Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room: http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Archive Real-Time Chat Logs (timestamp, entries/exits, position size):

http://www.thestrategylab.com/ftchat/forum/viewforum.php?f=20 Accolades (Testimonials): http://www.thestrategylab.com/Accolades.htmBusiness Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://stocktwits.com/wrbtrader (24/7)

http://twitter.com/wrbtrader (24/7)

Quote:

No trades today because I wanted to rest my right arm after feeling some soreness towards the end of yesterday's trading session that was very profitable for me due to the increasing volatility levels.

Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $0.00 dollars Disclaimer: Today's trading performance is not an indication of my future performance and not an indication of the future performance for any trader that decides to learn/apply WRB Analysis.Russell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Today's Trade Log: All of my live trades are posted

real-time in the timestamp ##TheStrategyLab

free chat room. The live trade is posted 3.2 seconds on average after the trade confirmation via an auto script to minimize delays in posting of my trades. You can read

today's price action trade journal about my trades (e.g. time, price entry, contract size, price exit, market analysis) as the trade traversed to its completion. In addition, sometimes I'll post

real-time trading tips in the free ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=160&t=2450 The free chat room is

not a signal calling trading room. I do

not mentor (never have) although I get many requests to do mentoring. There is education but

only in members private threads at the forum involving members asking questions (help) about their own trading. Thus, the primary purpose of the free chat room is for you to use as your

trade journal so that you can use as valuable feedback and for members to help each other...as in more eyes on the market. Also, you can use the free chat room to ask real-time WRB Analysis questions. Yet, please do

not post your brokerage statements in the free chat room. Instead, its highly recommended that you only post your brokerage statements in your private thread for

security reasons. The free chat room is on IRC via users request because the IRC servers are located in many different countries, software in many different languages and many different types of social media software can be used to log in. I'm the

moderator of the free chat room. Thus, I keep the peace between members and I keep out the trouble makers so that members can peacefully post their observations about the markets, trades and WRB Analysis commentary.

Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling trading room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=300&t=3238 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker PnL statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

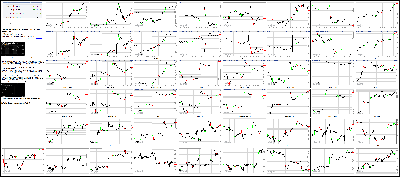

Attachment:

090216-Key-Price-Action-Markets.png [ 1.05 MiB | Viewed 295 times ]

090216-Key-Price-Action-Markets.png [ 1.05 MiB | Viewed 295 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market ended the week on a modestly higher note as an inconclusive reading of the Employment Situation Report for August left fed funds rate hike expectations up in the air. The S&P 500 (+0.4%) finished in-line with the Nasdaq Composite (+0.4%) and the Dow Jones Industrial Average (+0.4%). The three indices ended the week higher between 0.5% and 0.6%.

Today's session began on a higher note as weaker-than-expected headline figures from the August employment report spurred buying interest in the broader market. The report indicated that 151,000 nonfarm payrolls were added in August (Briefing.com consensus 180,000) while the July number was revised to 275,000 (from 255,000). Separately, average hourly earnings came in cooler-than-expected, rising 0.1% (Briefing.com consensus 0.2%). The implied probability of an interest rate hike at the September Fed meeting fell to 18.0% shortly after the release of the report.

Participants walked back the knee-jerk reaction throughout the session, eyeing the longer-term trend in labor market data. The monthly nonfarm reading missed consensus estimates, but job growth has still averaged 232,000 over the past three months. Separately, remarks from the likes of Bill Gross and Richmond Fed President (a non-FOMC voter) Jeffrey Lacker worked to keep the possibility of a rate hike in play. The implied probability for a rate hike at the September meeting rebounded to 21.0% by the end of the session, slipping from the prior session estimate of 24.0%.

The S&P 500 (+0.4%) settled off its best level of the day, testing technical support near the 2173/2176 price level. All ten sectors ended in the green with materials (+0.8%), energy (+0.8%), and utilities (+1.2%) leading the pack. Conversely, countercyclical health care (+0.1%) and telecom services (+0.1%) finished with the slimmest gains. Other focal points impacting today's trade included a rebound in crude oil and sector leadership from heavily-weighted financials (+0.5%).

The economically-sensitive financial sector (+0.5%) ended ahead of the benchmark index, extending this week's gain to 2.0%. Money center banks rebounded in the space as investors responded to a steepening yield curve and a reversal in rate hike expectations. JPMorgan Chase (JPM 67.49, +0.28) and Citigroup (C 47.51, +0.15) finished higher by 0.4% apiece.

The Dow Jones Transportation Average (+0.4%) ended in-line with the broader market as shipping names and airlines outperformed. The U.S. Global Jets ETF (JETS 22.75, +0.27) ended higher by 1.4% as investors mulled August operational results from Delta Air Lines (DAL 37.17, +0.35) and Alaska Air (ALK 68.21, +0.95). The broader transportation index ended the week higher by 1.6%.

In the consumer discretionary sector (+0.2%), lululemon athletica (LULU 68.57, -8.09) weighed on the retail sub-group, sinking 10.6%. The name reported in-line quarterly results, but issued full-year guidance that was a bit light relative to expectations. Separately, Gap (GPS 23.92, -0.63) ended lower by 2.6% after reporting that same-store sales fell 3.0% in August. This compares to last August's decline of 2.0%.

The heavily-weighted health care sector (+0.1%) finished near its flat line as biotechnology underperformed. The iShares Nasdaq Biotechnology ETF (IBB 280.61,- 0.83) was under pressure after Democratic Presidential nominee Hillary Clinton unveiled plans to combat "unjustified price hikes" in the pharmaceutical industry. The plan includes making alternative medications available and fining drug makers for excessive price increases for long-standing treatments.

Treasuries ended on a lower note with the long end of the curve demonstrating relative weakness. The yield on the 2-yr note ended higher by one basis point (0.79%) while the yield on the 10-yr note settled higher by three basis points (1.60%).

Today's participation was below the recent average as fewer than 782 million shares changed hands on the NYSE floor.

Today's economic data included the Employment Situation Report for August, the Trade Balance for July, and Factory Orders for July:

The August employment report showed a deceleration in the labor market from recent months.

Nonfarm payrolls increased by 151,000 (Briefing.com consensus 180,000). Over the past three months, job gains have averaged 232,000 per month.

July nonfarm payrolls revised to 275,000 from 255,000

Private sector payrolls increased by 126,000 (Briefing.com consensus 175,000)

July private sector payrolls revised to 225,000 from 217,000

Unemployment rate was 4.9% (Briefing.com consensus 4.8%) versus 4.9% in July

Persons unemployed for 27 weeks or more accounted for 26.1% of the unemployed versus 26.6% in July

August average hourly earnings were up 0.1% (Briefing.com consensus 0.2%) after being up 0.3% in July

Over the last 12 months, average hourly earnings have risen 2.4% versus 2.6% for the 12-month period ending in July

The average workweek was 34.3 hours (Briefing.com consensus 34.5) versus 34.4 hours in July

The labor force participation rate was 62.8% versus 62.8% in July

The July Trade Balance Report showed a narrowing in the trade deficit to $39.5 billion (Briefing.com consensus -$43.0 billion) from a downwardly revised $44.7 billion deficit (from -$44.5 billion) for June.

Net exports will provide a positive contribution to third quarter GDP as the real trade deficit of $58.3 billion for July was 4.3% less than the second quarter average.

New orders for manufactured goods increased 1.9% in July (Briefing.com consensus +2.0%) following a downwardly revised 1.8% decline (from -1.5%) for June. Excluding transportation, orders were up 0.2% after a 0.4% increase for June.

Transportation equipment orders (and particularly nondefense aircraft and parts orders ) drove much of the strength in July factory orders.

For further details on these economic releases, be sure to visit Briefing.com's Economic Calendar page.

Bond and equity markets will be closed on Monday in observance of Labor Day. Tuesday's economic data will be limited to ISM Services for August (Briefing.com consensus 54.7), which will cross the wires at 10:00 ET.

Russell 2000: +10.0% YTD

S&P 500: +6.7% YTD

Dow Jones: +6.1% YTD

Nasdaq Composite: +4.8% YTD

Week in Review: Stocks Climb Ahead of Labor Day

The stock market saw another week of limited movement, but managedto erase the bulk of last week's loss nonetheless. The S&P 500 added 0.5%thanks to a Friday rally, which took root after the release of a disappointing EmploymentSituation report for August.

According to the report, only 151,000 nonfarm payrolls wereadded, which was short of the Briefing.com consensus estimate of 180,000.Furthermore, average hourly earnings edged up just 0.1% (Briefing.com consensus0.2%), leaving the year-over-year growth rate at 2.4%, which was down from 2.6%in July. The dollar dipped after the release, but rebounded as the day wore on.

As for the fed funds futures market, the initial reaction tothe report saw a dip in near-term rate hike expectations, but only a portion ofthat move held. The implied likelihood of a hike in September ticked down to21.0% from 24.0% while the probability of a December hike improved to 54.2%from 53.6% on Thursday.

In sum, the Employment Situation report was not weak enoughto convince investors that a September rate hike is out of the question. The Treasurymarket agreed with that assessment, leading to some steepening in the yieldcurve on Friday as the long end underperformed.

With Labor Day around the corner, the upcoming weeksare expected to feature increased volume as market participants return fromvacations.

3:40 pm: [BRIEFING.COM]

Gold and silver futures held today's gains and finished near its HoD

Dec gold rose 0.7% to $1326.80/oz in today's session, while Dec silver gained 2.2% to $19.37/oz

In base metals, Dec copper, however, closed the day out unchanged at $2.08/lb

Moving onto the energy space...

Oct WTI oil held up nicely today, finishing 2.8% to $44.39/barrel

In other energy, Oct nat gas lost one cent to finish at $2.79/MMBtu

2:55 pm:

[BRIEFING.COM] As the stock market enters its final hour of trade, the S&P 500 sports a modest gain of 0.3%. Elsewhere, the S&P Mid Cap 400 (+0.7%) and the Russell 2000 (+0.7%) outperform.

Eight sectors trade in the green with energy (+0.9%) and utilities (+1.1%) leading to the upside. The remaining gainers show advances between 0.1% (consumer discretionary) and 0.6% (materials). Conversely, countercyclical telecom services (UNCH) and health care (UNCH) trade modestly lower.

In the financial sector (+0.5%), life insurance names outperform as MetLife (MET 43.28, +0.22) and Prudential (PRU 79.57, +0.73) trade higher by 0.5% and 0.9%, respectively. The broader group continues to benefit from steepening in the yield curve. The sector as a whole has gained 2.0% this week, leading the weekly leaderboard.

Treasuries trade on a lower note as the long end of the curve demonstrates relative weakness. The yield on the 10-yr note has risen three basis points (1.60%) while the yield on the 2-yr note is higher by one basis point (0.79%).

WTI crude ended its day higher by 2.8% ($44.39/bbl; +$1.22), trimming its weekly loss to 6.8%.

2:25 pm:

[BRIEFING.COM] The major averages have inched higher in recent action as the S&P 500 (+0.3%) continues to trade in-line with the Dow Jones Industrial Average (+0.3%). Both indices sport weekly gains of 0.4% apiece.

The energy sector (+0.8%) trades ahead of the broader market, trailing only the defensively-oriented utilities group (+0.9%). The space is benefiting from a rebound in crude oil futures. WTI crude trades higher by 3.4% ($44.64/bbl; +$1.48) ahead of its pit session close at 14:30 ET. The energy component has narrowed its week-to-date loss to 6.3%.

In the energy sector, independent oil and gas names demonstrate relative strength as Occidental Petroleum (OXY 77.48, +0.64) and ConocoPhillips (COP 41.02, +0.42) trade higher by 0.9% and 1.0%, respectively. Separately, Dow component Chevron (CVX 100.87, +0.66) trades ahead of the price-weighted index. The stock has declined 0.4% this week, which compares to a loss of 0.4% in the broader sector.

The U.S. Dollar Index (95.87, +0.21, +0.22%) floats near its session high as the greenback shows gains against the euro and the yen. The euro/dollar pair has lost 0.3% (1.1159) while the dollar has jumped 0.8% against the safe-haven yen (104.03).

2:00 pm:

[BRIEFING.COM] The S&P 500 (+0.2%) continues to hold a modest gain, trading ahead of the tech-heavy Nasdaq Composite (+0.1%).

The influential technology sector (+0.1%) hovers above its flat line, masking weakness in software name Salesforce.com (CRM 74.78, -1.13). The stock has extended its post-earnings decline to 5.8%. Conversely, Activision Blizzard (ATVI 42.69, +0.54) and Electronic Arts (EA 82.94, +1.18) outperform.

The high beta chipmakers display relative weakness as the PHLX Semiconductor Index (-0.4%) trims its week-to-date gain to 0.5%. In the group. Broadcom (AVGO 172.73, -4.36) and Ambarella (AMBA 66.59, -5.18) trade lower by 2.5% and 7.3%, respectively. Both names beat analysts' estimates for the quarter, but were unable to impress with largely in-line guidance.

On the central bank front, Richmond Fed President, and non-FOMC voter, Jeffrey Lacker recently stated that the fed funds rate should be significantly higher than it is now. President Lacker also expressed concerns over a potential upswing in inflation, causing the central bank to potentially fall behind the curve. Remarks from Mr. Lacker fit with today's action in the bond market where the yield curve has steepened.

1:30 pm:

[BRIEFING.COM] The major U.S. indices continue to trade in a very narrow range, sporting small gains ahead of the holiday weekend.

A look inside the Dow Jones Industrial Average shows that Chevron (CVX 101.14, +0.93), Boeing (BA 131.02, +1.12), & DuPont (DD 70.18, +0.45) are outperforming amid broad market gains, with all 10 major sectors in the green. Chevron is at the top of the Dow as the energy sector rallies on the heels of a 3% spike in crude oil futures.

Conversely, Wal-Mart (WMT 72.54, -0.30) is the worst-performing Dow component as shares cool off following yesterday's gains.

At current levels, the DJIA is posed to close the week higher by 0.4%.

1:05 pm:

[BRIEFING.COM] The stock market trades on a flat note at midday as investors continue to decipher the Employment Situation Report for August. At midday, the Dow Jones Industrial Average (+0.3%) trades neck-and-neck with the Nasdaq Composite (+0.3%) and the S&P 500 (+0.3%). The three indices sport week-to-date gains between 0.3% and 0.4%.

Equities climbed at the start of the session as participants mulled over the August employment report. The report signaled that nonfarm payrolls increased by 151,000, missing the Briefing.com consensus of 180,000. The report also contained a cooler-than-expected reading of average hourly earnings, indicating an increase of 0.1% (Briefing.com consensus +0.2%). Average hourly earnings have ticked higher by 2.4% year-over-year, slipping from last month's reading of 2.6%.

The initial headline reaction to the report sent fed funds futures lower, reducing the implied probability of a rate hike at the September meeting to 18.0% from yesterday's reading of 24.0%. However, participants have since walked back their initial reaction as the likelihood of a September hike rises back to 24.0%. The Treasury complex also erased early gains while the U.S. Dollar Index (95.81, +0.16, +0.16%) hovers near a session high.

The benchmark index has pared gains through the opening half of trade, floating near recently-establish support at the 2173/2176 price level. Eight sectors trade in the green with consumer staples (+0.7%), utilities (+0.8%), and energy (+0.9%) leading the advance. The remaining gainers sport upticks between 0.1% (technology) and 0.5% (materials). Conversely, countercyclical telecom services (-0.1%) and health care (-0.1%) underperform.

The Dow Jones Transportation Average (+0.3%) demonstrates relative strength as shipping companies outperform. Matson (MATX 42.35, +1.17) and Kirby (KEX 53.45, +1.55) top the index, gaining 2.9% and 3.0%, respectively. Conversely, rail names underperform as Union Pacific (UNP 95.13, -0.16) trades lower by 0.2%. The Transportation index sports a week-to-date gain of 1.5%, leading the broader industrial sector (+0.2%; week-to-date: +0.2%) over that time.

The consumer discretionary sector (+0.2%) trades slightly behind the broader market as cruise ship names underperform. Carnival (CCL 46.49, -2.21) trades lower by 4.5% after being downgraded to "Under-Weight" from "Equal-Weight" at Morgan Stanley. Separately, lululemon athletica (LULU 70.06, -6.59) weighs on the retail sector after getting downgraded to "Equal-Weight" at Morgan Stanley. The company reported in-line quarterly results and issued full-year guidance that was a bit light relative to expectations. Conversely, Dow component Home Depot (HD 135.11, +0.88) trades ahead of the price-weighted index.

The heavily-weighted health care sector (-0.1%) trades just beneath its flat line, responding to ongoing concerns regarding drug pricing practices. Democratic Presidential nominee Hillary Clinton recently announced plans to combat "unjustified price hikes" by making alternative medications available and fining drug makers for excessive price increases for long-standing treatments. The iShares Nasdaq Biotechnology ETF (IBB 280.43, -1.01) trades lower by 0.4%, extending its weekly loss to 1.7%. This compares to a week-to-date loss of 0.7% in the broader sector.

The Treasury complex trades lower as the long end of the curve demonstrates relative weakness. The yield on the 2-yr note is flat at 0.79% while the yield on the benchmark 10-yr note has increased two basis points to 1.59%.

Today's economic data included the Employment Situation Report for August, the Trade Balance for July, and Factory Orders for July:

The August employment report showed a deceleration in the labor market from recent months.

Nonfarm payrolls increased by 151,000 (Briefing.com consensus 180,000). Over the past three months, job gains have averaged 232,000 per month.

July nonfarm payrolls revised to 275,000 from 255,000

Private sector payrolls increased by 126,000 (Briefing.com consensus 175,000)

July private sector payrolls revised to 225,000 from 217,000

Unemployment rate was 4.9% (Briefing.com consensus 4.8%) versus 4.9% in July

Persons unemployed for 27 weeks or more accounted for 26.1% of the unemployed versus 26.6% in July

August average hourly earnings were up 0.1% (Briefing.com consensus 0.2%) after being up 0.3% in July

Over the last 12 months, average hourly earnings have risen 2.4% versus 2.6% for the 12-month period ending in July

The average workweek was 34.3 hours (Briefing.com consensus 34.5) versus 34.4 hours in July

The labor force participation rate was 62.8% versus 62.8% in July

The July Trade Balance Report showed a narrowing in the trade deficit to $39.5 billion (Briefing.com consensus -$43.0 billion) from a downwardly revised $44.7 billion deficit (from -$44.5 billion) for June.

Net exports will provide a positive contribution to third quarter GDP as the real trade deficit of $58.3 billion for July was 4.3% less than the second quarter average.

New orders for manufactured goods increased 1.9% in July (Briefing.com consensus +2.0%) following a downwardly revised 1.8% decline (from -1.5%) for June. Excluding transportation, orders were up 0.2% after a 0.4% increase for June.

Transportation equipment orders (and particularly nondefense aircraft and parts orders ) drove much of the strength in July factory orders.

12:30 pm:

[BRIEFING.COM] The major averages continue to pare early gains amid concerns that the Employment Situation report for August was not weak enough to prevent the Federal Reserve from hiking rates. The S&P 500 has narrowed its advance to 0.2%.

In the consumer staples sector (+0.7%), Costco (COST 157.70, +1.49) demonstrates relative strength, rebounding from yesterday's 3.6% decline. The name was under pressure after reporting flat same-store sales for the month of August. Separately, tobacco names outperform as Philip Morris International (PM 101.85, +1.25) and Reynolds American (RAI 50.60, +0.85) trade higher by 1.2% and 1.7%, respectively. Conversely, food product names continue to demonstrate relative weakness as Kraft Heinz (KHC 89.40, -0.08) trades lower by 0.1%. The sub-group came under pressure after Campbell Soup (CPB 57.66, +0.75) reported weaker-than-expected quarterly results yesterday. The broader sector has gained 0.8% this week, trailing only the financial sector (+0.2%; week-to-date: +1.6%) over that time.

The Treasury complex floats near its session low as yields rise through the curve. The yield on the benchmark 10-yr note has risen three basis points to 1.60%. For the week, the 10-yr yield has declined two basis points.

12:00 pm:

[BRIEFING.COM] Equities indices trades modestly higher with the S&P 500 gaining 0.4% while small-cap and mid-cap indices outperform with the S&P Mid Cap 400 and the Russell 2000 advancing 0.7% apiece.

The heavily-weighted health care sector (+0.1%) trades narrowly above its flat line as the group narrows its week-to-date loss to 0.6%. The group has been under pressure recently as drug pricing continues to draw public scrutiny. On that note, Democratic Presidential nominee Hillary Clinton recently announced plans to combat "unjustified price hikes." These included making alternative medications available and fining drug makers for excessive price increases involving long-standing treatments. Recall that Mylan Labs (MYL 41.04, -0.84) has been under pressure for price increases involving its EpiPen device. The broader iShares Nasdaq Biotechnology ETF (IBB 281.83, +0.39) sports a loss of 1.2% week to date.

Conversely, Biogen (BIIB 315.97, +9.94) outperforms after its Aducanumab medication was granted Fast Track designation by the FDA.

On the commodities front, WTI crude trades higher by 3.1% ($44.49/bbl; +1.33) while gold has ticked higher by 0.4% to $1,323.00/ozt.

11:35 am:

[BRIEFING.COM] The major U.S. indices have traded in sideways fashion as the Dow Jones Industrial Average (+0.5%) trades slightly ahead of the S&P 500 (+0.4%).

The consumer discretionary sector (+0.3%) trades a touch behind the broader market as cruise ship operators underperform. Carnival (CCL 46.39, -2.31) has declined by 4.7% after being downgraded to "Under-Weight" from "Equal-Weight" at Morgan Stanley. Meanwhile, Chipotle Mexican Grill (CMG 410.24, -4.44) has extended its week-to-date loss to 2.0%. The stock has underperformed as investors respond to reports that the company is being sued by some of its employees regarding alleged unpaid wages. Conversely, retail names have rallied off their opening levels as Dow component Home Depot (HD 135.25, +1.02) erases a modest week-to-date loss. The broader sector has declined 0.1% this week, leading only energy (+1.0%; week-to-date: -0.4%) and health care (UNCH; week-to-date: -0.6%).

The U.S. Dollar Index (95.90, +0.25, +0.26%) floats near its session high as the euro and the yen lose ground to the greenback. The single currency has lost 0.4% against the buck (1.1158) while the dollar/yen pair trades higher by 1.0% (104.19).

11:05 am:

[BRIEFING.COM] The stock market floats off its best level of the day as the S&P 500 trades higher by 0.4%. The broader market has pulled back in recent action as investors continue to mull over the rate hike implications of the recently-released August employment report.

The economically-sensitive financial sector (+0.4%) trades in-line with the broader market as money center banks float off their opening lows. Bank of America (BAC 16.04, +0.06) fell 1.0% at the start of the session as investors dialed back rate hike expectations for coming months. The odds of a rate hike in September fell to 18.0% shortly after the release of the weaker-than-expected employment report. The report signaled that 151,000 nonfarm payrolls were added in August (Briefing.com consensus 180,000), but also contributed to a three month average of 232,000 nonfarm payroll additions. Fed funds futures have since erased their early losses, signaling the odds of a rate hike in September at 24.0%, which matches yesterday's reading.

The Treasury complex trades near session lows as yields rise through the curve. The yield on the 2-yr note has risen one basis point (0.80%) while the yield on the benchmark 10-yr note has increased by five basis points (1.61%). This steepening in the yield curve has likely helped bank shares climb off their opening lows.

10:45 am: [BRIEFING.COM]

Following the jobs report this morning, the dollar index dropped quickly to a new low for the day, sending commodities such as oil, gold, silver and copper futures highe

Oil, gold and silver popped to new highs for the day on this move

Commodities are largely holding gains this morning

Commodities, as measured by the Bloomberg Commodity Index, are now +1.15 at 82.9986

Oct crude oil is +2.2% at $44.11/barrel

Oct natural gas +0.4% at $2.80/MMBtu

Dec gold +0.3% at $1320.80/oz

Dec silver +1.5% at $19.24/oz

Dec copper +0.2% at $2.08/lb

Dollar index +0.3% at 95.93

10:00 am:

[BRIEFING.COM] The major averages trade near fresh session highs as the Dow Jones Industrial Average (+0.6%) trades neck-and-neck with the S&P 500 (+0.6%).

The leaderboard remains little changed with materials (+0.8%), consumer staples (+0.9%), energy (+0.9%), and utilities (+1.2%) leading the pack. Conversely, health care (+0.1%) has erased its opening loss.

Just released, the Factory Orders Report for July indicated an increase of 1.9%, which compares to the Briefing.com consensus of +2.0%. The June reading was revised to -1.8% (from -1.5%).

The U.S. Dollar Index (95.51, -0.15, -0.15%) floats modestly lower as the euro and the pound hold gains against the greenback. The euro has ticked higher by 0.1% against the dollar (1.1206) while sterling has gained 0.5% against the buck (1.3340). Separately, the dollar has lost 0.7% against the commodity-sensitive Canadian dollar (1.3007).

9:50 am:

[BRIEFING.COM] The stock market began the day on a higher note as the Dow Jones Industrial Average (+0.5%) and the S&P 500 (+0.5%) trade slightly ahead of the Nasdaq Composite (+0.4%).

Nine sectors trade in the green with energy (+1.0%) and utilities (+1.2%) leading to the upside. The remaining gainers show upticks between 0.3% (financials) and 0.9% (telecom services). Conversely, heavily-weighted health care (-0.1%) floats narrowly beneath its flat line.

The Dow Jones Transportation Average (+0.8%) demonstrates relative strength as shipping companies outperform. Kirby (KEX 53.08, +1.18) and Matson (MATX 42.62, +1.44) have gained 2.3% and 3.5%, respectively. The broader Transposition Index has climbed 2.0% this week, which compares to an uptick of 0.6% in the benchmark index.

In the consumer discretionary space (+0.4%), retail names underperform, evidenced by the 0.1% gain in the SPDR S&P Retail ETF (XRT 44.25, +0.04). In the group, lululemon athletica (LULU 69.02, -7.64) weighs after reporting in-line earnings and issuing guidance on the low end of expectations.

On the commodities front, WTI crude trades higher by 2.9% ($44.39/bbl; +$1.23) while gold trades higher by 0.8% ($1,327.70/ozt, +$10.60).

9:15 am: [BRIEFING.COM] S&P futures vs fair value: +5.00. Nasdaq futures vs fair value: +16.90.

The stock market is on track for a higher open with S&P 500 futures trading five points above fair value.

Index futures erased modest losses as investors assessed a weaker-than-expected reading of the Employment Situation Report for August. The report showed that 151,000 nonfarm payrolls (Briefing.com consensus 180k) were added while July's reading was revised higher to 275,000 (from 255,000). The August report also featured a cooler-than-expected average hourly earnings component, which indicated an increase of just 0.1% (Briefing.com consensus +0.2%).

Participants have dialed back rate hike expectations for the coming months while the U.S. Dollar Index (95.57, -0.08, -0.09%) carved out a new session low. The Treasury complex currently trades on a mixed note with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note has risen one basis points to 1.58% while the yield on the 2-yr note has slipped to 0.78% (-1 bps).

The fed funds futures market currently reflects the odds of a rate hike at the September meeting at 18.0%, slipping from yesterday's estimate of 24.0%. The odds of a rate hike at the December meeting remain close to a coin toss, showing an implied probability of 54.5%. This compares to yesterday's reading of 53.6%. On a side note, Richmond Fed President, and non-FOMC voter, Jeffrey Lacker will be the first member of the Federal Open Market Committee to speak following the employment reading. Mr. Lacker will offer remarks at 13:00 ET.

Today's data will be capped off with July Factory Orders (Briefing.com consensus +2.0%), which will be released at 10:00 ET.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: +4.30. Nasdaq futures vs fair value: +14.80.

U.S. equity futures float near session highs, responding to this morning's below-consensus employment reading. The S&P 500 futures trade four points above fair value.

Equity markets across Asia ended the week on a mostly higher note, but once again, trading ranges remained narrow as participants employed caution ahead of the release of the U.S. Employment Situation Report for August. The report showed that 151,000 nonfarm payrolls (Briefing.com consensus 180k) were added in August.

In economic data:

Japan's August Household Confidence 42.0 (expected 41.6; last 41.3) and Monetary Base +24.2% year-over-year (consensus 23.1%; last 24.7%)

South Korea's Q2 GDP +0.8% quarter-over-quarter (expected 0.7%; last 0.7%); +3.3% year-over-year (consensus 3.2%; last 3.2%)

---Equity Markets---

Japan's Nikkei settled just below its flat line, but gained 3.5% for the week. Industrials (-0.5%) and materials (-0.5%) lagged while utilities (+2.1%), financials (+1.3%), and communications (+0.9%) outperformed. Alps Electric, Minebea, JTEKT, TDK, and Komatsu lost between 1.5% and 4.8%. On the upside, J Front Retailing spiked 5.2%.

Hong Kong's Hang Seng gained 0.5%, extending its weekly advance to 1.6%. Financials outperformed with China Life Insurance, Ping An Insurance, Bank of East Asia, Hang Seng Bank, and Bank of China posting gains between 0.6% and 1.8%. Consumer names lagged with Belle International falling 1.7% and Li & Fung surrendering 1.5%.

China's Shanghai Composite added 0.1%, narrowing its weekly decline to 0.1%. Baotou Tomorrow Technology, China Television Media, and Shaanxi Yanchang Petroleum Chemical Engineering gained between 3.8% and 5.3%.

Major European indices trade in the green with UK's FTSE (+1.3%) pacing the advance. The euro (1.1221) and pound (1.3336) gained ground against the dollar following the below-consensus reading of the U.S. Employment Situation report for August (151k; Briefing.com consensus 180,000). European economic data was limited in terms of volume, but it is worth noting that UK's August Construction PMI (49.2; expected 46.1) and YouGov Business Confidence (109.7; previous 105.0) surpassed estimates, adding to the list of above-consensus data points received in the wake of the Brexit referendum.

In economic data:

Eurozone July PPI +0.1% month-over-month (expected 0.1%; last 0.8%); -2.8% year-over-year (consensus -2.9%; last -3.1%)

UK's August Construction PMI 49.2 (expected 46.1; last 45.9)

Italy's Q2 GDP 0.0% quarter-over-quarter, as expected (last 0.0%); +0.8% year-over-year (consensus 0.7%; last 0.8%)

Spain's Unemployment Change 14,400 (expected 15,000; last -84,000)

---Equity Markets---

Germany's DAX is higher by 0.5%. Countercyclical names like RWE, Merck, E.On, Fresenius, and Deutsche Telekom are up between 0.9% and 2.5%. Exporters and financials lag with Daimler, Volkswagen, and BMW down between 0.1% and 1.2% while Deutsche Bank trades flat.

France's CAC trades up 1.2% amid broad strength. Veolia Environnement, Accor, Essilor International, L'Oreal, Carrefour, and Kering show gains between 1.3% and 3.3%. Lafarge is the weakest performer, falling 1.2%.

UK's FTSE has climbed 1.3% with consumer and health care names pacing the move. Imperial Brands, British American Tobacco, Unilever, Hikma Pharmaceuticals, GlaxoSmithKline, and AstraZeneca are up between 1.6% and 3.2%. Homebuilders lag with Persimmon, Taylor Wimpey, and Barratt Developments down between 1.7% and 2.3%.

8:33 am: [BRIEFING.COM] S&P futures vs fair value: +1.50. Nasdaq futures vs fair value: +8.00.

Equity futures moved to session highs following the release of the Employment Situation Report for August. The S&P 500 futures trade two points above fair value.

August nonfarm payrolls came in at 151,000 while the Briefing.com consensus expected a reading of 180,000. The prior month's reading was revised higher to 275,000 (from 255,000). Nonfarm private payrolls added 126,000 while the consensus expected an increase of 175,000. The unemployment rate came in at 4.9% (Briefing.com consensus 4.8%).

Average hourly earnings increased 0.1% (Briefing.com consensus 0.2%). The average workweek was reported at 34.3, compared to the 34.5 called for by the consensus estimate.

Separately, the July trade balance showed a deficit of $39.50 billion while the Briefing.com consensus expected the deficit to come in at $43.0 billion. The previous month's deficit was revised to $44.7 billion from $44.5 billion.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -3.00. Nasdaq futures vs fair value: -1.10.

U.S. equity futures trade on a modestly lower note with the S&P 500 futures floating three points below fair value. European markets outperform as the U.K.'s FTSE (+1.1%) demonstrates relative strength. The index is benefiting from better-than-expected readings of U.K. Construction PMI (49.2; expected 46.1) for August and YouGov Business Confidence (109.7; previous 105.0).

On the home front, market participants look ahead to the release of the Employment Situation Report for August. The Briefing.com consensus expects Nonfarm Payrolls to increase by 180k while it also expects to see the unemployment rate slip to 4.8% (from 4.9%). The report has taken on added significance following recent hawkish commentary from Federal Reserve officials. For its part, WTI crude trades higher by 1.1% ($43.63/bbl; +$0.47), narrowing its week-to-date loss to 8.4%.

Treasuries trade on a modestly lower note with the long end of the curve demonstrating relative weakness. The yield on the 10-yr note has risen one basis point to 1.58%.

On the economic front, data will include the Employment Situation Report for August (Briefing.com consensus 180k) and the Trade Balance for July (Briefing.com consensus -$43.0 billion), which will each cross the wires at 8:30 ET. Separately, Factory Orders for July (Briefing.com consensus +2.0%) will be released at 10:00 ET.

In U.S. corporate news of note:

lululemon athletica (LULU 70.16, -6.50): -8.5% after reporting in-line quarterly results and issuing in-line guidance for Q3

Teva Pharmaceuticals (TEVA 51.50, +0.60): +1.2% following the stock being upgraded to "Outperform" at Oppenheimer

Smith & Wesson (SWHC 29.07, -0.51): -1.7% despite beating top-and bottom-line estimates for the quarter and raising its FY17 outlook above consensus

VeriFone (PAY 16.81, -3.29): -16.4% following the company reporting a mixed quarter and issuing below-consensus guidance for Q4

Reviewing overnight developments:

Asia-Pacific indices ended the week on a mixed note with Hong Kong's Hang Seng (+0.5%) leading China's Shanghai Composite (+0.1%) and Japan's Nikkei (UNCH).

In economic data:

Japan's August Household Confidence 42.0 (expected 41.6; last 41.3) and Monetary Base +24.2% year-over-year (consensus 23.1%; last 24.7%)

South Korea's Q2 GDP +0.8% quarter-over-quarter (expected 0.7%; last 0.7%); +3.3% year-over-year (consensus 3.2%; last 3.2%)

In news:

Trading ranges remained narrow as participants employed caution ahead of the release of the U.S. Employment Situation Report for August.

The report will be released at 8:30 ET and is expected to show the addition of 180,000 nonfarm payrolls, according to the Briefing.com consensus.

European indices trade on a positive note with the UK's FTSE (+1.1%) leading France's CAC (+0.9%), and Germany's DAX (+0.3%).

In economic data:

Eurozone July PPI +0.1% month-over-month (expected 0.1%; last 0.8%); -2.8% year-over-year (consensus -2.9%; last -3.1%)

UK's August Construction PMI 49.2 (expected 46.1; last 45.9)

Italy's Q2 GDP 0.0% quarter-over-quarter, as expected (last 0.0%); +0.8% year-over-year (consensus 0.7%; last 0.8%)

Spain's Unemployment Change 14,400 (expected 15,000; last -84,000)

In news:

The euro (1.1192) has slipped 0.1% against the dollar.

The greenback is expected to be on the move with the U.S. Employment Situation report for August (Briefing.com consensus 180,000) crossing the wires at 8:30 ET.

UK's August Construction PMI (49.2; expected 46.1) and YouGov Business Confidence (109.7; previous 105.0) surpassed estimates.

The two have been added to the list of above-consensus data points received in the wake of the Brexit referendum.

5:59 am: [BRIEFING.COM] S&P futures vs fair value: -1.80. Nasdaq futures vs fair value: +1.00.

5:59 am: [BRIEFING.COM] Nikkei...16926...-1.20...0.00%. Hang Seng...23267...+104.40...+0.50%.

5:59 am: [BRIEFING.COM] FTSE...6796.09...+50.10...+0.70%. DAX...10551.56...+17.30...+0.20%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com