Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Attachment:

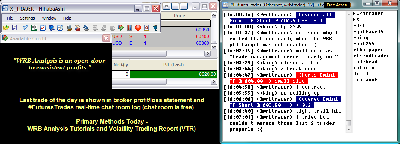

100311-wrbtrader-PnL-Blotter-Profit-8620.png [ 75.23 KiB | Viewed 350 times ]

100311-wrbtrader-PnL-Blotter-Profit-8620.png [ 75.23 KiB | Viewed 350 times ]

click on the above image to view today's trading summary Trade Performance for Today: +86.20 points or

$8620.00 dollars in the Russell 2000 Emini TF ($TF_F) Futures.

Russell 2000 Emini TF Futures - 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE.

S&P 500 Emini ES Futures - 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup.

In addition, all trades were posted real-time in the

free #FuturesTrades chat room. Today's

#FuturesTrades trading chat room logs provides details (e.g. time, price, contract size) about each one of my trades from entry to exit along with price action commentary as the trade traversed...all archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=95&t=1018.

To join our

free chat room...

registration instructions located at a different forum

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=5&t=630Also, posted below are direct links to information about my

trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=5&t=180.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our trade strategies with support

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=144&t=1237 -----------------------------

Market Summaries The below summaries by

Bloomberg,

CNNMoney and

Yahoo! Finance helps me to do a quick review of the fundamentals, FED/ECB/IMF actions or any important global economic events that had an impact on today's price action. Simply, I'm a strong believer that many variables (key market events) causes key changes in supply/demand and volatility that results in swing points and strong continuation price actions. Thus, I pay attention to these key market events from one trade to the next trade to give me the

market context for my

technical analysis. Just as important, these summaries becomes my

archives to allow me to understand what was happening on any given trading day in the past...something I can not get from my broker statements alone.

U.S. Stocks Tumble to 2011 Low on Concern Over Europe Oct. 3 (Bloomberg) -- Bloomberg's Ellen Braitman reports on the performance of the U.S. equity market today. U.S. stocks tumbled, sending the Standard & Poor's 500 Index to a one-year low, as concern over the Greek debt crisis and Bank of America Corp.'s slump offset a rebound in manufacturing and construction spending.

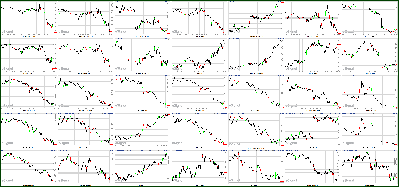

Stocks Tumble Into The Fourth-Quarter Attachment:

100311-Key-Price-Action-Markets.png [ 530.76 KiB | Viewed 290 times ]

100311-Key-Price-Action-Markets.png [ 530.76 KiB | Viewed 290 times ]

click on the above image to view today's price action of key markets By Hibah Yousuf October 3, 2011: 4:32 PM ET

NEW YORK (CNNMoney) -- Stocks just closed out the worst quarter since the 2008 financial crisis, and the swoon is hardly over. With worries about Greece's solvency still in the spotlight, stocks kicked off the fourth quarter with a huge sell-off.

As investors shrugged off a positive U.S. manufacturing report and focused on the worsening debt crisis in Europe, stocks finished at their lowest levels since September 2010.

The Dow Jones industrial average (INDU) tumbled 258 points, or 2.4%. Alcoa (AA, Fortune 500) and Bank of America (BAC, Fortune 500) dragged on the blue chip index, while Wal-Mart (WMT, Fortune 500) was the only Dow component to post a gain.

The S&P 500 (SPX) lost 32 points, or 2.9%, and the Nasdaq Composite (COMP) fell 80 points, or 3.2%.

The selling was broad and deep, with all major sectors firmly in the red.

Shares of American Airlines' parent AMR Corp. (AMR, Fortune 500) sank amid speculation that the airline company could be headed for steeper-than-expected loss this year. The selling spilled over to other airlines, including U.S. Airways (LCC, Fortune 500), United Continental (UAL, Fortune 500), Delta (DAL, Fortune 500), Jetblue (JBLU) and Southwest (LUV, Fortune 500).

Financial stocks including Citigroup (C, Fortune 500), Bank of America, UBS (UBS) and Morgan Stanely (MS, Fortune 500), were also down sharply.

Stocks managed to briefly log some gains earlier Monday following a solid manufacturing report. The Institute for Supply Management index showed that U.S. manufacturing activity expanded in September, surprising economists who were anticipating some weakness.

But the positive impact didn't last long.

Europe's debt problems are the "overriding driver," said Derek Hoyt, portfolio manager at KDV Wealth Management.

* Europe's debt crisis: Complete coverageInvestors' primary focus remains on Greece's attempts to deal with its deficit problems. Greece has slashed spending, reduced wages and raised taxes in an attempt to bring its debt under control.

The debt-ridden nation will miss key deficit targets for this year and next, according to the

draft budget announced by the Greek cabinet late Sunday.

"The economic and political backdrop is one of continued uncertainty as we start the fourth quarter," said Michael Sheldon, chief market strategist at RDM Financial Group. "There doesn't seem to be a near-term solution that will boost confidence among investors."

* Greece: This cannot end wellThere isn't a whole lot of optimism that Greece will pull though. Almost all of the 22 economists surveyed by CNNMoney believe Greece will default on its debt by the end of next year.

As investors mull over the gloomy future, the market's fear gauge, the VIX (VIX), spiked almost 5% Monday to 44.97. Any reading above 30 signals investor worry.

A two-day meeting was underway in Luxembourg among the Eurogroup and Economic and Finance Ministers Council. Greece and the expansion of the stability fund are expected to be among the main topics of discussion.

Stocks are coming off an ugly day and an ugly quarter. Stocks were hammered Friday, with all three major stock indexes shaving more than 2%.

The losses capped the biggest quarterly drop for the S&P 500 and the Nasdaq since the fourth quarter of 2008.

* Video - Euro bailout explained ... with beer pintsInvestors have been all consumed by the debt crisis in Europe and the outlook for global economic growth. The Federal Reserve and the International Monetary Fund have both warned of increasing risks to the global economic recovery.

World markets: European stocks closed sharply lower. Britain's FTSE 100 (UKX) fell 1%, the DAX (DAX) in Germany tumbled 2.2% and France's CAC 40 (CAC40) dropped 1.9%.

Asian markets also ended lower. The Hang Seng (HSI) in Hong Kong plunged 4.4%, while Japan's Nikkei (N225) shed 1.8%. Shanghai (SHCOMP) is closed this week for holiday.

Economy: A report from the Commerce Department showed that construction spending jumped 1.4% in August, after falling 1.3% the prior month. Economists were expecting construction spending to slip 0.5% during the month.

Major auto manufacturers reported auto sales for September throughout the day.

GM (GM, Fortune 500) said sales rose 19.8% during the month, above analyst expectations. Sales at Ford (F, Fortune 500) edged up 9%, and Chrysler Group said sales jumped 27%.

* Video - Yahoo's brighter futureCompanies: Yahoo (YHOO, Fortune 500) was a big winner on both the S&P 500 and Nasdaq, after the struggling online media firm announced a content alliance with ABC News, owned by Disney (DIS, Fortune 500). On Friday, Alibaba Group CEO Jack Ma said that his Chinese Internet conglomerate would be "interested" in buying all of Yahoo.

Shares of Eastman Kodak (EK, Fortune 500) surged more than 70% Monday, after plunging almost 60% Friday. Rumors swirled that the camera maker had hired a law firm for advice on a major restructuring or bankruptcy filing. The company later denied that it is planning bankruptcy moves.

Apple's new CEO, Tim Cook, will take the stage at the Town Hall auditorium on Apple's (AAPL, Fortune 500) Cupertino, Calif., campus Tuesday to unveil the new iteration of the iPhone. Rumors are swirling over whether there will be one new iPhone or two.

* Junk bonds get crushed in market chaosBonds: The price on the benchmark 10-year U.S. Treasury edged up, pushing the yield down to 1.75% from 1.92% late Friday. Earlier, the 10-year yield dipped to a record low of 1.67%.

Currencies and commodities: The dollar rallied against the euro and the British pound, but lost ground against the Japanese yen.

Oil for November delivery lost $1.59 to settle at $77.61 a barrel.

Gold futures for December delivery rose $35.40 to settle at $1,657.70 an ounce.

Market Update

Market Update 4:30 pm : The first session of the fourth quarter saw plenty of selling pressure. The effort culminated in a sharp loss for stocks, which settled at new 52-week lows.

Stocks just booked their worst quarter in almost three years, but sellers aren't yet ready to let up. As such, action today opened in negative territory. Participants continued to take their cues from Europe, where Greece admitted that it does not expect to hit a deficit target and the eurozone's PMI Manufacturing Index for September slipped. Between Germany, France, and the United Kingdom, only the UK experienced an increase in its monthly Manufacturing PMI.

The major averages managed to lure some buyers into the fold with help from a dose of upbeat data. Specifically, the ISM Manufacturing Index for September improved to 51.6 from 50.6 when it was widely expected to slip to 50.5. Construction spending swung from a 1.3% decline in July to a 1.4% increase in August, contrasting with the consensus call for a 0.5% decline.

Still, stocks struggled to sustain their midmorning move into positive territory. Once stocks faltered, the broad market was never able to return to higher ground. The struggle invited additional selling pressure, which prompted a steady descent. Bleeding was broad, but financials suffered the worst loss of any major sector by falling 4.5%.

Airlines experienced a dramatic drop, led lower by AMR (AMR 1.98, -0.98), which was caught up in rumors about bankruptcy. The company stated, though, that it is not seeking a prepackaged bankruptcy.

Given such aggressive selling pressure this session, the S&P 500 broke below the 1100 line and settled there for the first time in little more than a year. Both the Dow and Nasdaq also booked 52-week closing lows, but neither breached their one-year intraday lows.

Amid such weakness, many participants sought safety. In turn, the dollar advanced 1.1% against a basket of major foreign currencies and the benchmark 10-year Note climbed about a point and a half so that its yield tumbled to 1.75%. Gold prices advanced more than 2% to almost $1758 per ounce.

Advancing Sectors: (None)

Declining Sectors: Consumer Staples -1.5%, Telecom -1.8%, Utilities -2.3%, Tech -2.3%, Materials -2.6%, Consumer Discretionary -2.9%, Industrials -3.0%, Health Care -3.2%, Energy -3.3%, Financials -4.5%DJ30 -258.08 NASDAQ -79.57 NQ100 -2.5% R2K -5.4% SP400 -4.6% SP500 -32.19 NASDAQ Adv/Vol/Dec 209/1.71 bln/2352 NYSE Adv/Vol/Dec 294/1.39 bln/2789

3:30 pm : Concerns about the euro zone were once again the focus in commodities. Those concerns led to a flight to safety in the precious metals. Gold futures did most of their rallying in the overnight session. Throughout pit trade, prices moved sideways. Gold closed with gains of 2.2% at $1657.70 per ounce. Silver futures had a very similar pattern of trade, rallying in overnight trade only to spend pit trade range bound. Silver ended with gains of 2.8% at $30.79 per ounce.

Strength in the dollar, coupled with concerns about the euro zone, pressured crude oil prices, which finished lower by 2% at $77.61 per barrel, its lowest settlement in a year. Crude did rally into positive territory at one point, but quickly gave back those gains to trade back toward lows. Natural gas prices shed 2% to finish at $3.62 per MMBTu.DJ30 -211.38 NASDAQ -70.77 SP500 -21.74 NASDAQ Adv/Vol/Dec 267/1.9 bln/2326 NYSE Adv/Vol/Dec 295/898.9 mln/2792

3:00 pm : The stock market is trading just above its 52-week intraday low. Many market participants are watching intently to see if stocks break down as they head into the final hour of the trading day.

Share volume has been relatively strong, suggesting plenty of participation and a sense of conviction among traders.

Such a decidedly negative showing by stocks has caused many to pursue the relative safety of gold, the dollar, and Treasuries. All are up sharply this session. DJ30 -200.25 NASDAQ -67.16 SP500 -25.49 NASDAQ Adv/Vol/Dec 300/1.68 bln/2260 NYSE Adv/Vol/Dec 320/745 mln/2735

2:30 pm : The Amex Airline Index is down more than 6% this session as the likes of Delta Air Lines (DAL 6.78, -0.72) and US Airways (LCC 4.82, -0.68) slide in response to suggestions that AMR (AMR 2.15, -0.81) could face bankruptcy, even though the company has stated publicly that it is not seeking a prepackaged bankruptcy. The action in AMR shares caused several trading halts before circuit breakers were triggered.DJ30 -213.80 NASDAQ -64.22 SP500 -25.13 NASDAQ Adv/Vol/Dec 340/1.50 bln/2205 NYSE Adv/Vol/Dec 385/675 mln/2640

2:00 pm : Stocks continue to trade near session lows. That has the Nasdaq down well in excess of 2%. The Dow and S&P 500 aren't quite in that bad of shape, though. The Nasdaq's relatively outsized drop comes as large-cap tech names like Google (GOOG $498.00, -17.04) and Intel (INTC 20.68, -0.65) slide to losses in excess of 3%.DJ30 -189.43 NASDAQ 58.51 SP500 -22.90 NASDAQ Adv/Vol/Dec 335/1.37 bln/2205 NYSE Adv/Vol/Dec 395/620 mln/2625

1:30 pm : The S&P 500 recently broke beneath its 52-week closing low, which is right around the 1119-1120 region, but stocks managed to attract support before the broad market measure retested its 52-week intraday low of 1101.

In response to the stock market's slide, Treasuries have turned higher. The action now has the benchmark 10-year Note up more than a point so that its yield is back down to 1.80%. DJ30 -155.68 NASDAQ -47.50 SP500 -19.62 NASDAQ Adv/Vol/Dec 445/1.20 bln/2065 NYSE Adv/Vol/Dec 500/535 mln/2500

1:00 pm : A combination of underwhelming eurozone manufacturing data and news that Greece does not expect to hit a deficit target prompted selling pressure this morning. The midmorning release of a better-than-expected ISM Manufacturing Index for September and a surprise increase in construction spending in August brought buyers back into the mix, but the market's corresponding bounce ultimately gave way to renewed selling.

Stocks have since spent the past few hours chopping along in negative territory, and recently setting session lows near critical technical levels around the market's one-year closing low. While widespread weakness has all 10 major sectors in the red, more than half of them are down in excess of 1%.

Materials stocks have done the best job of limiting losses. The sector, although cyclical and therefore often subject to macro concerns, has managed to keep its loss at just 0.4%. Diversified metals and miners are providing support as gold prices climb today by 2% to $1655 per ounce.

The dollar has also staged a nice advance today. Its climb has come mostly against the sterling pound and the euro, both of which were recently quoted with losses of 0.7%. That has the pound probing the lows that it set last week, but the euro is now at its worst level in more than eight months. DJ30 -103.79 NASDAQ -37.27 SP500 -14.12 NASDAQ Adv/Vol/Dec 630/1.05 bln/1835 NYSE Adv/Vol/Dec 670/475 mln/2285

12:30 pm : During the course of the past couple of hours the broad market has made a few attempts to push into positive territory, but each time it has failed. That has left stocks to continue chopping along in negative territory.

Materials plays are showing some strength, however. The sector has managed to eke out an incremental gain with help from gold stocks like Newmont Mining (NEM 64.38, +1.43), which has had some help from a 2% jump in gold prices to $1655 per ounce today. No other major sector is in higher ground. DJ30 -67.50 NASDAQ -20.89 SP500 -9.22 NASDAQ Adv/Vol/Dec 830/935 mln/1615 NYSE Adv/Vol/Dec 935/420 mln/1980

12:00 pm : Europe's bourses closed recently. Action there was bogged down, once more, amid worries about conditions in Greece and the implications related to the country's inability to meet its fiscal targets. Of course, some displeasing manufacturing data for September did nothing to bolster buying interest in the face of such concerns. Among the more widely tracked regional averages, Britain's FTSE fell 1.0%, Germany's DAX dropped 2.3%, and France's CAC closed with a 1.9% loss.

The euro has also faltered today. It was last quoted at $1.328, which makes for a 0.7% loss and a new eight-month low. DJ30 +4.85 NASDAQ -7.79 SP500 -1.54 NASDAQ Adv/Vol/Dec 900/845 mln/1535 NYSE Adv/Vol/Dec 945/375 mln/1955

11:30 am : Despite more weakness this session, shares of Yahoo! (YHOO 13.72, +0.55) are up nicely after the head of Alibaba made mention of his interest in a potential acquisition of YHOO. Other Internet-related plays aren't faring so well -- Google (GOOG 505.65, -9.39) and AOL (AOL 11.72, -0.28) are both down markedly.DJ30 -3.29 NASDAQ -3.18 SP500 -1.20 NASDAQ Adv/Vol/Dec 935/725 mln/1465 NYSE Adv/Vol/Dec 1005/315 mln/1875

11:00 am : Stocks turned positive in response to a dose of better-than-expected data, but sellers have since redoubled their efforts, sending the major equity averages back into the red.

Financials had been a source of positive leadership in the early going, but the sector has been imbued by broad market weakness. In turn, the financial sector is now down to a 0.6% loss. Bank stocks continue to hold up relatively well, though; as a group, banking plays are essentially unchanged, according to the KBW Bank Index. DJ30 -66.45 NASDAQ -16.00 SP500 -7.51 NASDAQ Adv/Vol/Dec 750/565 mln/1600 NYSE Adv/Vol/Dec 820/250 mln/2015

10:35 am : Commodities are mostly lower this morning, while the dollar index is showing modest strength. Energy markets are lower, ag markets are mostly lower and metals are mixed. Overnight, corn futures fell 2.2% and wheat lost 0.7%.

Crude oil futures have been in the red all morning and hit a new session low of $76.85/barrel a few minutes after floor trading began. Crude crossed back over the $78 area in recent trade, but is now down 1.5% at $77.94/barrel. Natural gas is down 0.2% at $3.66/MMBtu.

Gold and silver futures have shown nice gains all morning. Gold has been in a rather tight trading range of ~ $1650-1655 for about the last six hours and is currently up 2.0% at $1654.60. Silver is displaying more volatility this morning and is about 2.7% off its session high. Silver rose as high as $31.43/oz. earlier, but is now up 1.6% at $30.57/oz.DJ30 -5.07 NASDAQ -2.90 SP500 -0.04 NASDAQ Adv/Vol/Dec 920/495 mln/1428 NYSE Adv/Vol/Dec 1109/229 mln/1716

10:05 am : Stocks recently retreated in a retracement of their move up from morning lows, but the major averages are now making another attempt to push higher. The move comes in response to the latest dose of data.

The ISM Manufacturing Index for September came in at 51.6, which is above the 50.5 that had been broadly expected among economists polled by Briefing.com. The latest reading also marks an improvement from the 50.6 that was posted for the prior month.

Separately, construction spending during August reportedly increased by 1.4%, which is far better than the 0.5% decline that had been generally anticipated. It also marks a strong turnaround from the 1.3% downturn suffered in the prior month. DJ30 -7.60 NASDAQ -7.36 SP500 -0.65 NASDAQ Adv/Vol/Dec 635/140 mln/1525 NYSE Adv/Vol/Dec 945/90 mln/1760

09:45 am : Stocks slipped to marked losses in the first few minutes of trade, but a broad bid has helped give the major averages a bit of a lift in recent trade. Financials are leading the move; the sector is already up to a 0.6% gain after it had opened in negative territory.

Energy stocks continue to suffer, however. As a group, energy plays have fallen to a 1.1% loss. Their weakness comes amid a sharp decline in oil prices, which were last quoted with a 2.0% loss at $77.60 per barrel. DJ30 -42.00 NASDAQ -11.95 SP500 -3.76

09:15 am : S&P futures vs fair value: -5.30. Nasdaq futures vs fair value: -16.50. Recent action has taken stock futures farther behind fair value, suggesting that a markedly lower start is in order for the fourth quarter. As was the case last quarter, weakness comes largely in response to fiscal concerns about Greece, which indicated it does not expect to hit a deficit target, and macro conditions in Europe, where a sluggish economy resulted in a lower eurozone Manufacturing PMI for September. To little surprise, Europe's bourses have fallen sharply amid those themes. Many of Asia's major averages also experienced aggressive selling in overnight action. All of it continues to perpetuate negative sentiment. In response to such a dour mood, the dollar has attracted some buyers, giving the greenback a 0.4% lead over a basket of major foreign currencies. Despite the dollar's advance, gold prices have garnered renewed buying interest, which has taken the yellow metal 2.2% higher to $1659 per ounce. Still on the agenda, though, are monthly construction spending numbers and the latest ISM Manufacturing Index, both of which are due at 10:00 AM ET.

09:05 am : S&P futures vs fair value: -7.50. Nasdaq futures vs fair value: -20.80. Commodities are mixed this morning, but the CRB Commodity Index is still down 1.2%. Among the most commonly tracked components, oil prices are down 2.5% to $77.25 per barrel in early pit trade. Meanwhile, natural gas prices are down 0.5% to $3.65 per MMbtu. Precious metals are shining, however. Specifically, gold is boasting a 2.0% gain at $1655 per ounce while silver is sporting a 1.7% gain at $30.60 per ounce.

08:35 am : S&P futures vs fair value: -6.90. Nasdaq futures vs fair value: -20.30. The combination of underwhelming data and news that Greece does not expect to hit a deficit target has weighed heavily on action in Europe. Greece's Athex 20 has fallen to a loss of more than 3%. Meanwhile, Germany's DAX has dropped to a 2.8% loss. Not one of its 30 members has managed to muster a gain. Commerzbank, BMW, and Volkswagen are the three worst performers -- each is down in excess of 5%. Recent data indicate that Germany's PMI Manufacturing Index for September slipped to 50.3 from 50.9 in August. France's CAC has fallen to a 2.3% loss. Weakness is widespread there, but Alcatel-Lucent (ALU), BNP Paribas, and Societe Generale are having the most damaging impact. Pernod Ricard is the only issue that has managed to find higher ground. France's Manufacturing PMI for September fell to 48.2 from 49.1 in the prior month. Selling has also been aggressive in Britain, where the FTSE has tumbled to a 1.6% loss. Burberry Group, Standard Chartered, and Royal Bank of Scotland (RBS) are leading losses. Only a limited number of names, including Randgold Resources, Fresnillo Plc, and Vodafone, have staged gains. Outside of equity market action, analysts at S&P affirmed the AAA-rating on the United Kingdom. Its outlook is also said to be stable. In contrast to neighbors, the United Kingdom experienced an increase in its September Manufacturing PMI, which went to 51.1 from 49.0. As for the broader eurozone, its Manufacturing PMI for September eased to 48.5 from 49.0 in the prior month.

China reported that its September PMI Manufacturing Index improved to 51.2 from 50.9 in the prior month. The report contradicted numbers that had been part of a preliminary look last Friday, but China's Shanghai Composite was closed for trade due to holiday observance. However, Hong Kong's Hang Seng remained opened. It dropped a precipitous 4.4%, which has left it at its lowest level since May 2009. Ping An led the slide as it plunged about 13%. Japan's Nikkei suffered a 1.8% loss. Sumitomo Electric led losses with its 11% slide. Automakers Toyota (TM), Honda Motor (HMC), and Suzuki all logged losses. A September vehicle sales report showed a 1.7% increase, which comes in stark contrast to the 25.5% drop that was endured during the same period one year ago. Obayashi, Shimizu, and Taisei Corp all showed strength in the face of broad market weakness.

08:05 am : S&P futures vs fair value: -0.40. Nasdaq futures vs fair value: -9.50. In the final session of September, stocks suffered another loss, which only added to their poor monthly performance and their worst quarterly showing in almost three years. Yet the same crucial themes that weighed on sentiment in recent months continue into the new quarter. More directly, underwhelming data from Europe and news that Greece will come short of its deficit target for 2011 have taken Europe's bourses down sharply and, by extension, put pressure on domestic stock futures. That said, premarket pressure hasn't been too intense. There are a couple of noteworthy releases on tap for today. Both the latest ISM Manufacturing Index and construction spending numbers are due at 10:00 AM ET. Monthly motor vehicle sales numbers will be released intermittently.

06:54 am : [BRIEFING.COM] S&P futures vs fair value: -1.60. Nasdaq futures vs fair value: -9.50.

06:54 am : Nikkei...8545.48...-154.80...-1.80%. Hang Seng...16822.15...-770.30...-4.40%.

06:54 am : FTSE...5039.25...-89.20...-1.70%. DAX...5379.75...-122.30...-2.20%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage