Written By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=72&t=459.

Quote:

Today's results are 3 wins : 0 loss. The market moved strongly out of the gate although it actually started around 9am est. Simply, not many trade signals when such occurs except for chasing via intuition (market experience) that the price action will continue the direction. Also, I missed most of the afternoon trading session. The key WRB S/R Zone was via the 2min chart from 0940am - 0942am est...it setup nicely the white hammer line on high volatility around 1002am est during the release of the 10am est economic reports.

Trading Tip: Multiple hammer lines or long shadow dojis in the same price area are forming a support or resistance area.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader

In addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

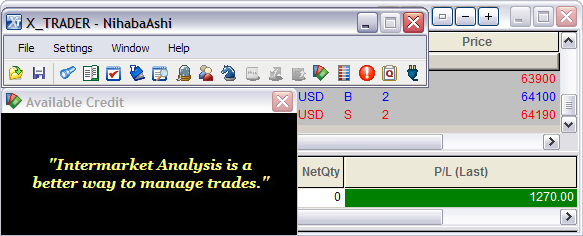

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

+12.70 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

030110_wrbtrader_PnLBlotterProfit.png [ 32.57 KiB | Viewed 1743 times ]

030110_wrbtrader_PnLBlotterProfit.png [ 32.57 KiB | Viewed 1743 times ]

------------------------------

Nasdaq, S&P Turn Positive For 2010By Alexandra Twin and Blake Ellis, staff writers

March 1, 2010: 6:28 PM ET

NEW YORK (CNNMoney.com) -- Stocks jumped Monday, with the Nasdaq and S&P 500 pushing back into positive territory for the year, as investors welcomed AIG's $35 billion asset sale and a pair of mergers in the pharmaceutical sector.

Signs that a Greek bailout package is in the works also came into play.

The Dow Jones industrial average (INDU) gained about 79 points, or 0.8%. The S&P 500 index (SPX) added 11 points, or 1%, and the Nasdaq composite (COMP) jumped 35 points, or 1.6%.

Both the S&P 500 and the Nasdaq ended in positive territory for the year for the first time in over a month.

Stocks rallied Monday, the first day of March, as investors dug back in after last week's retreat. Stocks have been choppy and volatile this year in the aftermath of 2009's big rally.

Stocks jumped last year after trillions of dollars in fiscal and monetary stimulus were injected into the financial system. But optimism about a 2010 economic recovery also fueled the advance.

However, mixed signals about the economy this year have given investors pause as they look for clearer indications that a recovery is not only in place, but can take on a life of its own once the government stimulus fades out.

Concerns that Greece's debt crisis could spread to the rest of Europe and that China is seeking to pull back its expansion all dragged on stocks earlier in the year. But stocks have risen in two of the last three weeks.

"There are a few positives today, with some of the deal news, but there's still uncertainty about the economy," said Gary Webb, CEO at Webb Financial Group.

"It's going to be a lot more volatile this year," he said. "We saw a correction through early February and now we're seeing a rebound. I think we're going to continue to see that seesaw effect throughout this year."

February auto and truck sales are due throughout the day Tuesday. Toyota Motor (TM) is expected to take a hit in the aftermath of its recall of millions of vehicles plagued with safety programs.

AIG: AIG said Monday that it was selling its Asian life insurance business to Britain's Prudential PLC in a deal worth $35.5 billion. The deal includes $25 billion in cash, $16 billion of which the company has earmarked to pay back the government and taxpayers.

Troubled AIG (AIG, Fortune 500) has avoided collapse by borrowing about $132 billion from the government since 2008.

On Friday, the company reported a fourth-quarter loss of $8.9 billion, due mostly to costs connected to selling off large stakes in its insurance businesses.

Shares gained 4% Monday.

Deal news: Japanese drugmaker Astellas Pharma made an unsolicited $3.5 billion bid for OSI Pharmaceuticals (OSIP), maker of the blockbuster Tarceva cancer drug. The deal represents a 40% premium over OSI's Friday closing price.

OSI said it would review the offer and that shareholders should make no move as of yet. OSI shares rallied 52% Monday.

Over the weekend, German pharmaceutical company Merck KGaA said it would buy U.S.-based Millipore (MIL) for $7.2 billion. Millipore is a life sciences tools maker. Millipore shares gained 11.1% Monday.

MSCI (MXB) said it would buy risk advisory firm RiskMetrics Group (RISK) in a $1.55 billion cash-and-stock deal. MSCI shares fell 4% while Risk shares gained 13%.

SanDisk (SNDK) jumping 12%, after the flash memory card maker raised its first-quarter sales outlook to between $925 million and $1 billion.

Market breadth was positive. On the New York Stock Exchange, winners topped losers three to one on volume of 967 million shares. On the Nasdaq, advancers beat decliners by more than three to one on volume of 2.46 billion shares.

0:00 /0:54AIG sells a 'crown jewel'

Economy: A busy day for economic news included readings on manufacturing, construction and income and spending.

The Institute for Supply Management's manufacturing index fell to 56.5 in February from 58.4 in January, surprising economists who thought it would only fall to 57.9. Any reading over 50 signifies expansion in the sector.

Construction spending declined 0.6% in January after falling 1.2% in the previous month, the government reported. The drop was in line with estimates.

Personal income rose 0.1% in January after gaining 0.3% in December. Economists expected income to climb 0.4%. Personal spending jumped 0.5% after rising 0.3% in the previous month. Economists thought spending would increase 0.4%.

Greece: Amid ongoing worries about Greece's ballooning deficit, Olli Rehn, the European Union's financial affairs commissioner, urged the nation to make more budget cuts. Greece has already announced plans to raise the retirement age and freeze wages, but Rehn said such moves are not enough.

Greece's finance minister, Giorgos Papaconstantinou, said the government would do "whatever it takes" to cut the deficit.

World Markets: In overseas trading, European markets rallied, with the London FTSE rising 1%, the French CAC 40 gaining 1.6% and the German DAX advancing 2%. Asian markets ended higher.

The dollar and commodities: The dollar gained versus the euro, the yen and the U.K. pound.

U.S. light crude oil for April delivery fell 96 cents to $79.66 a barrel on the New York Mercantile Exchange.

COMEX gold for April delivery eased 60 cents to settle at $1,118.30 per ounce.

Bonds: Treasury prices fell, raising the yield on the 10-year note to 3.61% from 3.59%. Treasury prices and yields move in opposite directions.

Yahoo! Finance

Yahoo! Finance 4:30 pm : Stocks started March with a strong, broad-based push to fresh one-month highs in the face of a stronger dollar, but equities ran into resistance as the S&P 500 attempted to turn positive for the year.

All three major indices spent the entire session in higher ground with solid gains. The Nasdaq Composite was the strongest of the headline indices, thanks to leadership from large-cap tech. SanDisk (SNDK 32.63, +3.48) was one of the best performers in the Nasdaq after the company's improved outlook during its investor conference this past Friday won it the favor of several Wall Street firms.

Though gains in the S&P 500 were strong, the broad market index struggled to move above the 1115 line, which separates year-to-date positive from year-to-date negative. The line was balanced for the entire afternoon, but stocks made a last minute spurt so that the broad market index was able to eke out a fractional year-to-date gain and settle back above its 50-day moving average.

Materials stocks were among the better performers in the broader market. The sector settled with a 1.6% gain as diversified metals and miners plays climbed amid copper supply concerns that stemmed from the recent earthquake in copper-rich Chile.

Such sentiment helped materials stocks shrug off a stronger dollar, which advanced roughly 0.5% against a basket of competing currencies. Though that was a strong gain for the greenback, it only half of what the dollar had traded with while at its session high. The greenback's gain came as the euro and British pound fell out of favor amid concerns related to deficits in Europe.

Despite concerns about the fiscal health of Europe's economies, strong manufacturing data out of the euro zone helped the major European bourses put together solid gains of their own in the week's first session. Those gains contributed to a 1.0% advance in the Dow Jones World Index.

U.S. economic data was met with little response as January personal income increased 0.1%, which was below the 0.4% increase that had been expected. Spending for January increased 0.5%, which was a bit sharper than the 0.4% increase that many had come to expect. Core personal consumption expenditures were flat from the prior month, but that was in-line with economists' consensus call.

The ISM Manufacturing Index for February came in at 56.5, which was below both the 57.9 that had been widely expected and below the 58.4 that was posted for the prior month.

Meanwhile, construction spending in January decreased 0.6% month-over-month, as expected.

There was a fair amount of news related to mergers and acquisitions this morning. German drug and chemical company Merck KGaA will acquire Millipore (MIL 104.90, +10.49) for $7.2 billion. Other biotech and life science stocks traded higher in sympathy to help the health care sector climb to a 1.0% gain.

European insurer Prudential PLC (PUK 16.13, -2.37) agreed to buy a pan-Asia insurance business from AIG (AIG 25.78, +1.01) for $35.5 billion in cash and stock. Though support for AIG faded into the close, it was still a leader in the financial sector which finished the session with a 0.4% gain after it failed to follow the broader market higher.

Advancing Sectors: Materials (+1.6%), Consumer Discretionary (+1.6%), Tech (+1.5%), Utilities (+1.3%), Health Care (+1.0%), Industrials (+1.0%), Energy (+1.0%), Consumer Staples (+0.7%), Telecom (+0.6%), Financials (+0.4%)

Declining Sectors: (None)DJ30 +78.53 NASDAQ +35.31 NQ100 +1.5% R2K +2.2% SP400 +1.7% SP500 +11.22 NASDAQ Adv/Vol/Dec 2022/2.45 bln/684 NYSE Adv/Vol/Dec 2418/967 mln/633

3:30 pm : Commodities put in a weak session, which saw the CRB Commodity Index slide 0.8%. Oil was a primary source of weakness as crude oil contract prices dropped 1.2% to $78.70 per barrel. In contrast with action in recent weeks, oil's slide actually intensified as the dollar pared its gains -- the greenback is currently up 0.5% against competing currencies after it had been up roughly 1% at its session high.

Natural gas prices also came under pressure, which culminated with contract prices 2.6% lower at $4.69 per MMBtu.

Precious metals traded with more moderate losses. Gold closed at $1118.30 per ounce, down fractionally. Silver prices settled 0.3% lower at $16.47 per ounce. DJ30 +73.61 NASDAQ +32.09 SP500 +10.06 NASDAQ Adv/Vol/Dec 1907/2.02 bln/773 NYSE Adv/Vol/Dec 2327/711 mln/700

3:00 pm : The dollar continues to drift downward as the final hour of the session approaches. Though the dollar is up 0.4% against competing currencies, it is still well off of its session high, which saw it trade with an approximate gain of 1%.

Meanwhile, stocks remain near their session highs with broad-based gains. Despite the apparent strength, stocks have been unable to break free from a tight trading range that has spanned just a few points during the course of the past four hours. The challenge facing the stock market is whether it can push into positive territory for the year.

Many participants appear to be waiting to see whether stocks can meet the challenge before commiting to the market. In turn, trading volume has been rather light this session.DJ30 +69.99 NASDAQ +30.70 SP500 +9.83 NASDAQ Adv/Vol/Dec 1897/1.82 bln/774 NYSE Adv/Vol/Dec 2323/642 mln/694

2:30 pm : The S&P 500 recently crossed the 1115 line, which put it into positive territory for the year, but it has since eased back a bit to settle along the line. In turn, gains remain strong and broad based.

With a 1.6% gain, consumer discretionary stocks are up the most at the moment. The sector has been helped by strength among retailers (+1.6%). Spending data for January was largely without surprise, though. According to the latest data, personal spending increased a 0.5% in January and core personal consumption expenditures were flat. DJ30 +74.29 NASDAQ +33.26 SP500 +10.43 NASDAQ Adv/Vol/Dec 1918/1.71 bln/736 NYSE Adv/Vol/Dec 2354/599 mln/659

2:00 pm : The 1115 line continues to keep the S&P 500 from putting together a year-to-date gain. The Dow has a bit further to go since it is still down 0.3% year-to-date, but the Nasdaq has moved to a 0.1% year-to-date gain with this session's advance.

Financials have made their way to an afternoon high after lagging for the first half of the session. The sector is up 0.3%, but that's still shy of its opening level.

Meanwhile, the dollar continues to drift downward, such that it has now seen its gain halved to 0.5%. Despite the greenback's pullback, commodities continue to trade with weakness. Pressure against commodities has the CRB Commodity Index near its session low with a loss of 0.8%. DJ30 +77.17 NASDAQ +33.03 SP500 +10.53 NASDAQ Adv/Vol/Dec 1920/1.56 bln/746 NYSE Adv/Vol/Dec 2383/544 mln/621

1:30 pm : The stock market recently pulled back a few points from session highs, which were set as the S&P 500 poked just above the 1115 line roughly one hour ago and threatened to turn positive for the year. Despite the dip, gains remain strong and broad-based.

The greenback has also moved off of its session highs. In turn, the Dollar Index is now up 0.6% after it had been up roughly 1% in the early going. DJ30 +68.17 NASDAQ +30.79 SP500 +9.34 NASDAQ Adv/Vol/Dec 1853/1.42 mln/763 NYSE Adv/Vol/Dec 2332/505 mln/668

1:00 pm : Despite a stronger dollar, the major equity averages are sharply higher with broad-based gains. However, the stock market's advance has stalled as the S&P 500 struggles to push through the 1115 line.

The dollar had been up some 1% against a basket of foreign currencies in the early going, but it has since pulled back a bit to trade with a 0.7% gain. The greenback has been helped by weakness in the euro and the British pound, which actually hit a multimonth low against the dollar earlier this morning. According to reports, weakness in the European currencies comes largely as a result of deficit concerns in the continent.

Though the greenback's gains have weighed on commodities, which are down a collective 0.4% based on the CRB Commodity Index, materials stocks are up handsomely. More specifically, materials stocks are up 1.1% as diversified metals and miners players climb 1.6% amid concerns that global copper supply will be slowed by the recent earthquake in Chile.

Tech has been a strong leader for the broader market this session, though its influence has been most pronounced in the Nasdaq, which has a solid lead over the other major indices. Tech stocks in the S&P 500 are up 1.2%.

Small-caps and mid-caps are among the best overall performers this session. Their gains have the Russell 2000 and the S&P 400 up 1.9% and up 1.5%, respectively.

Financials have failed to follow the broader market as they trade with a 0.1% loss. Regional banks have been a primary source of weakness; they are down 1.4% as investors take profits after the group booked last week a 3.0% weekly gain, which came in the face of the broader market's modest slide.

Economic data has had little influence on trade this session. Monthly spending and income numbers for January were mixed, while the ISM Manufacturing Index for February was lower than expected and construction spending in January dipped in-line with expectations. DJ30 +61.22 NASDAQ +29.71 SP500 +8.78 NASDAQ Adv/Vol/Dec 1857/1.32 bln/753 NYSE Adv/Vol/Dec 2313/465 mln/658

12:30 pm : Utilities make up one of the best performing sectors this session. They are currently up 1.5%, collectively.

NRG Energy (NRG 22.43, +0.59) and Exelon (EXC 44.63, +1.33) are the two primary leaders in the group's broad-based advance, which has lifted 33 of the sector's 35 members into positive ground.

Edison International (EIX 33.12, +0.49) is among the other strong performers in the energy sector. The company reported ahead of this morning's opening bell better-than-expected earnings. DJ30 +75.96 NASDAQ +31.34 SP500 +10.37 NASDAQ Adv/Vol/Dec 1871/1.21 bln/723 NYSE Adv/Vol/Dec 2376/422 mln/597

12:00 pm : This session's advance has put the stock market up to its best levels in more than one month. The move has also taken the S&P 500 back above its 50-day moving average. However, the benchmark index seems to have run into a bit of resistance at the 1115 line.

Materials stocks have made a recent run to fresh session highs. The sector is now up 1.3% as diversified metals players climb to a 2.0% gain. Metals stocks also fared well in overseas trade as many reacted to speculation that the recent earthquake in Chile will disrupt the supply of copper to the world. DJ30 +75.35 NASDAQ +30.57 SP500 +10.16 NASDAQ Adv/Vol/Dec 1875/1.02 bln/716 NYSE Adv/Vol/Dec 2355/386 mln/583

11:30 am : Stocks recently made their way to fresh session highs, but they have since eased back a bit. Financials continue to lag with a loss of 0.1%, but the rest of the stock market is up with broad-based gains.

This session's advance has almost completely undone the stock market's year-to-date loss, which is only fractional now.

Meanwhile, small-caps and mid-caps have managed to add to their yearly gains. The two stock classes are up a respective 1.8% and 1.3% this session, but up a respective 2.3% and 3.0% year-to-date. DJ30 +82.15 NASDAQ +29.19 SP500 +10.06 NASDAQ Adv/Vol/Dec 1859/944 mln/704 NYSE Adv/Vol/Dec 2347/339 mln/579

11:00 am : The Dollar Index has ascended to a 1.0% gain, but materials stocks and energy stocks haven't really been adversely affected. Instead, both sectors are up 0.7% at the moment.

With a 0.1% loss, financials are laggards, though. The financial sector is the only major sector in negative territory at the moment. Its weakness is largely concentrated around regional banks, which are down 1.5% on the heels of a strong weekly performance that helped put the group up nearly 13% year-to-date.

The tech sector has made its way to a 1.2% gain, which is the best of any major sector. Gains among tech issues have helped the Nasdaq take a sizable lead over its counterparts.DJ30 +69.46 NASDAQ +27.09 SP500 +8.18 NASDAQ Adv/Vol/Dec 1847/750 mln/671 NYSE Adv/Vol/Dec 2255/270 mln/617

10:35 am : The US Dollar Index is trading near its session highs in current activity. However, the energy markets aren't showing much weakness as crude and natural gas are mixed. Even precious metals are not getting hit much with the dollar index trading at highs as gold and silver are currently near the unchanged line.

April crude oil hit session highs of $80.62 per barrel overnight and has only traded in the red for a moment. An hour before the open, the energy component dipped into negative territory to session lows of $79.39 per barrel, and after spiking off those lows, crude is trading 0.3% lower at $79.46 per barrel. April natural gas traded modestly lower all night before finally spiking into positive territory shortly after pit trading began. Natural gas pushed to fresh session highs of $4.869 per MMBtu, but has pulled back modestly and is at $4.835 per MMBtu, up 0.4%.

Precious metals are off overnight highs (Gold $1123.90, Silver $16.77) and are trading near the flat line. Gold is 0.4% lower at $1114.00 per ounce, while silver is 0.3% higher at $16.465 per ounce. DJ30 +52.45 NASDAQ +21.58 SP500 +6.84 NASDAQ Adv/Vol/Dec 1824/575.8 mln/647 NYSE Adv/Vol/Dec 2216/210.6 mln/627

10:05 am : The ISM Manufacturing Index for February came in at 56.5, which is below the 57.9 that had been widely expected and below the 58.4 that was posted for the prior month.

Meanwhile, construction spending in January decreased 0.6% month-over-month, as expected. However, the decline marked a slowdown from the 1.2% monthly decline that had been posted in December.

Stocks dropped in knee-jerk fashion in response to the numbers, but they have since recovered to trade near their morning highs. Overall gains are broad-based with all 10 major sectors in the S&P 500 in positive territory.

Early movers: Trading up -- OSIP +49.8%, CIIC +24.7%, RISK +13%, BIOD +12.8%, HALO +12.3%, WWIN +11.6%, AIG +11.3%, MIL +10.9%, CADX +7.8%; Trading down -- GAME -14.8%, PUK -13.4%, MG -9.8%, SNDA -9%, PWRD -7.3%, HBC -7.2%, LYG -6.8%, TASR -6.4%

Advancing Sectors: Utilities (+0.9%), Industrials (+0.9%), Health Care (+0.9%), Energy (+0.7%), Tech (+0.7%), Consumer Discretionary (+0.6%), Consumer Staples (+0.4%), Telecom (+0.4%), Financials (+0.2%), Materials (+0.2%)

Declining Sectors: (None)DJ30 +54.49 NASDAQ +20.34 SP500 +7.06 NASDAQ Adv/Vol/Dec 1825/413 mln/571 NYSE Adv/Vol/Dec 2233/149 mln/578

09:35 am : Stocks have started the first session of March in higher ground, but the opening advance has been a bit hampered by strength in the dollar. The dollar is currently up a considerable 0.7% against a basket of foreign currencies, but its gains have been most notable against the euro and the British pound, which have been pressured by deficit concerns, according to reports. More mixed reports regarding the prospects of a resolution for Greece also seem to have helped prop up the greenback.

Economic data, which featured a mixed bag of monthly spending and income numbers for January, has done little to disrupt the morning mood. However, the ISM Manufacturing Index for February and construction spending figures for January are due at the top of the hour.

Recent data out of Europe showed strong manufacturing output, which has helped the continent's bourses put together strong gains. Such gains have helped to keep the mood positive among this morning's participants. DJ30 +46.33 NASDAQ +14.58 SP500 +6.00 NASDAQ Adv/Vol/Dec 1662/112 mln/563 NYSE Adv/Vol/Dec 2010/55 mln/526

09:05 am : S&P futures vs fair value: +4.70. Nasdaq futures vs fair value: +5.80. U.S. stock futures remain off of their morning highs, but they continue to point to a firm start for the session. Meanwhile, Germany's DAX is up 1.3% amid broad-based support. Bayer and Siemens (SI) are currently strong leaders, while Deutsche Post, Commerzbank, and Deutsche Lufthansa are the only three names in the 30-member bourse to trade with losses. Meanwhile, France's CAC is up 0.9%. Sanofi-Aventis (SNY) is a primarly leader at the moment, while AXA (AXA) is at the other end of the spectrum with a considerable loss. In Britain, the FTSE is up 0.5% amid support from natural resource plays, but hampered by losses among banking issues. As such, BP PLC (BP), Royal Dutche Shell (RDS.A), Rio Tinto (RTP), and BHP Billiton (BHP) presently top the FTSE's list of leading movers. Strength among the natural resource plays comes even though the dollar has gained considerable ground against the British pound this morning. Banking issues are weak in the wake of the latest results from HSBC (HBC), which reported a lower-than-expected income number. In economic news, euro zone manufacturing output hit a 30-month high in February as the manufacturing purchasing managers' index climbed more-than-expected to 54.2. In Asia, Japan's Nikkei advanced 0.5% as metal-related shares climbed as copper prices rallied to five-week highs amid supply worries that stemmed from the massive earthquake that hit copper-rich Chile. However, Toyota Motor (TM) slipped amid news that a U.S. congressional panel has found evidence Toyota routinely withheld company records it should have turned over in court and settled personal injury cases to avoid revealing key engineering data. Meanwhile, Hong Kong's Hang Seng climbed 2.2%, which put it at a five-week high. Financial plays were primary leaders amid hope that Beijing will put off tighter monetary policy. China Construction Bank was also helped by word that the bank has no plans to raise fresh capital. HSBC advanced ahead of its latest quarterly results. Metals plays were also strong. In mainland China, the Shanghai Composite advanced 1.2% to a five-week closing high. The advance came in the face of a sharper-than-expected slowdown by the February PMI to 52.0. However, the survey results led some to believe that a relatively loose monetary policy would be reaffirmed at a parliament meeting.

08:35 am : S&P futures vs fair value: +3.30. Nasdaq futures vs fair value: +4.50. Stock futures continue to chop along with modest gains in the wake of January personal income and spending numbers, which mark the first dose of actual data for the first quarter of 2010. Income for the month reportedly increased 0.1%, which is below the 0.4% increase that had been expected and below the downwardly revised 0.3% increase that was reported for the prior month. Spending for January increased 0.5%, which is a bit sharper than the 0.4% increase that many had come to expect. The latest monthly spending figure also marks a pickup from the upwardly revised 0.3% increase of the prior month. Core personal consumption expenditures for January were flat from the prior month, but that was in-line with economists' consensus call.

08:05 am : S&P futures vs fair value: +1.60. Nasdaq futures vs fair value: +5.20. Stock futures are up a bit, but they have eased back a bit from their morning highs as the greenback gains ground against competing currencies. Overseas markets have managed to put together decent gains, which have provided support to futures from a sentimental standpoint. Some merger and acquisition activity has helped, too. Specifically, Merck KGaA has entered into a definitive agreement to acquire Millipore (MIL) for $107 per share in cash; that's a premium of roughly 13% from MIL's closing price this past Friday. Meanwhile, AIG (AIG) will sell a pan-Asian life insurance business to Prudential PLC (PUK) for some $35.5 billion in cash and stock. The latest monthly personal income and spending figures are due at the bottom of the hour, followed by the latest ISM Manufacturing Index and monthly construction spending numbers at 10:00 AM ET.

07:00 am : S&P futures vs fair value: +1.60. Nasdaq futures vs fair value: +3.50.

07:00 am : Nikkei...10172.06...+46.00...+0.50%. Hang Seng...21056.93...+448.20...+2.20%.

07:00 am : FTSE...5364.34...+9.90...+0.20%. DAX...5644.52...+45.50...+0.80%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage