Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

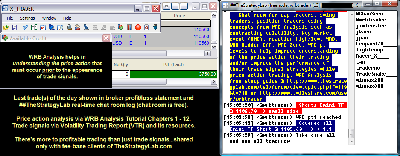

Attachment:

092514-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3750.00.png [ 176.85 KiB | Viewed 321 times ]

092514-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+3750.00.png [ 176.85 KiB | Viewed 321 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$3,750.00 dollars or +37.50 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $3,750.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1895 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

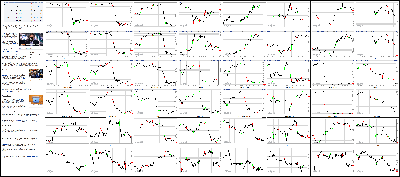

Attachment:

092514-Key-Price-Action-Markets.png [ 1.61 MiB | Viewed 342 times ]

092514-Key-Price-Action-Markets.png [ 1.61 MiB | Viewed 342 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:15 pm: [BRIEFING.COM] The stock market endured a broad-based retreat on Thursday that pressured the Nasdaq (-1.9%) and the S&P 500 (-1.6%) below their 50-day moving averages, while the Dow (-1.5%) notched a session low just above that mark. All ten sectors were encompassed in the slide with eight groups posting losses of 1.0% or more.

Equities began the day with modest losses and continued heading lower through the first 90 minutes of the session. Interestingly, dip-buyers showed very little interest in getting involved, which resulted in new session lows during the afternoon.

The reluctance to step into the fold was driven in part by the lack of notable leadership. To that point, all six cyclical sectors ended in-line or behind the S&P 500 with high-beta areas like biotechnology and chipmakers finishing among the laggards. The iShares Nasdaq Biotechnology ETF (IBB 273.97, -5.32) and the PHLX Semiconductor Index both lost 1.9%.

Both industry groups contributed to the underperformance of the Nasdaq, which also had to contend with significant weakness in its top-weighted component. Shares of Apple (AAPL 97.87, -3.88) tumbled 3.8% to end below the 50-day moving average for the first time since April 23. As for the technology sector (-2.3%), the group spent the day at the bottom of the leaderboard.

Meanwhile, the remaining cyclical sectors did not fare much better. The energy space (-1.5%) displayed relative strength in the early going, but fell in line with the market as the session wore on. The growth-sensitive sector widened its September decline to 7.1%.

The wide-ranging slide did not spare typical areas of relative strength like blue chip names and utility stocks. All 30 Dow components settled in the red with just three index members posting losses slimmer than 1.0%. As for utilities, the sector fell 0.6% despite a retreat in Treasury yields. The 10-yr note climbed throughout the session for a half-point gain to lower the benchmark yield six basis points to 2.51%.

Also of note, the Dollar Index (85.23, +0.19) pulled back from its morning high, but remained at its best level since 2010. The greenback retreated from highs amid intraday strength in the Japanese yen and the British pound. The yen rallied from its overnight low of 109.39 to 108.70 against the dollar, while the pound spiked off its low after Bank of England Governor Mark Carney said the first rate hike from the BoE has gotten closer.

The daylong weakness caused participants to increase their demand for volatility protection, sending the CBOE Volatility Index (VIX 15.95, +2.68) to its highest level since early August.

Participation was above average with nearly 720 million shares changing hands at the NYSE.

Economic data included Initial Claims and Durable Orders:

The initial claims level increased by 12,000 to 293,000 from an upwardly revised 281,000 (from 280,000), while the Briefing.com consensus expected an increase to 300,000

Once again, the Department of Labor reported that there were no special factors impacting the claims level, which implies labor market conditions are at, or very near, full employment

Durable goods orders fell 18.2% in August after increasing a slightly downwardly revised 22.5% (from 22.6%) in July, while the Briefing.com consensus expected a decline of 16.3%

A surge in aircraft orders in July resulted in the largest monthly increase in overall durable goods last month. The normal payback period came immediately and resulted in the largest monthly decline in overall orders in August

Tomorrow, the third estimate of Q3 GDP will be released at 8:30 ET (Briefing.com consensus 4.6%), while the final reading of the Michigan Sentiment index for September will cross the wires at 9:55 ET (consensus 85.0).

Nasdaq Composite +7.0% YTD

S&P 500 +6.4% YTD

Dow Jones Industrial Average +2.2% YTD

Russell 2000 -4.7% YTD

3:30 pm: [BRIEFING.COM] Dec gold traded in the red in overnight and early morning action while the dollar index held near its best levels since July 2010. Prices fell as low as $1206.60 per ounce, the metal's lowest level since January 2. Despite the early weakness, gold gained steam heading into afternoon floor trade and broke into positive territory. It brushed a session high of $1224.80 per ounce and settled with a 0.2% gain at $1221.70 per ounce.

Dec silver chopped around in negative territory during all of today's floor trade. It touched $17.27 per ounce as equity markets opened, its lowest since early 2010. Unable to gain much momentum, it settled with a 1.4% loss at $17.44 per ounce.

Nov crude oil touched a session high of $93.46 per barrel but retreated back into negative territory in afternoon action. It traded as low as $92.05 per barrel and settled with a 0.4% loss at $92.49 per barrel.

Nov natural gas lifted from its session low of $3.87 per MMBtu following inventory data that showed a build of 97 bcf when a build of 94-97 bcf was anticipated. It broke above the unchanged line in afternoon action and settled with a 1.0% gain at $4.01 per MMBtu, just below its session high of $4.02 per MMBtu.

3:00 pm: [BRIEFING.COM] The S&P 500 trades lower by 1.4% with one hour remaining in the session. Sector standing has not changed much with the technology sector (-2.1%) displaying the largest decline, while the utilities sector trades ahead of the broader market with a loss of 0.2%.

Investors will receive a couple quarterly reports of note after today's closing bell with Nike (NKE 79.69, -1.15) and Micron (MU 31.59, -0.63) set to report their results. The Capital IQ consensus expects Micron to show earnings growth of 305% on $4.15 billion in revenue. As for Nike, the apparel company is expected to report earnings growth of 2.3% on revenue of $7.78 billion.

The same two sectors will be represented tomorrow morning with BlackBerry (BBRY 9.95, -0.56) and Finish Line (FINL 29.64, -0.16) on the schedule.

2:30 pm: [BRIEFING.COM] Equity indices continue trolling near their lows, while Treasuries are on their highs with the 10-yr yield down five basis points at 2.51%.

This morning we highlighted the Dollar Index, which has climbed to its best level since 2010. The index remains at a four-year high, but has narrowed today's advance to 0.1%. The pullback took place during today's retreat in equities with the yen gaining ground on the dollar. The dollar/yen pair notched an overnight high at 109.39, but now trades near 108.63.

Elsewhere, Treasuries remain bid with the 10-yr note holding a half-point gain with its yield at 2.51%.

2:00 pm: [BRIEFING.COM] Afternoon action continues with the S&P 500 trading near its recently-established session low. Including today's decline, the S&P 500 is now down 2.1% for the week and lower by 1.8% so far in September.

The month-to-date loss puts the S&P 500 in the middle of the pack as the Dow sports a month-to-date decline of 0.9%, while the Nasdaq has surrendered 2.4% since the end of August. Small-cap stocks have weighed on the Nasdaq, but their weakness has been even more pronounced in the Russell 2000, which holds a month-to-date loss of 5.5% and is down 4.4% year-to-date.

1:30 pm: [BRIEFING.COM] With the stock market rallying back nicely on Wednesday after finding technical support at its 50-day moving average, today's quick reversal has raised more than a few eyebrows, especially since it took the S&P 500 right through its 50-day moving average at 1976.

Selling activity has abated somewhat since the violation of that technical support area, yet buyers have been a reluctant bunch as a rash of angst-inducing rationales for today's sell-off have been floated (eg. forced selling, high-yield bond weakness, Russia reportedly contemplating legislation that would allow it to seize foreign assets on its soil, ongoing dollar strength, valuation and growth concerns, etc.).

Apple's (AAPL 98.68, -3.07) 3.0% decline is certainly having an influential impact on the S&P 500 and Nasdaq Composite, yet there really isn't any leadership to speak of to help offset Apple's weakness. Decliners are outpacing advancers at the NYSE by a 5-to-1 margin and they are leading advancers at the Nasdaq by a better than 4-to-1 margin.

Every stock in the Dow Jones Industrial Average is down at this time and 9 out of 10 S&P sectors are down at least 1.0%. The utilities sector is the best-performing area -- relatively speaking -- as it is down "only" 0.5%.

12:55 pm: [BRIEFING.COM] The major averages trade broadly lower at midday with the Nasdaq Composite pacing the decline. The tech-heavy index has surrendered 1.7%, while the S&P 500 (-1.4%) trades a bit ahead.

Equity indices did not waste any time this morning, spending the first 90 minutes of the session in a steady retreat that erased yesterday's advance and sent the S&P 500 and Nasdaq below their 50-day moving averages.

The impact of the technical breach has been intensified by significant weakness in the top-weighted sector-technology (-2.0%). Furthermore, the largest component by weight-Apple (AAPL 98.70, -3.05)-began the session with a sharp drop after providing leadership in recent days. Currently, the stock is lower by 3.0%.

Although the tech sector slumped to the bottom of the leaderboard at the start, other groups have not performed much better. The remaining five cyclical sectors all sport losses near 1.4%.

The first-half slide has not spared typical areas of relative strength like blue chip names or rate-sensitive utilities. The price-weighted Dow trades in-line with the S&P 500 amid losses in all 30 components. Caterpillar (CAT 99.46, -1.74), UnitedHealth (UNH 86.12, -2.09), Goldman Sachs (GS 183.99, -3.82), and Intel (INTC 34.10, -0.66) are all down near 2.0%, which highlights the fact that today's losses have encompassed all sectors.

For its part, the utilities sector (-0.4%) is the only group with a slimmer decline than 1.0%. The sector hovers in the red despite today's retreat in rates. The 10-yr yield is lower by five basis points at 2.52%.

The widespread losses have led to increased demand for volatility protection, sending the CBOE Volatility Index (VIX 16.21, +2.94) to its best level since early August.

Economic data included Initial Claims and Durable Orders:

The initial claims level increased by 12,000 to 293,000 from an upwardly revised 281,000 (from 280,000), while the Briefing.com consensus expected an increase to 300,000

Once again, the Department of Labor reported that there were no special factors impacting the claims level, which implies labor market conditions are at, or very near, full employment

Durable goods orders fell 18.2% in August after increasing a slightly downwardly revised 22.5% (from 22.6%) in July, while the Briefing.com consensus expected a decline of 16.3%

A surge in aircraft orders in July resulted in the largest monthly increase in overall durable goods last month. The normal payback period came immediately and resulted in the largest monthly decline in overall orders in August

12:25 pm: [BRIEFING.COM] The stock market remains pinned to lows amid broad-based weakness. To that point, the A/D line has moved off its worst level of the day, but the improvement has been minor and there are still nearly six names trading in the red for each advancer.

Notably, the technology sector (-2.0%), which has lagged since the start, has recently inched down to a fresh low for the session with shares of Apple (AAPL 98.62, -3.12) widening their loss to 3.1%. Elsewhere among influential components, Google (GOOGL 587.39, -11.03), Intel (INTC 33.93, -0.82), and Microsoft (MSFT 46.26, -0.82) are down between 1.7% and 2.3%.

The continued weakness has provided support to Treasuries. The 10-yr note is now higher by 14 ticks with its yield down five basis points at 2.52%.

12:00 pm: [BRIEFING.COM] Equity indices continue hovering near their lows with few signs of dip buyers ready to test the waters.

Five of six cyclical sectors display losses of 1.2% or more, while the energy sector (-1.0%) trades a bit ahead of the broader market. However, it is worth mentioning that the sector has been the weakest performer of the month with today's loss widening its September decline to 6.9%. For its part, crude oil is higher by 0.1% today, but down 3.0% for the month.

Dollar strength has contributed to the lower price of crude while also weighing on earnings prospects of major sector components. The Dollar Index (85.22, +0.20) has added 0.2% today and is up 3.0% since the end of August.

11:30 am: [BRIEFING.COM] The S&P 500 (-1.2%) has maintained a narrow range near its session low since our last update after spending the initial 90 minutes in a steady slide. Meanwhile, the price-weighted Dow trades in-line with the benchmark index with all 30 of its components sitting in the red.

The losses have not been isolated to any particular industry group as representatives from sectors like industrials, health care, financials, and technology appear among the laggards. On that note, Caterpillar (CAT 99.35, -1.85), UnitedHealth (UNH 86.53, -1.68), Goldman Sachs (GS 184.84, -2.97), and Visa (V 210.64, -3.77) are all down near 1.8%.

With stocks enduring broad-based weakness, participants have increased their demand for volatility protection as evidenced by the CBOE Volatility Index (VIX 15.73, +2.46), which has jumped to its highest level since early August.

11:00 am: [BRIEFING.COM] Broad-based weakness in equities has pressured the S&P 500 (-1.2%) below its 50-day moving average after the index avoided slipping below that level during yesterday's session.

Cyclical sectors have fueled the retreat with five of six groups trading in-line or behind the S&P 500. The technology sector (-1.7%) was an early source of weakness and the group remains at the bottom of the leaderboard with its top component-Apple (AAPL 98.03, -3.72)-now down 3.7%. High-beta chipmakers tried to withstand the pressure in the early going, but the PHLX Semiconductor Index (-1.7%) trades in-line with the sector at this juncture.

Elsewhere, the high-beta biotech group has surrendered the bulk of its gain from yesterday. The iShares Nasdaq Biotechnology ETF (IBB 273.86, -5.43) trades down 1.9%, which has contributed to the relative weakness in the Nasdaq Composite. For its part, the health care sector (-1.2%) has kept pace with the S&P 500.

Also of note, the retreat has coincided with a rally in the yen after the Japanese currency spent the first three weeks of September in a steady retreat. The dollar/yen pair started the month near 104.14, ended at 109.01 yesterday, and now hovers near 108.70.

Throw in some murmurings about end-of-quarter rebalancing (trimming stocks and buying bonds as global economic data disappoints) and weak-handed long positions bailing out, and it is leading to a decidedly negative slant on things at this juncture.

10:35 am: [BRIEFING.COM] Precious metals continue to trade lower while the dollar index holds near its best levels since July 2010.

Dec gold fell as low as $1206.60 in overnight trade, its lowest level since January 2. It has since erased some of the loss and is now down 0.2% at $1216.80.

Dec silver touched $17.27 as equity markets opened, its lowest since early 2010. It is currently at $17.50, or 1.2% lower.

Nov crude oil gave up early morning gains as it pulled back from a session high of $93.46. It is now at $92.38, or 0.4% lower.

Nov natural gas is also trading in the red this morning. It touched a session low of $3.87 in recent action but rallied slightly on inventory data that showed a build of 97 bcf when expectations called for a build of 94-97 bcf. It is currently down 1.1% at $3.92.

10:00 am: [BRIEFING.COM] The major averages have extended their losses with the Nasdaq Composite (-1.0%) enduring the strongest selling pressure. Fittingly, the technology sector (-1.2%) is the weakest performer, and the only group holding a loss larger than 1.0% at this time.

The technology sector and the Nasdaq Composite have both been pressured by their top component. Shares of Apple (AAPL 99.16, -2.59) trade lower by 2.6%. Biotechnology also weighs on the Nasdaq with the iShares Nasdaq Biotechnology ETF (IBB 277.05, -2.24) down 0.8%.

Also of note, Treasuries have built on their gains. The 10-yr yield is now lower by four basis points at 2.53%.

9:40 am: [BRIEFING.COM] As expected, the stock market began the session on a cautious note. The S&P 500 trades lower by 0.4% with nine sectors holding opening losses.

The industrial sector (-0.5%) was among yesterday's laggards and the group began today's session in the same position. Transports lag with the Dow Jones Transportation Average trading down 0.7%.

Furthermore, the top-weighted technology sector (-0.4%) has also pressured the market in the early going. Shares of Apple (AAPL 100.41, -1.34) trade lower by 1.3%, which has contributed to the weakness. Meanwhile, high-beta chipmakers have tried to resist the pressure. The PHLX Semiconductor Index has given up 0.3% so far.

On the upside, the utilities sector (+0.1%) is the lone advancer at this time.

9:13 am: [BRIEFING.COM] S&P futures vs fair value: -4.20. Nasdaq futures vs fair value: -9.80. The stock market is on track for a cautious start as futures on the S&P 500 trade four points below fair value after failing to make a sustained move into positive territory during the overnight session. However, the Dollar has continued its recent advance, pushing the Dollar Index (85.33, +0.30) to its best level since 2010.

Participants did not receive any earnings of note today, while economic data featured just two reports.

The initial claims level increased by 12,000 to 293,000 from an upwardly revised 281,000 (from 280,000), while the Briefing.com consensus expected an increase to 300,000. Once again, the Department of Labor reported that there were no special factors impacting the claims level. If this is true, then the lack of biases in the data imply that labor market conditions are at, or very near, full employment.

Separately, Durable goods orders fell 18.2% in August after increasing a slightly downwardly revised 22.5% (from 22.6%) in July. The Briefing.com consensus expected a decline of 16.3%. A surge in aircraft orders in July resulted in the largest monthly increase in overall durable goods last month. The normal payback period came immediately and resulted in the largest monthly decline in overall orders in August.

Treasuries hover at their best levels of the morning with the 10-yr yield down three basis points near 2.54%.

9:00 am: [BRIEFING.COM] S&P futures vs fair value: -4.60. Nasdaq futures vs fair value: -10.50. The S&P 500 futures trade five points below fair value.

The major Asian bourses endured a mixed session. Reserve Bank of Australia chief Glenn Stevens indicated he would not rule out home-lending curbs in an effort to slow runaway home prices. Elsewhere, Taiwan's central bank held its key rate steady at 1.875%.

In economic data:

Japan's Corporate Services Price Index ticked up to 3.5% from 3.4% (expected 3.7%)

Hong Kong's trade deficit narrowed to HKD31.50 billion from HKD42.10 billion (expected deficit of HKD43.30 billion) as imports rose 3.4% month-over-month (expected 6.7%; previous 7.5%) and exports increased 6.4% (consensus 7.4%; prior 6.8%)

------

Japan's Nikkei gained 1.3% to finish at its best level in almost seven years. The weak yen continued to fuel exporters as Toyota Motor added 1.7% and Fanuc climbed 1.0%.

Hong Kong's Hang Seng lost 0.6%, ending at a two-month low as action slipped below the 100-day moving average. Casino shares remained weak as Galaxy Entertainment slumped 3.5% and Sands China fell 2.9% in anticipation of poor Macau gaming revenue figures.

China's Shanghai Composite ticked up 0.1% to its best close in six months. Brokerage names saw some profit-taking as Citic Securities and Hong Yuan Securities lost 1.3% and 1.9%, respectively.

India's Sensex slid 1.0% to a one-month low. Financials remained weak as Axis Bank sank 4.8% and State Bank of India fell 4.4%.

Major European indices have slipped from their highs with Great Britain's FTSE (-0.2%) leading to the downside. European Central Bank President Mario Draghi commented on policy, saying the ECB stands ready to change the size or composition of its measures.

Participants received several data points:

Eurozone M3 Money Supply rose 2.0% year-over-year (expected 1.9%; last 1.8%), while Private Loans fell 1.5%, as expected

Italy's Retail Sales ticked down 0.1% month-over-month (expected 0.2%; prior -0.1%), while the year-over-year reading fell 1.5% (consensus -0.7%; last -2.7%)

Great Britain's CBI Distributive Trades Survey fell to 31 from 37 (expected 30)

Spain's PPI fell 0.6% year-over-year (expected -0.1%; previous -0.5%)

------

Great Britain's FTSE is lower by 0.4% with miners on the defensive. Anglo American, BHP Billiton, Fresnillo, and Randgold Resources are down between 2.1% and 3.5%. Vodafone Group outperforms with a gain of 1.7%.

In France, the CAC trades up 0.1% with Airbus Group in the lead. The stock has added 3.7%. Consumer names lag with Carrefour, Danone, and L'Oreal holding losses between 0.4% and 2.3%.

Germany's DAX is higher by 0.2% amid strength in utilities. E.On and RWE are both up near 1.4%. BASF is the weakest performer, down 1.0%.

8:32 am: [BRIEFING.COM] S&P futures vs fair value: -2.00. Nasdaq futures vs fair value: -4.50. The S&P 500 futures trade two points below fair value.

The latest weekly initial jobless claims count totaled 293,000, while the Briefing.com consensus expected a reading of 300,000. Today's tally was above the revised prior week count of 281,000 (from 280,000). As for continuing claims, they rose to 2.439 million from 2.432 million.

August durable goods orders tumbled 18.2%, which was worse than the 16.3% decrease expected among economists polled by Briefing.com. This comes after the prior month's revised reading reflected a surge of 22.5% (from 22.6%). Excluding transportation, durable orders increased 0.7% (consensus 0.7%) to follow the prior month's revised decrease of 0.5% (from -0.7%).

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +0.50. Nasdaq futures vs fair value: +1.00. U.S. equity futures trade little changed despite upbeat action overseas. The S&P 500 futures hover within a point of fair value. Index futures respected narrow ranges overnight, but the greenback remained hot, sending the Dollar Index (85.42, +0.38) to its best level since 2010. The dollar strength has come at the expense of the euro (-60 pips) and the Canadian dollar (-50 pips), while the British pound (-20 pips) has held up relatively well.

Participants have not received any market-moving earnings this morning, while economic data will be limited to weekly Initial Claims (Briefing.com consensus 300K) and Durable Orders for August (consensus -16.3%). Both reports will be released at 8:30 ET.

Treasuries hold gains with the 10-yr yield down almost two basis points at 2.55%.

In U.S. corporate news of note:

Jabil Circuit (JBL 21.67, +0.82): +4.0% after beating estimates and raising its guidance.

Yahoo! (YHOO 39.59, -0.29): -0.7% after RBC Capital Markets downgraded the stock to 'Sector Perform' from 'Outperform.'

Reviewing overnight developments:

Asian markets ended mixed. Hong Kong's Hang Seng -0.6%, China's Shanghai Composite +0.1%, and Japan's Nikkei +1.3%

In economic data:

Japan's Corporate Services Price Index ticked up to 3.5% from 3.4% (expected 3.7%)

Hong Kong's trade deficit narrowed to HKD31.50 billion from HKD42.10 billion (expected deficit of HKD43.30 billion) as imports rose 3.4% month-over-month (expected 6.7%; previous 7.5%) and exports increased 6.4% (consensus 7.4%; prior 6.8%)

In news:

Asian Development Bank lowered its GDP forecast for Southeast Asia to 4.6% from 5.0%.

Major European indices trade mostly higher. Great Britain's FTSE is flat, France's CAC +0.3%, and Germany's DAX +0.5%. Elsewhere, Spain's IBEX +0.7% and Italy's MIB +0.8%

Participants received several data points:

Eurozone M3 Money Supply rose 2.0% year-over-year (expected 1.9%; last 1.8%), while Private Loans fell 1.5%, as expected

Italy's Retail Sales ticked down 0.1% month-over-month (expected 0.2%; prior -0.1%), while the year-over-year reading fell 1.5% (consensus -0.7%; last -2.7%)

Great Britain's CBI Distributive Trades Survey fell to 31 from 37 (expected 30)

Spain's PPI fell 0.6% year-over-year (expected -0.1%; previous -0.5%)

Among news of note:

European Central Bank President Mario Draghi commented on policy, saying the ECB stands ready to change the size or composition of its measures.

6:26 am: [BRIEFING.COM] S&P futures vs fair value: -0.50. Nasdaq futures vs fair value: flat.

6:26 am: [BRIEFING.COM] Nikkei...16,374.14...+206.70...+1.30%. Hang Seng...23,768.13...-153.50...-0.60%.

6:26 am: [BRIEFING.COM] FTSE...6,695.30...-11.00...-0.20%. DAX...9,698.05...+35.40...+0.40%.

Dollar Climbs to Four-Year High on Rate Bets; Yen Rallies By Rachel Evans Sep 25, 2014 5:13 PM ET

The dollar rose to a four-year high as Goldman Sachs Group Inc., Morgan Stanley and Bank of America Corp. forecast further strength amid bets the Federal Reserve will raise interest rates before its peers do.

The yen gained versus 31 major peers after Japan’s health minister signaled there’s no hurry on public-pension-fund changes that may boost investment in overseas assets. The greenback reached the strongest since November 2012 versus the euro before data tomorrow forecast to show U.S. economic growth quickened. New Zealand’s dollar slid to a one-year low as the nation’s central bank signaled possible intervention.

“Central-bank divergence is probably one of the keys to this dollar rally,” Lennon Sweeting, a San Francisco-based dealer at the broker and payment provider USForex Inc., said in a phone interview. “That divergence will only get greater as Europe tries to take a more accommodative stance and stimulate the economy there, while the U.S. does appear to be on an upward trajectory.”

The Bloomberg Dollar Spot Index, which tracks the U.S. currency against 10 of its major peers, increased 0.3 percent to 1,062.75 at 5 p.m. New York time, the highest close since June 2010. It has gained 5.9 percent since June 30, headed for the biggest quarterly advance in three years.

The yen strengthened 0.3 percent to 108.75 per dollar after depreciating 0.3 percent earlier to 109.37. It touched 109.46 on Sept. 19, the weakest since August 2008. The dollar gained 0.2 percent to $1.2751 per euro and reached $1.2697, the strongest level since Nov. 16, 2012. The euro dropped 0.5 percent to 138.67 yen.

Volatility RisesA measure of currency-market price swings increased for a fourth day, the longest stretch since July. JPMorgan Chase & Co.’s Global FX Volatility Index rose to 7.70 percent. The average this year is 6.89 percent.

Stocks dropped and Treasuries rose. The Standard & Poor’s 500 Index lost 1.6 percent, and U.S. 10-year note yields dropped to 2.50 percent, a two-week low. Gold touched $1,207.04 an ounce, the least since January, before ending the day at $1,221.58, up 0.4 percent.

Japan’s currency erased losses versus the dollar after Health Minister Yasuhisa Shiozaki cast doubt on the timing of a bill to reform the country’s pensions as he spoke on a television program, Yomiuri newspaper reported.

‘Push-Back’The nation is overhauling its Government Pension Investment Fund, the world’s biggest retirement fund, to make it more competitive. The GPIF invested about 55 percent of its 126.6 trillion yen ($1.2 trillion) in Japanese bonds as of March. Prime Minister Shinzo Abe has been seeking to spur better returns by having the fund buy more risky assets.

“It seems as if there’s some push-back on the GPIF reform,” said Mark McCormick, a foreign-exchange strategist in New York at Credit Agricole SA. “That’s clearly a positive development for the yen.”

Brazil’s real led emerging market currencies lower, tumbling 1.8 percent to 2.4278 per dollar as polls showed more support for President Dilma Rousseff before the Oct. 5 election amid a recession.

The New Zealand dollar was the biggest loser among the U.S. currency’s 31 major peers, sliding 1.9 percent to 79.24 U.S. cents. It touched 79.13 cents, the lowest level since Sept. 6, 2013.

Worst PerformanceThe kiwi, the currency is called for the image of the flightless bird on the NZ$1 coin, has fallen 4.9 percent in the past three months, the worst performance in a basket of 10 developed-nation currencies tracked by Bloomberg Correlation-Weighted Indexes.

Reserve Bank of New Zealand Governor Graeme Wheeler, in an unscheduled statement, called the kiwi’s level “unjustified,” one of the central bank’s criteria for intervention.

“The RBNZ governor’s comment on the ‘unjustified and unsustainable’ exchange rate is another example of jaw-boning,” said Joseph Capurso, a currency strategist at Commonwealth Bank of Australia in Sydney.

Sterling pared a decline against the dollar after Bank of England Governor Mark Carney said the case for interest-rate increases has become “more balanced.” Speaking to a conference of actuaries in Newport, Wales, Carney said the timing of the first interest-rate rise will depend on data and the BOE has no pre-set course.

“Carney’s definitely preparing the ground for the first interest-rate hike,” said Jane Foley, a senior currency strategist at Rabobank International in London.

The pound ended the day at $1.6318, down 0.1 percent, after dropping 0.4 percent earlier.

Dollar DemandThe dollar rose against most major currencies as Goldman Sachs and Bank of America highlighted in client notes diverging monetary policy in the U.S. and Europe as a support of further strength. Morgan Stanley also wrote that it sees the rally continuing thanks to positive economic data and expectations for rising U.S. government bond yields.

“There’s demand for the dollar,” said Richard Cochinos, head of Americas Group of 10 currency strategy at Citigroup Inc. in New York. “In the context of concerns about overall global growth, the U.S. is sticking out as an island of stability.”

A government report tomorrow is forecast to show U.S. gross domestic product grew 4.6 percent in the second quarter, more than the previous estimate of 4.2 percent released Aug. 28.

There’s a 75 percent chance the Fed will raise its benchmark target rate by September 2015, according to data compiled by Bloomberg based on federal funds futures.

The European Central Bank has decreased interest rates to record lows, and Draghi said policy makers are willing to use other tools if needed. The Bank of Japan has pledged to maintain unprecedented stimulus to spur economic growth.

To contact the reporter on this story: Rachel Evans in New York at

revans43@bloomberg.netTo contact the editors responsible for this story: Dave Liedtka at

dliedtka@bloomberg.net Greg Storey, Paul Cox

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage