Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

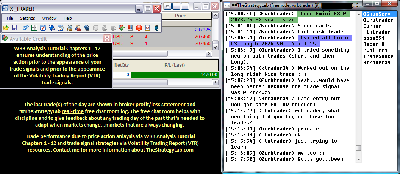

Attachment:

040815-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1470.00.png [ 93.14 KiB | Viewed 323 times ]

040815-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1470.00.png [ 93.14 KiB | Viewed 323 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$220.00 dollars or +2.20 points, Emini ES ($ES_F) futures @

$1,250.00 dollars or +25.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,470.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab

free chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips in ##TheStrategyLab chat room involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=142&t=2047 Quote:

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via Advance WRB Analysis Tutorial Chapters @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Analysis -----> Trade Signals Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR). All WRB Analysis Tutorial Chapters 1 - 12 are included in the purchase of the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=261&t=2728 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

Briefing,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

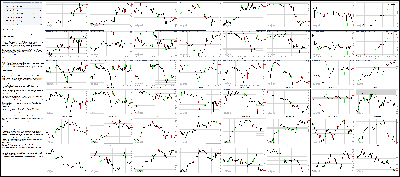

Attachment:

040815-Key-Price-Action-Markets.png [ 1.12 MiB | Viewed 370 times ]

040815-Key-Price-Action-Markets.png [ 1.12 MiB | Viewed 370 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The stock market ended Wednesday on a higher note, but not before making a couple appearances in the red. The S&P 500 added a modest 0.3% while the Nasdaq Composite (+0.8%) outperformed.

Equity indices climbed out of the gate with the Nasdaq receiving major support from biotechnology. Meanwhile, the S&P 500 notched its session high during the initial 30 minutes, but returned to its flat line shortly thereafter amid significant weakness in the energy sector (-1.0%).

The growth-sensitive energy space was pressured by a tailspin in crude oil futures after latest data from the American Petroleum Institute revealed that crude inventories increased by 10.9 million barrels since last week. As a result, total inventories have reached levels not seen at this time of the year in at least 80 years. WTI crude fell 6.5% to $50.44/bbl, erasing its Tuesday advance, and cutting into its gain from Monday.

Unlike energy, most of the remaining cyclical sectors ended near their flat lines while the consumer discretionary sector (+0.9%) outperformed after showing relative weakness yesterday. Today, however, the group enjoyed broad support, including relative strength among homebuilders. The iShares Dow Jones US Home Construction ETF (ITB 28.41, +0.40) climbed 1.4%.

Elsewhere, the health care sector (+0.9%) also displayed strength throughout the day, which was largely due to biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 352.01, +10.09) outperformed from the get-go and extended its gain after Mylan (MYL 68.36, +8.79) announced a proposal to acquire Perrigo (PRGO 195.00, +30.29) for $205/share. The news sent shares of PRGO higher by 18.4% while the biotech ETF advanced 3.0% and kept the Nasdaq in the lead.

Similar to biotechnology, the high-beta chipmaker space contributed to Nasdaq's strength with the PHLX Semiconductor Index advancing 0.7%. However, the technology sector (+0.2%) ended a bit behind the broader market following mixed action in large cap names. Google (GOOGL 548.84, +3.98) added 0.7% while Apple (AAPL 125.60, -0.41) lost 0.3% after Societe Generale downgraded the stock to 'Hold' from 'Buy.'

Treasuries ended the day on a modestly lower note with the 10-yr yield rising one basis point to 1.90%. The benchmark yield saw little reaction to the afternoon release of FOMC minutes that provided little clarity regarding the timing of the first rate hike.

According to the minutes, FOMC members were split over whether June would be the right time to begin raising rates. Several members believed that recent data and the outlook warranted a rate hike in June while others voiced concerns that the economic outlook would not be strong enough to support a rate hike in the near term.

The dollar was also discussed in the minutes with participants acknowledging that net exports would be hampered by the strong greenback. In addition, a few members voiced their belief that the dovish tone emanating from global central banks could lead to additional dollar strength.

Fittingly, the Dollar Index (98.02, +0.19) erased its intraday loss in reaction to the minutes, adding 0.2% for the day.

Today's participation was close to recent averages with roughly 750 million shares changing hands at the NYSE floor.

Economic data reported this morning was limited to the weekly MBA Mortgage Index, which ticked up 0.4% to follow last week's 4.6% increase.

Tomorrow, weekly Initial Claims (Briefing.com consensus 285K) will be released at 8:30 ET while the Wholesale Inventories report for February will cross at 10:00 ET (expected 0.2%).

Russell 2000 +4.9% YTD

Nasdaq Composite +4.5% YTD

S&P 500 +1.1% YTD

Dow Jones Industrial Average +0.5% YTD

3:35 pm: [BRIEFING.COM]

Crude oil continued to hold its losses today, which began after the API reported bearish oil storage late yesterday

Overall, WTI crude fell over $3 since the API released its weekly storage data to below $50.50/barrel in recent trade

May crude finished the day $-3.52 lower at $50.44/barrel

In other energy, May nat gas lost $0.06 to $2.62/MMBtu

Metals lost ground as well with gold, silver and copper all posting modest losses

June gold fell $7.30 in pit trading today to $1203.30/oz, while May silver declined $0.37 to $16.47/oz

May copper closed $0.03 lower to $2.73/lb.

3:00 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.2% with one hour remaining in the session.

Today's affair has featured a daylong battle between two influential sectors. The third-largest sector by weight-health care (+0.7%)-has held the lead since the start while the energy sector (-0.9%) has acted as a counterweight.

Going into the last hour, the consumer discretionary sector (+0.6%) is the only other group showing a gain larger than 0.2% while most of the remaining sectors hover near their flat lines.

Elsewhere, Treasuries have reclaimed their intraday losses with the 10-yr yield back to unchanged at 1.89%.

2:25 pm: [BRIEFING.COM] The Federal Reserve released the minutes from its latest policy meeting, but the document has not introduced any new insight.

According to the minutes, FOMC members were split over whether June would be the right time to begin raising rates. Several members believed that recent data and the outlook warranted a rate hike in June while others voiced concerns that the economic outlook would not be strong enough to support a rate hike in the near term.

The dollar was also discussed in the minutes with participants acknowledging that net exports would be hampered by the strong greenback. In addition, a few members voiced their belief that the dovish tone emanating from global central banks could lead to additional dollar strength.

The S&P 500 (+0.4%) slid to a fresh low following the minutes, but returned to its high shortly thereafter. Meanwhile, the 10-yr note slumped briefly, but it now trades back near its earlier levels (1.90%, +1 bp). Also of note, the Dollar Index (97.96, +0.13) spiked to a fresh session high and is now up 0.1%.

1:55 pm: [BRIEFING.COM] The S&P 500 hovers in the middle of its trading range.

With no economic releases today, we look ahead to tomorrow's initial claims report.

The initial claims level decreased to 268,000 for the week ending March 28 from 288,000 for the week ending March 21. The Briefing.com Consensus expects the initial claims level increased to 285,000 for the week ending April 4.

That was the lowest initial claims level since the end of January.

The improvement in claims, however, is not necessarily a reliable indicator for job growth. Even though businesses have reduced the number of layoffs, they haven't been in too much of a hurry to hire more workers. As a result, there has been a significant increase in the number of unfilled job openings.

The continuing claims level fell to 2.325 mln for the week ending March 21 from 2.413 mln for the week ending March 14. The consensus expects the continuing claims level increased to 2.395 mln for the week ending March 28. Reaction to the FOMC minutes from the March 18 meeting will be discussed in the next update at 1:30.

1:30 pm: [BRIEFING.COM] The major U.S. indices have sold off slightly in recent trade but still show mild gains on the day.

In equities, following earlier news that Mylan (MYL 68.74, +9.17) has submitted a proposal to acquire Irish healthcare company Perrigo (PRGO 196.29, +31.58) for $205 in cash and stock, Perrigo confirmed it has received the proposal and announced that its Board will meet to discuss the offer.

At the top of the hour, the U.S. Treasury auctioned off $21 bln in 10-year notes with a high yield of 1.925% and a bid-to-cover ratio of 2.62. The auction was met with average demand.

As we enter the last hours of the trading day, investors will be waiting on the FOMC minutes, which are expected to be release at 14:00 ET. In addition, aluminum giant Alcoa (AA 13.65, +0.22) is set to unofficially kick off Q1 earnings season when it releases its quarterly results after the bell.

12:55 pm: [BRIEFING.COM] The major averages sport midday gains with the Nasdaq Composite (+0.7%) trading well ahead of the S&P 500 (+0.2%).

Equity indices climbed out of the gate, but the S&P 500 notched its session high during the opening hour and returned to its flat line amid noteworthy weakness in the energy sector (-0.7%). That slide was brought on by a sell-off in crude oil after the API inventory report showed a weekly increase of 10.9 million barrels, representing the largest build in 14 years. As a result, WTI crude has erased yesterday's gain and is now down 5.7% at $50.95/bbl.

The S&P 500 has been able to return into the middle of its trading range, but the index has yet to challenge its early high. Interestingly, a recent surge in the influential health care sector (+1.0%) has had little impact on the market.

As for health care, the sector spiked to a new high after Mylan (MYL 67.95, +8.38) announced a proposal to acquire Perrigo (PRGO 200.69, +35.98) for $205/share. The news caused shares of PRGO to rocket higher by 21.8% while the iShares Nasdaq Biotechnology ETF (IBB 351.26, +9.93) is now up 2.7%.

In turn, biotechnology has helped the Nasdaq Composite spend the first half of the day well ahead of the broader market. High-beta chipmakers have also shown relative strength with the PHLX Semiconductor Index higher by 0.7% while the broader technology sector (+0.2%) trades in-line with the S&P 500.

Unlike microchip names, large cap sector components trade in mixed fashion. Google (GOOGL 550.48, +5.62) has climbed 1.0% while Apple (AAPL 125.74, -0.27) is lower by 0.2% after Societe Generale downgraded the stock to 'Hold' from 'Buy.'

Elsewhere, Treasuries have spent the day in a steady retreat from their overnight highs. The 10-yr yield is higher by four basis points at 1.92%.

Economic data reported this morning was limited to the weekly MBA Mortgage Index, which ticked up 0.4% to follow last week's 4.6% increase.

The minutes from the latest FOMC policy meeting will be released at 14:00 ET.

12:25 pm: [BRIEFING.COM] Not much change in the market with the S&P 500 (+0.3%) holding a modest gain.

Interestingly, the recent spike in the health care sector (+1.1%) has not done much for the broader market even though health care represents nearly 14.0% of the S&P 500. Meanwhile, the remaining countercyclical sectors lag. The consumer staples sector (-0.1%) hovers just below its flat line while telecom services (-0.7%) and utilities (-0.4%) display larger losses.

Elsewhere, Treasuries remain near their lows with the 10-yr yield higher by three basis points at 1.92%.

11:55 am: [BRIEFING.COM] Recent action saw the health care sector (+1.2%) surge to a fresh high after Mylan (MYL 67.29, +7.72) announced a proposal to acquire Perrigo (PRGO 205.71, +41.00) for $205/share. The news caused shares of PRGO to rocket higher by 25.0% while the iShares Nasdaq Biotechnology ETF (IBB 352.74, +10.82) is now up 3.2%.

At this time, the health care sector is the only group with a gain larger than 1.0% while the second-best performer-consumer discretionary-trades higher by 0.7%.

11:25 am: [BRIEFING.COM] Equity indices have climbed off their recent levels with the S&P 500 (+0.2%) returning into the middle of its trading range. Meanwhile, the Nasdaq Composite (+0.6%) has returned near its best level of the day.

The tech-heavy Nasdaq has been able to stay ahead of the broader market thanks to persistent strength in biotechnology names. The iShares Nasdaq Biotechnology ETF (IBB 349.09, +7.17) has extended its advance to 2.0% while the health care sector (+0.5%) remains among the leaders, trading only behind the consumer discretionary space (+0.6%).

Elsewhere, Treasuries have extended their decline with the 10-yr yield climbing to 1.91% (+3 bps).

11:00 am: [BRIEFING.COM] The major averages have retreated from their early highs with the S&P 500 (+0.1%) returning near its flat line. Only three sectors remain in positive territory with yesterday's laggards-consumer discretionary (+0.5%) and financials (+0.4%) showing relative strength alongside the health care sector (+0.4%).

On the downside, the energy space (-0.6%) has tumbled amid a sell-off in crude futures after the API inventory report showed a weekly increase of 10.9 million barrels, representing the largest build in 14 years. As a result, crude oil is now down 4.1% at $51.77/bbl.

Interestingly, the pullback in oil has coincided with a rebound in the greenback that has lifted the Dollar Index (97.92, +0.09) out of the red.

10:40 am: [BRIEFING.COM]

Crude oil futures sold off sharply late yesterday following bearish API data.

This morning, oil continues to trade near levels post-API data, and ahead of the EIA data to be released at 10:30 AM EST.

Estimations for inventory expected a build of ~3.3 mln.

Following the data, which showed the largest weekly build in 14 years, May crude oil is currently -2.9% at $52.44/barrel

The dollar index has been trading in the red all day, which has given some commodities price support. The index is now trading -0.1% at 97.76

Precious metals prices fell modestly in early trade, with June gold currently 0.26% at $1,207.50/oz, with May silver -0.5% at $16.75/oz

May copper is flat at $2.74/lb

9:55 am: [BRIEFING.COM] Equity indices have added to their early gains with the S&P 500 now up 0.5%. Meanwhile, the Nasdaq Composite (+0.7%) outperforms thanks to broad strength in biotechnology.

Furthermore, the technology sector (+0.5%) began the day behind the broader market, but the group has closed that early gap. The top-weighted component-Apple (AAPL 126.31, +0.30)-opened in the red, but now trades higher by 0.2%. Similarly, most other large cap names also trade in the green.

Elsewhere, Treasuries have inched down to new lows with the 10-yr yield ticking up one basis point to 1.90%.

9:40 am: [BRIEFING.COM] The major averages climbed out of the gate with the S&P 500 (+0.3%) erasing its entire decline from yesterday.

Eight of ten sectors display early gains with influential consumer discretionary (+0.6%) and health care (+0.5%) out in the lead. Similar to yesterday, the health care sector has received support from biotechnology with the iShares Nasdaq Biotechnology ETF (IBB 345.05, +3.13) trading higher by 0.9%.

Elsewhere, the top-weighted technology sector (+0.2%) trades a bit behind the broader market with Apple (AAPL 125.37, -0.64) down 0.5% after Societe Generale downgraded the stock to 'Hold' from 'Buy.'

9:09 am: [BRIEFING.COM] S&P futures vs fair value: +1.90. Nasdaq futures vs fair value: +4.90. The stock market is on track for a flat open as futures on the S&P 500 hover within two points of fair value.

Yesterday, equity indices held modest gains into the afternoon, but slumped into the close, giving in to daylong weakness among a couple influential sectors like consumer discretionary and financials.

This morning has been relatively quiet on the corporate front while economic data was limited to the weekly MBA Mortgage Index, which ticked up 0.4% to follow last week's 4.6% increase. Later today, the Federal Reserve will release the minutes from the latest FOMC meeting, with the document set to cross the wires at 14:00 ET.

Treasuries held modest gains overnight, but they are now little changed with the 10-yr yield at 1.88%.

8:54 am: [BRIEFING.COM] S&P futures vs fair value: +0.80. Nasdaq futures vs fair value: +3.20. The S&P 500 futures trade within a point of fair value.

Major stock indices in the Asia-Pacific region were mostly higher while smaller regional markets were mostly lower. The former were helped along by some M&A activity, enthusiasm for continued accommodative monetary policy stances, and a momentum trade. The Shanghai Composite scored its 18th gain in the last 20 trading sessions, but it was the Hang Seng, which soared 3.8%, that stole Wednesday's bullish show. Also of note, The Bank of Japan made no changes to its policy stance, but there were signs of growing dissent. For instance, Takahide Kiuchi argued for the annual monetary base growth to be reduced to JPY45 trillion.

Economic data was limited:

Japan's Current Account surplus narrowed to JPY600 billion from JPY1.06 trillion (expected surplus of JPY610 billion). Separately, Economy Watchers Current Index rose to 52.2 from 50.1 (expected 50.9)

------

Japan's Nikkei increased 0.8% and touched its highest level since June 2000 (19,845.53) following the Bank of Japan's decision to keep its monetary policy unchanged. Gains were led by the consumer non-cyclical (+1.5%) sector, although the financial sector (-0.1%) was a notable laggard. Dentsu (+6.1%), Shiseido Co (+5.3%), and Aeon Co (+5.0%) led individual gainers. Out of the 225 index members, 161 finished up, 53 closed down, and 11 were unchanged.

Hong Kong's Hang Seng soared 3.8% after re-opening from its holiday closure. The move was reportedly helped along by mainland investors who took full advantage of the daily quota under the Shanghai-Hong Kong Stock Connect program. Every sector closed higher with the influential financial sector (+3.6%) logging a healthy gain. Hong Kong Exchanges and Clearing (+12.2%) led all individual winners, followed by Belle International Holdings (+9.6%) and China Merchants Holdings (+8.8%). Out of the 50 index members, 46 ended higher, 3 finished lower, and 1 was unchanged.

China's Shanghai Composite jumped 0.8% and finished higher for the 18th time in the last 20 trading sessions. Over that span, the Shanghai Composite has gained 21.6%. The financial stocks were the main drivers of Wednesday's advance.

Major European indices trade in mixed fashion with UK's FTSE (+0.4%) showing relative strength thanks to M&A activity. Also of note, Greek Prime Minister Alexis Tsipras is meeting with Russian President Vladimir Putin in Moscow today. Coincidentally, Greece is due to pay EUR450 million to the International Monetary Fund tomorrow.

In economic data:

Eurozone Retail Sales -0.2% month-over-month; +3.0% year-over-year. Both figures matched expectations

French Trade Deficit narrowed to EUR3.50 billion from EUR3.70 billion (expected deficit of EUR3.80 billion)

Swiss CPI +0.3% month-over-month (expected 0.2%; prior -0.3%); -0.9% year-over-year (consensus -1.0%; last -0.8%)

------

UK's FTSE has added 0.4% thanks to strength among energy names after Royal Dutch Shell offered to acquire BG Group for GBP47 billion. Shell is lower by 5.7% while BG Group has surged 34.7%. Miners also display strength with Anglo American, BP, BHP Billiton, and Rio Tinto up between 1.6% and 1.8%.

In France, the CAC trades flat. Financials AXA and BNP Paribas have shown strength with respective gains of 0.3% and 1.0% while consumer names lag. Accor, Danone, and L'Oreal are down between 0.3% and 0.5%.

Germany's DAX has given up 0.4% with exporters on the defensive. BMW and Daimler trade lower by 2.0% and 1.3%, respectively. On the upside, Deutsche Lufthansa is higher by 2.5%.

8:28 am: [BRIEFING.COM] S&P futures vs fair value: +0.80. Nasdaq futures vs fair value: +3.20. U.S. equity futures continue drifting near their flat lines while markets in Europe also trade little changed.

Yesterday's session featured crude strength that coincided with a rally in the greenback and both moves have been partially retraced during overnight action. The Dollar Index (97.39, -0.44) is lower by 0.5%, having erased roughly half of yesterday's spike. Similarly, crude oil has also cut yesterday's gain in half, trading lower by 2.1% at $52.87/bbl.

7:58 am: [BRIEFING.COM] S&P futures vs fair value: +0.70. Nasdaq futures vs fair value: +3.70. U.S. equity futures trade little changed amid cautious action overseas. The S&P 500 futures hover within a point of fair value after trading inside a five-point range overnight.

Meanwhile, the Dollar Index (97.49, -0.34) spiked 1.2% yesterday, but a modest retreat has the Index trading lower by 0.3% at this time; however, the slight weakness has not been able to lift crude oil, which has given up 2.2%, sliding to $52.80/bbl.

The weekly MBA Mortgage Index ticked up 0.4% to follow last week's 4.6% increase. There will be no other economic releases today, but the minutes from the latest FOMC policy meeting will be released at 14:00 ET.

Treasuries hold slim losses with the 10-yr yield higher by a basis point at 1.89%.

In U.S. corporate news of note:

Apple (AAPL 125.46, -0.55): -0.4% after Societe Generale downgraded the stock to 'Hold' from 'Buy.'

Rite Aid (RAD 8.78, +0.09): +1.0% after beating bottom-line estimates and issuing cautious revenue guidance.

Reviewing overnight developments:

Asian markets ended higher. Japan's Nikkei +0.8%, China's Shanghai Composite +0.8%, and Hong Kong's Hang Seng +3.8%

Economic data was limited:

Japan's Current Account surplus narrowed to JPY600 billion from JPY1.06 trillion (expected surplus of JPY610 billion). Separately, Economy Watchers Current Index rose to 52.2 from 50.1 (expected 50.9)

In news:

The Bank of Japan made no changes to its policy stance, but there were signs of growing dissent. For instance, Takahide Kiuchi argued for the annual monetary base growth to be reduced to JPY45 trillion.

Hong Kong's Hang Seng outperformed, playing catch-up after being closed since last week.

Major European indices trade in mixed fashion. UK's FTSE +0.4%, Germany's DAX -0.3%, and France's CAC is flat. Elsewhere, Italy's MIB -0.3% and Spain's IBEX -0.3%

In economic data:

Eurozone Retail Sales -0.2% month-over-month; +3.0% year-over-year. Both figures matched expectations

French Trade Deficit narrowed to EUR3.50 billion from EUR3.70 billion (expected deficit of EUR3.80 billion)

Swiss CPI +0.3% month-over-month (expected 0.2%; prior -0.3%); -0.9% year-over-year (consensus -1.0%; last -0.8%)

Among news of note:

UK's FTSE outperforms thanks to strength among energy-related names after Shell offered to acquire BG Group for GBP47 billion.

5:51 am: [BRIEFING.COM] S&P futures vs fair value: +3.00. Nasdaq futures vs fair value: +3.80.

5:51 am: [BRIEFING.COM] Nikkei...19789.81...+149.30...+0.80%. Hang Seng...26236.86...+961.20...+3.80%.

5:51 am: [BRIEFING.COM] FTSE...6996.15...+34.40...+0.50%. DAX...12097.37...-26.20...-0.20%.

Special thanks to Bloomberg, Briefing, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage