Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

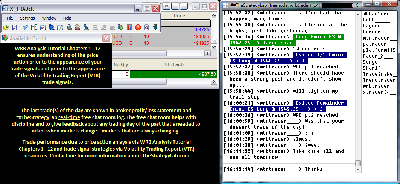

Attachment:

022516-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4937.50.png [ 93.88 KiB | Viewed 297 times ]

022516-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4937.50.png [ 93.88 KiB | Viewed 297 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$4937.50 dollars or +98.75 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $4937.50 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted

real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=153&t=2298 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=285&t=3049 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

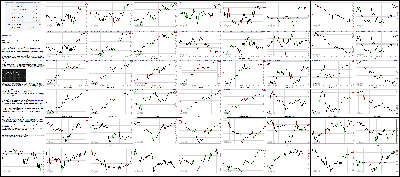

Attachment:

022516-Key-Price-Action-Markets.png [ 1.14 MiB | Viewed 301 times ]

022516-Key-Price-Action-Markets.png [ 1.14 MiB | Viewed 301 times ]

click on the above image to view today's price action of key markets 2:30 pm: [BRIEFING.COM] The stock market hovers below a fresh session high as the S&P 500 (+0.7%) trades behind the Dow Jones Industrial Average (+0.8%). The benchmark index trades one point off its high.

Energy (+0.1%) has moved into positive territory as consumer discretionary (+0.4%) follows the space. Meanwhile, the financial sector (+1.2%) has extended its lead.

The consumer discretionary space is being weighed down by large-cap components Disney (DIS 95.22, -0.21) and Lowe's (LOW 68.37, -0.25), which have tumbled 0.2% and 0.4%, respectively. Meanwhile, Dow component Nike (NKE 62.10, +1.69) outperforms that index and the broader discretionary sector. Nike has climbed 2.7% thus far today. Separately, L Brands (LB 85.36, +2.17) demonstrates relative strength after reporting above consensus results in Q4. However, the company lowered its earnings guidance for Q1.

WTI crude trades higher by 3.0% at $33.10/bbl ahead of the commodity's pit close at 14:30 ET.

2:00 pm:

[BRIEFING.COM] The Dow Jones Industrial Average (+0.9%) and the S&P 500 (+0.7%) trade at new session highs.

Nine of ten sectors have moved into positive territory as a rebound in oil lifts investor sentiment. At this juncture, WTI crude trades higher by 2.8% at $33.04/bbl. Materials (+1.0%) have rallied in recent action, following financials (+1.0%).

In the materials space, large-caps Dow Chemical (DOW 47.94, +0.75) and DuPont (DD 60.01, +0.99) show relative strength as the the two names climb 1.6% and 1.7%, respectively. Meanwhile, CF Industries (CF 33.23, +1.48) has rallied amid news that its CEO and Senior Vice President bought 33,000 shares valued at $1 million.

Safe haven gold and Treasuries have pulled back from their session highs. The yield on the 10-yr note is now lower by four basis points at 1.71% while gold trades lower by 0.3% at $1,235.90/ozt.

1:30 pm:

[BRIEFING.COM] The major U.S. indices have continued ticking higher, setting new intra-days highs in recent trade.

A look inside the Dow Jones Industrial Average shows that United Technologies (UTX 97.73, +4.12), Nike (NKE 61.74, +1.34), and Pfizer (PFE 30.56, +0.54) are outperforming. UTX shares are leading the Dow higher on potential deal hopes with Honeywell after an anti-trust representative from Honeywell in a CNBC interview expressed strong confidence that a potential merger could pass antitrust review.

Conversely, Chevron (CVX 84.05, -1.22) is the worst-performing Dow component as energy lags. The sector is today's worst performing industry, currently down 1.3%.

Extending yesterday's gains, the DJIA has now trimmed 2016's losses to 4.8%

1:05 pm:

[BRIEFING.COM] The major averages trade in mixed fashion at midday after recovering from larger losses. Today's early decline followed a corresponding tumble in the oil pit. Meanwhile, lax sector leadership from technology (+0.1%), a stronger than expected reading in the durable goods report, and a continued rebound in financials have influenced today's trade. At this juncture, the major averages trade on a mixed note with the Dow Jones Industrial (+0.3%) leading the S&P 500 (+0.2%) while the Nasdaq Composite trades lower by 0.2%.

Ahead of today's session oil remained pressured by mixed trade overseas and continued concerns regarding a supply glut. The energy component was able to bounce off its overnight low of $31.52/bbl ahead of the U.S. opening bell but notched a new low of $31.15/bbl during the morning session. At this juncture, WTI crude trades lower by 1.7% at $31.60/bbl.

As a result of the tumble in oil, independent oil and gas companies are seeing some of the largest losses in the energy sector (-1.8%). On that note, ConocoPhillips (COP 32.01, -0.95) has declined 2.9% thus far today. Conversely, Anadarko Petroleum (APC 37.04, +0.83) has jumped 2.3% after announcing that it closed or signed agreements to monetize approximately $1.3 billion of assets since the beginning of the year.

The economically-sensitive financial sector (+0.5%) and industrials (+0.3%) have received a boost from a stronger than expected reading in the January durable goods report (+4.9%; Briefing.com consensus +2.5%).

In the industrial space, aerospace and defense names outperform after the report showed that non-defense aircraft and parts orders surged 54.2% in January. Additionally, orders for defense aircraft and parts increased 84.8% over that same period, following a 66.8% decline in December. To that point, Lockheed Martin (LMT 219.79, 3.16) and United Technologies (UTX 97.31, +3.70) have gained 1.5% and 3.9%, respectively.

Meanwhile, the financial group has managed to remain near the top of the leaderboard throughout the day as real estate investment trusts demonstrate relative strength. Money center banks have ticked up in recent action while Morgan Stanley (MS 24.28, +0.57) has climbed 2.4%. As for the broader sector, it is down 3.6% in February and 0.1% for the week.

In the heavyweight technology space, large-cap constituents show relative weakness with Apple (AAPL 95.74, -0.35) and Microsoft (MSFT 51.18, -0.18) trading behind the broader sector and the overall market. Meanwhile, HP (HPQ 10.21, -0.58) remains pressured after disclosing a 11.6% decline in its revenue. The company has surrendered 5.6% despite reporting largely in-line results. To be fair though, the stock jumped 5.0% yesterday, ahead of its earnings report.

Meanwhile, utilities (+0.8%), consumer staples (+0.7%), telecom services (+0.6%), and health care (+0.4%) have topped the leaderboard throughout the day as investors continue favoring countercyclical sectors. On a similar note, the yield on the 10-yr note has notched a new session low in recent action. The benchmark yield is lower by seven-basis points at 1.69%. Also of note, gold has climbed 0.2% to trade at $1,241.00/ozt after recovering from a low of $1,228.80/ozt.

Today's economic data included weekly initial claims, Durable Orders for January, and the FHFA Housing Price Index for December.

Initial claims for the week ending February 20 increased 10,000 from the prior week to 272,000 (Briefing.com consensus 270,000).

Despite the increase, weekly claims remain in the lower half of the 250,000 to 300,000 range they have been in since July 2014. The four-week moving average dipped by 1,250 to 273,250. There were no special factors influencing the latest initial claims reading.

Continuing claims for the week ending February 13 decreased 19,000 to 2.253 million (Briefing.com consensus 2.268 mln). The four-week moving average for this series decreased 5,250 to 2.257 million.

Durable goods orders jumped 4.9% in January (Briefing.com consensus 2.0%) on the heels of an upwardly revised 4.6% decline (from -5.0%) in December. Excluding transportation, orders rose 1.8% (Briefing.com consensus +0.4%) after declining an upwardly revised 0.7% (from -1.0%) in December.

The January upturn followed on the back of month-over-month declines in both November and December. On a year-over-year basis, durable goods orders are up just 0.6%.

The durable goods orders data are notoriously volatile due to the influence of aircraft and defense spending. Both played a big part in driving the January turnaround. Orders for nondefense aircraft and parts surged 54.2% after a 29.1% decline in December while orders for defense aircraft and parts increased 84.8% following a 66.8% decline in December.

New order gains, however, were seen in a host of areas, including primary metals (+0.7%), fabricated metal products (+1.6%), and machinery (+6.9%).

The strength in January could simply be a rebound from a depressed base of order activity. We'll know more when the February report is released. For now, it can be seen as encouraging news, particularly since nondefense capital goods orders excluding aircraft -- a proxy for business spending -- increased 3.9%.

The one damper on things is that shipments of these goods, which factor into GDP computations, declined 0.4%.

The FHFA Housing Price Index for December rose 0.4% month-over-month after increasing a revised 0.6% (from 0.5%) in November.

12:30 pm:

[BRIEFING.COM] The major averages have ticked lower in recent action as the Nasdaq Composite (-0.1%) remains behind the S&P 500 (+0.2%). The benchmark index trades six points below its session high.

At this juncture, seven sectors trade in the green with consumer discretionary (UNCH) flirting with its flat line. Interestingly enough countercyclical utilities (+0.8%) and consumer staples (+0.7%) remain ahead of the other sectors.

The financial sector (+0.5%) has shown relative strength throughout today's session as real estate investment trusts demonstrate relative strength. Meanwhile, Morgan Stanley (MS 24.34, +0.63) has climbed 2.7%, outperforming the sector. JPMorgan Chase (JPM 56.60, +0.46) and Wells Fargo (WFC 47.96, +0.35) have climbed in recent action, as the two names advance 0.7% and 0.8%, respectively. Including today's trade, the heavyweight sector remains lower by 3.6% for the month and largely unchanged for the week.

On the commodities front, WTI crude trades lower by 1.8% at $31.59/bbl while gold is up 0.1% at $1,239.90/ozt.

12:00 pm:

[BRIEFING.COM] The major averages have ticked higher in recent action with the S&P 500 (+0.3%) trading nine points off its session low.

At this juncture, eight sectors trade in the green with financials (+0.6%) and countercyclical utilities (+0.6%) leading consumer staples (+0.5%). Meanwhile, heavily-weighted technology (+0.2%) has returned to positive territory.

In the tech space, HP (HPQ 10.21, -0.58) remains pressured after disclosing a 11.6% decline in its revenue. The company has surrendered 5.6% despite reporting largely in-line results. To be fair though, the stock jumped 5.0% ahead of its earnings report. Meanwhile, Salesforce.com (CRM 67.86, +5.40) has climbed 8.6% after reporting in-line results for Q4. Large-cap constituents continue to show spotty performances, with Apple (AAPL 95.81, -0.29) and Microsoft (MSFT 51.40, +0.04) trading behind the broader sector.

11:30 am:

[BRIEFING.COM] The broader market has followed oil lower in recent action as the S&P 500 (+0.1%) trades six points above its lowest level of the day.

Commodity-sensitive energy (-1.5%) remains pressured by the falling oil price. Currently, WTI crude trades lower by 2.4% at $31.40/bbl.

In the energy space, independent oil and gas companies are seeing the largest losses with ConocoPhillips (COP 32.29, -0.66) declining 2.0%. Conversely, Anadarko Petroleum (APC 37.54, +1.34) has jumped 3.7% after announcing that it closed or signed agreements to monetize approximately $1.3 billion of assets since the beginning of the year. Meanwhile, Dow components Chevron (CVX 84.19, -1.07) and Exxon Mobil (XOM 80.35, -1.21) show losses of 1.3% apiece.

Gold now flirts with its flat line, currently trading at $1,238.50/ozt (UNCH) after recovering from a 0.8% loss before today's session.

11:00 am:

[BRIEFING.COM] The major U.S. indices have climbed off their session lows as the Nasdaq Composite (UNCH) flirts with its flat line. The S&P 500 (+0.1%) trades seven points off its session low.

The heavily-weighted technology sector (+0.2%) has rallied in recent action. The space now joins financials (+0.4%) and industrials (+0.1%) as the only three cyclical sectors in the green.

In the industrial space, aerospace and defense names have shown relative strength after the durable goods report showed that non-defense aircraft and parts surged 54.2% in January. Additionally, orders for defense aircraft and parts increased 84.8% over that same period, following a 66.8% decline in December. To that point, Boeing (BA 116.28, 0.66) and United Technologies (UTX 95.22, +1.61) have gained 0.7% and 1.7%, respectively.

Oil has marked a new session low trading lower by 2.7% at $31.27/bbl.

The yield on the 10-yr note trades lower by five-basis points at 1.70%.

10:40 am: [BRIEFING.COM]

Natural gas futures sold off to a new LoD following this morning's EIA storage data, which showed a smaller-than-expected draw

Apr nat gas remains near today's low and is now -4.4% to $1.70/MMBtu

Oil is trading lower today with the front-month WTI Apr contract showing a 2% decline at $31.49/barrel

The dollar index is flat, which isn't helping move precious metals today

Apr gold is now -0.1% at $1237.80/oz, while Mar silver is -1% at $15.15/oz

Apr copper is -0.9% at $2.08/lb

10:00 am:

[BRIEFING.COM] The major averages continues to trade beneath their opening highs with the tech-heavy Nasdaq (-0.3%) trading behind the S&P 500 (UNCH). The benchmark index trades eight points off its best level.

The technology space (-0.5%) continues to show relative weakness with large-caps weighing on the broader sector. To that point, Apple (AAPL 95.65, -0.45), Facebook (FB 106.04, -0.84), and Alphabet (GOOGL 716.71, -4.19) have slipped between 0.5% and 0.7%.

Meanwhile, utilities (+0.6%) and telecom services (+0.6%) have been bid higher in a safe haven trade. On that note, the sectors trade broadly ahead of the remaining groups on a year-to-date basis with respective advances of 8.7% and 9.2%.

9:50 am:

[BRIEFING.COM] The major averages began their session on a mixed note as the S&P 500 (UNCH) outpaces the Nasdaq Composite (+0.2%).

Six of ten sectors have opened in the green while countercyclical telecom services (+0.7%) and utilities (+0.6%) lead. Meanwhile, commodity-sensitive energy (-1.0%) and materials (-0.4%) round out the board. The remaining sectors show performances between -0.1% (technology) +0.4% (consumer staples).

On the commodities front, WTI crude trades lower by 1.3% at $31.74/bbl while gold trades down 0.2% at $1,236.50/ozt.

The Treasury complex has seen increased buying interest as the yield on the 10-yr note falls four-basis points to 1.71%.

The U.S. Dollar Index (97.57, +0.11) has tumbled in recent action as the safe haven yen sees more interest. The dollar/yen pair trades at 112.73 off its session low (112.91).

9:19 am: [BRIEFING.COM] S&P futures vs fair value: +6.80. Nasdaq futures vs fair value: +14.00.

The stock market is on track for a modestly higher open with the S&P 500 futures trading seven points above fair value. Futures have been helped by better than expected expected economic data with January durable goods orders increasing 4.9% (Briefing.com consensus +2.0%) while excluding transportation, durable orders increased 1.8% (Briefing.com consensus +0.4%). These better than expected results followed sharp losses last month when the headline figure decreased 4.6% and core orders fell 0.7%. For its part WTI crude has climbed off its low to trade down 0.3% at $32.04/bbl.

In specific company news, Best Buy (BBY 31.86, +0.39) has climbed 1.2% in pre-market action as the company's bottom-line beat and a 22.0% increase in the stock's dividend outweighs below-consensus guidance. Meanwhile, HP (HPQ 10.19, -0.62) has surrendered 5.8% after the company reported a larger than expected revenue drop.

On the currency front, the yen has weekend against the dollar in recent trade with the dollar/yen pair currently trading at 112.89 (+0.6%). This has helped boost the U.S. Dollar Index (97.60, +0.15).

Meanwhile, the FHFA Housing Price Index for December rose 0.4% month-over-month after increasing a revised 0.6% (from 0.5%) in November.

8:57 am: [BRIEFING.COM] S&P futures vs fair value: +4.80. Nasdaq futures vs fair value: +9.80.

The S&P 500 futures trade five points above fair value.

Equity markets across Asia ended the Thursday session on a mixed note with Chinese stocks resuming their plunging act while Japan's Nikkei (+1.4%) outperformed. Bank of Japan Governor Haruhiko Kuroda appeared before the Japanese parliament once again and his remarks suggested he may be an early adopter of virtual reality technology, considering Mr. Kuroda stated that "Negative rates will surely improve people's lives" and that "spending is resilient." Recall that last week's GDP report pointed to a 0.8% quarter-over-quarter decline in private consumption during the fourth quarter (expected -0.6%) and that various reports have pointed to a surge in demand for safes in Japan.

In economic data:

Japan's Foreign Bonds Buying +JPY1.97 trillion (previous -JPY1.32 trillion)

South Korea's February Consumer Confidence fell to 98 from 100

Australia's Q4 Private New Capital Expenditure +0.8% quarter-over-quarter (expected -3.0%; last -8.4%) and Q4 Building Capital Expenditure +1.2% (expected -4.7%; last -8.3%)

---Equity Markets---

Japan's Nikkei climbed 1.4% with all ten sectors posting gains. Utilities (+4.9%) and financials (+2.9%) led the way while industrials (+0.7%) lagged. Chubu Electric Power, Nippon Light Metal Holdings, Panasonic, DOWA Holdings, TEPCO, Credit Saison, and Sumitomo Realty & Development gained between 3.7% and 6.9%. On the downside, Okuma, Komatsu, Hitachi Construction Machinery, and Fanuc lost between 1.3% and 4.6%.

Hong Kong's Hang Seng lost 1.6% amid broad weakness. Tingyi tumbled 5.5% while Cheung Kong Property Holdings, China Life Insurance, Ping An Insurance, Henderson Land, and New World Development lost between 2.4% and 3.8%. AIA Group was the lone advancer, adding 0.9%.

China's Shanghai Composite tumbled 6.4% with China Shipbuilding diving 10.0% while Bank of China, Agricultural Bank of China, China State Construction Engineering, and Hainan Airlines lost between 3.8% and 5.9%.

Major European indices trade higher across the board with Spain's IBEX (+2.8%) pacing the region-wide rally. In addition to European stocks, the pound (+0.2%) has climbed this morning. The cable trades near 1.3954. Meanwhile, the euro rose to 1.1040 against the dollar before falling to 1.1017 (UNCH).

Investors received a boatload of economic data:

Eurozone January CPI -1.4% month-over-month, as expected; +0.3% year-over-year (consensus 0.4%; last 0.4%). January Core CPI -1.7% month-over-month; +1.0% year-over-year, as expected. Separately, M3 Money Supply +5.0% year-over-year (consensus 4.7%; last 4.7%) and Private Sector Loans +1.4% year-over-year (expected 1.5%; last 1.4%)

Germany's March GfK Consumer Climate ticked up to 9.5 from 9.4 (expected 9.3)

UK's preliminary Q4 GDP +0.5% quarter-over-quarter, as expected; +1.9% year-over-year, as expected. Separately, Q4 Business Investment -2.1% quarter-over-quarter (expected -0.9%; last 1.2%)

Italy's December Retail Sales -0.1% month-over-month (expected 0.5%; last 0.2%); +0.6% year-over-year (last -0.2%). Separately, February Business Confidence 102.0 (expected 102.7; previous 103.0) and Consumer Confidence 114.5 (consensus 117.9; last 118.6)

Spain's Q4 GDP +0.8% quarter-over-quarter, as expected; +3.5% year-over-year, as expected. Separately, January PPI -2.5% (previous -1.7%)

Swiss Q4 Industrial Orders -7.7% (last -6.7%)

---Equity Markets---

Germany's DAX has climbed 1.8% amid broad strength. However, the advance has a countercyclical tilt with the likes of Deutsche Post, Fresenius, Merck, E.On, and RWE leading the rally. The five names hold gains between 2.7% and 5.0% while Deutsche Bank trades up 2.3% and BMW, Daimler, and Volkswagen show gains between 0.9% and 1.7%.

France's CAC is higher by 2.4% with all but two names in the green. Technip has surged 13.3% in reaction to better-than-feared results while financials Societe Generale and BNP Paribas trade near the top of the leaderboard with gains close to 3.7% apiece. On the downside, Peugeot has given up 2.6%

UK's FTSE trades up 2.5% with financials among the leaders. RSA Insurnace, Lloyds Banking, RBS, Prudential, and Barclays are up between 3.6% and 12.8%. Homebuilders lag with Persimmon and Taylor Wimpey both up near 0.4%.

Spain's IBEX is higher by 2.8% with Mediaset, Repsol, Telefonica, and ACS Construction in the lead with gains between 3.4% and 6.7%. Financials have also had a good showing. Santander, Bankinter, BBVA, and Caixabank are up between 2.0% and 3.5%.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: +5.50. Nasdaq futures vs fair value: +12.50.

The S&P 500 futures trade six points above fair value.

The latest weekly initial jobless claims count totaled 272,000 while the Briefing.com consensus expected a reading of 270,000. Today's tally compared to 262,000 in the prior week. As for continuing claims, they fell to 2.253 million from 2.272 million (revised from 2.273 million).

Separately, January durable goods orders increased 4.9% while the Briefing.com consensus expected an increase of 2.0%. This comes after the prior month's revised reading of -4.6% from -5.0%. Excluding transportation, durable orders increased 1.8% (Briefing.com consensus +0.4%) to follow the prior month's revised reading -0.7% (from -1.0%).

8:05 am: [BRIEFING.COM] S&P futures vs fair value: +4.30. Nasdaq futures vs fair value: +9.90.

U.S. equity futures trade higher with the S&P 500 futures trading four points above fair value.

Overnight, China's Shanghai Composite surrendered 6.4% amid liquidity concerns and worries of economic cooling. Meanwhile, European bourses have been able to drift higher so far in their session as volatile oil trade continues. At this juncture, WTI crude trades lower by 0.5% at $31.98/bbl. Separately, ahead of today's session St. Louis Fed President and FOMC voting member James Bullard echoed statements from last week that drew attention to "declining market-based inflation expectations" as a possible reason for putting off further tightening.

On the economic front, data will include the 8:30 ET release of weekly initial claims (Briefing.com consensus 270k) and Durable Orders for January (Briefing.com consensus +2.0%). Meanwhile, the FHFA Housing Price Index for December will cross the wires at 9:00 ET.

The yield on the 10-yr note has fallen overnight with its yield currently lower by two-basis points at 1.73%.

In U.S. corporate news of note:

Salesforce.com (CRM 68.55, +6.03): +9.6% after reporting in-line results in Q4 and issuing estimates for Q1 that match analyst expectations

Best Buy (BBY 30.50, -0.97): -3.1% following the company issuing guidance below-consensus despite a bottom-line beat in Q4

Restoration Hardware (RH 39.83, -12.09): -23.3% after the company issued earnings and revenue guidance well beneath analyst estimates

HP (HPQ 10.50, -0.32): -3.0% after Mizuho reaffirmed its neutral rating on the stock on in-line results in its earnings reporting

Reviewing overnight developments:

Asian markets ended their session on a mixed note as China's Shanghai Composite plummeted 6.4% and Hong Kong's Hang Seng surrendered 1.6%. Meanwhile, Japan's Nikkei advanced 1.4%.

In economic data:

Japan's Foreign Bonds Buying +JPY1.97 trillion (previous -JPY1.32 trillion)

South Korea's February Consumer Confidence fell to 98 from 100

Australia's Q4 Private New Capital Expenditure +0.8% quarter-over-quarter (expected -3.0%; last -8.4%) and Q4 Building Capital Expenditure +1.2% (expected -4.7%; last -8.3%)

In news:

Bank of Japan Governor Haruhiko Kuroda appeared before the Japanese parliament once again and his remarks suggested he may be an early adopter of virtual reality technology, considering Mr. Kuroda stated that "Negative rates will surely improve people's lives" and that "spending is resilient."

European indices trade higher across the board with the U.K.'s FTSE +2.3%, France's CAC +2.3%, and Germany's DAX +1.6%. Separately, Spain's IBEX outpaces their gains with a climb of 2.5%.

Investors received a boatload of economic data:

Eurozone January CPI -1.4% month-over-month, as expected; +0.3% year-over-year (consensus 0.4%; last 0.4%). January Core CPI -1.7% month-over-month; +1.0% year-over-year, as expected. Separately, M3 Money Supply +5.0% year-over-year (consensus 4.7%; last 4.7%) and Private Sector Loans +1.4% year-over-year (expected 1.5%; last 1.4%)

Germany's March GfK Consumer Climate ticked up to 9.5 from 9.4 (expected 9.3)

UK's preliminary Q4 GDP +0.5% quarter-over-quarter, as expected; +1.9% year-over-year, as expected. Separately, Q4 Business Investment -2.1% quarter-over-quarter (expected -0.9%; last 1.2%)

Italy's December Retail Sales -0.1% month-over-month (expected 0.5%; last 0.2%); +0.6% year-over-year (last -0.2%). Separately, February Business Confidence 102.0 (expected 102.7; previous 103.0) and Consumer Confidence 114.5 (consensus 117.9; last 118.6)

Spain's Q4 GDP +0.8% quarter-over-quarter, as expected; +3.5% year-over-year, as expected. Separately, January PPI -2.5% (previous -1.7%)

Swiss Q4 Industrial Orders -7.7% (last -6.7%)

5:56 am: [BRIEFING.COM] S&P futures vs fair value: +4.30. Nasdaq futures vs fair value: +10.50.

5:55 am: [BRIEFING.COM] Nikkei...16140...+224.60...+1.40%. Hang Seng...18889...-303.70...-1.60%.

5:55 am: [BRIEFING.COM] FTSE...5986.12...+118.90...+2.00%. DAX...9251.06...+83.30...+0.90%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com