Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

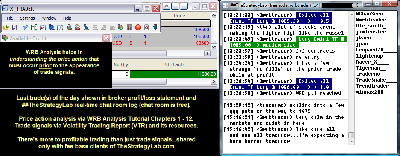

Attachment:

101614-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+11080.00.png [ 177.01 KiB | Viewed 387 times ]

101614-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+11080.00.png [ 177.01 KiB | Viewed 387 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$11,080.00 dollars or +110.80 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $11,080.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup Trade Log: All of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=135&t=1912 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=248&t=2530 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

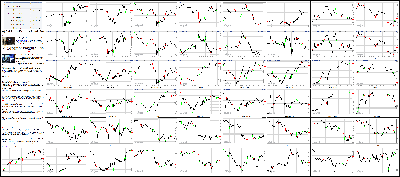

Attachment:

101614-Key-Price-Action-Markets.png [ 1.3 MiB | Viewed 359 times ]

101614-Key-Price-Action-Markets.png [ 1.3 MiB | Viewed 359 times ]

click on the above image to view today's price action of key markets 4:10 pm: [BRIEFING.COM] The major averages endured another whipsaw session that ended with a flat finish for the S&P 500 while the Russell 2000 (+1.1%) registered its second consecutive advance. The price-weighted Dow was the weakest performer of the day with a loss of 0.2%.

Equity indices tumbled out of the gate for the second day in a row amid broad-based selling pressure that also weighed on equities in Europe. The S&P 500 marked a session low near the 1,835 level during the first hour, but spiked more than 20 points following comments from St. Louis Fed President James Bullard. Mr. Bullard appeared on Bloomberg TV and said the Fed should consider delaying the end of its Quantitative Easing program, which is set to wind down at the October FOMC meeting.

The market jumped from lows in reaction to the comments, but it is worth noting that Mr. Bullard is not a voting FOMC member this year and only an alternate voter on next year's schedule. The non-voter status did not get in the way of a surge in equities while Minneapolis Fed President (and FOMC voter) Kocherlakota provided a similar view, saying there is more the Fed can do to achieve maximum employment.

The intraday rebound was paced by some of the groups that faced the most aggressive selling in recent days. The energy sector (+1.7%) led the way, trimming its October loss to 9.0%. Crude oil also rallied, climbing 1.0% to $82.61/bbl after recovering from its overnight low near $79.91/bbl. Meanwhile, the other commodity-linked group-materials (+1.0%)-followed not far behind.

Elsewhere, the industrial sector (+0.7%) advanced with help from transport stocks. Delta Air Lines (DAL 33.32, +0.94) jumped 2.9% after beating earnings estimates while the Dow Jones Transportation Average (+1.1%) extended this week's gain to 1.7%.

The three growth-sensitive sectors spent the entire afternoon in the green while other cyclical groups were a bit more reluctant in joining the rebound. Financials settled in-line with the S&P 500, but the sector was weighed down by Goldman Sachs (GS 172.58, -4.66), which fell 2.6% despite reporting better than expected earnings.

Also of note, the discretionary space (+0.2%) was underpinned by major apparel names like Nike (NKE 87.04, +1.86) and V F Corp (VFC 63.98, +1.18) with their strength masking a 19.4% plunge in the shares of Netflix (NFLX 361.70, -86.89). The video streaming service surpassed its earnings estimates, but guided Q4 results below consensus and said its recent price hike has resulted in slower user growth.

On the downside, the technology sector lost 0.6% even as chipmakers rallied broadly, sending the PHLX Semiconductor Index higher by 1.5%. Large cap listings kept the sector in the red with Apple (AAPL 96.26, -1.28) falling 1.3% after refreshing its product lineup during an afternoon press event. Similarly, Google (GOOGL 536.53, -4.20) lost 0.8% ahead of its quarterly report.

Treasuries ended on their lows after a steady slide from early morning highs. The 10-yr yield ticked up two basis points to 2.16%, which represented an 18-bps spike from the low.

Strong participation continued with more than a billion shares changing hands at the NYSE floor.

