Attachment:

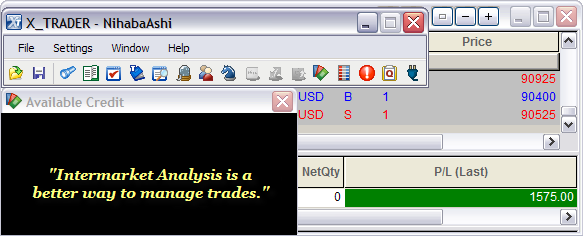

051209NihabaAshiPnLBlotterProfit.png [ 32.25 KiB | Viewed 1546 times ]

051209NihabaAshiPnLBlotterProfit.png [ 32.25 KiB | Viewed 1546 times ]

Today's trades that were posted in real-time in #FuturesTrades chat room via my IRC user name

NihabaAshi. You can review each trade from entry to exit along with commentary and an occasional trading tip because its all archived @

http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=20&t=186 My Trading Performance:

+31.50 Emini ES points

-------------------------------

Key WRB Price Action 2min Regular Chart - WRB at 1336pm est provided the support that send the market higher for the remainder of the trading day.

Dow Gains, Nasdaq FaltersInvestors show indecision following a two-month rally, jittery about automaker and housing market weakness.

By Alexandra Twin, CNNMoney.com senior writer

Last Updated: May 12, 2009: 6:10 PM ET

NEW YORK (CNNMoney.com) -- Blue chips gained and the Nasdaq declined in a mixed Tuesday session on Wall Street as investors showed caution after the recent rally and amid ongoing worries about banks and autos.

The Dow Jones industrial average (INDU) gained 50 points, or 0.6%.

The S&P 500 (SPX) index ended just below unchanged. The Nasdaq composite (COMP) lost 15 points, or 0.9%.

Stocks slumped through the early afternoon Tuesday, but managed to cut some losses in the last hour.

Chevron (CVX, Fortune 500), Exxon Mobil (XOM, Fortune 500), Johnson & Johnson (JNJ, Fortune 500) and Coca-Cola (KO, Fortune 500) were among the stocks lifting the Dow.

Stocks slipped Monday, with the Dow posting its worst day in 3 weeks, as the two-month old stock rally hit a wall. All three major gauges have risen more than 30% since hitting multi-year lows on March 9. Bets that the economy and financial sector are close to stabilizing have fueled the gains.

But after such a big run, stocks were vulnerable to a bit of a pullback, said John Wilson, chief technical strategist at Morgan Keegan.

"With everyone expecting a big correction, I don't think we'll see it," he said. "We'll probably just see a few more down days but not something more substantial."

He said the bank stocks have gotten a little ahead of themselves and are probably due for a bigger retreat, in particular.

After the close, Applied Materials (AMAT, Fortune 500) reported a steer-than-expected quarterly loss versus a profit a year ago. The chipmaker also reported a plunge in revenue, but results were better than expected.

Shares slumped 2% in after-hours trading.

Also after the close, Freddie Mac (FRE, Fortune 500) reported a $9.9 billion quarterly loss and asked the government for another $6.1 billion in help.

On Wednesday, April retail sales are due before the open from the Commerce Department. April sales are expected to hold steady after falling 1.2% in March. Sales excluding volatile autos are expected to have rise 0.2% after falling 1% in March.

Reports are also due on April import and export prices, March business inventories and weekly crude inventories.

Economy: The Treasury budget for April revealed a $20.9 billion deficit. It was the first during the month in 26 years, reflecting the impact of the recession and economic stimulus efforts. Economists surveyed by Briefing.com expected a deficit of $20 billion.

Treasury had reported a budget deficit of $191 billion in March.

Treasury also released its annual report on the health of social security and Medicare, which showed that the recession has hit both programs hard.

The housing market contracted at a record pace in the first three months of the year, according to a National Association of Realtors report released Tuesday.

The national median price of single family homes sold during the first three months of the year fell 13.8% versus a year ago to $169,000.

The March trade deficit widened after narrowing in February, according to a government report released Tuesday morning. The deficit widened to $27.6 billion from a revised $26.1 billion. Economists expected a reading of $29 billion, on average, according to a Briefing.com survey.

Financials: Bank of America (BAC, Fortune 500) reportedly made $7.3 billion from the sale of 13.5 million shares of China Construction Bank to a group of buyers, according to published reports.

A number of banks sold stock or said they plan to sell stock to raise money.

U.S. Bancorp (USB, Fortune 500) sold $2.5 billion of stock and Bank of New York Mellon (BK, Fortune 500) sold around $1.2 billion in stock. BB&T (BBT, Fortune 500) is expected to sell $1.5 billion in stock. Regulators determined that the three banks do not need to raise more capital as a result of the bank stress tests.

In other news, Citigroup (C, Fortune 500) said it has approved $8.2 billion in lending to consumers this year, thanks to the government funding it received through the bank bailout plan.

The bank sector was lower, but managed to trim losses late in the session. The KBW Bank (BKX) sector index, which includes two dozen of the largest banks, fell 4.2%.

Corporate news: Automakers were weaker, with General Motors (GM, Fortune 500) down on growing speculation that the company is likely to file for bankruptcy protection. The shares fell intraday to $1.09, the lowest level since 1933 Tuesday, one day after a group of the company's executives said they had sold stock and direct holdings in the automakers. Shares ended at $1.15, down 20%.

Ford Motor (F, Fortune 500) fell after saying late Monday that it will sell 300 million shares of stock to raise roughly $1.8 billion in capital.

Bonds: Treasury prices were little changed, with the yield on the benchmark 10-year note at 3.17% unchanged from Monday. Treasury prices and yields move in opposite directions.

Other markets: In global trading, Asian markets ended in mixed territory, while European markets ended lower.

In currency trading, the dollar fell versus the euro and the yen.

U.S. light crude oil for June delivery rose 35 cents to settle at $58.85 a barrel on the New York Mercantile Exchange.

COMEX gold for June delivery rose $10.40 to settle at $923.90 an ounce.

Yahoo! Finance

Yahoo! Finance 4:35 pm : Profit takers sold early gains and sent the major indices markedly lower for most of the session, but stocks were able to battle back in the second half and finish in mixed fashion despite a lack of positive catalysts.

Out of favor for the second straight session, financials fell 1.8%. Financials were actually up more than 1% in the early going, but sellers pounced on the sector, focusing their efforts on regional banks (-5.6%) and diversified banks (-3.2%).

Bank of America (BAC 12.26, -0.68) was a primary laggard in the financial sector. Investors were unimpressed by news that the company is selling a partial stake in China Construction Bank for $7.3 billion to a consortium of buyers.

Bank of New York (BK 28.43, -1.12) also traded with weakness. It was the latest financial outfit to announce a secondary common stock offering.

Ford (F 5.01, -1.07) also fell out of favor after it announced a common stock offering that will raise funds for general purposes and help provide for certain union obligations, but the offering is also expected to dilute existing shareholders.

General Motors (GM 1.15, -0.29) was dogged as investors become increasingly concerned about whether the company will have a restructuring plan ready for government review by June. Yesterday GM's management indicated that it is more probable that GM will need to accomplish its goals through bankruptcy. Shares of the Dow component are at their lowest level in decades.

Fellow Dow component Microsoft (MSFT 19.89, +0.57) will issue $3.75 billion of senior unsecured notes to help fund working capital requirements, capital expenditures, or share repurchases. Microsoft was a primary leader among tech stocks (-0.6%), which actually underperformed the broader market.

Participants also rotated out of early cycle stocks in favor of defensive-oriented holdings. As such, industrials fell 1.2% and consumer discretionary stocks slid 2.2% as shares of retailers surrendered 0.9%. Retailers will come into sharper focus tomorrow, when the Advance April Retail Sales data is unveiled (8:30 AM ET).

Meanwhile, consumer staples stocks climbed 1.3%, health care advanced 1.4%, telecom tacked on 1.1%, and utilities closed 0.6% higher. Gold gained 1.1% to settle pit trading at $923.90 per ounce.

There weren't any major earnings announcements this session. In terms of economic data, the U.S. trade deficit widened to $27.6 billion in March, which is the first time in eight months that the deficit widened. However, the increase comes off of February's $26.1 billion deficit, which was the narrowest deficit since 1999.

Additionally, the March reading is an improvement from the first quarter average through February, so it should factor favorably into the revised first quarter GDP reading. The latter point aside, the March trade balance report serves as another reminder that global trade continues to contract as countries around the globe grapple with the effects of the financial crisis.DJ30 +50.34 NASDAQ -15.32 NQ100 -1.3% R2K -1.4% SP400 -1.0% SP500 -0.89 NASDAQ Adv/Vol/Dec 975/2.48 bln/1747 NYSE Adv/Vol/Dec 1270/1.61 bln/1744

3:30 pm : June crude oil contracts opened the pit trade at session highs. The contracts traded below the flat line and hit session lows of $57.81 per barrel in the afternoon before closing back in positive territory at $58.85 per barrel, up 0.6%.

After another rally in natural gas this session, the June natural gas contracts are up almost 28% for the month of May. The June futures rallied into the close to finish up 1.6% at $4.47 per contract.

Precious metals performed well this session as they traded up 1.63%.

July silver futures opened the session significantly higher and were able to hold on to those gains for most of the session. The July contracts are now up about 15% for the month of May. The contracts closed at $14.22 per ounce, up 2.2%.

June gold futures traded in positive territory for the entire session and finished at $923.90 per ounce, up 1.1%.DJ30 +82.44 NASDAQ -5.96 SP500 +3.87 NASDAQ Adv/Vol/Dec 1062/2.11 bln/1633 NYSE Adv/Vol/Dec 1406/1.21 bln/1595

3:00 pm : The major indices are making an upward move, with the Dow and S&P 500 now posting a slight gain. Buying interest is broad-based, with six of the ten sectors now in positive territory.

Former Fed Chairman Alan Greenspan said that home prices are an "Achilles' heel" for the U.S. economy, but he is seeing "seeds of bottoming" in housing, Dow Jones reports.

Released at 14:00 ET, the Treasury deficit for April came in at $20.9 billion, which was near the consensus that called for a deficit of $20.0 billion. In April 2008, the Treasury had a surplus of $159.3 billion.DJ30 +44.53 NASDAQ -13.58 SP500 +0.46 NASDAQ Adv/Vol/Dec 920/1.88 bln/1781 NYSE Adv/Vol/Dec 1217/1.08 bln/1787

2:30 pm : The Dow had been making its way back to the unchanged mark, but recently encountered some resistance. Still, the Dow's advancers are evenly balanced with its declining issues.

Exxon Mobil (XOM 70.32, +1.05) is providing the most leadership to the Dow, but JPMorgan Chase (JPM 34.93, -0.90) is undercutting the blue chip index.

While Exxon Mobil and JPMorgan Chase are having the most influence over the price-weighted index, Pfizer (PFE 14.85, +0.70) is trading with the best percentage gain in the Dow and General Motors (GM 1.12, -0.32) is trading with the worst percentage loss of any Dow component.DJ30 -10.75 NASDAQ -25.32 SP500 -6.64 NASDAQ Adv/Vol/Dec 794/1.74 bln/1900 NYSE Adv/Vol/Dec 927/989 mln/2065

2:00 pm : Action remains listless in the absence of any market-moving earnings announcments, economic data, or other headlines. Amid a lack of bullish catalysts, profit takers have been able to retain control.

The presence of sellers has kept stocks in the red all afternoon, and a recent effort to pull up from session lows was resisted and put stocks on the backslide again.DJ30 -31.62 NASDAQ -28.77 SP500 -10.05 NASDAQ Adv/Vol/Dec 752/1.62 bln/1931 NYSE Adv/Vol/Dec 872/917 mln/2103

1:30 pm : For the second straight session, declining issues outnumber advancers by 4-to-1 in the S&P 500, which is now down more than 3% during the course of the past two sessions. Still, the stock market is up roughly 2.7% month-to-date.DJ30 -30.10 NASDAQ -30.08 SP500 -10.08 NASDAQ Adv/Vol/Dec 733/1.49 bln/1932 NYSE Adv/Vol/Dec 855/841 mln/2117

1:00 pm : Stocks are slipping in what looks like continued profit-taking from the prior session.

The major indices gapped up in the first few minutes of trading, but participants quickly turned against stocks and sent them into the red. For the second straight session, sellers have been focused on financials, which are down 4.5% after being up more than 1% in the early going. Financials are now down more than 10% during the course of the past two sessions.

Bank of America (BAC 12.23, -0.71) is among the primary laggards in the financial sector after climbing more than 60% last week. Reports indicate the company sold part of its stake in China Construction Bank to a consortium of buyers for $7.3 billion, which will likely help satisfy capital requirements for recent government stress tests.

Though it said it was one of only a few banks that would have made money under the government's stress test scenarios, Bank of New York (BK 28.17, -1.39) has announced a $1.2 billion common stock offering priced at $28.75 per share, which is $1 below the prior session's closing price. Shares of BK are making their worst two-day slide (-11.9%) in nearly two months.

Ford (F 5.41, -0.67) is under pressure after announcing a common stock offering of its own. The company will make public 300 million shares of common stock, which is expected to dilute current shareholders.

Dow component Microsoft (MSFT 19.74, +0.42) is looking to raise some cash of its own by offering $3.75 billion of senior unsecured notes, which will help fund working capital requirements, capital expenditures, or share repurchases. The offering isn't being construed as any sign of weakness since the company carries more than $25 billion in cash and short-term investments.

Despite Microsoft's strength, large-cap tech is surrendering gains from the prior session to trade with weakness.

With financials and large-cap tech failing to provide positive leadership and profit takers still in charge, many participants are rotating into safer sectors like telecom (+0.6%), consumer staples (+0.7%), and health care (+1.1%). The three sectors are the only ones sporting gains while the broader market slips to fresh session lows. DJ30 -44.76 NASDAQ -34.95 SP500 -12.34 NASDAQ Adv/Vol/Dec 716/1.37 bln/1934 NYSE Adv/Vol/Dec 825/776 mln/2133

12:30 pm : Stocks have descended to fresh session lows. Losses remain concentrated in financial stocks (-3.7%) and consumer discretionary stocks (-3.1%).

Small-caps and mid-caps are seeing strong selling too. The Russell 2000 is down 2.3% and the S&P 400 is off by 2.2%.DJ30 -33.93 NASDAQ -29.25 SP500 -9.46 NASDAQ Adv/Vol/Dec 781/1.24 bln/1846 NYSE Adv/Vol/Dec 912/703 mln/2014

12:00 pm : Large-cap tech continues to underperform the broader market. Among the bunch, Apple (AAPL 125.37, -4.20) and Research In Motion (RIMM 68.89, -4.29) are trading as primary laggards.

Microsoft (MSFT 19.74, +0.42) is providing some support, though. Microsoft, which carries a coveted AAA credit rating, announced it is offering $3.75 billion of senior unsecured notes, which could help fund working capital, capital expenditures, or share repurchases. The offering is expected to close on May 18, 2009.

Since Microsoft already keeps more than $25 billion in cash and short-term investments in its coffers, some analysts believe the firm's decision to issue the debt is aimed at lowering its cost of capital. Of the $3.75 billion being offered, $1 billion is in the form of 10-year notes, which will yield 4.20% -- approximately 100 basis points more than the 10-year Treasury Note currently yields.DJ30 -26.60 NASDAQ -23.98 SP500 -7.86 NASDAQ Adv/Vol/Dec 831/1.06 bln/1757 NYSE Adv/Vol/Dec 1022/602 mln/1887

11:30 am : Shares of automakers are under considerable pressure this session. General Motors (GM 1.11, -0.33) is having the hardest time

off the selling effort as its share price falls to its lowest level in decades amid the threat of bankruptcy; the company is just a couple of weeks away from its restructuring deadline.

Ford (F 5.52, -0.56) is also under pressure. By refusing to take any government assistance Ford appears to be in the best shape of the battered U.S. automakers. However, Ford announced last evening a public offering of 300 million shares of common stock.

Meanwhile, Asian automaker Toyota Motor (TM 76.40, -0.39) is seeing moderate selling pressure after forecasting a larger annual loss than many analysts had expected. Conversely, Nissan (NSANY 10.81, +0.47) surprised some by forecasting a narrower loss for the year than had been expected.DJ30 -19.35 NASDAQ -21.71 SP500 -6.12 NASDAQ Adv/Vol/Dec 834/954 mln/1731 NYSE Adv/Vol/Dec 1035/540 mln/1839

11:00 am : The stock market continues to trade with losses. However, stocks of defensive-oriented consumer staples (+1.1%), health care (+1.7%), and telecom (+0.4%) are trading with gains.

Energy stocks (+0.2%) and materials stocks (+0.3%), which are cyclical plays, recently made their way into positive territory amid a sudden pickup in buying interest.

Meanwhile, consumer discretionary stocks (-2.5%) are trading with the steepest loss of any sector.DJ30 +1.04 NASDAQ -15.06 SP500 -2.89 NASDAQ Adv/Vol/Dec 857/797 mln/1645 NYSE Adv/Vol/Dec 1082/458 mln/1758

10:30 am : Stocks have surrendered all of their initial gains, but commodities are sporting solid gains.

Crude oil futures contracts are currently pricing oil 1.2% higher at $59.20 per barrel. Crude prices actually climbed to a fresh six-month high of $60.08 per barrel in the minutes leading up to pit trading.

Natural gas prices are also making an impressive advance by climbing 1.9% to $4.38 per contract.

As for precious metals, gold prices are up 0.5% to $917.90 per ounce, while silver prices are up 1.9% to $14.17 per ounce.

The broad gains among key commodities are helping advance the CRB Commodity Index, which is currently sporting a 0.6% gain. The CRB has advanced roughly 10.5% month-to-date.

Meanwhile, the Baltic Dry Index advanced 1.7%, helped by each of its subindices.DJ30 -12.50 NASDAQ -13.72 SP500 -4.73 NASDAQ Adv/Vol/Dec 832/611 mln/1608 NYSE Adv/Vol/Dec 1038/353 mln/1763

10:05 am : While the broader market traded with weakness in the prior session, large-cap tech stocks showed strength. However, large-cap tech is grappling with stiff selling pressure this session, which has resulted in outsized declines for the Nasdaq 100 (-0.9%) and the Nasdaq Composite.

Early movers: Trading up -- AGM +96.1%, SSY +90.8%, FCL +35.1%, STEC +32%, CTRP +30.6%, CNB +26.5%, CPE +24.9%, BFR +24%, CHUX +23.7%, NNI +21.7%, ABCW +20.7%, TWTC +19.1%, FTBK +17.1%, WINN +16%, FOSL +15.3%, PDA +13.2%, CATT +13.1%, PQ +11.5%, WLT +10.1% Trading down -- NFP -17.2%, AIPC -14.5%, GAP -13.3%, QSFT -9.7%, MR -9.3%, AXL -8.9%DJ30 +9.01 NASDAQ -6.85 SP500 -1.18 NASDAQ Adv/Vol/Dec 1060/379 mln/1267 NYSE Adv/Vol/Dec 1293/228 mln/1415

09:50 am : The major indices have pulled back after making a solid start. The initial advance was led by strength in financial stocks and energy stocks, both of which were up more than 1%. However, financials are now down 1.3% and energy stocks are down 0.2%.

Financial stocks had actually led the prior session's losses by falling nearly 7%, which enticed some participants to make bids in an effort to lock in lower prices this morning.

Energy stocks were also out of favor in the prior session, but were initially helped this morning by a rebound in oil prices, which took crude futures above $60 per barrel near the opening of pit trading. Crude is now trading with a 1.2% gain at $59.20 per barrel, but that is still near six-month highs.DJ30 -4.06 NASDAQ -5.91 SP500 -2.11 NASDAQ Adv/Vol/Dec 1061/270 mln/1199 NYSE Adv/Vol/Dec 1202/169 mln/1453

09:20 am : S&P futures vs fair value: +4.50. Nasdaq futures vs fair value: +4.80. Despite a lack of upbeat headlines to act as buying catalysts, participants are showing a willingness to step in and pick up stocks after watching the major indices slip in the prior session. That has stock futures pointing to a solid start for the major U.S. indices. Meanwhile, European stocks are trading with fair gains after a mixed start. However, several major financial institutions remain under pressure amid reports the European Union will conduct stress tests on its banking system by September. Barclays (BCS) was downgraded by analysts at Credit Suisse and is trading as a primary laggard in Britain's FTSE, which is up 0.2%. In British economic news, Reuters reported that British industrial output fell less than expected in March, but still posted its biggest annual decline on record. According to statistics, industrial output dropped by 0.6% in March, less than the 0.8% drop forecast. This was still enough to take the annual rate down 12.4%. Meanwhile, France's CAC is up 0.1% and Germany's DAX is up 0.9%. German Ministry of Finance published a draft law that allows banks to swap toxic assets for guaranteed bonds under a voluntary program that has yet to be considered by the country's Chancellor. In Asia, the MSCI Asia-Pacific Index shed 1.2% and Japan's Nikkei fell 1.6%; both succumbed to profit-taking. Several financials felt considerable pressure. Meanwhile, selling against Dentsu, Japan's biggest advertising agency, was stimulated after the company reported a fourth quarter loss and forecast a weak recovery. Mazda fell amid profit concerns, and Nissan (NSANY) reported a net annual loss, but predicted the company will return to profitability by the finish of fiscal year 2010, which ends in March 2011, according to The Wall Street Journal. In Hong Kong, the Hang Seng advanced 0.4%, led by a China Construction Bank. China Construction Bank gained after Bank of America (BAC) sold $7.3 billion worth of shares in the company. In mainland China, the Shanghai Composite closed 1.5% higher. China's export data for last month showed a steeper-than-expected slide of almost 23%. However, fixed asset investment spiked 34% in April.

08:35 am : S&P futures vs fair value: +5.60. Nasdaq futures vs fair value: +7.50. The latest trade data has had little impact on stock futures, which continue to indicate a solid start for the major indices. The U.S. trading deficit for March totaled $27.6 billion, which is less than the $29.0 billion deficit that was widely expected. February's deficit, which had narrowed sharply from January due to a drop in imports, was revised modestly higher to $26.1 billion.

08:00 am : S&P futures vs fair value: +6.30. Nasdaq futures vs fair value: +6.80. Stock futures suggest a modest rebound from the prior session's drop is in order for the major indices. Shares of Bank of America (BAC) slid more than 8% Monday, but are trading 1.9% higher at $13.18 per share in Tuesday's premarket action. The Wall Street Journal reported that Bank of America sold 13.5 billion shares of China Construction Bank to Temasek Holdings, Hopu Investment Management, and China Life Insurance for $7.3 billion, which comes as Bank of America seeks capital to satisfy government requirements. Meanwhile, Bank of New York (BK) is down 2.2% to $28.90 per share in premarket trading after announcing last evening a proposed offering of $1 billion of its common stock to the public. The company may use part of the proceeds to fund preferred stock repurchases, common stock warrants held under TARP, or general corporate purposes. Reuters.com reported that the European Union will conduct stress test on its banking system by September. European bank stocks are currently under pressure in overseas trading, but the broader European bourses are trading in mixed fashion.

06:36 am : S&P futures vs fair value: +2.90. Nasdaq futures vs fair value: +1.00.

06:36 am : Nikkei...9298.61...-153.40...-1.60%. Hang Seng...17153.64...+65.70...+0.40%.

06:36 am : FTSE...4426.01...-9.50...-0.20%. DAX...4892.81...+26.10...+0.50%.

Go Back To TheStrategyLab.com Homepage