Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

041315-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4375.00.png [ 88.69 KiB | Viewed 299 times ]

041315-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+4375.00.png [ 88.69 KiB | Viewed 299 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$150.00 dollars or +1.50 points, Emini ES ($ES_F) futures @

$4,375.00 dollars or +87.50 points, Light Crude Oil CL ($CL_F) futures @

($150.00) dollars or -0.15 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $4,375.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=142&t=2050 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=261&t=2728 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

Attachment:

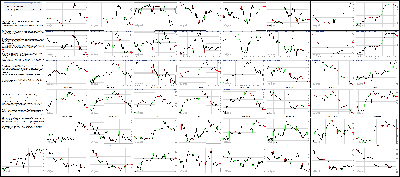

041315-Key-Price-Action-Markets.png [ 1.07 MiB | Viewed 364 times ]

041315-Key-Price-Action-Markets.png [ 1.07 MiB | Viewed 364 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The major averages began the new trading week on a lower note. The S&P 500 surrendered 0.5% after spending the day in a steady retreat from its opening high while the Nasdaq Composite shed 0.2% after showing relative strength throughout the day.

All in all, the Monday session was very quiet with the S&P 500 spending the day inside a 15-point range. Investors did not receive any noteworthy data or earnings, but that will change as the week wears on.

Today, however, the S&P 500 appeared to be on track for its fourth consecutive advance, but the index hit resistance during the opening hour and retreated into the afternoon. A handful of heavily-weighted sectors displayed early strength, but the financial sector (+0.3%) was the only group left in the green when the session ended.

Elsewhere, the top-weighted technology sector (-0.3%) ended ahead of the broader market, but could not avoid turning negative. Large cap names like Apple (AAPL 126.85, -0.25), Google (GOOGL 548.64, +0.10), and Microsoft (MSFT 41.76, +0.04) held up well while chipmakers struggled with the PHLX Semiconductor Index losing 0.6%.

Still, the relative strength in the technology sector helped the Nasdaq spend the day ahead of the S&P 500. The index also drew support from biotechnology with the iShares Nasdaq Biotechnology ETF (IBB 358.32, +0.88) adding 0.2%. The biotech ETF registered its sixth consecutive gain after being up more than 1.0% in the early going. Conversely, the health care sector (-0.6%) ended among the laggards despite showing relative strength early.

Similar to health care, two other countercyclical sectors-consumer staples (-0.5%) and utilities (-1.0%)-underperformed while telecom services shed 0.2%.

Moving back to the cyclical side, the energy sector contributed to the early strength, but reversed to end lower by 0.8% even as crude oil settled higher by 0.5% at $51.91/bbl after testing the $53.00/bbl level.

Also of note, industrials (-1.1%) settled behind the remaining nine sectors as General Electric (GE 27.63, -0.88) weighed. The largest sector component fell 3.1% after spiking 10.8% on Friday.

Treasuries registered modest gains after climbing off their overnight lows. The 10-yr note ended on its high with the benchmark yield down two basis points at 1.93%.

Today's participation matched recent averages with more than 650 million shares changing hands at the NYSE floor.

Economic data was limited to the Treasury Budget statement for March, which showed a deficit of $53.00 billion (Briefing.com consensus -$44.00 billion). The Treasury data are not seasonally adjusted, so the March deficit cannot be compared to the $36.90 billion deficit recorded in February.

Tomorrow, the March Retail Sales report (Briefing.com consensus 1.0%) and March PPI (consensus 0.2%) will be released at 8:30 ET while February Business Inventories (consensus 0.3%) will be reported at 10:00 ET.

Nasdaq Composite +5.3% YTD

Russell 2000 +5.1% YTD

S&P 500 +1.6% YTD

Dow Jones Industrial Average +0.9% YTD

3:35 pm: [BRIEFING.COM]

The dollar index held modest gains in afternoon trade, which helped weigh on select commodities, such as gold and silver.

Both of these precious metals remain in negative territory this afternoon, ending floor trading with modest losses.

Wheat futures declined as well, but fell largely due to rain in key crop regions, which helps supply prospects.

At the end of today's pit trading session, May wheat lost 5% to $5.03/bushel.

WTI crude oil pulled back from overnight highs just above $53/barrel, closing the day out $0.28 higher at $51.92/barrel

2:55 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.3% with one hour remaining in the session. The benchmark index drifted near its opening high through the first two hours of action, but dipped into negative territory shortly after noon ET. That being said, the index has spent the day within a 12-point range.

Eight sectors continue holding losses going into the home stretch with industrials (-0.9%) at the bottom of the leaderboard. The largest sector component by weight-General Electric (GE 27.70, -0.81)-has given up 2.8% while transport stocks are now among the laggards after showing relative strength earlier. The Dow Jones Transportation Average trades lower by 0.4%.

2:25 pm: [BRIEFING.COM] Equity indices remain near their session lows with the Dow (-0.2%) and S&P 500 (-0.2%) trading behind the Nasdaq Composite (unch).

With stocks on their lows, eight sectors trade in negative territory while financials (+0.5%) and telecom services (+0.3%) continue holding gains. Notably, the financial sector has extended its April gain to 1.1% with several major components scheduled to report their results this week. JPMorgan Chase (JPM 62.21, +0.51) and Wells Fargo (WFC 54.62, +0.30) are both set to report tomorrow morning while Bank of America (BAC 15.81, +0.09) and U.S. Bancorp (USB 44.08, +0.33) will announce their results on Wednesday morning.

Elsewhere, Treasuries remain on their highs with the 10-yr yield down two basis points at 1.93%.

2:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.2%.

The Treasury Budget statement for March was just released and it showed a deficit of $53.00 billion (Briefing.com consensus -$44.00 billion). The Treasury data are not seasonally adjusted, so the March deficit cannot be compared to the $36.90 billion deficit recorded in February.

1:25 pm: [BRIEFING.COM] It's a mixed market at the moment as the major indices have backtracked from larger gains seen earlier in the session. The retreat has been pushed in part by some profit-taking following some big gains last week that stirred concerns with the early rally effort about a near-term overbought condition.

Additionally, some reservations may be kicking in with the rush of the first quarter reporting period set to begin this week with a slate of results from the influential financial and technology sectors. The latest report from S&P Capital IQ indicates first quarter earnings per share are expected to decline 3.2% year-over-year.

JPMorgan Chase (JPM 62.17, +0.47), Wells Fargo (WFC 54.55, +0.23), and Johnson & Johnson (JNJ 100.86, -1.20) will get things rolling before the open on Tuesday. At the same time, market participants will be forced to digest the latest readings for the Retail Sales and Producer Price Index reports for March.

Accordingly, there shouldn't be a shortage of headlines on which to trade come Tuesday.

12:55 pm: [BRIEFING.COM] The major averages are mixed at midday after retreating from their early highs. The Nasdaq (+0.3%) has shown relative strength since the start while the S&P 500 hovers just below its flat line.

Equity indices have begun the trading week on an unassuming note, hitting their session highs during the opening hour. Since then, the S&P 500 has slowly dripped back to its flat line while the Nasdaq has been supported by large cap tech names like Apple (AAPL 127.37, +0.27), Google (GOOGL 551.68, +3.14), and Microsoft (MSFT 41.96, +0.24). The three heavyweights are up between 0.2% and 0.6% while the broader technology sector trades higher by 0.3%.

Furthermore, the Nasdaq has received another measure of support from biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 359.97, +2.53) has narrowed its gain to 0.7% after being up more than 1.0%, but the ETF remains on track to register its sixth consecutive advance. For its part, the health care sector (-0.1%) represented an area of early strength, but the heavily-weighted group has slipped behind the broader market.

Elsewhere among influential groups, the financial sector (+0.6%) outperforms with several major components set to report their earnings this week while energy (-0.4%) and industrials (-0.5%) lag.

Notably, the energy sector started in the lead, but the group has slumped to the bottom of the leaderboard amid a pullback in crude oil. Currently, the energy component is higher by 0.8% at $52.02/bbl after testing the unchanged level during the past hour.

Also of note, the industrial sector has retreated due to a 3.0% decline in General Electric (GE 27.65, -0.86) as the stock retraces a portion of its 10.8% surge from Friday. Meanwhile, transport names outperform with the Dow Jones Transportation Average trading higher by 0.2%.

Treasuries have reclaimed their overnight losses and they currently hold slim gains with the 10-yr yield down one basis point at 1.94%.

Investors did not receive any economic data this morning, but the Treasury Budget for March (Briefing.com consensus -$44.00 billion) will be released at 14:00 ET.

12:25 pm: [BRIEFING.COM] Recent action saw the S&P 500 return to its flat line, fueled by a retreat in sectors that had shown strength since the start. To that point, the health care space has dipped below its flat line while technology has narrowed its gain to 0.3%.

Outside of technology, only two other sectors-financials (+0.5%) and telecom services (+0.4%)-remain in the green while the remaining groups display losses of no more than 0.6%.

Unlike the S&P 500, the Nasdaq (+0.4%) continues holding a modest gain thanks to persistent strength in biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 360.00, +2.56) remains higher by 0.7%.

11:55 am: [BRIEFING.COM] Equity indices continue bouncing around narrow ranges with the S&P 500 (+0.1%) having spent the past hour between 2,104 and 2,106. Meanwhile, the Nasdaq Composite (+0.5%) outperforms thanks to the relative strength among large cap tech names and biotechnology.

The iShares Nasdaq Biotechnology ETF (IBB 361.79, +4.34) has extended its gain to 1.2% while another high-beta group-chipmakers-has traded in-line with the S&P 500. The PHLX Semiconductor Index has added 0.1%.

On a separate note, crude oil has surrendered its entire intraday gain and now trades lower by 0.1% at $51.60/bbl. In turn, the energy sector (-0.5%) trades behind the remaining sectors.

11:25 am: [BRIEFING.COM] The major averages remain near their recent levels with the S&P 500 (+0.2%) hovering in the top half of today's trading range.

All in all, heavily-weighted groups have done relatively well so far today with financials (+0.5%), technology (+0.4%), and health care (+0.3%) trading ahead of the broader market. That being said, another influential group-industrials-trails the broader market with a loss of 0.4%.

The industrial sector has been pressured by General Electric (GE 27.78, -0.73), which trades down 2.5% after spiking 10.8% on Friday. In addition, heavy machinery stocks like Caterpillar (CAT 82.18, -0.42) and Joy Global (JOY 38.47, -0.83) also lag while transport names outperform with the Dow Jones Transportation Average higher by 0.3%.

10:55 am: [BRIEFING.COM] Equity indices remain in the green with the S&P 500 trading higher by 0.2%.

The energy sector (-0.5%) was among the early leaders, but the cyclical group has dropped to the bottom of the leaderboard. Meanwhile, crude oil has retreated from its high, but the energy component remains higher by 0.3% at $51.80/bbl.

Elsewhere among cyclical sectors, industrials (-0.2%) also lag while financials (+0.5%) and technology (+0.4%) display relative strength. The technology sector has received support from large cap components with Apple (AAPL 127.90, +0.80), Google (GOOGL 551.94, +3.40), and Microsoft (MSFT 41.88, +0.16) up between 0.4% and 0.6%.

10:35 am: [BRIEFING.COM]

Crude oil futures have been trading higher today so far, which has been driven by several catalysts.

In China, disappointing trade came out overnight, around 3 am ET, which helps gives the idea that further stimulus measures may take place. At the same time, you can say that oil just shrugged off weak Chinese trade data.

Also, CFTC data that came out on Friday was bullish. It showed speculators boosted net future/options oil positions by 52 mln barrels.

Lastly, the IEA noted that following a final Iran nuclear deal, an increase in oil exports may take longer than previously expected. Crude oil is now trading +1% at $52.14/barrel

The dollar index is trading modestly higher this morning, which is helping add selling pressure onto commodities like gold and silver.

June gold is -0.4%, at $1199.40/oz, while May silver is now -0.4% at $16.31/oz

Natural gas rallied this morning and is currently near today's high. May nat gas is now +0.9% at $2.53/MMBtu

May Copper is trading flat at $2.74/lb

9:55 am: [BRIEFING.COM] The major averages have added to their early gains with the Nasdaq trading higher by 0.4%. The tech-heavy index has received support from the technology sector (+0.5%) while biotechnology has also contributed to the strength. The iShares Nasdaq Biotechnology ETF (IBB 360.21, +2.76) trades higher by 0.8%.

Interestingly, the advance in equities has coincided with strength in the Treasury market. The 10-yr note has marked a fresh high with its yield lower by a basis point at 1.94%.

9:40 am: [BRIEFING.COM] Equity indices have climbed off their opening lows with the Nasdaq Composite (+0.4%) holding the early lead. Meanwhile, the S&P 500 (+0.1%) hovers just above its flat line with six sectors showing opening gains.

The energy sector (+0.4%) has claimed the lead while another cyclical sector-technology (+0.3%)-follows right behind. Similarly, health care (+0.3%) and financials (+0.2%) also trade ahead of the broader market.

On the downside, the industrial sector is lower by 0.4% while the remaining decliners sport slimmer losses.

Treasuries remain flat with the 10-yr yield at 1.95%.

9:09 am: [BRIEFING.COM] S&P futures vs fair value: -2.90. Nasdaq futures vs fair value: +1.40. The stock market is on track for a modestly lower open as futures on the S&P 500 trade three points below fair value.

Index futures have maintained narrow ranges through what has been a quiet overnight session. In Asia, China's Shanghai Composite surged 2.2% on hopes for more stimulus after the March trade surplus came in at its lowest level in more than a year ($3.08 billion; expected $45.40 billion).

The Dollar Index (99.63, +0.29) climbed overnight and reached levels last seen in the middle of March, but recent comments from Koichi Hamada, who advises Prime Minister Shinzo Abe gave a boost the yen and pressured the greenback. Specifically, Mr. Hamada said that the current dollar/yen exchange rate of 120 is too high and that a level closer to 105 would be more appropriate.

Elsewhere, Treasuries have recovered their losses and they currently trade little changed with the 10-yr yield at 1.95%.

On the corporate front, Qualcomm (QCOM 72.70, +3.43) has jumped 5.0% in pre-market after the Wall Street Journal reported that activist investor Jana Partners has urged a breakup of the company.

Today's economic data will be limited to the 14:00 ET release of the Treasury Budget for March (Briefing.com consensus -$44.00 billion).

8:54 am: [BRIEFING.COM] S&P futures vs fair value: -4.30. Nasdaq futures vs fair value: -0.30. The S&P 500 futures trade four points below fair value.

Markets in the Asia-Pacific region finished mostly higher on Monday. Hong Kong's Hang Seng Index and China's Shanghai Composite continued their bull runs, rallying 2.7% and 2.2%, respectively in the face of weaker than expected trade data out of China. The latter reportedly left traders inclined to think further policy stimulus will be provided.

In economic data:

China's March Trade Balance $3.08 billion (expected $45.40 billion; prior $60.60 billion) as Exports -15.0% year-over-year (expected +12.0%; prior +48.3%) and Imports -12.7% year-over-year (expected -11.7%; prior -20.5%)

Japan's February Core Machinery Orders -0.4% month-over-month (expected -2.8%; prior -1.7%); +5.9% year-over-year (expected +3.7%; prior +1.9%) while M2 Money Stock +3.6% year-over-year (expected +3.6%; prior +3.5%)

South Korea's March Export Price Index -6.8% year-over-year (prior -8.1%) and March Import Price Index -17.1% year-over-year (prior -17.8%)

------

Japan's Nikkei drifted through Monday's trade and ended basically flat for the session. Gains in the communications (+0.9%) and energy (+0.3%) sectors were offset by weakness in the financial (-0.8%) and consumer non-cyclical (-0.8%) sectors. Nippon Electric Glass Co (+17.7%) and Mitsumi Electric Co (+7.2%) led all gainers while Kikkoman Corp (-3.6%) and Tokyo Gas Co (-3.5%) paced the losers. Out of the 225 index members 95 finished higher, 118 ended lower, and 12 were unchanged.

Hong Kong's Hang Seng surged another 2.7% and closed at its high for the session. The Hang Seng has soared a little over 3500 points, or 14.4%, over its last eight trading sessions with mainland investors helping to power the move. Monday's advance was led by the financial (+4.5%) sector. Hong Kong Exchanges and Clearing (+19.4%), Kunlun Energy Corp (+11.5%), Bank of China (+8.6%), and China Construction Bank (+7.8%) topped the list of winners. Out of the 50 index members, 30 ended higher, 15 closed lower, and 5 were unchanged.

China's Shanghai Composite jumped 2.2% in the wake of weaker than expected trade data for March, which fueled a trade based on the notion that further policy stimulus will be provided. The consumer non-cyclical (+2.5%) and industrial (+2.4%) sectors led the Chinese market. Over its last eight trading session, the Shanghai Composite has tacked on 374 points or 10%.

Major European indices trade in mixed fashion with Spain's IBEX (+0.6%) showing relative strength. Elsewhere, Germany's FAZ has reported that Greece has to prepare a list of reforms by April 20 in order to receive the next installment of EU bailout funds.

Economic data was limited:

French Current Account deficit widened to EUR1.80 billion from EUR300 million (expected deficit of EUR1.20 billion)

Italy's February Industrial Production +0.6% month-over-month (expected 0.5%; prior -0.7%); -0.2% year-over-year (consensus -1.3%; last -2.2%)

------

UK's FTSE is lower by 0.5% with miners and homebuilders on the defensive. Anglo American, Antofagasta, and BHP Billiton are all down near 3.0% while Barratt Developments and Taylor Wimpey trade lower by 3.0% and 2.2%, respectively.

Germany's DAX has given up 0.2% with Volkswagen trading lower by 1.2%. On the upside, financials outperform with Commerzbank and Deutsche Bank showing respective gains of 0.6% and 0.4%.

In France, the CAC trades flat. Growth-sensitive names lag with ArcelorMittal, Valeo, and Solvay all down near 0.9%. Telecom listings outperform with Alcatel-Lucent and Orange up 3.3% and 1.1%, respectively.

Spain's IBEX has added 0.6% with help from financials. Santander, BBVA, and Bankinter are up between 0.4% and 1.2%.

8:25 am: [BRIEFING.COM] S&P futures vs fair value: -3.50. Nasdaq futures vs fair value: -0.20. U.S. equity futures continue holding modest losses with S&P 500 futures four points below fair value.

Elsewhere, the Dollar Index (99.70, +0.36) is higher by 0.4% as it hovers just below its March high that was established on March 13. The index experienced a 4.0% pullback over the next couple weeks, but has come charging back in recent days.

Today, the dollar has added about 0.3% against the euro, pressuring the single currency to 1.0555.

7:55 am: [BRIEFING.COM] S&P futures vs fair value: -3.50. Nasdaq futures vs fair value: -0.90. U.S. equity futures trade modestly lower amid mixed action overseas. The S&P 500 futures hover four points below fair value after spending the night within a six-point range.

The new trading week has gotten off to a relatively quiet start with the dollar building on last week's strength. As a result, the Dollar Index (99.78, +0.44) hovers just below its best level from March.

Today's economic data will be limited to the 14:00 ET release of the Treasury Budget for March (Briefing.com consensus -$44.00 billion).

Treasuries hover near their lows with the 10-yr yield higher by three basis points at 1.98%.

In U.S. corporate news of note:

Netflix (NFLX 462.50, +7.93): +1.7% in reaction to a UBS upgrade to 'Buy' from 'Neutral.'

Qualcomm (QCOM 72.50, +3.34): +4.8% after the Wall Street Journal reported that activist investor Jana Partners has urged a breakup of the company.

UnitedHealth (UNH 121.30, +2.30): +1.9% after Jefferies upgraded the stock to 'Buy' from 'Hold.'

Reviewing overnight developments:

Asian markets ended mostly higher. China's Shanghai Composite +2.2%, Hong Kong's Hang Seng +2.7%, and Japan's Nikkei settled flat

In economic data:

China's March Trade Balance $3.08 billion (expected $45.40 billion; prior $60.60 billion) as Exports -15.0% year-over-year (expected +12.0%; prior +48.3%) and Imports -12.7% year-over-year (expected -11.7%; prior -20.5%)

Japan's February Core Machinery Orders -0.4% month-over-month (expected -2.8%; prior -1.7%); +5.9% year-over-year (expected +3.7%; prior +1.9%) while M2 Money Stock +3.6% year-over-year (expected +3.6%; prior +3.5%)

South Korea's March Export Price Index -6.8% year-over-year (prior -8.1%) and March Import Price Index -17.1% year-over-year (prior -17.8%)

In news:

China's trade surplus came in at its lowest level in more than a year amid declining shipments to the US, Europe, and Japan

Major European indices trade mixed. UK's FTSE -0.5% while Germany's DAX and France's CAC hover near their flat lines. Elsewhere, Italy's MIB +0.5% and Spain's IBEX+ 0.6%

Economic data was limited:

French Current Account deficit widened to EUR1.80 billion from EUR300 million (expected deficit of EUR1.20 billion)

Italy's February Industrial Production +0.6% month-over-month (expected 0.5%; prior -0.7%); -0.2% year-over-year (consensus -1.3%; last -2.2%)

Among news of note:

According to Germany's FAZ, Greece has to prepare a list of reforms by April 20 in order to receive the next installment of EU bailout funds

5:49 am: [BRIEFING.COM] S&P futures vs fair value: -2.30. Nasdaq futures vs fair value: -1.30.

5:49 am: [BRIEFING.COM] Nikkei...19905.46...-2.20...0.00%. Hang Seng...28016.34...+744.00...+2.70%.

5:49 am: [BRIEFING.COM] FTSE...7064.43...+25.40...+0.40%. DAX...12377.73...+3.00...+0.00%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage