Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

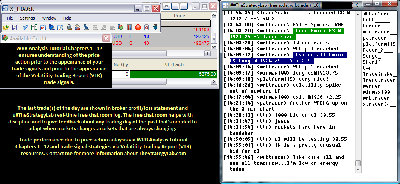

Attachment:

021716-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5375.00.png [ 94.01 KiB | Viewed 309 times ]

021716-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5375.00.png [ 94.01 KiB | Viewed 309 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$5375.00 dollars or +107.50 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $5375.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted

real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=153&t=2292 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=285&t=3049 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

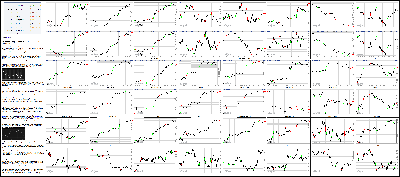

Attachment:

021716-Key-Price-Action-Markets.png [ 1.26 MiB | Viewed 327 times ]

021716-Key-Price-Action-Markets.png [ 1.26 MiB | Viewed 327 times ]

click on the above image to view today's price action of key markets 4:15 pm: [BRIEFING.COM] The major averages ended their Wednesday affair on a higher note, rallying throughout the day alongside crude oil. Adding to today's positive sentiment was sustained sector leadership from the heavily-weighted technology (+2.3%) and consumer discretionary spaces (+2.1%), dovish commentary from Boston Fed President Rosengren. The Nasdaq Composite (+2.2%) ended in the lead while the S&P 500 (+1.7%) and the Dow Jones Industrial Average (+1.6%) followed.

Throughout today's session oil climbed on speculation that OPEC ministers would convince Iran to cooperate on a production freeze. However, while Iran voiced support for market stabilization efforts, the country has yet to agree to take part in yesterday's proposed production freeze. Nevertheless, WTI crude ended its day higher by 5.5% at $30.65/bbl.

In central bank news, the minutes from the FOMC's January meeting echoed a dovish tone that was voiced yesterday by Boston Fed President and FOMC voter Eric Rosengren. The minutes reported concerns over a potential drag on the U.S. economy from larger-than-expected slowdowns in China and other emerging markets. On that note, Fed President Rosengren argued for a more gradual approach to hiking rates in response to headwinds from abroad.

Energy (+2.9%) and technology led the other sectors while materials (+2.0%) and consumer discretionary jockeyed one another. On the flipside, countercyclical utilities (-0.2%), telecom services (+0.3%),consumer staples (+1.0%), and health care (+1.3%) rounded out the board.

The commodity-sensitive energy space topped the leaderboard thanks to the rebound in crude oil. Energy giant Chevron (CVX 88.31, +3.50) climbed 4.1% to outperform the broader sector. Conversely, natural gas company Devon Energy (DVN 20.33, -0.93) surrendered 4.4% after reporting below-consensus revenue in Q4 and announcing a 75.0% dividend cut.

Separately, Salesforce.com (CRM 63.49, +3.77) showed relative strength in the technology sector. The company outperformed after Mizuho issued bullish commentary on the company when previewing Salesforce.com's Q4 earnings (February 24th). Large-cap Facebook (FB 105.19, +3.58) was able to recover from early relative weakness while Apple (AAPL 98.12, +1.48) ended its session behind the broader sector.

Priceline (PCLN 1,235.56, +124.88) outperformed in the consumer discretionary space after reporting above-consensus earnings prior to today's open. Meanwhile, fellow sector heavyweight Disney (DIS 95.50, +2.59) climbed 2.8%. The discretionary group has climbed 4.6% over the last two days, but remains lower by 1.7% for the month.

In the health care space, Johnson & Johnson (JNJ 102.50, +0.18) and Pfizer (PFE 29.63, -0.18) weighed on the broader sector while biotechnology outperformed today, evidenced by a 2.9% increase in the iShares Nasdaq Biotechnology ETF (IBB 266.32, +7.60).

Treasury yields traded higher throughout today's session as the rally in equities continued, but an afternoon bid in the Treasury complex pressured yields from their highs. The yield on the 10-yr note ended the day higher by four basis points at 1.81%.

Today's participation was true to the recent average with more than 1.2 billion shares changing hands at the NYSE floor.

Today's economic data included the weekly MBA Mortgage Index, January PPI, January Housing Starts, January Building Permits, the January Industrial Production Report, Capacity Utilization, and thee FOMC's January Minutes.

MBA Mortgage Index was reported at 7:00 ET, showing a seasonally adjusted increase of 8.2% in mortgage applications.

The Producer Price Index (PPI) for final demand increased 0.1% (Briefing.com consensus -0.2%) in January after an unrevised 0.2% decline in December.

Excluding food and energy, final demand prices increased 0.4% (Briefing.com consensus 0.0%) on top of an upwardly revised 0.2% increase (from 0.1%) in December.

A 0.5% increase in prices for final demand services drove the uptick in the PPI for final demand. That overrode a 0.7% decrease in prices for final demand goods, which flowed from a 5.0% decline for final demand energy goods.

With the January reading, total PPI is down 0.2% year-over-year on an unadjusted basis while core PPI is up 0.6%. There is still much room for improvement, yet January's readings would seem to have PPI headed in the right direction in the Fed's mind.

Housing starts declined 3.8% in January to an annualized rate of 1.099 million units (Briefing.com consensus 1.171 mln), as single-family starts dropped 3.9% and multi-units starts fell 3.7%.

Single-family starts in the South were flat in January; otherwise, there were declines in all other regions with the Northeast down 14.1%, the West down 10.0%, and the Midwest down 3.8%.

The number of housing units under construction at the end of the period stood at 978,000 versus 976,000 at the end of December and the fourth quarter average of 962,000. This should be a slight positive as it relates to first quarter GDP computations.

Building permits slipped 0.2% to an annualized rate of 1.202 million (Briefing.com consensus 1.200 mln), with single-family permits down 1.6% and multi-unit permits up 2.1%.

There was an outsized 55.4% decline in total permits for the Northeast region, which was likely due to the expiration of tax credits for building multi-family properties in New York City.

That decline was offset by a 26.5% increase for total permits in the Midwest and a 24.5% increase for total permits in the West.

Industrial production increased a robust 0.9% in January and could have bee a little bit stronger if not for a big winter storm late in the month, according to the Federal Reserve.

The January reading was much stronger than the Briefing.com consensus estimate of +0.3% and the downwardly revised 0.7% decline (from -0.4%) in December. On a year-over-year basis, total industrial production is still down 0.7%.

Following unseasonably warm weather in December, proper winter temperatures arrived in January and cranked up the demand for heating. That demand fueled a 5.4% increase in the index for utilities, which interrupted a string of three straight monthly declines. A 0.5% increase in manufacturing output was another big driver of the headline surprise. That increase was a byproduct of near 0.5% increases for both nondurables and durables.

The durables increase was powered by a 2.8% increase for motor vehicles and parts. On a related note, total motor vehicle assemblies increased 4.0% month-over-month to a seasonally adjusted annual rate of 12.11 million units. Mining output was surprisingly unchanged in January as substantial decreases for oil and gas well drilling and servicing, for coal mining, and for nonmetallic mineral mining were offset by increases for oil and gas extraction and for metal ore mining. That was the first time since August 2015 that mining output has not declined.

Separately, the total industry capacity utilization rate increased to 77.1% in January from a downwardly revised 76.4% (from 76.5%) in December. The bulk of that improvement stemmed from capacity utilization for utilities increasing to 77.5% from 73.6%.

St. Louis Fed President and FOMC voting member James Bullard will be speaking at 18:00 ET.

Tomorrow's economic data will be limited to the weekly initial claims (Briefing.com consensus 274k) and the February Philadelphia Fed Survey (Briefing.com consensus -2.9) with both reports set to cross the wires at 8:30 ET.

Russell 2000 -11.0% YTD

Nasdaq -9.5% YTD

S&P 500 -5.7% YTD

Dow Jones -5.6% YTD

3:40 pm: [BRIEFING.COM]

Energy futures rallied today, some extending recent gains

Mar crude oil futures rallied today, closing the session +5.5% at $30.65/barrel

Mar heating oil futures rallied as well, rising +7% to $1.10/gallon, while Mar RBOB gasoline rose 3.1% to $1.00/gallon

In other energy, Mar natural gas gained some steam, closing today's session +2.1% at $1.94/MMBtu

Metals climbed higher today as well, but showed much smaller gains

Apr gold rose 0.3% to $1211.20/oz, while Mar silver rose 0.3% to $15.38/oz

Copper gained three cents to end at $2.08/lb.

3:05 pm:

[BRIEFING.COM]

As the stock market enters its final hour of trade, the major averages have slipped from their session highs. Currently, the S&P 500 (+1.6%) trades five points below its best level of the day.

In the financials space (+1.1%) the group has underperformed the broader market for the bulk of today's trading, but the sector sits comfortably in the green. Insurance companies have had the best showing today with MetLife (MET 39.27, +1.25) displaying relative strength. Meanwhile, money center banks are mixed after their recent rally from monthly lows. JPMorgan Chase (JPM 58.52, +0.17) has only ticked higher by 0.3% while Bank of America (BAC 12.59, +0.34) has climbed 2.8%. Since the beginning of the month the two names have declined 1.6% and 11.0%, respectively. At its lowest point Bank of America was down as much as 22.3% in February.

On the commodities front, WTI crude ended its pit session higher by 5.5% at $30.65/bbl.

2:25 pm:

[BRIEFING.COM] The Federal Reserve has released its latest policy minutes, providing some insight into the January meeting.

Most notably, the minutes indicated that the FOMC was more cautious to downside risks in January. Specifically, the committee was concerned about the potential drag on the U.S. economy from the broader effects of a greater-than-expected slowdown in China and other emerging markets. Additionally, the committee discussed altering the path of the target range path for the fed funds rate, but agreed that this might be premature. Instead the committee chose to closely monitor global economic developments and to continue to assess their implications for the labor market and inflation.

Stocks have marked a new session high since the release with the S&P 500 extending its gain to 1.8%. Meanwhile, Treasuries ticked to new lows with the yield on the 10-yr note now higher by six basis points at 1.84%.

In currencies, the U.S. Dollar Index (96.92, +0.07) remains within a striking distance of the unchanged level.

2:00 pm:

[BRIEFING.COM] The major indices have drifted lower in recent action with the S&P 500 (+1.5%) now trading three points off its best level of the day.

The energy sector (+2.7%) has pulled away from its session high as oil trades likewise. Currently, WTI crude trades higher by 5.6% at $30.66/bbl after trading as high as $31.13/bbl.

In the health care space (+0.9%), heavyweight components Johnson & Johnson (JNJ 102.55, +0.23) and Pfizer (PFE 29.71, -0.10) weigh on the broader sector as both giants underperform. Meanwhile, biotechnology has outperformed today, evidenced by a 2.2% increase in the iShares Nasdaq Biotechnology ETF (IBB 264.50, +5.78). Interesting to note, biotechnology is enjoying a rally from oversold conditions after having plummeted 21.8% to begin the year while the broader health care space has only surrendered 8.2%.

Treasury yields have ticked lower with the yield on the 10-yr note now up six basis points at 1.83%.

The FOMC minutes from the January meeting will be released at 14:00 ET and the release will be summarized in our next update.

1:35 pm:

[BRIEFING.COM] The major U.S. indices are resting just under their intra-day highs as stocks maintain today's strong gains.

A look inside the Dow Jones Industrial Averages shows that Caterpillar (CAT 67.75, +2.54), Chevron (CVX 87.94, +3.13), and Walt Disney (DIS 95.99, +3.08) are outperforming amid broad market strength.

Conversely, McDonald's (MCD 118.34, -0.84) is the worst-performing Dow component as shares pull back following's yesterday gains.

With today's extension of recent gains, the DJIA has trimmed February's losses to 0.15%

1:00 pm:

[BRIEFING.COM] The major averages sport solid gains at midday as a rally in crude oil and dovish remarks from Boston Fed President Rosengren (an FOMC voter) have helped lift the broader market. Additionally, continued sector leadership from the consumer discretionary space (+2.0%) and technology (+2.2%), as well as better than expected PPI data has helped maintain today's advance. Currently, the Nasdaq Composite (+2.1%) leads the S&P 500 (+1.6%) and the Dow Jones Industrial Average (+1.5%).

After yesterday's closing bell, Fed President Rosengren stated that the Fed can be "fairly patient" with respect to raising the fed funds rate. Furthermore, President Rosengren believes that monetary policy normalization "should be unhurried" if inflation is slower to return to target. These comments came ahead of this afternoon's release of the FOMC minutes from the January meeting.

Overnight oil remained in focus while OPEC oil ministers traveled to Iran to attempt to garner the country's cooperation for a production freeze. At this juncture, Iran has voiced support for market stabilization efforts but has not agreed to take part in any production freeze. Currently, WTI crude trades higher by 6.4% at $30.91/bbl.

Energy (+3.3%) leads the other sectors while technology follows the group. Meanwhile, materials (+2.0%) and consumer discretionary round out the top of the leaderboard. On the flipside, countercyclical utilities (-0.3%), telecom services (+0.5%) and consumer staples (+1.1%) trail.

The energy group has been the main beneficiary in today's rebound in crude oil, with energy giant Chevron (CVX 87.96, +3.15) climbing 3.7%. Conversely, natural gas company Devon Energy (DVN 19.69, -1.57) has surrendered 7.4% after cutting its dividend by 75.0% and reporting below-consensus revenue in Q4.

Elsewhere, Salesforce.com (CRM 62.99, +3.27) has shown relative strength in the technology sector, after Mizuho issued some bullish commentary on the company when previewing Salesforce.com's Q4 earnings. The company is scheduled to report on February 24th after the close. Meanwhile large-cap Apple (AAPL 97.70, +1.06) has shown relative weakness, but is still up 1.1% today.

In the consumer discretionary space, large-cap Priceline (PCLN 1,224.53, +113.85) outperforms after reporting above-consensus earnings prior to today's opening bell. Fellow heavyweight Disney (DIS 95.98, +3.07) has gained 3.3%. Overall, the discretionary sector continues to rebound from its February loss. The group remains lower by 1.8% for the month despite climbing 4.5% over the last two days.

Freeport-McMoRan (FCX 7.38, +1.01) has climbed 16.0% in the materials group after Icahn Associates Holdings disclosed that the firm increased its position in the company from 100 million shares to 104 million shares.

Meanwhile, T-Mobile (TMUS 36.94, +0.49) outperforms in the telecom services space after reporting above-consensus earnings on revenue that matched expectations.

Today's economic data included the weekly MBA Mortgage Index, January PPI, January Housing Starts, January Building Permits, the January Industrial Production Report, and Capacity Utilization. Finally, the FOMC minutes from the January 27th meeting will be released at 14:00 ET.

MBA Mortgage Index was reported at 7:00 ET, showing a seasonally adjusted increase of 8.2% in mortgage applications.

The Producer Price Index (PPI) for final demand increased 0.1% (Briefing.com consensus -0.2%) in January after an unrevised 0.2% decline in December.

Excluding food and energy, final demand prices increased 0.4% (Briefing.com consensus 0.0%) on top of an upwardly revised 0.2% increase (from 0.1%) in December.

A 0.5% increase in prices for final demand services drove the uptick in the PPI for final demand. That overrode a 0.7% decrease in prices for final demand goods, which flowed from a 5.0% decline for final demand energy goods.

With the January reading, total PPI is down 0.2% year-over-year on an unadjusted basis while core PPI is up 0.6%. There is still much room for improvement, yet January's readings would seem to have PPI headed in the right direction in the Fed's mind.

Housing starts declined 3.8% in January to an annualized rate of 1.099 million units (Briefing.com consensus 1.171 mln), as single-family starts dropped 3.9% and multi-units starts fell 3.7%.

Single-family starts in the South were flat in January; otherwise, there were declines in all other regions with the Northeast down 14.1%, the West down 10.0%, and the Midwest down 3.8%.

The number of housing units under construction at the end of the period stood at 978,000 versus 976,000 at the end of December and the fourth quarter average of 962,000. This should be a slight positive as it relates to first quarter GDP computations.

Building permits slipped 0.2% to an annualized rate of 1.202 million (Briefing.com consensus 1.200 mln), with single-family permits down 1.6% and multi-unit permits up 2.1%.

There was an outsized 55.4% decline in total permits for the Northeast region, which was likely due to the expiration of tax credits for building multi-family properties in New York City.

That decline was offset by a 26.5% increase for total permits in the Midwest and a 24.5% increase for total permits in the West.

Industrial production increased a robust 0.9% in January and could have bee a little bit stronger if not for a big winter storm late in the month, according to the Federal Reserve.

The January reading was much stronger than the Briefing.com consensus estimate of +0.3% and the downwardly revised 0.7% decline (from -0.4%) in December. On a year-over-year basis, total industrial production is still down 0.7%.

Following unseasonably warm weather in December, proper winter temperatures arrived in January and cranked up the demand for heating. That demand fueled a 5.4% increase in the index for utilities, which interrupted a string of three straight monthly declines. A 0.5% increase in manufacturing output was another big driver of the headline surprise. That increase was a byproduct of near 0.5% increases for both nondurables and durables.

The durables increase was powered by a 2.8% increase for motor vehicles and parts. On a related note, total motor vehicle assemblies increased 4.0% month-over-month to a seasonally adjusted annual rate of 12.11 million units. Mining output was surprisingly unchanged in January as substantial decreases for oil and gas well drilling and servicing, for coal mining, and for nonmetallic mineral mining were offset by increases for oil and gas extraction and for metal ore mining. That was the first time since August 2015 that mining output has not declined.

Separately, the total industry capacity utilization rate increased to 77.1% in January from a downwardly revised 76.4% (from 76.5%) in December. The bulk of that improvement stemmed from capacity utilization for utilities increasing to 77.5% from 73.6%.

12:30 pm:

[BRIEFING.COM] The stock market has inched up to a fresh session high with the S&P 500 trading up 1.6%.

The technology sector (+2.1%) has passed the consumer discretionary space (+1.9%) on the leaderboard while energy (+3.1%) remains well ahead.

In the heavyweight technology space, Salesforce.com (CRM 63.11, +3.39) shows relative strength after Mizuho issue some bullish commentary on the company when previewing Salesforce.com's Q4 earnings. The company is scheduled to report on February 24th after the close. Meanwhile large-cap Apple (AAPL 97.37, +0.73) has shown relative weakness. Separately, high-beta chipmakers have shown relative strength today with the PHLX Semiconductor Index up 2.2%.

On the commodities front, WTI crude has climbed 6.5% today to trade at $30.90/bbl.

12:00 pm:

[BRIEFING.COM] The major indices continue to drift beneath their best levels of the day with the S&P 500 (+1.4%) and the Dow Jones Industrial Averages (+1.3%) three points and 11 points below their best levels of the session, respectively.

The energy group (+2.8%) has been the main beneficiary in today's rebound in crude oil with energy giant Chevron (CVX 87.68, +2.87) climbing 3.4%. Elsewhere in the space natural gas company Devon Energy (DVN 19.85, -1.41) has surrendered 6.6% after reporting Q4 revenue below analyst expectations. Currently, WTI crude is higher by 5.9% at $30.75/bbl.

11:30 am:

[BRIEFING.COM] The stock market drifts below its session high with the S&P 500 (+1.5%) trading behind the Nasdaq Composite (+1.8%). The benchmark index currently trades two points beneath its session high.

The technology sector (+1.7%) has climbed in recent action and now trades neck-in-neck with the consumer discretionary sector (+1.7%).

In the consumer discretionary space, large-cap Priceline (PCLN 1,228.86, +118.18) outperforms after reporting above-consensus earnings prior to today's opening bell. Elsewhere, fellow heavyweight Disney (DIS 95.59, +2.68) has gained 3.0%. Overall, the discretionary sector continues to rebound from its February loss. The group remains lower by 1.9% for the month despite climbing 4.3% over the last two days.

Treasury yields have notched new session highs in recent action as the rally in equities wears on. The yield on the 10-yr note is higher by six basis points at 1.84%.

11:00 am:

[BRIEFING.COM] The major indices hover at fresh session highs with the S&P 500 higher by 1.5%.

Energy (+2.6%), materials (+2.2%) and consumer discretionary (+1.8%) hold the lead while crude oil has extended its rally. WTI crude has climbed 5.3% to $30.55/bbl as speculation that Iran may join in a production freeze agreement boosts the beleaguered commodity.

In the commodity-sensitive materials space, Freeport-McMoRan (FCX 7.41, +1.04) has climbed 16.2% after Icahn Associates Holdings disclosed that the firm increased its position in the company from 100 million shares to 104 million shares. Meanwhile, Mosaic (MOS 24.67, +1.13), Alcoa (AA 8.56, +0.44) and DuPont (DD 60.56, +1.70) each show advances between 2.9% and 5.3%.

Elsewhere, T-Mobile (TMUS 36.86, +0.40) outperforms in the telecom services space (+0.4%) after reporting above-consensus earnings on revenue that matched expectations.

10:45 am: [BRIEFING.COM]

The dollar index is trading modestly higher right now, which is adding a slight amount of pressure on commodities currently

WTI oil is higher this morning, following the Saudi/Russia news

More headlines will hit of which OPEC and/or non-OPEC producers will participate in a possible production cut

Front-month Mar crude oil just extended gains further, now trading +5% at $30.49/barrel

Nat gas pulled back some and is now +0.6% at $1.92/MMBtu

Preciosu metals are showing just modest gains this morning.. Apr gold +0.1% at $1209.20/oz and Mar silver +0.1% at $15.35/oz

Copper is almost 1% higher at $2.07/lb

10:00 am:

[BRIEFING.COM] The major averages hover below their opening highs with the S&P 500 (+0.9%) and the Nasdaq Composite (+0.9%) each trading 3 points off their highs.

Energy (+0.8%) has slipped from the top of the leaderboard while materials (+1.4%) remains in the lead. Elsewhere, telecom services (UNCH) flirts with its flat line.

Rail companies have underperformed inside the Dow Jones Transportation average (+1.3%) as Union Pacific (UNP 79.83, +0.46) and Norfolk Southern (NSC 74.23, +0.24) trade lower in sympathy with CSX (CSX 24.47, -0.28). CSX has seen pressure this morning after comments from its CFO pointed to further headwinds for the company. The company expects its Q1 earnings to decline significantly and volume to decline in the mid-high single digits.

9:45 am:

[BRIEFING.COM] As expected, the major averages opened in positive territory with the tech-heavy Nasdaq (+1.0%) outpacing the S&P 500 (+0.9%).

Eight of ten sectors have opened in the green with commodity-sensitive materials (+1.6%) and energy (+1.5%) jockeying for the top spot. Most advancers show gains between 0.6% (technology) and 1.4% (consumer discretionary). The countercyclicals show the worst performances with health care (+0.4%), consumer staples (+0.3%), telecom services (-0.1%), and utilities (-0.6%) rounding out the board.

On the commodities front, WTI crude has slipped from its pre-market high but remains higher by 2.3% at $29.71/bbl.

The yield on the 10-yr note is higher by four basis points at 1.82%.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: +14.80. Nasdaq futures vs fair value: +36.40.

The stock market is on track for a higher open as S&P 500 futures trade 15 points above fair value.

Overnight, futures were helped by dovish commentary from Boston Fed President Rosengren (an FOMC voter), who stated that monetary policy normalization "should be unhurried" if inflation is slower to return to target. Additionally, a positive move in oil has helped investor sentiment. At this juncture, WTI crude trades higher by 3.7% at $30.10/bbl.

In corporate news, Priceline Group (PCLN 1,226.67, +113.77) has climbed 10.2% in pre-market trading after reporting above-consensus EPS and revenue results in Q4. The company also announced that it authorized a $3 billion share repurchase. Separately, Garmin (GRMN 37.60, +2.37) has rallied 6.7% this morning after beating top and bottom-line estimates in Q4. Garmin also issued mixed guidance for full year 2016 with EPS estimates below analyst consensus and revenue above expectations.

Just released, Industrial Production report pointed to an increase of 0.9% in January (Briefing.com consensus +0.3%) while capacity utilization hit 77.1% (Briefing.com consensus 76.6%). Today's economic data will be capped off with the 14:00 ET release of the FOMC minutes from the January 27th meeting.

The yield on the 10-yr note is higher by five basis points at 1.82%.

8:57 am: [BRIEFING.COM] S&P futures vs fair value: +12.30. Nasdaq futures vs fair value: +31.00.

The S&P 500 futures trade 12 points above fair value.

Equity markets across Asia ended the Wednesday session on a mixed note with investors showing renewed concern over Chinese monetary policy after the People's Bank of China set a weaker yuan fix for the second consecutive day. The developments did not stop the Shanghai Composite (+1.1%) from ending in the green, but other key indices in the region could not follow suit. In Japan, Prime Minister Shinzo Abe's adviser Etsuro Honda said that the Bank of Japan could step up its easing efforts, but a fiscal stimulus package and a postponement of the sales tax increase would also be welcome.

In economic data:

Japan's December Core Machinery Orders +4.2% month-over-month (expected 4.7%; last -14.4%); -3.6% year-over-year (consensus -3.1%; last 1.2%)

South Korea's January trade surplus KRW5.20 billion (expected surplus of KRW5.30 billion; previous surplus of KRW5.30) as imports -20.0% year-over-year (consensus -20.1%; last -20.1%) and exports -18.8% (expected -18.5%; previous -18.5%). Separately, January Unemployment Rate held at an upwardly revised 3.5%

Australia's MI Leading Index 0.0% month-over-month (previous -0.3%)

Singapore's January trade surplus SGD6.07 billion (previous SGD5.15 billion)

---Equity Markets---

Japan's Nikkei lost 1.4% with nine sectors posting losses between 0.2% (technology) and 3.4% (health care). The countercyclical communications sector (+1.6%) was the lone advancer. Inpex, Nisshin Steel, Fast Retailing, Toshiba, West Japan Railway, Sumitomo Metal Mining, Advantest, and TEPCO lost between 3.4% and 5.9%. On the upside, Softbank spiked 5.8% while Sharp, Casio, and Tokyo Electron gained between 2.8% and 3.3%.

Hong Kong's Hang Seng lost 1.0% with most components ending in the red. Energy-related names struggled notably with Kunlun Energy, CNOOC, China Petroleum & Chemical, and Petrochina falling between 3.0% and 4.1%. HSBC and Bank of China lost 1.7% and 2.0%, respectively, while Belle International and Sands China outperformed. The two names posted respective gains of 2.3% and 1.8%.

China's Shanghai Composite added 1.1%. China Shipbuilding and China State Construction both gained near 3.0% while Bank of China and Agricultural Bank of China added 0.3% and 1.0%, respectively.

Major European indices trade higher across the board while the euro slipped (1.1126) against the dollar. The early portion of the session has been relatively quiet with investors keeping an eye on crude oil. Market participants received some economic data this morning, but the reports have not had much impact on the action in equities.

In economic data:

UK's December Average Earnings Index + Bonus +1.9%, as expected (previous +2.1%). January Claimant Count Change -14,800 (expected -3,000; previous -15,200) and December Unemployment Rate held at 5.1% (consensus 5.0%)

Swiss February ZEW Expectations -5.9 (last -3.0)

---Equity Markets---

UK's FTSE trades up 1.8% with miners and consumer names in the lead. Anglo American, Glencore, Antofagasta, and Rio Tinto are up between 3.4% and 9.5% while Burberry, Sainsbury, and InterContinental Hotels show gains between 3.7% and 5.0%.

Germany's DAX is higher by 2.1% amid broad strength. ThyssenKrupp has surged 5.8% while Deutsche Bank, Daimler, Volkswagen, BMW, and Siemens are up between 1.3% and 2.9%. On the downside, RWE has plunged 12.9% after suspending its dividend. Peer E.On is lower by 2.3%.

France's CAC has climbed 2.2% with financials pacing the rally. Credit Agricole has surged 13.9% after its quarterly results showed restructuring plans. Societe Generale trades higher by 5.0% while BNP Paribas is up 2.3%. On the downside, Publicis Groupe and Total hold respective losses of 1.9% and 1.0%.

8:30 am: [BRIEFING.COM] S&P futures vs fair value: +10.00. Nasdaq futures vs fair value: +27.10.

The S&P 500 futures trade ten points above fair value.

January producer prices increased 0.1% while the Briefing.com consensus expected a downtick of 0.2%. Core producer prices increased 0.4% while the consensus expected a flat reading.

Separately, Housing starts rose to a seasonally adjusted annualized rate of 1.099 million units in January, which was down from a revised 1.143 million units in December (from 1.149 million). The Briefing.com consensus expected starts to increase to 1.171 million units. Building permits decreased to a seasonally adjusted annualized rate of 1.202 million in January from an unrevised 1.204 million for December. The Briefing.com consensus expected a reading of 1.200 million.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +13.50. Nasdaq futures vs fair value: +37.90.

U.S. equity futures trade at overnight highs with the S&P 500 futures 14 points above fair value. Futures trade higher ahead of a data heavy day while dovish remarks from Boston Fed President and FOMC voting member Eric Rosengren worked to boost market sentiment overnight. Oil remains in focus while OPEC oil ministers traveled to Iran to attempt to garner the country's cooperation for a production freeze. Currently, WTI crude is higher by 2.2% at $29.69/bbl.

On the economic front, the weekly MBA Mortgage Index was reported at 7:00 ET, showing a seasonally adjusted increase of 8.2% in mortgage applications. Meanwhile, January PPI (Briefing.com consensus -0.2%), January Housing Starts (Briefing.com consensus 1171k), and January Building Permits (Briefing.com consensus 1200k) will be released at 8:30 ET. Separately, the January Industrial Production Report (Briefing.com consensus +0.3%) and Capacity Utilization (Briefing.com consensus 76.6%) will cross the wires at 9:15 ET. Finally, the FOMC minutes from the January 27th meeting will be released at 14:00 ET.

Treasury yields have risen overnight with the yield on the 10-yr note higher by two basis points at 1.80%.

In U.S. corporate news of note:

Priceline (PCLN 1216.00, +103.10): +9.3% following a top and bottom-line beat in their Q4 earnings report

T-Mobile US (TMUS 38.00, +1.53): +4.2% after the company reported above-consensus EPS results on in-line revenue in Q4

Kinder Morgan (KMI 17.05, +1.43): +9.2% following Berkshire Hathaway (BRK.B 129.50, +0.00) disclosing the addition of 26.5 million shares to its position in the company

Cheesecake Factory (CAKE 47.90, -1.47): -3.0% after the company reported a beat on EPS with light revenue in its Q4 earnings report

Reviewing overnight developments:

Asian indices ended their session on a mixed note with Japan's Nikkei -1.4%, Hong Kong's Hang Seng -1.0%, and China's Shanghai Composite +1.1%.

In economic data:

Japan's December Core Machinery Orders +4.2% month-over-month (expected 4.7%; last -14.4%); -3.6% year-over-year (consensus -3.1%; last 1.2%)

South Korea's January trade surplus KRW5.20 billion (expected surplus of KRW5.30 billion; previous surplus of KRW5.30) as imports -20.0% year-over-year (consensus -20.1%; last -20.1%) and exports -18.8% (expected -18.5%; previous -18.5%). Separately, January Unemployment Rate held at an upwardly revised 3.5%

Australia's MI Leading Index 0.0% month-over-month (previous -0.3%)

Singapore's January trade surplus SGD6.07 billion (previous SGD5.15 billion)

In news:

The People's Bank of China set a weaker yuan fix for the second consecutive day

In Japan, Prime Minister Shinzo Abe's adviser Etsuro Honda said that the Bank of Japan could step up its easing efforts, but a fiscal stimulus package and a postponement of the sales tax increase would also be welcome.

European indices trade higher across the board with France's CAC +2.3%, Germany's DAX +2.2%, and the U.K.'s FTSE +1.8%.

In economic data:

UK's December Average Earnings Index + Bonus +1.9%, as expected (previous +2.1%). January Claimant Count Change -14,800 (expected -3,000; previous -15,200) and December Unemployment Rate held at 5.1% (consensus 5.0%)

Swiss February ZEW Expectations -5.9 (last -3.0)

5:50 am: [BRIEFING.COM] S&P futures vs fair value: +11.00. Nasdaq futures vs fair value: +20.10.

5:50 am: [BRIEFING.COM] Nikkei...15836...-218.10...-1.40%. Hang Seng...18924.6...-197.50...-1.00%.

5:50 am: [BRIEFING.COM] FTSE...5946.97...+84.80...+1.50%. DAX...9299.68...+164.60...+1.80%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com