Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

TheStrategyLab Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htmTheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

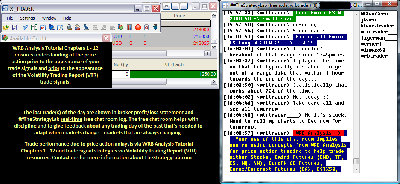

Attachment:

090816-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1250.00.png [ 96.3 KiB | Viewed 270 times ]

090816-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1250.00.png [ 96.3 KiB | Viewed 270 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$1,250.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,250.00 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room for anyone to do a real-time review. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can review

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=160&t=2454  ##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of TheStrategyLab free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use TheStrategyLab free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. TheStrategyLab free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I

keep the peace between members via removing trouble makers so that members can peacefully post their market observations, trades, WRB Analysis commentary about the markets.

TheStrategyLab free chat room is

not for traders looking for someone to hold their hands and tell them when to buy or sell. TheStrategyLab is for you to post

your real-time analysis or trades so that you can

review as feedback for any trading day to provide valuable information about the results in

your broker statements. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Quote:

Also, posted below for you to

review are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=302&t=3259 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives for easy review to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

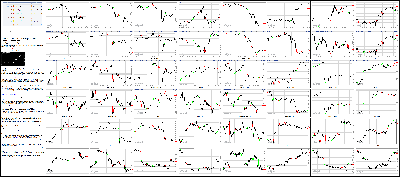

Attachment:

090816-Key-Price-Action-Markets.png [ 1.15 MiB | Viewed 258 times ]

090816-Key-Price-Action-Markets.png [ 1.15 MiB | Viewed 258 times ]

click on the above image to view today's price action of key markets 4:15 pm: [BRIEFING.COM] The stock market ended the Thursday affair modestly lower as the latest directive from the European Central Bank and commentary from ECB President Mario Draghi raised some concerns regarding the future of the central bank's asset purchase program. The Nasdaq Composite (-0.5%) finished behind the Dow Jones Industrial Average (-0.3%) and the S&P 500 (-0.2%).

The major averages began the day on a lower note as inaction from the European Central Bank weighed on European bourses. The central bank held its key interest rates at record lows and maintained the size and scope of its asset purchases. During his press conference, President Draghi noted that the central bank did not see a need to expand the asset purchase program at this time. However, the central bank did affirm plans to continue purchasing assets through March 2017 or beyond, if needed.

Equities retraced opening losses through the first half of trade, benefiting from a rally in crude oil futures. The energy component rallied throughout the session as investors pored over a better-than-expected reading of the Department of Energy's weekly inventory data. The EIA reported that crude oil stockpiles fell by 14.51 million barrels (consensus: +0.22 million) while gasoline inventories declined by 4.21 million barrels (consensus: -0.71 million). WTI crude ended the day higher by 4.8% ($47.66/bbl; +$2.18).

Sellers pressed the broader market shortly after midday as heavily-weighted consumer discretionary (-0.8%) and technology (-0.9%) weighed. The benchmark index managed to maintain technical support near the 2180/2175 price level, finishing the day above its 20-day simple moving average (2180.50). Seven sectors ended in the red with consumer staples (-0.5%), consumer discretionary (-0.8%), and technology (-0.9%) leading to the downside. Conversely, health care (+0.1%), utilities (+0.4%), and energy (+1.7%) topped the board.

The influential technology sector (-0.9%) lagged as top-weighted Apple (AAPL 105.52, -2.84) fell 2.6%. The Dow component was under pressure after announcing that it will no longer release iPhone pre-orders figures. However, the company did reaffirm its fourth-quarter guidance. Meanwhile, Hewlett Packard Enterprise (HPE 21.38, -0.71) declined by 3.2% after reporting a mixed quarter and issuing below-consensus guidance for the fourth quarter.

In the consumer discretionary space (-0.8%), department store names underperformed following the Goldman Sachs 23rd Global Annual Retailing Conference. Kohl's (KSS 43.01, -1.16) and Macy's (M 36.00, -1.19) ended lower by 2.7% and 3.2%, respectively. Elsewhere, Dow component Nike (NKE 56.17, -1.55) ended behind the price-weighted index, declining 2.7%. The stock was under pressure after being downgraded to "Neutral" from "Overweight" at Piper Jaffray.

Biotechnology demonstrated relative strength, evidenced by the 0.7% gain in the iShares Nasdaq Biotechnology ETF (IBB 288.03, +1.93). The sub-group finished ahead of the broader health care space (+0.1%) as Alexion Pharmaceuticals (ALXN 130.06, +4.97) outperformed. Meanwhile, Mylan Labs (MYL 40.57, +0.26) rebounded 0.7%. In the broader sector, Eli Lilly (LLY 79.89, +1.30) jumped 1.7% after being upgraded to "Overweight" at JP Morgan.

Treasuries ended sharply lower with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note rose seven basis points (1.61%) while the yield on the 2-yr note ticked higher by three basis points (0.77%).

Today's participation was above the recent average as more than 818 million shares changed hands on the NYSE floor.

Today's economic data included weekly initial claims and Consumer Credit for July:

Initial claims for the week ending September 3 dipped by 4,000 to 259,000 (Briefing.com consensus 265,000).

The latest report marked the 79th straight week that initial claims have been below 300,000 and it dropped the four-week moving average for the series to 261,250 from 263,000.

Continuing claims for the week ending August 27 decreased by 7,000 to 2.144 million.

The four-week moving average for continuing claims fell to 2.154 million from 2.158 million.

Total outstanding consumer credit increased by $17.7 billion in July (Briefing.com consensus $16.0 billion) after increasing an upwardly revised $14.5 billion (from $12.3 billion) in June.

In the preceding 12-month period leading up to July, consumer credit had risen by an average of $17.3 billion.

For more on these economic releases, be sure to visit Briefing.com's Economic Calendar page.

Tomorrow's economic data will be limited to Wholesale Inventories for July (Briefing.com consensus 0.0%), which will cross the wires at 10:00 ET.

Russell 2000: +10.7% YTD

S&P 500: +6.7% YTD

Dow Jones: +6.1% YTD

Nasdaq: +5.0% YTD

3:30 pm: [BRIEFING.COM]

Commodities, as measured by the Bloomberg Commodity Index, +1.5% around the 85.15 level

Crude oil surged & closed at session highs, extended this morning's post-API gains after EIA data reported notable draws in both crude oil & gasoline inventories

October crude oil futures rose $2.18 (+4.8%) to $47.66/barrel

Yesterday's API data showing an inventory draw of 12.08 mln barrels, compared to last week's build of 0.942 mln barrels and to expectations for a draw of ~100k barrels for the week ending Sept 2.

EIA petroleum inventory highlights:

Crude oil inventories had a draw of -14.513 mln (consensus called for a build of +0.23 mln barrels)

Gasoline inventories had a draw of -4.211 mln (consensus called for a draw of -0.17 mln barrels)

Distillate inventories had a build of +3.382 mln

Factors affecting the price of oil include:

Oil's recent rally was first sparked by API data yesterday evening which showed an inventory draw of 12.08 mln barrels, compared to last week's build of 0.942 mln barrels and to expectations for a draw of ~100k barrels for the week ending Sept 2. This was the largest single draw since 1999.

Gains were further exacerbated by EIA inventory data which showed a surprise large inventory draw in oil & gasoline inventories, a contributing factor to this anomaly is the recent shut downs near the Gulf of Mexico due to Hurricane Hermine as companies took precautions, disrupting production.

The next OPEC meeting will be held in Algiers, Algeria from Sept 26-28, oil prices will continue to see reactions from comments from OPEC & non-OPEC oil producers

Russia and Saudi Arabia agreed to form a coalition to track the oil markets and to provide recommendations, Russia & Saudi Arabia are the 2 largest oil producers in the world, responsible for 20% of global oil production

Natural gas erased yesterday's losses after EIA data showed a smaller-than-expected build compared to Consensus

October natural gas closed $0.13 higher (+4.9%) at $2.81/MMBtu

EIA natural gas inventory highlights:

Natural gas inventory showed a build of +36 bcf vs expectations for inventory to be a build of approximately +43 bcf.

Working gas in storage was 3,437 Bcf as of Friday, Sept 2, 2016, according to EIA estimates.

Stocks were 196 Bcf higher than last year at this time and 306 Bcf above the five-year average of 3,131 Bcf.

At 3,437 Bcf, total working gas is above the five-year historical range.

In precious metals, gold & silver extended the previous session's losses as the dollar traded nearly flat

December gold ended today's session down $7.70 (-0.6%) to $1341.30/oz

December silver closed today's session $0.17 lower (-0.9%) at $19.68/oz

3:05 pm:

[BRIEFING.COM] As the stock market enters its final hour of trade, the Nasdaq Composite (-0.5%) trails the Dow Jones Industrial Average (-0.2%) and the S&P 500 (-0.2%).

On the economic front, the just-released Consumer Credit report for July showed an increase of $17.7 billion while the Briefing.com consensus expected growth of $16.0 billion. The prior month's credit growth was revised higher to $14.5 billion from $12.3 billion.

The leaderboard remains little changed with consumer staples (-0.5%), materials (-0.5%), consumer discretionary (-0.7%), and technology (-0.9%) leading to the downside. Conversely, financials (UNCH), health care (+0.1%), utilities (+0.3%), and energy (+1.7%) sport the only advances.

Treasuries trade at session lows with yields rising through the curve. The yield on the 2-yr note has jumped four basis points (0.77%) while the yield on the 10-yr note is higher by eight basis points (1.62%).

WTI crude ended the day higher by 4.8% ($47.66/bbl; +$2.18).

2:30 pm:

[BRIEFING.COM] The major U.S. indices have inched higher in recent action as the S&P 500 (-0.2%) reclaims its 20-day simple moving average (2180.49).

The energy sector (+1.8%) continues to pace today's advance, extending the group's week-to-date gain to 3.7%. The space is benefiting from a leg higher in crude oil futures. Oil extended an early gain after the Department of Energy reported that weekly crude oil and gasoline inventories declined more than previously expected. WTI crude trades higher by 4.6% ($47.60/bbl; +$2.10) ahead of its pit session close at 14:30 ET.

The dollar-denominated commodity has been able to shrug off some incremental strengthening in the greenback. The U.S. Dollar Index (95.06, +0.10, +0.11%) floats modestly higher as the buck gains ground against the euro and the yen. The euro/dollar pair remains up 0.1% (1.1252) after falling from the 1.1327 price level at the start of the session. Separately, the dollar has jumped 0.8% against the safe-haven yen (102.50).

1:55 pm:

[BRIEFING.COM] The broader market has crept back towards session lows as the Nasdaq Composite (-0.6%) trails the S&P 500 (-0.3%). Elsewhere, the domestically-oriented Russell 2000 (-0.2%) outperforms slightly.

Eight sectors trade in the red with materials (-0.5%), consumer staples (-0.7%), consumer discretionary (-0.9%), and technology (-1.1%) rounding out the leaderboard.

In the consumer staples sector (-0.7%), tobacco names demonstrate relative weakness as the sub-group moves lower in sympathy with Reynolds American (RAI 49.79, -0.61). The name has been under pressure despite reaffirming its full-year outlook. Altria (MO 66.21, -0.51) and Philip Morris International (PM 100.96, -1.13) have lost 0.8% and 1.1%, respectively. Separately, Costco (COST 153.51, -2.13) has declined 1.4%, extending its month-to-date loss to 5.3%. This compares to a loss of 0.6% in the broader sector. The consumer staples group currently rounds out the weekly leaderboard, having fallen 1.3% over that time.

On the commodities front, gold ended its day lower by 0.6% ($1,341.30, -$7.70), narrowing its weekly gain to 1.1%.

1:30 pm:

[BRIEFING.COM] The major U.S. indices continue to see selling pressure in afternoon trading.

A look inside the Dow Jones Industrial Average shows that Apple (AAPL 105.59, -2.77), Nike (NKE 56.32, -1.40), & IBM (IBM 159.00, -2.64) are underperforming. Apple shares are pulling back following yesterday's product announcements after being downgraded to Market Perform at Wells Fargo. Similarly, Nike is lower following this morning's downgrade to Neutral at Piper Jaffray.

Conversely, Goldman Sachs (GS 171.28, +1.61) is the best-performing Dow component as shares extend their recent winning streak with financials modestly outperforming most sectors.

For the week, the DJIA is currently -0.10%.

1:05 pm:

[BRIEFING.COM] The major averages trade on a moderately lower note at midday as participants weigh a disappointing policy statement from the European Central Bank against a rebound in crude oil futures. The Nasdaq Composite (-0.4%) trades behind the Dow Jones Industrial Average (-0.2%) and the S&P 500 (-0.2%).

Equities began the day under pressure as participants responded to the September policy statement from the European Central Bank and somewhat hawkish commentary from ECB President Mario Draghi. The central bank opted to maintain its monetary policy stance, maintaining interest rates at record lows and holding its asset purchase program steady at EUR80 billion. Furthermore, Mr. Draghi noted that the central bank did not see a need to expand its asset purchase program for the time being. The policy statement fell short of expectations as participants remained hopeful for some hints of more easing on the way.

The benchmark index pared opening losses in the first hour as a rally in crude oil bolstered the broader market. The energy component gained overnight after the American Petroleum Institute reported a larger-than-expected draw in crude oil inventories. Crude oil extended its gain after the Department of Energy confirmed the bullish reading with its more influential inventory data. The EIA reported that crude oil stockpiles declined by 14.51 million barrels (consensus: +0.22 million) while gasoline inventories fell by 4.21 million barrels (consensus: -0.71 million). At this juncture, WTI crude trades higher by 4.0% ($47.34/bbl, +$1.84).

The S&P 500 (-0.2%) floats above its 20-day simple moving average (2180.54), maintaining position in the middle of today's trading range. Seven sectors trade in the red with consumer discretionary (-0.7%) and technology (-0.9%) demonstrating relative weakness. Conversely, financials (+0.1%), health care (+0.1%), and energy (+1.6%) outperform.

The economically-sensitive financial sector (+0.1%) demonstrates relative strength as the group responds to some steepening in the yield curve. In the group, money center banks and investment brokerages outperform as Citigroup (C 47.89, +0.41) gains 0.9%. Separately, Dow component Goldman Sachs (GS 171.47, +1.80) leads the price-weighted index. The broader sector has narrowed its week-to-date loss to 0.1%.

Biotechnology demonstrates relative strength in the health care space (+0.1%), evidenced by the 0.8% gain in the iShares Nasdaq Biotechnology ETF (IBB 288.27, +2.17). In the ETF, Alexion Pharmaceuticals (ALXN 129.69, +4.61) has gained 3.5%. Meanwhile, Eli Lilly (LLY 79.96, +1.37) has rallied 1.7% after being upgraded to "Overweight" at JP Morgan.

In the technology sector (-0.9%), Dow component Apple (AAPL 105.71, -2.64) underperforms, losing 2.4%. The name rounds out the price-weighted index after the company announced that it will not release iPhone 7 pre-orders figures. The company stated that the reading is not a representative metric, but reaffirmed its fourth-quarter guidance. Chipmakers trade slightly ahead of the broader sector as the PHLX Semiconductor Index ticks down 0.1%.

The consumer discretionary (-0.7%) space demonstrates relative weakness as Dow component Nike (NKE 56.37, -1.35) underperforms. The stock has declined 2.5% after being downgraded to "Neutral" from "Overweight" at Piper Jaffray. Macy's (M 36.12, -1.07) has declined 2.9% while the broader SPDR S&P Retail ETF (XRT 44.54, -0.22) is down 0.5%.

Treasuries trade lower with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note has increased six basis points (1.60%) while the yield on the 2-yr note has gained two basis points (0.76%).

Today's economic data included weekly initial claims:

Initial claims for the week ending September 3 dipped by 4,000 to 259,000 (Briefing.com consensus 265,000).

The latest report marked the 79th straight week that initial claims have been below 300,000 and it dropped the four-week moving average for the series to 261,250 from 263,000.

Continuing claims for the week ending August 27 decreased by 7,000 to 2.144 million.

The four-week moving average for continuing claims fell to 2.154 million from 2.158 million.

Today's economic data will be capped off with Consumer Credit for July (Briefing.com consensus $16.0 billion), which will be released at 15:00 ET.

12:30 pm:

[BRIEFING.COM] The major averages trade in the middle of today's trading ranges as the S&P 500 (-0.2%) continues to test support near the 2180/2175 price level.

The economically-sensitive financial sector (+0.2%) displays relative strength, enjoying some steepening in the yield curve. European banking names have also advanced with Deutsche Bank (DB 14.79, +0.25) and Credit Suisse (CS 13.69, +0.28) trading higher by 1.8% and 2.1%, respectively. The group has benefitted from a sell off in sovereign bonds. The move lower in bonds was spurred by inaction from the European Central Bank and somewhat hawkish commentary from ECB President Mario Draghi.

Money center banks and investment brokerages outperform with Citigroup (C 48.04, +0.56) and Bank of America (BAC 15.93, +0.22) gaining 1.2% and 1.4%, respectively. The broader sector has narrowed its week-to-date loss to 0.1%.

On the home front, Treasuries trade near session lows with the long end of the curve demonstrating relative weakness. The yield on the 2-yr note has gained two basis points (0.76%) while the yield on the 10-yr note has jumped five basis points (1.59%).

12:00 pm:

[BRIEFING.COM] The S&P 500 (-0.2%) has inched lower in recent trade, floating five points above its worst level of the day.

The influential technology sector (-0.8%) has slipped back towards its session low as Dow component Apple (AAPL 105.90, -2.46) continues to weigh. The stock rounds out the price-weighted index after the company announced that it will not release iPhone 7 pre-orders numbers. The company stated that the reading is not a representative metric. However, Apple did reaffirm its fourth-quarter guidance. Fellow tech large caps Oracle (ORCL 40.76, -0.49) and IBM (IBM 159.46, -2.18) have declined 1.2% and 1.4%, respectively. Oracle is under pressure after being downgraded by OTR.

The high-beta chipmakers pared losses in recent action as the PHLX Semiconductor Index (-0.1%) trades ahead of the broader market. In the group, Micron (MU 17.48, +0.32) outperforms after stating that the NAND flash memory space could be a little more open to potential M&A activity. The company is presenting at Citi's 2016 Global Technology Conference.

On the commodities front, WTI crude trades higher by 3.7% ($47.20/bbl; +$1.70) while gold has slipped 0.4% to $1,343.80/ozt.

11:30 am:

[BRIEFING.COM] The major averages have retraced another portion of their initial gap down as the S&P 500 narrows its loss to 0.1%. The move higher in the broader market corresponded with a similar move in crude oil.

Crude oil futures carved out fresh session highs as investors examined a better-than-expected reading of the Department of Energy's weekly inventory report. Crude oil inventories fell by 14.51 million barrels (consensus: +0.22 million) while gasoline stockpiles declined by 4.21 million barrels (consensus: -0.71 million). The influential inventory report confirmed last evening's inventory data from the American Petroleum Institute. WTI crude currently trades higher by 3.7% ($47.16/bbl, +$1.68).

The commodity-sensitive energy space (+1.3%) leads the remaining sectors, extending its week-to-date gain to 3.1%. The group is followed on the weekly leaderboard by countercyclical telecom services (UNCH; week-to-date: +1.2%) and utilities (+0.1%; week-to-date: +1.1%). Independent oil and gas names outperform as ConocoPhillips (COP 42.45, +0.97) and Apache (APA 57.79, +2.66) gain 2.4% and 4.8%, respectively. Separately, Dow component Chevron (CVX 103.58, +0.71) leads the price-weighted index, having gained 0.7%.

10:55 am:

[BRIEFING.COM] The major averages have pared losses since the last update as the S&P 500 (-0.2%) reclaims its 20-day simple moving average (2180.54).

The consumer discretionary (-0.5%) space demonstrates relative weakness as Dow component Nike (NKE 56.78, -0.94) trades behind the price-weighted index. The stock is underperforming after being downgraded to "Neutral" from "Overweight" at Piper Jaffray. Macy's (M 36.31, -0.88) has declined 2.4% ahead of the Goldman Sachs 23rd Global Annual Retailing Conference. The SPDR S&P Retail ETF (XRT 44.54, -0.22) has declined 0.5%, trading neck-and-neck with the broader sector.

Travel and leisure names outperform in the space as Carnival (CCL 45.37, +0.06) and Priceline (PCLN 1,448.84, +4.83) gain 0.2% and 0.3%, respectively. Meanwhile, Wynn Resorts (WYNN 95.74, +1.39) has jumped 1.5%, extending its month-to-date gain to 7.2%.

Treasuries trade lower with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note has increased three basis points (1.57%) while the yield on the 2-yr note has gained one basis point (0.75%).

The Department of Energy's weekly inventory report is set to cross the wires at 11:00 ET.

10:40 am: [BRIEFING.COM]

Commodities, as measured by the Bloomberg Commodity Index, +0.4% around the 84.24 level

Crude oil saw a boost after API inventory showed a much larger draw compared to expectations for a small build

October crude oil futures were up $0.66 (+1.5%) around the $46.16/barrel level ahead of 11:00 am EIA data

API data showed an inventory draw of 12.08 mln barrels, compared to last week's build of 0.942 mln barrels and to expectations for a draw of ~100k barrels for the week ending Sept 2.

Baker Hughes weekly rig count data will be released tomorrow at 1 pm ET.

Monthly IEA data will be released Sept 13

The next OPEC meeting will take place in Algiers, Algeria from Sept 26-28

Natural gas futures extended this morning's notable +2% surge, hit new highs of the day post-EIA, showed smaller build vs. Consensus

October natural gas futures were up $0.10 (+3.6%) around the $2.77/MMBtu level following EIA data

Natural gas inventory showed a build of +36 bcf vs expectations for inventory to be a build of approximately +43 bcf.

Working gas in storage was 3,437 Bcf as of Friday, September 2, 2016, according to EIA estimates.

Stocks were 196 Bcf higher than last year at this time and 306 Bcf above the five-year average of 3,131 Bcf.

At 3,437 Bcf, total working gas is above the five-year historical range.

In precious metals, gold & silver traded nearly flat as the dollar struggled to find direction

Gold futures were down $0.50 (-0.1%) around the $1348.70/oz level

Silver futures were down $0.02 (-0.1%) around the $19.83/oz level

10:00 am:

[BRIEFING.COM] The major averages notched new session lows as the Nasdaq Composite (-0.5%) trails the Dow Jones Industrial Average (-0.4%) and the S&P 500 (-0.3%).

Seven sectors continue to trade in the red with materials (-0.5%), consumer discretionary (-0.5%), and technology (-0.8%) rounding out the leaderboard. Conversely, telecom services (+0.1%), utilities (+0.1%), and energy (+0.5%) outperform.

The Dow Jones Transportation Average (-0.1%) trades ahead of the broader market as airline names continue to lead. The U.S. Global Jets ETF (JETS 23.77, +0.10) has gained 0.4%. On the flipside, rail names underperform as CSX (CSX 28.61, -0.19) declines 0.7%. The broader index sports a gain of 1.3% for the week, outperforming the benchmark index (-0.3%; week-to-date: -0.1%) over that time.

The U.S. Dollar Index (94.72, -0.23, -0.25%) has ticked off a session low as the yen and the euro gain ground against the greenback. The dollar has lost 0.2% against the safe-haven yen (101.56) while the euro has jumped 0.5% against the buck (1.1292). The euro is benefiting from recent commentary from ECB President Mario Draghi, indicating that the central bank is currently not looking to expand its asset purchasing programs.

9:45 am:

[BRIEFING.COM] The stock market began the day on a lower note with the Dow Jones Industrial Average (-0.4%) and the Nasdaq Composite (-0.4%) trading slightly behind the S&P 500 (-0.3%).

Nine sectors trade in the red with consumer discretionary (-0.5%) and technology (-0.5%) leading the downside. The remaining decliners sport losses between 0.1% (utilities) and 0.3% (health care). Conversely, the commodity-sensitive energy (+0.5%) sector tops the board.

In the technology space (-0.5%), top-weighted Apple (AAPL 106.48, -1.88) displays relative weakness. The stock has tumbled 1.7% after it unveiled the iPhone 7 yesterday. Apple recently announced that it will not release pre-order numbers for the device, indicating that it is not a representative metric. Separately, the PHLX Semiconductor Index underperforms, slipping 0.5%.

Biotechnology trades behind the broader health care space (-0.3%), evidenced by the 0.4% decline in the iShares Nasdaq Biotechnology ETF (IBB 284.87, -1.23).

On the commodities front, WTI crude trades higher by 2.0% ($46.38/bbl, +$0.88) while gold has ticked higher by 0.1% to $1,349.90/ozt.

9:19 am: [BRIEFING.COM] S&P futures vs fair value: -6.00. Nasdaq futures vs fair value: -17.10.

The stock market is on track for a lower open as the S&P 500 futures trade six points below fair value.

Equity futures carved out fresh session lows in recent action, responding to the recently-released September policy statement from the European Central Bank and commentary from ECB President Mario Draghi. The central bank opted to maintain its monetary policy stance, holding its main refinancing operations, marginal lending facility, and deposit facility rates unchanged at 0.00%, 0.25%, and -0.40%, respectively. The ECB also maintained its asset purchase levels, signaling that purchases will continue at least through March 2017. The statement was a disappointment for stimulus-hungry investors who hoped that the central bank would entertain the idea of expanding asset purchases.

ECB President Mario Draghi stated that there is no need for additional stimulus measures at this time, but that the central bank remains ready in the event of persistent downside risks. Mr. Draghi also signaled that third-quarter growth appears to expanding at the same rate as in the second quarter. The tone of the speech has elicited a bid in the euro with the single currency gaining 0.7% against the dollar (1.1313). However, the euro/dollar pair has pulled back from its best level (1.1327).

In company specific news, Nike (NKE 56.77, -0.95) trades lower by 1.7% after being downgraded to "Neutral" from "Overweight" at Piper Jaffray. The firm cited increased competition in the apparel sector. Separately, Tractor Supply (TSCO 71.80, -11.73) has tumbled 14.0% after lowering its third-quarter and full-year outlook below consensus. The company is scheduled to present at the Goldman Sachs Global Retailing Conference later in the day.

Today's economic data will be capped off with Consumer Credit for July (Briefing.com consensus $16.0 billion), which will be released at 15:00 ET.

8:55 am: [BRIEFING.COM] S&P futures vs fair value: -4.20. Nasdaq futures vs fair value: -11.90.

The S&P 500 futures trade four points below fair value.

Equity indices in the Asia-Pacific region ended Thursday on a mixed note, but once again, trading ranges were limited. Japan's second-quarter GDP was revised up to 0.2% from 0.0%, but that did not stop Bank of Japan officials from discussing more stimulus measures. Deputy Governor Hiroshi Nakaso said he would not rule out taking interest rates deeper into negative territory in hopes of achieving the 2.0% inflation target. Elsewhere, China's August trade surplus ($52.05 billion; expected $58.00 billion) missed headline expectations, but both imports (+1.5%; expected -4.9%) and exports (-2.8%; expected -4.0%) surpassed estimates.

In economic data:

China's August trade surplus $52.05 billion (expected $58.00 billion; last $52.31 billion). August Imports +1.5% year-over-year (expected -4.9%; last -12.5%) and August Exports -2.8% year-over-year (expected -4.0%; prior -4.4%)

Japan's Q2 GDP +0.2% quarter-over-quarter (expected 0.0%; last 0.0%); +0.7% year-over-year (expected 0.2%; last 0.2%). Q2 GDP Capital Expenditure -0.1% quarter-over-quarter (expected -0.4%; last -0.4%) and July adjusted current account surplus narrowed to JPY1.45 trillion from JPY1.65 trillion (expected surplus of JPY1.59 trillion). August Economy Watchers Current Index 45.6 (expected 45.2; last 45.1)

Australia's July trade deficit narrowed to AUD2.41 billion from AUD3.25 billion (expected deficit of AUD2.75 billion)

---Equity Markets---

Japan's Nikkei shed 0.3% with seven sectors ending in the red. Materials (-1.7%), utilities (-1.4%), and communications (-1.3%) lagged while health care (+0.8%) outperformed. Dentsu, Nitto Denko, Alps Electric, Mitsubishi Electric, Yamaha, Sumitomo Metal Mining, Daikin Industries, and Hitachi lost between 1.6% and 3.5%.

Hong Kong's Hang Seng climbed 0.8% to a fresh one-year high. Gaming and property names showed relative strength with Galaxy Entertainment, Sands China, Sino Land, Hang Lung Properties, SHK Properties, New World Development, and Bank of East Asia climbed between 1.5% and 5.3%.

China's Shanghai Composite added 0.1%. PCI-Suntek Technology, Jiangsu Sopo Chemical, Shanghai Zhixin Electric, and Shengyi Technology gained between 6.0% and 6.7%.

Major European indices trade lower as investors continue to respond to remarks from European Central Bank President Mario Draghi. The European Central Bank released its latest policy statement earlier, maintaining its monetary policy stance. The euro is higher by 0.7% against the dollar, trading at a two-week high, near 1.1315.

Economic data was limited:

France's Q2 Non-Farm Payrolls +0.2% quarter-over-quarter, as expected

---Equity Markets---

Germany's DAX is lower by 0.6%. Infineon is the weakest performer, down 1.6%, while select exporters also trade in negative territory. BMW is down 1.5% and Daimler has given up 0.8%. Financials outperform with Commerzbank and Deutsche Bank up 0.2% and 0.7%, respectively.

France's CAC trades lower by 0.5% amid weakness in consumer stocks. Carrefour, Danone, Louis Vuitton, and L'Oreal show losses between 1.4% and 1.9%. Financials have held up well with BNP Paribas, Credit Agricole, and Societe Generale all up near 0.3%.

UK's FTSE trades up 0.3% with Micro Focus in the lead. The stock has surged 16.0% after agreeing to acquire Hewlett Packard Enterprise's software arm for $8.80 billion. Consumer names and financials also outperform with Dixons Carphone, EasyJet, Hargreaves Lansdown, Taylor Wimpey, Persimmon, Barratt Developments, HSBC, and RBS climbing between 0.8% and 3.9%.

Spain's IBEX outperforms with a gain of 0.4%. Bank stocks lead with Banco Sabadell, Santander, Bankia, Banco Popular, BBVA, and Caixabank are up between 1.4% and 2.2%.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: -0.50. Nasdaq futures vs fair value: -4.50.

Futures trade little changed as investors weigh recently-released employment data and wait to hear from ECB President Mario Draghi. The S&P 500 futures trade within one point of fair value.

Just released, the latest weekly initial jobless claims count totaled 259,000 while the Briefing.com consensus expected a reading of 265,000. Today's tally was below the unrevised prior week's count of 263,000. As for continuing claims, they fell to 2.144 million from 2.151 million.

8:05 am: [BRIEFING.COM] S&P futures vs fair value: -1.00. Nasdaq futures vs fair value: -5.10.

U.S. equity futures trade modestly lower with the S&P 500 futures floating one point below fair value. Index futures inched lower after the European Central Bank announced that it would leave its key interest rates unchanged, as expected. The central bank also reaffirmed plans to continue its asset purchase program through March 2017 or beyond, if needed. As a reminder, ECB President Mario Draghi is slated to begin his press conference at 8:30 ET.

On the commodities front, the API reported that crude oil stockpiles fell by 12.0 million barrels (last: +0.94 million barrels) while gasoline inventories declined by 2.40 million barrels (last: -1.60 million barrels). WTI crude trades higher by 1.5% ($46.20/bbl; +$0.70). The Department of Energy's more influential stockpile data is set to cross the wires at 11:00 ET.

Treasuries trade on a lower note with yields rising through the curve. The yield on the 10-yr note is higher by one basis point (1.55%) while the yield on the 2-yr note has also ticked up one basis point (0.75%).

Today's economic data will include weekly initial claims (Briefing.com consensus 265k) and Consumer Credit for July (Briefing.com consensus $16.0 billion), which will cross the wires at 8:30 ET and 15:00 ET, respectively.

In U.S. corporate news of note:

Pier 1 Imports (PIR 4.05, -0.75): -15.6% after lowering its Q2 guidance below-consensus and announcing that President and CEO Alex Smith will step down

Hewlett Packard Enterprise (HPE 21.82, -0.27): -1.2% following the company reporting a mixed quarter and guiding Q4 earnings below consensus

Tesla Motors (TSLA 200.00, -1.71): -0.9% after Cowen initiated coverage on the name with an "Underperform" designation and a price target of $160

Tailored Brands (TLRD 15.92, +1.69): +11.9% following the company beating top- and bottom-line estimates for the quarter

Reviewing overnight developments:

Asia-Pacific indices ended on a mixed note with Hong Kong's Hang Seng (+0.8%) outpacing China's Shanghai Composite (+0.1%) and Japan's Nikkei (-0.3%).

In economic data:

China's August trade surplus $52.05 billion (expected $58.00 billion; last $52.31 billion). August Imports +1.5% year-over-year (expected -4.9%; last -12.5%) and August Exports -2.8% year-over-year (expected -4.0%; prior -4.4%)

Japan's Q2 GDP +0.2% quarter-over-quarter (expected 0.0%; last 0.0%); +0.7% year-over-year (expected 0.2%; last 0.2%). Q2 GDP Capital Expenditure -0.1% quarter-over-quarter (expected -0.4%; last -0.4%) and July adjusted current account surplus narrowed to JPY1.45 trillion from JPY1.65 trillion (expected surplus of JPY1.59 trillion). August Economy Watchers Current Index 45.6 (expected 45.2; last 45.1)

Australia's July trade deficit narrowed to AUD2.41 billion from AUD3.25 billion (expected deficit of AUD2.75 billion)

In news:

Japan's second-quarter GDP was revised up to 0.2% from 0.0%, but that did not stop Bank of Japan officials from discussing more stimulus measures.

Deputy Governor Hiroshi Nakaso said he would not rule out taking interest rates deeper into negative territory in hopes of achieving the 2.0% inflation target.

China's August trade surplus ($52.05 billion; expected $58.00 billion) missed headline expectations, but both imports (+1.5%; expected -4.9%) and exports (-2.8%; expected -4.0%) surpassed estimates.

European indices trade on a mixed note with the U.K.'s FTSE (+0.2%) leading France's CAC (-0.4%), and Germany's DAX (-0.6%). Elsewhere, Spain's IBEX outperforms (+0.6%).

Economic data was limited:

France's Q2 Non-Farm Payrolls +0.2% quarter-over-quarter, as expected

In news:

The European Central Bank released its latest policy statement, leaving its interest corridor unchanged.

ECB President Mario Draghi will conduct his press conference at 8:30 ET.

The euro is higher by 0.5% against the dollar, trading at a two-week high, near 1.1298.

6:00 am: [BRIEFING.COM] S&P futures vs fair value: +1.80. Nasdaq futures vs fair value: +0.60.

6:00 am: [BRIEFING.COM] Nikkei...16959...-53.70...-0.30%. Hang Seng...23919...+177.50...+0.80%.

6:00 am: [BRIEFING.COM] FTSE...6877.50...+30.90...+0.50%. DAX...10730.85...-22.10...-0.20%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries. Also, thank you for the review of TheStrategyLab performance record...hopefully the links will be useful for you.

Best Regards,

M.A. Perry

TheStrategyLab Price Action Trading

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

TheStrategyLab Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com