Price Action Trade Results of M.A. Perry

Price Action Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htm &

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Users of WRB Analysis Real-Time Trades - TheStrategyLab Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Users of WRB Analysis Reviews / Accolades / Testimonials: http://www.thestrategylab.com/Accolades.htm Review of TheStrategyLab: http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 &

http://www.thestrategylab.com/thestrategylab-reviews.htmPrice Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Telephone: +1 708 572-4885

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

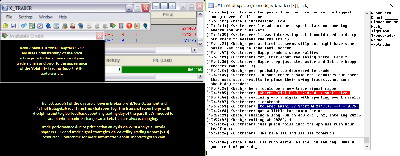

Attachment:

062518-wrbtrader-Price-Action-Trading-Broker-PnL-Statement-Profit+6862.50.png [ 137.27 KiB | Viewed 335 times ]

062518-wrbtrader-Price-Action-Trading-Broker-PnL-Statement-Profit+6862.50.png [ 137.27 KiB | Viewed 335 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini ES ($ES_F) futures @

$6862.50 dollars or +137.25 points, Emini RTY ($RTY_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6862.50 dollars Today's Trade Log & Price Action Analysis is archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=181&t=2856 All of my trades are posted

real-time at the above link for today's archive chat log in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader along with the real-time trades by other users of WRB Analysis for anyone to do a real-time review (you must be a member of the chat room for a real-time review). Also, as stated since the birth of the free chat room TheStrategyLab...we are

not a signal calling trade alert room. Thus, there is no trader telling you what to trade, when to buy and when to sell. I'm the moderator (I keep the peace between members) and my own live trades are posted within 3.2 seconds on average

after the trade confirmation in my broker trade execution platform via an

auto script to minimize delays in posting of my trades.

You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion at the

above direct link to the

archived chat log.

In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility...all key concepts from the WRB Analysis free study guide even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads.

Quote:

These real-time trades involves price action concepts from

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always

backtesting new concepts of WRB Analysis, new trade entry rules, new trade management rules, new position size management rules before application in real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades and

prior to sharing the new concepts with fee-base clients...living up to the name of my website.

TheStrategyLab.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The

purpose of TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. If you join the free chat room and then you decide to

not post any WRB Analysis about the price action or you decide to not post your trades or you decide to be silent (lurk without saying a word about today's markets)...you're not using the free chat room properly to help improve your trading and the chat room will be

useless to you. In addition, we

highly recommend that you use the free chat room with a professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they can provide you with the

quantitative statistical analysis of your trading. You can then download your results and post them in your private thread here at the forum.

Access instructions for the free chat room

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=352&t=3733 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini RTY futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

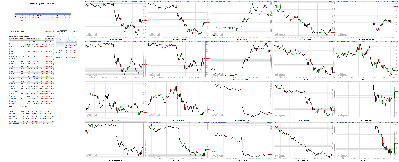

Attachment:

062518-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.85 MiB | Viewed 365 times ]

062518-TheStrategyLab-Chat-Room-Key-Markets.png [ 1.85 MiB | Viewed 365 times ]

click on the above image to view today's price action of key markets discussed by members of TheStrategyLab chat room or private thread discussions The Market at 04:30PM ETDow: -328.09… | Nasdaq: -160.81… | S&P: -37.81…

NASDAQ Vol: 2.4 bln… Adv: 709… Dec: 2300…

NYSE Vol: 900.0 mln… Adv: 711… Dec: 2231…

Moving the Market

White House reportedly looking to bar Chinese companies from investing in U.S. tech firms; President Trump threatens U.S. trading partners with "more than reciprocity"

Market trims losses after Peter Navarro, President Trump's top trade adviser, says the White House has no plans to impose investment restrictions

Dow drops below its 200-day moving average for first time in two years

Sector Watch

Strong: Consumer Staples, Utilities, Telecom Services, Real Estate

Weak: Consumer Discretionary, Energy, Technology

04:30PM ET

[BRIEFING.COM] Stocks got hit pretty hard on Monday amid escalated fears that the U.S. and China are headed towards a full-blown trade war. Losses were broad-based, with declining issues outnumbering advancing issues 3 to 1 on the New York Stock Exchange. However, the market did settle notably above session lows thanks to some late comments from the White House.

The S&P 500 lost 1.4%, but did manage to close a tick above its 50-day moving average despite spending most of the session below the key technical level. The Dow, meanwhile, lost 1.3% and suffered some technical damage, closing below its 200-day moving average for the first time in two years. The Nasdaq was particularly weak, losing 2.1%, as tech shares struggled, and the Russell 2000 lost 1.7%.

Trade war fears were escalated after a weekend report from The Wall Street Journal that the Trump administration is looking to bar Chinese companies from investing in U.S. technology firms. Treasury Secretary Steven Mnuchin refuted the report in a tweet on Monday morning, saying the administration is targeting all countries attempting to "steal our technology", not just China.

Then things got a little confusing.

Peter Navarro, President Trump's top trade adviser, made a late-day appearance on CNBC, saying the sell off was a "very large overreaction" and insisting that the White House has no plans to impose investment restrictions. Mr. Navarro's comments boosted the market, cutting the S&P 500's loss from 2.0% at its session low to 1.2% at its afternoon high.

Nine of eleven S&P sectors finished Monday in negative territory, with growth-sensitive groups being the weakest performers. The top-weighted technology sector (-2.3%) finished at the bottom of the sector standings. Chipmakers were particularly weak, evidenced by a 3.1% drop in the Philadelphia Semiconductor Index, and the tech-heavy FAANG names really struggled; Facebook (FB 196.35, -5.39), Apple (AAPL 182.17, -2.75), Amazon (AMZN 1663.15, -52.52), Alphabet (GOOG 1124.81, -30.67), and Netflix (NFLX 384.48, -26.61) lost between 1.5% and 6.5%.

Elsewhere, Harley-Davidson (HOG 41.57, -2.64) tumbled 6.0% after announcing it won't raise prices to cover the cost of the EU's reciprocal tariffs; instead, it'll work to shift production to international facilities. Carnival (CCL 58.54, -4.99) was also a notable laggard, losing 7.9%, after disappointing guidance outweighed upbeat quarterly results.

On a positive note, the countercyclical consumer staples (+0.4%) and utilities (+1.7%) sectors closed Monday in the green. Within the consumer staples space, Campbell Soup (CPB 42.23, +3.63) surged 9.4% and Kraft Heinz (KHC 63.32, +0.11) added 0.2% following a NY Post report that Kraft might be interested in acquiring the soup maker.

U.S. Treasuries rose amid the flight to safety, sending yields lower across the curve. The yield on the benchmark 10-yr Treasury note slipped two basis points to 2.88%. Meanwhile, the CBOE Volatility Index, often referred to as the "investor fear gauge", spiked 28.8%, hitting its highest level since late April.

Reviewing Monday's economic data, which was limited to the New Home Sales report for May:

New Home Sales in May hit an annualized rate of 689,000, which is above the Briefing.com consensus of 666,000. The April reading was revised to 646,000 (from 662,000).

The key takeaway from the report is that there wasn't any growth in new home sales outside the South region. That is the largest region for new home sales, though, and where there is a concentration of lower-priced housing markets, which helps explain the year-over-year drop in median and average selling prices.

On Tuesday, investors will receive the Case-Shiller 20-City Index for April and the Conference Board's Consumer Confidence Index for June.

Nasdaq Composite +9.1% YTD

Russell 2000 +8.0% YTD

S&P 500 +1.6% YTD

Dow Jones Industrial Average -1.9% YTD

Dow: -328.09… | Nasdaq: -160.81… | S&P: -37.81…

NASDAQ Adv/Dec 709/2300. …NYSE Adv/Dec 711/2231.

03:30PM ET

[BRIEFING.COM]

Energy Settlement Prices:

August Crude Oil futures fell $0.42 (-0.61%) to $68.17/barrel

August Natural Gas settled $0.02 lower (-0.68%) at $2.92/MMBtu

July RBOB Gasoline settled $0.02 lower (-0.98%) at $2.03/gallon

July Heating oil futures settled $0.01 lower (-0.47%) at $2.11/gallon

Metals Settlement Prices:

Aug gold settled today's session down $1.60 (0.13%) at $1269.10/oz

Jul silver settled today's session $0.04 lower (0.79%) at $16.33/oz

Jul copper settled $0.04 lower (1.32%) at $2.99/lb

Agriculture Settlement Prices:

July corn settled $0.08 lower at $3.49/bushel

July wheat settled $0.11 lower at $4.91/bushel

July soybeans settled $0.23 lower at $8.74/bushel

Dow: -427.77… | Nasdaq: -193.43… | S&P: -48.11…

NASDAQ Adv/Dec 648/2378. …NYSE Adv/Dec 638/2287.

02:55PM ET

[BRIEFING.COM] Equities have hit new session lows in recent trading. The tech-heavy Nasdaq is now down 2.7%, trimming its June gain to 0.6%.

Shares of American Express (AXP 98.17, +0.93) are outperforming today, up 1.0%, after the Supreme Court threw out a government lawsuit that accused the credit card company of hindering competition. The ruling could insulate names like Facebook (FB 193.80, -7.94) and Amazon (AMZN 1654.66, -61.03) from similar antitrust suits.

Elsewhere, the CBOE Volatility Index, often referred to as the "investor fear gauge", has spiked 30.7% today, hitting its highest level since late April.

Dow: -481.55… | Nasdaq: -211.92… | S&P: -54.77…

NASDAQ Adv/Dec 619/2289. …NYSE Adv/Dec 660/2246.

02:30PM ET

[BRIEFING.COM] The broader markets inch lower in recent trade, though still stand modestly higher compared to LoDs.

The losses in the S&P 500 information technology (-.2.7%) group have been well documented today, but glancing once more at the sector standings it, too, is difficult to look past the energy (-2.1%) and consumer discretionary (-2.2%) performances.

A modest move lower in WTI crude oil futures -- down 0.6% at $68.17/barrel -- today leaves many E&P names in the red -- OAS -3.96%, FANG -2.98%, XEC -2.70%, SWN -2.10%, EGN -2.01%, SM -1.51%, MTDR -1.26%, PE -0.91%. What's more, the top 10 weighted names in the iShares US Energy ETF (IYE 40.85, -0.88, -2.1%) portfolio fall worse than 1% on Monday with the steepest losses out of Exxon Mobil (XOM 79.72, -1.65), Chevron (CVX 122.85, -2.25), and Schlumberger (SLB 65.48, -1.10).

On the other hand, consumer discretionary names are reeling on Monday too. Top dog Amazon (AMZN 1,659.05, -56.62) sheds 3.3%, while Comcast (CMCSA 33.00, -0.80, -2.4%), Disney (DIS 104.00, -2.34, -2.2%), McDonald's (MCD 159.63, -4.92, -3.0%), and Netflix (NFLX 385.78, -25.30, -6.2%) don't have much to show for action on Monday either. Further, we're seeing multi-year low in coffee giant Starbucks (SBUX 50.52, -0.72, -1.4%) and a 52-week low in cruise name Carnival (CCL 59.31, -4.21, -6.6%). CCL's woes have, too, been well documented today but it may be worth pointing out that SBUX's struggles may likely be at least in part due to a cautious note out of sell side shop Wedbush where analysts no longer see risks to lowered FY18 expectations while also they do not see near-term drivers of positive revisions able to materialize.

Dow: -344.93… | Nasdaq: -181.02… | S&P: -40.97…

NASDAQ Adv/Dec 681/2219. …NYSE Adv/Dec 708/2178.

02:00PM ET

[BRIEFING.COM] The major averages sit little changed compared to our last update, still sporting loses between 1.2% and 2.3% on the day.

Gold futures settled at another 2018 low on Monday, down 0.1%, at $1,268.90/oz. Even though today's settlement marks a fresh YTD low, the yellow metal trimmed this morning's dollar-driven decline which was exacerbated by overwhelming tariff rhetoric.

Despite opening higher on Monday, the U.S. Dollar Index has faded somewhat into the afternoon and now show losses of 0.2% at 94.32.

Dow: -303.70… | Nasdaq: -172.87… | S&P: -38.70…

NASDAQ Adv/Dec 701/2189. …NYSE Adv/Dec 729/2149.

01:35PM ET

[BRIEFING.COM] The major U.S. indices are off their worst levels of the day, but remain under heavy pressure to begin the trading week as investors grow weary over escalating trade war rhetoric between the U.S. & China.

A look inside the Dow Jones Industrial Average shows that Intel (INTC 50.32, -2.18), Visa (V 130.36, -4.97), & Cisco (CSCO 41.94, -1.26) are underperforming. Intel is leading the Dow lower after being downgraded to Neutral from Buy at Nomura, while Visa is selling off following the Supreme Court's ruling on a case involving competitor American Express (see below).

Conversely, American Express (AXP 98.74, +1.51) is the best-performing Dow component after the Supreme Court ruled that the company did not violate antitrust laws in connection with contracts it makes merchants sign that says they can't encourage customers to use different credit cards for which they pay a smaller processing fee.

With today's sharp decline, the DJIA is now down 0.78% this month.

Dow: -390.22… | Nasdaq: -194.73… | S&P: -45.59…

NASDAQ Adv/Dec 621/2275. …NYSE Adv/Dec 658/2223.

01:00PM ET

[BRIEFING.COM] Stocks are tumbling today amid escalated trade tensions between the U.S. and China. The S&P 500 is down 1.6%, hovering about five points below its 50-day moving average. The Dow is also down about 1.6% while the tech-heavy Nasdaq and the small-cap Russell 2000 underperform, down 2.4% and 2.1%, respectively.

Over the weekend, The Wall Street Journal reported that the Trump administration is looking to bar many Chinese companies from investing in U.S. technology firms. Treasury Secretary Mnuchin refuted the report earlier today, saying the administration is targeting all countries attempting to "steal our technology", not just China. On a separate, but related, note, President Trump tweeted over the weekend that U.S. trading partners will face "more than reciprocity" if they fail to remove barriers on U.S. imports.

Losses are broad today, with eight of eleven S&P 500 sectors in negative territory. The top-weighted technology sector (-3.0%) is the worst-performing group with chipmakers, which derive a large chunk of their revenue from shipments to Beijing, showing particular weakness. The Philadelphia Semiconductor Index is down 3.9%, hovering at a seven-week low.

Meanwhile, FAANG names, including Facebook (FB 194.29, -7.46), Apple (AAPL 181.20, -3.73), Amazon (AMZN 1662.79, -52.79), Alphabet (GOOG 1120.82, -34.66), and Netflix (NFLX 384.153, -27.09), are down big, showing losses between 2.0% and 6.5%. Most of those companies are a part of the tech sector, although Amazon is within the consumer discretionary space (-2.1%).

The energy sector (-2.2%) is also a notable laggard, even though crude prices are just modestly lower. WTI crude futures are down 0.5% at $68.21/bbl.

On a positive note, the countercyclical consumer staples (+0.2%), utilities (+1.2%), and telecom services (+0.1%) sectors are in the green.

In corporate news, Campbell Soup (CPB 42.59, +3.99) is up 10.3% and Kraft Heinz (KHC 63.44, +0.23) is up 0.4% following a NY Post report that Kraft might be interest in purchasing the soup maker. Harley-Davidson (HOG 41.69, -2.51), meanwhile, is down 5.7% after announcing it won't raise prices to cover the cost of the EU's reciprocal tariffs; instead, it'll work to shift production to international facilities. Also of note, Carnival (CCL 58.64, -4.89) is down 7.6% after disappointing guidance outweighed upbeat quarterly results.

U.S. Treasuries are higher today, benefiting from a flight to safety trade and leaving yields lower across the curve. The yield on the benchmark 10-yr Treasury note down three basis points at 2.87%, and the yield on the 2-yr Treasury note down two basis points at 2.53%. The CBOE Volatility Index has spiked 32.6% to 18.26, its highest level since April 12.

Reviewing today's economic data, which was limited to the New Home Sales report for May:

New Home Sales in May hit an annualized rate of 689,000, which is above the Briefing.com consensus of 666,000. The April reading was revised to 646,000 (from 662,000).

The key takeaway from the report is that there wasn't any growth in new home sales outside the South region. That is the largest region for new home sales, though, and where there is a concentration of lower-priced housing markets, which helps explain the year-over-year drop in median and average selling prices.

Dow: -345.85… | Nasdaq: -180.85… | S&P: -40.17…

NASDAQ Adv/Dec 597/2289. …NYSE Adv/Dec 616/2244.

12:25PM ET

[BRIEFING.COM] Stocks continue to slide, with the S&P 500 now down 1.8% and the Dow lower by 1.7%.

Despite losses in the broader market, three S&P 500 sectors -- consumer staples (+0.1%), utilities (+1.0%), and telecom services (+0.1%) -- are in the green. All three groups are countercyclical in nature, meaning they tend to perform relatively well even in times of economic uncertainty. Investors are flocking to these groups today amid escalated trade tensions between the U.S. and China.

In Europe, the major bourses suffered heavy losses on Monday, dropping between 1.9% and 2.5%, with Germany's DAX leading the retreat.

Dow: -429.05… | Nasdaq: -199.38… | S&P: -49.14…

NASDAQ Adv/Dec 520/2351. …NYSE Adv/Dec 504/2347.

11:55AM ET

[BRIEFING.COM] The market has slipped to new lows in recent trading. The tech-heavy Nasdaq is now down 2.2% -- more than double its opening loss.

FAANG names -- including Facebook (FB 195.35, -6.32), Apple (AAPL 182.44, -2.45), Amazon (AMZN 1675.06, -40.72), Alphabet (GOOG 1121.00, -34.48), and Netflix (NFLX 385.15, -25.91) -- are down big today, showing losses between 1.3% and 6.3%. The S&P's technology sector is currently down 2.4%.

In Washington, Treasury Secretary Steven Mnuchin recently tweeted that all countries will be barred from "trying to steal our technology", refuting earlier reports that the White House is specifically trying to bar Chinese companies from investing in U.S. tech firms.

Dow: -336.56… | Nasdaq: -163.59… | S&P: -38.90…

NASDAQ Adv/Dec 565/2289. …NYSE Adv/Dec 545/2295.

11:25AM ET

[BRIEFING.COM] The major averages are drifting near their lowest marks of the day, with the S&P 500 down 1.3%.

8 of 11 sectors are in the red, with consumer discretionary (-2.0%), energy (-2.2%), and information technology (-2.2%) leading the retreat. Within the consumer discretionary space, Carnival (CCL 57.35, -6.19) has tumbled 9.7% after disappointing guidance overshadowed better-than-expected quarterly earnings.

In the bond market, U.S. Treasuries are hovering near their session highs, leaving yields lower across the curve. The yield on the benchmark 10-yr Treasury note, for instance, is down three basis points at 2.87%, which marks a new June low.

Dow: -353.91… | Nasdaq: -159.95… | S&P: -40.75…

NASDAQ Adv/Dec 574/2247. …NYSE Adv/Dec 532/2296.

10:55AM ET

[BRIEFING.COM] The S&P 500 and the Dow are still solidly lower, down around 1.0% apiece, and the tech-heavy Nasdaq is especially weak, down 1.5%.

Chipmakers are under heavy pressure today, pushing the Philadelphia Semiconductor Index down 2.6% to its lowest level in seven weeks. Fears of a trade war between the U.S. and China have fueled today's semiconductor sell off as chipmakers derive a large chunk of their revenue from shipments to Beijing.

The S&P 500's technology sector, which comprises a quarter of the broader market by itself, is down 1.6%, hovering near the bottom of today's sector standings. The energy sector (-1.9%) is the only space with a more substantial loss.

Dow: -253.44… | Nasdaq: -116.39… | S&P: -28.21…

NASDAQ Adv/Dec 669/2143. …NYSE Adv/Dec 598/2210.

10:35AM ET

[BRIEFING.COM]

Commodities are starting the day off lower

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently -1.2% at 86.24

Dollar index is currently -0.15% at 94.05

Looking at energy...

Aug WTI crude oil futures are now +$0.22 at $68.80/barrel

In other energy, Aug natural gas is -$0.02 at $2.92/MMBtu

Moving on to metals...

Aug gold is currently -$2.50 at $1268.20/oz, while Jul silver is -$0.15 at $16.31/oz

Jul copper is now -$0.01 at $3.04/lb

Dow: -257.79… | Nasdaq: -117.25… | S&P: -29.52…

NASDAQ Adv/Dec 643/2142. …NYSE Adv/Dec 540/2234.

10:05AM ET

[BRIEFING.COM] The major averages have slipped from their opening levels, with the S&P 500 extending its loss to 1.0%.

Just in, New Home Sales in May hit an annualized rate of 689,000, which is above the Briefing.com consensus of 666,000. The April reading was revised to 646,000 (from 662,000).

Dow: -287.99… | Nasdaq: -110.94… | S&P: -29.05…

NASDAQ Adv/Dec 570/2173. …NYSE Adv/Dec 579/2127.

09:40AM ET

[BRIEFING.COM] Equity indices are down in the opening minutes, showing losses between 0.6% and 1.0%.

Most S&P 500 sectors are in negative territory, with the top-weighted technology group (-1.3%) leading the retreat. The consumer discretionary sector (-0.9%) is also relatively weak, but countercyclical groups are showing relative strength. Utilities (+0.6%) is the top-performing sector.

As a reminder, New Home Sales for May (Briefing.com consensus 666K) will be released at 10:00 AM ET.

Dow: -175.20… | Nasdaq: -86.92… | S&P: -19.02…

NASDAQ Adv/Dec 653/2015. …NYSE Adv/Dec 746/1843.

09:10AM ET

[BRIEFING.COM] S&P futures vs fair value: -12.50. Nasdaq futures vs fair value: -60.80.

The stock market is on course for a lower start, as the S&P 500 futures are trading 13 points, or 0.5%, below fair value.

Trade tensions are weighing once again this morning following a Sunday tweet from President Trump, who said that U.S. trading partners will face "more than reciprocity" if they fail to remove barriers on U.S. imports. This warning was followed by a Wall Street Journal report that the White House is looking to bar many Chinese companies from investing in U.S. technology firms and attempting to block additional technology exports to Beijing.

In corporate news, Campbell Soup (CPB 40.99, +2.37) is up 6.1% in pre-market trading following a NY Post report that Kraft (KHC 62.60, -0.61) might be interested in purchasing the company. Separately, Harley-Davidson (HOG 44.21, 0.00) is flat despite announcing it won't raise prices to cover the cost of the EU's reciprocal tariffs; instead, it'll work to shift production to international facilities and expects an aggregate annual impact of $90 mln -$100 mln as a result.

Elsewhere, U.S Treasuries are higher, pushing yields lower across the curve. The yield on the benchmark 10-yr Treasury note is down one basis point at 2.89%. Meanwhile, the U.S. Dollar Index is down 0.2% at 94.05, and WTI crude futures are up 0.7% at $69.06 per barrel.

There's just one notable piece of economic data on today's calendar, New Home Sales for May (Briefing.com consensus 666K), which will be released at 10:00 AM ET.

08:50AM ET

[BRIEFING.COM] S&P futures vs fair value: -11.30. Nasdaq futures vs fair value: -51.80.

The S&P 500 futures are trading 11 points, or 0.4%, below fair value.

Equity indices in the Asia-Pacific region began the week on a lower note. The People's Bank of China announced that the reserve requirement ratio will be lowered by 50 basis points for certain lenders. The cut, which will release about CNY700 billion in liquidity, will go into effect on July 5 and it comes after weeks of speculation about such a move. Weekend press reports indicate the Trump administration will look to restrict Chinese investment in the U.S. technology sector.

In economic data:

Japan's April Leading Index 106.2 (expected 105.6; last 105.6)

Singapore's May CPI +0.4% month-over-month (expected 0.3%; last 0.1%)

---Equity Markets---

Japan's Nikkei fell 0.8%, approaching last week's low. SUMCO, Advantest, Subaru, Trend Micro, TOTO, Suzuki Motor, Yamaha Motor, Nippon Express, Shin-Etsu Chemical, Tokyo Electron, and Toyota Motor lost between 1.5% and 3.2%.

Hong Kong's Hang Seng ended lower by 1.3%. Country Garden Holdings dropped 5.8% while Sunny Optical Tech and AAC Technologies fell 4.9% and 1.9%, respectively. Property names like China Overseas, Wharf Real Estate, Sino Land, and New World Development surrendered between 1.5% and 3.4%.

China's Shanghai Composite settled lower by 1.1%. Gemdale, Beijing Airport High-Tech Park, China Southern Airlines, and China Eastern Airlines lost between 5.6% and 10.0%.

India's Sensex lost 0.6%. Tata Motors lost 7.1% amid concerns about tariffs. ICICI Bank, AXIS Bank, and SBI fell between 1.8% and 3.8%.

Major European indices trade lower across the board with the UK's FTSE (-1.6%) and Germany's DAX (-1.6%) trailing other regional markets. Italian debt is facing selling pressure once again, weighing on investor sentiment in the region. The selling comes after Lega had a very strong showing in yesterday's municipal elections, which reaffirmed support for the right-wing party. Italy's Prime Minister Giuseppe Conte said he was extremely satisfied with the weekend mini-summit, because the debate was steered in the right direction. A broader summit will take place during the upcoming weekend and immigration is certain to be the main item on the agenda as German Chancellor Angela Merkel fights for her political life.

In economic data:

Germany's June Ifo Business Climate Index 101.8 (expected 101.9; last 102.2). Business Expectations 98.6 (expected 98.0; last 98.5) and Current Assessment 105.1 (expected 105.6; last 106.0)

Spain's April trade deficit EUR3.10 billion (last deficit of EUR830 million)

---Equity Markets---

France's CAC is lower by 1.0%. STMicroelectronics is the weakest performer, falling 3.2% while Renault, Peugeot, BNP Paribas, Credit Agricole, and Airbus are down between 1.2% and 3.0%.

UK's FTSE has given up 1.6%. Miners like Anglo American, Fresnillo, Antofagasta, BHP Billiton, Glencore, and Rio Tinto are down between 1.8% and 2.5% while Prudential, HSBC, BP, Barclays, RBS, and Diageo hold losses between 1.5% and 2.1%.

Germany's DAX trades lower by 1.6%. Lufthansa, Infineon, Thyssenkrupp, Daimler, Volkswagen, BMW, Deutsche Bank, and BASF are down between 1.5% and 3.7%.

Italy's MIB has slid 1.3%. Unipol Gruppo, STMicroelectronics, Mediobanca, Banco Bpm, Banca Mediolanum, Intesa Sanpaolo, UBI Banca, and Ferrari are down between 1.8% and 4.3%.

08:25AM ET

[BRIEFING.COM] S&P futures vs fair value: -11.00. Nasdaq futures vs fair value: -53.30.

The S&P 500 futures are trading 11 points, or 0.4%, below fair value.

In the UK, private ride-haling company Uber is headed to court today, trying to reverse a decision by London's transport regulator to suspend the company's operating license on grounds of public safety and security. If Uber loses, it could ultimately be

from operating in London, which is its largest European market.

New Uber CEO Dara Khosrowshahi, who took over for founder Travis Kalanick in August 2017, is looking to take advantage of this opportunity to clean up the company's reputation as it prepares for a massive initial public offering -- which scheduled for 2019.

07:55AM ET

[BRIEFING.COM] S&P futures vs fair value: -11.50. Nasdaq futures vs fair value: -64.30.

Futures are pointing towards a lower start as U.S.-China trade tensions continue to weigh. The S&P 500 futures are 12 points, or 0.4%, below fair value.

President Trump on Sunday tweeted that U.S. trading partners will face "more than reciprocity" if they fail to remove barriers on U.S. imports. This warning was followed by a Wall Street Journal report that the White House is looking to bar many Chinese companies from investing in U.S. technology firms and attempting to block additional technology exports to Beijing.

U.S. Treasuries are up this morning, sending yields modestly lower. The yield on the benchmark 10-yr Treasury note is down two basis points at 2.88%. The 2-yr yield is also lower by two basis points, hovering at 2.53%. Meanwhile, the U.S. Dollar Index is down 0.1% at 94.09.

There's just one notable piece of economic data on today's calendar, New Home Sales for May (Briefing.com consensus 666K), which will be released at 10:00 AM ET. The earnings front is also light today, with Carnival (CCL) set to report its quarterly results before the opening bell.

In U.S. corporate news:

Intel (INTC 51.25, -1.25): -2.4% after being downgraded to 'Neutral' from 'Buy' at Nomura.

Campbell Soup (CPB 40.90, +2.30): +6.0% following a NY Post report that Kraft (KHC 62.82, -0.39) might be interested in purchasing the company.

Harley-Davidson (HOG 43.00, -1.21): -2.7% after announcing that it won't raise prices to cover new EU tariffs.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region began the week on a lower note. Japan's Nikkei -0.8%, Hong Kong's Hang Seng -1.3%, China's Shanghai Composite -1.1%, India's Sensex -0.6%.

In economic data:

Japan's April Leading Index 106.2 (expected 105.6; last 105.6)

Singapore's May CPI +0.4% month-over-month (expected 0.3%; last 0.1%)

In news:

The People's Bank of China announced that the reserve requirement ratio will be lowered by 50 basis points for certain lenders. The cut, which will release about CNY700 billion in liquidity, will go into effect on July 5 and it comes after weeks of speculation about such a move.

Weekend press reports indicate the Trump administration will look to restrict Chinese investment in the U.S. technology sector.

Major European indices trade lower across the board with Italy's MIB (-1.4%) and Germany's DAX (-1.4%) trailing other regional markets. France's CAC -0.7%, UK's FTSE -1.2%.

In economic data:

Germany's June Ifo Business Climate Index 101.8 (expected 101.9; last 102.2). Business Expectations 98.6 (expected 98.0; last 98.5) and Current Assessment 105.1 (expected 105.6; last 106.0)

Spain's April trade deficit EUR3.10 billion (last deficit of EUR830 million)

In news:

Italian debt is facing selling pressure once again, weighing on investor sentiment in the region. The selling comes after Lega had a very strong showing in yesterday's municipal elections, which reaffirmed support for the right-wing party.

Italy's Prime Minister Giuseppe Conte said he was extremely satisfied with the weekend mini-summit, because the debate was steered in the right direction. A broader summit will take place during the upcoming weekend and immigration is certain to be the main item on the agenda as German Chancellor Angela Merkel fights for her political life.

07:28AM ET

[BRIEFING.COM] S&P futures vs fair value: -13.50. Nasdaq futures vs fair value: -64.50.

06:59AM ET

[BRIEFING.COM] S&P futures vs fair value: -14.50. Nasdaq futures vs fair value: -67.50.

06:59AM ET

[BRIEFING.COM] Nikkei...22338...-178.70...-0.80%. Hang Seng...28961...-377.30...-1.30%.

06:59AM ET

[BRIEFING.COM] FTSE...7587.08...-95.20...-1.20%. DAX...12389.96...-189.80...-1.50%.

04:25PM ET

[BRIEFING.COM] The S&P 500 ended the week on a positive note by advancing 0.2% on Friday. Energy shares led the broad-based rally thanks to a spike in oil prices, which surged to a four-week high as OPEC wrapped up its latest summit in Vienna. However, financials, technology, and consumer discretionary stocks lagged, keeping gains in check. For the week, the S&P 500 lost 0.9%.

Friday's session was range-bound to say the least. The S&P 500 held a gain between 0.2% and 0.5% throughout the entire session, sticking to a 12-point range. Trading volume was extremely high due to the annual re-balancing of the Russell 1000 and Russell 2000 indices. Roughly 2.2 million shares changed hands at the New York Stock Exchange.

The OPEC summit was the biggest event of the day, as it ended on a somewhat unexpected note. Following a contentious two-day meeting, the oil-producing countries agreed to increase total output by roughly 600,000 barrels per day -- far less than the top end of estimates, which were calling for an increase of up to 1.5 million barrels per day.

West Texas Intermediate crude futures rallied 4.5% to $68.59 per barrel in reaction, helping the energy sector (+2.2%) finish unchallenged atop the sector standings; the next best-performing group -- materials -- added 1.4%. In total, eight of the eleven sectors finished in the green, with financials (-0.5%), technology (-0.4%), and consumer discretionary (-0.1%) being the three laggards. Unfortunately for the bulls, those three groups are heavily-weighted, representing around 50% of the broader market combined.

The financials and consumer discretionary sectors were holding up alright until the afternoon when they dropped to fresh session lows, while technology was weak throughout the session. Within the tech space, software company Red Hat (RHT 142.14, -23.59) tumbled 14.2% after disappointing guidance for its fiscal second quarter overshadowed its better-than-expected Q1 results.

In Washington, President Trump announced a new tariff threat via Twitter on Friday, vowing to slap a 20% tariff on automobiles produced in EU countries if the European Union fails to remove duties on imports of U.S. autos. The U.S. stock market dropped to new lows following the tweet, but didn't stay there for long.

U.S. Treasuries finished Friday on a flattish note, although shorter-dated issues showed relative weakness. The yield on the benchmark 10-yr Treasury note finished unchanged at 2.90%, while the yield on the 2-yr Treasury note climbed two basis points to 2.55%. The U.S. Dollar Index declined 0.4%, slipping from an 11-month high.

Investors did not receive any notable economic data on Friday.

Nasdaq Composite +11.4% YTD

Russell 2000 +9.8% YTD

S&P 500 +3.0% YTD

Dow Jones Industrial Average -0.6% YTD

Week In Review: Trade Tensions Weigh

Stocks fell this week as trade tensions helped to keep buyers at bay. The benchmark S&P 500 index ended the week lower by 0.9%. The tech-heavy Nasdaq lost 0.7%, but did notch a new all-time high on Wednesday, and the Dow Jones Industrial Average tumbled 2.0%.

At the start of the week, investors were still weighing the prospect of a trade war between the U.S. and China after President Trump confirmed last Friday that he has approved a 25% tariff on $50 billion worth of Chinese goods. Beijing responded swiftly to that news, vowing to implement equivalent duties on U.S. goods.

The story added a new chapter on Monday evening when President Trump asked his administration to identify an additional $200 billion worth of Chinese goods that he says will be hit with a 10% tariff should China follow through on its promise to retaliate. In addition, if China retaliates against the new $200 billion list, Mr. Trump said he will place tariffs on yet another $200 billion worth of Chinese goods.

The industrial sector, which is viewed as being in the crosshairs of protectionist trade actions, was the worst-performing S&P 500 group this week, losing 3.4%. Similarly, chipmakers, which derive a large chunk of their revenue from shipments to China, were also under pressure, sending the Philadelphia Semiconductor Index lower by 3.6%.

President Trump issued another tariff threat on Friday, this time targeting the European Union. The president said the U.S. will be imposing a 20% tariff on all automobiles imported from EU countries if the EU fails to remove duties on imports of U.S. automobiles. On a related note, as of Friday, the European Union has officially implemented tariffs on $3.2 billion worth of U.S. goods in retaliation to U.S. tariffs on imports of steel and aluminum that went into effect earlier this month.

Elsewhere, the Organization of Petroleum Exporting Countries (OPEC) met in Vienna this week to discuss easing production caps that have been in place for more than 18 months. The meeting was reportedly contentious, but the countries eventually agreed to boost oil output by a less-than-expected 600,000 barrels per day. WTI crude futures rallied to a four-week high on Friday following the news, and the energy sector reclaimed losses registered earlier in the week, finishing with a weekly gain of 1.5%.

In U.S. corporate news, Walgreens Boots Alliance (WBA) will be joining the Dow Jones Industrial Average on June 26, taking the spot of General Electric (GE), which was one of the original Dow components and has been a continuous part of the average for more than a century. The decision follows a disastrous 18-month stretch for GE shares, which have dropped around 60% since the end of 2016.

Separately, media names returned to the spotlight on Wednesday when Walt Disney (DIS) increased its offer for 21st Century Fox's (FOXA) entertainment assets. Disney is now offering $38 per share, up from its previous offer of $28 per share and better than last week's offer from Comcast (CMCSA) of $35 per share.

E-commerce companies, including Amazon (AMZN), eBay (EBAY), Wayfair (W), Overstock.com (OSTK), and Etsy (ETSY), sold off on Thursday after the U.S. Supreme Court ruled that states can require online retailers to collect sales tax, overturning a 1992 precedent.

Also of note, Intel's (INTC) chief executive, Brian Krzanich, resigned after breaking the company's non-fraternization policy, Oracle (ORCL) shares dropped to a 15-month low after the company's quarterly update provided less insight than usual into its growing cloud business, and Starbucks (SBUX) shares hit a three-year low after the company announced it will be scaling back store growth.

U.S. Treasuries ended the week on a modestly higher note, pushing the benchmark 10-yr yield lower by two basis points to 2.90%.

Dow: +119.19… | Nasdaq: -20.13… | S&P: +5.12…

NASDAQ Adv/Dec 1595/1374. …NYSE Adv/Dec 1962/994.

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Rebuttal to Emmett Moore via TheStrategyLab.com Review

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 Where did wrbtrader go? | Elite Trader

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=307&t=3770 The Strategy Lab: Valforex - The Manipulative Review Scam

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3676 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htm Advance WRB Analysis Tutorial Chapters 4 - 12

@ http://www.thestrategylab.com/WRBAnalysisTutorials.htmDisclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis. The risk of loss can be substantial. Therefore, you must carefully consider if trading is suitable for you within the context of your financial condition. TheStrategyLab.com is an education and research site. The resources on this site are provided for informational purposes only and should not be used to replace professional educational and professional research because we are retail traders only. TheStrategyLab.com does not accept liability for your use of the website and its resources.

We make no guarantees of success and your level of success is dependent upon other factors including your skill as a trader, knowledge, financial condition, market conditions and other factors. Trading is stressful and you should always consult a doctor in all matters relating to physical and mental health of you & your family because trading can impact beyond your financial condition regardless if you're a profitable or losing trader. Also, you can read our full disclaimer statement @ http://www.thestrategylab.com/Disclaimer.htmBest Regards,

M.A. Perry

Online user name

wrbtrader (more info about me)

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=127&t=850 & http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading (no indicators)

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com