had been widely forecasted. Note: ticker quotes reflect premarket prices.

09:05 am : S&P futures vs fair value: -1.50. Nasdaq futures vs fair value: -1.30. Oil prices have fallen to $87.50 per barrel for a 0.4% loss. Only minutes ago the price of oil fell to about $87.15 per barrel for a new 2012 low. Weekly inventory numbers will be posted at 11:00 AM ET. Before that, though, weekly natural gas inventory numbers will be released at 10:30 AM ET. Natural gas prices are also on the slide ahead of the inventory release, such that the energy component currently trades with a 1.1% loss at $2.39 per barrel. Precious metals are more mixed in that gold is up 0.1% to $1567 per ounce, while silver sits at $27.93 per ounce with a 0.2% loss.

08:35 am : S&P futures vs fair value: -1.70. Nasdaq futures vs fair value: -2.00. Stock futures have been undercut by the latest dose of data, which features a revised reading of first quarter GDP that points to a 1.9% increase, down from the 2.2% increase that was featured in the preliminary reading. The downwardly revised increase is less than the 2.0% increase that economists polled by Briefing.com had expected, on average. Also, the first quarter GDP Deflator was revised upward to reflect a 1.7% increase.

Separately, the latest initial weekly jobless claims count climbed by 10,000 week-over-week to 383,000 when it had been widely expected to ease down to 368,000. However, continuing weekly claims declined to about 3.24 million from roughly 3.28 million.

Still on tap for today is the latest Chicago PMI at 9:45 AM ET. Today's calendar also includes weekly natural gas inventory numbers at 10:30 AM ET, followed by weekly crude oil inventory numbers at 11:00 AM ET.

08:15 am : S&P futures vs fair value: +1.00. Nasdaq futures vs fair value: +2.30. Stock futures have attracted a modest bid after an aggressive bout of selling in the prior session sank the major equity averages for losses in excess of 1%. The improved tone comes as the euro ticks up against the greenback -- it is currently up 0.3% -- after it descended to a near two-year low yesterday. Moreover, yields on the debt of countries in the eurozone periphery have pulled back, suggesting concerns regarding macro conditions have been tempered, for now anyway.

Economic releases have been limited all week, but market participants were just dealt the latest ADP Employment Change, which indicates that private payrolls increased by 133,000 during May. The call among economists polled by Briefing.com had been for an increase of 157,000.

The bottom of the hour brings the second reading on first quarter GDP and weekly initial jobless claims. At 9:45 AM ET the Chicago PMI will be posted. Today's calendar also includes weekly natural gas inventory numbers at 10:30 AM ET, followed by weekly crude oil inventory numbers at 11:00 AM ET.

06:19 am : [BRIEFING.COM] S&P futures vs fair value: +1.70. Nasdaq futures vs fair value: +3.30.

06:19 am : Nikkei...8542.73...-90.50...-1.10%. Hang Seng...18629.52...-60.70...-0.30%.

06:19 am : FTSE...5344.32...+47.00...+0.90%. DAX...6316.69...+35.90...+0.60%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@

http://twitter.com/wrbtrader,

http://stocktwits.com/wrbtrader and

http://chart.ly/users/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage