Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htmFree Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htm TheStrategyLab Reviews: http://www.thestrategylab.com/thestrategylab-reviews.htm Price Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

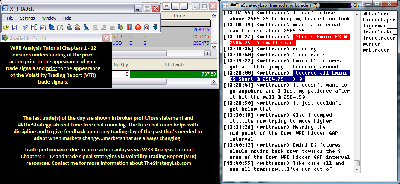

Attachment:

110717-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+737.50.png [ 96.96 KiB | Viewed 227 times ]

110717-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+737.50.png [ 96.96 KiB | Viewed 227 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini RTY ($RTY_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$737.50 dollars or +14.75 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $737.50 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis. The risk of loss can be substantial. Therefore, you must carefully consider if trading is suitable for you within the context of your financial condition. TheStrategyLab.com is an education and research site. The resources on this site are provided for informational purposes only and should not be used to replace professional educational and professional research because we are retail traders only. TheStrategyLab.com does not accept liability for your use of the website and its resources.

We make no guarantees of success and your level of success is dependent upon other factors including your skill as a trader, knowledge, financial condition, market conditions and other factors. Trading is stressful and you should always consult a doctor in all matters relating to physical and mental health of you and your family because trading can impact beyond your financial condition regardless if you're a profitable or losing trader.Russell 2000 Emini RTY Futures: 1 tick or 0.10 = $5.00 dollars and there's more contract information @

CMEGroup (formerly as TF @

The ICE)

S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log is archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=173&t=2689 All of my trades are posted

real-time at the above link for today's archive chat log in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader for anyone to do a real-time review (you must be a member of the chat room for a real-time review). Although the trades are posted by me and other users of WRB Analysis in real-time...this is

not a signal calling chat room

nor is this a live trading room that has a head trader telling you what to do. I'm the moderator (I keep the peace between members) and my own live trades are posted within 3.2 seconds on average

after the trade confirmation in my broker trade execution platform via an

auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility...all key concepts from the WRB Analysis free study guide even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads.

Quote:

2017 has been the most difficult trading year since I've begun trading +25 years ago because successful trading involves more than just trade methods than any other trading year. This is a key concept many traders have difficulties in understanding. Some blame it on algorithms. Others blame it on the political environment while I blame it on the inability to adapt, failure to backtest, failure to document trades (real-money or simulator) and underestimating how our environment influences our cognitive decision making while trading...all while trading in low volatility market conditions that statistically have the reputation for difficult trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room

nor is it a live trading room with a head trader even though members of the chat room are posting their trades & market analysis in real-time. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the

primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback about

your own trading and for members to help each other...as in more eyes on the market. In addition, we

highly recommend that you use the free chat room with a professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they can provide you with the

quantitative statistical analysis of your trading. You can then download your results and post them in your private thread at the forum.

Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your quantitative statistical analysis, brokerage statements in the free chat room. Instead, its highly recommended that you only post that particular information in your private thread for

security & privacy reasons. Yet, if you want to post that type of information at another website, blog or chat room...that's your choice.

TheStrategyLab free chat room is on IRC via

users request because the IRC servers are located in many different countries, software in many different languages, many different mobile apps, many different types of social media software can be used to log in along with IRC being easier to moderate via

script codes when trouble makers, spammers and trolls show up. I'm the

moderator of the free chat room via the user name

wrbtrader. Thus, I

keep the peace between members without hesitation in removing problematic traders & trolls so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets without being

trolled or harassed.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell nor do we allow the free chat room to be used for mentoring because we do

not offer a mentoring service. The

purpose of TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. If you join the free chat room and then you decide to

not post any WRB Analysis about the price action or you decide to not post your trades or you decide to be silent (lurk without saying a word about today's markets)...you're not using the free chat room properly to help improve your trading.

In fact, we do

not want silent (lurkers) traders to join the free chat room unless they are actively posting at the forum about their trading after the markets close.

Access instructions for the free chat room

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Quote:

All of my real-time posted trades involves price action concepts from the

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always backtesting new concepts of WRB Analysis, new trade entry rules, new trade management rules, new position size management rules before application in real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades or sharing the new concepts with fee-base clients...living up to the name of my website. TheStrategy

Lab.

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=333&t=3556 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini RTY futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

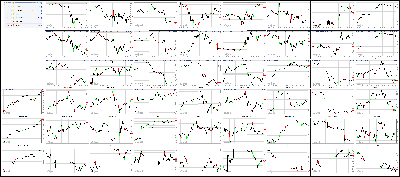

Attachment:

110717-Key-Price-Action-Markets.png [ 855.39 KiB | Viewed 246 times ]

110717-Key-Price-Action-Markets.png [ 855.39 KiB | Viewed 246 times ]

click on the above image to view today's price action of key markets The Market at 04:30PM ET Dow: +8.81… | Nasdaq: -18.65… | S&P: -0.49…

NASDAQ Vol: ---… Adv: 787… Dec: 1960…

NYSE Vol: 904.3 mln… Adv: 1259… Dec: 1695…

Moving the Market

Stocks struggle to advance as market-moving catalysts remain in short supply

Heavily-weighted financial sector faces heavy selling; weighs on broader market

Sector Watch

Strong: Industrials, Materials, Health Care, Consumer Staples, Utilities, Telecom Services, Real Estate

Weak: Financials, Consumer Discretionary, Energy

04:30PM ET

[BRIEFING.COM] Equities ended Tuesday little changed after heavy losses from financial shares roughly balanced gains in most other areas. The Dow eked out a slim victory--and its fourth consecutive record close--while the S&P 500 finished just a tick below its flat line. The Nasdaq (-0.3%) struggled to keep pace with its peers, but the small-cap Russell 2000 significantly underperformed, plunging 1.3%.

The financial sector tumbled 1.3% amid broad weakness, finishing at the very bottom of the sector standings. Heavyweights like JPMorgan Chase (JPM 98.75, -2.03), Bank of America (BAC 27.18, -0.57), and Wells Fargo (WFC 55.05, -1.13) showed particular weakness, settling with losses of around 2.0% apiece. Today's slide leaves the sector at a fresh two-week low.

Meanwhile, the consumer discretionary sector also struggled on Tuesday, declining by 0.6%. Travel sites Priceline (PCLN 1645.72, -257.28) and TripAdvisor (TRIP 30.35, -9.18) were the sector's worst-performing components, plunging 13.5% and 23.2%, respectively, after Priceline issued disappointing profit guidance for the fourth quarter and TripAdvisor missed Q3 revenue estimates.

Retailers also weighed on the sector, evidenced by the 2.4% decline in the SPDR S&P Retail ETF (XRT 39.00, -0.94)--which finished at a two-month low. There wasn't a single catalyst for the retail slide, but it did follow a Reuters report that some retailers are ordering less merchandise for the holiday season in fear of being stuck with unsold goods at the end.

On a positive note, the consumer staples (+1.1%), utilities (+1.2%), and real estate (+0.9%) sectors finished Tuesday solidly higher. Within the consumer staples space, pharmacy retailers CVS Health (CVS 68.95, +2.15) and Walgreens Boot Alliance (WBA 67.92, +1.98) bounced back from recent weakness, ending with respective gains of 3.2% and 3.0%.

In the bond market, U.S. Treasuries finished mostly higher, with the yield on the benchmark 10-yr Treasury note slipping one basis point to 2.31%.

Elsewhere, WTI crude futures dropped 0.3% to $57.20/bbl after hitting their highest level since July 2015 on Monday. A stronger U.S. dollar worked against the commodity; the U.S. Dollar Index climbed 0.2% to 94.79.

Reviewing Tuesday's economic data, which included the September Job Openings and Labor Turnover Survey (JOLTS) and the September Consumer Credit Report:

The September Job Openings and Labor Turnover Survey showed that job openings stayed at 6.09 million.

The Consumer Credit report for September showed an increase of $20.8 billion (Briefing.com consensus +$18.3 billion).

On Wednesday, investors will receive just one economic report--the weekly MBA Mortgage Applications Index--which will be released at 7:00 ET.

Nasdaq Composite +25.7% YTD

Dow Jones Industrial Average +19.2% YTD

S&P 500 +15.7% YTD

Russell 2000 +9.0% YTD

Dow: +8.81… | Nasdaq: -18.65… | S&P: -0.49…

NASDAQ Adv/Dec 787/1960. …NYSE Adv/Dec 1259/1695.

03:35PM ET

[BRIEFING.COM] Commodities end the day lower:

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently down 0.7% at 87.5385

Dollar index is currently up 0.13% at 94.88

Oct WTI Crude is down 0.23% on the day.

API inventory data to be released at 4:30 pm ET.

Futures settle $0.13 lower to $57.22/barrel.

In other energy, Dec Natural Gas settled up $0.02 at $3.15/MMBtu

On the metals:

Dec Gold lost $5.90 to settle at $1275.7/oz, while Dec silver lost $0.28 to $16.96/oz

Dec Copper dropped $0.07 to $3.09/lb

Finally, agriculture:

Dec Corn settled unchanged at $3.48/bu.

Dec Soy settled up $0.0025 at $9.9625/bu.

Dec wheat settled flat at $4.27/bu.

Dow: -22.85… | Nasdaq: -25.01… | S&P: -3.44…

NASDAQ Adv/Dec 784/2087. …NYSE Adv/Dec 1180/1753.

03:00PM ET

[BRIEFING.COM] Equity indices trade modestly lower moving into the final stretch.

Just in, the Consumer Credit report for September showed an increase of $20.8 billion while the Briefing.com consensus expected growth of $18.3 billion. The prior month's credit growth was left unrevised at $13.1 billion.

Dow: -26.72… | Nasdaq: -25.03… | S&P: -4.18…

NASDAQ Adv/Dec 767/2114. …NYSE Adv/Dec 1153/1738.

02:30PM ET

[BRIEFING.COM] The major indices are still drifting a step below their unchanged marks.

Four sectors are trading in the red this afternoon--financials (-1.2%), consumer discretionary (-0.5%), energy (-0.3%), and technology (-0.1%)--while seven are trading in the green--materials (unch), industrials (+0.1%), telecom services (+0.1%), health care (+0.1%), real estate (+0.5%), consumer staples (+0.9%), and utilities (+1.1%).

Tonight's batch of earnings will include reports from Snap (SNAP 15.17, +0.34), Marriott (MAR 121.09, -0.88), Zillow (ZG 40.29, -0.68), and Fossil (FOSL 6.89, -0.09).

As a reminder, the September Consumer Credit Report (Briefing.com consensus $18.3 billion) will be released at 15:00 ET.

Dow: -18.56… | Nasdaq: -24.38… | S&P: -3.96…

NASDAQ Adv/Dec 830/2045. …NYSE Adv/Dec 1159/1720.

01:55PM ET

[BRIEFING.COM] Equity indices continue to hover near their recent levels. The Nasdaq is down 0.3%, while the S&P 500 and the Dow shows losses of 0.1% apiece.

Retailers are struggling today, evidenced by the SPDR S&P Retail ETF (XRT 38.97, -0.97), which is lower by 2.4%. Names like Target (TGT 57.87, -1.42), Macy's (M 17.59, -0.58), Kohl's (KSS 40.67, -1.95), and Bed Bath & Beyond (BBBY 19.24, -0.73) show particular weakness, holding losses between 2.4% and 4.6%. Today's slide leaves the XRT at its lowest level since late August.

The consumer discretionary sector (-0.4%), which houses the aforementioned names, trades near the bottom of the sector standings, surpassed only by the heavily-weighted financial group (-1.1%).

Dow: -11.29… | Nasdaq: -18.82… | S&P: -2.04…

NASDAQ Adv/Dec 835/2031. …NYSE Adv/Dec 1161/1706.

01:30PM ET

[BRIEFING.COM] The major U.S. indices have been creeping higher since our last update, but still show modest losses at this time.

A look inside the Dow Jones Industrial Average shows that JP Morgan (JPM 98.92, -1.86), Nike (NKE 55.15, -0.89), & Goldman Sachs (GS 240.49, -3.00) are underperforming.

Conversely, Walt Disney (DIS 101.87, +1.23) is the best-performing Dow component as shares add to yesterday's gains that came in the wake of a CNBC report that the company recently held talks to acquire most of 21st Century Fox (FOXA 28.21, +0.76).

For the week, the DJIA is down 0.06%.

Elsewhere, at the top of the hour, the Treasury's $24 bln 3-year auction drew a high yield of 1.75% on a bid-to-cover of 2.76.

Dow: -24.61… | Nasdaq: -21.49… | S&P: -2..55…

NASDAQ Adv/Dec 816/2039. …NYSE Adv/Dec 1143/1718.

01:05PM ET

[BRIEFING.COM] Stocks have moved modestly lower today, retreating from their freshly-minted record highs. Small caps have shown particular weakness, sending the Russell 2000 lower by 1.3%, while the Nasdaq (-0.3%), the Dow (-0.1%), and the S&P 500 (-0.1%) trade just a step below their unchanged marks. Stocks held slim gains for much of the morning, but then slipped into the red about an hour ago.

Financials have paced today's retreat, sending the S&P 500's financial sector (-1.3%) to a two-week low. Heavyweights like JPMorgan Chase (JPM 98.61, -2.17), Wells Fargo (WFC 55.20, -0.97), Bank of America (BAC 27.03, -0.71), and Citigroup (C 72.50, -1.29) show relative weakness, losing between 1.7% and 2.5%.

A flattening of the yield curve, which doesn't bode well for lenders' net interest margins, has also worked against the sector. The yield on the benchmark 10-yr Treasury note has slipped two basis points to 2.30%, while the 2-yr yield has climbed one basis point to 1.63%.

Meanwhile, the consumer discretionary space (-0.4%) has also struggled today, with travel sites Priceline (PCLN 1672.45, -230.49) and TripAdvisor (TRIP 31.57, -7.96) plunging 12.1% and 20.2%, respectively, in reaction to their latest earnings reports. Priceline issued disappointing profit guidance for the fourth quarter, while TripAdvisor missed revenue estimates.

Elsewhere within the group, retailers are also underperforming, sending the SPDR S&P Retail ETF (XRT 39.01, -0.93) lower by 2.3%.

On a positive note, select countercyclical sectors are trading higher, including the utilities (+1.2%), consumer staples (+1.0%), and health care (+0.1%) groups. Within the consumer staples space, pharmacy retailers like CVS Health (CVS 68.93, +2.13) and Walgreens Boot Alliance (WBA 67.86, +1.92) sport respective gains of 3.2% and 2.9%, bouncing back from recent weakness.

Today's economic data has been limited to the Job Openings and Labor Turnover Survey, which showed that job openings stayed at 6.09 million in September. The September Consumer Credit Report (Briefing.com consensus $18.3 billion) will be released at 15:00 ET.

Dow: -33.17… | Nasdaq: -23.33… | S&P: -3.14…

NASDAQ Adv/Dec 756/2098. …NYSE Adv/Dec 1073/1777.

12:25PM ET

[BRIEFING.COM] Stocks continue to hover at session lows as financial shares tumble. The Nasdaq is down 0.5%, while the S&P 500 and the Dow show losses of 0.2% apiece.

The financial sector is lower by 1.3% amid broad weakness; outside of a handful of insurance names, just about all of the sector's components are trading in the red. Heavyweights like JPMorgan Chase (JPM 99.10, -1.68), Wells Fargo (WFC 55.20, -0.98), Bank of America (BAC 27.18, -0.58), Citigroup (C 72.77, -1.03), and Goldman Sachs (GS 240.31, -3.18) show losses between 1.3% and 2.1%.

In addition to financials, five other sectors are trading in negative territory--consumer discretionary (-0.6%), energy (-0.5%), telecom services (-0.4%), technology (-0.3%), and materials (unch).

Elsewhere, U.S. Treasuries have climbed to fresh session highs in recent action, with longer-dated issues showing relative strength; the yield on the benchmark 10-yr Treasury note is down two basis points at 2.30%. Meanwhile, the 2-yr yield continues to trade flat, hovering at 1.62%.

Dow: -58.37… | Nasdaq: -35.50… | S&P: -6.28…

NASDAQ Adv/Dec 705/2167. …NYSE Adv/Dec 1004/1841.

12:00PM ET

[BRIEFING.COM] The major U.S. indices are hovering at fresh session lows, with the S&P 500 showing a loss of 0.2%. Small caps show relative weakness, sending the Russell 2000 lower by 0.8%.

European stocks finished Tuesday's session broadly lower, evidenced by the Euro Stoxx 50, which slipped 0.7%. Germany-based automaker BMW showed particular weakness, losing 2.7%, after reporting worse-than-expected earnings. Meanwhile, French lenders like Societe Generale and Credit Agricole outperformed, adding around 0.5% apiece.

In the currency market, the euro has slipped 0.3% against the U.S. dollar to 1.1574--hitting its lowest level since mid-July--while the pound has dropped 0.2% against the greenback to 1.3146.

Dow: -52.96… | Nasdaq: -30.48… | S&P: -4.59…

NASDAQ Adv/Dec 753/2117. …NYSE Adv/Dec 1024/1812.

11:25AM ET

[BRIEFING.COM] Equity indices have popped back to their flat lines in recent action after slipping into the red for a short while. The Nasdaq still shows relative weakness, however, holding a loss of 0.2%.

The heavily-weighted financial sector (-0.3%) is struggling today amid broad weakness. Within the group, influential banking names like JPMorgan Chase (JPM 99.93, -0.84), Bank of America (BAC 27.42, -0.33), and Wells Fargo (WFC 55.70, -0.48) show particular weakness, losing between 0.9% and 1.2%. Financials have been largely trending sideways over the last two weeks following a bullish seven week run from September 7 to October 24--during which the sector added more than 12.0%.

Conversely, the lightly-weighted telecom services space has stayed true to its bearish trend, losing another 0.3% in today's session to extend its November loss to 4.3%. The group has lost 19.7% year to date, while the S&P 500 has climbed 15.8%.

Dow: -2.75… | Nasdaq: -17.27… | S&P: +0.12…

NASDAQ Adv/Dec 907/1962. …NYSE Adv/Dec 1220/1592.

10:55AM ET

[BRIEFING.COM] Equity indices have slipped to new session lows in recent action, with the S&P 500 now showing a loss of 0.1%.

The S&P 500's energy sector (-0.3%) trades near the bottom of today's sector standings as the price of crude oil slides following Monday's big gain of 3.0%; WTI crude futures are down 0.3% at $57.18/bbl. The consumer discretionary space (-0.3%) also shows relative weakness, with travel sites Priceline (PCLN 1706.98, -196.00) and TripAdvisor (TRIP 32.49, -7.04) plunging 10.4% and 18.1%, respectively, in reaction to their latest earnings reports. Priceline issued disappointing guidance for the fourth quarter, while TripAdvisor missed revenue estimates.

Meanwhile, select countercyclical groups like consumer staples (+0.7%) and utilities (+0.8%) show relative strength.

Dow: -22.64… | Nasdaq: -21.63… | S&P: -1.89…

NASDAQ Adv/Dec 776/2065. …NYSE Adv/Dec 1090/1679.

10:30AM ET

[BRIEFING.COM] Commodities begin the day flat :

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently unchanged -0.8% at 87.4526

Dollar index is currently up 0.34% at 95.08

Dec WTI crude is down 0.38% on the day.

API inventory data to be released at 4:30 pm ET.

Futures are $0.22 lower to $57.13/barrel.

In other energy, Dec natural gas is down $0.02 at $3.11/MMBtu

Metals:

Dec gold lost $6.70 and trades at $1274.9/oz, while Dec silver lost $0.20 to $17.04/oz

Dec copper dropped 0.07 to $3.09/lb

Finally, agriculture:

Dec corn is down $0.01 at $3.47/bu.

Dec soy is up $0.03 at $9.97/bu.

Dec wheat is down $0.06 at $4.25/bu.

Dow: +0.47… | Nasdaq: -15.79… | S&P: +0.41…

NASDAQ Adv/Dec 883/1922. …NYSE Adv/Dec 1179/1564.

10:05AM ET

[BRIEFING.COM] The S&P 500 (+0.2%) trades a step above its flat line.

Just in, the September Job Openings and Labor Turnover Survey showed that job openings stayed at 6.09 million.

Dow: +50.08… | Nasdaq: +1.45… | S&P: +4.67…

NASDAQ Adv/Dec 1207/1507. …NYSE Adv/Dec 1464/1224.

09:45AM ET

[BRIEFING.COM] The major U.S. indices trade a tick above their flat lines in the opening minutes of today's session, with the S&P 500 sporting a gain of 0.1%.

Most sectors are trading in positive territory, but gains have been limited; no group holds a gain of more than 0.4%. The health care sector (+0.4%) is the strongest group, while the energy (-0.4%) and telecom services (-0.4%) spaces are the weakest.

Elsewhere, U.S. Treasuries continue hovering near their flat lines, with the benchmark 10-yr yield unchanged at 2.32%.

Dow: +37.77… | Nasdaq: +5.07… | S&P: +4.12…

NASDAQ Adv/Dec 1232/1393. …NYSE Adv/Dec 1391/1260.

09:12AM ET

[BRIEFING.COM] S&P futures vs fair value: +0.50. Nasdaq futures vs fair value: -1.90.

The stock market is on track to open Tuesday's session flat as the S&P 500 futures drift roughly in line with fair value.

In earnings news, Priceline (PCLN 1747.00, -156.00) has dropped 8.2% after issuing below-consensus guidance for the fourth quarter. Avis Budget (CAR 37.01, -4.41) is also solidly lower, down 10.7%, after cutting the top end of its earnings guidance for the fiscal year. Conversely, Weight Watchers (WTW 51.12, +6.32) has spiked 14.1% after beating both top and bottom line estimates and issuing upbeat guidance for the fiscal year.

As for economic data, investors will receive two economic reports today--the September Job Openings and Labor Turnover Survey (JOLTS) and September Consumer Credit (Briefing.com consensus $18.3 billion). The reports will be released at 10:00 ET and 15:00 ET, respectively.

U.S. Treasuries are trading flat this morning, with the benchmark 10-yr yield unchanged at 2.32%. Meanwhile, the U.S. Dollar Index is up 0.4% at 95.03--marking its highest level since mid-July. The greenback has climbed 0.4% against the euro (1.1565), 0.4% against the pound (1.3125), and 0.3% against the yen (114.09).

The dollar's strength has worked against WTI crude futures, which are down 0.2% at $57.26/bbl following yesterday's 3.0% rally. Despite the downtick, the commodity continues to hover near its best level since July 2015. The American Petroleum Institute will release its weekly crude inventory report this afternoon at 16:30 ET.

Coming into today's session, all three major indices--the S&P 500, the Dow, and the Nasdaq--are hovering at all-time highs.

08:50AM ET

[BRIEFING.COM] S&P futures vs fair value: +0.60. Nasdaq futures vs fair value: +1.50.

The S&P 500 futures trade one point above fair value.

Equity indices in the Asia-Pacific region ended Tuesday on a mostly higher note. The Reserve Bank of Australia left its cash rate at 1.50%, as expected, but the central bank's statement was dovish, noting uncertainty associated with household consumption. New Zealand's Prime Minister Jacinda Ardern said she is "not at all" concerned with the recent Kiwi weakness. The New Zealand dollar trades at 0.6924 against the U.S. dollar, hovering just above this year's low. President Trump is in South Korea today, where he called on "every responsible nation, including China and Russia to act with urgency and with great determination" to implement sanctions against North Korea.

In economic data:

Japan's September Overtime Pay +0.9% year-over-year (last 1.5%) and Average Cash Earnings +0.9% year-over-year (consensus 0.6%; last 0.7%)

China's FX Reserves $3.109 trillion (expected $3.107 trillion; last $3.108 trillion)

Australia's AIG Construction Index 53.2 (last 54.7)

---Equity Markets---

Japan's Nikkei spiked 1.7%. Japan Steel Works surged 17.5% and Toho Zinc jumped 8.2% while Dainippon Screen Manufacturing, Nippon Sheet Glass, Kyocera, Hitachi Construction, Konami, Mitsubishi, and Fast Retailing advanced between 3.4% and 6.5%.

Hong Kong's Hang Seng rose 1.4%. Geely Automobile led with a gain of 5.7% after reporting record October sales. China Petrol & Chemical and PetroChina hold respective gains of 3.7% and 2.9% while property names like Link Reit, Sino Land, Wharf Holdings, and SHK Properties added between 1.2% and 2.7%.

China's Shanghai Composite gained 0.8%. China United Network Communications, CEC Corecast, But'one Information Corp, Shanghai Zhixin Electric, and Shanghai Haixin Group posted gains between 5.3% and 7.1%.

India's Sensex lost 1.1%. Lupin plunged 16.8% after the U.S. FDA issued a warning letter to two of the company's facilities, likely delaying a new product release. Cipla fell 7.2% while financials like SBI, ICICI Bank, AXIS Bank, and HDFC Bank surrendered between 0.4% and 3.6%.

Major European indices trade near their flat lines. Outgoing Eurogroup Chief Jeroen Dijsselbloem said the Eurogroup hopes to make a decision regarding a banking union in June. Reports from the recent Eurogroup meeting indicate that many members favored establishing a budget for stabilization purposes. This was the first Eurogroup meeting without the participation of Germany's Wolfgang Schaeuble. European Central Bank President Mario Draghi said there is little evidence that negative rates are undermining the profitability of banks.

In economic data:

Eurozone September Retail Sales +0.7% month-over-month (expected 0.6%; last -0.1%); +3.7% year-over-year (consensus 2.7%; last 2.3%). Retail PMI 51.1 (last 52.3)

Germany's September Industrial Production -1.6% month-over-month (expected -0.8%; last 2.6%)

UK's October Halifax House Price Index +0.3% month-over-month (expected 0.2%; last 0.8%); +4.5% year-over-year, as expected (last 4.0%)

France's Q4 Industrial Investments 4.0% (last 7.0%). September government budget balance -EUR76.30 billion (last -EUR93.00 billion)

Italy's September Retail Sales +0.9% month-over-month (expected 0.2%; last -0.2%); +3.4% year-over-year (last -0.1%)

---Equity Markets---

UK's FTSE is lower by 0.2% with consumer names showing relative weakness. G4S and Associated British Foods hold respective losses of 5.4% and 4.4% after missing earnings expectations. Kingfisher, WPP, and Sky are down between 1.4% and 2.7%. On the upside, Imperial Brands has climbed 1.1% and BP is higher by 1.4%.

France's CAC has shed 0.1%. Valeo and STMicroelectronics are both down near 1.5% while Peugeot and Renault hold respective losses of 0.8% and 0.1%. Consumer names like Danone, L'Oreal, Pernod Ricard, Carrefour, and Accor are down between 0.5% and 0.9%.

Germany's DAX is down 0.1%. Financials Commerzbank, Deutsche Bank, and Allianz are up between 0.5% and 0.7% while automakers are mixed. Volkswagen has climbed 0.4% while Daimler is down 0.3% and BMW has slid 2.8% after missing earnings expectations.

08:29AM ET

[BRIEFING.COM] S&P futures vs fair value: flat. Nasdaq futures vs fair value: -0.10.

The S&P 500 futures trade in line with fair value.

Investors will receive just two economic reports today, and neither is expected to have much impact on the market. The September Job Openings and Labor Turnover Survey (JOLTS) will cross the wires at 10:00 ET and will be followed by the September Consumer Credit Report (Briefing.com consensus $18.3 billion), which will be released at 15:00 ET. The rest of the week's economic calendar looks much the same, containing few notable reports.

As for earnings, Snap (SNAP 14.86, +0.03), Marriott (MAR 122.25, +0.27), Zillow (ZG 41.00, +0.03), and Fossil (FOSL 7.05, +0.07) will report following today's close.

08:00AM ET

[BRIEFING.COM] S&P futures vs fair value: -1.00. Nasdaq futures vs fair value: -0.10.

Equities kicked off the week on a positive note yesterday, eking out their fifth consecutive win and another record high close. Wall Street looks to be on track for a flat open this morning as the S&P 500 futures trade one point below fair value. Elsewhere, indices in the Asia-Pacific region ended Tuesday mostly higher, while European bourses are trading slightly lower.

Crude futures are hovering a tick lower this morning after settling at their best level since July of 2015 on Monday; WTI crude futures are down 0.2% at $57.26/bbl. The commodity jumped 3.0% yesterday, giving energy stocks a big boost, following a weekend purge in Saudi Arabia that resulted in the arrests of current and former high-level officials and members of the royal family.

On a related note, the American Petroleum Institute will release its weekly crude inventory report this afternoon at 16:30 ET.

U.S. Treasuries are trading modestly lower this morning, giving back a good chunk of Monday's gains. The yield on the benchmark 10-yr Treasury note is up one basis point at 2.32% after slipping two basis points yesterday. Meanwhile, the U.S. Dollar Index is up 0.4% at 95.00--marking its highest level since mid-July.

The greenback has climbed 0.4% against the euro (1.1566), 0.3% against the pound (1.3136), and 0.4% against the yen (114.15).

On the data front, investors will receive two economic reports today--the September Job Openings and Labor Turnover Survey (JOLTS) and September Consumer Credit (Briefing.com consensus $18.3 billion). The reports will be released at 10:00 ET and 15:00 ET, respectively.

In U.S. corporate news:

Salesforce (CRM 105.90, +3.48): +3.4% after announcing a new strategic partnership with Alphabet (GOOG 1026.95, +1.05).

Priceline (PCLN 1718.00, -185.00): -9.7% after issuing disappointing earnings guidance for the fourth quarter.

TripAdvisor (TRIP 35.50, -4.03): -10.2% after reporting below-consensus revenues.

Avis Budget (CAR 36.00, -5.42): -13.1% after missing revenue estimates and cutting the high end of its guidance for the fiscal year.

Red Robin Gourmet (RRGB 53.55, -13.50): -20.1% after missing estimates for both earnings and revenues and issuing below-consensus guidance.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region ended Tuesday on a mostly higher note. Japan's Nikkei +1.7%, Hong Kong's Hang Seng +1.4%, China's Shanghai Composite +0.8%, India's Sensex -1.1%.

In economic data:

Japan's September Overtime Pay +0.9% year-over-year (last 1.5%) and Average Cash Earnings +0.9% year-over-year (consensus 0.6%; last 0.7%)

China's FX Reserves $3.109 trillion (expected $3.107 trillion; last $3.108 trillion)

Australia's AIG Construction Index 53.2 (last 54.7)

In news:

The Reserve Bank of Australia left its cash rate at 1.50%, as expected, but the central bank's statement was dovish, noting uncertainty associated with household consumption.

New Zealand's Prime Minister Jacinda Ardern said she is "not at all" concerned with the recent Kiwi weakness. The New Zealand dollar trades at 0.6924 against the U.S. dollar, hovering just above this year's low.

President Trump is in South Korea today, where he called on "every responsible nation, including China and Russia to act with urgency and with great determination" to implement sanctions against North Korea.

Major European indices trade near their flat lines. UK's FTSE -0.3%, France's CAC -0.1%, Germany's DAX unch.

In economic data:

Eurozone September Retail Sales +0.7% month-over-month (expected 0.6%; last -0.1%); +3.7% year-over-year (consensus 2.7%; last 2.3%). Retail PMI 51.1 (last 52.3)

Germany's September Industrial Production -1.6% month-over-month (expected -0.8%; last 2.6%)

UK's October Halifax House Price Index +0.3% month-over-month (expected 0.2%; last 0.8%); +4.5% year-over-year, as expected (last 4.0%)

France's Q4 Industrial Investments 4.0% (last 7.0%). September government budget balance -EUR76.30 billion (last -EUR93.00 billion)

Italy's September Retail Sales +0.9% month-over-month (expected 0.2%; last -0.2%); +3.4% year-over-year (last -0.1%)

In news:

Outgoing Eurogroup Chief Jeroen Dijsselbloem said the Eurogroup hopes to make a decision regarding a banking union in June. Reports from the recent Eurogroup meeting indicate that many members favored establishing a budget for stabilization purposes. This was the first Eurogroup meeting without the participation of Germany's Wolfgang Schaeuble.

European Central Bank President Mario Draghi said there is little evidence that negative rates are undermining the profitability of banks.

05:50AM ET

[BRIEFING.COM] S&P futures vs fair value: +0.30. Nasdaq futures vs fair value: -2.90.

05:50AM ET

[BRIEFING.COM] Nikkei...22938...+389.30...+1.70%

Hang Seng...28994...+397.50...+1.40%

05:50AM ET

[BRIEFING.COM] FTSE...7548.51...-13.80...-0.20%

DAX...13468.97...+0.20...0.00

04:30PM ET

[BRIEFING.COM] The U.S. equity market ticked higher on Monday, with all three major indices rewriting the record highs they posted on Friday. The Nasdaq and the S&P 500 added 0.3% and 0.1%, respectively, while the Dow (unch) eked out a narrow victory. The major indices traded within a pretty narrow range from start to finish.

Energy stocks led Monday's advance as the price of crude oil rallied to its highest level since July 2015; WTI crude futures finished higher by 3.0% at $57.29/bbl. The price increase followed a weekend purge in Saudi Arabia, in which Crown Prince Mohammed bin Salman imprisoned dozens of princes, ministers, and ex-ministers on allegations of corruption. The S&P 500's energy sector finished at the top of the day's sector standings with a gain of 2.2%.

The consumer discretionary sector (+0.7%) also finished comfortably ahead of the broader market. Within the group, 21st Century Fox (FOXA 27.45, +2.48) and Walt Disney (DIS 100.64, +2.00) jumped 9.9% and 2.0%, respectively, following a CNBC report that the two companies have discussed a deal in recent weeks that would result in Disney owning most of 21st Century Fox. Meanwhile, Michael Kors (KORS 54.62, +7.00) surged 14.7% after reporting better-than-expected earnings and revenues.

Conversely, telecoms within the S&P 500 struggled on Monday, losing 2.4%, after Sprint (S 5.90, -0.77) and T-Mobile US (TMUS 55.54, -3.37) announced that they failed to reach a merger agreement; the two companies lost 11.5% and 5.7%, respectively. However, Charter Communications (CHTR 348.40, +12.97) jumped 3.9% following reports that Softbank--the parent company of Sprint--is now willing to re-explore acquisition talks with the company.

The consumer staples sector (-1.1%) also underperformed amid broad weakness. Within the group, pharmacy retailer CVS Health (CVS 66.80, -2.45) and food distributor Sysco (SYY 54.17, -2.49) dropped 3.5% and 4.4%, respectively, despite reporting above-consensus earnings.

In other corporate news, Broadcom (AVGO 277.52, +3.89) submitted a $70 per share takeover offer for Qualcomm (QCOM 62.52, +0.71), which, if completed, would mark the largest technology acquisition in history. However, CNBC reported that Qualcomm is expected to reject Broadcom's offer. The two chipmakers finished with gains of more than 1.0% apiece.

Elsewhere, U.S. Treasuries finished mostly higher, with the yield on the benchmark 10-yr Treasury note slipping two basis points to 2.32%. However, the 2-yr Treasury note bucked the trend, sending its yield one basis point higher to 1.62%. Meanwhile, the U.S. Dollar Index slid 0.2% to 94.63.

Also of note, New York Fed President William Dudley announced his decision to retire in mid-2018. Mr. Dudley has headed the New York Fed since 2009.

Investors did not receive any economic data on Monday, but they will receive three reports on Tuesday--the NFIB Small Business Optimism Index at 7:00 ET, the September Job Openings and Labor Turnover Survey (JOLTS) at 10:00 ET, and September Consumer Credit (Briefing.com consensus $18.3 billion) at 15:00 ET.

Nasdaq Composite +26.1% YTD

Dow Jones Industrial Average +19.2% YTD

S&P 500 +15.7% YTD

Russell 2000 +10.4% YTD

Dow: +9.23… | Nasdaq: +22.00… | S&P: +3.29…

NASDAQ Adv/Dec 1431/1306. …NYSE Adv/Dec 1701/1246.

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Review of TheStrategyLab

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htmSpecial thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

Online user name

wrbtrader (more info about me)

@ http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com