Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

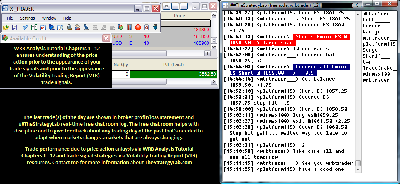

Attachment:

021016-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3562.50.png [ 94.71 KiB | Viewed 401 times ]

021016-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3562.50.png [ 94.71 KiB | Viewed 401 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$0.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$3562.50 dollars or +71.25 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3562.50 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted

real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=153&t=2287 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=285&t=3049 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

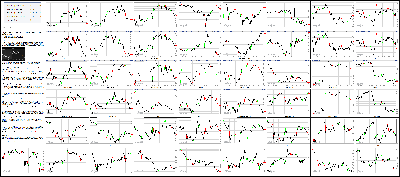

Attachment:

021016-Key-Price-Action-Markets.png [ 1.16 MiB | Viewed 388 times ]

021016-Key-Price-Action-Markets.png [ 1.16 MiB | Viewed 388 times ]

click on the above image to view today's price action of key markets 4:20 pm: [BRIEFING.COM] The major averages ended Wednesday's affair under heavy selling pressure, which left the Dow Jones Industrial Average and S&P 500 in negative territory when the closing bell rang. The Nasdaq managed a modest gain, yet still gave back a huge chunk of an earlier 101-point gain. Once again, trade centered on troubles inthe oil patch, concerns over global and domestic growth, currency swings, and the future path of the fed funds rate. Today saw limited articulation of that final point as Fed Chair Yellen gave her semiannual monetary policy report before the House Financial Services Committee.

The major averages hit session highs within the first hour of trading but were unable to hold those levels as participants once again showed a propensity to sell into strength. The financial sector, for instance, was an early leader -- and an influential one at that -- as it followed in the footsteps of European banks, which attracted a bargain-hunting bid on Wednesday. Deutsche Bank (DB 16.21, +0.83), which has been under heavy selling presure of late on investor concerns about its financial condition, helped lead that effort. Financials (-0.5%) here, though, were unable to hold their gains and helped precipitate the late-day selling interest.

Oil prices attempted an early rally, climbing above $29.00/bbl after the weekly inventory report from the EIA report showed a draw of 0.754 million barrels. That rally was short-lived though and the commodity soon rolled over. The disappointing price action there after an ostensibly bullish catalyst took some wind out of the stock market's sails. WTI crude settled the day down 1.6% at $27.54/bbl. The S&P 500 energy sector declined 0.5%.

Fed Chair Yellen's testimony was largely a middle-of-the-road presentation as she made it sound as if the Fed is open to holding off on another rate hike at its March meeting; however, she didn't make it sound as if the Fed is willing to concede anything past that meeting. One notable thing she said in the Q&A portion of her testimony was that she doesn't think it will be necessary to cut rates soon, yet she did add the Fed will do what is necessary to achieve its goals.

By and large, the response to Ms. Yellen's presentation was mixed and was reflected in the S&P closing the day relatively flat.

Healthcare (+0.9%) and technology (+0.4%) were the only sectors that were able to end the day with a gain, yet both groups ended the session well off their highs (+2.4% and +1.8%, respectively). The technology group saw leadership from large-cap components like Facebook (FB 101.00, +1.46) and Microsoft (MSFT 49.71, +0.43) while health care could attribute its relative strength to the biotechnology stocks.

The commodity-sensitive materials sector (-1.0%) ended the day with the worst performance.

At their highs of the day, the Dow Jones Industrial Average, Nasdaq Composite, and S&P 500 were up 1.2%, 2.4%, and 1.3%, respectively.

There were 1.05 billion shares traded at the NYSE, which was a bit light of the recent average.

Treasuries traded in a narrow range for most of the session, but came on strong in the afternoon and rolled to their best levels of the session as stocks sold off in the final hour of trading. The yield on the 10-yr note dropped four basis points to 1.69%.

Strikingly, the late selling in the equity market took place alongside a strengthening in the Japanese yen. The stronger yen has been problematic for Japanese exporters and has been a catalyst for heavy selling in Japan's stock market this month.

Today's economic data included the weekly MBA Mortgage Index and the Treasury Budget for January:

Mortgage applications were up 9.3% in the latest week driven by a 16.0% surge in refinancing applications.

The January Treasury Budget showed a surplus of $55.2 billion versus a deficit of $17.5 billion for the same period a year ago. This Treasury data is not seasonally adjusted, so the January surplus cannot be compared to the December deficit of $14.4 billion.

Total receipts in January were $313.6 billion while total outlays were $258.4 billion. Receipts were $6.8 billion more than January 2015 receipts while total outlays were $65.9 billion less than January 2015. The 12-month deficit decreased by $72.7 billion to $405.3 billion.

Tomorrow's economic data is limited to the weekly Initial Claims (Briefing.com consensus 280k). Tomorrow will also conclude Fed Chair Yellen's semiannual monetary policy report before the House Financial Services Committee

Russell 2000 -15.2% YTD

Nasdaq -14.5% YTD

S&P 500 --9.4% YTD

Dow Jones -8.7% YTD

3:40 pm: [BRIEFING.COM]

The dollar index has been sliding lower since morning trade and is now in negative territory

However, commodities such as precious metals are still sitting in the red

WTI oil prices were a big mover today, surging today above $29/barrel following the weekly EIA storage data

However, this move was short-lived and Mar crude closed the day -1.6% at $27.54/barrel

In other energy, natural gas lost steam today as well, with the Mar contract ending the day -2.4% at $2.05/MMBtu

Metals closed lower today as well. Apr gold finished -0.3% at $1194.70/oz, while Mar silver ended -1.2% at $15.27/oz

3:00 pm:

[BRIEFING.COM] The major averages have ticked higher in recent trade after hovering above their session lows. The Dow Jones Industrial Average (UNCH) briefly traded in negative territory before ticking above its flat line again.

Only the materials (-0.5%) sector trades in the red as it leads the downside. On the flipside, technology (+1.1%) and health care (+1.6%) have trimmed their advance from their session highs of 2.4% and 1.8%, respectively.

The heavyweight technology sector has managed to maintain a modest gain thanks to strength from sector large-caps. On the other hand, the high-beta chipmakers have shown relative weakness in the group with Intel (INTC 28.60, -0.21) and Qualcomm (QCOM 43.33, -0.27) showing respective losses of 0.8% and 0.7%.

Treasuries have notched a new session high with the yield on the 10-yr note lower by two basis points to 1.70%.

2:30 pm:

[BRIEFING.COM] The stock market continues to see chop above the middle half of its trading range, as the S&P 500 sees noticeable resistance between the 1868/1872 level.

The commodity-sensitive materials sector (-0.2%) now shows the largest loss as Monsanto (MON 88.48, -3.22) weighs on the group. The company is exhibiting weakness after it disclosed an $80 million penalty for accounting violations. Dow component DuPont (DD 58.10, -0.60) also weighs on the larger group with a loss of 1.1%.

Treasuries have inched to new session highs with the yield on the 10-yr note now lower by one basis points to 1.71%.

On the commodities front, WTI crude ended its pit session lower by 1.5% at $27.54/bbl.

2:00 pm:

[BRIEFING.COM] The major U.S. averages have slid lower in recent action as wavering trade in oil drags on the larger market. The commodity hovers above its session low ($27.39/bbl), currently trading lower by 1.5% at $27.51/bbl.

Airlines continue to show relative strength inside the Dow Jones Transportation Average (+0.7%). The group is benefiting from a January Traffic report from JetBlue (BLU 20.27, +0.20), which sees only a small loss from the recent winter storms.

Separately, the Treasury Budget statement for January was just released and it showed a surplus of $55.2 billion. The Treasury data is not seasonally adjusted so the January surplus cannot be compared to the December deficit of $14.4 billion.

1:35 pm:

[BRIEFING.COM] The major U.S. indices are relatively flat since our last update as stocks hold firm in positive territory, lead by the Nasdaq.

A look inside the Dow Jones Industrial Average shows that Nike (NKE 57.51, +1.83), Visa (V 70.17, +1.98), and Pfizer (PFE 29.80, +0.70) are outperforming amid broad market strength.

Conversely, Walt Disney (DIS 88.76, -3.56) is the worst-performing Dow component despite reporting strong Q1 results as investors eye issues at its ESPN unit. The report earned a number of price target reductions from analysts who cover the stock.

Rebounding from yesterday, the DJIA is now down just 1.04% this week.

Elsewhere, the Treasury's $23 bln 10-year note auction at the top of the hour drew a high yield of 1.73% on a bid-to-cover of 2.56.

1:05 pm:

[BRIEFING.COM] The US equity market has been swayed today by developments abroad as well as developments at home, namely the rebound in the European banking sector, Fed Chair Yellen's semiannual monetary policy report before the House Financial Services Committee, and some volatile action (again) in the energy pit.

The rebound in European banks, which was helped by an abeyance of concerns surrounding Deutsche Bank's (DB 16.45, +1.07) financial position, helped fuel sizable gains in European bourses and a positive bias in the futures market that led to a higher start for the cash market. The overall trading action, however, has been a bit skittish as traders have been busy toiling with Ms. Yellen's remarks and some frenetic oil price movements.

Briefly, the takeaway from Ms. Yellen's testimony is that it sounds like Ms. Yellen is open to taking a pass on raising the fed funds rate in March, but that she is not willing to concede anything past that meeting because more time and data need to pass to help the Fed gain a better feel for the effects on the U.S. economy of the recent tightening in financial conditions and foreign economic developments.

One notable revelation in the Q&A portion of her testimony was her acknowledgment that she doesn't think it will be necessary soon to cut interest rates. She did add, however, that the Fed will do what is necessary to achieve its goals.

At their highs of the morning, the Dow Jones Industrial Average, Nasdaq Composite, and S&P 500 were up 1.2%, 2.4%, and 1.3%, respectively. The Dow Jones eventually slipped into negative territory, hurt by weakness in Disney (DIS 88.83, -3.49), which failed to impress investors with its latest earnings results.

The major indices have been putting up a fight today though and have shown some resilience to more concerted selling efforts. The relative strength of the health care (+2.4%) and technology (+1.8%) sectors, which have been underpinned by the outperformance of the biotech stocks and large-cap leaders like Facebook (FB 102.72, +3.18) and Alphabet (GOOG 694.70, +16.59), has provided an important measure of broad market support.

The energy sector (+0.7%) is also helping at this time in what has been a roller-coaster trade for oil prices following weekly inventory data from the Department of Energy that showed a 0.754 million barrel draw in stockpiles.

That headline led to a spike in prices above $29 per barrel, yet just as quickly as oil prices spiked, they rolled back over again and eventually slipped below $28.00 per barrel. There was some related movement in the broader market in response to that volatility. Oil prices are currently down 0.3% at $27.86 per barrel.

There weren't any key economic releases out this morning, although it was reported that mortgage applications were up 9.3% in the latest week driven by a 16% surge in refinancing applications.

Consistent with the standing of the major indices, market internals show advancing issues leading declining issues by a better than 2-to-1 margin at the NYSE and Nasdaq.

Exiting the New York lunch hour, the Dow Jones Industrial Average, Nasdaq Composite, and S&P 500 are up 0.5%, 2.0%, and 1.2% respectively.

12:30 pm:

[BRIEFING.COM] The stock market has ticked higher in choppy trade as the major averages hover in the lower half of their daily trading ranges. The Nasdaq (+1.6%) continues to outperform the S&P 500 (+1.0%) as the tech-heavy Nasdaq rebounds from a monthly loss of 6.0% compared to the 3.6% loss in the benchmark.

Today's trade has been hallmarked by less of an interest in risk adverse sectors such as utilities (-0.6%) and telecom services (-0.3%). This is a departure from recent trend as the pair show the best performances of the year, with gains of 6.8% and 5.8%, respectively. This is echoed in the Treasuries market, which continues to see difficulty in moving yields lower. Currently, the yield on the 10-yr note is unchanged at 1.72%.

Oil has been able move back into the green with WTI crude higher by 0.5% at $28.10

12:10 pm:

[BRIEFING.COM] The major averages have ticked higher in recent action with the Dow Jones Industrial Average vacillating between positive and negative territory. This loss of upward momentum in the broader market has coincided with faltering key sector leadership. To that point, the financials sector (+0.4%) has trimmed its advance after the sector was up 1.9% and it now trades behind the broader market.

In the financial group, money center banks helped pace the retreat from today's highs. JPMorgan Chase (JPM 56.12, -0.07), Citigroup (C 37.73, +0.22), and Wells Fargo (WFC 46.53, +0.07) have all slipped from earlier highs.

Oil volatility continues to impact the broader market which is gyrating in response to the movement in oil prices. WTI crude flirts with its flat line with crude lower by 0.2% at $27.89/bbl.

11:35 am:

[BRIEFING.COM] The major averages have ticked continue to struggle to hold early gains. In the past half hour, Fed Chair Yellen testified that she doesn't think that it will be necessary to cut rates. It would be remiss not to add that she also said the Fed will do what is necessary to achieve its goals.

Health care (+1.5%) has climbed ahead of technology (+1.2%) in recent trade with biotechnology showing relative strength. At this juncture, the iShares Nasdaq Biotechnology ETF (IBB 25.97, +4.57) trade higher by 1.8%.

On the currencies front the U.S. Dollar Index continues to back away from its high, with the yen showing some added strength against the dollar. The dollar/yen pair is at 114.09.

Treasuries aren't doing much in the midst of action elsewhere. The yield on the 10-yr note is higher by one basis point at 1.74%.

11:05 am:

[BRIEFING.COM] The stock market ran to new session highs a short time ago but has since pulled back. Fed Chair Yellen has begun the Q&A portion of her testimony without any notable policy revelations thus far. At the same time, oil price have been volatile in the wake of the latest inventory report from the Department of Energy (EIA).

The EIA report showed a draw of 0.754 million barrels. That headline led to a spike in crude prices above $29.00/bbl, yet prices have begun to fade and are now crossing at $27.89/bbl.

The volatility in oil prices has contributed to roller coaster action in the major indices, which are now well off their session highs.

Eight of ten sectors currently trade in the green with technology (+1.3%) and health care (+1.4%) leading to the upside. Energy (+0.2%) climbed out of negative territory in recent action but has abandoned its high following the move in crude.

10:45 am: [BRIEFING.COM]

WTI oil futures started off the morning lower again, falling as low as

However, following the weekly EIA oil storage data, which showed a surprise draw of 0.754 mln barrels, Mar crude oil rallied

Oil has since pulled back some and Mar crude is now +0.6% at $28.11/barrel

In other energy, natural gas has been sliding lower this morning and is now -2.5% at $2.05/MMBtu

Precious metals have been in negative territory all day as strength in the dollar helps put on the pressure

Apr gold is now -1% at $1186.30/oz, while Mar silver is -1.8% at $15.17/oz

10:00 am:

[BRIEFING.COM] The stock market has climbed back to its opening high with the Nasdaq Composite (+1.5%) and the S&P 500 (+0.9%)

At this juncture, seven sectors trade in positive territory with consumer discretionary (+0.5) rebounding from its flat line in recent trade. Utilities (-1.5%) has fallen to the back of the pack with energy (-0.1%) trimming its loss.

In the heavily-weighted consumer discretionary space, media names underperform with Time Warner (TWX 59.07, -4.14) and Disney (DIS 88.94, -3.36) declining 6.7% and 3.6%, respectively. The stocks have tumbled into the day despite both reporting EPS beats before today's open. Time Warner has plummeted amid concerns regarding falling operating income in all its operating division while Disney has succumbed to pressure from its ESPN division.

On the commodities front, WTI crude has ticked off its low but still remains underneath its flat line. Currently, oil trades lower by 0.7% at $27.75/bbl.

Treasuries have slipped from their session highs with the yield on the 10-yr rising one basis point to 1.74%.

9:45 am:

[BRIEFING.COM] The stock market has opened the day on a higher note with the tech-heavy Nasdaq (+1.1%) leading the advance while the S&P 500 (+0.7%) follows.

Seven sectors currently trade in positive territory with technology (+1.4%) and health care (+1.3%) leading the advance. The remaining advancers show gains between 1.2% (financials) and 0.4% (consumer discretionary). On the flipside, commodity-sensitive energy (-1.0%) shows the largest decline.

On the commodities front, WTI crude has slipped 1.6% to trade at $27.50/bbl. The energy component will be looking ahead to the EIA weekly inventory report, crossing the wires at 10:30 a.m. ET.

Treasuries have ticked higher since the open to have the group trade largely flat. The yield on the 10-yr note trades unchanged at 1.73%.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: +11.30. Nasdaq futures vs fair value: +46.00.

The stock market is on track for a modestly higher open with S&P 500 futures trading 11 points above fair value. Futures slipped from their overnight highs after Fed Chair Yellen released her prepared statements ahead of today's Congressional testimony. Ms. Yellen cited tightening financial conditions amidst a global slowdown but also maintained that moderate growth at home would justify "gradual adjustments" to the Fed's monetary policy stance.

Overnight, a rebound in European Banking stocks has helped regional indices overseas enjoy moderate gains. Deutsche Bank (DB 16.42, +1.04) has rebounded from short-term oversold conditions on news that the bank is considering a big buyback of its senior bonds. Oil helped add on to early gains in futures but have since reversed ahead of the Department of Energy's Inventory Report at 10:30 ET. At this juncture oil trades lower by 0.6% at $27.81/bbl.

On the corporate front, Panera Bread (PNRA 189.94, +5.22) has climbed 2.8% after reporting Q4 EPS results above-consensus on in-line revenue. The company also issued in-line guidance with Q1 EPS estimates growing 2.0-5.0%.

Treasuries have pulled off their lows but the yield on the 10-yr note remains higher by two basis points at 1.75%.

8:55 am: [BRIEFING.COM] S&P futures vs fair value: +15.50. Nasdaq futures vs fair value: +54.30.

The S&P 500 futures trade 16 points above fair value.

Equity markets in the Asia-Pacific region had another rough outing on Wednesday with defensive sentiment pressuring most of the markets that were open. However, the yen notched its high early in the session (114.26), spending the rest of the night in a steady retreat from that mark. The dollar/yen pair currently trades near 114.80. On a somewhat related note, Japan's Prime Minister Shinzo Abe voiced confidence in the Bank of Japan despite the recent volatility in the country's bond market.

In economic data:

Japan's January Corporate Goods Price Index -0.9% month-over-month (expected -0.7%; last -0.3%); -3.1% year-over-year (consensus -2.8%; last -3.4%)

Australia's December HIA New Home Sales +6.0% month-over-month (last -2.7%) and February Westpac Consumer Sentiment 4.2% (expected -1.0%; last -3.5%)

New Zealand's January Electronic Card Retail Sales +0.3% month-over-month (consensus 0.3%; prior 0.1%); +5.2% year-over-year (last 6.6%)

---Equity Markets---

Japan's Nikkei lost 2.3%, setting a new low for the year. All ten sectors ended the day in negative territory with utilities (-5.0%), communications (-3.6%), and financials (-3.4%) leading the retreat. Mitsubishi Materials, Asahi Group Holdings, TEPCO, Ebara, Pioneer, Shinsei Bank, and Sharp lost between 6.0% and 12.8%.

Hong Kong's Hang Seng was closed for Lunar New Year.

China's Shanghai Composite was closed for Lunar New Year.

Major European indices trade higher across the board after gathering steam through the first three hours of the session. The advance comes ahead of Fed Chair Janet Yellen's semiannual congressional testimony. Ms. Yellen's will begin at 10:00 ET.

Economic data was limited:

UK's December Industrial Production -1.1% month-over-month (expected -0.1%; last -0.8%); -0.4% month-over-month (expected 1.0%; last 0.7%). December Manufacturing Production -0.2% month-over-month (consensus 0.1%; prior -0.3%); -1.7% year-over-year (consensus -1.4%; last -1.2%)

France's December Industrial Production -1.6% month-over-month (consensus 0.2%; last -0.9%)

Italy's December Industrial Production -0.4% month-over-month (expected 0.3%; last -0.5%); -1.0% year-over-year (consensus 1.4%; previous 1.1%).

---Equity Markets---

UK's FTSE trades up 0.6% with more than 85% of its components in the green. Financials have shown relative strength with Prudential, Aberdeen Asset Management, Old Mutual, and Hargreaves Lansdown up between 3.1% and 6.6%. On the downside, miners have struggled with Randgold Resources, Glencore, Fresnillo, and BHP Billiton down between 0.7% and 3.1%. Hikma Pharmaceuticals has plunged 12.6% after agreeing to lower the price for its acquisition of Roxane Laboratories and Boehringer Ingelheim Roxane.

France's CAC has spiked 2.0%, erasing its loss from yesterday. Just about every index component trades in the green with financials pacing the advance. Societe Generale, BNP Paribas, Credit Agricole hold gains between 5.8% and 8.2% while consumer names like Accor, Vivendi, Kering, and L'Oreal have climbed between 2.6% and 4.4%.

Germany's DAX is higher by 2.1% amid broad strength. Deutsche Bank has surged 12.6% following reports the bank is considering a multi-billion buyback. Commerzbank has followed, trading higher by 8.6%, while Thyssenkrupp, Lufthansa, Linde, and BMW show gains between 2.5% and 4.0%.

8:26 am: [BRIEFING.COM] S&P futures vs fair value: +23.30. Nasdaq futures vs fair value: +70.30.

Equity futures continue to trade sharply higher with the S&P 500 futures currently trading 23 points above fair value.

On the corporate front, media giant Time Warner (TWX 60.50, -2.71) has tumbled 4.3% despite reporting a Q4 earnings beat. Investors appear to be focusing on the company's revenue miss with revenue falling 5.9% year-over-year. The company has seen large headwinds from their Warner Bros. division. Fellow discretionary large-cap Disney (DIS 89.63, -2.69) has seen pullback after it reported earnings after yesterday's close. The company's top and bottom-line beat is being outshined by continued pessimism regarding the company's ESPN component. Disney also received several downgrades this morning with its price target lowered to $118 from $120 at JP Morgan.

In commodities, oil has slid from its recent high with the commodity still up 1.6% to $28.39/bbl.

Treasuries continue to inch lower with the yield on the 10-yr note now higher by four basis points at 1.77%.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +23.50. Nasdaq futures vs fair value: +67.10.

U.S. equity futures hover at overnight highs with the S&P 500 futures trading 24 points above fair value. The rally in futures can be attributed to a similar rally in oil and a rebound from European banking stocks. The market appears to maintain a wait-and-see attitude ahead of Fed Chair Yellen's monetary policy report testimony at 10:00 a.m. ET.

On the economic front, the weekly MBA Mortgage Index was reported at 7:00 ET, showing a seasonally adjusted increase of 9.3% in mortgage applications. Meanwhile, Fed Chair Janet Yellen will offer monetary policy testimony in front of Congress at 10:00 ET and the Treasury Budget for January will cross the wires at 14:00 ET.

Treasuries float near session lows with the yield on the 10-yr note rising three basis points to 1.76%.

In U.S. corporate news of note:

Disney (DIS 88.96, -3.36): -3.6% following continued perceived ESPN weakness despite a top and bottom-line beat in its Q1 earnings report

Time Warner (TWX 62.00, -1.21): -1.9% after reporting a Q4 revenue miss with adjusted operating income declining 12.0%

SolarCity (SCTY 18.15, -8.20): -31.1% following the company issuing below-consensus Q1 guidance with losses per share between $2.65-2.55

Reviewing overnight developments:

In the Asian Market, Japan's Nikkei shed 2.3% while Hong Kong's Hang Seng and China's Shanghai Composite remained closed for the Lunar New Year.

In economic data:

Japan's January Corporate Goods Price Index -0.9% month-over-month (expected -0.7%; last -0.3%); -3.1% year-over-year (consensus -2.8%; last -3.4%)

Australia's December HIA New Home Sales +6.0% month-over-month (last -2.7%) and February Westpac Consumer Sentiment 4.2% (expected -1.0%; last -3.5%)

New Zealand's January Electronic Card Retail Sales +0.3% month-over-month (consensus 0.3%; prior 0.1%); +5.2% year-over-year (last 6.6%)

In news:

Japan's Prime Minister Shinzo Abe voiced confidence in the Bank of Japan despite the recent volatility in the country's bond market.

The Dollar/Yen pair notched an early high (114.26) but has since dipped to 114.95.

European markets trade broadly higher with Germany's DAX +2.5%, France's CAC +2.5%, and the U.K.'s FTSE +1.1%.

Economic data was limited:

UK's December Industrial Production -1.1% month-over-month (expected -0.1%; last -0.8%); -0.4% month-over-month (expected 1.0%; last 0.7%). December Manufacturing Production -0.2% month-over-month (consensus 0.1%; prior -0.3%); -1.7% year-over-year (consensus -1.4%; last -1.2%)

France's December Industrial Production -1.6% month-over-month (consensus 0.2%; last -0.9%)

Italy's December Industrial Production -0.4% month-over-month (expected 0.3%; last -0.5%); -1.0% year-over-year (consensus 1.4%; previous 1.1%).

5:51 am: [BRIEFING.COM] S&P futures vs fair value: +20.30. Nasdaq futures vs fair value: +58.90.

5:51 am: [BRIEFING.COM] Nikkei...15713.4...-372.10...-2.30%. Hang Seng...Holiday.........

5:51 am: [BRIEFING.COM] FTSE...5696.64...+64.50...+1.10%. DAX...9088.13...+208.70...+2.40%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com