Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

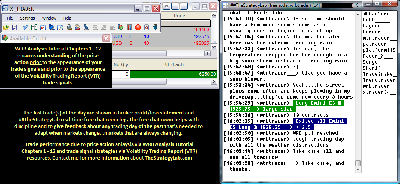

Attachment:

022416-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6250.00.png [ 94.22 KiB | Viewed 285 times ]

022416-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+6250.00.png [ 94.22 KiB | Viewed 285 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$6250.00 dollars or +125.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $6250.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted

real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=153&t=2297 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=285&t=3049 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

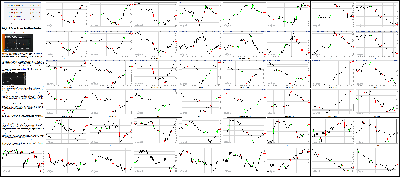

Attachment:

022416-Key-Price-Action-Markets.png [ 1.26 MiB | Viewed 268 times ]

022416-Key-Price-Action-Markets.png [ 1.26 MiB | Viewed 268 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market ended the Wednesday affair on a positive note as the major indices managed to recover from steep morning losses. Today's trade saw equity markets moving in tandem with oil while heavily-weighted sectors like financials (-0.2%) and industrials (+0.1%) recovered from respective morning losses of 2.2% and 1.8%. The Nasdaq Composite (+0.9%) ended its session ahead of the S&P 500 (+0.4) and the Dow Jones Industrial Average (+0.3%).

This morning oil conceded to heavy selling pressure as a bearish reading from the weekly API inventory report and concerns over the effectiveness of a supply cap weighed on the commodity. The energy component found room to rally after the Department of Energy reported a gasoline inventory draw of 2.236 million barrels compared to the forecast 1.033 million barrel draw. Additionally, largely in-line results regarding a crude oil build (3.502 mln barrels vs est. 3.427 mln) bolstered the commodity. WTI crude rallied off its session low of $30.70/bbl to end its day higher by 1.3% at $32.21/bbl.

As a result of this rally in crude oil, the commodity-sensitive energy space (+0.9%) was able to move from laggard to leader. Independent oil and gas companies saw the largest rebound but Chevron (CVX 85.27, +0.36) and Exxon Mobil (81.52, +0.29) were able to end their day with gains of 0.4% apiece. Separately, Chesapeake Energy (CHK 2.69, +0.50) surged 22.8% after reporting above consensus bottom-line results and announcing plans to divest $700 million in assets by the end of the second quarter.

The early underperformance of heavily-weighted sectors contributed to the sharp opening losses as technology (+0.9%) and consumer discretionary (+0.6%) weighed on the benchmark index. Meanwhile, financials (-0.2%) and industrials (+0.1%) underperformed the broader market throughout the day.

In the financial sector, money center banks demonstrated relative weakness after JPMorgan Chase (JPM 56.14, +0.02) admitted Tuesday that it increased its loan loss reserves for its oil, gas, and mining exposures. The broader financial sector was to recover from a 2.2% loss to end its day down 0.1%.

In the heavyweight technology space, top-weighted constituent Apple (AAPL 96.10, +1.41) gained 1.5% while the high-beta chipmakers outperformed. The PHLX Semiconductor Index climbed 1.4% today as SanDisk (SNDK 69.90, +3.29) led the index. Separately, HP (HPQ 10.82, +0.51) jumped 5.0% ahead of its earnings report after today's closing bell.

Retail names boosted the consumer discretionary space after TJX (TJX 74.24, +1.55) reported an earnings beat while Target (TGT 76.94, +2.95) impressed investors with above-consensus guidance.

The Dow Jones Transportation Average (-0.5%) underperformed with components Avis Budget (CAR 22.04, -7.95) and Matson (MATX 38.39, -1.84) displaying relative weakness after disappointing investors with their earnings reports and guidance. Meanwhile, industrial large-caps General Electric (GE 28.96, -0.26) and Boeing (BA 115.59, -1.31) also underperformed.

Today's trade saw a steady retreat from safe haven assets as the Treasury complex slid to its lows. The yield on the 10-yr note ended higher by two-basis points at 1.74%. On a related note, the U.S. Dollar Index (97.47, -0.02) climbed back to its flat line as the safe haven yen pulled back from its session high (111.07). The dollar/yen pair ended at 111.91. The euro also fell from its high (1.1044), pressuring the euro/dollar pair to 1.1012 (-0.1%).

Today's participation fell beneath the recent average with fewer than 1.012 billion shares changing hands on the NYSE floor.

Today's economic data was limited to the weekly MBA Mortgage Index and the January New Home Sales Report:

The weekly MBA Mortgage Index showed a seasonally adjusted decrease of 4.3% in mortgage applications.

Sales of new single-family houses in January ran at a seasonally adjusted annual rate of 494,000 (Briefing.com consensus 523,000)

That was 9.2% below the sales rate in December and new home sales in January were down 5.2% year-over-year.

Weather can't really be blamed as the culprit for the drop in sales for a few reasons. First, the Northeast, which was struck by a blizzard late in the month, saw sales increase 3.4%. Secondly, the West, which did not have to contend with blizzard conditions, saw a huge 32.1% month-over-month decline in new home sales. Separately, sales were down 5.9% in the Midwest and up 1.8% in the South.

Pricing can't be thought of as the culprit either. The median sales price of $278,800 was down 5.8% from the prior month and down 4.5% year-over-year.

This January downturn, then, has the appearance at first blush of simply being the result of a drop off in demand. As a reminder, new home sales are counted when the contract is signed versus existing home sales which are counted when the sale is closed.

At the sales pace seen in January, the inventory of new homes for sale stretched to a 5.8-months supply from 5.1 months in December. That is the highest inventory level since September 2015.

Separately, St. Louis President and Federal Open Market Committee voting member James Bullard will speak at 19:00 ET.

Tomorrow's economic data will include the 8:30 ET release of weekly initial claims (Briefing.com consensus 270k) and Durable Orders for January (Briefing.com consensus +2.0%). Meanwhile, the FHFA Housing Price Index for December will cross the wires at 9:00 ET.

Russell 2000: -10.1% YTD

Nasdaq -9.3% YTD

S&P 500 -5.6% YTD

Dow Jones -5.4% YTD

3:45 pm: [BRIEFING.COM]

Oil prices have fully recovered today weakness and is now at today's high

In floor trading, Apr crude finished +1.3% at $32.21/barrel

Apr natural gas rose one cent to $1.84/MMBtu

Precious metals reversed today's rally

However, Apr gold did end with a gain, closing +1.4% at $1239.20/oz, while Mar silver ended +0.5% at $15.30/oz

Apr gold is now at $1230.00/oz

3:00 pm:

[BRIEFING.COM] The major indices hover near their best levels of the day with the Nasdaq Composite (+0.3%) leading the S&P 500 (UNCH). The benchmark index trades three points off its high (1923.50).

Five sectors remain in the red with financials (-0.7%) and industrials (-0.3%) showing the sharpest losses. Meanwhile, telecom services (+0.6%) and materials (+0.5%) are jockeying for the lead.

Today's trade saw a steady retreat from safe haven assets as the Treasury complex slides to its lows. Currently, the yield on the 2-yr note is the only domestic yield remaining in negative territory at 0.74% (-1bps). Meanwhile, the yield on the 10-yr note is higher by one-basis point at 1.73%. On a related note, the U.S. Dollar Index (97.47, -0.02) has climbed back to its flat line as the safe haven yen pulled back from its session high (111.07). The dollar/yen pair trades at 111.68. The euro also fell from its high (1.1044), pressuring the euro/dollar pair to 1.1012 (-0.1%).

On the commodities front, WTI crude was able to end in positive territory with a gain of 1.3% at $32.21/bbl. Separately, gold has pared its gain to 0.7% at $1,230.40/ozt.

2:30 pm:

[BRIEFING.COM] Recent action saw the Nasdaq Composite (+0.2%) and S&P 500 (+0.1%) turn positive after a steady charge off their morning lows. The benchmark index has rallied 31 points off today's lowest level.

Six sectors currently trade in the green with telecom services (+0.6%), materials (+0.5%) and technology (+0.4%) showing the largest gains.

The heavily-weighted health care space (UNCH) has received a boost in recent action as biotechnology outperforms. The iShares Nasdaq Biotechnology ETF (IBB 257.76, +0.34) has climbed 2.8% from its lowest point of the day.

Elsewhere, automotive names Ford (F 11.99, -0.43) and General Motors (GM 28.69, -0.68) have ticked off their session lows but remain lower by 3.4% and 2.4%, respectively. Ford received a downgrade at Credit Suisse from "Neutral" to "Underperform" while Morgan Stanley resumed coverage of General Motors with an "Underweight" designation. Separately, consumer discretionary(+0.2%) large-cap Starbucks (SBUX 58.12, -0.34) has tumbled 0.6% today.

The yield on the 10-yr note now trades unchanged at 1.72%.

2:00 pm:

[BRIEFING.COM] The stock market has inched higher since the last update with the S&P 500 (-0.6%) trading 21 points above its session low.

The energy space (-0.2%) has slipped in recent action while the materials sector (UNCH) treads near its flat line.

In the heavyweight technology space (-0.5%) the high-beta chipmakers outperform, evidenced by a 0.4% gain in the PHLX Semiconductor Index. The sub-group is being helped by Cypress Semiconductor (CY 7.74, +0.11), which has climbed 1.4% after the company received a "Buy" rating at Craig Hallum. The stock has gained 21.1% since February 11th. Separately, HP (HPQ 10.69, +0.38) has jumped 3.7% ahead of its earnings report after today's closing bell.

On the commodities front, WTI crude trades at $31.88/bbl (UNCH) while gold has maintained most of its advance at $1,239.10/ozt (+1.3%).

1:35 pm:

[BRIEFING.COM] The major U.S. indices continue their charge higher off this morning's lows.

A look inside the Dow Jones Industrial Average shows that General Electric (GE 28.52, -0.70), Boeing (BA 114.39, -2.51), and Caterpillar (CAT 64.46, -1.32) are underperforming as industrials lag.

Conversely, United Technologies (UTX 93.66, +2.06) is the best-performing Dow component after Honeywell (HON 102.38, -1.26) issued an official statement, confirming that over the past year it has engaged in discussions with United Technologies regarding a possible business combination. Honeywell disagreed with United Technologies' commentary, saying that it does not see the regulatory process as a material obstacle to a transaction. Honeywell contends that a combination would benefit their customers and enhance its ability to offer a more comprehensive and compelling suite of technologies to serve their needs.

For the week, the DJIA is now down 0.5%.

1:05 pm:

[BRIEFING.COM] The major averages have rallied off their session lows as the stock market recovers from early selling pressure that was sparked by a selloff in oil and poorer than expected economic data. Meanwhile, a recovery in the energy component has helped provide fodder to a larger rebound effort while the heavily-weighted consumer discretionary (-0.7%) and technology (-0.6%) spaces helped lift the broader market. Currently, the Dow Jones Industrial Average (-0.7%) trades in line with the S&P 500 (-0.7%) and behind the Nasdaq (-0.6%).

Oil remained pressured this morning as a bearish reading from the API inventory report and commentary from Saudi Arabia's oil minister weighed on the commodity overnight. However, WTI crude was able to rally off its low after the Department of Energy's weekly inventory report showed a draw of 2.236 million barrels from the gasoline inventory compared to the forecast 1.033 million barrel draw. Additionally, largely in-line results regarding a crude oil build (3.502 mln barrels vs est. 3.427 mln) bolstered the commodity. At this juncture, WTI crude trades higher by 0.8% at $32.12/bbl after trading as low as $30.70/bbl.

As a result, the energy space (+0.2) has managed to climb up the leaderboard as oil and gas companies rallied. To that point, Dow component Chevron (CVX 84.74, -0.17) has moved off of its low (82.90). Separately, Chesapeake Energy (CHK 2.68, +0.49) has gained 22.4% after reporting a bottom-line beat on in-line revenue. The company also announced $700 million in asset divestitures that will close by the end of the second quarter of 2016.

The economically-sensitive financial space (-1.5%) shows the worst performance of the day while industrials (-1.0%) follow. On the flipside, countercyclical telecom services (+0.1%) and energy (+0.2%) are the only sectors in the green.

In financials, money center banks continue to demonstrate relative weakness after JPMorgan Chase's (JPM 55.10, -1.02) admission Tuesday that it is increasing its reserves for its oil, gas, and mining exposures.

The Dow Jones Transportation Average (-1.4%) underperforms with components Avis Budget (CAR 22.55, -7.44) and Matson (MATX 35.99, -4.24) showing relative weakness after disappointing investors with their earnings reports and guidance. Meanwhile, industrial large-caps Boeing (BA 114.07, -2.83) and Caterpillar (CAT 64.46, -1.32) also underperform.

Retail names have helped boost the consumer discretionary space (-0.7%) as TJX (TJX 74.41, +1.72) and Target (TGT 75.96, +1.98) climb 2.4% and 2.7%, respectively. TJX is benefiting from top-and bottom line beats while Target impressed investors with above-consensus guidance.

The Treasury complex has slipped from its high as equities rebounded. Currently, the yield on the 10-yr note remains lower by two basis points at 1.71%.

Today's economic data was limited to the weekly MBA Mortgage Index and the January New Home Sales Report:

The weekly MBA Mortgage Index showed a seasonally adjusted decrease of 4.3% in mortgage applications.

Sales of new single-family houses in January ran at a seasonally adjusted annual rate of 494,000 (Briefing.com consensus 523,000)

That was 9.2% below the sales rate in December and new home sales in January were down 5.2% year-over-year.

Weather can't really be blamed as the culprit for the drop in sales for a few reasons. First, the Northeast, which was struck by a blizzard late in the month, saw sales increase 3.4%. Secondly, the West, which did not have to contend with blizzard conditions, saw a huge 32.1% month-over-month decline in new home sales. Separately, sales were down 5.9% in the Midwest and up 1.8% in the South.

Pricing can't be thought of as the culprit either. The median sales price of $278,800 was down 5.8% from the prior month and down 4.5% year-over-year.

This January downturn, then, has the appearance at first blush of simply being the result of a drop off in demand. As a reminder, new home sales are counted when the contract is signed versus existing home sales which are counted when the sale is closed.

At the sales pace seen in January, the inventory of new homes for sale stretched to a 5.8-months supply from 5.1 months in December. That is the highest inventory level since September 2015.

12:30 pm:

[BRIEFING.COM] The major averages hover below intraday highs as the S&P 500 (-0.8%) trades 16 points off its worst level of the day.

The move higher in equities followed a rally in oil. WTI crude currently trades higher by 0.1% at $31.89/bbl. As a result, commodity-sensitive energy (-0.2%) and materials (-0.1%) have pared most of their losses.

In the consumer discretionary space (-0.8%), retail names have shown relative strength with TJX (TJX 74.41, +1.72) climbing 2.4% after reporting a top and bottom-line beat in its Q4 earnings report. The company issued lower earnings estimates for Q1 and full year 2017, but added to its stock buyback and raised its dividend 24.0% to $0.26 per share. Meanwhile, Target (TGT 76.08, +2.09) has rallied off its low after reporting a bottom-line miss on in-line revenue while guiding earnings estimates higher for full year 2017. Conversely, Lowe's (LOW 67.27, -0.63) underperforms despite reporting above-consensus bottom-line results and issuing 2017 earning guidance above analyst estimates.

The Treasury complex has retreated from its highs with the 10-yr yield narrowing its loss to two basis points at 1.70%.

12:00 pm:

[BRIEFING.COM] The major averages have climbed in recent action as the S&P 500 (-0.8%) trades nine points off its session low.

Consumer discretionary (-0.8%) and technology (0.8%) have inched higher as industrials (-1.1%) demonstrate relative weakness.

The Dow Jones Transportation Average (-1.7%) has returned to bear market designation considering it once again shows a decline of more than 20.0% from its high (9214.77). The index is being led lower by Avis Budget (CAR 22.98, -7.01), which has plunged 23.5% after missing Q4 sales estimates and guiding full year 2016 earnings below consensus. Meanwhile, Matson (MATX 35.77, -4.46) has plummeted 11.1% after the company reported top and bottom-line misses and estimating that first quarter income will be 25.0% lower than the first quarter of 2015.

In the broader industrial sector, Boeing (BA 113.49, -3.40) and Caterpillar (CAT 64.44, -1.34) underperform the market while fellow large-cap United Technologies (UTX 92.99, +1.38) outperforms.

On the commodities front, WTI crude continues to move off its low, but is still down 0.4% at $31.73/bbl.

11:30 am:

[BRIEFING.COM] The stock market has traded in sideways fashion since our last update and the tech-heavy Nasdaq (-1.3%) now trades in-line with the S&P 500 (-1.3%). The benchmark index trades six points off its low.

The economically-sensitive financial sector (-1.9%) continues to trail the remaining groups as energy (-1.5%) follows the heavyweight group.

Money center banks continue to demonstrate relative weakness after JPMorgan Chase's (JPM 54.91, -1.21) admission Tuesday that it is increasing its reserves for its oil, gas, and mining exposures. Morgan Stanley (MS 22.83, -0.88) also underperforms, declining 3.7%. Separately, State Street (STT 53.02, -2.61) trades behind the broader sector and market.

The Treasury complex continues to see increased buying interest as the yield on the 10-yr note trades lower by five-basis points at 1.67%.

11:00 am:

[BRIEFING.COM] The major averages have moved off fresh session lows as a similar move takes place in crude oil. The S&P 500 (-1.2%) trades six points off its worst level of the day.

The energy space (-1.2%) was helped by a better than feared weekly inventory report from the Energy Information Association. This morning's report showed a draw of 2.236 million barrels from the gasoline inventory compared to the forecasted 1.033 million barrel draw. However, the report also showed a build of 3.502 million barrels of crude oil, compared to the estimated 3.427 million barrel build. At this juncture, WTI crude has lifted off its session low of $30.70/bbl to trade at $31.02/bbl (-2.7%).

As a result, Dow component Chevron (CVX 83.98, -0.93) has moved off of its low (82.90). Meanwhile, Chesapeake Energy (CHK 2.59, +0.40) has gained 18.5% after reporting a bottom-line beat on in-line revenue. The company also announced $700 million in asset divestitures that will close by the end of the second quarter of 2016.

On the currency front, the yen hovers near its session high of 111.19 (+0.8%) against the dollar. Elsewhere in safe-haven assets, gold has climbed 2.1% to $1,248.40/ozt.

10:45 am: [BRIEFING.COM]

Oil prices sold off overnight following the weekly API storage data, falling over 3%

This morning, following the EIA's own weekly storage data, which showed a nice draw in fuel products, such as gasoline and distillated, oil prices got a boost

Apr crude oil is still in negative territory, but is recover some. Crude is now -2% at $31.22/barrel

Nat gas has been sitting near the flat line today and is currently unchanged at $1.78/MMBtu

Gold is up again with precious metals showing nice gains

Apr gold is currently +2.1% at $1248.60/oz, while Mar silver is +1.8% at $15.52/oz

10:00 am:

[BRIEFING.COM] The S&P 500 (-1.4%) has extended its opening decline after a disappointing reading in the February Markit PMI Services report, which fell to 49.8 from a downwardly revised 52.3 (from 53.7). Normally, this report is not seen as a market mover, but there was a clear response today given the increased anxiety among participants and the fact that the number dropped below 50.0, signifying contraction in activities. Notably, the report indicated that the deterioration in data suggests "a significant risk of the U.S. economy falling into contraction during the first quarter".

Just released, New Home Sales in January hit an annualized rate of 494,000, which was below the unrevised December rate of 544,000, and less than the 523,000 that was expected by the Briefing.com consensus.

Separately, the Dollar Index has surrendered its overnight gain in recent action as the yen rallies 0.6% to 111.41 against the dollar.

9:40 am:

[BRIEFING.COM] As expected, the major averages began their day in negative territory with the tech-heavy Nasdaq (-1.3%) leading the S&P 500 (-1.2%) to the downside.

Nine of ten sectors have opened in the red with energy (-1.9%) and financials (-1.6%) leading the losses. Utilities (+0.3%) and the remaining countercyclicals outperform with losses between 0.3% (telecom services) and 1.0% (health care). The remaining decliners show losses between 1.4% (consumer discretionary) and 1.1% (technology).

On the commodities front, WTI crude trades lower by 3.7% at $30.68/bbl while gold has climbed 1.8% at $1,244.80/ozt.

The Treasury complex trades higher with the yield on the 10-yr note falling five-basis points to 1.68%.

9:14 am: [BRIEFING.COM] S&P futures vs fair value: -18.00. Nasdaq futures vs fair value: -51.00.

The stock market is on track for a lower open as S&P 500 futures trade 18 points below fair value.

Overnight, futures traded in line-line with the direction of oil as investors ruminated over commentary from Saudi Arabia that halted speculation regarding future supply cuts. Meanwhile, the API weekly inventory report showed an increase of 7.1 million barrels of crude oil, compared to the expected 3.0 million barrel build. Adding to the uncertain environment was commentary from Fed Vice Chair Stanley Fischer who stated that it was too early to assess the impact of recent market volatility on the FOMC's March meeting.

On the corporate front, Avis Budget (CAR 25.39, -4.60) has plunged 15.3% in pre-market action after issuing below-consensus guidance for full year 2016. The disappointing guidance overshadowed a bottom-line beat on light revenue. Separately, Lowe's (LOW 67.90, +0.00) has managed to climb off its pre-market low after reporting in-line earnings.

In commodities, WTI crude trades lower by 3.4% at $30.78/bbl. Elsewhere, gold trades higher by 1.8% at $1,244.10/ozt.

The Treasury complex trades broadly higher with the yield on the 10-yr note lower by three-basis points at 1.69% while the yield on the 2-yr note is also lower by three-basis points at 0.72%. In the overseas bond market, the yield on Japan's 10-yr note fell five-basis points to -0.05%. The German bund yield sits at just 0.15% after starting the year at 0.63%.

8:59 am: [BRIEFING.COM] S&P futures vs fair value: -17.50. Nasdaq futures vs fair value: -49.90. The S&P 500 futures trade 18 points below fair value.

Equity markets in the Asia-Pacific region ended Wednesday on a mostly lower note with yen strength remaining one of the main storylines as the dollar/yen pair returned into the neighborhood of its low from two weeks ago. Meanwhile, Bank of Japan Governor Haruhiko Kuroda appeared before the Japanese parliament once again, saying the central bank does not target foreign exchange rates or stock prices. Mr. Kuroda tried to downplay the recent yen strength by saying that other major currencies have also rallied against the dollar, but conveniently ignored the fact that the yen has been showing even more strength against other currencies. For instance, the pound/yen rate has dropped to 155.30 in overnight action after starting the month near 172.50 (-10.0%).

In economic data:

Japan's Corporate Services Price Index +0.2% year-over-year (expected 0.3%; previous 0.4%) and Leading Index ticked up to 102.1 from 102.0 (expected 102.0)

Hong Kong's Q4 GDP +0.2% quarter-over-quarter, as expected (prior 0.9%); +1.9% year-over-year (consensus 2.0%; last 2.3%)

Australia's Q4 Construction Work Done -3.6% (expected -2.0%; last -1.8%) and Q4 Wage Price Index +0.5% quarter-over-quarter (expected 0.6%; last 0.6%); +2.2% year-over-year (consensus 2.3%; last 2.3%)

Singapore's Q4 GDP +6.2% quarter-over-quarter (expected 4.0%; last 5.7%); +1.8% year-over-year, as expected (previous 2.0%)

---Equity Markets---

Japan's Nikkei was down more than 1.0% in the early going, narrowing its loss to 0.9% by the close. The financial sector (+0.3%) ended in the green while the remaining nine groups posted losses with industrials (-1.4%), materials (-1.0%), and technology (-1.0%) leading the slide. Yokogawa Electric, Toshiba, SUMCO, Mitsui Chemicals, Unitika, Alps Electric, TDK, Minebea, Kawasaki Heavy Industries, and Mitsubishi lost between 2.9% and 6.5%. On the upside, Credit Saison, Fukuoka Financial Group, and Mitsubishi Financial added between 1.0% and 1.7%.

Hong Kong's Hang Seng lost 1.2% with most components ending in the red. Tingyi plunged 6.4% in reaction to disappointing results while Li & Fung, CNOOC, China Life Insurance, Petrochina, and Sands China fell between 2.1% and 3.1%. On the upside, Sino Land added 0.2%.

China's Shanghai Composite rose 0.9%. China Shipbuilding, Metallurgical Corp of China, and Ningbo Marine posted gains between 2.5% and 4.4%.

Major European indices have spent the early portion of the trading day in a steady retreat with Spain's IBEX (-2.8%) pacing the region-wide slide amid relative weakness in financials. Elsewhere, the British pound has dropped below 1.40 against the dollar for the first time since 2009 with fears of a Brexit driving the weakness. Sterling trades at 1.3936 against the dollar at this time, representing a 3.3% decline so far this week.

In economic data:

UK's February CBI Distributive Trades Survey fell to 10 from 16 (expected 12) and BBA Mortgage Approvals hit 47,500 (expected 45,200; previous 43,700)

France's February Consumer Confidence fell to 95 from 97 (expected 97)

Swiss January Consumption Indicator ticked up to 1.66 from 1.61)

Italy's December Industrial New Orders 1.5% year-over-year (last 12.1%) and Industrial Sales -3.0% year-over-year (last 0.8%)

---Equity Markets---

UK's FTSE is lower by 1.4% with miners and consumer names leading the retreat. Anglo American, BHP Billiton, Glencore, Sports Direct, Burberry, and GKN are down between 4.5% and 9.1%. Homebuilders Barratt Developments and Persimmon outperform with respective gains of 1.5% and 1.9%.

France's CAC trades down 2.1% amid broad weakness. ArcelorMittal, Renault, Solvay are down between 4.1% and 4.7% while financials Credit Agricole, Societe Generale, and BNP Paribas hold losses between 1.2% and 3.1%.

Germany's DAX has tumbled 2.3% with Volkswagen, Daimler, and BMW showing losses between 4.0% and 5.0%. Financials also lag with Deutsche Bank and Commerzbank both down near 3.5%.

Spain's IBEX has surrendered 2.8% with Banco Sabadell, Banco Popular, Bankia, Bankinter, BBVA, and Caixabank down between 2.1% and 3.6%.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: -18.00. Nasdaq futures vs fair value: -50.50.

The S&P 500 futures trade 18 points below fair value.

On the corporate front, shares of Lowe's (LOW 65.50, -2.40) have ticked lower in pre-market action despite the company's positive earnings report. Lowe's reported bottom-line results in-line with analyst expectations while issuing higher than expected earnings guidance for full year 2017. Separately, Target (TGT 73.19, 0.80) has slipped 1.1% after investors focus on the bottom-line in Q4 compared to the above consensus earnings guidance for FY17.

WTI crude trades lower by 3.2% at $30.84/bbl while risk-averse gold has gained 1.0% to trade at $1,234.90/ozt.

The U.S. Dollar Index (97.78, +0.30) climbed higher overnight but has since retreated as the dollar/yen pair trades lower by 0.2% at 111.83. Elsewhere, the euro has weakened against the dollar to trade at 1.0983 (-0.3%).

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -18.20. Nasdaq futures vs fair value: -51.90.

U.S. equity futures hover above overnight lows with the S&P 500 futures trading 18 points below fair value. Overnight, futures traded lower with oil as a bearish API inventory report and commentary from influential oil ministers weighed on the commodity. At this juncture, WTI crude trades lower by 3.1% at $30.88/bbl. Investors look ahead to the Department of Energy's Inventory report at 10:30 ET.

On the economic front, the weekly MBA Mortgage Index was reported at 7:00 ET, showing a seasonally adjusted decrease of 4.3% in mortgage applications. Meanwhile, the January New Home Sales Report (Briefing.com 523k) will cross at 10:00 ET. Separately, Richmond Fed President Jeffrey Lacker is due to speak at 8:00 ET with St. Louis Fed President James Bullard speaking after the closing bell at 19:00 ET.

The Treasury complex trades higher with the yield on the 10-yr note lower by three-basis points at 1.70%.

In U.S. corporate news of note:

Lowes (LOW 65.75, -2.15): -3.2% despite reporting in-line earnings results on larger than expected revenue while issuing better than expected guidance for FY17

Chesapeake Energy (2.07, -0.12): -5.5% after reporting a bottom-line beat on in-line revenue. The struggling energy company also announced approximately $700 million in divestitures by the end of the second quarter.

First Solar (FSLR 63.25, +1.46): +2.4% following top and bottom-line figures above analyst estimates on its Q4 earnings report

Reviewing overnight developments:

Asian-Pacific indices ended on a mixed note with Hong Kong's Hang Seng -1.2% and Japan's Nikkei -1.0% while China's Shanghai Composite rose 0.9%.

In economic data:

Japan's Corporate Services Price Index +0.2% year-over-year (expected 0.3%; previous 0.4%) and Leading Index ticked up to 102.1 from 102.0 (expected 102.0)

Hong Kong's Q4 GDP +0.2% quarter-over-quarter, as expected (prior 0.9%); +1.9% year-over-year (consensus 2.0%; last 2.3%)

Australia's Q4 Construction Work Done -3.6% (expected -2.0%; last -1.8%) and Q4 Wage Price Index +0.5% quarter-over-quarter (expected 0.6%; last 0.6%); +2.2% year-over-year (consensus 2.3%; last 2.3%)

Singapore's Q4 GDP +6.2% quarter-over-quarter (expected 4.0%; last 5.7%); +1.8% year-over-year, as expected (previous 2.0%)

In news:

Bank of Japan Governor Haruhiko Kuroda appeared before the Japanese parliament once again, saying the central bank does not target foreign exchange rates or stock prices.

Meanwhile, the yen rallied against the dollar to 111.80 (-0.2%) while the pound yen/rate dropped to 155.30 in overnight action after starting the month near 172.50 (-10.0%).

European indices trade broadly lower with Germany's DAX -2.3%, France's CAC -2.0%. and the U.K.'s FTSE -1.4%. Meanwhile, Spain's IBEX (-2.7%) paces the region-wide slide.

In economic data:

UK's February CBI Distributive Trades Survey fell to 10 from 16 (expected 12) and BBA Mortgage Approvals hit 47,500 (expected 45,200; previous 43,700)

France's February Consumer Confidence fell to 95 from 97 (expected 97)

Swiss January Consumption Indicator ticked up to 1.66 from 1.61)

Italy's December Industrial New Orders 1.5% year-over-year (last 12.1%) and Industrial Sales -3.0% year-over-year (last 0.8%)

In news:

The British pound has dropped below 1.40 against the dollar for the first time since 2009 with fears of a Brexit driving the weakness.

6:06 am: [BRIEFING.COM] S&P futures vs fair value: -13.80. Nasdaq futures vs fair value: -36.30.

6:06 am: [BRIEFING.COM] Nikkei...15916...-136.30...-0.90%. Hang Seng...19192.5...-222.30...-1.20%.

6:06 am: [BRIEFING.COM] FTSE...5876.15...-86.20...-1.50%. DAX...9191.82...-225.00...-2.40%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com