Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htmFree Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htm TheStrategyLab Reviews: http://www.thestrategylab.com/thestrategylab-reviews.htm Price Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

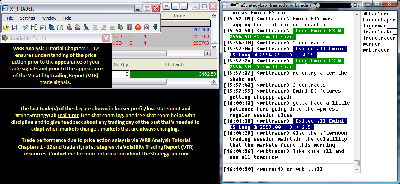

Attachment:

102517-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3462.50.png [ 96.41 KiB | Viewed 261 times ]

102517-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3462.50.png [ 96.41 KiB | Viewed 261 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini RTY ($RTY_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$3462.50 dollars or +69.25 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3462.50 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis. The risk of loss can be substantial. Therefore, you must carefully consider if trading is suitable for you within the context of your financial condition. We make no guarantees of success and your level of success is dependent upon other factors including your skill as a trader, knowledge, financial condition, market conditions and other factors. Trading is stressful and you should always consult a doctor in all matters relating to physical and mental health of you and your family because trading can impact beyond your financial condition regardless if you're a profitable or losing trader.Russell 2000 Emini RTY Futures: 1 tick or 0.10 = $5.00 dollars and there's more contract information @

CMEGroup (formerly as TF @

The ICE)

S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log is archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=172&t=2678 All of my trades are posted

real-time at the above link for today's archive chat log in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader for anyone to do a real-time review (you must be a member of the chat room for a real-time review). Although the trades are posted by me and other users of WRB Analysis in real-time...this is

not a signal calling chat room

nor is this a live trading room that has a head trader telling you what to do. I'm the moderator (I keep the peace between members) and my own live trades are posted within 3.2 seconds on average

after the trade confirmation in my broker trade execution platform via an

auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility...all key concepts from the WRB Analysis free study guide even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads.

Quote:

2017 has been the most difficult trading year since I've begun trading +25 years ago because successful trading involves more than just trade methods than any other trading year. This is a key concept many traders have difficulties in understanding. Some blame it on algorithms while I blame it on the inability to adapt, failure to backtest, failure to document trades (real-money or simulator) and underestimating how our environment influences our cognitive decision making while trading...all while trading in low volatility market conditions that statistically have the reputation for difficult trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room

nor is it a live trading room with a head trader telling you what to do even though members of the chat room are posting their trades & market analysis in real-time. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the

primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback about

your own trading and for members to help each other...as in more eyes on the market. In addition, we

highly recommend that you use the free chat room with a professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they can provide you with the

quantitative statistical analysis of your trading. You can then download your results and post them in your private thread at the forum.

Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your quantitative statistical analysis, brokerage statements in the free chat room. Instead, its highly recommended that you only post that particular information in your private thread for

security reasons. Yet, if you want to post that type of information at another website, blog or chat room...that's your choice.

TheStrategyLab free chat room is on IRC via

users request because the IRC servers are located in many different countries, software in many different languages, many different mobile apps, many different types of social media software can be used to log in along with IRC being easier to moderate via

script codes when trouble makers, spammers and trolls show up. I'm the

moderator of the free chat room via the user name

wrbtrader. Thus, I

keep the peace between members without hesitation in removing problematic traders so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets without being

trolled or harassed.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell nor do we allow the free chat room to be used for mentoring because we do

not offer a mentoring service. The

purpose of TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. If you join the free chat room and then you decide to

not post any WRB Analysis about the price action or you decide to not post your trades or you decide to be silent (lurk without saying a word about today's markets)...you're not using the free chat room properly to help improve your trading.

In fact, we do

not want silent (lurkers) traders to join the free chat room unless they are actively posting at the forum about their trading after the markets close.

Access instructions for the free chat room

@ http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Quote:

All of my real-time posted trades involves price action concepts from the

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always backtesting new concepts of WRB Analysis, new trade entry rules, new trade management rules, new position size management rules before application in real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades or sharing the new concepts with fee-base clients...living up to the name of my website. TheStrategy

Lab.

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=331&t=3532 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

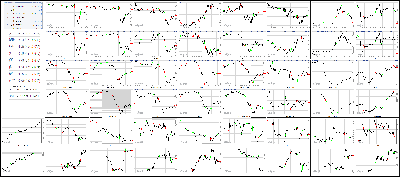

Attachment:

102517-Key-Price-Action-Markets.png [ 1.02 MiB | Viewed 250 times ]

102517-Key-Price-Action-Markets.png [ 1.02 MiB | Viewed 250 times ]

click on the above image to view today's price action of key markets The Market at 04:30PM ETDow: -112.30… | Nasdaq: -34.54… | S&P: -11.98…

NASDAQ Vol: ---… Adv: 925… Dec: 1582…

NYSE Vol: 910.0 mln… Adv: 762… Dec: 2207…

Moving the Market

Investors take some money off the table as equities hover at record highs

September New Home Sales and Durable Goods Orders beat estimates

John Taylor--who is considered hawkish--looks increasingly likely to land Fed Chair

Latest batch of earnings comes in mixed

Sector Watch

Strong: Technology, Health Care, Consumer Staples, Real Estate

Weak: Industrials, Energy, Telecom Services

04:30PM ET

[BRIEFING.COM] Stocks declined for the second time in three sessions on Wednesday, but an afternoon rally left the major indices a ways above their session lows. The Dow (-0.5%) and the Nasdaq (-0.5%) finished roughly in line with the S&P 500, which lost 0.5%. The benchmark index traded within a wide range, holding a loss between 0.1% and 1.0% throughout the session.

The S&P 500's telecom services sector led the retreat, finishing with a loss of 2.3%, after AT&T (T 33.49, -1.37) reported worse-than-expected earnings and revenues for the third quarter; AT&T shares lost 3.9%. Industrials also showed relative weakness, losing 1.0%. Within the group, Boeing (BA 258.42, -7.58) was among the weakest performers, shedding 2.9%, despite beating profit estimates.

As for the other sectors, most finished roughly in line with the broader market. The top-weighted technology space (-0.3%) outperformed slightly, thanks in part to Visa (V 109.49, +1.08), which added 1.0% on better-than-expected earnings and revenues. Alphabet (GOOGL 991.46, +2.97) also showed relative strength ahead of Thursday evening's earnings release.

However, the tech sector's semiconductor components struggled after Advanced Micro (AMD 12.33, -1.92) forecasted a decline in revenue for the fourth quarter. The PHLX Semiconductor Index dropped 1.3%, while AMD shares plunged 13.5%.

Chipotle Mexican Grill (CMG 277.01, -47.29) also dropped significantly on Wednesday, losing 14.6%, after posting a big miss on earnings and lowering its comparable sales guidance. However, the consumer discretionary sector (-0.4%) still beat the broader market, thanks in large part to Nike (NKE 54.94, +1.52), which jumped 2.9% after providing a solid five-year outlook at its investor day.

Dow component Coca-Cola (KO 46.05, -0.13) also reported earnings on Wednesday, beating both top and bottom line estimates, but slipped 0.3% nonetheless.

U.S. Treasuries ended on a lower note, sending yields higher across the curve; the benchmark 10-yr yield climbed four basis points to 2.44%. Speculation that Stanford University economist John Taylor, who is considered relatively hawkish, is likely to become the next Fed Chair helped fuel the sell off.

Reviewing Wednesday's batch of economic data, which included September New Home Sales, September Durable Orders, the August FHFA Housing Price Index, and the weekly MBA Mortgage Applications Index:

New Home Sales in September hit an annualized rate of 667,000, which is above the revised August rate of 561,000 (from 560,000), and higher than the Briefing.com consensus of 555,000.

The key takeaway from the report is that the sales increases were broad-based, underscoring the point that the rebound in new home sales, which are counted when a contract is signed, was not just a function of a rebound from the depressed activity in the South due to the hurricanes.

September durable goods orders rose 2.2%, which is more than the 1.3% increase expected by the Briefing.com consensus. The prior month's reading was revised to +2.0% (from +1.7%). Excluding transportation, durable orders increased 0.7% (Briefing.com consensus +0.5%) to follow the prior month's revised uptick of 0.7% (from +0.2%).

The key takeaway from the report is that it is hard data that corroborates the upbeat readings in the soft manufacturing surveys; moreover, it is going to lead to stronger Q3 GDP forecasts given the 0.7% increase in shipments of nondefense capital goods excluding aircraft, which followed an upwardly revised 1.2% increase (from +0.7%) for August.

The FHFA Housing Price Index rose 0.7% in August (Briefing.com consensus 0.4%), while the July reading was revised to 0.4% from 0.2%.

The weekly MBA Mortgage Applications Index decreased 4.6% to follow last week's 3.6% increase.

On Thursday, investors will receive just two economic reports--weekly Initial Claims (Briefing.com consensus 235K) and September Pending Home Sales. The two pieces of data will cross the wires at 8:30 ET and 10:00 ET, respectively.

Nasdaq Composite +21.9% YTD

Dow Jones Industrial Average +18.1% YTD

S&P 500 +14.2% YTD

Russell 2000 +10.1% YTD

Dow: -112.30… | Nasdaq: -34.54… | S&P: -11.98…

NASDAQ Adv/Dec 925/1582. …NYSE Adv/Dec 762/2207.

03:35PM ET

[BRIEFING.COM] Commodities end the day lower:

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently down 0.17% at 85.891

Dollar index is currently down 0.07% at 93.7

Oct WTI Crude is down 0.61% on the day.

Oil futures got a boost following reports that Saudi Arabia and Russia want to extend the current OPEC/non-OPEC oil cut deal through the end of 2018

EIA inventory data showed a build of 0.9 mln barrels

Futures settle $0.32 lower to $52.15/barrel.

In other energy, Nov Natural Gas settled down $0.05 at $2.92/MMBtu

On the metals:

Dec Gold gained $0.8 to settle at $1279.1/oz, while Dec silver lost $0.04 to $16.93/oz

Dec Copper dropped $0.02 to $3.18/lb

Finally, agriculture:

Dec Corn settled unchanged at $3.51/bu.

Nov soy settled flat at $0.34/bu.

Dec Wheat settled down $0.01 at $4.35/bu.

Dow: -109.61… | Nasdaq: -31.56… | S&P: -10.56…

NASDAQ Adv/Dec 951/1654. …NYSE Adv/Dec 784/2181.

03:00PM ET

[BRIEFING.COM] The major U.S. indices remain solidly lower moving into the final stretch, but they are trading a ways above their worst marks of the day. The S&P 500 and the Dow currently hold losses of 0.5% apiece, while the Nasdaq (-0.6%) trades a tick below its peers.

On the earnings front, Amgen (AMGN 177.10, -3.27) and O'Reilly Auto (ORLY 202.16, -1.33) will deliver their quarterly reports following today's closing bell, while Comcast (CMCSA 36.67, +0.17), UPS (UPS 118.74, -0.96), Celgene (CELG 119.19, -1.15), and Ford Motor (F 12.03, -0.16) will report tomorrow morning, along with many other other notable names.

As for economic data, investors will receive just two reports on Thursday--weekly Initial Claims (Briefing.com consensus 235K) and September Pending Home Sales. The two pieces of data will cross the wires at 8:30 ET and 10:00 ET, respectively.

Dow: -120.30… | Nasdaq: -41.56… | S&P: -13.57…

NASDAQ Adv/Dec 854/1832. …NYSE Adv/Dec 676/2278.

02:30PM ET

[BRIEFING.COM] Stocks have continued trimming their losses, bringing the S&P 500 within 0.4% of its unchanged mark.

Chipmakers are broadly lower this afternoon, evidenced by the PHLX Semiconductor Index, which is down 1.2%. Advanced Micro (AMD 12.59, -1.65) is by far the weakest semiconductor name, plunging 11.6%, after forecasting a decline in revenue for the fourth quarter. Texas Instruments (TXN 95.09, -1.36) is also lower, showing a loss of 1.4%, despite reporting better-than-expected earnings and revenues.

Still, the top-weighted technology sector (-0.3%), which houses chipmakers, has managed to keep ahead of the broader market. Within the group, Alphabet (GOOGL 989.85, +1.36) shows particular strength ahead of tomorrow's earnings release; GOOGL shares are higher by 0.1%.

Dow: -95.55… | Nasdaq: -32.86… | S&P: -10.76…

NASDAQ Adv/Dec 944/1751. …NYSE Adv/Dec 730/2218.

02:00PM ET

[BRIEFING.COM] Equities have retraced a portion of their earlier losses, leaving the major indices in the middle of their tradings ranges; the S&P 500 is down 0.6%.

All 11 sectors are still trading in the red, but the health care space (-0.1%) has nearly made it back to its flat line. Most of the other groups hold losses between 0.4% and 0.7%, but the industrials (-1.1%) and and telecom services (-2.2%) sectors show relative weakness. For the week, the telecom services group is by far the weaskest performer, showing a week-to-date loss of 3.6%.

In Washington, President Trump said he likes Fed Chair Janet Yellen, but needs to "make his own mark" on the Fed. Reports suggest that the two leading candidates to replace Ms. Yellen are Fed Governor Jerome Powell and Stanford University economist John Taylor.

Dow: -121.85… | Nasdaq: -40.73… | S&P: -14.08…

NASDAQ Adv/Dec 952/1765. …NYSE Adv/Dec 671/2259.

01:30PM ET

[BRIEFING.COM] The major U.S. indices remain under notable pressure in afternoon trading in a broad-based selloff.

A look inside the Dow Jones Industrial Average shows that Boeing (BA 256.62, -9.38), General Electric (GE 21.31, -0.58), & Caterpillar (CAT 134.97, -3.27) are underperforming. Boeing is under pressure, and weighing on the Dow following this morning's earnings report, while GE is seeing continued weakness to fresh multi-year lows.

Conversely, Nike (NKE 55.01, +1.59) is the best-performing Dow component after the company provided a solid five-year outlook at today's Investor Day.

With the pullback, the DJIA has slipped into negative territory for the week.

Elsewhere, at the top of the hour, the Treasury's $34 bln 5-year auction drew a high yield of 2.058% on a bid-to-cover of 2.44.

Dow: -158.74… | Nasdaq: -48.16… | S&P: -17.64…

NASDAQ Adv/Dec 799/1916. …NYSE Adv/Dec 496/2432.

01:05PM ET

[BRIEFING.COM] Equities have been tumbling today following a string of record closes and a mixed bag of earnings. The major indices opened the session slightly below their flat lines, but have been extending those losses ever since. At midday, stocks hover near their session lows, with the S&P 500, the Nasdaq, and the Dow showing losses between 0.7% and 0.9%.

The stock market was likely overdue for a pullback coming into the midweek session, but some additional factors have helped fuel today's sell off, namely a little nervousness that Stanford University economist John Taylor--who is considered relatively hawkish--may become the next Fed Chair and worries that Senator Jeff Flake (R-AZ) may work against GOP legislation following his decision not to run for re-election.

In addition, the latest batch of earnings had some notable disappointments. For instance, Chipotle Mexican Grill (CMG 276.58, -47.74) has plunged 14.8% after posting a big miss on earnings and lowering its comparable sales guidance. Similarly, Advanced Micro (AMD 12.39, -1.86) is down 13.0% after forecasting a decline in revenue for the fourth quarter.

Even some of the companies that beat earnings expectations have moved lower today, including Dow component Boeing (BA 255.01, -10.88), which is down 4.1%. Fellow Dow components Visa (V 109.58, +1.17) and Coca-Cola (KO 46.14, -0.04) also reported better-than-expected earnings, but have had better luck than Boeing. Visa is up 1.1%, while Coca-Cola trades flat.

Wireless giant AT&T (T 33.51, -1.34) has dragged the S&P 500's telecom services sector to the bottom of today's leaderboard, extending the group's huge year-to-date loss to 15.6%. AT&T is lower by 3.8% after reporting worse-than-expected earnings and revenues. The telecom services space is lower by 2.2%.

As for the ten remaining sectors, losses range from 0.3% to 1.4%. The health care space (-0.3%) shows relative strength, thanks to positive performances from select names, including Anthem (ANTM 202.96, +7.71), Thermo Fisher (TMO 198.88, +4.50), and Express Scripts (ESRX 60.63, +1.78). The three companies reported mostly better-than-expected results and sport gains between 2.3% and 4.0%.

In the bond market, U.S. Treasuries are trading lower, sending yields higher across the curve; the benchmark 10-yr yield is up three basis points at 2.44%. Meanwhile, the yield on the 2-yr Treasury note has also climbed three basis points and currently hovers at 1.60%.

Reviewing Wednesday's batch of economic data, which included September New Home Sales, September Durable Orders, the August FHFA Housing Price Index, and the weekly MBA Mortgage Applications Index:

New Home Sales in September hit an annualized rate of 667,000, which is above the revised August rate of 561,000 (from 560,000), and higher than the Briefing.com consensus of 555,000.

The key takeaway from the report is that the sales increases were broad-based, underscoring the point that the rebound in new home sales, which are counted when a contract is signed, was not just a function of a rebound from the depressed activity in the South due to the hurricanes.

September durable goods orders rose 2.2%, which is more than the 1.3% increase expected by the Briefing.com consensus. The prior month's reading was revised to +2.0% (from +1.7%). Excluding transportation, durable orders increased 0.7% (Briefing.com consensus +0.5%) to follow the prior month's revised uptick of 0.7% (from +0.2%).

The key takeaway from the report is that it is hard data that corroborates the upbeat readings in the soft manufacturing surveys; moreover, it is going to lead to stronger Q3 GDP forecasts given the 0.7% increase in shipments of nondefense capital goods excluding aircraft, which followed an upwardly revised 1.2% increase (from +0.7%) for August.

The FHFA Housing Price Index rose 0.7% in August (Briefing.com consensus 0.4%), while the July reading was revised to 0.4% from 0.2%.

The weekly MBA Mortgage Applications Index decreased 4.6% to follow last week's 3.6% increase.

Dow: -162.62… | Nasdaq: -54.38… | S&P: -18.73…

NASDAQ Adv/Dec 726/1996. …NYSE Adv/Dec 483/1460.

12:25PM ET

[BRIEFING.COM] Equity indices begin the afternoon at fresh session lows, with the Nasdaq (-1.1%) leading today's sizable retreat.

The industrial sector (-1.2%) is struggling today amid broad weakness. As mentioned in the prior comment, aerospace heavyweight Boeing (BA 256.49, -9.51) shows particular weakness, but airlines are also underperforming, especially Alaska Air (ALK 73.58, -5.81), which is down 7.4% after missing earnings estimates.

Railroads are also broadly lower, with Norfolk Southern (NSC 127.36, -4.95) pacing the retreat. The company is down 3.7% despite reporting above-consensus earnings this morning. Railroad peer Union Pacific (UNP 110.49, -2.41) will report its quarterly results on Thursday.

Dow: -164.19… | Nasdaq: -69.44… | S&P: -22.20…

NASDAQ Adv/Dec 620/2131. …NYSE Adv/Dec 379/2552.

12:00PM ET

[BRIEFING.COM] Equity indices continue drifting near their recent levels, with the Dow Jones Industrial Average (-0.5%) showing relative strength.

Within the Dow, Visa (V 109.89, +1.51) is one of the few components trading in the green after the credit card company beat both top and bottom line estimates this morning; V shares are up 1.5%. Coca-Cola (KO 46.10, -0.07) also shows relative strength, trading lower by just 0.2%, after reporting above-consensus earnings and revenues.

Meanwhile, Boeing (BA 258.16, -7.82) is the weakest Dow component, showing a loss of 3.0%, despite reporting better-than-expected earnings.

Dow: -122.08… | Nasdaq: -63.69… | S&P: -18.15…

NASDAQ Adv/Dec 653/2109. …NYSE Adv/Dec 423/2481.

11:25AM ET

[BRIEFING.COM] Stocks have extended their losses in recent action; the S&P 500 is now lower by 0.7%.

The telecom services sector (-2.2%) still leads today's retreat as shares of wireless giant AT&T (T 33.74, -1.11) continue to sell off following the company's below-consensus earnings and revenues. As for the ten remaining sectors, most hold losses somewhere between 0.5% and 0.9%. The only exception is the health care group, which is lower by just 0.2%.

Anthem (ANTM 205.83, +10.58), Thermo Fisher (TMO 198.52, +4.14), and Express Scripts (ESRX 60.41, +1.51) have helped keep the health care group ahead of the broader market, adding between 2.1% and 5.4%, following their quarterly earnings. Both Anthem and Thermo Fisher beat profit estimates, while Express Scripts met expectations.

Dow: -112.78… | Nasdaq: -67.54… | S&P: -18.67…

NASDAQ Adv/Dec 573/2213. …NYSE Adv/Dec 382/2513.

10:55AM ET

[BRIEFING.COM] The major indices are trading near their freshly minted session lows this morning, with the S&P 500 (-0.5%) exhibiting relative weakness.

Just moments ago, the Energy Information Administration released its weekly crude inventory report, which showed that U.S. stockpiles increased by 0.9 million barrels last week. The EIA reading was seen as a disappointment considering the consensus estimate called for a draw of 3.0 million barrels. Nonetheless, the price of crude oil hasn't shifted much following the release; WTI crude futures are down 0.4% at $52.24 per barrel.

Meanwhile, the S&P 500's energy sector is hovering roughly in line with the broader market, showing a loss of 0.4%. Dow components Chevron (CVX 118.94, -0.29) and Exxon Mobil (XOM 83.41, -0.07) are down 0.3% and 0.1%, respectively.

Dow: -71.04… | Nasdaq: -25.40… | S&P: -11.90…

NASDAQ Adv/Dec 869/1911. …NYSE Adv/Dec 529/2336.

10:30AM ET

[BRIEFING.COM] Commodities begin the day flat :

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently unchanged at 86.0787

Dollar index is currently down 0.15% at 93.63

Dec WTI crude is currently flat on the day.

The EIA reported crude oil inventories had a build of 0.9 mln barrels for the week ended Oct 20th

Futures are $0.25 lower to $52.22/barrel.

In other energy, Nov natural gas is down $0.02 at $2.95/MMBtu

Metals:

Dec gold lost $1.6 and trades at $1276.7/oz, while Dec silver lost $0.01 to $16.96/oz

Dec copper remains unchanged at $3.18/lb

Finally, agriculture:

Dec corn is up $0.02 at $3.55/bu.

Nov soy is unchanged $0 at $0.34/bu.

Dec wheat is flat at $4.43/bu.

Dow: -61.63… | Nasdaq: -18.38… | S&P: -10.83…

NASDAQ Adv/Dec 909/1871. …NYSE Adv/Dec 563/2275.

10:00AM ET

[BRIEFING.COM] Stocks have slipped from their opening levels in recent action, sending the S&P 500 lower by 0.3%

Just in, New Home Sales in September hit an annualized rate of 667,000, which is above the revised August rate of 561,000 (from 560,000), and higher than the Briefing.com consensus of 555,000.

Dow: -17.25… | Nasdaq: -15.85… | S&P: -6.73…

NASDAQ Adv/Dec 1046/1631. …NYSE Adv/Dec 799/1909.

09:40AM ET

[BRIEFING.COM] The major U.S. indices are relatively flat in the opening minutes of today's session, with the S&P 500 holding a slim loss of 0.1%.

Most sectors are lower this morning, but losses have been modest for the most part. The telecom services sector (-1.4%) is easily the worst-performing sector, thanks to AT&T (T 34.13, -0.72), which is down 2.1% after reporting below-consensus earnings and revenues yesterday evening. As for the other laggards, most sectors hold losses of no more than 0.4%.

The heavily-weighted financial sector (+0.1%) exhibits relative strength in the early going, benefiting from an increase in interest rates. A sell off in the bond market has pushed yields higher across the curve, with the benchmark 10-yr yield climbing four basis points to 2.45%.

As a reminder, September New Home Sales (Briefing.com consensus 555K) will be released at 10:00 ET.

Dow: +8.09… | Nasdaq: -4.24… | S&P: -2.94…

NASDAQ Adv/Dec 1152/1407. …NYSE Adv/Dec 892/1725.

09:14AM ET

[BRIEFING.COM] S&P futures vs fair value: -4.00. Nasdaq futures vs fair value: -14.60.

The stock market is on track to open Wednesday's session modestly lower as the S&P 500 futures trade four points, or 0.1%, below fair value.

A number of notable companies have reported quarterly earnings since yesterday's closing bell. On the upside, Walgreens Boot Alliance (WBA 70.22, +2.93) is up 4.4% in pre-market trade after beating earnings estimates. Visa (V 109.60, +1.19) is also trading higher, up 1.1%, after reporting better-than-expected earnings and revenues.

On the downside, Chipotle Mexican Grill (CMG 284.80, -39.50) is lower by 12.2% after posting a big miss on earnings and lowering its comparable sales guidance. Advanced Micro (AMD 12.88, -1.39) is also solidly lower, losing 9.7%, after forecasting a decline in revenue for the fourth quarter.

WTI crude is down 0.5% at $52.22 per barrel following last night's inventory report from the American Petroleum Institute, which showed a build of 0.5 million barrels for the week ended October 13. The official government figures from the Department of Energy will be released later this morning at 10:30 ET.

As for economic data, durable goods orders increased more than expected in September, climbing 2.2% (Briefing.com consensus 1.3%). The August reading was upwardly revised to 2.0% from 1.7%. Excluding transportation, durable orders increased 0.7% in September (Briefing.com consensus +0.5%), and the August reading was revised to 0.7% from 0.2%.

U.S. Treasuries extended their losses following the durable goods release, sending yields to fresh overnight highs. The benchmark 10-yr yield is currently up five basis points at 2.46%, while the yield on the 2-yr Treasury note is higher by three basis points at 1.60%.

Investors also received two additional economic reports this morning--the August FHFA Housing Price Index and the weekly MBA Mortgage Applications Index. The FHFA Housing Price Index rose 0.7% in August (Briefing.com consensus 0.4%), while the July reading was revised to 0.4% from 0.2%. Meanwhile, the weekly MBA Mortgage Applications Index decreased 4.6%.

Today's last economic report--September New Home Sales (Briefing.com consensus 555K)--will be released at 10:00 ET.

08:50AM ET

[BRIEFING.COM] S&P futures vs fair value: -3.90. Nasdaq futures vs fair value: -13.60.

The S&P 500 futures trade four points, or 0.1%, below fair value.

Equity indices in the Asia-Pacific region ended the midweek affair on a mostly higher note while Japan's Nikkei (-0.5%) recorded its first loss in the past 17 sessions. The pullback in the Nikkei took place amid a spike in the yen, but the Japanese currency surrendered that gain shortly after the Asian session ended. Chinese debt retreated, pushing up the country's 10-yr yield to 3.77%, the highest level in three years. The Australian dollar (0.7703) has retreated 0.9% against the U.S. dollar following cooler than expected inflation data. Reports suggest Japan's government is considering tax benefits for companies that raise wages.

In economic data:

Australia's Q3 CPI +0.6% quarter-over-quarter (expected 0.8%; last 0.2%); +1.8% year-over-year (consensus 2.0%; last 1.9%). Q3 Trimmed Mean CPI +0.4% quarter-over-quarter (expected 0.5%; last 0.5%); +1.8% year-over-year (consensus 2.0%; last 1.8%)

---Equity Markets---

Japan's Nikkei lost 0.5%. Dentsu, DeNA, Kirin Holdings, Tokyo Gas, J Front Retailing, KDDI, Familymart, Meiji Holdings, Casio, and Fanuc posted losses between 1.1% and 4.1%. On the upside, Kobe Steel, Komatsu, SUMCO, and Yamaha Motor advanced between 1.7% and 3.7%.

Hong Kong's Hang Seng rose 0.5%. Energy-related names like CNOOC, China Shenhua Energy, Kunlun Energy, and PetroChina gained between 0.8% and 2.4% while gaming names Tencent Holdings and Sands China both gained near 1.0%.

China's Shanghai Composite added 0.3%. Joincare Pharmaceutical, Shanghai Fosun Pharmaceutical, Hainan HNA Infrastructure Investment, Sichuan Langsha Holding, and Tonghua Dongbao Pharmaceutical posted gains between 4.2% and 5.3%.

India's Sensex jumped 1.3% to a fresh record high. Financials outperformed after the government announced a capital infusion plan for state-owned banks and a road development program. SBI soared 27.6% while ICICI Bank and AXIS Bank spiked 14.7% and 4.6%, respectively. Tech consultants like Infosys and Wipro both gained near 0.9% while Tata Consultancy lost 0.8%.

Major European indices trade on a mostly flat note while Spain's IBEX (+0.4%) outperforms. The Catalan Parliament will be in session tomorrow morning to plot a response to Madrid's activation of Article 155. Spanish Prime Minister Mariano Rajoy said that an election in Catalonia is the 'only way out.' Italy's Senate will vote tomorrow on a new electoral law that would allow coalition talks between parties to take place prior to elections. It is believed Italy's 5-Star Movement will be hurt the most by the passage of the new law. The European Central Bank is expected to provide some insight about the future of its asset purchase program tomorrow.

In economic data:

Germany's October Ifo Business Climate Index 116.7 (expected 115.2; last 115.3). October Current Assessment 124.8 (expected 123.5; previous 123.7) and October Business Expectations 109.1 (consensus 107.3; last 107.5)

UK's Q3 GDP +0.4% quarter-over-quarter (expected 0.3%; last 0.3%); +1.5% year-over-year (consensus 1.4%; last 1.5%). Index of Services +0.4%, as expected. BBA Mortgage Approvals 41,600 (expected 41,900; last 41,800)

Italy's August Industrial New Orders +8.7% month-over-month (last 0.4%); +12.2% year-over-year (last 10.1%). August Industrial Sales +2.0% month-over-month (last -0.2%); +3.4% year-over-year (last 4.0%)

Spain's PPI +3.4% year-over-year (last 3.3%)

Swiss September Consumption Indicator 1.56 (last 1.50) and October ZEW Expectations 32.0 (last 28.0)

---Equity Markets---

UK's FTSE is down 0.5%. Miners are among the laggards with Antofagasta, Fresnillo, BHP Billiton, Anglo American, Rio Tinto, and Randgold Resources showing losses between 1.7% and 4.7%. Consumer stocks like GKN, Whitbread, Associated British Foods, Sainsbury, and Tesco are down between 0.7% and 2.0%.

Germany's DAX hovers just above its flat line. Lufthansa has spiked 3.1% despite missing expectations. Heavyweights like BASF, Commerzbank, Deutsche Bank, Allianz, and SAP show gains between 0.3% and 1.5%. Utilities lag with RWE and E.On both down near 1.6%.

France's CAC trades up 0.2% with Kering jumping 7.2% after beating expectations. Cap Gemini, Louis Vuitton, Accor, AXA, and Michelin show gains between 0.3% and 3.9%. Financials trade in the middle of the pack with Credit Agricole, BNP Paribas, and Societe Generale holding gains of around 0.2% apiece.

Spain's IBEX has climbed 0.4%. Acciona, Caixabank, BBVA, Santander, and Bankinter are up between 0.9% and 1.9%.

08:32AM ET

[BRIEFING.COM] S&P futures vs fair value: -2.80. Nasdaq futures vs fair value: -8.50.

The S&P 500 futures trade three points, or 0.1%, below fair value.

Just in, September durable goods orders rose 2.2%, which is more than the 1.3% increase expected by the Briefing.com consensus. The prior month's reading was revised to +2.0% (from +1.7%). Excluding transportation, durable orders increased 0.7% (Briefing.com consensus +0.5%) to follow the prior month's revised uptick of 0.7% (from +0.2%).

08:00AM ET

[BRIEFING.COM] S&P futures vs fair value: -3.30. Nasdaq futures vs fair value: -10.80.

Equity futures are pointing to a modestly lower open for the U.S. equity market, which has had a mixed performance so far this week. The S&P 500 futures are currently trading three points, or 0.1%, below fair value. Coming into Wednesday's session, the benchmark index holds a week-to-date loss of 0.2% and trades just six points below its record close.

Investors have received another large batch of earnings since yesterday's close, but the market's reaction has been largely negative thus far. Some of the most notable pre-market movers are Chipotle Mexican Grill (CMG 290.00, -34.30) and Advanced Micro (AMD 12.85, -1.40), which are down around 10.0% apiece. Chipotle posted a big miss on earnings, while AMD issued downbeat guidance.

U.S. Treasuries are trading lower this morning, sending yields higher across the curve; the benchmark 10-yr yield is up four basis points at 2.45%.

WTI crude is down 0.3% at $52.32 per barrel following last night's inventory report from the American Petroleum Institute, which showed a build of 0.5 million barrels for the week ended October 13. The official government figures from the Department of Energy will be released later this morning at 10:30 ET.

On the data front, investors will receive several economic reports today, including September Durable Orders (Briefing.com consensus 1.3%) at 8:30 ET, the August FHFA Housing Price Index (Briefing.com consensus 0.4%) at 9:00 ET, and September New Home Sales (Briefing.com consensus 555K) at 10:00 ET.

In addition, the weekly MBA Mortgage Applications Index, which was released earlier this morning, decreased 4.6% to follow last week's 3.6% increase.

In U.S. corporate news:

AT&T (T 34.15, -0.71): -2.0% after reporting worse-than-expected earnings and revenues.

Walgreens Boot Alliance (WBA 70.20, +2.91): +4.3% after reporting better-than-expected earnings.

Chipotle Mexican Grill (CMG 290.00, -34.30): -10.6% after posting a big miss on earnings and lowering its comparable sales guidance.

Advanced Micro (AMD 12.85, -1.40): -9.8% after forecasting a decline in revenue for the fourth quarter.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region ended the midweek affair on a mostly higher note while Japan's Nikkei recorded its first loss in the past 17 sessions. Japan's Nikkei -0.5%, Hong Kong's Hang Seng +0.5%, China's Shanghai Composite +0.3%, India's Sensex +1.3%.

In economic data:

Australia's Q3 CPI +0.6% quarter-over-quarter (expected 0.8%; last 0.2%); +1.8% year-over-year (consensus 2.0%; last 1.9%). Q3 Trimmed Mean CPI +0.4% quarter-over-quarter (expected 0.5%; last 0.5%); +1.8% year-over-year (consensus 2.0%; last 1.8%)

In news:

Chinese debt retreated, pushing up the country's 10-yr yield to 3.77%, the highest level in three years.

The Australian dollar (0.7705) has retreated 0.9% against the U.S. dollar following cooler than expected inflation data.

Reports suggest Japan's government is considering tax benefits for companies that raise wages.

Major European indices trade on a mostly flat note while Spain's IBEX (+0.5%) outperforms. UK's FTSE -0.2%, Germany's DAX unch, France's CAC +0.4%.

In economic data:

Germany's October Ifo Business Climate Index 116.7 (expected 115.2; last 115.3). October Current Assessment 124.8 (expected 123.5; previous 123.7) and October Business Expectations 109.1 (consensus 107.3; last 107.5)

UK's Q3 GDP +0.4% quarter-over-quarter (expected 0.3%; last 0.3%); +1.5% year-over-year (consensus 1.4%; last 1.5%). Index of Services +0.4%, as expected. BBA Mortgage Approvals 41,600 (expected 41,900; last 41,800)

Italy's August Industrial New Orders +8.7% month-over-month (last 0.4%); +12.2% year-over-year (last 10.1%). August Industrial Sales +2.0% month-over-month (last -0.2%); +3.4% year-over-year (last 4.0%)

Spain's PPI +3.4% year-over-year (last 3.3%)

Swiss September Consumption Indicator 1.56 (last 1.50) and October ZEW Expectations 32.0 (last 28.0)

In news:

The Catalan Parliament will be in session tomorrow morning to plot a response to Madrid's activation of Article 155. Spanish Prime Minister Mariano Rajoy said that an election in Catalonia is the 'only way out.'

Italy's Senate will vote tomorrow on a new electoral law that would allow coalition talks between parties to take place prior to elections. It is believed Italy's 5-Star Movement will be hurt the most by the passage of the new law.

The European Central Bank is expected to provide some insight about the future of its asset purchase program tomorrow.

05:49AM ET

[BRIEFING.COM] S&P futures vs fair value: flat. Nasdaq futures vs fair value: flat.

05:49AM ET

[BRIEFING.COM] Nikkei

...21708...-97.60...-0.50%

Hang Seng

...28303...+147.90...+0.50%

05:49AM ET

[BRIEFING.COM] FTSE

...7495.14...-31.40...-0.40%

DAX

...13002.26...-10.70...-0.10%

04:30PM ET

[BRIEFING.COM] The stock market crept higher on Tuesday, notching its first win of the week, following a largely solid batch of third quarter earnings. Caterpillar (CAT 138.24, +6.56) and 3M (MMM 234.65, +13.10) pushed the Dow (+0.7%) to a new record high after reporting particularly strong Q3 results, while the S&P 500 (+0.2%) and the Nasdaq (+0.2%) finished with more modest gains.

Caterpillar and 3M both reported stronger-than-expected earnings and revenues on Tuesday morning and raised their guidance for fiscal year 2017. The two industrial giants climbed 5.0% and 5.9%, respectively, helping the S&P 500's industrial sector (+0.5%) settle near the top of the sector standings.

However, fellow industrial giant--and Dow component--United Technologies (UTX 119.74, -1.15) tumbled 1.0%, despite beating third quarter profit estimates.

The lightly-weighted materials sector (+0.6%) finished roughly in line with the industrial space, but the heavily-weighted financial sector (+0.7%) did even better, making the most of a curve-steepening trade in the bond market. Treasuries finished mixed, with the yield on the benchmark 10-yr Treasury note climbing three basis points to 2.41%, while the 2-yr yield slipped one basis point to 1.57%.

McDonald's (MCD 163.88, +0.54) advanced 0.3% on Tuesday, even though its third quarter earnings fell short of expectations. The opposite was true for health care giants Eli Lilly (LLY 85.17, -2.01) and Biogen (BIIB 315.73, -12.82), which tumbled 2.3% and 3.9%, respectively, despite reporting stronger-than-expected earnings and revenues.

The health care sector (-0.7%) finished at the bottom of the sector standings, alongside other countercyclical groups like consumer staples (-0.3%) and telecom services (-0.6%). In general, cyclical sectors outperformed their countercyclical peers on Tuesday, signaling an increased appetite for risk among investors.

In Washington, Senator Jeff Flake (R-AZ) announced that he will not run for re-election in 2018. Mr. Flake has been a critic of President Trump and will be a Senator to watch as he now seemingly has fewer political consequences if he decides to vote against Republican legislation. The GOP holds just a two-seat majority in the Senate.

Investors did not receive any economic data on Tuesday.

However, on Wednesday, market participants will receive several economic reports, including the weekly MBA Mortgage Applications Index at 7:00 ET, September Durable Orders (Briefing.com consensus 1.3%) at 8:30 ET, the August FHFA Housing Price Index (Briefing.com consensus 0.4%) at 9:00 ET, and September New Home Sales (Briefing.com consensus 555K) at 10:00 ET.

Nasdaq Composite +22.6% YTD

Dow Jones Industrial Average +18.6% YTD

S&P 500 +14.8% YTD

Russell 2000 +10.6% YTD

Dow: +167.80… | Nasdaq: +11.60… | S&P: +4.15…

NASDAQ Adv/Dec 1330/1385. …NYSE Adv/Dec 1558/1343.

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Review of TheStrategyLab

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htmSpecial thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

Online user name

wrbtrader (more info about me)

@ http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com