Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

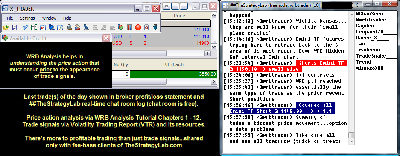

Attachment:

103014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3550.00.png [ 175.37 KiB | Viewed 398 times ]

103014-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3550.00.png [ 175.37 KiB | Viewed 398 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,550.00 dollars or +35.50 points, Emini ES ($ES_F) futures @

$0.00 dollars or +00.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,550.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=135&t=1922 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=248&t=2530 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

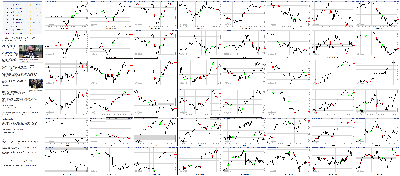

Attachment:

103014-Key-Price-Action-Markets.png [ 1.57 MiB | Viewed 403 times ]

103014-Key-Price-Action-Markets.png [ 1.57 MiB | Viewed 403 times ]

click on the above image to view today's price action of key markets 4:20 pm: [BRIEFING.COM] The major averages ended the Thursday session on a higher note with the Dow Jones Industrial Average (+1.3%) spending the entire day in the lead. However, the strength among blue chips masked the underperformance of high-beta chipmaker and transport stocks. Furthermore, defensively-oriented health care (+1.8%) and utilities (+2.1%) finished in the lead, suggesting a lack of strong conviction.

Shortly before the open, the advance reading of Q3 GDP revealed growth of 3.5% while the Briefing.com consensus expected an increase of 3.0%. The news contributed to a rebound in the futures market, which had been pressured by early weakness in European equities. However, markets across Europe were able to erase their losses before ending for the day.

The Dow held the lead from the start thanks to a surge in its top-weighted component. Shares of Visa (V 236.65, +21.99) soared 10.2% in reaction to a bottom-line beat and news of a $5 billion buyback.

Visa's peer, MasterCard (MA 83.13, +7.14), also had a strong showing, spiking 9.4%, after it too surpassed earnings estimates. However, the two names were unable to push the technology sector (+0.2%) ahead of the broader market as other influential components like Apple (AAPL 106.98, -0.36), Facebook (FB 74.11, -1.75), and Microsoft (MSFT 46.05, -0.57) underperformed. Chipmakers also lagged with the PHLX Semiconductor Index falling 1.2%.

The high-beta group slumped after ending yesterday's session on its 50-day average (623.74). The complex widened its October loss to 3.4% with its largest component-Intel (INTC 32.58, -1.34)-plunging 4.0%.

Elsewhere among cyclical sectors, the materials space (+0.7%) had the strongest showing while energy (-0.3%) spent the day in the red. Crude oil, which fell 1.4% to $81.10/bbl, contributed to the weakness, while Chevron (CVX 117.20, +0.06) and ExxonMobil (XOM 94.45, -0.14) ended little changed ahead of their quarterly reports.

Also of note, industrials (+0.4%) could not catch up to the broader market due to the weakness among transports. The Dow Jones Transportation Average slid 1.2% with Con-way (CNW 42.35, -2.81) diving 6.2% despite beating bottom-line estimates. Meanwhile, peer C.H. Robinson (CHRW 69.22, -2.88) tumbled 4.0% in reaction to a Credit Suisse downgrade to 'Underperform' from 'Neutral.'

Meanwhile on the countercyclical side, consumer staples (+0.55%) and telecom services (+0.3%) slipped behind the market in the afternoon while health care (+1.8%) and utilities (+2.1%) finished in the lead.

The health care sector was boosted by strong results from AmerisourceBergen (ABC 84.84, +5.10) and Cigna (CI 97.10, +3.10). As for biotechnology, the iShares Nasdaq Biotechnology ETF (IBB 296.70, +6.07) settled higher by 2.1%.

Treasuries notched their highs right after the GDP report before spending the session in a steady retreat. The 10-yr yield slipped one basis point to 2.31%.

Today's participation was ahead of average with 730 million shares changing hands at the NYSE.

