Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

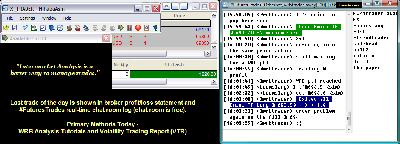

101911-wrbtrader-PnL-Blotter-Profit-1820.png [ 75 KiB | Viewed 277 times ]

101911-wrbtrader-PnL-Blotter-Profit-1820.png [ 75 KiB | Viewed 277 times ]

click on the above image to view today's trading summary Trade Performance for Today: +18.20 points or

$1820.00 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. Today's

#FuturesTrades trading chat room logs provides details (e.g. time, price, contract size) about each one of my trades from entry to exit along with price action commentary as the trade traversed...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=95&t=1031.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=5&t=180.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=144&t=1237 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

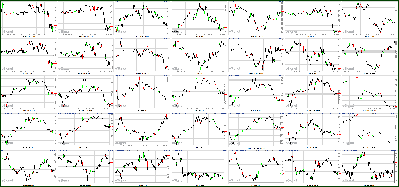

Attachment:

101911-Key-Price-Action-Markets.png [ 538.84 KiB | Viewed 259 times ]

101911-Key-Price-Action-Markets.png [ 538.84 KiB | Viewed 259 times ]

Market Update

Market Update 4:30 pm : The major equity averages descended to varied losses after they had spent the first half of the session chopping along listlessly in mixed fashion.

Momentum from the prior session's broad-based bounce was lost this morning as reports regarding plans to boost bailout funds in the EFSF were contradicted. Headlines indicative of conflicting goings on at meetings between eurozone officials played a part in an afternoon sell-off that left stocks to end the session at lows.

Of the major averages, the Nasdaq suffered the worst loss today. Its outsized decline came as Apple (AAPL 398.62, -23.62) shares dove in response to an earnings miss, which has been a rare occurrence in recent years. Shares of AAPL booked their worst percentage loss in three years. Given the weight of AAPL shares in the Nasdaq, its weakness offset strength in shares of Intel (INTC 24.24, +0.84) and Yahoo! (YHOO 15.94, +0.47), both of which reported a better-than-expected bottom line for the latest quarter.

Materials stocks were actually the worst performers. Challenged to find support, the sector slumped to a 3.0% loss.

Morgan Stanley (MS 16.64, +0.01) posted an upside surprise for the latest quarter, but its shares ended the day only a penny above where they began. In contrast, Travelers (TRV 54.39, +2.93) came short of the consensus earnings estimate, but its shares still rallied to a two-month high. Following its 5% spike yesterday, the financial sector failed to sustain an early bounce that left them to trade flat before descending alongside the rest of the market in late trade. They finished with a collective loss of 1.7%.

Homebuilders failed to sustain buying interest that had the SPDR S&P Homebuilders ETF (XHB 15.18, -0.17) up nicely on the back of news that housing starts climbed in September to an annualized clip of 658,000, which is the fastest pace since April 2010. The consensus among economists polled by Briefing.com had called for a slower rate more on the order of 595,000. Meanwhile, building permits slid to a rate of 594,000 from 610,000 in the prior month. An annualized rate of 610,000 permits had been generally expected.

There weren't any surprises to consumer price data for September. Overall consumer prices increased by 0.3%, just as had been broadly expected, while core prices increased by 0.1%, which is even less than the consensus call for a 0.2% increase. Just yesterday it was learned that overall producer prices increased by 0.8% in September, while core producer prices increased by 0.2% for the month.

There were no surprises to the Fed's latest Beige Book, which indicated that economic activity in many districts expanded at a modest or slight pace during September. A weaker or less certain outlook for business conditions was also generally noted.

Just as stocks wrestled with sellers this afternoon, oil futures came under pronounced pressure. The energy component benefited from an unexpected draw in weekly inventories and even traded as high as $89.69 per barrel before it dropped to $86.11 per barrel for a 2.5% loss. Other commodities were also clipped, resulting in a 1.3% loss for the CRB Commodity Index.

Amid the afternoon selling, the Volatility Index, often euphemistically labeled the Fear Gauge, spiked. At the close it was up more than 9% to trade above 34.

Advancing Sectors: Utilities +0.1%

Declining Sectors: Health Care -0.3%, Consumer Staples -0.4%, Telecom -0.6%, Energy -0.9%, Industrials -1.2%, Consumer Discretionary -1.5%, Financials -1.7%, Materials -3.0%DJ30 -72.43 NASDAQ -53.39 NQ100 -2.0% R2K -2.1% SP400 -1.6% SP500 -15.50 NASDAQ Adv/Vol/Dec 619/1.97 bln/1942 NYSE Adv/Vol/Dec 837/964 mln/2190

3:35 pm : It was a volatile session for crude oil, which posted a loss of 2.5% to finish at $86.11 per barrel. Crude oil rallied on the back of this morning's bearish inventory data, which showed a sizeable draw down versus expectations for a build. Futures, however, reversed off of highs at $89.69 and proceeded to trade back to the flat line, where they remained heading into the last 20 minutes of pit trade. Futures proceeded to fall on the back of the headlines pertaining to the euro zone and the role of the ECB, shedding approximately 2 points to trade to lows at $86.45 and ended just above that low. Natural gas posted a gain of 1.1% to settle at $3.59 per MMBtu. Futures rallied sharply heading into afternoon trade, notching highs at $3.63. They were unable to maintain that upward move and pulled back slightly into the close.

Precious metals pulled back heading into afternoon trade, after spending the majority of the morning chopping around the unchanged mark. Gold futures posted a decline of 0.4% to settle at $1647 per ounce, while silver shed 1.9% to end at $31.28 per ounce.DJ30 -71.29 NASDAQ -51.17 SP500 -14.79 NASDAQ Adv/Vol/Dec 661/1.6 bln/1862 NYSE Adv/Vol/Dec 882/680.6 mln/2151

3:00 pm : Stocks remain stuck near session lows as they enter into the final hour of the trading day. Despite the persistent pressure, participants are preparing for the next round of earnings reports. After the close, American Express (AXP 46.18, -0.50), eBay (EBAY 33.30, -0.57), Noble (NE 31.74, -0.66), and Stryker (SYK 49.36, +0.31) all report, along with a bevy of other names.DJ30 -73.07 NASDAQ -48.14 SP500 -15.11 NASDAQ Adv/Vol/Dec 660/1.33 bln/1840 NYSE Adv/Vol/Dec 880/540 mln/2090

2:30 pm : Stocks are descending deeper into negative territory with accelerating momentum. All three major equity averages are now at new session lows with marked losses. The drop still has a ways to go before it can fully offset the prior session's bounce, which actually undid a near 2% drop during trade on Monday.DJ30 -68.72 NASDAQ -50.50 SP500 -14.35 NASDAQ Adv/Vol/Dec 770/1.15 bln/1695 NYSE Adv/Vol/Dec 1135/465 mln/1820

2:05 pm : Stocks recently came under a bout of selling interest. The move coincided with word from CNBC commentators, citing other financial media, that officials in Europe are focusing on buying collateral for guarantees as part of the EFSF, but EU lawyers have rejected direct EFSF guarantees.

The Fed just released its latest Beige Book, which indicated that economic activity continued to expand in September, although many districts described the the pace of growth as modest or slight. A weaker or less certain outlook for business conditions was also generally noted. There hasn't been much of a reaction to the report among market participants. DJ30 +29.33 NASDAQ -22.78 SP500 -3.03 NASDAQ Adv/Vol/Dec 870/1.09 bln/1570 NYSE Adv/Vol/Dec 1265/430 mln/1660

1:30 pm : The major equity averages continue to trade in varied fashion as this session's listless, lackluster action continues. That said, share volume has been solid, suggesting that there remains plenty of participation on the part of investors.DJ30 +42.20 NASDAQ -16.86 SP500 -1.58 NASDAQ Adv/Vol/Dec 1070/955 mln/1345 NYSE Adv/Vol/Dec 1540/385 mln/1360

1:00 pm : Trade has been choppy all session. The lack of direction comes amid a lack of leadership.

Financials surged 5% yesterday to drive broad market gains, but overall action in the sector has slowed down today, leaving the sector to trade near the neutral line. However, a better-than-expected quarterly report from Morgan Stanley (MS 16.82, +0.19) has the investment banking and brokerage outfit boasting a nice gain. Dow component and insurance giant Travelers (TRV 54.85, +3.39) is an even stronger performer, despite an earnings miss.

Apple (AAPL 405.24, -17.00) also came short of the consensus earnings estimate, a foul infrequently commited by the company in recent years. The stock's weight and weakness have the overall tech sector down 0.9%. Although shares of AAPL have kept the Nasdaq in the red all session, Intel (INTC 24.45, +1.05) and Yahoo! (YHOO 16.16, +0.69) are both providing support to the tech-rich Index.

Materials stocks are generally in the worst shape. The sector is currently down 1.3% as steel stocks and chemical plays come under sharp pressure. Even Freeport McMoRan (FCX 35.24, -0.14) has drifted into the red, despite a quarterly report that featured a bottom line beat.

A handful of homebuilder shares are up nicely after data indicated this morning housing starts for September increased at a much stronger clip than what had been generally expected. The rate registered in September was actually the highest since April 2010.

Consumer price data for September were also posted. Both overall prices and core prices increased in stride with what had been expected.

Coming up at 2:00 PM ET is the latest Beige Book from the Fed. DJ30 +45.30 NASDAQ -12.36 SP500 +0.45 NASDAQ Adv/Vol/Dec 960/875 mln/1425 NYSE Adv/Vol/Dec 1440/350 mln/1455

12:30 pm : Stocks continue to chop along without much leadership. The action, or lack thereof, has made for a rather unexciting day of trade. It has also kept Treasuries confined to a narrow trading range.DJ30 +22.93 NASDAQ -16.27 SP500 -1.71 NASDAQ Adv/Vol/Dec 870/805 mln/1485 NYSE Adv/Vol/Dec 1355/320 mln/1540

12:00 pm : Stocks have come under a bit of pressure in recent trade. That has the S&P 500 back in negative territory, although its loss is only marginal.

Financials have had a rather choppy day after surging 5% in the prior session. A break in buying has left the sector to trade at the flat line, although it had been up with a solid gain a couple of hours ago. Morgan Stanley (MS 16.84, +0.21) has been a steady source of support whle many diversified bank stocks have faltered. Strength in the investment banking and brokerage outfit comes on the back of a better-than-expected quarterly report. DJ30 +14.91 NASDAQ -19.52 SP500 -1.93 NASDAQ Adv/Vol/Dec 1035/705 mln/1305 NYSE Adv/Vol/Dec 1615/285 mln/1255

11:30 am : Stocks are little changed from earlier levels. As such, the major equity averages continue to trade with varied results.

Treasuries have had a rather quiet trading session. The lack of action has left the benchmark 10-year Note near the neutral line and kept its yield just a couple of basis points below 2.20%.

The dollar remains under pressure, however. Its weakness today comes as both the euro and the sterling pound push higher. The euro was recently quoted with a 0.4% gain at $1.379, while the pound is presently up 0.6% at $1.580. DJ30 +48.82 NASDAQ -8.51 SP500 +2.74 NASDAQ Adv/Vol/Dec 980/575 mln/1310 NYSE Adv/Vol/Dec 1545/235 mln/1305

11:00 am : The S&P 500 managed to attract some support at the 1220 line, allowing the broad market to work its way out of the red. The benchmark Index now sports a modest gain. The Dow has followed suit and has actually moved a nose ahead of its counterpart.

The Nasdaq remains mired in the red, though. Its weakness comes as participants push against tech stocks after Apple (APPL 406.13, -16.11) failed to meet the consensus earnings estimate, let alone exceed it. Such a foul has occurred in only a few instances in recent years, resulting in a concerted selling effort that dropped the stock to a loss of more than 5%, which put shares on pace for one of their worst losses of the past two years. Although pressure has eased in the past hour, the stock is still on track for its poorest performance in two months. DJ30 +39.02 NASDAQ -8.93 SP500 +2.29 NASDAQ Adv/Vol/Dec 990/445 mln/1230 NYSE Adv/Vol/Dec 1625/185 mln/1150

10:35 am : Oil prices oscillated ahead of the open, but were able to start pit trade in positive territory. The energy component then struggled to sustain an established direction ahead of weekly inventory numbers, which were just posted. Crude oil inventories for the week ended October 14 showed a draw of 4.7 million barrels, which comes in stark contrast with the consensus call for a build of 2.0 million barrels. Oil prices responded by making a run above $89.50 per barrel, but they have since pulled back so that they now trade at $89.25 per barrel. That makes for a 0.8% gain.

Elsewhere in the energy complex, natural gas prices are up 1.6% to $3.61 per MMbtu. The commodity has sported a strong gain all morning.

Action among precious metals has given gold a modest 0.3% gain, which puts the yellow metal at $1657.50 per ounce. Meanwhile, silver has surrendered its morning gain so that it now trades with a 0.2% loss at $31.77 per ounce. DJ30 +28.23 NASDAQ -11.34 SP500 +2.57 NASDAQ Adv/Vol/Dec 800/335 mln/1385 NYSE Adv/Vol/Dec 1325/140 mln/1380

10:00 am : Broad market action remains choppy. That has kept the S&P 500 not far from the neutral line. The Nasdaq has descended deeper into negative territory, though.

While tech stocks have declined to a collective loss of 1.4%, materials stocks are actually in the worst shape of any major sector. They're already down 2.0% as diversified chemicals plays, agricultural chemicals plays, and diversified metals and miners issues come under pronounced selling pressure.

Utilities have attracted strong buying interest as some participants show an increased apprehension toward risk taking. In turn, the sector is up in excess of 1%. DJ30 -15.66 NASDAQ -23.72 SP500 -4.55 NASDAQ Adv/Vol/Dec 820/115 mln/1150 NYSE Adv/Vol/Dec 1305/55 mln/1230

09:45 am : The Dow and S&P 500 are both stuck near the flat line, but the Nasdaq is lagging due to weakness in heavyweight Apple (AAPL 403.62, -18.62). That said, large-cap tech plays Yahoo! (YHOO 16.17, +0.70) and Intel (INTC 24.19, +0.79) are providing support. Overall, though, tech stocks are collectively down 1.0%, which makes them one of this morning's worst performing sectors.DJ30 -21.57 NASDAQ -16.37 SP500 -2.29 NASDAQ Adv/Vol/Dec NA/NA/NA NYSE Adv/Vol/Dec NA/NA/NA

09:15 am : S&P futures vs fair value: +1.60. Nasdaq futures vs fair value: -11.00. Stock futures point to a mixed start for today's trade. The muddled action comes amid conflicting reports about the willingness of eurozone leaders to increase the funds in the region's EFSF bailout plan. Those reports haven't dissuaded buyers from boosting Europe's major bourses, though. Buying continues in the wake of some relatively unsurprising news that Spain's debt was downgraded by analysts at Moody's. Earnings haven't exactly boosted confidence this morning. The latest report from Apple (AAPL) featured earnings that actually failed to meet what Wall Street had expected. However, fellow large-cap issues Intel (INTC) and Yahoo! (YHOO) both bested expectations for the bottom line. Investment banking and brokerage outfit Morgan Stanley (MS) also posted an upside surprise. Data today has featured tepid increases in consumer prices and an unexpectedly strong pickup in the pace of new home sales. Still on the economic calendar for today is the Fed's latest Beige Book, which will be posted at 2:00 PM ET.

09:05 am : S&P futures vs fair value: +2.00. Nasdaq futures vs fair value: -10.50. Oil prices are up 0.4% to $88.85 per barrel in the first few minutes of pit trade. Price action could pick up with weekly inventory numbers at 10:30 AM ET. Elsewhere in the energy complex, natural gas prices are up 1.4% to $3.60 per MMBtu. As for precious metals, gold prices are up 0.2% to $1656 per ounce, while silver prices are sporting a 0.7% gain at $32.05 per ounce. Overall action in the commodity complex has the CRB Commodity Index up 0.4% this morning.

08:35 am : S&P futures vs fair value: +2.70. Nasdaq futures vs fair value: -9.30. Action ahead of the open generally remains lackluster, but stock futures have reclaimed a few points following the latest dose of data. Overall consumer prices increased in September by 0.3%, just as had been expected among economists polled by Briefing.com. Core prices increased a mere 0.1%, which is slightly less than the consensus call for a tepid increase of 0.2%. Just yesterday it was learned that overall producer prices increased by 0.8% in September, while core producer prices increased by 0.2% for the month.

Separately, the pace housing starts climbed in September to an annualized clip of 658,000 from a downwardly revised 572,000 in the prior month. The consensus among economists polled by Briefing.com had called for a rate closer to 595,000 units for September. Meanwhile, building permits registered a rate of 594,000, which is less than the annualized rate of 625,000 recorded for the prior month and also less than the rate of 610,000 permits that had been generally expected.

08:05 am : S&P futures vs fair value: -0.10. Nasdaq futures vs fair value: -15.50. The stock market advanced 2% yesterday, but momentum from the move has failed to extend into premarket trade as participants question the validity of recent reports regarding a bigger bailout plan for Europe. That said, the euro is up 0.6% to $1.382 at the moment.

Meanwhile, earnings from Apple (AAPL) came short of the consensus estimate for one of the few times in recent history. The miss has shares of AAPL down about 5% this morning. In contrast, shares of both Intel (INTC) and Yahoo! (YHOO) are up more than 3% following upside surprises. Abbott Labs (ABT) boasts a gain on the order of 10% after it posted a bottom line beat of its own, but also announced plans to separate its core businesses.

Action has been quient among the more widely tracked commodities. In particular, crude oil prices are down only fractionally to $88.45 per barrel ahead of pit trade. Volatility could increase with the release of weekly inventory numbers at 10:30 AM ET.

Consumer price data are due at the bottom of the hour, along with monthly housing starts. Also on the economic calendar is the latest Beige Book, which will be released at 2:00 PM ET and is expected to be as exciting as its name suggests.

06:53 am : [BRIEFING.COM] S&P futures vs fair value: +6.40. Nasdaq futures vs fair value: -5.00.

06:53 am : Nikkei...8772.54...+30.60...+0.40%. Hang Seng...18309.22...+232.80...+1.30%.

06:53 am : FTSE...5461.15...+50.80...+0.90%. DAX...5949.30...+71.90...+1.20%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage