Price Action Trade Results of M.A. Perry

Price Action Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htm &

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Users of WRB Analysis Real-Time Trades - TheStrategyLab Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Users of WRB Analysis Reviews / Accolades / Testimonials: http://www.thestrategylab.com/Accolades.htm Review of TheStrategyLab: http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 &

http://www.thestrategylab.com/thestrategylab-reviews.htmPrice Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Telephone: +1 708 572-4885

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

Quote:

No trades for me today. Its a designated rest/relax day for me due to the national Canada holiday. Simply, I spent the day barbecuing and relaxing with the kids today but I have a ton of personal things to do all week...its a big mental distraction for me but I did log into the free chat room and left my computer on to record the chat room conversation for other traders that were in the chat room to post their real-time trades and price action analysis to ensure that guest visitors reading the chat logs will know that some

users of TheStrategyLab did in fact post their real time trades and/or price action analysis. Oddly, whenever I'm on a holiday...only a few members show up as if they know its a holiday here in Canada and I won't be trading. TheStrategyLab members chat log at the below link.

![[ec44]](./images/smilies/emoticonreading.gif "Reading")

Quote:

Announcement - On Wednesday July 11th 2018, I will

move my public trade journal into the private trade journal section. You must be a registered member of TheStrategyLab with an active trade journal here

@ TheStrategyLab via a minimum of 21 trade journaling days (real money

or simulator) to gain access to my now

private trade journal

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=362All of my trades are posted

real-time at the above link for today's archive chat log in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader along with the real-time trades by other users of WRB Analysis for anyone to do a real-time review (you must be a member of the chat room for a real-time review). Also, as stated since the birth of the free chat room TheStrategyLab...we are

not a signal calling trade alert room. Thus, there is no trader telling you what to trade, when to buy and when to sell. I'm the moderator (I keep the peace between members) and my own live trades are posted within 3.2 seconds on average

after the trade confirmation in my broker trade execution platform via an

auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion.

In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility...all key concepts from the WRB Analysis free study guide even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads.

Quote:

These real-time trades involves price action concepts from

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always

backtesting new concepts of WRB Analysis, new trade entry rules, new trade management rules, new position size management rules before application in real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades and

prior to sharing the new concepts with fee-base clients...living up to the name of my website.

TheStrategyLab.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The

purpose of TheStrategyLab is for you to post

your real-time price action analysis or real-time trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements...it also gives guest readers of the chat logs a peek into the trade performance of users of TheStrategyLab. If you join the free chat room and then you decide to

not post any WRB Analysis about the price action or you decide to not post your trades or you decide to be silent (lurk without saying a word about today's markets)...you're not using the free chat room properly to help improve your trading and the chat room will be

useless to you

except for those silent chat room members that are posting their broker statements & quantitative statistical analysis of their trading in their private threads at the forum itself. Thus, we highly recommend that you use your broker trade execution platform (real money or simulator) with a

professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they will provide you with the

quantitative statistical analysis of your trading regardless if you're posting real-time trades or real-time price action analysis in the free chat room.

You can download your results and then post them in your private thread at the forum at the end of your trading day. This allows silent members to continue using the free chat room to just monitor the real time discussion whenever they want..useful if you view chat rooms as a distraction from your trading if you were to share real-time info about your trading for documentation in the chat room logs.

Access instructions for the free chat room

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Member's Private Threads @ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=118 Member's Private Trade Journals @ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=349 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=358&t=3788 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini RTY futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

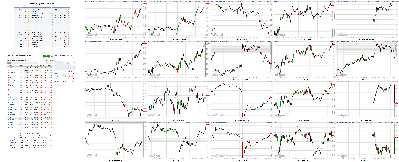

Attachment:

070218-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.95 MiB | Viewed 352 times ]

070218-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.95 MiB | Viewed 352 times ]

click on the above image to view today's price action of key markets discussed by members of TheStrategyLab chat room or private thread discussions The Market at 04:30PM ETDow: +35.77… | Nasdaq: +57.38… | S&P: +8.34…

NASDAQ Vol: 1.76 bln… Adv: 1772… Dec: 1149…

NYSE Vol: 755.9 mln… Adv: 1627… Dec: 1334…

Moving the Market

Trade matters in focus; President Trump says he's not backing down on China tariffs; EU threatens $300 billion worth of retaliatory tariffs on U.S. goods

Crude oil prices tick lower after President Trump says he's reached a deal with Saudi Arabia's King Salman to boost production by up to two million barrels per day

Top-weighted technology and financials sectors outperform; tech space leads broad-based afternoon rally

Sector Watch

Strong: Financials, Technology, Utilities

Weak: Energy, Materials, Consumer Staples, Real Estate

04:30PM ET

[BRIEFING.COM] A tech-charged afternoon rally saved the U.S. equity market from kicking off the abbreviated Fourth of July week on a lower note. The S&P 500 advanced 0.3%, closing at its best mark of the day and about eight points above its 50-day moving average. The Dow added 0.2%, the Nasdaq jumped 0.8%, and the Russell 2000 climbed 0.7%.

Trade tensions were heightened on Monday morning after President Trump said over the weekend that he will not back down on China tariffs. Separately, the European Union warned that it would impose tariffs on nearly $300 billion worth of American goods if the U.S. follows through with duties on EU automobiles. Mr. Trump said U.S. and EU officials will be meeting fairly soon to try to "work something out."

On Wall Street, the trade war rhetoric led stocks lower at the opening bell; the S&P 500 was down as much as 0.7%. However, the market started retracing some losses soon thereafter, and then the top-weighted technology sector led a full-fledged rebound in the afternoon.

The tech space -- which represents a quarter of the broader market -- finished atop Monday's sector standings with a gain of 1.0%. Tech giants like Apple (AAPL 187.18, +2.07), Microsoft (MSFT 100.01, +1.40), Facebook (FB 197.36, +3.04), and Alphabet (GOOG 1127.46, +11.81) added between 1.1% and 1.6%.

In total, seven of eleven sectors finished in the green. The utilities space (+0.8%) closed right behind technology, and the heavily-weighted financial group (+0.7%) also had a strong outing. On the flip side, the energy sector (-1.6%) finished at the bottom of the leaderboard, with consumer staples (-0.5%) being the next-worst performer.

The energy sector's decline came amid a modest sell off in the crude oil futures market, which was under pressure after President Trump said he's struck a deal with Saudi Arabia to increase output by up to two million barrels per day. WTI crude futures ended lower by 0.3% at $73.94 per barrel.

In corporate news, Tesla (TSLA 355.07, -7.88) got off to a good start, adding as much as 6.4%, after CEO Elon Musk said the electric automaker hit its long-elusive production target of 5,000 Model 3 vehicles per week in the last seven days of the second quarter, but shares quickly reversed course, eventually ending lower by 2.3%.

Elsewhere, U.S. Treasuries slipped on Monday, pushing yields higher across the curve; the benchmark 10-yr yield climbed to 2.87% from 2.85%. Meanwhile, the U.S. Dollar Index rallied 0.5% to 94.70, and the CBOE Volatility Index was up as much as 23.2%, but finished lower by 2.1% at 15.76.

Reviewing Monday's economic data, which was limited to the ISM Manufacturing Index for June and the Construction Spending report for May:

The ISM Index for June increased to 60.2 from an unrevised reading of 58.7 in May, while the Briefing.com consensus expected a reading of 58.5.

The key takeaway from the report is that it reflects continued strength in the manufacturing sector with the Prices Index sitting just below its best level in more than seven years.

Construction Spending rose 0.4% in May, while the Briefing.com consensus expected an increase of 0.6%. The April reading was revised to +0.9% from +1.8%.

The key takeaway from the report is that, combined with the downward revision for April, construction spending will make a smaller contribution to Q2 GDP forecasts than what was originally expected.

Looking ahead, Tuesday's trading session will end early (1:00 PM ET), and markets will be closed on Wednesday for the Fourth of July.

Nasdaq Composite +9.6% YTD

Russell 2000 +7.8% YTD

S&P 500 +2.0% YTD

Dow Jones Industrial Average -1.7% YTD

Dow: +35.77… | Nasdaq: +57.38… | S&P: +8.34…

NASDAQ Adv/Dec 1772/1149. …NYSE Adv/Dec 1627/1334.

03:30PM ET

[BRIEFING.COM]

Energy Settlement Prices:

August Crude Oil futures rose $0.54 (0.74%) to $73.91/barrel

August Natural Gas settled $0.08 lower (-2.72%) at $2.86/MMBtu

July RBOB Gasoline settled unch at $2.1/gallon

July Heating oil futures settled $0.02 lower (-0.92%) at $2.16/gallon

Metals Settlement Prices:

Aug gold settled today's session down $9.10 (0.73%) at $1241.7/oz

Sept silver settled today's session $0.03 lower (2.16%) at $15.84/oz

Sept copper settled $0.03 lower (1.01%) at $2.94/lb

Agriculture Settlement Prices:

Sept corn settled $0.03 higher at $3.48/bushel

Sept wheat settled $0.04 higher at $4.82/bushel

Aug soybeans settled $0.09 lower at $8.53/bushe

Dow: -23.44… | Nasdaq: +31.94… | S&P: +0.53…

NASDAQ Adv/Dec 1667/1307. …NYSE Adv/Dec 1472/1475.

02:55PM ET

[BRIEFING.COM] The S&P 500 (-0.1%) touched positive territory for the first time today in recent trading. Meanwhile, the tech-heavy Nasdaq is up 0.3%.

Looking ahead, there aren't any notable earnings reports due out this week, but the Employment Situation report for June will be released on Friday. The Briefing.com consensus expects the report will show the addition of 195,000 nonfarm payrolls, a 0.3% increase in average hourly earnings, and an unemployment rate of 3.8%, unchanged from May.

Tomorrow's trading session will end early (1:00 PM ET), and markets will be closed on Wednesday for the Fourth of July.

Dow: -51.28… | Nasdaq: +23.81… | S&P: -2.36…

NASDAQ Adv/Dec 1521/1366. …NYSE Adv/Dec 1384/1572.

02:25PM ET

[BRIEFING.COM] The major averages continue to steadily climb to their best levels. The Nasdaq Composite now holds a 0.4% gain into the latter half of Monday while the Dow and the S&P have trimmed their losses in half since our last update.

Checking in once again on the S&P 500 sectors, it's been widely covered that heavyweights financials (+0.3%) and information technology (+0.6%) buck the broader market trend. On the flip side, the energy (-1.9%), lightly-weighted real estate (-1.1%), and consumer staples (-0.7%) groups represent the worst performers.

In that vein, the energy sector is pressured today despite a mostly flat trade in WTI crude oil futures. At one point this morning, futures were down as much as 1.4% following comments from President Donald Trump who stated he's struck a deal with Saudi Arabia to increase output by up to two million barrels per day. Energy bellwethers Exxon Mobil (XOM 81.34, -1.39, -1.7%), Chevron (CVX 123.81, -2.62, -2.1%), and Schlumberger (SLB 65.46, -1.57, -2.3%) all lose worse than 1% today. Broadly, the iShares US Energy ETF (IYE 41.07, -0.86, -2.1%) is poised to fall worse than 2% today, extending its decline from late-May highs to about 5.9%.

After ending Friday near the top of the sector standings real estate names have given back a portion of their strength to begin the week. Constituents Simon Properties (SPG 168.29, -1.89, -1.1%), Prologis (PLD 64.42, -1.27, -1.9%), and Weyerhaeuser (WY 36.08, -0.38, -1.0%) all shed more than 1% on Monday. On the whole, the Real Estate Sector SPDR (XLRE 32.38, -0.33, -1.0%) has been faring quite well these past few weeks, up nearly 7% since mid-May; today's losses, though, serve as a modest reality check as tepid participation among the more widely-held sectors has trickled down to real estate.

Lastly, consumer staples names CVS (CVS 64.83, +0.48, +0.8%), and Walgreens Boots Alliance (WBA 60.74, +0.72, +1.2%) buck the broader sector trend, recouping a portion of last week's Amazon (AMZN 1,705.74, +5.94, +0.4%) PillPack-related losses. The majority of the sector is in the red, though, as bellwethers Wal-Mart (WMT 83.79, -1.85, -2.2%), Kraft Heinz (KHC 61.91, -0.91, -1.5%), and Tyson Foods (TSN 66.64, -2.21, -3.2%) all limp into the holiday.

Dow: -51.81… | Nasdaq: +29.24… | S&P: -4.16…

NASDAQ Adv/Dec 1510/1354. …NYSE Adv/Dec 1385/1578.

01:55PM ET

[BRIEFING.COM] The tech-heavy Nasdaq Composite sits near HoDs, up about 0.2%, while the Dow and the S&P lose about 0.4% apiece.

Gold futures began the holiday-shortened week with losses that took the yellow metal back to 2018 lows; all told, gold settled about 1% lower to start July at $1,241.70/oz. Gold was pressured, among other things, by a decent session out of the dollar.

The U.S. Dollar Index adds about 0.5% at this juncture to 95.07.

Dow: -100.69… | Nasdaq: +9.97… | S&P: -11.01…

NASDAQ Adv/Dec 1430/1437. …NYSE Adv/Dec 1281/1677.

01:35PM ET

[BRIEFING.COM] The major U.S. indices have slid back lower since our last update as stocks drag on the first day of the abbreviated trading week.

A look inside the Dow Jones Industrial Average shows that Nike (NKE 77.27, -2.41), Wal-Mart (WMT 83.51, -2.14), & Chevron (CVX 123.79, -2.64) are underperforming. Nike is the Dow's biggest decliner as shares pullback following Friday's 11% earnings-driven spike. Helping to apply some pressure to shares, Tennis legend Roger Federer this morning revealed an apparel partnership with Uniqlo, replacing a prior deal the athlete had maintained with Nike.

Conversely, Goldman Sachs (GS 221.75, +1.18) is the best-performing Dow component as financials display relative strength.

Starting off the month and quarter with one step backwards, the DJIA is now down 2.46% this year.

Dow: -157.51… | Nasdaq: -20.27… | S&P: -14.84…

NASDAQ Adv/Dec 1280/1581. …NYSE Adv/Dec 1127/1818.

12:55PM ET

[BRIEFING.COM] Stocks have extended last week's losses today, with energy shares pacing the retreat. The S&P 500 is down 0.4%, dropping below its 50-day moving average. The Dow Jones Industrial Average is down 0.5%, the tech-heavy Nasdaq Composite is lower by 0.2%, and the small-cap Russell 2000 has shed 0.3%.

Trade-related headlines are still in the mix today after President Trump told FOX News over the weekend that he will not back down on China tariffs. The president also repeated his threat to impose tariffs on auto imports from the European Union, to which the EU responded by vowing to impose retaliatory tariffs on as much as $300 billion worth of U.S. products.

The energy sector (-1.4%) is hovering at the bottom of today's sector standings, even though crude prices have rebounded following a lower start. WTI crude futures are currently flat at $74.10 per barrel, but were down as much as 1.4% earlier after President Trump said he's struck a deal with Saudi Arabia to increase output by up to two million barrels per day.

Almost all S&P 500 sectors are in the red, but the financial space (unch) has managed to keep near its unchanged mark. Meanwhile, the information technology group (-0.1%) -- the only sector with more influence than financials -- is also showing relative strength with tech giants Apple (AAPL 185.71, +0.60) and Microsoft (MSFT 98.91, +0.30) sporting modest gains.

In corporate news, Tesla (TSLA 333.67, -9.31) has reversed earlier gains, now down 2.7%, even though the electric automaker said it hit its production target of 3,000 Model 3s in the last seven days of the second quarter. Also of note, Dell is reportedly looking to return to the public markets after going private five years ago.

Elsewhere, U.S. Treasuries are modestly lower today, pushing the benchmark 10-yr yield one basis point higher to 2.86%. The U.S. Dollar Index up 0.6% at 94.79, and the CBOE Volatility Index has risen 1 point, or 6.5%, to 17.09.

Reviewing today's economic data, which was limited to the ISM Manufacturing Index for June and the Construction Spending report for May:

The ISM Index for June increased to 60.2 from an unrevised reading of 58.7 in May, while the Briefing.com consensus expected a reading of 58.5.

Construction Spending rose 0.4% in May, while the Briefing.com consensus expected an increase of 0.6%. The April reading was revised to +0.9% from +1.8%.

Dow: -93.05… | Nasdaq: -8.28… | S&P: -8.59…

NASDAQ Adv/Dec 1344/1502. …NYSE Adv/Dec 1243/1696.

12:25PM ET

[BRIEFING.COM] The S&P 500 has nearly returned to its opening level, now down 0.5%.

All sectors are in the red this afternoon, with energy (-1.4%) and materials (-1.0%) leading the retreat. Meanwhile, within the consumer discretionary sector (-0.8%), 21st Century Fox (FOXA 49.28, -0.41) hit a new session low in recent trading following reports that Comcast (CMCSA 32.97, +0.35) is not likely to counter Disney's (DIS 104.35, -0.46) offer for Fox's entertainment assets.

In currencies, the U.S. Dollar Index has climbed 0.6% to 94.77 today. The greenback is particularly strong against the euro, up 0.7% at 1.1606.

Dow: -142.64… | Nasdaq: -18.29… | S&P: -12.22…

NASDAQ Adv/Dec 1225/1604. …NYSE Adv/Dec 1110/1810.

11:55AM ET

[BRIEFING.COM] Equity indices have slipped from their session highs in recent trading, with the Dow Jones Industrial Average now down 0.5%.

Transports are outperforming today, evidenced by the 0.3% increase in the Dow Jones Transportation Average. However, the outperformance of transports hasn't been evident in the broader industrial sector, which is hovering roughly in line with the broader market, down 0.4%. Industrial giant General Electric (GE 13.24, -0.37) is especially weak today, down 2.7%, after rallying 4.3% last week.

In Europe, the major bourses finished Monday on a lower note, losing between 0.6% and 1.2%. The Euro Stoxx 50 is now down 3.8% for the year.

Dow: -125.54… | Nasdaq: -21.07… | S&P: -10.51…

NASDAQ Adv/Dec 1128/1677. …NYSE Adv/Dec 1104/1806.

11:25AM ET

[BRIEFING.COM] Equity indices are hovering near their recent levels, showing losses between 0.1% and 0.4%.

The top-weighted technology sector (unch) is hovering near the top of today's sector standings, with giants like Facebook (FB 194.75, +0.43), Microsoft (MSFT 99.02, +0.40), and Apple (AAPL 186.37, +1.28) sporting gains between 0.2% and 0.7%. Chipmakers are lagging though, evidenced by a 0.8% decrease in the PHLX Semiconductor Index.

Meanwhile, the financials space (-0.1%) is also outperforming. Within the space, Wells Fargo (WFC 55.62, +0.18) is among the best performers with a gain of 0.4% after Morgan Stanley upgraded WFC shares to 'Equal-Weight' from 'Underweight' this morning.

Dow: -91.50… | Nasdaq: -9.35… | S&P: -7.59…

NASDAQ Adv/Dec 1195/1611. …NYSE Adv/Dec 1167/1713.

10:55AM ET

[BRIEFING.COM] Equity indices have rebounded since opening solidly lower, cutting their losses in half. The S&P 500 is now down just 0.3%.

Three sectors, including financials (+0.2%), technology (+0.2%), and utilities (+0.1%), are trading in the green, but the rest are in negative territory. The energy space (-1.4%) is the weakest performer by a decent margin as crude futures slip from a three-and-a-half year high. WTI crude futures are down 0.6% at $73.72/bbl.

In the bond market, U.S. Treasuries have reversed course and are now in the red. The yield on the benchmark 10-yr note is now up one basis point at 2.86%.

Dow: -79.05… | Nasdaq: -6.98… | S&P: -7.29…

NASDAQ Adv/Dec 1309/1468. …NYSE Adv/Dec 1199/1655.

10:35AM ET

[BRIEFING.COM]

Commodities are starting the day off lower

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently -1.3% at 86.27

Dollar index is currently +0.6% at 94.80

Looking at energy...

Aug WTI crude oil futures are now -$0.32 at $73.83/barrel

In other energy, Aug natural gas is -$0.07 at $2.86/MMBtu

Moving on to metals...

Aug gold is currently -$6.50 at $1248.00/oz, while Jul silver is -$0.27 at $15.93/oz

Jul copper is now -$0.03 at $2.94/lb

Dow: -100.14… | Nasdaq: -4.08… | S&P: -7.58…

NASDAQ Adv/Dec 1225/1533. …NYSE Adv/Dec 1140/1688.

10:05AM ET

[BRIEFING.COM] Equity indices are still lower, but have ticked up from their opening levels. The S&P 500 is down 0.3%.

Just in, the ISM Index for June increased to 60.2 from an unrevised reading of 58.7 in May, while the Briefing.com consensus expected a reading of 58.5.

Separately, Construction Spending rose 0.4% in May, while the Briefing.com consensus expected an increase of 0.6%. The April reading was revised to +0.9% from +1.8%.

Dow: -147.65… | Nasdaq: -31.05… | S&P: -12.99…

NASDAQ Adv/Dec 900/1809. …NYSE Adv/Dec 833/1932.

09:45AM ET

[BRIEFING.COM] The major averages are down in the opening minutes of today's session, showing losses of around 0.5% apiece.

10 of 11 S&P 500 sectors are in the red, with utilities (+0.3%) being the lone advancer. The energy sector (-1.6%) is the worst-performing group, followed from a distance by the materials space (-0.9%). No other group is down more than 0.7%.

As a reminder, the ISM Manufacturing Index for June (Briefing.com consensus 58.5) and the Construction Spending report for May (Briefing.com consensus +0.6%) will be released at 10:00 AM ET.

Dow: -161.15… | Nasdaq: -42.16… | S&P: -14.35…

NASDAQ Adv/Dec 782/1887. …NYSE Adv/Dec 792/1953.

09:14AM ET

[BRIEFING.COM] S&P futures vs fair value: -14.30. Nasdaq futures vs fair value: -45.80.

The S&P 500 futures are trading 14 points, or 0.5%, below fair value as trade war fears continue to weigh.

The U.S. is set to impose tariffs on $34 billion worth of Chinese goods on Friday, to which Beijing has promised retaliatory tariffs on an equal amount of U.S. goods. Meanwhile, the EU has threatened to hit the U.S. with nearly $300 billion worth of retaliatory tariffs if the U.S. moves forward with duties on European automobiles.

In corporate news, Dell is reportedly planning to return to the public markets after going private five years ago, and Tesla (TSLA 363.14, +20.19) is up 6.0% in pre-market trading after CEO Elon Musk tweeted that the company produced 7,000 cars in seven days -- although it's unclear how many were Model 3s.

On the data front, investors will receive two pieces of economic data today, the ISM Manufacturing Index for June (Briefing.com consensus 58.5) and the Construction Spending report for May (Briefing.com consensus +0.6%), both of which will be released at 10:00 AM ET.

Elsewhere, U.S. Treasuries are slightly higher, with the benchmark 10-yr yield down one basis point at 2.84%.

08:53AM ET

[BRIEFING.COM] S&P futures vs fair value: -15.30. Nasdaq futures vs fair value: -48.30.

The S&P 500 futures are trading 15 points, or 0.6%, below fair value.

Equity indices in the Asia-Pacific region began the week on a mostly lower note, but overall trading volume was reduced as Hong Kong's Hang Seng was closed for SAR Establishment Day. South Korean press speculated that the country will not meet its 3.0% GDP growth target due to sluggish employment, investment, and consumption. The Reserve Bank of Australia will hold a policy meeting overnight, but the market now expects the RBA to maintain rates at their current levels for another year.

In economic data:

China's June Manufacturing PMI 51.5 (expected 51.6; last 51.9) and non-Manufacturing PMI 55.0 (expected 54.7; last 54.9). June Caixin Manufacturing PMI 51.0 (expected 51.1; last 51.1)

Japan's June Manufacturing PMI 53.0 (expected 53.1; last 53.1). Q2 Tankan Large Non-Manufacturers Index 24 (expected 23; last 23) and Q2 Tankan Large Manufacturers Index 21 (expected 22; last 24). Q2 Tankan All Big Industry CAPEX +13.6% (expected 9.3%; last 2.3%)

South Korea's June trade surplus $6.30 billion (last surplus of $6.61 billion). June Imports +10.7% year-over-year (expected 11.4%; last 14.5%) and June Exports -0.1% year-over-year (expected 0.4%; last -1.5%). Nikkei June Manufacturing PMI 49.8 (last 48.9)

Australia's June AIG Manufacturing Index 57.4 (last 57.5). June ANZ Job Advertisements -1.7% month-over-month (last 1.4%)

India's June Nikkei Markit Manufacturing PMI 53.1 (expected 51.4; last 51.2)

---Equity Markets---

Japan's Nikkei fell 2.2% to levels from mid-April. Kikkoman, Furukawa, JGC, Konami, Familymart, TOTO, Bridgestone, Okuma, J Front Retailing, and Yamaha lost between 3.3% and 6.3%.

Hong Kong's Hang Seng was closed.

China's Shanghai Composite dropped 2.5%. Xinjiang Tianrun Dairy, Zhengzhou Yutong Bus, China Fortune Land Development, Tongwei, and Shanghai Jinjiang International Hotels Development posted losses between 7.4% and 10.1%.

India's Sensex shed 0.5%. Bharti Airtel, Adani, Hero MotoCorp, Mahindra & Mahindra, Larsen & Toubro, Reliance Industries, and Tata Motors dropped between 0.8% and 3.5%.

Major European indices trade in negative territory to begin the week. The optimism that followed last week's EU summit dissipated quickly after Germany's Interior Minister Horst Seehofer offered to resign due to continued inability to find common ground with Chancellor Angela Merkel's CDU on a plan for immigration. Mr. Seehofer is reportedly meeting with Chancellor Merkel today before making a final decision. EU officials have warned the U.S. Department of Commerce that up to $300 billion worth of imports from the U.S. could be impacted by tariffs.

In economic data:

Eurozone June Manufacturing PMI 54.9 (expected 55.0; last 55.0) and May Unemployment Rate 8.4% (expected 8.5%; last 8.5%)

Germany's June Manufacturing PMI 55.9, as expected (last 55.9)

UK's June Manufacturing PMI 54.4 (expected 54.1; last 54.3)

France's June Manufacturing PMI 52.5 (expected 53.1; last 53.1)

Italy's June Manufacturing PMI 53.3 (expected 52.6; last 52.7) and Monthly Unemployment Rate 10.7% (expected 11.1%; last 11.0%)

Spain's June Manufacturing PMI 53.4 (expected 53.6; last 53.4)

Swiss June SVME PMI 61.6 (expected 61.1; last 62.4) and May Retail Sales -0.1% year-over-year (expected 2.6%; last 2.9%)

---Equity Markets---

Germany's DAX is down 0.5%. Fresenius, Allianz, Lufthansa, Adidas, Henkel, SAP, and Deutsche Bank show losses between 0.5% and 1.9% while automakers are mixed. Volkswagen is little changed while BMW and Daimler hold respective gains of 0.8% and 2.0%.

France's CAC has given up 0.8%. TechnipFMC, ArcelorMittal, Airbus Group, Kering, L'Oreal, Vivendi, and Hermes are down between 0.9% and 2.4%. Financials like BNP Paribas, AXA, Credit Agricole, and Societe Generale hold losses between 0.3% and 0.9%.

UK's FTSE trades lower by 0.8%. Miners are among the laggards with Glencore, Antofagasta, BHP Billiton, Anglo American, Rio Tinto, and Fresnillo hold losses between 1.6% and 3.1%. Consumer names like Barratt Developments, Persimmon, ITV, Taylor Wimpey, and Sainsbury have slid between 1.3% and 2.4%.

08:25AM ET

[BRIEFING.COM] S&P futures vs fair value: -13.30. Nasdaq futures vs fair value: -47.30.

The S&P 500 futures are trading 13 points, or 0.5%, below fair value.

Today's trading session will mark the first of the third quarter. So far in 2018, only four of eleven sectors have advanced, including the consumer discretionary (+10.8%), technology (+10.2%), energy (+5.3%), and health care (+1.0%) groups. The other spaces show year-to-date losses between 1.0% and 10.8%.

As for the major averages, the Dow is down 1.8% year-to-date, while the S&P 500 and the Nasdaq are up 1.7% and 8.8%.

07:58AM ET

[BRIEFING.COM] S&P futures vs fair value: -11.30. Nasdaq futures vs fair value: -39.50.

Stocks look ready to extend last week's losses at the opening bell as trade war fears continue to weigh. The S&P 500 futures are currently trading 11 points, or 0.4%, below fair value. Last week, the S&P 500 lost 1.3% in total and finished Friday's session just a tick above its 50-day moving average.

The U.S. is set to impose tariffs on $34 billion worth of Chinese goods on Friday, to which Beijing has promised retaliatory tariffs on an equal amount of U.S. goods. Meanwhile, the EU has threatened to hit the U.S. with nearly $300 billion worth of retaliatory tariffs if the U.S. moves forward with duties on European automobiles.

Many nations released manufacturing data for the month of June this morning. Overall, the readings were fairly disappointing, with China, Japan, Australia, France, and Spain all missing estimates. In the U.S., the ISM Manufacturing Index for June (Briefing.com consensus 58.5) will be released at 10:00 AM ET, alongside the Construction Spending report for May (Briefing.com consensus +0.6%).

U.S. Treasuries are rallying this morning, sending yields lower across the curve; the benchmark 10-yr yield is down two basis points at 2.83%. Meanwhile, the U.S. Dollar Index is up 0.4% at 94.59, and WTI crude futures are flat at $74.13/bbl after President Trump said he's reached a deal with Saudi Arabia's King Salman to boost production by "maybe up to" two million barrels per day.

In U.S. corporate news:

Dell (private) is reportedly planning to return to the public markets after going private five years ago.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region began the week on a mostly lower note, but overall trading volume was reduced as Hong Kong's Hang Seng was closed for SAR Establishment Day. Japan's Nikkei -2.2%, China's Shanghai Composite -2.5%, India's Sensex -0.5%.

In economic data:

China's June Manufacturing PMI 51.5 (expected 51.6; last 51.9) and non-Manufacturing PMI 55.0 (expected 54.7; last 54.9). June Caixin Manufacturing PMI 51.0 (expected 51.1; last 51.1)

Japan's June Manufacturing PMI 53.0 (expected 53.1; last 53.1). Q2 Tankan Large Non-Manufacturers Index 24 (expected 23; last 23) and Q2 Tankan Large Manufacturers Index 21 (expected 22; last 24). Q2 Tankan All Big Industry CAPEX +13.6% (expected 9.3%; last 2.3%)

South Korea's June trade surplus $6.30 billion (last surplus of $6.61 billion). June Imports +10.7% year-over-year (expected 11.4%; last 14.5%) and June Exports -0.1% year-over-year (expected 0.4%; last -1.5%). Nikkei June Manufacturing PMI 49.8 (last 48.9)

Australia's June AIG Manufacturing Index 57.4 (last 57.5). June ANZ Job Advertisements -1.7% month-over-month (last 1.4%)

India's June Nikkei Markit Manufacturing PMI 53.1 (expected 51.4; last 51.2)

In news:

South Korean press speculated that the country will not meet its 3.0% GDP growth target due to sluggish employment, investment, and consumption.

The Reserve Bank of Australia will hold a policy meeting overnight, but the market now expects the RBA to maintain rates at their current levels for another year.

Major European indices trade in negative territory to begin the week. Germany's DAX -0.4%, France's CAC -0.8%, UK's FTSE -0.9%.

In economic data:

Eurozone June Manufacturing PMI 54.9 (expected 55.0; last 55.0) and May Unemployment Rate 8.4% (expected 8.5%; last 8.5%)

Germany's June Manufacturing PMI 55.9, as expected (last 55.9)

UK's June Manufacturing PMI 54.4 (expected 54.1; last 54.3)

France's June Manufacturing PMI 52.5 (expected 53.1; last 53.1)

Italy's June Manufacturing PMI 53.3 (expected 52.6; last 52.7) and Monthly Unemployment Rate 10.7% (expected 11.1%; last 11.0%)

Spain's June Manufacturing PMI 53.4 (expected 53.6; last 53.4)

Swiss June SVME PMI 61.6 (expected 61.1; last 62.4) and May Retail Sales -0.1% year-over-year (expected 2.6%; last 2.9%)

In news:

The optimism that followed last week's EU summit dissipated quickly after Germany's Interior Minister Horst Seehofer offered to resign due to continued inability to find common ground with Chancellor Angela Merkel's CDU on a plan for immigration. Mr. Seehofer is reportedly meeting with Chancellor Merkel today before making a final decision.

EU officials have warned the U.S. Department of Commerce that up to $300 billion worth of imports from the U.S. could be impacted by tariffs.

07:31AM ET

[BRIEFING.COM] S&P futures vs fair value: -13.00. Nasdaq futures vs fair value: -39.80.

07:05AM ET

[BRIEFING.COM] S&P futures vs fair value: -13.30. Nasdaq futures vs fair value: -42.30.

07:05AM ET

[BRIEFING.COM] Nikkei...21811.93...-492.60...-2.20%. Hang Seng...Holiday.........

07:05AM ET

[BRIEFING.COM] FTSE...7562.95...-74.00...-1.00%. DAX...12264.39...-42.50...-0.40%.

04:30PM ET

[BRIEFING.COM] Stocks got off to a good start on Friday, but gave back nearly everything during the final hour of trading. The S&P 500 was up 1.0% at its best mark of the day, but ended with a gain of just 0.1%, closing a tick above its 50-day moving average. The Nasdaq also added 0.1%. The Dow climbed 0.2%.

Financials led the market higher out of the gate after the Fed cleared most big banks to increase their dividends and share buybacks. However, the heavily-weighted sector faded as the day went along, entirely retracing a gain of 1.8%, and ended lower by 0.1%.

Despite the disappointing finish, eight of eleven sectors closed Friday in the green. Energy (+0.7%) was the top-performing space as crude prices climbed for a fourth straight session. WTI crude futures advanced 1.0% to $74.12 per barrel, hitting a new three-and-a-half year high and locking in a weekly gain of 8.1%.

In corporate news, Nike (NKE 79.68, +7.98) spiked 11.1%, hitting a new all-time high, after reporting better-than-expected earnings and revenues and announcing a $15 billion share repurchase program. Conversely, General Motors (GM 39.40, -1.12) struggled, losing 2.8%, after warning President Trump that the proposed tariffs on imported vehicles could lead to "a smaller GM". It's worth noting that selling in the broader market started picking up around the same time that GM made the announcement, although it's unlikely that it was the sole cause as financials led the reversal.

In politics, Fox News correspondent Maria Bartiromo reported that President Trump is working on a phase two of his tax plan and is considering cutting the corporate tax rate to 20% from 21%. Separately, European Union leaders reached a deal on a migration, which has been an especially contentious issue since the Syrian refugee crisis.

Reviewing Friday's economic data, which included Personal Income, Personal Spending, and PCE Prices for May, the Chicago PMI for June, and the final reading of the University of Michigan Consumer Sentiment Index for June:

Personal income climbed 0.4% in May (Briefing.com consensus +0.4%) following a revised increase of 0.2% in April (from 0.3%). Meanwhile, personal spending rose 0.2% in May (Briefing.com consensus +0.4%) following a revised increase of 0.5% in April (from 0.6%). The PCE Price Index rose 0.2% in May (Briefing.com consensus +0.2%), and the core PCE Price Index, which excludes food and energy, increased 0.2% (Briefing.com consensus +0.2%). Year-over-year, the core PCE Price Index is up 2.0%, up from 1.8% in the last reading.

The key takeaway from the report is twofold: (1) Real PCE was flat, which is likely to prompt some downward revisions to Q2 GDP forecasts and (2) the price indexes are moving in the direction anticipated by the Fed, which means the Fed is also likely to keep moving the fed funds rate higher as anticipated.

The Chicago PMI for June hit 64.1 (Briefing.com consensus 61.0), up from an unrevised 62.7 in May.

The key takeaway from the report is that manufacturers are experiencing a slowdown in production activity on account of longer supplier lead times that have been impacted by elevated input prices.

The final reading of the University of Michigan Consumer Sentiment Index for June slipped to 98.2 (Briefing.com consensus 99.0) from 99.3 in the preliminary reading.

The key takeaway from the report is that the downshift from the preliminary reading was driven primarily by tariff concerns, yet favorable assessments of jobs and incomes were a mitigating influence that left the overall index little changed from the prior month.

Looking ahead to Monday, investors will receive the June ISM Manufacturing Index and the May Construction Spending report.

Nasdaq Composite +8.8% YTD

Russell 2000 +7.0% YTD

S&P 500 +1.7% YTD

Dow Jones Industrial Average -1.8% YTD

Week In Review: Trade Tensions Strike Again

U.S. equities declined for the second week in a row as investors continued to focus on U.S.-China trade tensions. The S&P 500 and the Dow Jones Industrial Average dropped 1.3% apiece, while the tech-heavy Nasdaq Composite slid 2.4%. Small caps were hit especially hard, sending the Russell 2000 lower by 2.5%.

Trade war fears weighed at the start of the week due to reports that the White House is looking to bar Chinese companies from investing in U.S. tech firms. The Trump administration first responded to the reports with a mixed message; Treasury Secretary Steven Mnuchin said the White House is targeting all countries, not just China, while President Trump's top trade adviser, Peter Navarro, said the administration doesn't have any plans to impose investment restrictions, regardless of country.

However, the administration eventually cleared things up, deciding to defer foreign investment regulation to the Committee on Foreign Investment in the United States (CFIUS). That decision was seen as a positive alternative to direct White House intervention and helped the equity market rebound in the second half of the week.

Separately, the U.S. State Department threatened to impose powerful sanctions on countries that don't cut oil imports from Iran to "zero" by November 4. That headline, paired with a larger-than-expected draw in U.S. crude inventories (9.9 million barrels), pushed crude prices back to a three-and-a-half year high. WTI crude futures added 8.1% for the week, closing at $74.12 per barrel.

Also out of Washington, Supreme Court Justice Anthony Kennedy announced his retirement, effective July 31. Although he identifies as a conservative, Mr. Kennedy has often sided with his liberal colleagues. His retirement gives President Trump the chance to strengthen the court's conservative majority.

In corporate news, Amazon (AMZN) made headlines after announcing a deal to acquire online pharmacy start-up PillPack. That news sent shares of drug distributors like CVS Health (CVS) and Walgreens Boots Alliance (WBA) solidly lower. Amazon also announced it is inviting entrepreneurs to form small companies to carry packages over the last leg of the delivery journey.

Elsewhere, General Electric (GE) announced plans to spin off its health care business and to sell its 62.5% stake in oil and gas company Baker Hughes (BHGE); Walt Disney (DIS) won DOJ approval to buy most of Fox's assets for $71.3 billion, subject to the condition that Disney sells 22 regional sports networks; and Nike (NKE) spiked to a new record on Friday after beating both top and bottom line estimates and announcing a new $15 billion share repurchase program.

As for this week's S&P sector standings, utilities (+2.3%), telecom services (+1.2%), real estate (+1.1%), and energy (+1.0%) were the top-performing groups, while the heavily-weighted technology (-2.2%), financials (-1.9%), consumer discretionary (-1.9%), and health care (-1.8%) sectors finished at the back of the pack.

Dow: +55.36… | Nasdaq: +6.62… | S&P: +2.06…

NASDAQ Adv/Dec 1629/1372. …NYSE Adv/Dec 1692/1219.

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Rebuttal to Emmett Moore via TheStrategyLab.com Review

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 Where did wrbtrader go? | Elite Trader

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=307&t=3770 The Strategy Lab: Valforex - The Manipulative Review Scam

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3676 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htm Advance WRB Analysis Tutorial Chapters 4 - 12

@ http://www.thestrategylab.com/WRBAnalysisTutorials.htmDisclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis. The risk of loss can be substantial. Therefore, you must carefully consider if trading is suitable for you within the context of your financial condition. TheStrategyLab.com is an education and research site. The resources on this site are provided for informational purposes only and should not be used to replace professional educational and professional research because we are retail traders only. TheStrategyLab.com does not accept liability for your use of the website and its resources.

We make no guarantees of success and your level of success is dependent upon other factors including your skill as a trader, knowledge, financial condition, market conditions and other factors. Trading is stressful and you should always consult a doctor in all matters relating to physical and mental health of you & your family because trading can impact beyond your financial condition regardless if you're a profitable or losing trader. Also, you can read our full disclaimer statement @ http://www.thestrategylab.com/Disclaimer.htmBest Regards,

M.A. Perry

Online user name

wrbtrader (more info about me)

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850 & http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading (no indicators)

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com