Economic data included Initial Claims, Industrial Production, Philadelphia Fed Survey, and the NAHB Housing Market Index:

The weekly initial claims level fell to 264,000 from an unrevised 287,000, while the Briefing.com consensus expected an increase to 290,000

The Department of Labor said there were no special factors influencing the report

Industrial production increased 1.0% in September after falling a downwardly revised 0.2% (from -0.1%) while the Briefing.com consensus expected an increase of 0.4%

Manufacturing production did a full 180 degree turnaround. After falling 0.5% in August, production rose 0.5% in September. That gain was in-line with the improvements in the Federal Reserve regional manufacturing surveys and the national ISM production index

The Philadelphia Fed's Business Outlook Survey Dipped to 20.7 in October from 22.5, while the Briefing.com consensus expected a decline to 19.8

Production levels softened as the Shipments Index fell to 16.6 from 21.6 in September

Employment conditions worsened with the Number of Employees Index falling to 12.1 from 21.2

The NAHB Housing Market Index for October fell to 54 from 59, while the Briefing.com consensus expected the reading to hold at 59

Tomorrow, September Housing Starts (Briefing.com consensus 1013K) and Building Permits (consensus 1030K) will be released at 8:30 ET while the preliminary reading of the Michigan Sentiment survey for October (expected 84.0) will cross the wires at 9:55 ET.

Nasdaq Composite +1.0% YTD

S&P 500 +0.8% YTD

Dow Jones Industrial Average -2.8% YTD

Russell 2000 -6.8% YTD

3:35 pm: [BRIEFING.COM]

Crude's LoD of $79.78 was reached in early morning trading on light volume, and futures have since trended higher, rallying as much as 5 points hitting its HoD of $84.83 shortly after lunch.

Futures pulled back slightly following this mornings inventory data that showed inventories had a build of 8.923 mln (consensus called for a build of 2.7 mln), but recovered quickly.

Natural gas sold off sharply to its LoD of $3.744 after data natural gas inventory data showed a build of 94 bcf vs expectations for a build of ~91 bcf.

Nov crude oil closed the day 0.9% higher at $82.51/barrel, while Nov nat gas -0.3% at $3.97/MMBtu.

Despite settling in negative territory, gold trended higher during the pit session after hitting its LoD of $1235.2 ~15min before the US equity market opened.

Dec gold ultimately fell 0.3% at $1241.20/oz, while Dec silver lost 0.2% at $17.43/oz

Copper prices fell below $3/lb, finishing the day 0.9% lower at $2.98/lb

3:00 pm: [BRIEFING.COM] The S&P 500 trades flat with one hour remaining in the Thursday session. Should the benchmark index end today's session near its current level that would hold its week-to-date loss at 2.3%.

Meanwhile, the Russell 2000 (+1.2%) has fared much better with today's gain extending this week's advance to 2.9%. Despite the newfound strength, the Russell 2000 is still lower by 6.8% since the end of 2013 versus a modest gain for the S&P 500 (0.8%).

Treasuries remain near their lows with the 10-yr yield up one basis point at 2.15%.

2:30 pm: [BRIEFING.COM] Equity indices continue hovering near their recent levels with the S&P 500 higher by 0.3%. The benchmark index trades roughly nine points below its session high, which is a level that represents the midpoint of this year's trading range. Following its downtick from the high, the index is back in the bottom half of that range.

Elsewhere, the Dow Jones Industrial Average (-0.1%) has dipped back into the red. 18 of 30 Dow components trade lower with Goldman Sachs (GS 173.02, -4.22) showing the largest loss. The stock trades lower by 2.4% despite reporting better than expected results. However, the financial sector (+0.3%) has been able to keep pace with the broader market.

1:55 pm: [BRIEFING.COM] The major averages have extended to new highs with the Russell 2000 (+1.6%), the energy sector (+1.9%), and the Dow Jones Transportation Average (+1.8%) continuing to pace the rally.

With stocks padding their gains, only three sectors remain in negative territory at this juncture. Countercyclical consumer staples (-0.5%) and telecom services (-0.3%) display modest losses, while the technology sector hovers right below its flat line. The same cannot be said for chipmakers as the PHLX Semiconductor Index (+2.0%) is among the leaders with all but three components trading higher. On the downside, Intel (INTC 31.13, -0.14) brings up the rear with a 0.5% decline.

The recent rally has caused participants to reduce their hedges as evidenced by the CBOE Volatility Index (VIX 25.57, -0.68), which has backtracked from a morning high near 29.41%.

1:30 pm: [BRIEFING.COM] The stock market has gotten its act together -- sort of. After enduring sharp losses at the open, it has battled back and all indices are in positive territory.

The Russell 2000 (+1.4%) and the energy sector (+2.4%) are leading the recovery, which is catching a lot of attention because they also led yesterday's afternoon recovery try. The relative strength they are exhibiting is noteworthy because they led the broader market into the fit of selling interest it has been experiencing since the Alibaba Group (BABA 88.26, +2.66) IPO on September 19.

The recognition that they are bouncing back is creating some hope that the recent selling interest is at, or near, a point of being exhausted.

The latter consideration, along with the understanding that St. Louis Fed President Bullard and Minneapolis Fed President Kocherlakota made dovish remarks ahead of Fed Chair Yellen's speech tomorrow, has undoubtedly driven some short-covering activity due to concerns that Ms. Yellen could say something that drives faith in the Fed put remaining intact.

1:00 pm: [BRIEFING.COM] Equity indices sit near their rebound highs at midday with the S&P 500 up 0.2% while the Russell 2000 (+1.3%) outperforms for the second day in a row.

Once again, the major averages tumbled out of the gate amid broad-based selling pressure that also weighed on equities in Europe. The S&P 500 notched a session low near the 1,835 level during the opening hour, but surged more than 20 points after St. Louis Fed President James Bullard, who appeared on Bloomberg TV, said the Fed should consider delaying the end of its Quantitative Easing program, which is set to wind down at the October FOMC meeting. Although the market spiked from lows in reaction to the comments, it is worth mentioning that Mr. Bullard is not a voting FOMC member this year and only an alternate voter on next year's schedule.

Equities surged despite Mr. Bullard's non-voter status and the S&P 500 followed the initial spike with a second effort that put the index back at its flat line after Minneapolis Fed President (and voting member) Kocherlakota, who is a well-known dove, said there is more the Fed can do to achieve maximum employment.

The remarks from the two policymakers sparked a rally among growth-sensitive areas like energy (+1.5%), industrials (+0.7%), and materials (+0.7%). The energy sector has narrowed its October loss to 9.2% while crude oil trades higher by 0.8% at $82.49/bbl after climbing off its overnight low near $79.90/bbl.

Elsewhere, the industrial sector has received support from transport stocks. The Dow Jones Transportation Average trades higher by 1.0% to extend this week's advance to 1.3%. Delta Air Lines (DAL 33.34, +0.96) has added 3.0% after beating earnings estimates.

Staying on the earnings theme, Goldman Sachs (GS 175.81, -1.43) trades lower by 0.8% despite beating earnings and revenue estimates. For its part, the broader financial sector (+0.2%) hovers just above its flat line.

Meanwhile, another heavily-weighted sector-consumer discretionary-trades in-line with the market, which has masked a 21.3% nosedive in the shares of Netflix (NFLX 353.07, -95.52). The company reported a bottom-line beat on below-consensus revenue this morning and guided Q4 results below consensus, saying its recent price hike has resulted in slower growth.

Also of note, the influential technology sector (-0.6%) remains among the laggards with large cap names on the defensive. Facebook (FB 71.88, -1.33), Google (GOOGL 532.19, -8.54), and Microsoft (MSFT 42.44, -0.78) are down between 1.6% and 1.8% while Apple (AAPL 96.80, -0.74) is lower by 0.8% with its product refresh event set to begin shortly.

Treasuries are on their lows after sliding from their overnight high. The 10-yr yield is higher by two basis points at 2.16% after marking a low at 1.98%.

Economic data included Initial Claims, Industrial Production, Philadelphia Fed Survey, and the NAHB Housing Market Index:

The weekly initial claims level fell to 264,000 from an unrevised 287,000, while the Briefing.com consensus expected an increase to 290,000

The Department of Labor said there were no special factors influencing the report

Industrial production increased 1.0% in September after falling a downwardly revised 0.2% (from -0.1%) while the Briefing.com consensus expected an increase of 0.4%

Manufacturing production did a full 180 degree turnaround. After falling 0.5% in August, production rose 0.5% in September. That gain was in-line with the improvements in the Federal Reserve regional manufacturing surveys and the national ISM production index

The Philadelphia Fed's Business Outlook Survey Dipped to 20.7 in October from 22.5, while the Briefing.com consensus expected a decline to 19.8

Production levels softened as the Shipments Index fell to 16.6 from 21.6 in September

Employment conditions worsened with the Number of Employees Index falling to 12.1 from 21.2

The NAHB Housing Market Index for October fell to 54 from 59, while the Briefing.com consensus expected the reading to hold at 59

12:30 pm: [BRIEFING.COM] Equity indices continue hovering near their recent levels with four sectors up and six groups trading in the red.

Today's leading group-energy-trades well ahead of the broader market with a gain of 1.1%. However, that advance does not look nearly as good when taking into account the sector's performance so far this month. Despite today's strength, the group is still down 9.5% in October, while the second-weakest performer-materials-has surrendered 7.6% so far this month. Fittingly, the sector is today's second-best performer, up 0.6%.

Elsewhere, Treasuries have slipped to lows with the 10-yr yield climbing two basis points to 2.16%.

12:00 pm: [BRIEFING.COM] The S&P 500 (-0.3%) has backed away from its flat line while the Russell 2000 has narrowed its gain to 0.2%.

Although the benchmark index has been able to rally back to unchanged, extending the move is proving to be a challenge. The outperformance of the Russell 2000 has invited money into some high-beta areas, but large cap names continue weighing the market down.

To that point, the top-weighted sector-technology-trades lower by 0.8% with the likes of Apple (AAPL 96.37, -1.17), Google (GOOGL 531.54, -9.19), and Microsoft (MSFT 42.50, -0.72) down between 1.2% and 1.7%. Shares of Apple are among the laggards ahead of the company's product refresh event, scheduled to begin in an hour.

11:25 am: [BRIEFING.COM] Equity indices hover near their highs with the S&P 500 flat and the small-cap Russell 2000 up 1.0%.

The relative strength among small caps has given a boost to high-growth areas like biotechnology, chipmakers, and transport stocks.

The iShares Nasdaq Biotechnology ETF (IBB 257.26, +0.79) is higher by 0.3% while the health care sector (-0.4%) remains on the defensive. Elsewhere, the PHLX Semiconductor Index trades up 1.5%, but losses among top-weighted tech names have kept the technology sector (-0.5%) in the red.

Also of note, transport stocks display broad gains with the Dow Jones Transportation Average up 1.1%. Only three index components hover in the red with UPS (UPS 96.07, -0.38) showing the largest decline (-0.4%). The strength has helped underpin the industrial sector (+0.8%), which is among today's top performers.

10:55 am: [BRIEFING.COM] During the past hour, the S&P 500 (-0.2%) slipped to a fresh low near the 1,835 area before surging to a rebound high near its flat line. The move followed comments from St. Louis Fed President James Bullard who appeared on Bloomberg TV and said the Fed should consider delaying the end of its Quantitative Easing program, which is set to wind down at the upcoming FOMC meeting.

Although the market spiked from lows in reaction to the comments, it is worth mentioning that Mr. Bullard is not a voting FOMC member this year and only an alternate voter on next year's schedule.

Growth-sensitive sectors surged off their lows with energy (+0.7%), materials (+0.9%), industrials (+0.6%), and financials (+0.1%) spiking into the green. Elsewhere, heavily-weighted technology (-0.4%) and health care (-0.5%) continue showing relative weakness.

Meanwhile, Treasuries have accelerated their retreat from highs. The 10-yr yield is now back to unchanged at 2.14%.

10:35 am: [BRIEFING.COM]

Natural gas futures were about 0.5% higher just ahead of the weekly storage data.

Following the data, nat gas dropped to a new session low of $3.74/MMBtu as the actual build of 94 bcf came in higher than expected.

Crude oil is in the red again today and is currently down 1% at $80.96/barrel

Gold and silver have been in the red this morning, but rallied in recent action to help erase some of its losses.

Dec gold is now -0.2% at $1242.70, Dec silver is -0.3% at $17.42/oz

Copper is lower again and is currently -1.3% a $2.97/lb

10:00 am: [BRIEFING.COM] The S&P 500 has regained about ten points, but still trades lower by 0.6% with all ten sectors in the red.

The Philadelphia Fed Survey for October fell to 20.7 from 22.5. Economists polled by Briefing.com had expected that the Survey would slip to 19.8.

Separately, the NAHB Housing Market Index for October fell to 54 from 59, while the Briefing.com consensus expected the reading to hold at 59.

9:45 am: [BRIEFING.COM] The major averages began the session on the defensive with the Nasdaq Composite (-1.0%) trailing the S&P 500 (-0.9%). All ten sectors started the trading day in negative territory with consumer discretionary (-0.9%) and energy (-1.4%) pressuring the market in the early going.

The discretionary space lags amid weakness in the shares of Netflix (NFLX 343.28, -105.32). The stock has surrendered 23.5% after disappointing guidance overshadowed its bottom-line beat on below-consensus revenue.

Elsewhere, the energy sector has been pressured by crude oil, which is lower by 1.7% at $80.39/bbl. Major sector components have not fared much better with Chevron (CVX 107.60, -1.67) and ExxonMobil (XOM 89.10, -1.12) down 1.5% and 1.2%, respectively.

Treasuries have surrendered a portion of their advance, but they remain in the green. The 10-yr yield is lower by six basis points at 2.08%.

The Philadelphia Fed Survey for October (consensus 19.8) and the October NAHB Housing Market Index (expected 59) will both be reported at 10:00 ET.

9:16 am: [BRIEFING.COM] S&P futures vs fair value: -28.60. Nasdaq futures vs fair value: -72.00. The stock market is on track for another rocky start with the S&P 500 futures trading 29 points below fair value. Futures on the benchmark index made a brief overnight appearance above fair value before slumping to lows after the start of the European session. S&P futures have tried to stage a couple comebacks, but both rebounds were met with renewed selling.

Once again, crude oil is under pressure with WTI crude making a brief appearance below the $80.00/bbl level. The energy component currently trades lower by 1.5% at $80.53/bbl. Meanwhile, the Dollar Index (85.18, +0.03) hovers just above its flat line with the greenback showing gains against the euro (+50 pips), but taking a backseat to the yen (-30 pips).

The safe-haven demand is also visible in the Treasury market where the 10-yr yield is lower by 10 basis points at 2.04%.

Corporate news has been unable to provide a lift even though the likes of Delta Air Lines (DAL 31.25, -1.13), Goldman Sachs (GS 171.80, -5.44), Taiwan Semiconductor (TSM 20.34, +0.27), and UnitedHealth Group (UNH 84.97, +2.81) reported better than expected results. Meanwhile, disappointing guidance from eBay (EBAY 48.55, -1.69) and Netflix (NFLX 328.55, -120.04) overshadowed their better than expected Q3 results.

Just reported, Industrial Production increased 1.0% in September, which was above the 0.4% increase expected by the Briefing.com consensus. Industrial production for August was revised lower to show a decrease of 0.2% (from -0.1%). Separately, capacity utilization hit 79.3% while the Briefing.com consensus expected a reading of 79.0%.

The Philadelphia Fed Survey for October (consensus 19.8) and the October NAHB Housing Market Index (expected 59) will both be reported at 10:00 ET.

8:56 am: [BRIEFING.COM] S&P futures vs fair value: -32.90. Nasdaq futures vs fair value: -83.00. The S&P 500 futures trade 33 points below fair value.

It was a sea of red across Asia as most of the region's bourses ended lower following yesterday's carnage on Wall Street. Power consumption in China recovered from an August contraction to grow at 2.7% in September, but that represented the second lowest reading in 18 months

In economic data:

China's New Loans came in at CNY857.20 billion (expected CNY750.00 billion; previous CNY702.50 billion)

Australia's MI Inflation Expectations ticked down to 3.4% from 3.5%

New Zealand's Business PMI rose to 58.1 from 56.5

------

Japan's Nikkei lost 2.2%, falling to its lowest level in four and a half months as sellers held control for the sixth time in seven sessions. Exporters were hit hard once again as the yen strengthened. Honda Motor lost 3.9% and Panasonic sank 3.6%.

Hong Kong's Hang Seng fell 1.0% to close at its lowest levels since the end of June. Property developers lagged as Hang Lung Properties and China Resources Land dropped 2.6% and 1.9%, respectively.

China's Shanghai Composite slipped 0.7% to finish near two-week lows. Commodity-related names were a drag as Datong Coal Industry tumbled 6.0% and Yunnan Aluminum sank 5.3%.

India's Sensex slid 1.3%, pressing to a two-month low and finishing on the 100-day moving average. Hindalco Industries was the top decliner, slumping 5.7%.

Major European indices trade lower across the board with Spain's IBEX (-3.2%) showing the largest loss. Earlier, Spain failed to reach its target in today's 10-yr note sale, causing a yield spike. Spain's 10-yr yield is higher by 13 basis points at 2.23% while Italy's benchmark yield has added 21 basis points to 2.61%.

Economic data was limited:

Eurozone CPI rose 0.4% month-over-month while the year-over-year reading increased 0.3%. Both figures matched expectations. Also of note, Core CPI rose 0.8% year-over-year (expected 0.7%; prior 0.9%) and the trade surplus expanded to EUR15.80 billion from EUR12.70 billion (expected surplus of EUR13.50 billion)

Italy's trade surplus narrowed to EUR2.06 billion from EUR6.92 billion (expected surplus of EUR3.24 billion)

------

Germany's DAX is lower by 1.6% with financials leading the slide. Commerzbank and Deutsche Bank are both down near 4.0%. Continental and Daimler outperform with respective gains of 1.5% and 0.4%.

Great Britain's FTSE has given up 1.8%. Shire is lower by 12.2% as yesterday's weakness continues. On the upside, distributor of industrial goods, Bunzl, outperforms with a gain of 1.7%.

In France, the CAC trades down 1.9% with financials and utilities showing big losses. BNP Paribas, Societe Generale, Electricite de France, and Veolia Environnement are down between 3.1% and 6.4%. Alstom outperforms with a gain of 0.2%.

Spain's IBEX holds a loss of 3.2%. Banco Popular, Banco Sabadell, Bankinter, and Caixabank are down between 4.2% and 4.9%. Construction names also lag with FCC and Sacyr down 9.3% and 5.4%, respectively.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: -27.50. Nasdaq futures vs fair value: -63.30. The S&P 500 futures trade 28 points below fair value.

The latest weekly initial jobless claims count totaled 264,000, while the Briefing.com consensus expected a reading of 290,000. Today's tally was below the unrevised prior week count of 287,000. As for continuing claims, they rose to 2.389 million from 2.382 million.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -27.60. Nasdaq futures vs fair value: -67.80. U.S. equity futures trade near their pre-market lows amid defensive action overseas. The S&P 500 futures hover 28 points below fair value with the entire loss coming after the start of the European session.

The Dollar Index began climbing off its overnight low as futures retreated. The Index currently hovers just above its flat line with the dollar showing strength against the euro (+50 pips), but giving way to the yen (-30 pips). On a somewhat related note, crude oil trades in the red once again, down 1.6% at $80.50/bbl.

Treasuries are near their highs with the 10-yr yield down ten basis points at 2.04%.

Weekly Initial Claims (Briefing.com consensus 290K) will be released at 8:30 ET, while September Industrial Production (consensus 0.4%) and Capacity Utilization (expected 79.0%) will both be reported at 9:15 ET. Also of note, the Philadelphia Fed Survey for October (consensus 19.8) and the October NAHB Housing Market Index (expected 59) will both be reported at 10:00 ET.

In U.S. corporate news of note:

Baker Hughes (BHI 48.00, -5.63): -10.5% after missing bottom-line estimates.

Blackstone (BX 28.25, -0.81): -2.8% in reaction to its earnings miss on better than expected revenue.

Delta Air Lines (DAL 31.60, -0.78): -2.3% despite beating earnings estimates by two cents.

eBay (EBAY 48.40, -1.84): -3.7% after its cautious Q4 guidance overshadowed its one-cent beat. RBC Capital Markets downgraded the stock to 'Sector Perform' from 'Outperform' in reaction to the results.

Goldman Sachs (GS 176.80, -0.44): -0.3% despite reporting better than expected results.

Netflix (NFLX 337.00, -111.59): -24.9% following its bottom-line beat on below-consensus revenue. The company guided Q4 results below consensus and said its recent price hike has resulted in slower growth.

Taiwan Semiconductor (TSM 20.37, +0.30): +1.5% after beating earnings estimates and guiding ahead of analyst expectations.

UnitedHealth (UNH 81.00, -1.16): -1.4% despite beating earnings expectations and raising its earnings guidance for the full year.

Reviewing overnight developments:

Asian markets ended lower. China's Shanghai Composite -0.7%, Hong Kong's Hang Seng -1.0%, and Japan's Nikkei -2.2%

In economic data:

China's New Loans came in at CNY857.20 billion (expected CNY750.00 billion; previous CNY702.50 billion)

Australia's MI Inflation Expectations ticked down to 3.4% from 3.5%

New Zealand's Business PMI rose to 58.1 from 56.5

In news:

Power consumption in China recovered from an August contraction to grow at 2.7% in September, but that represented the second lowest reading in 18 months

Major European indices trade lower across the board. Germany's DAX -1.8%, Great Britain's FTSE -1.8%, and France's CAC -2.5%. Elsewhere, Italy's MIB -3.4% and Spain's IBEX -3.7%

Economic data was limited:

Eurozone CPI rose 0.4% month-over-month while the year-over-year reading increased 0.3%. Both figures matched expectations. Also of note, Core CPI rose 0.8% year-over-year (expected 0.7%; prior 0.9%) and the trade surplus expanded to EUR15.80 billion from EUR12.70 billion (expected surplus of EUR13.50 billion)

Italy's trade surplus narrowed to EUR2.06 billion from EUR6.92 billion (expected surplus of EUR3.24 billion)

Among news of note:

Spain has failed to reach its target in today's 10-yr note sale, causing a yield spike. Spain's 10-yr yield is higher by 16 basis points at 2.26% while Italy's benchmark yield has added 23 basis points to 2.63%

6:18 am: [BRIEFING.COM] S&P futures vs fair value: -34.00. Nasdaq futures vs fair value: -78.00.

6:18 am: [BRIEFING.COM] Nikkei...14,738.38...-335.10...-2.20%. Hang Seng...22,900.94...-239.10...-1.00%.

6:18 am: [BRIEFING.COM] FTSE...6,100.32...-111.30...-1.80%. DAX...8,408.25...-163.70...-1.90%.

Euro Slides on Periphery Bonds’ Slump By Andrea Wong Oct 16, 2014 5:06 PM ET

The dollar climbed versus a majority of its major peers with growth in the U.S. forecast to outpace Europe and Japan, and on speculation the worst slump against the yen in 15 months yesterday was overdone.

The Australian dollar and Brazilian real declined the most against the greenback after Federal Reserve Bank of St. Louis President James Bullard said U.S. economic fundamentals remain strong, sending bond yields higher. The euro fell as concern increased that a financial crisis is returning to the region’s so-called peripheral nations.

“U.S. Treasuries yields are higher, that’s a sign of overshooting earlier and we’re getting back to an orderly market,” said Masafumi Takada, a New York-based director at BNP Paribas SA. “Dollar-yen should come back up.”

The dollar rose 0.4 percent to 106.33 yen at 5 p.m. New York time, after falling as much as 1.7 percent yesterday, the steepest loss since July 2013. It gained 0.2 percent against the euro to $1.2809 per euro, while the 18-nation currency climbed 0.2 percent to 136.20 yen.

JPMorgan Chase & Co.’s Global FX Volatility Index increased to as much as 8.56 percent, the highest since Feb. 6. The measure has increased from 5.28 percent in July, the lowest on record.

Speculation the U.S. central bank will raise rates next year had led to a record rally in the U.S. currency. The advance started to reverse last week after minutes of the Sept. 16-17 Federal Open Market Committee meeting showed participants said expansion “might be slower than they expected if foreign economic growth came in weaker than anticipated.”

Fed ExpectationsThe currency plunged yesterday as a bigger-than-forecast drop in retail sales prompted traders to push back bets the Fed will raise interest rates until the end of next year.

“The data that sparked the move was weaker than expected but overall data-wise, and as far as the growth outlook is concerned, the U.S. looks more favorable than elsewhere,” Ian Stannard, the London-based head of European foreign-exchange strategy at Morgan Stanley said, referring to the decline in the dollar yesterday. Morgan Stanley predicts the U.S. currency will appreciate to $1.24 per euro by the end of this year.

The U.S. economy will expand 2.2 percent this year and 3 percent in 2015, according to Bloomberg News surveys. The euro area will grow 0.8 percent and 1.3 percent, while Japan’s will expand 1 percent in 2014 and 1.2 percent the following year, the surveys predict.

Bond markets in the so-called European peripheral nations slumped as euro-area finance ministers clashed with Greece’s leaders over their plan to leave its bailout, sparking concern that the nation won’t be able to finance itself at sustainable rates without the support of its regional partners.

Periphery YieldsGreece’s 10-year yield jumped 111 basis points, or 1.11 percentage point, to 8.96 percent after rising 85 basis points yesterday. Spain’s 10-year yield climbed six basis points to 2.17 percent. Even France (GFRN10) wasn’t immune to the selloff, with that nation’s 10-year yield increasing 12 basis points to 1.26 percent.

“Periphery bond yields have really exploded,” said Peter Kinsella, a senior foreign-exchange strategist at Commerzbank AG in London. “The worse that situation gets the more likely it is that the ECB has to do some more aggressive form of QE,” he said, referring to government bond purchases, or quantitative easing.

European Central Bank President Mario Draghi in Washington said on Oct. 11 that the central bank will use further unconventional monetary policy instruments if needed to support a recovery. The ECB has already implemented a negative deposit rate, offered cheap loans to banks and unveiled a plan to buy asset-backed securities.

Currency Report“It’s partly down to liquidation of overseas investors in euro-zone peripheral assets,” Neil Jones, head of hedge-fund sales at Mizuho Bank Ltd. in London said, referring to the euro’s decline. “They are selling the euro out and repatriating.”

In a twice-yearly report to Congress on foreign exchange, the U.S. Treasury Department said changes to China’s currency policy remain incomplete and the Asian nation should allow the market to play a greater role in setting the yuan’s value. The report covering the first half of this year concluded that no country was designated a currency manipulator.

The Chinese currency “remains significantly undervalued,” it said. The People’s Bank of China increased its daily reference rate by 0.1 percent to 6.1395 per dollar today, the highest since March 19.

“The lack of criticism from the U.S. may actually please China, which is happy to let the yuan gain a bit more,” said Daniel Chan, an analyst at Brilliant & Bright Investment Consultancy Ltd. in Hong Kong.

The yuan climbed 0.05 percent to 6.1231 per dollar, China Foreign Exchange Trade System prices show. It appreciated to 6.1209 earlier today, the strongest level since March 7.

To contact the reporter on this story: Andrea Wong in New York at

awong268@bloomberg.netTo contact the editors responsible for this story: Dave Liedtka at

dliedtka@bloomberg.net Cecile Gutscher

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage