Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

wrbanalysis@gmail.com (24/7)

http://twitter.com/wrbtrader (24/7)

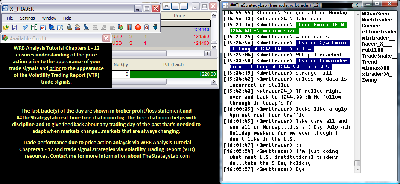

Attachment:

070215-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1220.00.png [ 92.6 KiB | Viewed 383 times ]

070215-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1220.00.png [ 92.6 KiB | Viewed 383 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$470.00 dollars or +4.70 points, Emini ES ($ES_F) futures @

$750.00 dollars or +15.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,220.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=145&t=2114 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=267&t=2814 contains brief information about trading plan, market context, brokers, trading time frames, position size management and other discussions.

-----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

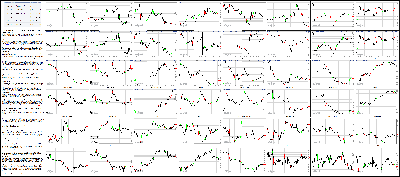

Attachment:

070215-Key-Price-Action-Markets.png [ 1.21 MiB | Viewed 379 times ]

070215-Key-Price-Action-Markets.png [ 1.21 MiB | Viewed 379 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The major averages ended an abbreviated trading week on a cautious note, which wasn't all that surprising since the weekend will feature a Sunday referendum in Greece. The S&P 500 shed 0.1%, widening its weekly decline to 1.2%, while small cap stocks endured more aggressive selling with the Russell 2000 losing 0.7% to end the week lower by 2.5%.

Equity indices held modest gains at the start after the Nonfarm Payrolls report for June missed estimates (223,000; Briefing.com consensus 230,000) with the wage component showing no monthly growth. The lack of wage growth was viewed as an argument in favor of the Federal Reserve delaying its first rate hike, evidenced by a surge in the Treasury market. The 10-yr note backed away from its high ahead of the close, but still ended firmly in the green with the benchmark yield slipping four basis points to 2.38%.

Despite opening on a higher note, stocks retreated from their early levels, turning negative during late morning action. Interestingly, the benchmark index slipped below its flat line after the International Monetary Fund admitted that Greece will need approximately EUR50 billion in funds over the next three years and that a 20-year grace period should take place before any repayment begins. The comments from the IMF are likely to galvanize the 'no' camp ahead of Sunday's referendum in Greece.

Six sectors ended the day in negative territory while energy (+0.4%), technology (+0.2%), telecom services (+0.3%), and utilities (+1.4%) posted gains. The utilities sector held the lead throughout the session thanks to the morning drop in Treasury yields. The rate-sensitive sector was the only group that ended the week in the green, adding 1.1% since last Friday.

For its part, the energy sector was able to end in the green even as crude oil surrendered its intraday gain, ending the pit session unchanged at $56.93/bbl. For the week, WTI crude surrendered 4.5% while the energy sector lost 1.9%.

Elsewhere among cyclical groups, the technology sector (+0.2%) struggled early on, but the group rallied into the close, lifting the benchmark index off its session low. Chipmakers led the afternoon rebound with the PHLX Semiconductor Index adding 0.5%.

There wasn't much in the way of corporate news today, but Health Net (HNT 71.57, +6.51) jumped 10.0% after agreeing to be acquired by Centene (CNC 74.44, -6.46) for roughly $78.57/share in cash and stock, which represents a 21.0% premium to Wednesday's closing price. Meanwhile, the broader health care sector (-0.3%) ended among the laggards while biotech names finished little changed with iShares Nasdaq Biotechnology ETF (IBB 370.17, +0.27) adding 0.1%.

Today's trading volume was well below average with roughly 700 million shares changing hands at the NYSE floor.

Economic data included Nonfarm Payrolls, Initial Claims, and Factory Orders:

Nonfarm payrolls added 223,000 jobs in June after adding a downwardly revised 254,000 (from 280,000) in May while the Briefing.com consensus expected an increase of 230,000

Government payrolls were flat, and the entire increase in payrolls came from the private sector as private payrolls increased by 223,000 while the consensus expected an increase of 225,000

Although the payroll data was not far from expectations, the details of the report highlight extreme weaknesses as average workweek and hourly earnings were both flat in June

Total aggregate earnings increased a minuscule 0.1% in June, down from a 0.5% gain in May

The unemployment rate fell to 5.3% in June from 5.5% while the consensus expected a decline to 5.4%; however, the entire decrease was due to a decline in labor force participation as opposed to employment growth

The initial claims level increased to 281,000 for the week ending June 27 from an unrevised 271,000 while the Briefing.com consensus expected an increase to 271,000

Despite the big increase, the four-week moving average increased by only 1,000 to 275,000, leaving the overall trend near a 15-year low

Factory orders declined 1.0% in May following a downwardly revised -0.7% (from -0.4%) decline in April while the Briefing.com consensus expected a decline of 0.5%

Durable goods orders declined 2.2% in May, which was revised down from a 1.8% decline in the advance report

The entire decline resulted from continued weakness in the transportation sector with those orders declining 6.5% in May after falling 4.0% in April

Monday's data will be limited to the 10:00 ET release of the ISM Services Index for June.

Nasdaq Composite +5.8% YTD

Russell 2000 +3.6% YTD

S&P 500 +0.8% YTD

Dow Jones Industrial Average -0.5% YTD

Week in Review: All Eyes on Greek Referendum

On Monday, global markets were shaken after Greek leaders said 'no' to the Eurogroup's cash-for-reform proposal and investors around the world in turn said 'no' to buying stocks. Just about every major market closed down at least 2.0%. The hardest-hit markets were the European bourses, which included Germany's DAX Index (-3.6%) and Spain's IBEX (-4.6%). Japan's Nikkei dropped 2.9% while China's Shanghai Composite fell 3.3% despite the People's Bank of China cutting its benchmark lending and deposit rates by 25 basis points each to 4.85% and 2.00%, respectively. In comparison, the U.S. stock market fared reasonably well, yet that doesn't mean it did well. Hit with broad-based selling pressure, the S&P 500 declined 2.1% as buyers basically wanted no part of the day's action outside a few areas of specific interest. One area was the utilities sector (-0.6%), which traded with a modest gain for most of the day before ultimately feeling the gravitational pull of the weak market. Another area was the Treasury market, which attracted safe-haven flows. The 10-yr note surged more than a point and saw its yield drop 15 basis points to 2.33%.

On Tuesday, the stock market ended the final June session on a higher note, but that did not stop the S&P 500 (+0.3%) from registering a 2.1% loss for the month. Equity indices spent the first three hours of the day in a steady retreat from their opening highs with the S&P 500 making a momentary appearance in the red after German Chancellor Angela Merkel said that Germany cannot consider new proposals from Greece until after Sunday's referendum. However, the benchmark index climbed to a fresh high during afternoon action with the move taking place amid reports Greece could cancel its Sunday referendum if negotiations are resumed and an agreement could be reached on required prior actions. To that point, Eurogroup Chief Jeroen Dijsselbloem acknowledged the receipt of a new proposal from the Greek government with the offer set to be reviewed at tomorrow's Eurogroup meeting. The speculation about a potential cancellation of the referendum had little impact on the euro, which spent the afternoon near its session low reached after Ms. Merkel's comments. The single currency slid 0.6% against the dollar to 1.1145.

The major averages spent the Wednesday session in a slow retreat from their opening highs, but they were able to keep more than half of their opening gains. The S&P 500 climbed 0.7% while the Nasdaq Composite (+0.5%) underperformed. Equities surged out of the gate amid reports from Europe indicating Greece is now ready to accept all conditions in order to secure a bailout. The report sparked a rush to risk assets, but the Greek offer was met with a cool reception from Eurozone leaders. Most notably, Germany's Chancellor Angela Merkel reiterated that talks will not resume until after Sunday's referendum, adding that "a compromise at any price" is not worthwhile. Similarly, Eurogroup Chief Jeroen Dijsselbloem said he does not see the need for a resumption of talks ahead of Sunday's referendum. Despite charging at the start, stocks began inching away from their highs about 30 minutes into the session after Greek Prime Minister Alexis Tsipras reiterated his call for a 'no' vote during Sunday's referendum. A small pullback ensued as Mr. Tsipras' comments cast doubt on earlier speculation that the referendum could be cancelled altogether.

3:40 pm: [BRIEFING.COM]

The dollar index remained in the red this afternoon, which helped out a handful of commodities

WTI crude oil futures was not one of them

WTI finished today's pit trading session one cent lower at $56.93/barrel, selling off from its HoD of $57.95/barrel

Crude continued to sell off in afternoon trade and just hit a new low for today near the $56.50/barrel area

Aug natural gas closed $0.04 higher at $2.82/MMBtu and remained in positive territory all day

Aug gold lost $5.08 today to $1163.40/oz, while Sept silver closed $0.01 lower at $15.56/oz

Sept copper ended unchanged at $2.63/lb

2:55 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.3% with one hour remaining in the session. The benchmark index held a slim gain at the start, but relative weakness among influential sectors like consumer discretionary (-0.3%), financials (-0.6%), and health care (-0.4%) have forced the index below its flat line.

Above all, it is worth noting that today's participation has been very limited, which is not all that surprising with a three-day weekend approaching. As a result, only 400 million shares have changed hands at the NYSE floor while Nasdaq volume has yet to cross the one billion mark.

2:25 pm: [BRIEFING.COM] Not much change in the market with the S&P 500 (-0.3%) holding a six-point loss. The benchmark index dipped into negative territory around 11:00 ET and has been inching lower since then.

The S&P 500 is on course to end the week lower by 1.4% while nine sectors are tracking weekly losses between 0.7% (consumer staples) and 2.7% (materials). Conversely, the utilities sector (+1.1%) trades higher by 0.9% for the week thanks to today's outperformance.

Elsewhere, Treasuries remain near their highs heading into the home stretch. The benchmark 10-yr yield is lower by four basis points at 2.38% today and down 10 basis points since last Friday.

1:55 pm: [BRIEFING.COM] The major averages remain near their session lows.

Improvements in the employment sector remain hard to come by.

Nonfarm payrolls added 223,000 jobs in June after adding adding a downwardly revised 254,000 (from 280,000) in May. The Briefing.com Consensus expected nonfarm payrolls to increase by 230,000 jobs.

Government payrolls were flat, and the entire increase in payrolls came from the private sector. Private payrolls increased by 223,000 after adding a downwardly revised 250,000 (from 262,000) in May. The consensus expected private payrolls to increase by 225,000.

While the payroll data nearly matched expectations, the details of the employment report highlight extreme weaknesses.

Both the average workweek and hourly earnings were flat in June. Total aggregate earnings increased a minuscule 0.2% in June, down from a 0.5% gain in May.

Any sizable gain in consumption will have to come from consumers dipping into their savings. There simply was not enough income growth to sustain May spending trends.

Income growth was also not strong enough to support any type of acceleration in core inflation.

1:30 pm: [BRIEFING.COM] The major indices continue to experience selling pressure as they rest near their session lows.

A look inside the Dow Jones Industrial Average shows DuPont (DD 60.14, -1.29), UnitedHealth Group (121.50, -1.88), and United Technologies (109.47, -1.35) are underperforming. Dupont is the weakest Dow component after its price target was lowered at two separate analyst agencies following the completion of its Chemours (CC 16.30, -0.21) spin-off.

Conversely, Intel (INTC 30.58, +0.40) is the best-performing Dow component amid relative strength in semiconductors.

Ahead of the holiday weekend, the DJIA is currently down 1.4% for the week.

12:55 pm: [BRIEFING.COM] The major averages hover near their lows at midday with the Dow (-0.3%) and S&P 500 (-0.3%) trading a little ahead of the Nasdaq Composite (-0.4%).

Equity indices began the day on an upbeat note after the Nonfarm Payrolls report for June missed estimates (223,000; Briefing.com consensus 230,000) with the wage component showing no monthly growth. The lack of wage growth was viewed as an argument in favor of the Federal Reserve delaying its first rate hike, evidenced by a surge in the Treasury market. The 10-yr note remains near its best level of the day with the benchmark yield down six basis points at 2.37%.

Meanwhile, stocks began the day with gains, but the first half has featured a slow and steady retreat from opening highs. The benchmark index slipped below its flat line after the International Monetary Fund admitted that Greece will need approximately EUR50 billion in funds over the next three years and that a 20-year grace period should take place before any repayment begins. The comments from the IMF are likely to galvanize the 'no' camp ahead of Sunday's referendum in Greece.

Only three sectors remain in positive territory with the rate-sensitive utilities sector (+1.1%) holding the lead thanks to today's decline in Treasury yields. Similarly, the telecom services sector (+0.4%) also trades in the green while the heavily-weighted health care space (-0.4%) has struggled to keep pace with the market. Interestingly, biotechnology was among the early laggards, but iShares Nasdaq Biotechnology ETF (IBB 369.28, -0.62) has narrowed its decline to 0.2%.

Over on the cyclical side, the technology sector (-0.2%) trades near the broader market while consumer discretionary (-0.4%) and financials (-0.6%) are keeping the market under pressure. On the upside, the energy sector trades higher by 0.5% thanks to crude oil, which has climbed 0.9% to $57.48/bbl after tumbling 4.2% yesterday.

Today has been very quiet on the corporate front, but it is worth noting that Health Net (HNT 72.08, +7.02) has spiked 10.8% after agreeing to be acquired by Centene (CNC 76.08, -4.82) for roughly $78.57/share in cash and stock, representing a 21.0% premium to yesterday's closing price.

Economic data included Nonfarm Payrolls, Initial Claims, and Factory Orders:

Nonfarm payrolls added 223,000 jobs in June after adding a downwardly revised 254,000 (from 280,000) in May while the Briefing.com consensus expected an increase of 230,000

Government payrolls were flat, and the entire increase in payrolls came from the private sector as private payrolls increased by 223,000 while the consensus expected an increase of 225,000

Although the payroll data was not far from expectations, the details of the report highlight extreme weaknesses as average workweek and hourly earnings were both flat in June

Total aggregate earnings increased a minuscule 0.1% in June, down from a 0.5% gain in May

The unemployment rate fell to 5.3% in June from 5.5% while the consensus expected a decline to 5.4%; however, the entire decrease was due to a decline in labor force participation as opposed to employment growth

The initial claims level increased to 281,000 for the week ending June 27 from an unrevised 271,000 while the Briefing.com consensus expected an increase to 271,000

Despite the big increase, the four-week moving average increased by only 1,000 to 275,000, leaving the overall trend near a 15-year low

Factory orders declined 1.0% in May following a downwardly revised -0.7% (from -0.4%) decline in April while the Briefing.com consensus expected a decline of 0.5%

Durable goods orders declined 2.2% in May, which was revised down from a 1.8% decline in the advance report

The entire decline resulted from continued weakness in the transportation sector with those orders declining 6.5% in May after falling 4.0% in April

12:25 pm: [BRIEFING.COM] Equity indices continue holding modest losses with the S&P 500 (-0.3%) trading just ahead of the Nasdaq Composite (-0.4%) and well ahead of the Russell 2000 (-0.9%).

Broadly speaking, countercyclical sectors continue trading ahead of their growth-sensitive counterparts, but that is a small victory considering just about every sector has backed away from its session high. That being said, the utilities space (+1.4%) remains not far below its best level of the day, but the sector has little impact on the broader market since it represents just 3.0% of the S&P 500.

Meanwhile, the top-weighted technology sector (-0.3%) is keeping pace with the benchmark index while financials (-0.5%) and health care (-0.4%) continue showing relative weakness.

Related Quotes

11:55 am: [BRIEFING.COM] Not much change in the market with participants showing little willingness to step into the fold. The S&P 500 (-0.1%) remains just below its flat line with five of six cyclical sectors showing losses.

The materials sector (-1.0%) has lagged since the start and the group remains behind other growth-sensitive sectors. On the upside, the energy sector (+0.5%) trades ahead of most other groups thanks to a 1.2% increase in crude oil, which currently hovers near $57.66/bbl.

In all likelihood, today's session will produce below-average trading volume considering only 240 million shares have changed hands at the NYSE floor so far. As for market breadth, it is essentially even with one stock trading in the green for each decliner.

Elsewhere, Treasuries remain bid with the 10-yr yield down five basis points at 2.38%.

11:25 am: [BRIEFING.COM] The major averages have marked new lows for the day with the Nasdaq Composite now down 0.3%.

The tech-heavy index underperforms amid relative weakness in biotechnology, evidenced by a 0.4% decline in iShares Nasdaq Biotechnology ETF (IBB 368.35, -1.55). Furthermore, large cap technology components like Apple (AAPL 125.95, -0.65), Microsoft (MSFT 44.18, -0.27), and MasterCard (MA 94.14, -0.36) trade with losses between 0.4% and 0.6% while the broader tech sector is lower by 0.1%.

Given its current level, the S&P is on track to end the week lower by 1.3% while the tech-heavy Nasdaq has surrendered 1.6%. Also of note, recent underperformance among small cap names has the Russell 2000 trading lower by 0.6% today and down 2.4% for the week.

10:55 am: [BRIEFING.COM] Recent action saw the S&P 500 return to its flat line as heavily-weighted sectors like technology (unch), health care (-0.3%), and financials (-0.3%) underperform. Furthermore, the consumer discretionary sector (-0.2%) was among the early leaders, but the group now trades in the red, leaving industrials (+0.1%) and energy (+0.7%) as the only two cyclical sectors trading in the green.

Things look a bit better on the countercyclical side with consumer staples (+0.4%), telecom services (+0.7%), and utilities (+1.4%) trading ahead of the broader market.

Elsewhere, Treasuries remain not far below their best levels of the session with the 10-yr yield down four basis points at 2.38%.

10:40 am: [BRIEFING.COM]

The dollar hovered near unchanged from last session in early trading, prior to the morning's release of US unemployment and jobs data

Upon release of the data, which showed higher unemployment claims and lower non-farm payroll figures, the index sold off sharply.

The dollar's weakness has since extended, and given support to crude oil, precious metals and copper. The index is now -0.3% to 96.01

Crude oil was slightly positive in early trade, finding support near the flat line, ahead of the US data release and following yesterday's inventory figures

WTI rallied strong as the dollar weakened upon this morning's data release, and is still extending those gains, nearing its HoD at +1.4% to $57.73/barrel

Natural gas was strongly positive early, with highs near $2.84/MMBtu as the market expected the morning's inventory data to show more modest stockpile additions

EIA nat gas inventory data showed a modest build, which caused a rally in nat gas prices, that are now +2.7% at $2.86/MMBtu

August copper lifted on a weaker dollar/US factory data, which in combination with market sentiment toward economic stabilization in China, has the commodity +0.4% to $2.64/lb

Precious metals saw support from the dollar index, with August gold -0.5% to $1163.80/oz and August silver +0.4% to $15.64/oz

10:00 am: [BRIEFING.COM] The S&P 500 trades higher by 0.2% with eight sectors remaining in the green.

It is worth noting that the top-weighted countercyclical sector-health care-has dipped into the red while another influential group-financials-hovers just above its flat line. Those two sectors, alongside with technology (+0.2%), deserve close attention as their performance can dictate the overall direction of the market.

According to the just-released Factory Orders report for May, orders decreased 1.0% while the Briefing.com consensus expected a decline of 0.5%.

9:40 am: [BRIEFING.COM] As expected, the major averages began the day with gains. The Dow, Nasdaq, and S&P 500 are all up near 0.3% apiece in the early going with nine sectors displaying opening gains.

The rate-sensitive utilities sector (+1.3%) has seized the lead thanks to today's drop in Treasury yields (10-yr -5 bps to 2.37%). Meanwhile, the remaining advancers hold gains slimmer than 1.0%. The heavily-weighted consumer discretionary sector (+0.4%) trades ahead of other cyclical groups while the materials sector (-0.5%) represents the lone decliner at this juncture.

The Factory Orders report for May (consensus -0.5%) will be released at 10:00 ET.

9:10 am: [BRIEFING.COM] S&P futures vs fair value: +6.50. Nasdaq futures vs fair value: +12.80. The stock market is on track for a higher open as futures on the S&P 500 trade seven points above fair value.

Index futures held modest gains through the bulk of the night, climbing to highs during the past 45 minutes after the Nonfarm Payrolls report crossed the wires. According to the report, payrolls increased by 223,000 in June, which was below the Briefing.com consensus of 230,000. Furthermore, the Unemployment Rate dropped to 5.3% from 5.5%, but that was a result of a large exodus from the labor force. As a result, the participation rate has dropped to its lowest level since October 1977.

Also of note, hourly earnings were unchanged while the consensus expected an increase of 0.2%. In all likelihood, this is why equity futures jumped to highs as the lack of wage growth makes the Federal Reserve less likely to begin hiking rates in the near term.

Treasuries surged off their lows in reaction to the report with the benchmark 10-yr yield now down four basis points at 2.38%.

The Factory Orders report for May (consensus -0.5%) will be released at 10:00 ET.

8:53 am: [BRIEFING.COM] S&P futures vs fair value: +7.80. Nasdaq futures vs fair value: +16.90. The S&P 500 futures trade eight points above fair value.

Markets in the Asia-Pacific region ended the day on a mostly higher note while China's Shanghai Composite (-3.5%) remained pressured. Meanwhile, China Securities Journal called on the People's Bank of China to focus on stock volatility and inject liquidity "when stock prices fall." Separate reports indicate the Shanghai Exchange could allow the use of real estate as collateral in margin calls.

In economic data:

Japan's Monetary Base +34.2% year-over-year (expected 36.2%; prior 35.6%)

Australia's May trade deficit narrowed to AUD2.75 billion from AUD4.14 billion (expected deficit of AUD2.20 billion) as exports rose 1.0% month-over-month (last -6.0%) while imports fell 4.0% (prior 4.0%)

New Zealand's ANZ Commodity Price Index -3.1% month-over-month (last -4.9%)

------

Japan's Nikkei increased 1.0% on broad-based gains that were led by the Health Care (+2.2%), Consumer Discretionary (+1.8%), Financials (+1.8%). Individual standouts included Sharp (+8.6%) and Shinsei Bank (+2.8%).

Hong Kong's Hang Seng increased just 0.1% today. Galaxy Entertainment was a notable mover, rising 13.2% after the latest Macau gaming figures were released. Likewise, gaming peer Sands China posted a 12.1% gain.

China's Shanghai Composite declined 3.5% to close the weak. Financials bucked the broader market trend, after being notable laggards yesterday. Ind & Comm Bank of China rose 5.8%, while China Construction Bank gained 3.9% today.

Major European indices trade near their flat lines while Italy's MIB (-0.6%) underperforms. Elsewhere, Greek Finance Minister Yanis Varoufakis announced plans to resign in the event of a 'yes' vote in Sunday's referendum, saying he would "cut his arm off" rather than sign a deal without debt restructuring.

Participants received several data points:

Eurozone May PPI 0.0% month-over-month (expected 0.1%; prior -0.1%); -2.0% year-over-year, as expected

UK's June Nationwide HPI -0.2% month-over-month (consensus 0.5%; prior 0.2%); +3.3% year-over-year (last 4.3%; prior 4.6%). Separately, June Construction PMI rose to 58.1 from 55.9 (expected 56.5)

Spain's Unemployment Change -94,700 (expected -124,000; prior -118,000)

------

UK's FTSE trades higher by 0.4% with miners and utilities showing relative strength. BHP Billiton, Rio Tinto, Centrica, and National Grid are up between 1.2% and 1.7%. Consumer names underperform with Burberry, Coca-Cola HBC, and Intertek down between 1.7% and 2.6%.

France's CAC trades flat. Utility stocks like Electricite de France, GDF Suez, and Veolia Environnement are up between 2.0% and 2.5% while Unibail-Rodamco is the weakest performer, down 2.4%. Other financials hold slimmer losses with Credit Agricole and Societe Generale down 0.6% and 0.3%, respectively.

Germany's DAX is higher by 0.1%. Similar to UK and France, utilities trade well ahead of other index components with RWE and E.On showing respective gains of 6.2% and 3.8%. On the downside, K+S has given up 1.2% after rejecting a takeover offer from Potash.

Italy's MIB underperforms with a loss of 0.6% amid weakness in financials. Banca di Milano Scarl, UBI Banca, BMPS, and Banco Popolare are down between 0.9% and 1.6%.

8:35 am: [BRIEFING.COM] S&P futures vs fair value: +6.70. Nasdaq futures vs fair value: +15.80. The S&P 500 futures trade seven points above fair value.

June nonfarm payrolls came in at 223,000 while the Briefing.com consensus expected a reading of 230,000. The prior month's reading was revised down to 254,000 from 280,000. Nonfarm private payrolls also added 223,000 against the 225,000 expected by the consensus. The unemployment rate fell to 5.3% while the Briefing.com consensus expected the rate to decline to 5.4%.

Hourly earnings were unchanged while the consensus expected growth of 0.2%. The average workweek was reported at 34.5, which is what the consensus expected.

Separately, the latest weekly initial jobless claims count totaled 281,000 while the Briefing.com consensus expected a reading of 273,000. Today's tally was above the unrevised prior week count of 271,000. As for continuing claims, they rose to 2.264 million from 2.249 million.

7:57 am: [BRIEFING.COM] S&P futures vs fair value: +6.00. Nasdaq futures vs fair value: +11.40. U.S. equity futures trade modestly higher amid cautious action overseas. The S&P 500 futures hover six points above fair value, but some volatility is expected around 8:30 ET when the Nonfarm Payrolls report for June crosses the wires. The Briefing.com consensus expected the report to indicate the addition of 230,000 payrolls while the Unemployment Rate is expected to tick down to 5.4% from 5.5%.

Treasuries hover in the red with the 10-yr yield higher by three basis points at 2.45%.

In addition to Nonfarm Payrolls, weekly Initial Claims (consensus 273K) will also be reported at 8:30 ET while the Factory Orders report for May (consensus -0.5%) will be released at 10:00 ET.

In U.S. corporate news of note:

AT&T (T 35.86, +0.29): +0.8% after Cowen upgraded the stock to 'Outperform' from 'Market Perform.'

Health Net (HNT 76.99, +11.93): +18.3% after agreeing to be acquired by Centene (CNC 86.64, +5.74) for roughly $78.57/share in cash and stock, representing a 21.0% premium to yesterday's closing price.

Reviewing overnight developments:

Asian markets ended mixed. China's Shanghai Composite -3.5%, Hong Kong's Hang Seng +0.1%, and Japan's Nikkei +1.0%

In economic data:

Japan's Monetary Base +34.2% year-over-year (expected 36.2%; prior 35.6%)

Australia's May trade deficit narrowed to AUD2.75 billion from AUD4.14 billion (expected deficit of AUD2.20 billion) as exports rose 1.0% month-over-month (last -6.0%) while imports fell 4.0% (prior 4.0%)

New Zealand's ANZ Commodity Price Index -3.1% month-over-month (last -4.9%)

In news:

China Securities Journal called on the People's Bank of China to focus on stock volatility and inject liquidity "when stock prices fall." Separate reports indicate the Shanghai Exchange could allow the use of real estate as collateral in margin calls.

Major European indices trade near their flat lines. UK's FTSE +0.2%, France's CAC -0.1%, and Germany's DAX is flat. Elsewhere, Italy's MIB -0.4% and Spain's IBEX -0.1%

Participants received several data points:

Eurozone May PPI 0.0% month-over-month (expected 0.1%; prior -0.1%); -2.0% year-over-year, as expected

UK's June Nationwide HPI -0.2% month-over-month (consensus 0.5%; prior 0.2%); +3.3% year-over-year (last 4.3%; prior 4.6%). Separately, June Construction PMI rose to 58.1 from 55.9 (expected 56.5)

Spain's Unemployment Change -94,700 (expected -124,000; prior -118,000)

In news:

Greek Finance Minister Yanis Varoufakis announced plans to resign in the event of a 'yes' vote in Sunday's referendum, saying he would "cut his arm off" rather than sign a deal without debt restructuring

5:51 am: [BRIEFING.COM] S&P futures vs fair value: +4.00. Nasdaq futures vs fair value: +8.60.

5:51 am: [BRIEFING.COM] Nikkei...20522.50...+193.20...+1.00%. Hang Seng...26282.32...+32.30...+0.10%.

5:51 am: [BRIEFING.COM] FTSE...6608.43...-0.20...0.00%. DAX...11178...-2.50...0.00%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

wrbanalysis@gmail.com Go Back To TheStrategyLab.com Homepage