Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htm TheStrategyLab Reviews: http://www.thestrategylab.com/thestrategylab-reviews.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

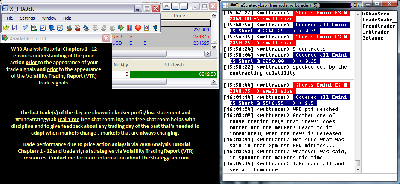

Attachment:

040517-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6812.50.png [ 93.76 KiB | Viewed 428 times ]

040517-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6812.50.png [ 93.76 KiB | Viewed 428 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$6,812.50 dollars or +136.25 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6,812.50 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room for anyone to do a real-time review. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=166&t=2521  ##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. TheStrategyLab free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I

keep the peace between members via removing trouble makers so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell. TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Quote:

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=317&t=3373 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

Attachment:

040517-Key-Price-Action-Markets.png [ 1 MiB | Viewed 313 times ]

040517-Key-Price-Action-Markets.png [ 1 MiB | Viewed 313 times ]

click on the above image to view today's price action of key markets 4:25 pm: [BRIEFING.COM] Stocks started strong out of the gate following an upbeat ADP Employment Change Report on Wednesday morning, but the hawkish tone of the FOMC Minutes prompted an afternoon retreat. The S&P 500 settled lower by 0.3% while the Dow (-0.2%) performed slightly better and the Nasdaq (-0.6%) finished slightly worse.

The ADP National Employment Report, which showed an increase of 263,000 in March (Briefing.com consensus 175,000), provided an encouraging signal for the domestic labor market and future economic growth. However, the domestically-oriented Russell 2000 (-1.0%), which is closely tied to the performance of the U.S. economy, struggled to keep pace with the broader market. The lack of buying conviction among small caps pointed to the fact that not all market participants bought into the positive narrative attached to the better than expected ADP reading.

That narrative was tested during the afternoon session with the release of the FOMC Minutes from the March meeting. In the report, the committee revealed that it would like to start reducing the Fed's balance sheet later in the year. In addition, the Minutes showed that some Fed officials are worried about high equity valuations. Stocks held steady immediately following the report, but the hawkish tone eventually seeped in, sending the cash market into the red.

It's also important to note that investors have been on edge all week amid a cloud of uncertainty; it's unclear what will come from President Trump's upcoming meeting with Chinese President Xi Jinping, what the resurgence of health care reform will mean for tax reform, and how the U.S. will deal with the ongoing tensions in Syria and North Korea, among a host of other concerns. With all of these narratives playing in the background, it would be unfair to attribute today's slip to any one factor.

On that note, House Speaker Paul Ryan added to the market's anxiety on Wednesday afternoon, acknowledging that tax reform will take longer than repealing and replacing the Affordable Care Act. Mr. Ryan said that the House currently has a tax reform plan, but the Senate is still working on its version.

Most sectors finished today's session in negative territory with only a couple countercyclical groups--utilities (+0.5%) and real estate (+0.2%)--escaping with wins. The financial sector (-0.7%) settled at the bottom of the day's leaderboard with the remaining sectors closing modest lower with losses no greater than 0.4%.

It's worth pointing out that crude oil settled 0.3% higher at $51.14/bbl despite a bearish inventory report from the Energy Information Administration. The EIA reading showed a build of 1.6 million barrels while the consensus called for a modest draw. Nonetheless, the energy sector (-0.3%) performed in line with its cyclical peers throughout the majority of today's action.

In the Treasury market, Treasuries experienced increased demand in the wake of the FOMC Minutes. The benchmark 10-yr yield finished four basis points lower at 2.33%.

On the data front, investors received March ADP Employment Change, March ISM Services, and the weekly MBA Mortgage Applications Index:

The ADP National Employment Report showed an increase of 263,000 in March (Briefing.com consensus 175,000) while the February reading was revised lower to 245,000 from 298,000.

The ADP reading precedes Friday's more influential Employment Situation Report for March, which the Briefing.com consensus expects will show the addition of 180,000 nonfarm payrolls. The Employment Situation Report for February indicated that nonfarm payrolls increased by 235,000.

The ISM Services Index for March declined to 55.2 from an unrevised reading of 57.6 in February while the Briefing.com consensus expected a downtick to 57.0.

The key takeaway from the report is that growth in the services sector, which accounts for a much bigger slice of economic activity than the manufacturing sector does, persisted for the 87th straight month.

The weekly MBA Mortgage Applications Index decreased 1.6% to follow last week's 0.8% decline.

Tomorrow, March Challenger Job Cuts will be released at 7:30 ET while Initial Claims (Briefing.com consensus 245,000) will cross the wires at 8:30 ET.

Nasdaq Composite +8.9% YTD

S&P 500 +5.1% YTD

Dow Jones Industrial Average +4.5% YTD

Russell 2000 -0.4% YTD

3:40 pm: [BRIEFING.COM]

May crude oil closed today's floor trading session+0.3% at $51.14/barrel following the recent API/EIA storage data

In other energy, May natural gas futures slipped -1.2% to end at $3.26/MMBtu

Precious metals lost some steam, while base metals such as copper fared better

June gold ended -0.8% at $1248.60/oz, while May silver lost -0.8% at $18.18/oz

May copper finished +0.7% at $2.68/lb

3:00 pm:

[BRIEFING.COM] The hawkish tone of the Fed Minutes has finally seeped into the stock market, and it has pulled the major averages off their best marks of the day. The S&P 500 is now up just 0.3%.

Sector standings remain largely the same going into the final stretch, but gains have been cut across the board. Cyclical groups still lead with the energy (+0.5%) and materials (+0.5%) spaces demonstrating relative strength. Meanwhile, countercyclical sectors like health care (+0.1%) and utilities (-0.1%) underperform.

On the earnings front, investors will receive a batch of notable reports between today's close and tomorrow's open. Bed Bath & Beyond (BBBY 38.64, -0.34) will deliver its quarterly results this evening while CarMax (KMX 57.38, +1.55), Constellation Brands (STZ 162.00, +0.49), Fred's (FRED 12.83, +0.09) will follow suit on Thursday morning.

2:30 pm:

[BRIEFING.COM] The Fed Minutes from the March 14-15 meeting were released at the top of the hour, but the effect on equities has been relatively modest. The S&P 500 holds a gain of 0.6%.

In the report, the committee revealed that it would like to start gradually, and predictably, reducing the Fed's balance sheet later this year. The Minutes also showed that some Fed officials viewed stock prices as 'quite high' by standard valuation measures.

U.S. Treasuries ticked down slightly following the release while the U.S. dollar maintained its prior level. The benchmark 10-yr yield trades one basis point higher at 2.37% while the U.S. Dollar Index (100.66, +0.23) holds a gain of 0.2%.

2:00 pm:

[BRIEFING.COM] The Dow Jones Transportation Average (+1.0%) outperforms the benchmark S&P 500 (+0.7%) as all of the price-weighted average's components trade in the green.

After slipping in yesterday's session, airlines have rebounded today with names like Delta Air Lines (DAL 45.83, +0.72), Southwest Airlines (LUV 54.04, +0.97), and United Continental (UAL 70.99, +1.23) showing gains between 1.6% and 1.9%. However, the DJTA's best-performing component is the shipping company Matson (MATX 31.69, +0.61).

Despite today's upbeat performance, the Dow Jones Transportation Average has largely underperformed the broader market in 2017. The DJTA holds a year-to-date gain of 1.7%, which is only about a quarter of the S&P 500's 2017 advance of 6.2%.

1:30 pm:

[BRIEFING.COM] The major U.S. indices continue to show strong gains at this time following this morning's ADP report.

A look inside the Dow Jones Industrial Average shows that DuPont (DD 81.43, +1.63), Caterpillar (CAT 95.77, +1.64), & McDonald's (MCD 131.33, +2.04) are outperforming amid broad market strength.

Conversely, Cisco (CSCO 33.35, -0.06) is the worst-performing, and lone Dow component in negative territory amid developments arising from the company's ongoing intellectual property battle with Arista Networks (134.00, +0.80).

With today's rally, the DJIA is now up 0.94% to kick off the second quarter.

At the bottom of the hour, the minutes from the FOMC's March meeting will be released.

1:00 pm:

[BRIEFING.COM] An upbeat ADP Employment Change Report was all it took for investors to overcome yesterday's cautious sentiment and push the major averages solidly higher in the first half of Wednesday's session. At midday, the Dow (+0.8%) holds a slight edge on the S&P 500 (+0.7%) and the Nasdaq (+0.6%). However, the domestically-oriented Russell 2000 (+0.3%) is having trouble keeping pace with the broader market, which is somewhat unexpected given today's reported catalyst.

The ADP National Employment Report, which showed an increase of 263,000 in March (Briefing.com consensus 175,000), provided an encouraging signal for the domestic labor market and future economic growth. The upbeat reading should be a supportive consideration for small-cap stocks since small-cap companies are tied most closely to the performance of the U.S. economy, but that hasn't been realized in the Russell 2000 so far today.

Equally noticeable is the performance of the Treasury market, which, surprisingly, has been a picture of relative strength in the wake of the ADP report. Yields are little changed across the curve, which certainly isn't the standing one would expect following a strong jobs report that validates the Fed's policy tightening inclination.

The counter-intuitive manner in which the Russell 2000 and the Treasury market have traded suggest there are reservations still among market participants that the U.S. economy will live up to the heightened growth expectations.

As for sector standings, the cyclical groups hold an edge over their countercyclical peers this afternoon. The financials, consumer discretionary, industrials, materials, technology, and energy sectors trade roughly in line with one another, holding gains between 0.7% and 0.9%. The energy sector's outperformance is particularly notable, given the EIA's bearish crude oil inventory report.

Crude oil squandered most of its solid overnight gain after the EIA reported a build of 1.6 million barrels while the consensus called for a modest draw. WTI crude currently trades just a step above its flat line at $51.17/bbl.

On the countercyclical side, the consumer staples (+0.3%), utilities (+0.1%), and telecom services (+0.2%) sectors struggle to stay in positive territory while the health care group (+0.6%) performs in line with the benchmark index.

On the data front, investors received March ADP Employment Change, March ISM Services, and the weekly MBA Mortgage Applications Index:

The ADP National Employment Report showed an increase of 263,000 in March (Briefing.com consensus 175,000) while the February reading was revised lower to 245,000 from 298,000.

The ADP reading precedes Friday's more influential Employment Situation Report for March, which the Briefing.com consensus expects will show the addition of 180,000 nonfarm payrolls. The Employment Situation Report for February indicated that nonfarm payrolls increased by 235,000.

The ISM Services Index for March declined to 55.2 from an unrevised reading of 57.6 in February while the Briefing.com consensus expected a downtick to 57.0.

The key takeaway from the report is that growth in the services sector, which accounts for a much bigger slice of economic activity than the manufacturing sector does, persisted for the 87th straight month.

The weekly MBA Mortgage Applications Index decreased 1.6% to follow last week's 0.8% decline.

In addition, the FOMC Minutes from the March 14-15 meeting will be released this afternoon at 14:00 ET.

12:30 pm:

[BRIEFING.COM] All three major averages hold solid gains this afternoon with the Dow (+0.7%) leading the advance.

The lightly-weighted materials sector (+1.0%) trades near the top of today's sector standings as large-cap chemical names like DuPont (DD 81.08, +1.28) and Dow Chemical (DOW 64.08, +0.88) show relative strength. Monsanto (MON 116.00, +1.80) laid the groundwork for the sector's positive performance early this morning by beating both top and bottom line estimates in its latest earnings report.

At the opposite end of the leaderboard, the telecom services (+0.2%) space struggles to stay above water as AT&T (T 41.63, -0.05) underperforms. The wireless giant shows a modest loss of 0.1% after announcing that subscribers of its unlimited mobile data plan will also receive free HBO access, a move that points to increased competition within the wireless space.

12:05 pm:

[BRIEFING.COM] The S&P 500 still trades comfortably in the green with a gain of 0.6%.

Like the major U.S. averages, the small-cap Russell 2000 (-0.1%) jumped to solid a gain out of the gate this morning following a better than expected ADP National Employment report. However, unlike the major averages, the small-cap index has since relinquished all of said gain. For the year, the Russell 2000 shows a year-to-date gain of 1.0%, which is far below the benchmark S&P 500's gain of 6.0%.

In the Treasury market, U.S. sovereign debt trades modestly higher with the benchmark 10-yr yield down one basis point at 2.36%.

11:25 am:

[BRIEFING.COM] The major averages have been moving lower as of late, in tandem with the financials (+0.3%) and energy (+0.3%) sectors. The two groups hover at their worst levels of the day while the S&P 500 trades higher by 0.5%.

Panera Bread (PNRA 311.84, +37.84) has spiked 13.8% in today's session after the company agreed to be acquired by JAB Holding Co. for $315.00 per share in cash, which is 15.0% above Tuesday's closing stock price. Over the years, JAB has purchased the likes of Caribou Coffee, Keurig, Krispy Kreme and Einstein Bagels, inviting speculation that peer Dunkin Brands (DNKN 52.51, -1.25) could be on the short list of future targets. As such, Dunkin trades lower by 2.3% as the PNRA buyout may be viewed as a knock against DNKN's attractiveness to private equity.

Meanwhile, restaurants like McDonald's (MCD 131.41, +2.13), Starbucks (SBUX 58.69, +0.37), and Yum! Brands (YUM 64.56, +0.72) outperform, helping the consumer discretionary sector (+0.7%) stay ahead of the broader market.

10:55 am:

[BRIEFING.COM] Equity indices hold solid gains this morning with the S&P 500 trading higher by 0.6%.

Crude oil has come off its session high in recent action after the EIA's weekly inventory report showed a build of 1.6 million barrels while the consensus called for a modest draw. The energy component still trades higher, up 0.5% at $51.30/bbl, but its current gain is only a third of its earlier advance. All things considered, the energy sector (+0.9%) has held up well. The group still trades near the top of the day's leaderboard.

All sectors trade in the green, but the cyclical groups have outperformed their countercyclical peers thus far. The financials, consumer discretionary, industrials, materials, and technology sectors hold gains between 0.6% and 0.9% while the consumer staples (+0.4%), utilities (+0.4%), and telecom services (+0.1%) sectors struggle to keep pace with the broader market.

10:45 am: [BRIEFING.COM]

Commodities are beginning the day higher, despite modest strength in the dollar index

Overall, commodities, as measured by the Bloomberg Commodity Index, are currently +0.5% at 85.7488

Dollar index is currently +0.1% at 100.59

Looking at energy...

May WTI crude oil futures are now +0.7% at $51.40/barrel

In other energy, May natural gas is +0.6% at $3.31/MMBtu

Moving on to metals...

June gold is currently -0.6% at $1251.00/oz, while May silver is -0.4% at $18.25/oz

May copper is now +2.7% at $2.68/lb

10:00 am:

[BRIEFING.COM] The major averages trade comfortably higher with the Dow sporting a gain of 0.7%.

Just in, the ISM Services Index for March declined to 55.2 from an unrevised reading of 57.6 in February while the Briefing.com consensus expected a downtick to 57.0.

9:40 am:

[BRIEFING.COM] The S&P 500 opens Wednesday's session with a gain of 0.3%.

Most sectors trade in positive territory with cyclical spaces showing relative strength. The energy group (+1.0%) has paced the advance, moving higher in tandem with crude oil, which currently trades 1.3% higher at $51.70/bbl. The heavily-weighted financial sector (+0.7%) also outperforms.

On the countercyclical side, the consumer staples (-0.2%), utilities (-0.3%), and telecom services (-0.1%) sectors hold modest losses. The health care group also underperforms, clinging to a slim gain of 0.1%.

9:18 am: [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +3.90.

Wall Street is set for a modestly higher open this morning after the ADP National Employment Report came in better than expected (263,000 vs Briefing.com consensus 175,000). The S&P 500 futures hovered near their flat lines preceding the report, but they now trade six points above fair value.

The ADP reading is often seen as a preview of Friday's more influential Employment Situation Report from the Bureau of Labor Statistics. The Briefing.com consensus expects Friday's report to show an addition of 180,000 nonfarm payrolls.

The positive economic data pushed equity futures into the green, but it's important to note that the gains are relatively modest as uncertainty still looms in the cash market. Some of the most notable factors contributing to the uneasiness include the upcoming meeting between President Trump and Chinese President Xi Jinping, heightened tensions with North Korea, and the resurgence of health care reform (and what it will mean for tax reform).

With these narratives playing in the background, it will be challenging for either the bulls or the bears to exert their influence on equities.

On the corporate front, Apple (AAPL 143.80, -0.97) has dropped 0.7% after reports that the company may delay its new iPhone release by a couple of months. Walgreens Boot Alliance (WBA 82.08, -0.42) also trades lower, down 0.5%, after the company reported worse than expected revenues. Conversely, Monsanto (MON 116.00, +1.79) has jumped 1.6% in pre-market trade after beating top and bottom line estimates.

Crude oil trades solidly higher in early action, up 1.3% at $51.67/bbl, after the American Petroleum Institute (API) reported a draw of 1.8 million barrels in U.S. crude stockpiles. Investors will be looking for the Energy Information Administration (EIA) to confirm that bullish figure when it releases its weekly inventory report later this morning at 10:30 ET.

In the Treasury market, U.S. sovereign debt trades flat with the benchmark 10-yr yield (2.36%) hovering at its unchanged mark.

Wednesday's last economic report, March ISM Services (Briefing.com consensus 57.0), will cross the wires at 10:00 ET. Meanwhile, the latest FOMC Minutes are due this afternoon at 14:00 ET.

8:51 am: [BRIEFING.COM] S&P futures vs fair value: +5.30. Nasdaq futures vs fair value: +0.50.

The S&P 500 futures trade five points above fair value.

Equity indices in the Asia-Pacific region ended Wednesday on a higher note. China's Shanghai Composite (+1.5%) outperformed with participants playing catch-up after a two-day holiday. The rally in China took shape even though the People's Bank of China refrained from injecting liquidity for the eighth consecutive session. Investors received a reminder of elevated geopolitical tensions, as North Korea conducted another missile test ahead of a weekend meeting between U.S. President Donald Trump and China's President Xi Jinping.

In economic data:

South Korea's February Current Account surplus narrowed to KRW8.40 billion from KRW10.51 billion

Australia's March AIG Services Index 51.7 (last 49.0)

New Zealand's ANZ Commodity Price Index +0.4% month-over-month (last 2.0%)

---Equity Markets---

Japan's Nikkei added 0.3%. Toshiba jumped 4.1% amid speculation the company may have found a buyer for its Westinghouse unit. Furukawa Electric, Fanuc, Familymart, Rakuten, Mitsubishi, Konami, Trend Micro, and West Japan Railway advanced between 0.9% and 3.7%.

Hong Kong's Hang Seng rose 0.6%. Want Want China spiked 8.8% while property names like Hang Lung Properties, SHK Properties, Cheung Kong Property Holdings, and China Resources Land advanced between 0.6% and 3.8%. On the downside, financials like Bank of China, Bank of East Asia, BOC Hong Kong, and HSBC lost between 0.2% and 1.3%.

China's Shanghai Composite rallied 1.5% to close at its best level since late 2016. Shanghai Lingyun Industries, Langfang Development, Beijing Airport High-Tech Park, Beijing Vantone Real Estate, and Lucky Film all jumped the limit, 10.0%.

India's Sensex added 0.2%, closing just below its all-time intraday high from early 2015. Adani Ports and Maruti Suzuki both spiked near 4.5% while Reliance Industries, Larsen & Toubro, Hindustan Unilever, Tata Steel, and Tata Motors added between 0.7% and 3.2%.

Major European indices trade mixed with Spain's IBEX (+0.8%) showing relative strength. Eurogroup chief Jeroen Dijsselbloem said that good progress has been made in talks with Greece, but the two sides remain apart on negotiations to unlock the next tranche of bailout funds. Greek Prime Minister Alexis Tsipras said that an emergency summit of EU leaders should take place if the sides are unable to reach an agreement at Friday's Eurogroup meeting in Malta.

In economic data:

Eurozone March Services PMI 56.0 (expected 56.5; last 56.5)

UK's March Services PMI 55.0 (consensus 53.5; last 53.3)

Germany's March Services PMI 55.6, as expected (last 55.6)

France's March Services PMI 57.5 (consensus 58.5; last 58.5)

Italy's March Services PMI 52.9 (expected 54.2; previous 54.1)

Spain's March Services PMI 57.4 (consensus 57.1; prior 57.0)

---Equity Markets---

Germany's DAX is down 0.2% with automakers Daimler, Volkswagen, and BMW leading the retreat. The three names show losses between 0.5% and 0.8%. Lufthansa, Adidas, Siemens, and BASF also trade lower, showing losses between 0.2% and 0.4%. On the upside, Commerzbank has climbed 2.6%.

France's CAC trades higher by 0.2%. Growth-sensitive names like TechnipFMC, Total, ArcelorMittal, and Solvay have added between 0.4% and 2.7% while financials Societe Generale, BNP Paribas, and Credit Agricole show gains between 0.5% and 1.5%. On the downside, Nokia, Renault, and Kering are down between 0.6% and 1.0%.

UK's FTSE shows a gain of 0.3%. Miners BHP Billiton, Antofagasta, Anglo American, and Rio Tinto are up between 1.7% and 2.6%. Select financials lag with Old Mutual and Standard Life showing losses of 3.9% and 0.3%, respectively.

Spain's IBEX trades up 0.8% amid broad strength. BBVA, Caixabank, Santander, Bankinter, Bankia, and Banco Sabadell outperform with gains between 0.6% and 1.7%.

8:27 am: [BRIEFING.COM] S&P futures vs fair value: +5.50. Nasdaq futures vs fair value: +5.40.

The S&P 500 futures trade six points above fair value.

Released not long ago, the ADP National Employment Report showed an increase of 263,000 in March (Briefing.com consensus 175,000) while the February reading was revised lower to 245,000 from 298,000.

The ADP reading precedes Friday's more influential Employment Situation Report for March, which the Briefing.com consensus expects will show the addition of 180,000 nonfarm payrolls. The Employment Situation Report for February indicated that nonfarm payrolls increased by 235,000.

7:59 am: [BRIEFING.COM] S&P futures vs fair value: +0.80. Nasdaq futures vs fair value: +0.40.

The stock market is poised for a muted open on Wednesday as the uncertainty that fueled yesterday's flat finish continues to loom. The S&P 500 futures trade one point above fair value.

Many factors have led to investors' indecisiveness, but some of the most prominent elements are the upcoming meeting between President Trump and Chinese President Xi Jinping, heightened tensions with North Korea, and the resurgence of health care reform (and what it will mean for tax reform). With these narratives playing in the background, it will be challenging for either the bulls or the bears to get a handle on the cash market.

Crude oil trades solidly higher in early action, up 1.0% at $51.58/bbl, after the American Petroleum Institute (API) reported a draw of 1.8 million barrels in U.S. crude stockpiles. Investors will be looking for the Energy Information Administration (EIA) to confirm that bullish figure when it releases its weekly inventory report later this morning at 10:30 ET.

Action has been subdued in the Treasury and currency markets this morning. The benchmark 10-yr yield (2.36%) trades flat while the U.S. Dollar Index (100.33, -0.09) shows a modest loss of 0.1%

On the data front, investors will receive March ADP Employment Change (Briefing.com consensus 175,000) at 8:15 ET, March ISM Services (Briefing.com consensus 57.0) at 10:00 ET, and the FOMC Minutes from the March 14-15 meeting at 14:00 ET.

Also of note, the weekly MBA Mortgage Applications Index, which was released earlier this morning, decreased 1.6% to follow last week's 0.8% decline.

In U.S. corporate news:

Walgreens Boot Alliance (WBA 81.63, -0.87): -1.1% after the company missed top line estimates and announced a $1 billion buyback.

Staples (SPLS 9.75, +0.24): +2.5% after the company's stock was upgraded to 'Buy' from 'Neutral' at Citigroup.

Reviewing overnight developments:

Equity indices in the Asia-Pacific region ended Wednesday on a higher note. Japan's Nikkei +0.3%, Hong Kong's Hang Seng +0.6%, China's Shanghai Composite +1.5%, India's Sensex +0.2%.

In economic data:

South Korea's February Current Account surplus narrowed to KRW8.40 billion from KRW10.51 billion

Australia's March AIG Services Index 51.7 (last 49.0)

New Zealand's ANZ Commodity Price Index +0.4% month-over-month (last 2.0%)

In news:

The People's Bank of China refrained from injecting liquidity for the eighth consecutive session.

North Korea conducted another missile test ahead of a weekend meeting between U.S. President Donald Trump and China's President Xi Jinping.

Major European indices trade mixed with Spain's IBEX showing relative strength. Germany's DAX -0.5%, France's CAC unch, UK's FTSE unch, Spain's IBEX +0.5%.

In economic data:

Eurozone March Services PMI 56.0 (expected 56.5; last 56.5)

UK's March Services PMI 55.0 (consensus 53.5; last 53.3)

Germany's March Services PMI 55.6, as expected (last 55.6)

France's March Services PMI 57.5 (consensus 58.5; last 58.5)

Italy's March Services PMI 52.9 (expected 54.2; previous 54.1)

Spain's March Services PMI 57.4 (consensus 57.1; prior 57.0)

In news:

Eurogroup chief Jeroen Dijsselbloem said that good progress has been made in talks with Greece, but the two sides remain apart on negotiations to unlock the next tranche of bailout funds. Greek Prime Minister Alexis Tsipras said that an emergency summit of EU leaders should take place if the sides are unable to reach an agreement at Friday's Eurogroup meeting in Malta.

5:56 am: [BRIEFING.COM] S&P futures vs fair value: -0.50. Nasdaq futures vs fair value: -1.40.

5:56 am: [BRIEFING.COM] Nikkei...18861...+51.00...+0.30%. Hang Seng...24401...+139.30...+0.60%.

5:56 am: [BRIEFING.COM] FTSE...7339.26...+17.40...+0.20%. DAX...12249.5...-32.80...-0.30%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

TheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com