Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

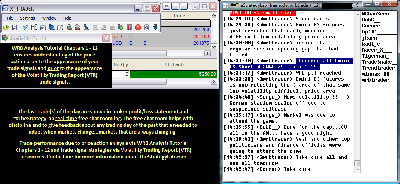

Attachment:

111715-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5250.00.png [ 93.64 KiB | Viewed 309 times ]

111715-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+5250.00.png [ 93.64 KiB | Viewed 309 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$00.00 dollars or +0.00 points, Emini ES ($ES_F) futures @

$5250.50 dollars or +105.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $5250.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted

real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=149&t=2221 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Daily Trading Plan Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=277&t=2948 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

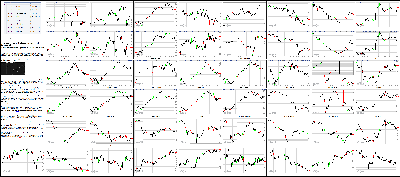

Attachment:

111715-Key-Price-Action-Markets.png [ 1.13 MiB | Viewed 295 times ]

111715-Key-Price-Action-Markets.png [ 1.13 MiB | Viewed 295 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market finished the day on a flat note after enjoying an opening rally that briefly placed the S&P 500 (-0.1%) above its 200-day moving average (2,064). The benchmark index was up around 0.7% during late morning action, but steady afternoon selling ensured a lower finish.

The second-half retreat accelerated after police officials in Hanover, Germany confirmed that a credible bomb threat forced the cancellation of a soccer match between Germany and the Netherlands. Press reports suggested that an emergency vehicle loaded with explosives was found at the soccer stadium, but this was refuted by the German Interior Minister just before the market closed for the day.

Treasuries notched their highs in reaction to the news, but to be fair, they spent the day in a steady climb off their lows that were set around 10:30 ET. The 10-yr note ended the day with a modest gain, pressuring its yield two basis points to 2.26% after testing the 2.31% level during morning action.

Six sectors ended the day with losses while health care (+0.4%) ended in the lead thanks to daylong strength in biotechnology. To that point, the iShares Nasdaq Biotechnology ETF (IBB 329.14, +4.25) gained 1.3%, helping keep the Nasdaq Composite ahead of the broader market. However, that was a small victory considering the Nasdaq returned to its flat line as large cap tech sector (unch) components struggled, overshadowing a good showing from the chipmaker space where the PHLX Semiconductor Index gained 0.6%.

Similar to technology, most cyclical sectors ended the day with modest losses while energy (-1.1%) underperformed notably. The growth-sensitive sector struggled from the start after surging more than 3.0% on Monday. As for today, the sector retreated while crude oil lost 2.4%, ending the pit session at $40.74/bbl.

Although the energy sector posted a notable loss, the group still ended ahead of the utilities sector, which lagged throughout the day, settling lower by 1.8%. Elsewhere among countercyclical groups, the consumer staples sector ended flat, masking a 3.5% spike in the shares of Wal-Mart (WMT 59.92, +2.05) after the retail giant reported a one-cent beat. Meanwhile, another retailer-Home Depot (HD 126.18, +5.34)-also had a solid showing, spiking 4.4%, in reaction to better than expected results, but the consumer discretionary sector was limited to a slim gain of 0.2%.

In other earnings of note, Dick's Sporting Goods (DKS 36.96, -3.85) tumbled 9.4% after missing estimates and lowering its guidance. The report cast a pall over apparel retailers with the likes of Under Armour (UA 84.99, -5.01), Finish Line (FINL 15.52, -0.40), and Lululemon (LULU 44.09, -1.15) falling between 2.5% and 5.6%.

Today's session generated above-average activity with more than a billion shares changing hands at the NYSE floor.

Economic data included CPI, Industrial Production, and NAHB Housing Market Index:

The October Consumer Price Index was right in-line with expectations. Both total CPI and core CPI, which excludes food and energy, increased 0.2%.

Total CPI is up 0.2% year-over-year on an unadjusted basis while core CPI is up 1.9%, which is steady with the year-over-year change seen in September

October Industrial Production declined 0.2% on top of an unrevised 0.2% decline in September while the Briefing.com consensus estimate called for a 0.1% increase

Total industrial production is up 0.3% year-over-year

The October weakness was driven entirely by the mining and utilities groups, which saw output decline 1.5% and 2.5%, respectively, while manufacturing output increased 0.4%, which was the biggest gain since a 1.0% jump in July and the first increase in the last three months

The NAHB Housing Market Index for November fell to 62 from an upwardly revised 65 (from 64) while the Briefing.com consensus expected the reading to come in at 64.5

Tomorrow, the weekly MBA Mortgage Index will be released at 7:00 ET while October Housing Starts (Briefing.com consensus 1.173 million) and Building Permits (consensus 1.137 million) will be reported at 8:30 ET. Also of note, the Federal Reserve will release the minutes from its October meeting at 14:00 ET.

Nasdaq Composite +5.3% YTD

S&P 500 -0.4% YTD

Dow Jones Industrial Average -1.9% YTD

Russell 2000 -4.2% YTD

3:20 pm: [BRIEFING.COM]

The dollar index trended near the flat-line in early morning trade, following the release of in-line US CPI and Core CPI data sets (showing +0.2% growth)

As the session progressed the index saw a moderate rally- which exacerbated prior sell-offs in WTI, precious metals and copper- and is now +0.2% to 99.68

Crude Oil followed its early trend-as sentiment ahead of tonight's API and tomorrow's EIA inventory reports caused a pullback from yesterday's positive close

January WTI closed -2.3% to $40.74/barrel

Natural gas got pummeled in early trading (on weather-related demand drivers) before lifting mid-session to close modestly negative at -0.8% to $2.37/MMBtu

Precious metals and copper closed lower: Gold on the dollar's strength, and silver/copper on Asian industrial demand concerns.

Gold closed -1.4% to $1068.60/oz, silver closed -0.4% to $14.17/oz and copper fell -0.9% to $2.10/lb

2:55 pm:

[BRIEFING.COM] The major averages have slipped to lows with the S&P 500 (-0.1%) now showing a slim loss for the day.

Equity indices have surrendered the remaining portion of their gains in recent going after police officials in Hanover, Germany confirmed that there was a credible bomb threat to a soccer match that had been scheduled to take place between Germany and the Netherlands. First reports of the cancellation were out about 90 minutes ago, but the official confirmation came through within the past 30 minutes. On a related note, subway and tram stations in Hanover have been closed.

Treasuries have been on the comeback trail since early morning action and they have recently marked their highs with the 10-yr yield currently lower by a basis point at 2.26%.

2:25 pm:

[BRIEFING.COM] The major averages remain near their recent levels with the S&P 500 trading higher by 0.2%.

Although the market has not moved much in recent going, the materials sector has seen a brief spike that has now been mostly retraced. That short-lived move occurred after it was reported that Airgas (ARG 110.04, +7.86) will be acquired by Air Liquide (AIQUY 26.43, +0.38) for $143/share. Shares of Airgas have been halted after surging to highs earlier in the day in the wake of a Bloomberg report, which indicated an acquisition is in the cards.

Elsewhere, Treasuries have returned near their session highs, pushing the 10-yr yield down one basis point to 2.26%.

2:00 pm:

[BRIEFING.COM] Equity indices continue holding modest gains after sliding from their morning highs. The S&P 500 is higher by 0.3% while the Nasdaq (+0.4%) remains ahead.

Despite the pullback from day's highs, seven sectors continue holding gains with six up 0.3% or more. The health care sector (+0.7%) is back in the lead after the consumer discretionary space (+0.6%) slipped behind the countercyclical sector. Furthermore, biotechnology remains ahead of the broader market with the iShares Nasdaq Biotechnology ETF (IBB 329.87, +4.98) up 1.5% at this juncture.

On the downside, the utilities sector (-0.9%) trades well behind the broader market despite a rebound in Treasuries while energy (-0.7%) has been trapped in the red throughout the day after yesterday's 3.0%+ surge. Crude oil, meanwhile, is on track to end the pit session lower by 2.0% at $40.92/bbl.

1:35 pm:

[BRIEFING.COM] The major U.S. indices are off their intra-day highs, but are holding firm in positive territory.

A look inside the Dow Jones Industrial Average shows that Home Depot (HD 126.04, +5.20), Wal-Mart (WMT 60.21, +2.34), and Intel (INTC 32.63, +0.53) are outperforming. Home Depot and Wal-Mart are both higher after reporting their quarterly earnings. The do-it-yourself retailer reported its Q3 results which surpassed on top and bottom line metrics, and said it expected its FY16 earnings to be at the top end of its prior guidance. Wal-Mart delivered Q3 earnings that also exceeded analyst expectations, and guided for Q4 slightly above consensus.

Conversely, Caterpillar (CAT 69.52, -0.87) is the worst-performing Dow component as industrials lag.

For the week, the DJIA is up 1.5%, but still down 0.9% this month.

Related Quotes

12:55 pm:

[BRIEFING.COM] The major averages are on track for their second consecutive advance, but they have backed away from their highs in recent going. The Nasdaq Composite is higher by 0.4% while the S&P 500 (+0.3%) follows right behind. The first half of the Tuesday session has been very similar to yesterday's affair as stocks followed their range-bound start with a broad-based rally that has lifted the S&P 500 back into the neighborhood of its 200-day moving average (2,064).

Unlike yesterday, the energy sector (-0.6%) has not taken part in today's climb, trading in the red amid a 2.3% decline in crude oil, which has slid to $40.80/bbl. Dollar strength may have contributed to the weakness in oil as the Dollar Index (99.65, +0.26) inches back to levels last seen in mid-March. The index climbed to highs after October CPI (+0.2%) matched expectations.

Eight sectors sport midday gains with consumer discretionary (+0.6%) and health care (+0.5%) jockeying for the lead. The discretionary sector has been boosted by Netflix (NFLX 117.43, +6.08) and Home Depot (HD 124.99, +4.15) with the latter surging 3.4% in reaction to above-consensus results. On a related note, Wal-Mart (WMT 60.71, +2.84) has spiked 4.9% after reporting a one-cent beat, which has underpinned the consumer staples sector (+0.4%).

Elsewhere, the top-weighted technology sector (+0.4%) has also provided a measure of support with high-beta chipmakers showing relative strength. The PHLX Semiconductor Index has gained 0.9%, which has contributed to the relative strength in the Nasdaq. In that same vein, the Nasdaq has drawn strength from biotech names, evidenced by a 1.4% gain in the iShares Nasdaq Biotechnology ETF (IBB 329.47, +4.58).

Interestingly, Treasuries retreated into the morning, but they have been on the comeback trail with the 10-yr yield currently flat at 2.27%.

Economic data included CPI, Industrial Production, and NAHB Housing Market Index:

The October Consumer Price Index was right in-line with expectations. Both total CPI and core CPI, which excludes food and energy, increased 0.2%.

Total CPI is up 0.2% year-over-year on an unadjusted basis while core CPI is up 1.9%, which is steady with the year-over-year change seen in September.

October Industrial Production declined 0.2% on top of an unrevised 0.2% decline in September while the Briefing.com consensus estimate called for a 0.1% increase

Total industrial production is up 0.3% year-over-year

The October weakness was driven entirely by the mining and utilities groups, which saw output decline 1.5% and 2.5%, respectively, while manufacturing output increased 0.4%, which was the biggest gain since a 1.0% jump in July and the first increase in the last three months

The NAHB Housing Market Index for November fell to 62 from an upwardly revised 65 (from 64) while the Briefing.com consensus expected the reading to come in at 64.5

12:30 pm:

[BRIEFING.COM] The major averages have backed away from their highs with the Nasdaq (+0.5%) holding posture ahead of the S&P 500 (+0.4%).

Recent action saw the health care sector (+0.6%) slipping from the top spot, leaving the consumer discretionary sector (+0.9%) in the lead. It is worth noting that the discretionary sector has received a significant measure of support from Netflix (NFLX 117.90, +6.55) as the stock surges 6.0% to build on yesterday's relative strength amid no news. Thanks to today's gain, the stock is now back at levels last seen in late August.

Interestingly, Treasuries have erased the bulk of their losses, leaving the 10-yr yield higher by a basis point at 2.28%.

11:55 am:

[BRIEFING.COM] Equity indices remain near their best levels of the session with the S&P 500 trading higher by 0.5%.

The major averages have held their ground in recent going while a wave of greenback strength has sent the Dollar Index (99.69, +0.31) to a fresh session high, which puts the index back near its levels from the middle of March. Accordingly, the euro has returned to its lows from early April, trading near 1.0635 against the dollar.

Elsewhere, Treasuries have ticked up off their lows, but they remain in negative territory with the 10-yr yield up two basis points at 2.29%.

11:30 am:

[BRIEFING.COM] The major averages continue holding solid gains after overcoming a shaky start. The S&P 500 trades higher by 0.5% with just two sectors trading in the red.

On the upside, the health care sector (+1.0%) leads the way with biotechnology largely responsible for the strength as the iShares Nasdaq Biotechnology ETF (IBB 330.65, +5.76) trades higher by 1.8%. That strength has helped the Nasdaq (+0.6%) vault ahead of the benchmark index. In addition, the Nasdaq has drawn strength from the technology sector (+0.5%, which continues trading just ahead of the S&P 500.

Elsewhere, energy (-0.2%) and utilities (-0.5%) continue trading in negative territory.

10:55 am:

[BRIEFING.COM] Equity indices have overcome the early indecision, rallying to new highs. The S&P 500 is now up 0.5% with eight sectors trading in the green.

Most cyclical sectors struggled at the start, but they have propelled the market higher in recent going. The consumer discretionary space has extended its gain to 0.8% while the top-weighted technology sector (+0.5%) also trades ahead of the broader market. Meanwhile, the energy sector was down more than 1.0% at the start of the session, but now trades just above its flat line while crude oil remains lower by 1.1% at $41.27/bbl.

Elsewhere, Treasuries have slipped to new lows with the 10-yr yield up four basis points at 2.31%.

10:30 am: [BRIEFING.COM]

The dollar trended higher overnight (driven by yesterday's rate-hike commentary from Janet Yellen), before pulling-back to near flat ahead of US CPI data

Upon the release of in-line CPI and Core CPI data (both at +0.2%) the index spiked higher, putting additional pressure on already negative WTI and gold futures

Currently, the dollar has once again failed to hold most of its prior gains, now +0.2% to $99.62

Gold and silver are trading mixed, with December gold trending lower all session- at -0.8% to $1074.70/oz- on a periodically-strong dollar and increased risk-on trades. Silver meanwhile, is holding closer to flat, at -0.3% to $14.18/oz.

WTI sold off in early trade, and continues to hold strong losses near its LoD, as market sentiment ahead of this evening's API data release has begun to outweigh speculation on potential near-term supply disruption in the Middle East. January crude is now -2.1% to $40.89/MMBtu

Natural gas is booking strong losses at -2.4% to $2.33/MMBtu, as mild near-term weather forecasts have exacerbated a pull-back from yesterday's rally

Copper is now -0.2% to $2.11/lb

10:00 am:

[BRIEFING.COM] The major averages remain near their flat lines as energy (-0.8%) and three other sectors trade in negative territory while the two consumer sectors outperform.

Just released, the NAHB Housing Market Index for November fell to 62 from an upwardly revised 65 (from 64) while the Briefing.com consensus expected the reading to come in at 64.5.

9:40 am:

[BRIEFING.COM] Equity indices flashed modest gains at the start of the session, but they have ticked back near their flat lines. The S&P 500 currently hovers within a point of its unchanged level with seven sectors showing early losses.

Most notably, the energy sector (-1.4%) has stumbled at the start after spiking more than 3.0% yesterday. To little surprise, today's opening weakness in the sector has coincided with selling in the oil market as WTI crude trades lower by 1.7% at $41.01/bbl.

Elsewhere, the remaining decliners show losses of no more than 0.2% while consumer discretionary (+0.3%) and consumer staples (+0.3%) outperform.

Treasuries have inched up off their lows, but they remain in the red with the 10-yr yield up two basis points at 2.29%.

The November NAHB Housing Market Index (consensus 64.5) will be released at 10:00 ET.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: +4.50. Nasdaq futures vs fair value: +11.40.

The stock market is on track for a higher open as S&P 500 futures trade five points above fair value after charging off their lows at the start of the European session. Index futures have made their way higher alongside markets in Europe with equity indices in France, Germany, and the UK showing gains between 1.8% and 2.4% at this juncture.

The rally in Europe has been fueled by defense names like Airbus, BAE Systems, and Rolls Royce while U.S. futures have climbed in sympathy. That being said, a couple large names are on track to display early strength with Home Depot (HD 124.75, +3.91) up 3.2% in pre-market while Wal-Mart (WMT 59.47, +1.60) has added 2.8%. Both names are tracking solid opening gains in reaction to better than expected quarterly results.

On the economic front, October CPI (+0.2%) was reported in-line with expectations while the just released Industrial Production report pointed to a decrease of 0.2% in October while the Briefing.com consensus expected an uptick of 0.1%. Capacity utilization hit 77.5%, which is what the Briefing.com consensus expected.

Treasuries hover near their session lows with the 10-yr yield higher by three basis points at 2.31%.

8:52 am: [BRIEFING.COM] S&P futures vs fair value: +6.50. Nasdaq futures vs fair value: +14.00.

The S&P 500 futures trade seven points above fair value.

Asian equity markets were mostly higher on Tuesday on a session where macro data was exceptionally light and non-eventful. Early strength was seen in China and Hong Kong after unconfirmed reports suggested that the PBoC lowered its RRR for the Bank of Beijing in an attempt to inspire lending in rural areas. The Shanghai Composite was unable to sustain gains, closing down just slightly for the session. Japanese shares got a boost after local reports suggested that the central government may propose additional fiscal measures when it announces its 2016 budget projections next week. This may allow the BoJ to hold status quo when it meets later this week.

In economic data:

Hong Kong's October Unemployment Rate held at 3.3%, as expected

Singapore's trade surplus narrowed to SGD7.92 billion from SGD5.84 billion with October non-oil exports rising 1.1% month-over-month (expected -1.9%; previous 2.8%)

New Zealand's Inflation Expectations held at 1.9% quarter-over-quarter

------

Japan's Nikkei increased 1.2%. The index was paced by robust gains in Energy (+3.0%), Industrials (+1.9%), and Materials (+1.8%), while Telecom (-0.1%) was the only sector to close negatively. Among the leaders in Energy were Showa Shell (+3.2%) and JX Holdings (+3.1%). Toyota was also among the leaders with the automaker posting a gain of 1.8%.

Hong Kong's Hang Seng advanced by 1.2%. Earnings were front and center with the likes of PICC Group, which posted a 2.2% gain after it reported its latest earnings update. Likewise, China Shenhua Energy Co tacked on 2.6% after the co reported better than expected results. ZTE also posted a robust 3.2% gain after the company announced it had won a series of new contracts

China's Shanghai Composite declined 0.1% after being up well over 1% shortly after the start of trading. Traders kept a lid on gains and selling pressure picked up after the mid-way point, after the speculation of the Bank of Beijing news never seemed to find firm ground. Among some of the notable names, Tingyi Cayman Islands Holding Corp (-0.3%) was little changed after it reported its third quarter results. China Airlines managed to post a 1.4% gain after it published better than expected Q3 results.

Major European indices trade higher across the board with France's CAC (+2.3%) leading the way. The euro has remained under pressure, setting a new seven-month low against the dollar at 1.0643 before erasing a portion of its decline. The euro currently hovers near 1.0666 against the greenback.

Investors received several data points:

Eurozone ZEW Economic Sentiment slipped to 28.3 from 30.1 (expected 35.2)

Germany's November ZEW Economic Sentiment 10.4 (expected 6.0; last 1.9) and ZEW Current Conditions 54.4 (consensus 55.0; last 55.2)

UK's October CPI +0.1% month-over-month, as expected; -0.1% year-over-year, as expected. Separately, Core CPI +1.1% year-over-year (consensus 1.0%; last 1.0%) and Input PPI -12.1% year-over-year (consensus -12.0%; last -13.4%)

Italy's September Trade surplus expanded to EUR2.19 billion from EUR1.85 billion (expected surplus of EUR2.24 billion)

------

UK's FTSE is higher by 1.9% with all but four components trading in the green. Smiths Group has surged 9.6% in reaction to better than expected results while defense names like BAE Systems and Rolls Royce hold respective gains of 2.1% and 4.2%. On the downside, miners Anglo American, Randgold Resources, and Fresnillo show losses between 0.4% and 2.0%.

Germany's DAX has climbed 1.9% with growth-sensitive names in the lead. BASF, ThyssenKrupp, and Continental are up between 2.5% and 3.2%. Meanwhile, financials hold slimmer gains with Commerzbank and Deutsche Bank both up near 1.3%.

France's CAC has spiked 2.3% amid gains in all 40 components. Airbus leads with a 3.6% surge while Cap Gemini, Vivendi, and Technip show gains between 2.8% and 3.4%.

8:31 am: [BRIEFING.COM] S&P futures vs fair value: +4.80. Nasdaq futures vs fair value: +13.00.

The S&P 500 futures trade five points above fair value.

Total CPI increased 0.2% (Briefing.com consensus +0.2%) in October while core CPI, which excludes food and energy, also increased 0.2% (Briefing.com consensus +0.2%). On a year-over-year basis, total CPI is up 0.2% and core CPI is up 1.9%.

7:55 am: [BRIEFING.COM] S&P futures vs fair value: +5.50. Nasdaq futures vs fair value: +15.80.

U.S. equity futures trade in the green amid upbeat action overseas. The S&P 500 futures hover six points above fair value after rallying off their lows after the start of the European session.

Meanwhile, Treasuries have retreated, pushing the 10-yr yield higher by two basis points to 2.29%.

Yesterday was very quiet on the economic front, but today will be a bit busier with October CPI (Briefing.com consensus 0.2%) set to be reported at 8:30 ET while October Industrial Production (expected 0.1%) will be announced at 9:15 ET and the November NAHB Housing Market Index (consensus 64.5) will be released at 10:00 ET.

In U.S. corporate news of note:

Wal-Mart (WMT 59.25, +1.38): +2.4% in reaction to a one-cent beat and in-line guidance.

Home Depot (HD 124.95, +4.11): +3.4% after beating estimates and guiding towards the high end of its prior outlook range.

Cheetah Mobile (CMCM 18.39, +1.22): +7.1% after beating bottom-line estimates.

Reviewing overnight developments:

Asian markets ended mostly higher. Japan's Nikkei +1.2%, Hong Kong's Hang Seng +1.2%, and China's Shanghai Composite -0.2%

In economic data:

Hong Kong's October Unemployment Rate held at 3.3%, as expected

Singapore's trade surplus narrowed to SGD7.92 billion from SGD5.84 billion with October non-oil exports rising 1.1% month-over-month (expected -1.9%; previous 2.8%)

New Zealand's Inflation Expectations held at 1.9% quarter-over-quarter

Among news of note:

The Reserve Bank of Australia released the minutes from its latest meeting, which showed that the central bank has room for additional easing, but is likely to be reluctant to lower rates considering how low they already are

Major European indices trade higher across the board. UK's FTSE +1.7%, Germany's DAX +1.8%, and France's CAC +2.2%. Elsewhere, Italy's MIB +1.7% and Spain's IBEX +2.1%

Investors received several data points:

Eurozone ZEW Economic Sentiment slipped to 28.3 from 30.1 (expected 35.2)

Germany's November ZEW Economic Sentiment 10.4 (expected 6.0; last 1.9) and ZEW Current Conditions 54.4 (consensus 55.0; last 55.2)

UK's October CPI +0.1% month-over-month, as expected; -0.1% year-over-year, as expected. Separately, Core CPI +1.1% year-over-year (consensus 1.0%; last 1.0%) and Input PPI -12.1% year-over-year (consensus -12.0%; last -13.4%)

Italy's September Trade surplus expanded to EUR2.19 billion from EUR1.85 billion (expected surplus of EUR2.24 billion)

Among news of note:

The euro has remained under pressure, setting a new seven-month low against the dollar at 1.0643 before erasing a portion of its decline. The euro currently hovers near 1.0666 against the greenback.

5:49 am: [BRIEFING.COM] S&P futures vs fair value: +7.30. Nasdaq futures vs fair value: +16.00.

5:49 am: [BRIEFING.COM] Nikkei...19630.63...+236.90...+1.20%. Hang Seng...22264.25...+253.40...+1.20%.

5:49 am: [BRIEFING.COM] FTSE...6259.38...+112.70...+1.80%. DAX...10909.03...+195.80...+1.80%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com