Trade Journal By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, this public trade journal contains

useful trading tips a few times per week to encourage readers to return for more information and to help ensure I myself don't forget the importance of basic concepts within my own trading plan. Further, there are

market summaries from Youtube Bloomberg, CNNMoney and Yahoo Finance as a quick archive of what happened in the markets on a particular day of trading. Thus, if you're looking for trading tips and market summaries that can improve your trading and/or understanding of what happen on a particular day that involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader.

Today's

#FuturesTrades chat room logs is archived

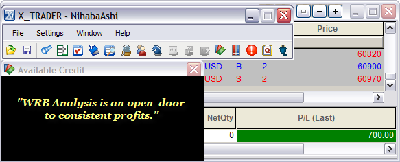

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=77&t=605 click on the below images to view normal sizeAttachment:

082610_wrbtrader_PnL_Blotter_Profit.png [ 32.73 KiB | Viewed 308 times ]

082610_wrbtrader_PnL_Blotter_Profit.png [ 32.73 KiB | Viewed 308 times ]

Trade Performance for Today: +7.00 points or $700 dollars in the ICE Russell 2000 Emini TF ($TF_F) Futures.

1 tick or 0.10 = $10 dollars and to find out more contract information about the Russell 2000 Emini TF...

click here.

Quote:

Today's results are 3 wins : 2 losses (see above #FuturesTrades log). I'm on a semi-vacation for today and tomorrow. Basically that implies I'm only trading the first hour and then spending the rest of the day with my family. First two trades were losers. However, I had a trade management problem (my fault) in the first trade via exiting at -1.30 per contract when I could have minimized it to -0.60 per contract when I realized the bearish price action had stalled and was trying to develop a new support.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about any thing related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtraderIn addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).

WRB Analysis Tutorials

WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=119. However, you must join the TSL Support Forum to access the free study guide. To register...

click here.

Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm Daily Trade Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=120&t=731------------------------------

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries.  U.S. Stocks Fall on Spain Concern, Slowing Manufacturing: Video

U.S. Stocks Fall on Spain Concern, Slowing Manufacturing: VideoAug. 26 (Bloomberg) -- Bloomberg's Courtney Donohoe reports on the performance of the U.S. equity market today. Stocks fell, sending the Dow Jones Industrial Average below 10,000 for the first time in seven weeks, as concern about Spain's fiscal stability and a slowdown in manufacturing wiped out early gains triggered by a drop in jobless claims.

Stocks Slump On Slowdown Fears Attachment:

![spx500-close[1].png](./download/file.php?id=706&t=1&sid=485a67d41d333d7c31c9184ffd33d1f6) spx500-close[1].png [ 18.37 KiB | Viewed 317 times ]

spx500-close[1].png [ 18.37 KiB | Viewed 317 times ]

By Blake Ellis, staff reporter

August 26, 2010: 5:24 PM ET

NEW YORK (CNNMoney.com) -- Stocks slipped Thursday, erasing earlier gains as worries about a sputtering economy overshadowed a better-than-expected report on jobless claims.

The Dow Jones industrial average (INDU) lost 74 points, or 0.7%, the Nasdaq (COMP) composite fell 23 points, or 1%, and the S&P 500 (SPX) ticked down 8 points, or 0.8%.

An earlier bounce lost steam as investors turned their focus to the economy, bracing for the latest reading on second-quarter gross domestic product due early Friday. GDP, the broadest gauge of economic activity, is expected to show the economy grew much less than previously estimated.

"When things are as bad as they are, any news like [today's] jobs data showing a slight improvement helps," said Gary Webb, CEO at Webb Financial Group. "But we're still in a mess, and I think it's going to continue to be a rocky road for the market until we see some gradual momentum."

The three major indexes finished higher Wednesday after spending most of the session in the red following an unexpected plunge in new home sales.

Economic gloom continued to hang over investors Thursday, with losers outnumbering winners by nearly two-to-one on both the New York Stock Exchange and the Nasdaq. Declines were broad based, with big names like Intel (INTC, Fortune 500) losing more than 1%, while winners included Boeing (BA, Fortune 500) and First Solar (FSLR).

Economy slowing to a crawl -- or a halt?

Economy: The Labor Department said the number of people filing for first-time unemployment insurance eased to 473,000 last week, which was lower than forecast.

But the weekly jobless claims report wasn't enough to calm jittery investors, especially with a closely-watched GDP reading on tap Friday. Economists expect the government to revise second-quarter GDP to 1.4%, a significant slowdown from the previous reading of 2.4%.

"We're pretty much just waiting for the GDP number at this point, and everybody is anticipating a poor number," said Ron Kiddoo, CIO at Cozad Asset Management. "If it comes in as expected, we may not see much movement since we seem to already be pricing that in, but if you have a number below 1%, the market could get really ugly."

Companies: PC-maker Dell (DELL, Fortune 500) said data-storage company 3PAR has accepted its $1.6 billion takeover bid, sending shares of 3PAR (PAR) down nearly 3% in regular trading. But after the market close, rival HP said it has sweetened its bid, topping Dell's earlier offer.

Shares of Toyota (TOYOF) fell more than 1% after the automaker said it will recall more than 1 million Corolla and Corolla Matrix vehicles due to engine problems.

The Federal Aviation Administration proposed a $24 million fine against American Airlines. The airline said it will challenge the civil penalty, which would be the largest fine in FAA's history. Shares of AMR Corp. (AMR, Fortune 500), which owns American Airlines, fell nearly 1%.

0:00 /1:03Gold shines on Wall Street

World markets: European shares rallied. The CAC 40 in France ended 0.7% higher, Britain's FTSE 100 climbed 0.9% and the DAX in Germany added 0.2%.

Asian markets ended mixed. Japan's benchmark Nikkei index increased 0.7%, and the Shanghai Composite edged up 0.3%. The Hang Seng in Hong Kong lost 0.1%.

Currencies and commodities: The dollar fell against the euro, the British pound and the Japanese yen.

Oil futures for October delivery rose 84 cents to settle at $73.36 a barrel. Gold for December delivery fell $3.60, settling at $1,237.70 an ounce.

Bonds: The yield on the 10-year Treasury note slipped to 2.50% from 2.54% late Wednesday.

Yahoo! Finance

Yahoo! Finance 4:30 pm : Technical resistance and a lack of leadership led stocks to roll over in the face of a better-than-expected weekly jobless claims report, but near-term support helped keep the averages from closing at their session lows.

Initial jobless claims for the week ended August 21 totaled 473,000, which is less than the 485,000 claims that had been widely expected. It was also down from the prior week's nine-month high of a half million. As for continuing claims, they eased to 4.46 million from 4.52 million in the prior week.

Given that the jobs report wasn't as ugly as some had feared, stocks were able to open higher and build on the prior session's advance. It didn't take long for the move to run into resistance, though. Once the S&P 500 came into contact with 1060, which marked a 50% retracement of the slide that spanned this week's high to this week's low, stocks stalled.

Following a couple of hours of muddled, listless trade, stocks rolled over. The slide stopped when the S&P 500 found support at 1045, which acted as a spring ahead of the close. However, sellers redoubled their efforts so that stocks finished with their fifth loss in six sessions. The final drop also offset the prior session's gain and left stocks to settle at a new monthly low.

Banking stocks failed to free themselves from broader market weakness, even though the KBW Bank Index had been up nearly 2% at its session high. It inevitably reversed to log a 0.7% loss, or its sixth consecutive slide. The KBW is now down 11% month-to-date.

Metals plays managed to put together solid gains, though. Specifically, shares of diversified metals and miners advanced 0.6%, while gold stocks gained 1.2%. That helped the materials sector finish with a fractional gain. It was the only sector to settle in higher ground.

Tech was the worst performing sector. It shed 1.1%. Among its members, Dell (DELL 11.75, -0.04) announced that its bid to acquire 3Par (PAR 26.03, -0.73) for $24.30 per share has been accepted. The offer beat out a bid of $24 per share from Hewlett-Packard (HPQ 38.22, -0.02).

Outsized losses among tech issues caused the Nasdaq to underperform the other headline indices. With a 6.6% year-to-date loss, the Nasdaq is also down the most in 2010.

Treasuries had surrendered early gains, but they won them back when the stock market moved lower late in the session. They also reacted positively to results from an auction of 7-year Notes. The auction drew a yield of 1.99%, a bid-to-cover ratio of 2.98, and had an indirect bidder participation rate of 56.7%. Both the bid-to-cover ratio and indirect bidder rate were above recent averages.

The dollar remained in the red for the entire session. Its 0.5% loss was largely due to a stronger euro, which climbed a 0.5% against the dollar. The euro's bounce came amid strong results from Ireland's latest debt offering, which came on the heels of a downgrade of Ireland's sovereign rating.

Advancing Sectors: (None)

Declining Sectors: Tech (-1.1%), Energy (-1.0%), Financials (-0.9%), Health Care (-0.8%), Consumer Staples (-0.7%), Consumer Discretionary (-0.7%), Utilities (-0.5%), Telecom (-0.4%), Industrials (-0.3%)

Unchanged: MaterialsDJ30 -74.25 NASDAQ -22.85 NQ100 -1.2% R2K -0.8% SP400 -0.7% SP500 -8.11 NASDAQ Adv/Vol/Dec 861/1.83 bln/1770 NYSE Adv/Vol/Dec 1064/1.04 bln/1928

3:30 pm : It was a mixed session for commodities, but the CRB Commodity Index managed to end comfortably higher helped by a 1.9% gain in grains and a 1% gain in energy.

Oct crude oil settled higher by 1.2% to $73.36 per barrel, extending its gains to a second straight session. Sept natural gas dropped 1.1% to finish at $3.83 per MMBtu. A larger-than-expected build in inventory data pushed futures to their lowest intraday level in ~11 months. It managed to bounce off those lows to recoup some of its losses.

Dec gold shed 0.2% to close at $1237.60 per ounce while Sept silver ended off 0.4% to $18.98 per ounce. Stronger-than-expected economic data stemmed the flight to safety, for the time being at least. DJ30 -61.91 NASDAQ -18.04 SP500 -6.31 NASDAQ Adv/Vol/Dec 876/1.4 bln/1719 NYSE Adv/Vol/Dec 1135/685.6 mln/1847

3:00 pm : Stocks have extended their recent slide so that all of the prior session's gains have been undone. Though the downside move is gaining momentum, the S&P 500 still has a ways to go before it comes in contact with the prior session's low of about 1040.

Share volume this session is paltry. Only an hour remains before the close and just over 600 million shares have traded hands on the NYSE. DJ30 -87.38 NASDAQ -22.12 SP500 -8.90 NASDAQ Adv/Vol/Dec 841/1.29 bln/1746 NYSE Adv/Vol/Dec 1033/610 mln/1960

2:30 pm : Choppy trade has given way to a bit of a slide. As a result, stocks are now at new session lows.

Though the move lower has been broad based, tech stocks are in the worst shape. The sector is now down 0.9%. Such weakness has caused the tech-rich Nasdaq to lag the other headline indices. Losses are even more pronounced in the Nasdaq 100, which is now down 0.9%.

The recent slip has helped prop up Treasuries, though they are still only up modestly. The dollar remains under moderate pressure, however. DJ30 -56.54 NASDAQ -17.18 SP500 -6.12 NASDAQ Adv/Vol/Dec 960/1.15 bln/1609 NYSE Adv/Vol/Dec 1250/541 mln/1711

2:00 pm : Stocks are testing session lows as weakness spreads. Eight of the 10 major sectors are now in the red, but none of their losses are excessively large or severe. As for this session's gainers, only the industrials (+0.2%) and materials (+0.7%) sectors are in higher ground. DJ30 -36.07 NASDAQ -10.48 SP500 -3.30 NASDAQ Adv/Vol/Dec 1124/1.05 bln/1415 NYSE Adv/Vol/Dec 1461/485 mln/1463

1:30 pm : Stocks continue to chop along. Losses remain modest in scope.

Meanwhile, Treasuries have started to tick higher. Their modest climb comes as stocks lose luster and results from an auction of 7-year Notes hit newswires. The auction drew a yield of 1.99% and a bid-to-cover of 2.98, which is above recent averages. Indirect bidder participation was 56.7%, which is also above that of recent averages. DJ30 -22.71 NASDAQ -6.32 SP500 -1.67 NASDAQ Adv/Vol/Dec 1194/960 mln/1325 NYSE Adv/Vol/Dec 1640/445 mln/1272

1:00 pm : Despite a better -than-expected weekly jobless claims report, stocks have struggled to extend the prior session's advance.

Action has been both choppy and listless since the open, though there was a positive reaction to news that the latest initial jobless claims count came in at 473,000. Initial claims declined from the prior week's half million figure and weren't as high as the 485,000 claims that had been widely expected.

The jobs data helped stocks start the session in higher ground, but the major averages have failed to sustain their opening gains. Stocks have been mired near the neutral line for the past couple of hours.

While broader market action has been lackluster, materials stocks have had a rather solid session. Most of that is owed to metals plays - diversified metals and miners shares are up 1.9% and gold stocks are up 0.9%.

Bank stocks are also up, but their gains have been slashed. Specifically, the KBW Bank Index had been up 1.9% at its session high, but it is now up a much more modest 0.4%. Still, the Index is up after falling for five straight sessions to test its 2010 low yesterday.

Corporate news has been relatively limited. Among the more interesting items, Dell (DELL 11.86, +0.08) has won the bidding battle against Hewlett-Packard (HPQ 38.43, +0.19) to acquire 3Par (PAR 26.11, -0.65) for $24.30 per share.

Meanwhile, apparel and accessories retailer Guess? (GES 33.90, -4.33) posted better-than-expected earnings, but the spread of its beat was narrower than the blowouts posted in past quarters. That has the stock under sharp pressure.

Due at any moment are results from an auction of 7-year Notes. Treasuries had been up ahead of the opening bell, but they pulled back once the session opened. DJ30 -19.15 NASDAQ -7.03 SP500 -1.70 NASDAQ Adv/Vol/Dec 1219/900 mln/1292 NYSE Adv/Vol/Dec 1639/415 mln/1252

12:30 pm : The S&P 500 is stuck at the neutral line as stocks continue to trade listlessly. The lackluster action has lasted for almost a couple of hours.

Commodities are also mixed at the moment. Specifically, oil prices are up 1.3% to $73.50 per barrel, while natural gas prices are down 0.9% to $3.84 per MMBtu following bearish inventory figures. As for precious metals, gold prices are down 0.1% to $1238.20 per ounce and silver prices are up 0.3% to $19.08 per ounce as they continue to trade near two-month highs. DJ30 -10.22 NASDAQ -3.13 SP500 -0.26 NASDAQ Adv/Vol/Dec 1309/819 mln/1191 NYSE Adv/Vol/Dec 1705/372 mln/1158

12:00 pm : Stocks recently dipped to fresh session lows, but they have since recovered. Overall losses remain negligible to slight.

However, apparel and accessories retailer Guess? (GES 33.90, -4.33) is under sharp pressure following its latest quarterly report. The company actually had better-than-expected earnings, but the spread of its results over the consensus was more narrow than the blowout quarters that Guess? has had in the past. DJ30 -12.19 NASDAQ -3.98 SP500 -0.39 NASDAQ Adv/Vol/Dec 1231/739 mln/1228 NYSE Adv/Vol/Dec 1679/344 mln/1200

11:30 am : Stocks recently rolled over. Though there was no headline or news item to account for the downturn, the move came after the Dow had retraced 50% of its bounce off of the prior session's low. Resistance at such key retracement levels has kept a cap on the stock market's advances in recent weeks.

Despite this session's swings and generally choppy action, volatility is flat, as measured by the Volatility Index. The Volatility Index is up more than 20% year-to-date. DJ30 -4.21 NASDAQ -2.55 SP500 -0.82 NASDAQ Adv/Vol/Dec 1312/643 mln/1125 NYSE Adv/Vol/Dec 1805/285 mln/1059

11:00 am : Trade remains choppy as stocks continue to lack any real leaders. Despite that, financials have attracted strong support, such that the sector is now up 0.9%. Regional banks like Fifth Third (FITB 11.32, +0.34) and KeyCorp (KEY 7.46, +0.19) along with diversified banks like Wells Fargo (WFC +23.99, +0.39) underpin the sector's strength. They have also helped drive the KBW Bank Index to a 1.7% gain, which marks its first advance in six sessions and just its third gain in 13 sessions. DJ30 +20.77 NASDAQ +2.89 SP500 +3.76 NASDAQ Adv/Vol/Dec 1387/498 mln/975 NYSE Adv/Vol/Dec 1986/226 mln/827

10:30 am : Weakness in the dollar index this morning is providing mixed results in the commodities space.

September natural gas was in positive territory all session, excluding a brief moment when it dipped in the red, ahead of today's inventory data. Ahead of the data, the energy component was just above the unchanged line. Following the data, which showed a build of 40 bcf versus consensus of 38 bcf, natural gas sold off to new session lows of $3.79 per MMBtu and is currently 1.5% lower at $3.81 per MMBtu. October crude is trading near recently hit session highs of $73.76 per barrel after trading in positive territory so far in today's session. Currently, crude is trading 1.2% higher at $73.38 per barrel.

Precious metals are mixed in current trade after gold fell into negative territory and hit new session lows of $1237.520 per ounce. Currently, the yellow metal is trading just under the flat line at $1239.50 per ounce. September silver has been in positive territory for the vast majority of the last four hours. Silver hit new session highs of $19.17 per ounce around 8:20am ET, about an hour and a half after gold hit its own. Despite weakness in gold this morning, silver is trading 0.4% higher at $19.11 per ounce.DJ30 +9.61 NASDAQ +4.11 SP500 +3.03 NASDAQ Adv/Vol 868/362.0 mln1418 NYSE Adv/Vol/Dec 1982/166.0 mln/774

10:00 am : Stocks recently ran into a sudden flurry of selling pressure, which sent the Dow briefly into the red and dropped both the Nasdaq and the S&P 500 to the neutral line. Stocks have since made a modest bounce back.

The dollar has dropped to a fresh session low. It is now down 0.5% against a basket of major foreign currencies. Meanwhile, the euro is up 0.6% and near the session high that it set amid news of a solid debt auction from Ireland.

Advancing Sectors: Materials (+0.9%), Industrials (+0.7%), Consumer Discretionary (+0.5%), Financials (+0.4%), Tech (+0.3%), Energy (+0.3%), Telecom (+0.2%)

Declining Sectors: Consumer Staples (-0.3%), Health Care (-0.1%), Utilities (-0.1%)DJ30 +11.12 NASDAQ +7.55 SP500 +3.06 NASDAQ Adv/Vol/Dec 1436/214 mln/749 NYSE Adv/Vol/Dec 1895/98 mln/754

09:45 am : Stocks are up with modest gains in the first few minutes of trade, but action is a bit choppy at the moment.

Materials stocks are out in front of the broader market. The sector has already advanced 0.9%. Most of that move is owed to strength in metals plays like AK Steel (AKS 12.53, +0.19) and Alcoa (AA 10.26, +0.15).

Consumer staples stocks are lagging. The sector's 0.2% loss is largely the result of weakness in giants like Procter & Gamble (PG 59.52, -0.15) and Wal-Mart (WMT 51.21, -0.34). DJ30 +28.30 NASDAQ +8.56 SP500 +4.41 NASDAQ Adv/Vol/Dec 1479/131 mln/596 NYSE Adv/Vol/Dec 2003/64 mln/589

09:15 am : S&P futures vs fair value: +3.60. Nasdaq futures vs fair value: +7.80. A smaller-than-expected initial jobless claims tally has stock futures pointing toward a positive open. Such a start would add to the solid gains of the prior session and put stocks on pace for their first back-to-back advance in a week. Improvement among stock futures has undercut Treasuries, which had been up solidly earlier this morning, though their yields weren't quite back to the annual lows that were set yesterday. Still, participants are expected to take note of results from an auction of 7-year Notes at 1:00 PM ET. The dollar continues to trade with moderate weakness. Its loss stems largely from renewed strength in the British pound and the euro following a successful debt offering from Ireland. Europe's major bourses are also up solidly and near session highs. Overnight action in Asia was rather mixed, however.

09:05 am : S&P futures vs fair value: +4.60. Nasdaq futures vs fair value: +9.30. Futures for the S&P 500 continue to trade with a healthy lead over fair value. Europe's bourses are still up nicely, too. In Germany, the DAX is up 0.7%. It is currently led by Man SE and Volkswagen. Deutsche Telekom and Fresenius SE are causing a drag, though. In France, the CAC has ascended to a 1.0% gain. It is currently led by L'Oreal and Credit Agricole, both of which posted a solid report for the latest fiscal quarter. Britain's FTSE is up 1.0% at the moment. Advancing issues, which are led by BP Plc (BP), Standard Charter, and Barclays (BCS), currently outnumber declining issues, such as Diageo Plc (DEO), by 4-to-1. The British pound is also strong. It has bounced to a 0.4% gain against the greenback. Meanwhile, the euro has eased back to trade with a 0.2% gain against the dollar. It had been up 0.7% amid news that Ireland saw strong demand for a debt offering following yesterday's news that its sovereign debt rating was trimmed to AA- from AA by Standard & Poor's.

In Asia, the Shanghai Composite gained 0.3%. Individual leaders featured banking issues like Industrial & Commercial Bank and Bank of China. In contrast, insurers like China Life and China Pacific were weak. In turn, financials fell 0.2%, collectively. They were the only sector to log a loss. A 1.0% gain made health care the strongest sector. It was led by pharmaceutical plays like Shanghai Fosun. Hong Kong's Hang Seng slipped 0.1% for the second straight session. Industrials were a drag as they dropped 1.0%. Tech stocks offset some of their weakness with a 1.3% advance. Japan's Nikkei climbed 0.7%. Softbank and Kyocera (KYO) were primary leaders. Honda Motor (HMC) was also strong as the yen moderated overnight. The yen has since climbed back toward the flat line.

08:35 am : S&P futures vs fair value: +6.10. Nasdaq futures vs fair value: +10.80. Stock futures have spiked with the release of the latest weekly jobless claims tally. Initial jobless claims for the week ended August 21 totaled 473,000, which is down 31,000 week-over-week and less than the 485,000 claims that had been expected, on average, by a sample of economists polled by Briefing.com. Continuing claims came in at 4.46 million, which is down from the prior week's upwardly revised total of 4.52 million.

08:00 am : S&P futures vs fair value: +0.50. Nasdaq futures vs fair value: -0.30. The prior session's late squeeze helped stocks snap a four-session losing streak, but there hasn't been much follow through as premarket participants await the latest weekly jobless claims count (8:30 AM ET). A sample of economists polled by Briefing.com expects, on average, initial claims of 485,000. That follows last week's initial claims count of a half million, which marked a nine-month high. Outside of claims, results from an auction of 7-year Notes are due this afternoon (1:00 PM ET). The dollar is currently under moderate pressure as the euro advances. European stocks are also up. The tone of trade has been helped by a successful debt offering from Ireland, which recently had its sovereign rating lowered to AA- from AA. As for Asia, action was more mixed. The Japanese yen moderated overnight, but its now back near 84.5 yen per dollar.

06:42 am : S&P futures vs fair value: +3.50. Nasdaq futures vs fair value: +5.50.

06:42 am : Nikkei...8906.48...+61.10...+0.70%. Hang Seng...20612.06...-22.90...-0.10%.

06:42 am : FTSE...5143.93...+34.50...+0.70%. DAX...5922.09...+22.60...+0.40%.

Special thanks to Bloomberg, CNNMoney and Yahoo! Finance for their market summaries. Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader and http://stocktwits.com/wrbtrader Phone: +1.708.572.4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage