Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

Attachment:

092914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1670.00.png [ 175.45 KiB | Viewed 329 times ]

092914-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+1670.00.png [ 175.45 KiB | Viewed 329 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$1,670.00 dollars or +16.70 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $1,670.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1897 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

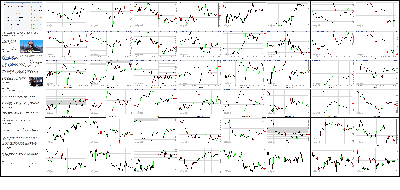

Attachment:

092914-Key-Price-Action-Markets.png [ 1.54 MiB | Viewed 345 times ]

092914-Key-Price-Action-Markets.png [ 1.54 MiB | Viewed 345 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:15 pm: [BRIEFING.COM] The stock market began the new week on a cautious note. The S&P 500 lost 0.3%, but managed to erase more than half of its opening decline. Thanks to the rebound, the benchmark index reclaimed its 50-day moving average (1976.78) after slipping below that level in the morning.

Equities slumped at the open amid a couple global developments that dampened the overall risk appetite. Continued student protests in Hong Kong and a potential response from China weighed on the Hang Seng index (-1.9%), while other regional indices held up relatively well with Japan's Nikkei (+0.5%) and the Shanghai Composite (+0.4%) posting gains.

Meanwhile in Europe, participants showed concerns about the Catalan independence referendum scheduled to take place on November 9. Over the weekend, the regional government outlined an official referendum plan despite pushback from national leaders. Spanish debt sold off on the developments with the 10-yr yield climbing four basis points to 2.22%. Another twist was introduced to the story during the afternoon when the Spanish Constitutional Court announced it will block the independence vote.

The overseas developments contributed to a lower start, but the key indices wasted little time in staging a rebound. The S&P 500 narrowed its loss to just five points during the initial 90 minutes of action and held its ground until the close.

In large part, the technology sector (-0.1%) was responsible for the rebound with chipmakers displaying relative strength. Intel (INTC 34.90, +0.64) surged 1.9% after announcing a partnership with Mitsubishi Electric to create next generation factory automation systems, while the PHLX Semiconductor Index climbed 0.1%.

Outside of Intel, most large cap sector components struggled to keep pace with the broader market. Facebook (FB 79.00, +0.21) and Microsoft (MSFT 46.44, +0.03) settled just above their flat lines, while Apple (AAPL 100.11, -0.64), Qualcomm (QCOM 74.82, -0.24), and Oracle (ORCL 38.44, -0.51) lagged.

The technology sector was the only group able to overtake the broader market, while the remaining five cyclical sectors ended behind the S&P 500. Notably, the energy space (-0.4%) widened its September loss to 6.5% and extended its Q3 decline to 8.0%.

Elsewhere, the consumer discretionary sector (-0.6%) lagged amid weakness in carmakers after Ford (F 15.11, -1.22) said it projects a pre-tax loss of $250 million for its European unit in 2015. The stock plunged 7.5%, while peer General Motors (GM 32.22, -0.95) lost 2.9%. Homebuilders also lagged despite lower Treasury yields. The iShares Dow Jones US Home Construction ETF (ITB 22.77, -0.16) lost 0.7%.

Although things were relatively quiet on the corporate front, M&A activity made some headlines. On that note, TIBCO Software (TIBX 23.65, +4.14) surged 21.2% after agreeing to be acquired by Vista Equity Partners for $24.00 per share, representing a 26.3% premium to the closing price on September 23. Separately, Athlon Energy (ATHL 58.32, +11.59) spiked 24.8% in reaction to news that Encana (ECA 21.59, +0.46) will acquire all of the issued and outstanding shares of ATHL for $58.50/share. Lastly, DreamWorks Animation (DWA 28.18, +5.82) jumped 26.0% amid speculation the company could be acquired by Softbank (SFTBY 35.24, -1.14).

Treasuries ended near their highs with the 10-yr yield falling six basis points to 2.48%.

Participation was below average with fewer than 640 million shares changing hands at the NYSE floor.

Economic data was limited to Personal Income/Spending and Pending Home Sales for August:

Related Stories

InPlay from Briefing.com Briefing.com

Stock Market News for September 15, 2014 Zacks

U.S. Stock Prices Gain, Helped by Data The Wall Street Journal

Dow closes at record high, again USA TODAY

Stocks Bounce As Nasdaq, S&P 500 Close With Small Gains Investor's Business Daily

Personal income increased 0.3% in August, up from an unrevised 0.2% increase in July, while the Briefing.com consensus expected an increase of 0.3%

The August employment report showed a 0.4% increase in aggregate earnings, which matched the 0.4% increase in wages and salaries

Personal spending levels increased 0.5% in August after no change in spending (from -0.1%) in July, while the Briefing.com consensus expected an increase 0.4%

Big gains in motor vehicle sales were a primary catalyst for a 0.4% increase in goods spending

Services spending rose 0.5% after reporting no change in July

Core PCE prices rose 0.1%, while the Briefing.com consensus expected an unchanged reading

Pending home sales for August fell 1.0%, which was worse than the 0.2% decrease forecast by the Briefing.com consensus o The July reading was revised down to 3.2% from 3.3%

Tomorrow, the Case-Shiller 20-city Index for July (Briefing.com consensus 7.4%) will be released at 9:00 ET, while the Chicago PMI for September (consensus 61.5) will cross the wires at 9:45 ET. The day's data will be topped off with the 10:00 ET release of the Consumer Confidence report for September (expected 92.0).

Nasdaq Composite +7.9% YTD

S&P 500 +7.0% YTD

Dow Jones Industrial Average +3.0% YTD

Russell 2000 -3.9% YTD

3:25 pm: [BRIEFING.COM] Dec gold saw modest gains today while the dollar index traded slightly below the unchanged line. The precious metal pulled back from a session high of $1222.50 per ounce set in early morning pit trade and chopped around the $1218.00 per ounce level for the remainder of pit trade, closing with a 0.3% gain at $1218.80 per ounce.

Dec silver dipped to a session low of $17.43 per ounce in morning floor trade but quickly rose back up towards the break-even line. It eventually settled with a 0.2% gain at $17.58 per ounce.

Nov crude oil lifted from its session low of $92.85 per barrel and trended higher. It broke into positive territory by mid-morning pit trade and settled with a 1.0% gain at $94.53 per barrel.

Nov natural gas also trended upwards after coming off its session low of $4.05 per MMBtu set shortly after equity markets opened. It climbed as high as $4.16 per MMBtu and closed with a 2.7% gain at $4.14 per MMBtu.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.5% with one hour remaining in the session. Tomorrow's affair will represent the final trading day of the quarter, which means the Q3 earnings reporting period will begin shortly thereafter.

With the earnings season still a couple weeks away, tomorrow morning will feature just one report from Walgreens (WAG 59.39, -0.79). The retailer is expected to report modest year-over-year earnings growth of 1.4% on $19.01 billion in revenue.

On the economic front, the Case-Shiller 20-city Index for July (Briefing.com consensus 7.4%) will be released at 9:00 ET, while the Chicago PMI for September (consensus 61.5) and September Consumer Confidence (expected 92.0) will cross the wires at 9:45 ET and 10:00 ET, respectively.

2:30 pm: [BRIEFING.COM] The S&P 500 trades lower by 0.6% with nine sectors showing afternoon losses. The energy sector (-1.0%) is the weakest performer at this juncture, which is fitting since the group has shown relative weakness throughout the month. The growth-sensitive sector has surrendered 7.1% in September with that slide widening the sector's quarter-to-date loss to 8.6%.

Meanwhile, crude oil slumped during the first half of the month, but has been able to reclaim the bulk of its September loss. The energy component has narrowed its month-to-date decline to 1.5% and currently trades near late August levels.

2:00 pm: [BRIEFING.COM] Afternoon action continues with the S&P 500 (-0.4%) trading within a few points of its rebound high. After cutting its opening loss in half, the benchmark index has been trading in sideways fashion near its 50-day moving average (1976.74). Similarly, the Nasdaq Composite (-0.3%) hovers near its own 50-day average (4496.79).

Given their current levels, the S&P 500 and Nasdaq are on track to enter the final session of September with respective losses of 1.4% and 1.8%. Tomorrow will also mark the end of the quarter with the two indices looking to hold their gains. The S&P 500 has added 0.8% since the end of Q2, while the Nasdaq is higher by 2.0% for the quarter.

1:30 pm: [BRIEFING.COM] The major indices remain stuck in red figures, but are well off their lows of the session established shortly after the start of trading with the Dow, Nasdaq, and S&P 500 down 178, 48, and 19 points, respectively.

Even though losses have been pared, declining issues still hold a commanding lead over advancing issues at the NYSE (2-to-1 margin) and the Nasdaq (8-to-5 margin).

Currently, nine out of ten economic sectors are losing ground with losses ranging from 0.2% to 0.6%. The winning standout today is the utilities sector.

The latter is up 0.4%, aided both by a drop in long-term rates today and NiSource's (NI 41.40, +2.82) outperformance after the company announced it will be splitting into two separate publicly-traded companies -- a pure-play natural gas pipeline company and a pure-play natural gas and electric utilities company -- in an effort to bolster shareholder value.

1:00 pm: [BRIEFING.COM] Equity indices trade in the red at midday with the Dow Jones Industrial Average (-0.5%) showing the largest decline. For its part, the S&P 500 is lower by 0.4% after reclaiming more than half of its original slide.

The opening drop followed a couple global developments that pressured the overall risk appetite. Continued student protests in Hong Kong and a potential response from China weighed on the Hang Seng index (-1.9%), while other regional indices held up relatively well with Japan's Nikkei (+0.5%) and the Shanghai Composite (+0.4%) posting gains.

Once European markets opened for action, participants began showing concerns about the Catalan independence referendum planned to take place on November 9. Over the weekend, the regional government outlined an official referendum plan despite pushback from national leaders. Spanish debt has been on the defensive with the 10-yr yield climbing four basis points to 2.22%.

Meanwhile in the U.S., equity indices followed their sharply lower open with a rally that briefly placed the Nasdaq (-0.3%) and S&P 500 (-0.4%) back above their respective 50-day moving averages. The technology sector (specifically chipmakers) fueled the rebound, but the group fell back in-line with the broader market when the S&P 500 dipped back below its 50-day average.

Similar to technology (-0.3%), the health care sector (-0.3%) made a brief appearance in the green with help from biotechnology. However, the iShares Nasdaq Biotechnology ETF (IBB 275.59, -0.82) has backed away from its high and now trades lower by 0.3%.

Elsewhere among influential sectors, energy (-0.6%) and financials (-0.5%) lag, while consumer discretionary (-0.4%) and industrials (-0.4%) trade in-line with the S&P 500.

Treasuries climbed overnight and have held near their highs notched at 9:00 ET. The 10-yr note is higher by 12 ticks with its yield at 2.48%.

Economic data was limited to Personal Income/Spending and Pending Home Sales for August:

Personal income increased 0.3% in August, up from an unrevised 0.2% increase in July, while the Briefing.com consensus expected an increase of 0.3%

The August employment report showed a 0.4% increase in aggregate earnings, which matched the 0.4% increase in wages and salaries

Personal spending levels increased 0.5% in August after no change in spending (from -0.1%) in July, while the Briefing.com consensus expected an increase 0.4%

Big gains in motor vehicle sales were a primary catalyst for a 0.4% increase in goods spending

Services spending rose 0.5% after reporting no change in July

Core PCE prices rose 0.1%, while the Briefing.com consensus expected an unchanged reading

Pending home sales for August fell 1.0%, which was worse than the 0.2% decrease forecast by the Briefing.com consensus

The July reading was revised down to 3.2% from 3.3%

12:30 pm: [BRIEFING.COM] Recent action saw the S&P 500 (-0.4%) back away from its rebound high amid continued weakness in influential sectors like financials (-0.5%), consumer discretionary (-0.5%), and energy (-1.0%). Meanwhile, the technology sector (-0.4%), which fueled the rebound off the lows, is pressuring the broader market once again.

Large cap components are keeping the tech sector under pressure with the likes of Apple (AAPL 99.88, -0.87), Google (GOOGL 584.56, -3.34), and Oracle (ORCL 38.44, -0.51) down between 0.6% and 1.3%. However, chipmaker names continue showing relative strength with the PHLX Semiconductor Index up 0.1%.

11:55 am: [BRIEFING.COM] The major averages continue hovering near their best levels of the session after a swift rebound from their lows. The S&P 500 (-0.2%) has had no issues reclaiming about 10 points, but still trades roughly five below its flat line.

As mentioned earlier, the technology sector (-0.1%) has helped the market climb off the lows, but other cyclical groups like consumer discretionary (-0.3%), financials (-0.4%), and energy (-0.5%) continue showing relative weakness. In the discretionary sector, homebuilders trade broadly lower despite today's retreat in Treasury yields. The iShares Dow Jones US Home Construction ETF (ITB 22.85, -0.08) is lower by 0.4% to widen its September decline to 5.0%.

As for Treasuries, the 10-yr note has inched down from its high with the benchmark yield ticking up to 2.49%.

11:30 am: [BRIEFING.COM] Equity indices have continued their rebound effort with the Nasdaq (-0.1%) making a brief appearance in the green with significant help from biotechnology and chipmakers. The iShares Nasdaq Biotechnology ETF (IBB 276.90, +0.49) is higher by 0.2%, while the PHLX Semiconductor Index has added 0.3%.

The relative strength of chipmakers has helped the technology sector erase the bulk of its opening loss. Intel (INTC 34.93, +0.67) has done some heavy lifting, climbing 1.9% after announcing a partnership with Mitsubishi Electric to create factory automation systems.

Other top-weighted technology components are mixed with Apple (AAPL 100.00, -0.73) down 0.7% and Facebook (FB 78.91, +0.12) up 0.2%.

11:00 am: [BRIEFING.COM] The major averages have spent the first 90 minutes of the session in steady climb off their opening lows. The S&P 500 (-0.4%) has cut its loss in half and currently finds itself right below the 50-day moving average (1976.59), which is a level that has posed a technical challenge for the benchmark index.

Elsewhere, the Nasdaq Composite (-0.2%) also dropped below its 50-day average (4496.89) at the start, but the tech-heavy index has been able to reclaim that level in recent action. Biotechnology has played a part in the rebound as evidenced by a modest 0.2% uptick in the iShares Nasdaq Biotechnology ETF (IBB 276.84, +0.43). Meanwhile, the health care sector (-0.1%) trades ahead of the remaining groups.

In addition to biotech, high-beta chipmakers have also showed signs of strength with the PHLX Semiconductor Index trading higher by 0.2%.

10:30 am: [BRIEFING.COM] Precious metals are mixed this morning while the dollar index trades slightly below the unchanged line.

Dec gold has been trading in positive territory but is trending lower. It pulled back from an overnight high of $1223.90 and is now up 0.2% at $1218.10.

Dec silver also pulled back from an overnight high of $17.64 and dipped into the red in recent action. It is now 0.3% lower at $17.49.

Nov crude oil brushed a session low of $92.85 in early morning pit trade but has lifted in recent action to chop around near the break-even level. It is currently flat at $93.54.

Nov natural gas has been trading higher this morning in a tight range between $4.05 and $4.08. Currently, it is up 0.8% at $4.06.

10:00 am: [BRIEFING.COM] The S&P 500 trades lower by 0.7%.

Just reported, pending home sales for August fell 1.0%, which was worse than the 0.2% decrease forecast by the Briefing.com consensus. Today's reading followed last month's revised increase of 3.2% (from 3.3%).

9:40 am: [BRIEFING.COM] The major averages began the session on the defensive amid broad weakness in the six cyclical sectors. The S&P 500 trades lower by 0.8% with five of six growth-sensitive groups trailing the broader market.

The energy sector (-1.3%), which has endured a rough September, began the day at the bottom of the leaderboard, while crude oil trades lower by 0.3% at $93.31/bbl. The remaining growth-sensitive groups are down near 0.9%, while the consumer discretionary sector (-0.7%) trades a bit ahead of the broader market.

On the upside, the utilities sector (+0.1%) is the lone advancer with help from lower yields. The 10-yr yield hovers at 2.48% after ending last week near 2.54%.

The Pending Home Sales report for August (consensus -0.2%) will be released at 10:00 ET.

9:15 am: [BRIEFING.COM] S&P futures vs fair value: -18.00. Nasdaq futures vs fair value: -42.50. The stock market is on track for a sharply lower start to the trading week with futures on the S&P 500 trading 18 points below fair value. The benchmark index will begin today's session near its 50-day moving average (1982.85) after spending the past two sessions in the neighborhood of that level.

Index futures have spent the entire night in negative territory with early weakness being traced back to concerns over continued student protests in Hong Kong. The situation pressured the Hang Seng (-1.9%), while other regional indices held up relatively well with Japan's Nikkei (+0.5%) and the Shanghai Composite (+0.4%) posting gains.

Over in Europe, investors have been displaying increased worries over the independence referendum planned to take place in Catalonia on November 9. The Catalan government outlined an official referendum plan over the weekend despite pushback from national leaders. Spanish debt has been pressured with the 10-yr yield up five basis points at 2.23%.

Domestically, M&A activity has been in focus this morning. On that note, TIBCO Software (TIBX 23.63, +4.12) has added 21.1% in pre-market after agreeing to be acquired by Vista Equity Partners for $24.00 per share, representing a 26.3% premium to the closing price on September 23. Separately, Athlon Energy (ATHL 58.26, +11.53) trades up 24.7% in reaction to news that Encana (ECA 21.66, +0.53) will acquire all of the issued and outstanding shares of ATHL for $58.50/share.

Finally, DreamWorks Animation (DWA 28.50, +6.14) has jumped 27.5% amid speculation the company could be acquired by Softbank (SFTBY 36.38, 0.00).

Treasuries hover on their highs with the 10-yr yield down six basis points at 2.48%.

The Pending Home Sales report for August (consensus -0.2%) will be released at 10:00 ET.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: -18.00. Nasdaq futures vs fair value: -43.30. The S&P 500 futures trade 18 points below fair value.

Markets fell across most of Asia. Student protests for democracy paralyzed business and government districts in Hong Kong, while also pressuring the global risk appetite.

Economic data was limited:

Hong Kong's Retail Sales rose 3.4% (previous -3.1%)

South Korea's current account surplus narrowed to $7.27 billion from $7.84 billion

------

Japan's Nikkei added 0.5%, ending just shy of seven-year highs. Heavyweight Softbank was a laggard, falling 1.2% as shares remained pressured after the Alibaba IPO.

Hong Kong's Hang Seng lost 1.9%, seeing significant outperformance as traders dumped shares in response to the protests. China Shenhua Energy added 0.2% and was the lone listing to finish in positive territory.

China's Shanghai Composite climbed 0.4% to its best level in 18 months. Coal stocks were among the leaders as Datong Coal Industry and Yanzhou Coal Mining rose 2.8% and 2.3%, respectively.

India's Sensex shed 0.1%. Blue chips finished mixed as Tata Consultancy Services climbed 3.1% and Mahindra & Mahindra lost 0.7%.

Major European indices trade lower across the board with Spain's IBEX (-1.3%) leading the slide. Despite opposition from Spanish authorities, the leader of the Catalan independence movement, Artur Mas, has signed a decree to authorize an independence referendum on November 9. Spanish bonds are on the defensive with the 10-yr yield up six basis points at 2.25%. Conversely, German Bunds have been in demand, lowering the benchmark one basis point to 0.91%.

Participants received several data points:

Eurozone Business and Consumer Survey worsened to 99.9 from 100.6 (expected 100.0)

Great Britain's BoE Consumer Credit expansion slowed to GBP898 million from GBP1.11 billion. Separately, Mortgage Approvals came in at 64.21K (expected 65.00K; previous 66.10K)

Spain's CPI fell 0.2% year-over-year (expected -0.3%; previous -0.5%), while Retail Sales rose 0.4% year-over-year (expected -0.3%; prior -0.2%)

------

Great Britain's FTSE is lower by 0.4% with financials and miners on the defensive. HSBC Holdings, Standard Chartered, and Rio Tinto are down between 1.3% and 1.8%. Oil services company, Petrofac, leads with a gain of 2.7%.

Germany's DAX trades down 0.7% with 29 of 30 components in the red. Commerzbank is the weakest performer, down 4.8%. On the flip side, Linde is higher by 0.8%.

In France, the CAC has given up 0.7%. Consumer names lag with LVMH Moet Hennessy and Pernod Ricard both down near 1.0%. Michelin leads with a gain of 1.1%.

Spain's IBEX is lower by 1.3% amid weakness in financials. Bankinter, BBVA, CaixaBank, and Santander are hold losses between 1.4% and 2.5%.

8:31 am: [BRIEFING.COM] S&P futures vs fair value: -11.80. Nasdaq futures vs fair value: -26.50. The S&P 500 futures trade 12 points below fair value.

August personal income increased 0.3%, which matched the Briefing.com consensus. Meanwhile, personal spending rose 0.5%, while the consensus expected an uptick of 0.4%.

Separately, core PCE prices rose 0.1%, while the Briefing.com consensus expected an unchanged reading.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: -9.80. Nasdaq futures vs fair value: -23.00. U. S. equity futures trade near their pre-market lows amid cautious action overseas. The S&P 500 futures hover 10 points below fair value, which suggests the benchmark index will start near its 50-day moving average (1982.85) after reclaiming that noteworthy level during Friday's session.

Index futures retreated overnight amid a continuation of public protests in Hong Kong. Also weighing on sentiment was news from Europe, indicating Catalonia will hold an independence referendum on November 9 in an attempt to break away from Spain.

Treasuries hold gains with the 10-yr yield down nearly four basis points at 2.50%.

Personal Income (Briefing.com consensus 0.3%) and Spending (consensus 0.4%) data for August will be reported at 8:30 ET alongside core PCE Prices (expected 0.0%). The day's data will be topped off with the Pending Home Sales report for August (consensus -0.2%).

In U.S. corporate news of note:

Athlon Energy (ATHL 58.12, +11.39): +24.4% in reaction to news that Encana (ECA 21.13, 0.00) will acquire all of the issued and outstanding shares of ATHL for $58.50/share

DreamWorks Animation (DWA 27.00, +4.64): +20.8% amid speculation the company could be acquired by Softbank (SFTBY 36.38, 0.00)

Tibco Software (TIBX 19.51, 0.00): to be acquired by Vista Equity Partners for $24.00 per share, representing a 26.3% premium to the closing price on September 23

Reviewing overnight developments:

Asian markets ended mixed. China's Shanghai Composite +0.4%, Japan's Nikkei +0.5%, and Hong Kong's Hang Seng -1.9%

In economic data:

Hong Kong's Retail Sales rose 3.4% (previous -3.1%)

South Korea's current account surplus narrowed to $7.27 billion from $7.84 billion

In news:

Equities in Hong Kong were pressured by concerns over the continuation of public protests that began at the end of last week

Major European indices trade lower across the board. Great Britain's FTSE -0.3%, Germany's DAX -0.6%, and France's CAC -0.6%. Elsewhere, Italy's MIB -1.0% and Spain's IBEX -1.0%

Participants received several data points:

Eurozone Business and Consumer Survey worsened to 99.9 from 100.6 (expected 100.0)

Great Britain's BoE Consumer Credit expansion slowed to GBP898 million from GBP1.11 billion. Separately, Mortgage Approvals came in at 64.21K (expected 65.00K; previous 66.10K)

Spain's CPI fell 0.2% year-over-year (expected -0.3%; previous -0.5%), while Retail Sales rose 0.4% year-over-year (expected -0.3%; prior -0.2%)

Among news of note:

Despite opposition from Spanish authorities, the leader of the Catalan independence movement, Artur Mas, has signed a decree to authorize an independence referendum on November 9. Spanish bonds are on the defensive with the 10-yr yield up six basis points at 2.25%.

6:34 am: [BRIEFING.COM] S&P futures vs fair value: -7.00. Nasdaq futures vs fair value: -16.00.

6:34 am: [BRIEFING.COM] Nikkei...16,310.64...+80.80...+0.50%. Hang Seng...23,229.21...-449.20...-1.90%.

6:34 am: [BRIEFING.COM] FTSE...9,470.78...-15.30...-0.20%. DAX...9,470.78...-19.90...-0.20%.

Dollar Climbs Versus Emerging-Market CurrenciesBy Andrea Wong Sep 29, 2014 5:17 PM ET

The dollar climbed to a six-month high against emerging-market currencies as signals the U.S. economy is improving bolstered the case for the Federal Reserve to raise interest rates for the first time since 2006.

Currencies of developing countries fell for a third day and volatility rose as unrest in Hong Kong damped risk appetite. Brazil’s real touched the weakest in almost six years after a poll showed President Dilma Rousseff widened her lead over opposition candidate Marina Silva. The U.S. dollar headed for its biggest monthly gain since 2012, while New Zealand’s currency reached a 13-month low.

“Developments in Hong Kong have definitely caught the market’s attention; it’s helping drive the risk-off sentiment,” said Shaun Osborne, chief currency strategist at Toronto-Dominion Bank, in a phone interview. “The dollar’s strength is starting to endanger some of the commodity currencies that have done quite well in the quantitative-easing environment.”

The MSCI EM Currency Index, which sets the weights of each currency equal to the relevant country weight in the MSCI Emerging Markets Index, fell 0.5 percent to 1,633.76 at 5 p.m. New York time, the lowest since March 27. Brazil’s real fell 1.1 percent to 2.4477 per dollar, the weakest since August 2013, and reached 2.4781, the least since December 2008. Indonesia’s rupiah declined 1.2 percent to 12,170 per dollar.

The Bloomberg Dollar Spot Index rose 0.2 percent to 1,068.85, the highest close since June 2010. It has increased 3.8 percent in September, headed for the most since May 2012.

Diverging PoliciesThe Fed is considering when to raise interest rates amid an improving U.S. economy, as the European Central Bank and the Bank of Japan use monetary stimulus to spur slumping economies. The U.S. central reiterated on Sept. 17 its pledge to hold rates at almost zero for a considerable time after completing a bond-purchase stimulus program under quantitative easing next month. It also warned the timing may move forward if data continue to exceed expectations.

Consumer spending in the U.S. increased 0.5 percent in August, Commerce Department figures showed today. A report on Sept. 26 showed the U.S. economy grew at a revised 4.6 percent annualized rate last quarter, the fastest since the last three months of 2011.

Central banks are “creating opportunities in the currency and rates markets,” Mihir Worah, who has taken over management of Pacific Investment Management Co.’s total return strategy with Mark Kiesel and Scott Mather, said on Pimco’s website. “Divergent monetary policy is likely to mean continued strength in the dollar, particularly against the euro and yen.”

Brazilian ElectionBrazil’s currency has lost 9.5 percent this quarter, the biggest drop in three years, as Rousseff pursues re-election amid economic turmoil.

Rousseff’s support rose to 40 percent for the Oct. 5 first-round vote, according to a Datafolha poll published Sept. 26 after markets were closed, up from 37 percent in the previous Datafolha survey released Sept. 19. Her opponent’s first-round support fell to 27 percent, down from 30 percent. Speculation a new government would revive economic growth had helped to push the real to a one-month high on Aug. 29.

JPMorgan Chase & Co.’s Global FX Volatility Index touched 7.95 percent, the highest intraday level since March 4. The average this year is 6.89 percent.

Kiwi DropsNew Zealand’s dollar slid as much as 2 percent to 77.09, the lowest since August 2013, after the country’s Reserve Bank said its currency sales in August were the most in seven years. It traded later at 77.62 U.S. cents, down 1.3 percent.

The nation’s prime minister, John Key, said the so-called Goldilocks level for the kiwi dollar is around 65 cents, Interest.co reported, citing comments to reporters. While it was logical for the central bank to intervene at these levels, Key wasn’t aware of such a move, he was reported as saying.

“Key is trying to burst the bubble,” Douglas Borthwick, head of foreign exchange at New York brokerage Chapdelaine & Co., said by phone. “He’s saying, ’New Zealand is an attractive place, but is it really that attractive?’”

The euro was little changed at $1.2685 after falling earlier to $1.2664, the weakest level since November 2012. The dollar rose 0.2 percent to 109.50 yen and touched 109.75, the most since August 2008. Europe’s shared currency gained 0.2 percent to 138.90 yen.

ECB MeetingECB policy makers meet Oct. 2. President Mario Draghi said last week the bank is able to implement more stimulus if required to stave off the threat of deflation in the euro area. He signaled this month he intends to expand the ECB’s balance sheet by as much as 1 trillion euros ($1.3 billion) with stimulus measures.

U.S. stocks fell today with emerging-market equities as tens of thousands of protesters swelled demonstrations in Hong Kong’s main districts pressing for free and open elections and the resignation of Chief Executive Leung Chun-ying. Student leaders set an Oct. 1 deadline for their demands to be met.

Hong Kong’s currency plunged amid the biggest police crackdown on protesters since the city returned to Chinese rule. The clashes, which saw anti-riot police use teargas and pepper spray on demonstrators, are disrupting businesses in one of Asia’s financial centers and risk a strong response from the government in Beijing if they continue.

The Hong Kong dollar, which is pegged to its U.S. peer, depreciated 0.15 percent to HK$7.7693 versus the greenback, the largest loss on a closing basis since 2011.

To contact the reporter on this story: Andrea Wong in New York at

awong268@bloomberg.netTo contact the editors responsible for this story: Dave Liedtka at

dliedtka@bloomberg.net Greg Storey, Paul Cox

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage