Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htmFree Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htm TheStrategyLab Reviews: http://www.thestrategylab.com/thestrategylab-reviews.htm Price Action Trading: http://www.thestrategylab.com/price-action-trading.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

Stocktwits @

http://stocktwits.com/wrbtrader (24/7)

Twitter @

http://twitter.com/wrbtrader (24/7)

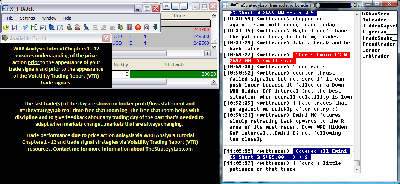

Attachment:

092617-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+300.00.png [ 96.47 KiB | Viewed 241 times ]

092617-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+300.00.png [ 96.47 KiB | Viewed 241 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini RTY ($RTY_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$300.00 dollars or +6.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $300.00 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini RTY Futures: 1 tick or 0.10 = $5.00 dollars and there's more contract information @

CMEGroup (formerly as TF @

The ICE)

S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room via the user name

wrbtrader for anyone to do a real-time review. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility even though the free chat room is not design to be an education chat room because the education is

only performed at the forums in the private threads. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=171&t=2651  ##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. In addition, we

highly recommend that you use the free chat room with a professional trade journal software like tradebench.com, edgewonk.com, tradervue.com, tradingdiarypro.com, stocktickr.com, journalsqrd.com, tradingdiary.pro, mxprofit.com or trademetria.com because they can provide you with the

quantitative statistical analysis of your trading. You can then download your results and post them in your private thread at the forum. Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. TheStrategyLab free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages, many different mobile apps and many different types of social media software can be used to log in. I'm the

moderator of the free chat room via the user name

wrbtrader. Thus, I

keep the peace between members without hesitation in removing trouble makers so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets without being trolled.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell. TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Quote:

All of my real-time posted trades involves price action concepts from the

WRB Analysis free study guide,

Advance WRB Analysis Tutorial Chapters 4 - 12 and the

Volatility Trading Report (VTR) trade signal strategies. Yet, I'm always backtesting new concepts of WRB Analysis, new entries, new trade management, new position size management and then directly testing them real money trades (small position size trades) to adapt to changed market conditions

prior to large position size trades or sharing the new concepts with fee-base clients...living up to the name of my website. TheStrategy

Lab.

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=327&t=3486 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

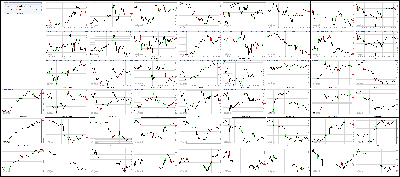

Attachment:

092617-Key-Price-Action-Markets.png [ 822.98 KiB | Viewed 224 times ]

092617-Key-Price-Action-Markets.png [ 822.98 KiB | Viewed 224 times ]

click on the above image to view today's price action of key markets The Market at 04:30PM ETDow: -11.77… | Nasdaq: +9.57… | S&P: +0.18…

NASDAQ Vol: 1.92 bln… Adv: 1556… Dec: 1114…

NYSE Vol: 738.0 mln… Adv: 1637… Dec: 1274…

Moving the Market

Tech stocks bounce back from Monday's decline; Apple (AAPL) shows particular strength

Sector Watch

Strong: Technology

Weak: Energy, Materials, Health Care, Utilities, Telecom Services

04:30PM ET

[BRIEFING.COM] Equities finished mixed on Tuesday as the broader market largely ignored a modest bounce-back performance from the technology sector (+0.4%)--which moved sharply lower on Monday. The tech-heavy Nasdaq climbed 0.2%, the S&P 500 finished just a tick above its flat line, and the Dow slipped 0.1%.The Russell 2000 (+0.3%) settled at a fresh record high for the third session in a row.

The technology sector never touched negative territory on Tuesday, but the magnitude of its gain did fluctuate a bit, hovering between 0.01% and 0.84%. However, the sector's top component by market cap--Apple (AAPL 153.14, +2.59)--remained strong throughout the session, determined to end its four-session losing streak. AAPL shares settled higher by 1.7%.

Meanwhile, NVIDIA (NVDA 171.96, +0.96) was strong early following news that it will provide GPU hardware to several Chinese tech giants, but weakened throughout the day. The chipmaker hit a new session low in the late afternoon following a report that Tesla (TSLA 345.25, +0.26) will use Intel (INTC 37.47, +0.31) technology for infotainment instead of NVIDIA.

Still, NVIDIA managed to contribute to the technology rally, settling higher by 0.6%. Red Hat (RHT 110.07, +4.31) also contributed (+4.1%), jumping to its best level in nearly two decades, after beating both top and bottom line estimates and issuing upbeat guidance.

Outside of the tech sector, Darden Restaurants (DRI 77.71, -5.43), the owner of brands like Olive Garden and LongHorn Steakhouse, dropped 6.5% despite reporting in-line earnings and revenues. Conversely, Carnival (CCL 65.32, +1.82) climbed 2.9% after reporting better-than-expected top and bottom lines.

The S&P 500's consumer discretionary sector, which houses both Darden Restaurants and Carnival, finished slightly behind the broader market, ticking down 0.1%. In general, sector movement was pretty modest as eight of the eleven groups settled within 0.2% of their unchanged marks.

Fed Chair Janet Yellen spoke at a NABE meeting in Cleveland on Tuesday, defending a gradual path of rate hikes despite continued uncertainty in the area of inflation. Her comments did not move either the stock market or the Treasury market, which declined modestly, sending yields slightly higher.

The yield on the benchmark 10-yr Treasury note climbed one basis point to 2.23% while the 2-yr yield jumped two basis points to 1.44%.

In Washington, Senator Bill Cassidy (R-LA) confirmed that the Senate will not vote on the Cassidy-Graham health care bill as the piece of legislation failed to gain enough support within the GOP. Lawmakers will table the health care reform effort for now and return their attention to tax reform.

Reviewing Tuesday's economic data, which included August New Home Sales, the Conference Board's Consumer Confidence Index for September, and the Case-Shiller 20-City Composite Home Price Index for July:

New Home Sales in August hit an annualized rate of 560,000, which is below the revised July rate of 580,000 (from 571,000), and lower than the Briefing.com consensus of 577,000.

The key takeaway from the report isn't that sales declined 4.7% in the South, which was partly impacted by Hurricane Harvey, but that sales declined 2.7% in the West, which wasn't impacted by Hurricane Harvey, after declining 15.3% in July. The weakness in the West could be a function of constraints related to high prices, yet it will need to be watched closely as a potential harbinger of a broader slowdown in the housing market related to affordability constraints.

The consumer confidence reading for September declined to 119.8 from the prior month's revised reading of 120.4 (from 122.9). The Briefing.com consensus expected the survey to hit 119.4.

The key takeaway from the report is that the downturn was driven mostly by changing attitudes among consumers in the hurricane-ravaged states of Texas and Florida, which manifested themselves in the Present Situation Index. Overall, consumers remained relatively upbeat about the short-term outlook.

The July Case-Shiller 20-city Index hit 5.8%, which is in line with the Briefing.com consensus. The prior month's reading was revised to 5.6% from 5.7%.

On Wednesday, investors will receive several economic reports, including the weekly MBA Mortgage Applications Index at 7:00 ET, August Durable Goods Orders (Briefing.com consensus +0.7%) at 8:30 ET, and August Pending Home Sales (Briefing.com consensus -0.4%) at 10:00 ET.

Nasdaq Composite +18.5% YTD

Dow Jones Industrial Average +12.8% YTD

S&P 500 +11.5% YTD

Russell 2000 +7.4% YTD

Dow: -11.77… | Nasdaq: +9.57… | S&P: +0.18…

NASDAQ Adv/Dec 1556/1114. …NYSE Adv/Dec 1637/1274.

03:30PM ET

[BRIEFING.COM] Commodities end the day lower:

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently down 0.64% at 84.7846

Dollar index is currently up 0.41% at 93.03.

Nov WTI crude is lower on the day.

API inventory data to be released at 4:30pm ET

Futures settled $0.34 down to $51.90/barrel.

In other energy, Nov natural gas settled up $0.01 at $3.00/MMBtu

On to metals:

Gold and silver moved slowly lower most of the day.

Dec gold settled down $9.80 at $1301.80/oz, while Sept silver dropped $0.25 to settle at $16.90/oz

Dec copper lost $0.02 to settle at $2.92/lb

Finally, agriculture futures settled lower:

Dec corn settled $0.02 at $3.52/bu.

Nov soy settled down $0.07 at $9.64/bu.

Dec wheat settled $0.01 lower at $4.53/bu.

Dow: +18.20… | Nasdaq: +21.97… | S&P: +4.22…

NASDAQ Adv/Dec 1648/1114. …NYSE Adv/Dec 1756/1134.

02:55PM ET

[BRIEFING.COM] The major averages are on track to register modest victories moving into the final stretch. Meanwhile, the small-cap Russell 2000 (+0.5%) outperforms and is on track to settle at a new all-time high for the third session in a row.

Four sectors are trading in the green this afternoon--technology (+0.5%), real estate (+0.2%), consumer staples (+0.1%), and industrials (+0.1%)--while seven groups are trading in the red--financials (unch), consumer discretionary (unch), energy (-0.1%), health care (-0.1%), utilities (-0.1%), materials (-0.2%), and telecom services (-0.8%).

Dow component Nike (NKE 53.32, +0.09) will report its quarterly earnings following today's closing bell, as will chipmaker Micron Technology (MU 34.84, -0.03). Both companies last reported on June 29 and have added 0.3% and 10.7%, respectively, since.

For comparison, the S&P 500 has climbed 3.3% since June 29.

Dow: +13.79… | Nasdaq: +17.73… | S&P: +2.74…

NASDAQ Adv/Dec 1655/1110. …NYSE Adv/Dec 1735/1158.

02:30PM ET

[BRIEFING.COM] The major U.S. indices hover near their recent levels with the S&P 500 sporting a gain of 0.1%.

In Washington, the Cassidy-Graham health care bill, which gained traction within the GOP last week, appears to be dead after Senator Susan Collins (R-ME) became the third GOP Senator to publicly oppose the bill. The Senate was planning to vote on the bill this week, but Senator Bill Cassidy (R-LA) recently confirmed the vote will not happen.

The influential health care sector is currently trading at its unchanged mark, even though biotechnology names underperform; the iShares Nasdaq Biotechnology ETF (IBB 328.83, -2.57) is down 0.8%. For the month, the health care sector holds a modest gain of 0.4%.

For comparison, the S&P 500 has slipped 0.1% in September.

Dow: +12.79… | Nasdaq: +22.19… | S&P: +3.06…

NASDAQ Adv/Dec 1701/1087. …NYSE Adv/Dec 1730/1153.

02:00PM ET

[BRIEFING.COM] The major averages are hovering near the top of their trading ranges with the Nasdaq (+0.4%) showing relative strength.

Fed Chair Janet Yellen addressed the National Association for Business Economics (NABE) earlier this afternoon, saying that the U.S. central bank needs to continue its gradual path of rate hikes despite the uncertainty surrounding inflation. However, Ms. Yellen noted that the Fed will watch the incoming data closely and adjust its views accordingly.

U.S. Treasuries had a largely muted response to Ms. Yellen's comments and continue to hover modestly below their unchanged marks. The yield on the benchmark 10-yr Treasury note is up one basis point at 2.23%.

Dow: +25.50… | Nasdaq: +27.21… | S&P: +4.69…

NASDAQ Adv/Dec 1710/1052. …NYSE Adv/Dec 1776/1092.

01:30PM ET

[BRIEFING.COM] The major U.S. indices continue to show modest gains as technology stocks bounce back from yesterday's sell off.

A look inside the Dow Jones Industrial Average shows that Apple (AAPL 153.24, +2.69) is the strongest performer, retracing a portion of its September decline. AAPL shares are up 1.9% in today's session, but hold a month-to-date loss of 6.7%.

Conversely, McDonald's (MCD 154.20, -2.06) is the worst-performing Dow component as restaurants display relative weakness in today's session.

At current levels, the DJIA is up 4.5% for the quarter, which effectively ends on Friday.

Dow: +8.52… | Nasdaq: +22.74… | S&P: +3.44…

NASDAQ Adv/Dec 1670/1093. …NYSE Adv/Dec 1682/1168.

01:05PM ET

[BRIEFING.COM] Equities are slightly higher this afternoon, but the day has been somewhat disappointing considering its optimistic start. The Dow and the Nasdaq trade roughly in line with the S&P 500, which is up 0.1%. Meanwhile, small caps are outperforming once again, putting the Russell 2000 (+0.4%) on track to close at a new all-time high for the third session in a row.

Technology stocks were in demand this morning as investors bought Monday's dip, sending the S&P 500's technology sector 0.8% above its flat line. However, the rally petered out less than an hour into the session, pulling the tech group, and the broader market, back toward its flat line. The tech sector is currently up 0.4%.

At their best marks of the day, the S&P 500 and the tech-heavy Nasdaq held gains of 0.3% and 0.5%, respectively.

Within the technology space, Apple (AAPL 152.33, +1.78) is still outperforming (+1.1%), bouncing back from a four-session slide. Likewise, semiconductor giant NVIDIA (NVDA 174.01, +3.04) has reversed its recent downward trend, jumping 1.8% in reaction to news that the company will provide GPU hardware to several Chinese tech giants.

Red Hat (RHT 110.15, +4.42) also shows notable strength after beating both top and bottom line estimates and issuing upbeat guidance. RHT shares are currently up 4.2% and trade at their highest level in nearly two decades.

Elsewhere on the earnings front, Darden Restaurants (DRI 78.21, -4.93), the owner of brands like Olive Garden and LongHorn Steakhouse, is down 6.0% despite reporting in-line earnings and revenues. Conversely, Carnival (CCL 65.51, +2.01) is up 3.2% after reporting better-than-expected top and bottom lines.

In other corporate news, Equifax (EFX 104.17, -0.92) announced that CEO Richard Smith will step down following the company's highly-publicized data breach, which compromised the personal information of approximately 143 million Americans. The company disclosed the breach on September 7.

Meanwhile, the financial sector (+0.1%), which is the second most influential sector behind technology, has bounced back from early weakness, helping keep the broader market afloat. However, JPMorgan Chase (JPM 93.82, -0.30) still lags (-0.3%) after Deutsche Bank downgraded the company's shares to 'Hold' from 'Buy' this morning.

U.S. Treasuries are trading lower across the board this afternoon amid a speech from Fed Chair Janet Yellen, who is addressing the NABE in Cleveland. The benchmark 10-yr yield is up two basis points at 2.24%, which places it about four basis points below last week's high and about 19 basis points above its September low.

Reviewing Tuesday's economic data, which included August New Home Sales, the Conference Board's Consumer Confidence Index for September, and the Case-Shiller 20-City Composite Home Price Index for July:

New Home Sales in August hit an annualized rate of 560,000, which is below the revised July rate of 580,000 (from 571,000), and lower than the Briefing.com consensus of 577,000.

The key takeaway from the report isn't that sales declined 4.7% in the South, which was partly impacted by Hurricane Harvey, but that sales declined 2.7% in the West, which wasn't impacted by Hurricane Harvey, after declining 15.3% in July. The weakness in the West could be a function of constraints related to high prices, yet it will need to be watched closely as a potential harbinger of a broader slowdown in the housing market related to affordability constraints.

The consumer confidence reading for September declined to 119.8 from the prior month's revised reading of 120.4 (from 122.9). The Briefing.com consensus expected the survey to hit 119.4.

The key takeaway from the report is that the downturn was driven mostly by changing attitudes among consumers in the hurricane-ravaged states of Texas and Florida, which manifested themselves in the Present Situation Index. Overall, consumers remained relatively upbeat about the short-term outlook.

The July Case-Shiller 20-city Index hit 5.8%, which is in line with the Briefing.com consensus. The prior month's reading was revised to 5.6% from 5.7%.

Dow: +7.83… | Nasdaq: +11.59… | S&P: +2.02…

NASDAQ Adv/Dec 1593/1187. …NYSE Adv/Dec 1649/1184.

12:25PM ET

[BRIEFING.COM] The major U.S. indices are trading in the green this afternoon, but gains have been limited. The S&P 500 is higher by just 0.1%.

Transports are outperforming today, evidenced by the Dow Jones Transportation Average (+0.5%), which has been bullish all month (+4.8%). Nearly all of the DJTA's 20 components are trading in positive territory this afternoon, with Matson (MATX 27.95, +0.97) and Avis Budget (CAR 38.42, +0.88) pacing the advance. The two names sport respective gains of 3.6% and 2.2%.

On the flip side, American Airlines (AAL 47.54, -0.17), Union Pacific (UNP 115.48, -0.30), and UPS (UPS 118.14, -0.10) underperform, showing losses between 0.1% and 0.3%.

The Dow Jones Transportation Average is a leading indicator, meaning it tends to do well when the outlook for the U.S. economy is seen as favorable.

Dow: +6.29… | Nasdaq: +9.97… | S&P: +1.79…

NASDAQ Adv/Dec 1630/1164. …NYSE Adv/Dec 1690/1138.

12:00PM ET

[BRIEFING.COM] The major averages have not changed since the last update.

Darden Restaurants (DRI 78.29, -4.85), the parent company of brands like Olive Garden and LongHorn Steakhouse, has dropped 5.8% in today's session after reporting earnings this morning. The company reported in-line earnings and revenues, but it just wasn't enough to justify its early-September rally, in which DRI shares climbed 9.5% over seven sessions.

The consumer discretionary sector (-0.1%), which houses restaurant names, hovers a step below the broader market. The sector's top component by market cap--Amazon (AMZN 936.89, -3.90)--is down 0.4%, extending its two-week decline to 6.3%.

Dow: +11.44… | Nasdaq: +4.23… | S&P: +1.66…

NASDAQ Adv/Dec 1580/1216. …NYSE Adv/Dec 1668/1143.

11:25AM ET

[BRIEFING.COM] Equity indices are trading near their session lows, hovering just a tick above their unchanged marks. The Dow (+0.1%) shows relative strength.

The heavily-weighted financial sector (-0.2%) is struggling to keep pace with the broader market this morning as baking names pare their September gains. JPMorgan Chase (JPM 93.48, -0.63) shows particular weakness, dropping 0.7%, after JPM shares were downgraded to 'Hold' from 'Buy' at Deutsche Bank earlier this morning.

In the bond market, U.S. Treasuries are lower across the board, sending yields into the green. The yield on the benchmark 10-yr Treasury note is currently up two basis points at 2.24%, which places it about four basis points below last week's high and about 19 basis points above its September low.

Dow: +12.49… | Nasdaq: +1.52… | S&P: +0.27…

NASDAQ Adv/Dec 1569/1217. …NYSE Adv/Dec 1630/1150.

11:00AM ET

[BRIEFING.COM] Equities have trimmed their gains a bit in recent action as technology stocks move back toward their unchanged marks. The S&P 500 is up just 0.1%.

Sector movement has been pretty modest in general; nine of the eleven groups are currently drifting within 0.2% of their flat lines. The only exceptions are the top-weighted technology sector, which holds a gain of 0.4%, and the lightly-weighted telecom services group, which holds a loss of 0.3%.

Within the tech group, Apple (AAPL 152.86, +2.29) shows particular strength (+1.5%), bouncing back from a four-session slide. However, Red Hat (RHT 109.43, +3.67) has done even better, climbing 3.5% after beating both top and bottom line estimates and issuing above-consensus guidance.

Meanwhile, semiconductor giant NVIDIA (NVDA 175.11, +4.14) is up 2.4% following news that the company will provide GPU hardware to several Chinese tech giants. The bullish bias has been limited within the broader semiconductor space, however, evidenced by the PHLX Semiconductor Index, which is higher by just 0.1%.

Dow: +23.35… | Nasdaq: +7.20… | S&P: +1.47…

NASDAQ Adv/Dec 1574/1167. …NYSE Adv/Dec 1616/1139.

10:30AM ET

[BRIEFING.COM] Commodities begin the day lower:

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently down 0.51% at 84.8911

The dollar index is up 0.48% at 93.10.

Oct WTI crude is down this morning

API inventory data will be released at 4:30pm ET.

Last week's data showed build of 1.443 mln barrels

Futures are $0.56 lower to $51.66/barrel.

In other energy,

Oct natural gas has experienced some volatility this morning and trades slightly higher.

Futures are up $0.013 at $3.001/MMBtu

Metals are moving lower across the board:

Dec gold has lost $7.80 and trades at $1303.70/oz, while Sept silver has dropped $0.217 to $16.93/oz

Sept copper is down $0.025 to $2.9125/lb

Finally, agriculture:

Dec corn is up $0.0075 at $3.545/bu.

Nov soy is down $0.0675 at $9.645/bu.

Dec wheat is up $0.0575 at $4.5975/bu.

Dow: +54.50… | Nasdaq: +26.04… | S&P: +5.57…

NASDAQ Adv/Dec 1593/1070. …NYSE Adv/Dec 1643/1075.

10:00AM ET

[BRIEFING.COM] The major averages continue to sport modest gains.

Just in, the consumer confidence reading for September declined to 119.8 from the prior month's revised reading of 120.4 (from 122.9). The Briefing.com consensus expected the survey to hit 119.4.

Separately, New Home Sales in August hit an annualized rate of 560,000, which is below the revised July rate of 580,000 (from 571,000), and lower than the Briefing.com consensus of 577,000.

Dow: +65.86… | Nasdaq: +22.26… | S&P: +5.77…

NASDAQ Adv/Dec 1432/1156. …NYSE Adv/Dec 1602/1014.

09:40AM ET

[BRIEFING.COM] The major U.S. indices opened Tuesday's session with modest gains. The Nasdaq (+0.4%) is the early leader and hovers a step ahead of the S&P 500 (+0.2%).

Around half of the S&P 500's 11 sectors are trading in the green this morning, led by the technology space (+0.7%), which is attempting to bounce back from a disappointing performance on Monday. Within the tech space, semiconductor giant NVIDIA (NVDA 177.30, +6.35) shows particular strength, adding 3.6%, following news that the company will provide GPU hardware to several Chinese tech giants.

On the flip side, the energy space (-0.4%) is the weakest sector, moving lower in tandem with the price of crude oil, which is down 1.0% at $51.69/bbl.

Today's last pieces of economic data--the Conference Board's Consumer Confidence Index for September (Briefing.com consensus 119.4) and August New Home Sales (Briefing.com consensus 577K)--will be released shortly at 10:00 ET.

Dow: +65.13… | Nasdaq: +28.48… | S&P: +5.64…

NASDAQ Adv/Dec 1561/960. …NYSE Adv/Dec 1590/954.

09:12AM ET

[BRIEFING.COM] S&P futures vs fair value: +4.60. Nasdaq futures vs fair value: +29.40.

The equity market is on track to reclaim a solid chunk of yesterday's decline at the opening bell as the S&P 500 futures currently trade five points, or 0.2%, above fair value. The tech-heavy Nasdaq 100 futures (+0.5%) show relative strength, which is an encouraging sign in light of yesterday's technology sell off.

Fed Chair Janet Yellen is scheduled to give a speech titled "Inflation, Uncertainty, and Monetary Policy" in Cleveland today at 12:45 ET. Market participants will be watching for any clues as to the timing of the next rate hike, which the fed funds futures market believes will occur before the year's end with an implied probability of 77.9%.

Several other Fed officials will also speak on Tuesday, including Cleveland Fed President Loretta Mester (non-FOMC voter) at 9:30 ET, Fed Governor Lael Brainard at 10:30 ET, and Atlanta Fed President Raphael Bostic (non-FOMC voter) at 12:30 ET.

In earnings news, Red Hat (RHT 110.01, +4.25) is up 4.0% in pre-market action after beating both top and bottom line estimates and issuing above-consensus guidance. Conversely, Darden Restaurants (DRI 80.60, -2.54) has tumbled 3.1% despite reporting in-line earnings and revenues.

On the data front, the July Case-Shiller 20-city Index hit 5.8%, which is in line with the Briefing.com consensus. The prior month's reading was revised to 5.6% from 5.7%.

Investors will receive two additional pieces of economic data today--the Conference Board's Consumer Confidence Index for September (Briefing.com consensus 119.4) and August New Home Sales (Briefing.com consensus 577K)--both of which will be released at 10:00 ET.

U.S. Treasuries are trading slightly lower this morning, sending yields higher across the curve; the benchmark 10-yr yield is up one basis point at 2.23%. Meanwhile, the U.S. Dollar Index is up 0.4% at 92.82 amid broad strength.

Also of note, WTI crude futures are trading lower this morning, down 0.7% at $51.86/bbl, after jumping around 3.0% on Monday. Despite this morning's slip, the commodity is hovering near its best mark in over five months and trades more than 20.0% above its June lows, meeting the definition of a bull market.

08:50AM ET

[BRIEFING.COM] S&P futures vs fair value: +3.80. Nasdaq futures vs fair value: +25.90.

The S&P 500 futures trade four points, or 0.2%, above fair value.

Equity indices in the Asia-Pacific region ended Tuesday on a mixed note. The focus was on North Korea once again, after the country's foreign minister said that U.S. President Trump's remarks at the United Nations amounted to a declaration of war. South Korea's Financial Services Commission announced reforms for retail customers of banks. South China Morning Post reported that top Chinese officials and economists support a move to a free-floating yuan. In Japan, the Bank of Japan's latest minutes showed agreement among policymakers that reaching the 2.0% inflation target is vital.

In economic data:

Japan's Corporate Services Price Index +0.8% year-over-year (expected 0.7%; last 0.6%)

New Zealand's August trade deficit narrowed to NZD3.20 billion from NZD3.21 billion (expected deficit of NZD2.91 billion). August Imports NZD4.92 billion (expected NZD4.80 billion; last NZD4.53 billion) and August Exports NZD3.69 billion (expected NZD4.05 billion; last NZD4.63 billion). September ANZ Business Confidence 0.0 (last 18.3)

South Korea's September Consumer Confidence 108 (last 110)

Singapore's August Industrial Production +0.6% month-over-month (expected -0.4%; last 0.9%); +19.1% year-over-year (consensus 14.2%; last 21.2%)

---Equity Markets---

Japan's Nikkei shed 0.3%. Taiyo Yuden, SUMCO, Furukawa Electric, Tokyo Electron, Sony, Konami, Dainippon Screen Manufacturing, Daikin Industries, Fanuc, and Hitachi Construction lost between 1.2% and 5.4%. On the upside, Dentsu, Yamaha, Meiji Holdings, Haseko, and Suzuki Motor gained between 0.7% and 1.7%.

Hong Kong's Hang Seng added 0.1%. Energy-related names like Kunlun Energy, China Shenhua Energy, CNOOC, and PetroChina gained between 2.1% and 3.7%. On the downside, Apple supplier AAC Technologies lost 1.1% while property names like China Overseas, Swire Pacific, New World Development, and Sino Land lost between 0.4% and 1.0%.

China's Shanghai Composite rose 0.1%. Hangzhou Tian-Mu-Shan Pharmaceutical, Guangdong Boxin Investing, Zhejiang Xinan Chemical, and Shanghai Lingang Holdings climbed between 4.2% and 6.6%.

India's Sensex slipped 0.1% amid losses in more than half of its components. Hindustan Unilever, Dr. Reddy's Labs, Tata Consultancy, Mahindra & Mahindra, and Wipro lost between 0.5% and 2.3%.

Major European indices hover near their flat lines with Spain's IBEX (-0.2%) trading a bit behind its peers. There are five days left ahead of the planned independence referendum in Catalonia and neither side has backed down. In Germany, AfD chair, Frauke Petry, will not be joining AfD in parliament. Italy's Finance Minister Pier Carlo Padoan made upbeat comments about the Italian economy.

In economic data:

Germany's August Import Price Index 0.0% month-over-month (expected 0.1%; last -0.4%); +2.1% year-over-year, as expected (last 1.9%)

UK's BBA Mortgage Approvals 41,800 (expected 41,700; last 41,600)

France's September Business Survey 110 (last 111)

Italy's August non-EU trade surplus EUR2.53 billion (last EUR4.53 billion)

---Equity Markets---

Germany's DAX is up 0.1%. Henkel, Adidas, Infineon, and SAP are down between 0.3% and 1.3% while Deutsche Bank, Continental, Commerzbank, Daimler, Merck, and Volkswagen show gains between 0.3% and 1.2%.

UK's FTSE trades flat as consumer stocks display relative weakness while energy names outperform. Next, Carnival, Associated British Foods, Kingfisher, and Burberry are down between 0.5% and 1.5% while BP and Royal Dutch Shell hold respective gains of 0.6% and 0.9%.

France's CAC is lower by 0.1%. L'Oreal is the weakest performer, falling 0.9%, while Societe Generale, AXA, Accor, Total, Danone, and BNP Paribas show losses between 0.1% and 0.4%.

Spain's IBEX is down 0.2%. Mediaset has slid 1.8% while BBVA, Banco Sabadell, Santander, and Bankia are down between 0.2% and 0.3%.

08:31AM ET

[BRIEFING.COM] S&P futures vs fair value: +1.50. Nasdaq futures vs fair value: +16.10.

The S&P 500 futures trade two points, or 0.1%, above fair value.

WTI crude futures are trading lower this morning, down 0.6% at $51.91/bbl, after jumping around 3.0% on Monday. Despite this morning's slip, the commodity is hovering near its best mark in over five months and trades more than 20.0% above its June lows, meeting the definition of a bull market. Likewise, energy stocks--which typically move in tandem with the price of crude oil--have been quiet bullish as of late, sending the S&P 500's energy sector higher by 9.3% this month.

The American Petroleum Institute (API) will deliver its weekly crude inventory report this evening at 16:30 ET, but the more influential weekly report from the Department of Energy will cross the wires on Wednesday morning at 10:30 ET.

07:56AM ET

[BRIEFING.COM] S&P futures vs fair value: +1.80. Nasdaq futures vs fair value: +14.50.

The stock market started the week on the back foot as technology stocks tumbled, giving back some of their impressive quarter-to-date returns. However, it appears that investor sentiment has shifted a bit this morning as the S&P 500 futures trade two points, or 0.1%, above fair value. The tech-heavy Nasdaq 100 futures show relative strength, hovering 13 points (0.2%), above fair value.

Fed Chair Janet Yellen is scheduled to give a speech titled "Inflation, Uncertainty, and Monetary Policy" in Cleveland today at 12:45 ET. Market participants will be watching for any clues as to the timing of the next rate hike, which the fed funds futures market believes will occur before the year's end with an implied probability of 72.8%.

In addition, several other Fed officials will speak on Tuesday, including Cleveland Fed President Loretta Mester (non-FOMC voter) at 9:30 ET, Fed Governor Lael Brainard at 10:30 ET, and Atlanta Fed President Raphael Bostic (non-FOMC voter) at 12:30 ET.

U.S. Treasuries are trading flat this morning, keeping the benchmark 10-yr yield at its unchanged mark (2.22%). Meanwhile, the U.S. Dollar Index is up 0.4% at 92.82 amid broad strength.

On the data front, investors will receive several economic reports today, including the Case-Shiller 20-City Composite Home Price Index for July (Briefing.com consensus +5.8%) at 9:00 ET, the Conference Board's Consumer Confidence Index for September (Briefing.com consensus 119.4) at 10:00 ET, and August New Home Sales (Briefing.com consensus 577K) also at 10:00 ET.

In U.S. corporate news:

Red Hat (RHT 110.20, +4.44): +4.2% after beating both top and bottom line estimates and raising its guidance.

JPMorgan Chase (JPM 93.60, -0.52): -0.6% after JPM shares were downgraded to 'Hold' from 'Buy' at Deutsche Bank.

Darden Restaurants (DRI 79.25, -3.89): -4.7% despite reporting in-line earnings and revenues.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region ended Tuesday on a mixed note. Japan's Nikkei -0.3%, Hong Kong's Hang Seng +0.1%, China's Shanghai Composite +0.1%, India's Sensex -0.1%.

In economic data:

Japan's Corporate Services Price Index +0.8% year-over-year (expected 0.7%; last 0.6%)

New Zealand's August trade deficit narrowed to NZD3.20 billion from NZD3.21 billion (expected deficit of NZD2.91 billion). August Imports NZD4.92 billion (expected NZD4.80 billion; last NZD4.53 billion) and August Exports NZD3.69 billion (expected NZD4.05 billion; last NZD4.63 billion). September ANZ Business Confidence 0.0 (last 18.3)

South Korea's September Consumer Confidence 108 (last 110)

Singapore's August Industrial Production +0.6% month-over-month (expected -0.4%; last 0.9%); +19.1% year-over-year (consensus 14.2%; last 21.2%)

In news:

The focus was on North Korea once again, after the country's foreign minister said that U.S. President Trump's remarks at the United Nations amounted to a declaration of war.

South Korea's Financial Services Commission announced reforms for retail customers of banks.

South China Morning Post reported that top Chinese officials and economists support a move to a free-floating yuan.

The Bank of Japan's latest minutes showed agreement among policymakers that reaching the 2.0% inflation target is vital.

Major European indices hover near their flat lines with Spain's IBEX trading a bit behind its peers. Germany's DAX unch, UK's FTSE unch, France's CAC -0.1%, Spain's IBEX -0.3%.

In economic data:

Germany's August Import Price Index 0.0% month-over-month (expected 0.1%; last -0.4%); +2.1% year-over-year, as expected (last 1.9%)

UK's BBA Mortgage Approvals 41,800 (expected 41,700; last 41,600)

France's September Business Survey 110 (last 111)

Italy's August non-EU trade surplus EUR2.53 billion (last EUR4.53 billion)

In news:

There are five days left ahead of the planned independence referendum in Catalonia and neither side has backed down.

In Germany, AfD chair, Frauke Petry, will not be joining AfD in parliament.

Italy's Finance Minister Pier Carlo Padoan made upbeat comments about the Italian economy.

06:40AM ET

[BRIEFING.COM] S&P futures vs fair value: +2.50. Nasdaq futures vs fair value: +13.00.

06:40AM ET

[BRIEFING.COM] Nikkei...20330.19...-67.40...-0.30%

Hang Seng...27530.53...+30.20...+0.10%

06:40AM ET

[BRIEFING.COM] FTSE...7302.60...+1.30...0.00

DAX...12622.94...+28.10...+0.20%

Price Action Trading

@ http://www.thestrategylab.com/price-action-trading.htm Trade Strategies via Volatility Analysis

@ http://www.thestrategylab.com/VolatilityTrading.htm Review of TheStrategyLab

@ http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=84&t=3167 TheStrategyLab Review

@ http://www.thestrategylab.com/thestrategylab-reviews.htmSpecial thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

Online user name

wrbtrader (more info about me):

http://www.thestrategylab.com/wrbtrader.htmTheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com