Economic data was limited to GDP and Initial Claims:

According to the advance estimate, GDP grew at an annualized rate of 3.5% during the third quarter while the Briefing.com consensus expected the reading to come in at 3.0%

Real final sales jumped 4.2%, which was the largest spike since Q4 2010

The export deficit narrowed to $409.90 billion from $460.40 billion, boosting GDP growth by 1.32 percentage points

Government spending surged 4.6%, representing the sharpest increase since Q2 2009

Weekly Initial Claims increased to 287,000 from a revised rate of 284,000 (from 283,000) while the Briefing.com consensus called for a reading of 284,000

Claims have held below the 300,000 mark for the past several weeks, suggesting payroll gains should surpass 200,000

Continuing claims increased to 2.384 million from an upwardly revised 2.355 million (from 2.351 million)

Tomorrow, September Personal Income (Briefing.com consensus 0.3%), Personal Spending (consensus 0.1%), Core PCE Prices (expected 0.1%), and the Q3 Employment Cost Index (expected 0.5%) will all be released at 8:30 ET while the Chicago PMI report for October (consensus 60.0) will cross the wires at 9:45 ET. The day's data will be topped off with the final release of the Michigan Sentiment survey for October (expected 86.4).

Nasdaq Composite +9.3% YTD

S&P 500 +7.9% YTD

Dow Jones Industrial Average +3.7% YTD

Russell 2000 -0.7% YTD

3:30 pm: [BRIEFING.COM]

Crude trended lower overnight into the pit session open, eventually reaching a LoD of $80.8 near lunch time; futures moved higher but has since moved back toward the session low. Dec crude finished the day at $81.10/barrel, down 1.4%.

Natural gas has been trending higher since yesterday's LoD of $3.696, ending today's session 1.2% higher at $3.83/MMBtu

Silver was the worst performing commodity today, tanking 4.5% to $16.44/oz.

Dec gold lost 2.2% at $1198.50/oz, while Dec copper fell 1.2% at $3.07/lb

3:05 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.3% with one hour remaining in the session. The benchmark index has backed away from its session high just below the 2,000 level to an area where it traded before NYSE reported an issue with disseminating quotes.

Investors received a full slate of earnings since yesterday's closing bell with Visa's (V 237.88, +23.22) results giving a big boost to the Dow (+1.1%).

Another batch of results will be released after today's closing bell with discretionary names Expedia (EXPE 80.19, +0.65), Starbucks (SBUX 77.22, +0.68), and Live Nation (LYV 24.78, +0.04) expected to receive attention.

Tomorrow morning, the focus will shift to Chevron (CVX 116.67, -0.47), ExxonMobil (XOM 94.03, -0.56), and Anheuser-Busch InBev (BUD 109.64, -0.28) among others.

2:30 pm: [BRIEFING.COM] Afternoon action continues with the S&P 500 trading higher by 0.7%. Meanwhile, the Dow (+1.2%) remains in the lead with shares of Visa (V 236.15, +21.49) boosting their gain to 10.0%.

Visa notwithstanding, 24 other Dow components hover in the green while six names remain lower. Chevron (CVX 116.70, -0.44) and ExxonMobil (XOM 94.16, -0.43) have narrowed their losses to about 0.5% each, while Intel (INTC 32.59, -1.33) has been unable to take part in the rally. The influential chipmaker trades down 3.9% after sliding to a fresh low in recent action.

2:00 pm: [BRIEFING.COM] A peculiar session has gotten a bit stranger with news from the New York Stock Exchange indicating the National Market System has suffered an outage that affected the Securities Information Processor, otherwise known as SIP. This has prevented the New York Stock Exchange from accurately publishing and receiving trades for shares listed at the NYSE and ICE Exchange OPRA (options).

http://www.reuters.com/article/2014/10/ ... AY20141030 http://www.marketwatch.com/story/key-ny ... 2014-10-30 http://www.businessweek.com/news/2014-1 ... d-kicks-inThe issues cropped up shortly after 13:00 ET, but reports received during the past few minutes indicate the NYSE has returned to operating normally.

The exchange issues have not stopped the market from extending its advance. The Dow is now higher by 1.4% while the S&P 500 has boosted its gain to 0.8%.

1:30 pm: [BRIEFING.COM] The stock market is up today and the action is admittedly a bit strange.

On the one hand, you have the reassuring report and outlook from Visa (V 234.76, +20.10) driving a big gain in the Dow Jones Industrial Average and raising some optimism about consumer spending activity. On the other hand, there are notable laggards with leading indicator status -- the Philadelphia Semiconductor Index (-1.3%) and Dow Jones Transportation Average (-0.7%) -- and notable outperformers known for their countercyclical orientation -- the utilities sector (+1.7%) and the health care sector (+1.6%).

In turn, oil prices are down 1.3% to $81.13/bbl, the U.S. Dollar Index is up 0.1%, and the Treasury market is little changed as the major stock indices power to new session highs. Remarkably, the S&P 500 is just 1.3% below the all-time high it hit on September 19 after being down as much as 9.8% from that high at its low on October 15.

Not sure what to make of it all, yet month-end activity is probably playing a part behind some of the strangeness.

12:55 pm: [BRIEFING.COM] The major averages sit on their highs at midday with the Dow Jones Industrial Average (+0.9%) in the lead. Meanwhile, the S&P 500 (+0.3%) trades closer to its flat line, but eight of ten sectors hover in the green.

This morning, the advance reading of Q3 GDP revealed growth of 3.5% while the Briefing.com consensus expected an increase of 3.0%. The news helped propel a rebound in the futures market, which was pressured by early weakness in European equities. However, like their U.S. counterparts, markets in Europe were able to overcome their losses.

The price-weighted Dow has held the lead since the opening bell thanks in large part to an 8.9% surge in the shares of Visa (V 233.79, +19.13). The largest Dow member reported better than expected earnings and boosted its buyback by $5 billion.

Although Visa has given a major boost to the Dow, the payment processor has been unable to lift the technology sector (-0.1%), which remains pressured by chipmakers. The PHLX Semiconductor Index trades down 1.8% after failing to overtake its 50-day moving average (623.72). The high-beta group has surrendered its gain from the first half of the week and is now down 4.0% for the month of October.

Meanwhile, the second decliner, energy (-0.8%), has had to contend with another drop in crude oil. The energy component is lower by 1.3% at $81.15/bbl. For its part, the other commodity-related sector-materials (+0.6%)-is the leading cyclical group.

On the countercyclical side, the utilities sector (+1.6%) has padded its October advance to 7.3% while health care (+1.4%) follows not far behind. The influential sector has been underpinned by strong earnings from AmerisourceBergen (ABC 84.27, +4.53) and Cigna (CI 96.99, +2.99). Biotechnology has also shown strength with the iShares Nasdaq Biotechnology ETF (IBB 295.53, +4.90) trading higher by 1.7%.

Treasuries have inched away from their highs, but they remain in positive territory. The 10-yr yield is lower by two basis points at 2.29%.

Economic data was limited to GDP and Initial Claims:

According to the advance estimate, GDP grew at an annualized rate of 3.5% during the third quarter while the Briefing.com consensus expected the reading to come in at 3.0%

Real final sales jumped 4.2%, which was the largest spike since Q4 2010

The export deficit narrowed to $409.90 billion from $460.40 billion, boosting GDP growth by 1.32 percentage points

Government spending surged 4.6%, representing the sharpest increase since Q2 2009

Weekly Initial Claims increased to 287,000 from a revised rate of 284,000 (from 283,000) while the Briefing.com consensus called for a reading of 284,000

Claims have held below the 300,000 mark for the past several weeks, suggesting payroll gains should surpass 200,000

Continuing claims increased to 2.384 million from an upwardly revised 2.355 million (from 2.351 million)

12:30 pm: [BRIEFING.COM] Equity indices continue holding their levels with the S&P 500 (+0.3%) hovering just below its session high.

Cyclical sectors struggled this morning and three of six sectors continue trailing the broader market at this time. The energy sector (-1.0%) remains pressured by a 1.6% drop in crude oil ($80.94/bbl), while technology (-0.1%) remains modestly lower amid continued weakness in the PHLX Semiconductor Index (-1.8%). Elsewhere, industrials (+0.1%) have been kept from catching up to the broader market by the underperformance among transport stocks.

The Dow Jones Transportation Average trades lower by 0.5% with 11 of its 20 components in the red. Con-way (CNW 43.00, -2.16) is the weakest performer, down 4.8%, despite beating bottom-line estimates. Meanwhile, peer C.H. Robinson (CHRW 69.60, -2.50) has given up 3.5% in reaction to a Credit Suisse downgrade to 'Underperform' from 'Neutral.'

12:00 pm: [BRIEFING.COM] The S&P 500 (+0.3%) has climbed to a new session high, leaving just two sectors-energy (-1.0%) and technology (-0.2%)-in the red.

On the upside, the health care sector (+1.2%) remains strong, but another countercyclical group-utilities (+1.6%)-holds the lead. The rate-sensitive sector has climbed steadily since the opening bell to extend its October gain to 7.4%. Furthermore, the two leaders also represent the strongest two groups of the year. Health care leads with a 2014 gain of 20.0% while the utilities sector has surged 19.0% so far this year.

Elsewhere among defensively-oriented sectors, consumer staples (+0.4%) trade ahead of the broader market while telecom services (+0.1%) lag.

11:30 am: [BRIEFING.COM] Recent action saw the S&P 500 (+0.1%) join the Dow (+0.7%) in positive territory thanks in part to the continued strength of the health care sector (+1.1%). The countercyclical group has been boosted by upbeat earnings from AmerisourceBergen (ABC 83.52, +3.78) and Cigna (CI 97.03, +3.03), while biotechnology has also shown strength with the iShares Nasdaq Biotechnology ETF (IBB 294.76, +4.13) trading higher by 1.4%.

However, the solid gains in biotechnology have been unable to fuel a rebound in the Nasdaq Composite (-0.3%), which continues facing weakness among chipmakers. The PLHX Semiconductor Index has extended its decline to 2.4%, which makes it lower by 0.4% for the week.

Recall that the high-beta group endured a broad-based plunge during the first half of the month after Microchip Technology (MCHP 40.52, -1.70) made cautious comments about the health of the industry. The SOX index has climbed off its October low, but remains down 4.6% for the month.

10:55 am: [BRIEFING.COM] The major averages remain mixed with the Dow (+0.6%) trading ahead of the Nasdaq (-0.5%) and S&P 500 (-0.1%).

The price-weighted Dow continues drawing significant support from shares of Visa (V 233.88, +19.22), while only 11 other components display gains. Furthermore, most of the remaining advancers sport gains of no more than 0.5%. On the downside, five Dow members have surrendered 1.0% or more.

Intel (INTC 32.91, -1.01) is the weakest performer, down 3.0%, while Chevron (CVX 116.05, -1.09) and ExxonMobil (XOM 93.70, -0.89) are both down near 1.0%. Fittingly, the three names represent two areas of relative weakness. The PHLX Semiconductor Index is lower by 2.1% after failing to retake its 50-day average (623.7) while the energy sector (-0.8%) sits at the bottom of the leaderboard.

10:35 am: [BRIEFING.COM]

Commodities are mostly lower this morning.

Precious metals are getting hit this morning, especially silver futures, which are down 4.2% at $16.54/oz

Gold is currently -1.9% at $1202.30/oz (both are Dec contracts)

Dec crude oil is holding above $81/barrel currently, but is now down 1.1% at $81.33//barrel

Dec nat gas +0.4% at $3.80/MMBtu

Dec copper -2% at $3.04/lb

9:55 am: [BRIEFING.COM] The S&P 500 has returned to its flat line, leaving the Nasdaq Composite (-0.2%) in the red.

Chipmakers have been a bit of a drag on the tech-oriented index in the early going with the PHLX Semiconductor Index trading lower by 1.4%. However, biotechnology has counteracted some of that weakness as evidenced by a 0.6% gain in the iShares Nasdaq Biotechnology ETF (IBB 292.49, +1.86). In turn, the health care sector (+0.5%) trails only the utilities space (+0.9%).

On the downside, the energy sector is lower by 1.3% with crude factoring into the retreat. The energy component trades down 1.5% at $81.00/bbl.

9:40 am: [BRIEFING.COM] Equity indices began the session on a mixed note. The S&P 500 hovers right below its flat line while the price-weighted Dow (+0.5%) has been able to climb out of the gate thanks to strength in its top-weighted component. Visa (V 233.06, +18.40) has spiked 8.6% in reaction to a bottom-line beat and an increased share buyback.

Visa's strength has given a boost to the technology sector (+0.1%) while the remaining nine groups trade mixed. Consumer discretionary (+0.1%), materials (+0.2%), health care (+0.3%), and utilities (+0.3%) outperform while energy (-0.6%), industrials (-0.3%), and consumer staples (-0.3%) lag.

Treasuries remain just below their highs with the 10-yr yield down two basis points at 2.30%.

9:14 am: [BRIEFING.COM] S&P futures vs fair value: -7.40. Nasdaq futures vs fair value: -19.80. The stock market is on track for a modestly lower open with futures on the S&P 500 trading seven points below fair value. Index futures slipped from their overnight highs at the start of the European session, but have been able to spend the past 90 minutes in a steady climb off their lows.

A better than expected advance GDP report (+3.5%; Briefing.com consensus +3.0%) for the third quarter has contributed to the rebound. Real final sales surged 4.2%, registering the biggest jump since Q4 2010. Also of note, government spending spiked 4.6%, which represents the biggest increase since Q2 2009. Interestingly, the report did not lead to weakness in Treasuries. To the contrary, the 10-yr note climbed to a new high, pressuring its yield almost three basis points to 2.29%. For its part, the Dollar Index (86.18, +0.23) returned to its overnight high before pulling back.

On the corporate front, Dow component Visa (V 225.22, +10.56) is on track to open higher by 4.9% after beating bottom-line estimates and announcing a $5 billion buyback. Peer MasterCard (MA 77.89, +1.90) holds a pre-market gain of 2.5% after it too reported better than expected results.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: -9.10. Nasdaq futures vs fair value: -22.80. The S&P 500 futures trade nine points below fair value.

The major Asian bourses finished mixed.

In economic data:

South Korea's Industrial Production ticked up 0.1% month-over-month (expected 1.9%; previous -3.9%) while the year-over-year reading fell 1.9% (consensus 2.8%; last -2.8%). Separately, Retail Sales fell 3.2% month-over-month (previous 2.7%) and Manufacturing BSI Index ticked down to 76 from 78

Australia's Import Price Index fell 0.8% quarter-over-quarter (expected 0.3%; prior -3.0%) while Export Price Index dropped 3.9% (consensus -4.8%; last -7.9%). Separately, HIA New Home Sales were unchanged month-over-month (prior 3.3%)

------

Japan's Nikkei rallied 0.7% to a three-week high. Nintendo surged 7.7% following better than expected quarterly results.

Hong Kong's Hang Seng shed 0.5% after being rejected by the 100-day average as disappointing earnings weighed. Energy plays PetroChina and CNOOC slumped 1.3% and 5.1%, respectively, after missing analyst estimates.

China's Shanghai Composite climbed 0.8% to its best level since February 2013. China Railway Group jumped the limit, 10%, on reports of more state-owned enterprise reform.

India's Sensex added 0.9% to close at a record high. IT service providers paced the advance as Infosys gained 1.6% and Tata Consultancy Services advanced 2.3%.

Major European Indices have climbed off their lows, but they remain down across the board with Spain's IBEX (-1.2%) showing the largest decline. European equities have retreated on a broad basis despite better than expected earnings from Renault, Volkswagen, Eni, Shell, among others. Elsewhere, Greek government bonds are sharply lower in response to headlines from Germany indicating there will be no more support for the troubled sovereign

Participants received several data points:

Eurozone Business and Consumer Survey rose to 100.7 from 99.9 (expected 99.7)

Germany's Claimant Count declined 22,000 (consensus 5,000; previous 9,000), but the Unemployment Rate held steady at 6.7%, as expected

Spain's GDP rose 0.5% quarter-over-quarter while the year-over-year reading jumped 1.6%. Both figures matched expectations. Separately, CPI ticked down 0.1% year-over-year (consensus 0.0%; last -0.2%)

Great Britain's Nationwide HPI rose 0.5% month-over-month (expected 0.3%; previous -0.1%) while the year-over-year reading jumped 9.0% (consensus 8.5%; prior 9.4%)

------

In France, the CAC trades down 0.3% with financials on the defensive. BNP Paribas and Societe Generale hold respective losses of 1.5% and 3.3%. Alcatel-Lucent and Renault outperform with respective gains of 11.6% and 2.3% in reaction to better than expected results.

Great Britain's FTSE is lower by 0.6% amid broad weakness. Miners lead the retreat with Anglo American, Fresnillo, and Randgold Resources down between 3.0% and 3.6%.

Germany's DAX holds a loss of 0.8% with all but two components in the red. Deutsche Lufthansa has given up 6.2% in reaction to disappointing results while Bayer and Volkswagen outperform with gains close to 0.8% apiece. Volkswagen reported above-consensus results while Bayer boosted its guidance.

Spain's IBEX is lower by 1.2% with Bankia, BBVA, and Bankinter down between 1.9% and 2.4%.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: -9.90. Nasdaq futures vs fair value: -24.80. The S&P 500 futures trade ten points below fair value.

The advance third quarter GDP report indicated growth of 3.5%, which was better than the 3.0% increase that had been expected by the Briefing.com consensus. Meanwhile, the third quarter GDP Deflator came in at +1.3%, while the Briefing.com consensus expected a reading of +1.5%.

Separately, the latest weekly initial jobless claims count totaled 287,000, while the Briefing.com consensus expected a reading of 284,000. Today's tally was above the revised prior week count of 284,000 (from 283,000). As for continuing claims, they rose to 2.384 million from 2.355 million.

8:01 am: [BRIEFING.COM] S&P futures vs fair value: -12.30. Nasdaq futures vs fair value: -29.50. U.S. equity futures trade near their pre-market lows amid cautious action overseas. The S&P 500 futures hover 12 points below fair value after slipping from their highs at the start of the European session. The retreat has taken place despite upbeat economic data and earnings from the region.

Meanwhile, the Dollar Index (86.23, +0.28) is working on its second consecutive advance with the greenback logging gains against the euro and the yen. However, some volatility is expected in the foreign exchange market around the 8:30 ET release of Q3 GDP (Briefing.com consensus 3.0%). The advance reading will be released alongside weekly Initial Claims (Briefing.com consensus 284,000).

Treasuries hold slim gains with the 10-yr yield down two basis points at 2.30%.

In U.S. corporate news of note:

Baidu (BIDU 221.48, -3.07): -1.4% despite beating earnings estimates and guiding in-line.

JDS Uniphase (JDSU 12.94, +0.51): +4.1% after beating earnings and revenue estimates.

Take-Two Interactive (TTWO 25.00, +2.20): +9.7% in reaction to better than expected results and upbeat guidance.

TASER (TASR 17.60, +1.13): +6.9% following better than expected earnings and revenue.

Teva Pharmaceutical (TEVA 54.30, -0.19): -0.4% after its cautious guidance overshadowed above-consensus earnings and a $3 billion increase to its buyback.

Visa (V 223.00, +8.34): +3.9% after beating bottom-line estimates and announcing a $5 billion buyback.

Reviewing overnight developments:

Asian markets ended mixed. Japan's Nikkei +0.7%, China's Shanghai Composite +0.8%, and Hong Kong's Hang Seng -0.5%

In economic data:

South Korea's Industrial Production ticked up 0.1% month-over-month (expected 1.9%; previous -3.9%) while the year-over-year reading fell 1.9% (consensus 2.8%; last -2.8%). Separately, Retail Sales fell 3.2% month-over-month (previous 2.7%) and Manufacturing BSI Index ticked down to 76 from 78

Australia's Import Price Index fell 0.8% quarter-over-quarter (expected 0.3%; prior -3.0%) while Export Price Index dropped 3.9% (consensus -4.8%; last -7.9%). Separately, HIA New Home Sales were unchanged month-over-month (prior 3.3%)

In news:

The Reserve Bank of New Zealand held its key interest rate unchanged at 3.5%, as expected

Press reports in Japan suggested the government may implement a modest corporate tax rate cut for the next fiscal year

Major European Indices trade lower across the board. Great Britain's FTSE -1.0%, France's CAC -1.2%, and Germany's DAX -1.8%. Elsewhere, Italy's MIB -2.5% and Spain's IBEX -2.3%

Participants received several data points:

Eurozone Business and Consumer Survey rose to 100.7 from 99.9 (expected 99.7)

Germany's Claimant Count declined 22,000 (consensus 5,000; previous 9,000), but the Unemployment Rate held steady at 6.7%, as expected

Spain's GDP rose 0.5% quarter-over-quarter while the year-over-year reading jumped 1.6%. Both figures matched expectations. Separately, CPI ticked down 0.1% year-over-year (consensus 0.0%; last -0.2%)

Great Britain's Nationwide HPI rose 0.5% month-over-month (expected 0.3%; previous -0.1%) while the year-over-year reading jumped 9.0% (consensus 8.5%; prior 9.4%)

Among news of note:

European equities have retreated on a broad basis despite better than expected earnings from Renault, Volkswagen, Eni, Shell, among others

7:07 am: [BRIEFING.COM] S&P futures vs fair value: -12.00. Nasdaq futures vs fair value: -27.00.

7:07 am: [BRIEFING.COM] Nikkei...15,658.20...+104.30...+0.70%. Hang Seng...23,702.04...-117.80...-0.50%.

7:07 am: [BRIEFING.COM] FTSE...6,380.16...-73.90...-1.10%. DAX...8,936.70...-163.80...-1.80%.

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage