Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

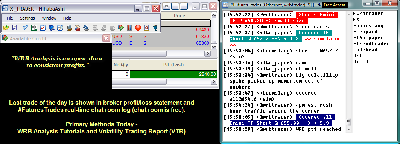

Attachment:

100711-wrbtrader-PnL-Blotter-Profit-2840.png [ 74.94 KiB | Viewed 343 times ]

100711-wrbtrader-PnL-Blotter-Profit-2840.png [ 74.94 KiB | Viewed 343 times ]

click on the above image to view today's trading summary Trade Performance for Today: +28.40 points or

$2840.00 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. Today's

#FuturesTrades trading chat room logs provides details (e.g. time, price, contract size) about each one of my trades from entry to exit along with price action commentary as the trade traversed...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=95&t=1022.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=5&t=180.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=144&t=1237 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

U.S. Stocks Fall as Europe Concern Offsets Jobs Report Oct. 7 (Bloomberg) -- Bloomberg's Deborah Kostroun reports on the performance of the U.S. equity market today. U.S. stocks retreated, trimming a weekly advance for the Standard & Poor's 500 Index, as concern Europe's debt crisis will worsen overshadowed faster-than-forecast growth in American employment.

Stocks post gains for the week Attachment:

100711-Key-Price-Action-Markets.png [ 540.15 KiB | Viewed 331 times ]

100711-Key-Price-Action-Markets.png [ 540.15 KiB | Viewed 331 times ]

click on the above image to view today's price action of key markets By Ben Rooney October 7, 2011: 5:09 PM ET

NEW YORK (CNNMoney) -- U.S. stocks ended a strong week on a low note Friday as ongoing concerns about the European debt crisis overshadowed a better-than-expected report on the U.S. job market.

The Dow Jones industrial average (INDU) fell 20 points, or 0.2%, to close at 11,103. The S&P 500 (SPX) lost 9 points, or 0.8%, to 1,155. The tech-heavy Nasdaq composite (COMP) dropped 27 points, or 1.1%, 2,479.

Despite the poor performance Friday, all three indexes posted gains for the week. The Dow rose 1.7%, the S&P 500 added 2.1% and the Nasdaq rose 2.6% over the last five days.

The gains were driven largely by speculation that European leaders are warming to the idea of pumping more money into troubled banks. On Thursday, the European Central Bank announced plans to increase the flow of capital to the banking system.

But investors remain skeptical that policy makers will be able to effectively resolve the underlying sovereign debt problems in Greece, Portugal, Ireland, Italy and Spain.

"The market knows that talk is cheap," said Ryan Larson, a senior equity trader at RBC Global Asset Management. "At some point, the talk has to turn into action if this rally is going to be sustained."

On Friday, stocks opened higher after the U.S. government said employers added 103,000 jobs in September, much more than expected.

But concerns about the debt crisis in Europe were thrust back into the spotlight after Fitch cut its credit ratings for Italy and Spain.

Fitch downgraded Italy's long-term default rating one notch to A+, saying the intensifying eurozone debt crisis "constitutes a significant financial and economic shock which has weakened Italy's sovereign risk profile."

The ratings agency also cut is default rating for Spain two notches to AA+. Fitch said the downgrade reflects Spain's fiscal position and dim economic outlook, as well as the broader debt crisis.

The outlook for both nations is negative, said Fitch.

In addition, Moody's downgraded 12 U.K. financial institutions Friday, warning that some smaller banks may be allowed to fail.

"This continues to be a headline-by-headline driven market," said Larson.

* Video - Buffett on the economy, taxes and ObamaThe employment report provided "some reason to be cautiously optimistic," he said, adding that "the selling accelerated after the headlines from Fitch."

The ratings action was not a surprise. Italy has already been downgraded recently by Moody's and Standard & Poor's. "Nonetheless, the market is responding," said Larson.

Shares of financial institutions were among the hardest hit. Bank of America (BAC, Fortune 500), JPMorgan (JPM, Fortune 500), Citigroup (C, Fortune 500), Morgan Stanley (MS, Fortune 500), Goldman Sachs (GS, Fortune 500) fell sharply.

Investors gravitated toward defensive stocks in the health care and consumer staples sectors. Pfizer (PFE, Fortune 500), Merck (MRK, Fortune 500), Johnson & Johnson (JNJ, Fortune 500) and Walmart (WMT, Fortune 500) were all higher.

On Thursday, U.S. stocks rallied for a third straight day as investors grew optimistic that European leaders are planning a coordinated plan to

recapitalize troubled banks.

Doug Cote, chief market strategist at ING Investment Management, said eliminating the threat of a banking crisis in Europe could set the stage for a sustained rally.

"All the market wants is a fence built around the risk in Europe," he said. "And it looks like that's happening."

Cote said stocks could move sharply higher if policy makers in Europe contain the crisis and investors refocus on the economic and corporate "fundamentals."

"The market has priced in a worse case scenario and once that gets unwound, we may be in for an explosive rally," he said. "We're telling clients: don't capitulate because this could turn around very fast."

Economy: The economy gained 103,000 jobs last month, while the unemployment rate held steady at 9.1%.

A CNNMoney survey of 22 economists had forecast that the U.S. economy added 65,000 jobs in September, with the unemployment rate expected to remain unchanged at 9.1%.

Investors are worried about the economy heading into another recession if the labor situation doesn't start to show marked improvement.

Companies: Shares of biotech firm Illumina (ILMN) plunged 32% after the company sharply cut its revenue outlook Thursday and several analysts cut their ratings on Illumina early Friday.

Other biotechs followed suit, with shares of Life Technologies (LIFE), Qiagen (QGEN), Thermo Fisher Scientific (TMO, Fortune 500) and Affymetrix (AFFX) all down sharply.

Sprint (S, Fortune 500) shares sank 19% as analysts questioned the cost of the company's plan to offer unlimited data plans for Apple's (AAPL, Fortune 500) iPhone.

World markets:European stocks closed higher. Britain's FTSE 100 (UKX) rose 0.2%, the DAX (DAX) in Germany and France's CAC 40 (CAC40) both added 0.5%.

Japan's central bank announced Friday it would keep its already very low interest rates unchanged.

Asian markets ended higher. The Hang Seng (HSI) in Hong Kong advanced 3.1% and Japan's Nikkei (N225) rose 1.0%. Shanghai (SHCOMP) was closed for holiday.

* China isn't the only currency 'manipulator'Currencies and commodities: The dollar weakened against the euro and the British pound, but gained versus the Japanese yen.

Oil for November delivery gained 39 cents to $82.98 a barrel.

Gold futures for December delivery fell $17.40 to $1,635.80 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury increased to 2.07%, up from 1.99% late Thursday.

Market Update

Market Update 4:45 pm : Failure to sustain a rebound from midday losses left stocks to roll into the red during the final hour. They still made it out with week 2% higher than where they started.

The major equity averages lacked direction this morning, even though premarket participants had cheered the September jobs report. Nonfarm payrolls grew by 103,000, up from an upwardly revised 57,000 in August. However, the upside surprise is mostly due to the end of a strike at Verizon. Excluding those workers, payrolls increased by 58,000, which is on par with the 60,000 new jobs that had been generally expected among economists polled by Briefing.com. Meanwhile, private payrolls increased by 137,000, which came on top of the upwardly revised 42,000 jobs that were added during the prior month. An increase of 83,000 had been broadly expected.

The number of people entering the workforce was roughly the same as the number of workers who found jobs in September, so the unemployment rate remained at 9.1%, which is exactly what had been expected. However, job gains were mostly part-time, resulting in an increase in underemployment that took the "real" unemployment rate up to 16.5% from 16.2% in the prior month.

Even though the payrolls report proved better-than-expected, stocks lacked leadership at the open of trade. That made it difficult for the major equity averages to extend their streak of gains to a fourth straight session.

The listlessness of early trade left stocks to slide into negative territory. Selling intensified in response to news that analysts at Fitch cut their ratings on Italy and Spain. At its low, the stock market was down more than 1%.

Stocks managed to stage a steady afternoon rebound that took the market back to a modest gain, but the move ultimately broke down in the final few minutes of trade. Although the late dive took all three major equity averages into negative territory, losses were steepest for the Nasdaq, which was hurt by weakness among biotech plays. Strength among a few blue chips helped limit the extent of the Dow's decline.

Financials were a drag all session. The sector descended to a 3.7% loss as bank stocks buckled. Banks were likely imbued by news that analysts at Moody's downgraded a dozen banks in the United Kingdom and a handful of others in Portugal.

Financials actually fueled broad market gains in the prior session, but only after the sector rallied back from an early loss. Their leadership yesterday helped the S&P 500 push through resistance at the 1160 line. Of course, the late slide on Friday caused the S&P 500 to finish the week below that mark.

Shares or retailers were also in play yesterday. The attention came after a relatively mixed batch of same-store sales results for September.

Initial weekly jobless claims on Thursday didn't have much of an influence on the mood of market participants, mostly because the 401,000 initial claims essentially matched what had been widely expected. That tally was indicative of an improving labor sector since it stayed at a level that is within the Briefing.com "Recovery Zone."

Europe was in close focus yesterday, too. Participants were generally surprised at the lack of accommodative action taken by the European Central Bank, which opted to keep its benchmark lending rate at 1.50%. The Bank of England opted to keep its target rate at 0.50%, but it increased its asset purchase plan to 275 billion pounds from 200 billion pounds. That news initially put pressure on the pound, but it eventually rallied back and even finished the week on a positive note.

Tuesday and Wednesday saw stocks climb sharply for the broad market's best back-to-back performance in more than a month. On Wednesday, participants were given insight into the official September payrolls number by an ADP Employment Change report that showed that private payrolls increased by 91,000. The Briefing.com consensus had called for an increase of 45,000. Although the report doesn't always accurately forecast the exact payrolls number, it is often directionally accurate relative to expectations. The ISM Services Index for September was shrugged off; it slipped to 53.0 from 53.3 in the prior month, but still narrowly exceeded the 52.8 that had been widely expected.

Trade on Tuesday may have kicked off a three-day rally, which took stocks 6% higher, but what's more impressive is that stocks had to crawl out of a hole that had the S&P 500 at a 52-week low and more than 20% below its May high. The rally from those depths came once participants opted, for the time being, to look past the threat that Greece could default on its debt, let alone meet its deficit reduction targets, and the systemic troubles of the broader eurozone.

Such threats had weighed heavily on trade in the first session of the week, overshadowing an improvement in the ISM Manufacturing Index to 51.6 from 50.6 when it had been expected to slip to 50.5. The increase came amid solid growth in new orders, which actually played a part in the first increase in order backlogs since early summer. Weakness on Monday marked an extension of the selling that caused stocks to slide so sharply in the fourth quarter -- the worst quarter for the market in almost three years. That weakness had many seeking the safety of the benchmark 10-year Note. The Note's yield was down to 1.75% at the start of the week, but climbed back 2.00 by week's end. The bond market will be closed on Monday in observance of Columbus Day.DJ30 -20.21 NASDAQ -27.47 NQ100 -0.7% R2K -2.6% SP400 -1.6% SP500 -9.51 NASDAQ Adv/Vol/Dec 620/2.09 bln/1918 NYSE Adv/Vol/Dec 867/1.14 bln/2147

3:30 pm : Several closely tracked commodities succumbed to selling pressure this session. Specifically, oil prices ended pit trade at $82.79 per barrel for a 0.2% loss. For the week, though, they advanced 4.5%. Elsewhere in the energy complex, natural gas prices tumbled 3.1% to $3.49 per MMbtu. The decline fueled a weekly loss of almost 5%.

Precious metals failed to find favor amid a downturn among equities. In turn, gold prices gave up 1.1% to end the day at $1635.50 per ounce, but they managed to muster a 0.8% gain for the week. As for silver, it slid 3.0% to $31.05 per ounce for the session, but still scored a 3.2% gain for the week. DJ30 +90.21 NASDAQ +3.59 SP500 +4.01 NASDAQ Adv/Vol/Dec 715/1.55 bln/1785 NYSE Adv/Vol/Dec 905/715 mln/2080

3:00 pm : Stocks continue to work their way up from midsession lows. The effort has stocks near their best levels of the afternoon.

Another dose of data was just released, but it has had no real impact on trade. The data showed that consumer credit dropped by $9.5 billion during August. It had been broadly expected to climb by $7.0 billion.DJ30 +9.42 NASDAQ -18.40 SP500 -6.04 NASDAQ Adv/Vol/Dec 695/1.45 bln/1800 NYSE Adv/Vol/Dec 830/655 mln/2160

2:30 pm : Stocks have spent the past hour trying to recover from session lows. Although the S&P 500 and Nasdaq are still stuck in the red, the Dow recently poked back into positive territory.

Financials continue to weigh on broad market action. The sector is mired near its session low, contending with a 3% loss. That almost completely offsets its gain from the prior session. DJ30 -1.70 NASDAQ -19.19 SP500 -7.19 NASDAQ Adv/Vol/Dec 615/1.35 bln/1870 NYSE Adv/Vol/Dec 710/600 mln/2280

2:00 pm : Treasuries have rallied off their worst levels of the session following the Fitch downgrades of both Italy and Spain, and the placement of Portugal on 'negative watch.' The 10-yr yield was printing at session highs near 2.12% in the moments ahead of the downgrades, but has since fallen below the 2.05% threshold as buyers rushed into longer dated paper. The long bond was down three full points at its worst levels of the day, but has since recouped more than two-third of its losses. The 30-yr yield is now up just 3 bps on the session at 2.978% after touching a high of 3.087%. After blowing out to a session wide near 185 bps the 2-10-yr spread has tightened to 176 bps.DJ30 -26.87 NASDAQ -25.77 SP500 -9.90 NASDAQ Adv/Vol/Dec 579/1.28 bln/1897 NYSE Adv/Vol/Dec 645/582.7 mln/2367

1:30 pm : The major market averages are off their worst levels of the session, but are still decidedly in the red after Fitch downgraded Italy and Spain and put Portugal on negative watch. The 1.0% drop in the Nasdaq paces the decline while the S&P and Dow hold losses of 0.8% and 0.2% respectively.

Financials are the worst performing sector today, collectively trading down 2.7%. The big financial firms are leading the way lower as Bank of America (BAC 5.96, -0.32) and Goldman Sachs (GS 93.00, -4.93) are both down more than 5.0%. Competitors Citigroup (C 24.96, -1.06) and JP Morgan Chase (JPM 31.04, -1.33) aren't fearing much better as both trade lower by 4.2%. DJ30 -21.65 NASDAQ -25.74 SP500 -8.98 NASDAQ Adv/Vol/Dec 597/1.20 bln/1852 NYSE Adv/Vol/Dec 713/549.2 mln/2298

1:00 pm : Stocks entered Friday with three straight gains that accumulated to a 6% advance, but not even a better-than-expected jobs report has been able to convice participants to extend the rally.

Action this morning in Europe was mixed amid news that analysts at Moody's downgraded the ratings of a dozen banks in the United Kingdom and a handful of others in Portugal. That and a cautious posture ahead of the September payrolls report restrained premarket trade.

However, the tone ahead of the open picked up in response to news that non-farm payrolls for September climbed by 103,000 while private payrolls increased by 137,000. Economists polled by Briefing.com had expected, on average, respective increases of 60,000 and 83,000. Despite the better-than-expected results and some significant upward revisions to prior month totals, a 9.1% headline unemployment rate was what had been widely anticipated.

Buying interest failed to extend into cash market trade, though. Instead, action has been generally choppy and listless, leaving the major equity averages to move in mixed fashion. Early afternoon downgrades of Italy and Portugal by Fitch have dropped the major averages into negative terrtory.

Among the more influential sectors, financials have fallen to a 3.1% loss after rallying to a gain of more than 3% yesterday. Banks led the prior session's advance, but are generally driving downside action today. As for tech, the sector is down 0.9%.

A few blue chips have been performing relatively well, though. That has given the Dow a decent gain on the day. Its advance comes in contrast to the weakness displayed by the Nasdaq, which has been hampered by pressure against biotech plays.

Outside of equities, the dollar has recently turned positive. It is however trading lower against the pound sterling, which has extended its prior session rally by climbing 0.8% to $1.5555 today. After spending most of the day in positive territorty, the euro has slide below the flat line on the Spanish and Italian downgrades.DJ30 -52.75 NASDAQ -33.93 SP500 -12.01 NASDAQ Adv/Vol/Dec 560/1.12 bln/1882 NYSE Adv/Vol/Dec 680/506.5 mln/2314

12:30 pm : Stocks are falling in response to some aggressive selling pressure. The effort comes in the wake of headlines that analysts at Fitch have downgraded the debt of both Italy and Spain.

Those headlines have helped give the greenback a big boost, though. The dollar was lagging a basket of major foreign currencies by about 0.5% only minutes ago. It is now down only fractionally for the day. Most of the move has come against the euro, which was last quoted with a 0.1% loss at $1.342. DJ30 -23.01 NASDAQ -32.80 SP500 -9.09 NASDAQ Adv/Vol/Dec 705/910 mln/1700 NYSE Adv/Vol/Dec 1065/390 mln/1845

12:00 pm : Pressure has picked up in recent trade, causing stocks to move to session lows. Although that made for more substantial losses between the Nasdaq and S&P 500, the Dow was able to stabilize at the flat line. The trio has since worked its way up from recent lows.

The Dow's relative strength today comes amid support from blue chips like Pfizer (PFE 18.68, +0.45), Wal-Mart (WMT 53.54, +0.79), and Home Depot (HD 33.96, +0.58). Shares of HD were actually downgraded a couple of days ago by analysts at Goldman Sachs. DJ30 +52.07 NASDAQ -14.67 SP500 -0.90 NASDAQ Adv/Vol/Dec 630/785 mln/1730 NYSE Adv/Vol/Dec 1025/320 mln/1880

11:30 am : The Nasdaq is significantly underperforming its counterparts. Its weakness comes as traders turn against large-cap names like Apple (AAPL 370.87, -6.50) and eBay (EBAY 31.07, -0.37) come under sharp pressure. Several biotech plays are also under pressure, resulting in a substantial loss for the iShares Nasdaq Biotech Index ETF (IBB 94.67, -1.33).DJ30 +39.73 NASDAQ -20.74 SP500 -1.72 NASDAQ Adv/Vol/Dec 760/660 mln/1575 NYSE Adv/Vol/Dec 1165/270 mln/1705

11:00 am : Stocks recently made an attempt to move higher, but selling pressure has undermined the effort. As such, the major market averages continue to chop along listlessly in mixed fashion.

Financials have fallen deeper into negative territory. In turn, the sector now trades with a loss of 1%, which makes it the worst performing sector this morning. The sector's weakness comes in contrast to its performance in the prior session, when it climbed more than 3% amid leadership from bank stocks. Today, bank stocks have been backed down to a collective loss of 1.4%, as measured by the KBW Bank Index. DJ30 +61.04 NASDAQ -6.28 SP500 +0.98 NASDAQ Adv/Vol/Dec 730/125 mln/1255 NYSE Adv/Vol/Dec 1405/68 mln/1220

10:35 am : Commodities rallied earlier this morning as the dollar fell sharply to new session lows. Precious metals rallied as a result, but pulled back just as quickly. Other commodities such as crude oil held the majority of its gains.

Crude has been in positive territory territory since its earlier morning rally and is back near session highs; now at $83.41, up 1%. Natural gas has been on a steady downtrend and are currently near its session low of $3.50/MMBtu.

Gold moved back into positive territory in recent trade and is currenlty up 0.4% at $1660.10/oz. Silver has been moving higher as well from the unchanged line and is now up 1.4% at $32.45/oz. DJ30 +96.38 NASDAQ +4.81 SP500 +5.10 NASDAQ Adv/Vol/Dec 1114/473 mln/1100 NYSE Adv/Vol/Dec 1703/198 mln/1091

10:00 am : Wholesale inventories for August increased by 0.4%, which isn't quite as much as the 0.5% increase that had been expected, on average, among economists polled by Briefing.com. The data hasn't really done anything to drive action in stocks. As a result, the major equity averages remain mixed.DJ30 +76.52 NASDAQ -5.17 SP500 +0.82 NASDAQ Adv/Vol/Dec 730/125 mln/1255 NYSE Adv/Vol/Dec 1400/65 mln/1220

09:45 am : The positive mood among premarket participants has failed to hold in the opening minutes of trade. In turn, the major equity averages have slipped, leaving them to trade in mixed fashion.

Leadership is lacking in the early going. Consumer staples stocks, collectively up 0.5%, and telecom stocks, up 0.4% as a group, are the best performers, but neither has the capitalization to do much for the broad market. Meanwhile, heavyweights like financials and energy are both down 0.3%, while tech, the largest sector by market weight, remains mired near the neutral line. DJ30 +54.19 NASDAQ -9.32 SP500 +0.27 NASDAQ Vol N/A NYSE Vol N/A

09:15 am : S&P futures vs fair value: +5.70. Nasdaq futures vs fair value: +1.50. Thanks to a better-than-expected jobs report for September, premarket participants have bid higher stock futures, such that a positive start to today's trade appears to be in order. Stocks have already strung together three consecutive advances, which have combined for a 6% climb. As things currently stand, the stock market is on pace for a weekly gain of 3%, which would make for only the third weekly gain in 11 weeks.

09:05 am : S&P futures vs fair value: +5.50. Nasdaq futures vs fair value: +1.00. The CRB Commodity Index is up 0.4% this morning. Most of that move is owed to higher crude oil prices, which are up 1.0% to $83.45 per barrel in the opening minutes of pit trade. That builds on the energy component's back-to-back gains, which combined for a 9% advance. Natural gas prices are under pressure, however. The commodity was last quoted at $3.54 per MMbtu for a 1.7% loss. That makes for a poor follow-up to its 1% hike in the prior session. As for precious metals, gold is essentially flat at $1654 per ounce after a solid 0.7% climb in the prior session. Meanwhile, silver is sporting a 0.4% gain at $32.13 per ounce. Silver had surged 5% in the prior session.

08:35 am : S&P futures vs fair value: +11.50. Nasdaq futures vs fair value: +10.20. A better-than-expected jobs report has spurred stock futures higher, but put pressure on the dollar and Treasuries. The official report for September showed that in September non-farm payrolls climbed by 103,000 and private payrolls increased by 137,000. Increases of 60,000 and 83,000, respectively, had been broadly anticipated. Although the increases exceeded what had been expected and there were some strong upward revisions to prior month totals, there was no surprise to the headline unemployment rate, which stands at 9.1%.

08:00 am : S&P futures vs fair value: -5.90. Nasdaq futures vs fair value: -16.30. The stock market has climbed 6% over the course of the past three sessions, but participants are pushing back a bit this morning. Their caution comes ahead of the always-pivotal non-farm payrolls report, which will be released at the bottom of the hour. The only other data for the day are wholesale trade numbers at 10:00 AM ET and consumer credit figures at 3:00 PM ET.

Limited in number and significance, corporate headlines have given premarket participants few cues for trade ahead of the economic releases.

However, Europe's bourses, regularly regarded as a reflection of sentiment in the region, are mixed at the moment. Their listlessness comes after analysts at Moody's downgraded a bevy of banks and financial institutions in the United Kingdom and Portugal.

Meanwhile, action among currencies has left the euro to trade flat at $1.344, but the sterling pound has extended its prior session rebound so that it is up 0.7% to $1.554 today.

06:57 am : [BRIEFING.COM] S&P futures vs fair value: -5.50. Nasdaq futures vs fair value: -13.80.

06:57 am : Nikkei...8605.62...+83.60...+1.00%. Hang Seng...17707.01...+534.70...+3.10%.

06:57 am : FTSE...5275.46...-15.80...-0.30%. DAX...5635.05...-10.20...-0.20%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage