Written By M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

Trade journals are crucial in preventing us traders from becoming complacent or content with our trading plan or the markets because without having the ability to review archives of past trading days in a forever changing market...we won't know it's time to adapt when change occurs in the markets because broker statements alone doesn't help us keep that

edge in comparison to a trade journal. In addition, although this journal contains advertisements involving my trade methods, it does contain

useful trading tips a few times per week. Thus, if you're looking for trading tips that can improve your trading and understand that profitable trading involves more than just entry signals...consistently read this trade journal and the #FuturesTrades chat room logs where I post my trades in real-time from entry to exit (see link below) via my IRC user name

wrbtrader that's the same as my user name on twitter.

Today's #FuturesTrades chat room logs is archived

@ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=71&t=448.

Quote:

Today's results are 11 wins : 5 losses. A lot of distractions today at home along with an unexpected guest that prevented me from trading between 1521pm - 1615pm est...a price area that would have given me three more trade opportunities along with a Long signal @ 1536pm via the

Volatility Trading Report (VTR). Regardless, a good controlled trading day along with good trading reach in which I was able to reach my profit goal each trading day of this week.

Trading Tip: Only add to a profitable trade if you get another trade signal prior to the profit target being reach. However, manage the original entry and the add as two independent trades. Thus, for example, each will have different stop/loss protections.

FYI - You can ask me questions here at the forum or you can tweet me on twitter about anything related to today's trading or related to your own trading.

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader

In addition, posted below are direct links about my trade methodology or trading approach that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body analysis).http://www.thestrategylab.com/WRBAnalysisTutorials.htmhttp://www.thestrategylab.com/TradeStrategies.htm Also, if you're interested in having

free access to one of my profitable trade strategies along with earning extra income with little effort...join my referral program @

http://www.thestrategylab.com/ReferralProgram.htm My Trading Performance:

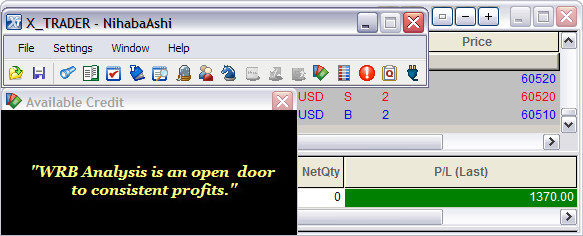

+13.70 points in the ICE Russell 2000 Emini TF ($TF_F) Futures

Attachment:

021210_wrbtrader_PnLBlotterProfit.png [ 32.44 KiB | Viewed 1607 times ]

021210_wrbtrader_PnLBlotterProfit.png [ 32.44 KiB | Viewed 1607 times ]

------------------------------

Dow Slides On China Worries Dow slides on China worries

By Alexandra Twin, senior writer

February 12, 2010: 7:29 PM ET

NEW YORK (CNNMoney.com) -- The Dow tumbled Friday after China's bid to limit bank loans and slower-than-expected European growth raised worries about the global recovery. But a late-session run up in select techs gave the Nasdaq a boost.

A rallying greenback dragged on dollar-traded commodities, as well as companies that do a lot of business overseas and benefit from a weaker dollar.

The Dow Jones industrial average (INDU) lost 45 points, or 0.4%. The Dow had dropped as much as 160 points in the morning before recovering.

The S&P 500 index (SPX) slid 3 points, or 0.3%. The Nasdaq composite (COMP) rose 6 points, or 0.3%, thanks to gains in chip makers and other technology shares.

Stocks had slumped heavily in the early morning, but managed to cut losses in the afternoon thanks to some gains in the tech sector.

Investors may have also been reluctant to sell too aggressively going into a long holiday weekend. All financial markets are closed Monday for Presidents Day.

"Between China and continued concerns about what the EU is going to do about Greece, there are a lot of negatives out there," said Tom Schrader, managing director at Stifel Nicolaus.

He said that after a big run up over the last 12 months, people are looking at the negatives and are concerned about leaving any money on the table.

"We can't seem to get an uptrend going. The selling has been on heavy volume and that makes people nervous," Schrader said.

Stocks surged Thursday after the European Union agreed to help out Greece, but the advance was a rare bright spot in what has been a tumultuous start to 2010.

On the upside, all three major gauges were set to end with a weekly gain, after declining for four weeks.

Tough start to 2010: Wall Street extended 2009's rally through the middle of January, but lost steam soon after.

The Dow, S&P 500 and the Nasdaq have all declined the past four weeks as better-than-expected corporate profit reports have been overshadowed by worries about China slowing its growth, U.S. plans to limit bank trading and European debt issues.

Also in play: the stronger dollar, which has pressured commodities and companies that do a lot of business overseas and therefore benefit from a weaker dollar.

Between rally highs hit Jan. 19 and the lows of last week, the S&P 500 lost over 9%, careening close to the 10% selloff that is the technical definition of a correction. The Dow's high-to-low was just over 7%.

Asia: China told banks to raise reserves for the second time in a month, in an effort to slow lending and contain any inflation threat that could set back the economic recovery.

The government boosted the reserve requirement for financial institutions by a half-percentage point to 16.5% for big lenders and 14.5% for small lenders. Rural lenders will see no change.

China kept its yearly target for bank lending unchanged, suggesting it isn't looking to cut back lending, so much as slow the pace.

Asian stocks rose Friday, with Japan's Nikkei and other indexes ending higher.

0:00 /1:42No EU bailout for Greece

Greece: European Union members meeting in Brussels, Belgium, on Thursday said Greece must do whatever is necessary to cut its huge budget deficit and that the group would be prepared to step in if needed.

In recent weeks, Greece's proposals to save money -- including cutting wages and raising the retirement age -- have prompted a series of worker strikes.

Although Greece's impact is small, the nation's financial problems have sparked fears of a broader debt crisis in Europe with Portugal, Spain, Ireland and Italy among the other euro zone nations seen as having growing debt problems.

U.S. investors have been trying to gauge what kind of impact such a crisis would have on financial institutions as well as the global economic recovery.

Euro zone growth stalls: Meanwhile, a report showed that euro zone GDP growth in the fourth quarter was 0.1%, short of the 0.3% economists were expecting. Problems in Greece and a struggling German economy were among the factors dragging on growth.

European stocks slid Friday, with London's FTSE 100 down 0.4%, the German DAX barely lower and France's CAC 40 down 0.5%.

On the move: The B shares of Warren Buffett's Berkshire Hathaway (BRK.B) were among the most actively-traded on the New York Stock Exchange Friday. The stock was added to the S&P 500 after the close of trading. Managers of funds that mirror the 500-share average had to buy the stock ahead of the inclusion.

Motorola (MOT, Fortune 500) gained 7.5% in heavy NYSE volume after announcing a long-in-the-works decision to split itself into two publicly-traded companies. Motorola is splitting its cell phone and cable set-top box business from its networking gear sales businesses.

The company said late Thursday it will complete the deal in the first quarter of 2011.

Market breadth was positive. On the New York Stock Exchange, winners beat losers eight to seven on volume of 1.43 billion shares. On the Nasdaq, advancers topped decliners three to two on volume of 2.26 billion shares.

Apple, Priceline and six other stocks we love

Economy: In the U.S., January retail sales growth was stronger than expected, according to a Commerce Department report released in the morning.

The report, delayed by snow storms in Washington, showed sales rose 0.5% versus forecasts for a rise of 0.3%, according to Briefing.com estimates. Sales excluding autos rose 0.6% versus forecasts for a jump of 0.5%.

A separate report from the University of Michigan showed that consumer sentiment dipped to 73.7 in early February from 74.4 in late January. Economists thought it would rise to 75.

The dollar and commodities: The dollar rallied versus the euro and against the Japanese yen.

The dollar's strength pressured dollar-traded commodity prices.

U.S. light crude oil for March delivery fell $1.15 to settle at $75.28 a barrel on the New York Mercantile Exchange.

COMEX gold for April delivery fell $4.70 per ounce to settle at $1,090.

Bonds: Treasury prices rose, lowering the yield on the 10-year note to 3.69% from 3.72% late Thursday. Treasury prices and yields move in opposite directions.

Yahoo! Finance

Yahoo! Finance 4:30 pm : Leadership from the tech sector helped stocks trim steep losses that stemmed from a stronger dollar.

The stock market gapped down in the early going to trade with a loss of more than 1% as the Dollar Index climbed to a near 1% gain amid a sharp decline in the euro, which was weakened by a weaker-than-expected fourth quarter eurozone GDP reading. Meanwhile, pledged support for Greece from the International Monetary Fund (IMF) and the European Central Bank failed to support the euro.

Early market participants also had to digest news that China's central bank will hike reserve requirements at banks in order to curtail lending. That announcement comes as a stark reminder that China has switched from efforts to stimulate growth to a mindset of growth management, which has underpinned concerns for the pace of a global economic recovery.

Such macro concerns coupled with a stronger dollar caused participants to look past a stronger-than-expected 0.5% increase in January's advance retail sales figures. Sales less autos increased 0.6%, which was also stronger than expected.

A lower-than-expected preliminary University of Michigan Consumer Sentiment Survey reading of 73.7 for February and a surprise 0.2% decrease in December business inventories were met with little reaction.

Despite the dour disposition of participants in the early going, stocks were able to trim their losses as the dollar surrendered some of its gains. It finished the session with a 0.4% gain against competing currencies.

Though the greenback's pullback helped materials stocks reverse a near 2% loss in the early going to close with a fractional loss for the session, large-cap tech was the real leader in the stock market's afternoon move. Tech helped the Nasdaq finish the session with a gain, but the broader market was unable to overcome resistance at the neutral line.

Despite its inability to break into positive ground, the S&P 500 was still able to settle the week with a 0.9% gain. That marks its first weekly advance in five weeks.

Trading volume was strong this session as the number of shares exchanged on the NYSE exceeded recent averages. The spike in participation comes ahead of a three-day weekend for the markets, which will be closed Monday in observance of Presidents Day.

Advancing Sectors: Tech (+0.1%)

Declining Sectors: Utilities (-0.7%), Industrials (-0.7%), Energy (-0.6%), Telecom (-0.5%), Financials (-0.3%), Health Care (-0.3%), Consumer Staples (-0.2%), Materials (-0.1%)

Unchanged: Consumer DiscretionaryDJ30 -45.05 NASDAQ +6.12 SP500 -2.96 NASDAQ Adv/Vol/Dec 1556/2.23 bln/1051 NYSE Adv/Vol/Dec 1609/1.43 bln/1387

3:35 pm : The dollar index hit a session high early in the morning as the euro sold off following a disappointing Q4 eurozone GDP figure. Even as the dollar index pared its gains in the morning, its strength continued to hamper commodity prices this session.

As a result, precious metals attempted to pare losses throughout the session. Both gold and silver futures established an upward pattern for the session, but still closed lower. April gold hit a session low at $1078.10 per ounce before closing down 0.5% at $1088.80 per ounce. March silver hit a session low at $15.21 per ounce before closing down 1.0% at $15.43 per ounce.

Due to inclement weather earlier this week, the DOE reported both crude oil and natural gas weekly inventories this morning. A greater-than-expected draw in natural gas inventories resulted in higher natural gas prices for the session. The March contract bounced off the $5.35 level following the bullish data and closed 1.5% higher at $5.47 per MMBtu. Natural gas was the only energy commodity to end higher this session as bearish crude oil inventory data kept a lid on the rest of the commodity space. Crude oil prices were already substantially lower going into the data, however. The March contract closed 1.6% lower at $74.04 per barrel after moving higher off of the $73.00 per barrel level soon after the bearish data was released. DJ30 -90.47 NASDAQ -2.02 SP500 -7.36 NASDAQ Adv/Vol/Dec 1221/1.74 bln/1368 NYSE Adv/Vol/Dec 1159/772 mln/1785

3:00 pm : Small-caps and mid-caps have garnered support as participants head into the final hour of the session. In fact, both the Russell 2000 and the S&P 500 Mid-Cap Index are up 0.4%, while the broad-based S&P 500 is down 0.5%.

Among small-caps, Kenneth Cole (KCP 11.74, +1.26) is a primary leader, while Cheesecake Factory (CAKE 23.56, +0.90) is a primary leader among mid-caps. Both companies posted better-than-expected earnings for the latest quarter.

Despite the broader market's weakness this session, it is on track for a weekly gain of roughly 0.6%, which would mark its first weekly gain in five weeks. However, small-caps and mid-caps have outperformed the broughder market for the week, too. Small-caps are on track for a weekly gain of 2.2%, while mid-caps are up 1.9% this week. DJ30 -64.62 NASDAQ +0.97 SP500 -4.38 NASDAQ Adv/Vol/Dec 1220/1.58 bln/1356 NYSE Adv/Vol/Dec 1197/693 mln/1749

2:30 pm : The S&P 500 recently rallied to a fresh session high, but ran into resistance near the neutral line. Tech stocks have been a primary leader in the move -- the sector is still up 0.3%, while every other major sector remains in the red.

Semiconductor and semiconductor equipment stocks countinue to outperform. They are now up a collective 1.0%, which has helped the Nasdaq outperform its counterparts and make its way back into positive territory. DJ30 -26.08 NASDAQ +5.62 SP500 -1.30 NASDAQ Adv/Vol/Dec 1272/1.46 bln/1281 NYSE Adv/Vol/Dec 1315/641 mln/1616

2:00 pm : Volatility is up 2.5% this session, as measured by the Volatility Index. Since the start of the new year the Volatility Index has climbed 13%. Most of that move has come since the stock market pulled back from its January high.

Since its January high, the stock market has logged four straight weekly losses, which have left stocks down almost 7% from their 52-week high. Despite that downward move, the stock market is still up more than 60% since its 52-week low last March. DJ30 -91.67 NASDAQ -4.78 SP500 -7.87 NASDAQ Adv/Vol/Dec 1027/1.34 bln/1526 NYSE Adv/Vol/Dec 955/590 mln/1968

1:30 pm : The S&P 500 has rolled over from its session high, which took it within two points of the unchanged mark. All 10 major sectors are back in the red after tech (-0.4%), materials (-0.8%), and consumer staples (-0.5%) made their way to modest gains.

The Nasdaq, though back in the red, continues to outperform its counterparts. Large-cap tech has been a primary source of relative support.

Airline stocks are also strong this session. Leadership from Delta Air Lines (DAL 12.15, +0.32) has the Amex Airline Index up 1.1% in the face of broader market weakness. DJ30 -100.52 NASDAQ -6.63 SP500 -8.82 NASDAQ Adv/Vol/Dec 1008/1.22 bln/1533 NYSE Adv/Vol/Dec 919/537 mln/1983

12:55 pm : The major indices recovered much of their morning losses to trade with slight declines. The tech-heavy Nasdaq is outperforming with a slight gain thanks to strength in semiconductor stocks.

Selling interest this morning was driven by news that China will increase its reserve requirement for a second time as the as officials move to reign in stimulus to prevent the fast-growing economy from overheating.

The major indices started to pare losses shortly after the open, with a notable surge higher around 12:00ET on no specific news item.

In economic news, January retail sales surprised to the upside. Specifically, total retail sales rose 0.5% (consensus +0.3%) from the prior month, which was revised up to a decline of 0.1% from a decline of 0.3%, while sales excluding autos jumped 0.6% (consensus +0.5%). Sales gains were fairly broad-based in January. The notable exceptions were furniture and home furnishing stores (-1.4%), building material and supplies dealers (-1.2%), and miscellaneous store retailers (-1.1%).

But December business inventories declined 0.2% month-over-month, missing the consensus that called for a 0.2% increase.DJ30 -52.15 NASDAQ +1.27 SP500 -3.65 NASDAQ Adv/Vol/Dec 1027/1.10 bln/1474 NYSE Adv/Vol/Dec 1073/483 mln/1812

12:30 pm : Buying interest picks up, with the Nasdaq crossing into positive territory for the first time this session.

All ten sectors have moved higher, with tech (+0.3%), materials (+0.3%) and consumer staples (+0.1%) now posting a gain.

There does not appear to be a specific news item that accounts for the gains.DJ30 -47.46 NASDAQ +2.18 SP500 -3.25 NASDAQ Adv/Vol/Dec 1045/996 mln/1452 NYSE Adv/Vol/Dec 1164/442 mln/1709

12:00 pm : In the face of broader market weakness, semiconductor stocks have managed to extend their strong gains from the previous session. As such, the Philadelphia Semiconductor Index is up 0.4% this session and up 4.3% week-to-date. Intel (INTC 20.32, +0.26) remains a primary leader in its space, but Marvell Tech (MRVL 19.48, +0.36) is also strong after analysts raised their estimates for the company.

Strength among semiconductor stocks has helped the Nasdaq pare its losses. The Nasdaq had been down as much as 1.2% in the early going, but it has since more than halved that loss. DJ30 -107.89 NASDAQ -10.46 SP500 -975 NASDAQ Adv/Vol/Dec 810/853 mln/1680 NYSE Adv/Vol/Dec 748/381 mln/2123

11:30 am : Stocks have recovered some of their losses, but weakness remains widespread as all 10 major sectors trade in the red.

Despite its status as a defensive-oriented sector, utilities are among the weakest performers. The sector is currently down 1.2%. Hawaiian Electric (HE 19.50, -0.34) is especially weak after it reported an earnings miss for its latest quarter.

Consumer staples stocks have managed to limit their losses to just 0.4%, collectively. Shares of Clorox (CLX 59.38, -0.74) and Colgate-Palmolive (CL 79.30, -1.03) were given Neutral ratings by analysts at Credit Suisse, but they gave an Outperform rating to Procter & Gamble (PG 61.48, -0.48). DJ30 -112.53 NASDAQ -13.88 SP500 -10.09 NASDAQ Adv/Vol/Dec 733/769 mln/1718 NYSE Adv/Vol/Dec 677/348 mln/2181

11:00 am : Natural resource plays remain among the worst performers this session. As such, the materials sector is down 1.6%, while the energy sector is down 1.7%.

Energy stocks certainly haven't been helped by the latest weekly oil inventory data, which showed a larger-than-expected build of 2.42 million barrels. The announcement has caused oil prices to fall to fresh session lows, such that it is down 2.3% to $72.85 per barrel.

In addition to the data, oil prices still face a stiff headwind in a stronger dollar, which is currently up almost 0.6% against a basket of foreign currencies. DJ30 -131.55 NASDAQ -17.76 SP500 -12.39 NASDAQ Adv/Vol/Dec 644/637 mln/1745 NYSE Adv/Vol/Dec 619/288 mln/2230

10:35 am : Though the dollar has pulled back from its morning highs, it continues to keep pressure on both stocks and commodities alike. As such, the S&P 500 is still down slightly more than 1% with more than 90% of its components in the red, while the CRB Commodity Index is down 1.3% after it had hit a weekly high in the previous session.

Within the commodity complex, oil is particularly weak. Contracts were last quoted 2.8% lower at $73.20 per barrel. Prices could swing in either direction with the 11:00 AM ET release of weeky inventory data. The data are typically released on Wednesdays, but weather conditions led to a postponement.

Natural gas inventory data, which was postponed from Thursday to this morning, was just released. It showed a draw of 191 bcf, which is slightly more than expected since the consensus had called for a draw of 185 bcf. Prices have been whipsawed in the report's wake, but natural gas now trades with a 0.4% loss at $5.37 per contract.

Precious metals are also weak this morning. Gold prices were last quoted 0.8% lower at $1085.60 per ounce, while silver prices are down 1.4% to $15.37 per ounce. DJ30 -113.36 NASDAQ -13.31 SP500 -9.36 NASDAQ Adv/Vol/Dec 672/491 mln/1667 NYSE Adv/Vol/Dec 606/225 mln/2177

10:00 am : Stocks have pulled up a bit from their morning lows, but continue to trade with widespread weakness. The upturn comes as the dollar gives up part of its gain against competing currencies -- the Dollar Index had been up nearly 0.9%, but it now trades with a 0.5% gain.

Separately, the preliminary Consumer Sentiment Survey for February from University of Michigan came in at 73.7, which is below the reading of 75.0 that had been widely expected. The latest reading also marked a pullback from the 12-month high of 74.4 that was registered for January.

Meanwhile, business inventories for December decreased 0.2%, which is a disappointment since the consensus had called for a 0.2% increase. Inventories for November were revised slightly higher to reflect an increase of 0.5%.

Advancing Sectors: (None)

Declining Sectors: Energy (-1.5%), Materials (-1.5%), Financials (-1.5%), Industrials (-1.5%), Tech (-1.0%), Utilities (-1.0%), Health Care (-1.0%), Consumer Discretionary (-0.8%), Telecom (-0.8%), Consumer Staples (-0.5%)DJ30 -126.74 NASDAQ -19.26 SP500 -11.97 NASDAQ Adv/Vol/Dec 469/274 mln/1795 NYSE Adv/Vol/Dec 384/134 mln/2312

09:45 am : Stocks are bleeding with broad-based losses in the first few minutes of trade as a near 0.9% gain for the Dollar Index has brought about a stiff selling effort among participants in the equity market.

Natural resource plays are under some of the most pressure after they had outperformed in the previous session. Materials stocks are presently down 1.6%, while energy stocks are down 1.8%.

Industrial stocks are also weak, though. The sector has shed 1.6% so far. Conglomerate 3M (MMM 78.85, -1.42) is a primary laggard in the group, partly due to a downgrade by analysts at Bank of America's Merrill Lynch. DJ30 -146.47 NASDAQ -24.55 SP500 -15.07 NASDAQ Adv/Vol/Dec 364/154 mln/1825 NYSE Adv/Vol/Dec 290/84 mln/2351

09:15 am : S&P futures vs fair value: -7.90. Nasdaq futures vs fair value: -11.80. Stocks head into Friday's session with a week-to-date gain of more than 1%, which could make for the stock market's first weekly gain in five weeks. However, the possibility of such a feat has come under pressure amid a sharp rise by the U.S. dollar to fresh multimonth highs against a basket of foreign currencies. The greenback has since pulled back a bit, but it continues to sport a strong 0.7% gain. The dollar's strength stems primarily from a weaker euro, which has been pressured in the wake of a weaker-than-expected fourth quarter eurozone GDP reading. Offers of financial support to Greece from the International Monetary Fund (IMF) and a pledge from the European Central Bank to monitor the situation haven't done anything to support the continent's chief currency. Meanwhile, news that China's central bank will hike reserve requirements at banks in order to curtail lending has likely dampened the mood among participants this morning as they consider the implications of efforts to slow growth in China. All of this has overshadowed an upbeat U.S. advance retail sales report that showed a stronger-than-expected increase in sales and sales less autos for January. Still to come, though, is the preliminary consumer confidence survey for February from University of Michigan (9:55 AM ET) and business inventory data for December (10:00 AM ET). Weekly natural gas inventory data is due at 10:30 AM ET, followed by weekly crude oil inventory data at 11:00 AM ET.

09:00 am : S&P futures vs fair value: -6.30. Nasdaq futures vs fair value: -9.80. U.S. stock futures remain weak, but Europe's major bourses are mixed amid news that eurozone GDP increased at a slower-than-expected 0.1% pace in the fourth quarter. That has caused the euro to slide to eight-month lows against the U.S. dollar. As for plans to provide Greece with financial assistance, the IMF has stepped forward to offer its support. However, specifics to any sort of plan have yet to be disclosed and Greece has yet to actually accept offers for aid. Meanwhile, Germany reported that its fourth quarter GDP was flat, which contrasted with expectations for moderate growth. To compound the offense, industrial production for December declined 1.7% from November, though a slight increase had been expected. Despite those disappointments, Germany's DAX has made its way to a 0.4% gain. Bayer is a primary leader as it puts together its best single-session percentage gain in more than one month. France's CAC is currently flat, though declining issues have a 3-to-2 advantage over advancers. Advancers are presently led by energy giant Total (TOT), while financial issues are directing losers. Financial issues are also weak in Britain, where the FTSE is flat, as well. In Asia, the MSCI Asia Pacific Index mustered a 0.4% gain, while Japan's Nikkei played catch-up as it returned from holiday to log a 1.3% gain. Toyota Motor (TM) was a strong performer, but Nissan Motor (NSANY) was weak. Fast Retailing was a primary leader as it booked its best single-session percentage gain in two weeks. In Hong Kong, the Hang Seng slipped 0.1%. Data showed that China's banks had issued stronger-than-forecast loan volume in January, but China Construction Bank and Bank of China still faltered. After the close it was announced that China's central bank will raise reserve requirements at banks for the second time this year. Meanwhile, mainland China's Shanghai Composite finished the weak on a solid note as it booked a 1.1% gain.

08:35 am : S&P futures vs fair value: -7.40. Nasdaq futures vs fair value: -10.50. Advance retail sales for January increased 0.5%, which is stronger than the 0.3% increase that had been widely expected and marks an improvement from the upwardly revised 0.1% decline for December. Excluding autos, sales increased 0.6%, which is slightly stronger than the 0.5% increase that many economists had come to expect. Sales less autos for December had declined 0.2%. Excluding both autos and gas, retail sales for January increased 0.6%, which exceeds the consensus call for a 0.5% increase and marks an improvement from the 0.3% decline that had been posted for December. Stock futures haven't shown a reaction to the data since the dollar continues to weigh on the mood of premarket participants.

08:00 am : S&P futures vs fair value: -7.40. Nasdaq futures vs fair value: -12.30. A sharp gain by the dollar has put pressure on both stock futures and commodity futures this morning, effectively threatening to undo some of the broad-based gains that were made in the previous session. The greenback's gain comes amid a sharp pullback by the euro in the wake of news that eurozone GDP eked out a smaller-than-expected 0.1% increase in the fourth quarter. There is also news this morning from The Wall Street Journal that for already the second time this year China's central bank will raise the reserve requirement for banks. That announcement was made after the close of trade in Asia, where markets finished the week in mixed fashion after they had been cautiously traded during recent weeks for fear of that China's central bank would engage in such a move or other measures to tighten monetary policy. There haven't been any market-moving corporate items this morning, but the January Advance Retail Sales Report is due at the bottom of the hour, followed by the preliminary consumer confidence survey for February from University of Michigan at 9:55 AM ET. Shortly thereafter business inventory data for December will be released (10:00 AM ET). The latest Treasury Budget, which had been scheduled for 2:00 PM ET, has been postponed.

06:22 am : S&P futures vs fair value: -8.90. Nasdaq futures vs fair value: -15.00.

06:22 am : Nikkei...10092.19...+128.20...+1.30%. Hang Seng...20268.69...-22.00...-0.10%.

06:22 am : FTSE...5144.19...-17.70...-0.30%. DAX...5517.87...+13.90...+0.30%.

Special thanks to Yahoo! Finance and CNNMoney for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body analysis)

@

http://twitter.com/wrbtrader Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.comGo Back To TheStrategyLab.com Homepage