Trade Results of M.A. Perry

Trade Results of M.A. Perry Trader and Founder of

WRB Analysis (wide range body/bar analysis)

Price Action Trading (no technical indicators)

Phone: +1 708 572-4885

Free Chat Room:

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164Business Hours: 8am - 5pm est (Mon - Fri)

questions@thestrategylab.com (24/7)

http://twitter.com/wrbtrader (24/7)

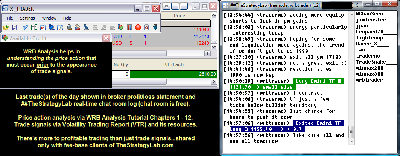

Attachment:

092414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2610.00.png [ 176.06 KiB | Viewed 305 times ]

092414-wrbtrader-Price-Action-Trading-PnL-Blotter-Profit+2610.00.png [ 176.06 KiB | Viewed 305 times ]

click on the above image to view today's performance verification Price Action Trade Performance for Today: Emini TF ($TF_F) futures @

$2,610.00 dollars or +26.10 points, Emini ES ($ES_F) futures @

$0.00 dollars or +0.00 points, Light Crude Oil CL ($CL_F) futures @

$0.00 dollars or +0.00 points, Gold GC ($GC_F) futures @

$0.00 dollars or +0.00 points and EuroFX 6E ($6E_F) futures @

$0.00 dollars or +0.0000 ticks.

Total Profit @ $2,610.00 dollarsRussell 2000 Emini TF Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

The ICE S&P 500 Emini ES Futures: 1 tick or 0.25 = $12.50 dollars and there's more contract information @

CMEGroup Light Crude Oil CL (WTI) Futures: 1 tick or 0.01 = $10.00 dollars and there's more contract information @

CMEGroup Gold GC Futures: 1 tick or 0.10 = $10.00 dollars and there's more contract information @

CMEGroupEuroFX 6E Futures: 1 tick or 0.0001 = $12.50 dollars and there's more contract information @

CMEGroup In addition, all of my trades were posted real-time in the timestamp ##TheStrategyLab chat room. You can read

today's price action trading information about my trades (e.g. time, price entry, contract size, price exit) as the trade traversed to its completion. Also, sometimes I'll post

real-time trading tips involving WRBs, WRB Hidden GAPs, Key Market Events (KME), Tutorial Chapters 2 & 3, WRB Zones, Reaction Highs/Lows, Contracting Volatility or Expanding Volatility. Its all

archived @ http://www.thestrategylab.com/ftchat/forum/viewtopic.php?f=134&t=1894 Quote:

If any of my

real-time posted trades are via key concepts discussed in the WRB Analysis

free study guide or the Fading Volatility Breakout (FVB)

free trade signal strategy...I will discuss the reasons (trade strategy) behind those trades

if/when a user of ##TheStrategyLab chat room ask questions about the trades. In contrast, real-time posted trades that are via the

Advance WRB Analysis Tutorial Chapters 4 - 12 or the

Volatility Trading Report (VTR) trade signal strategies...I discuss the reasons (trade strategy) behind those trades with fee-base clients in a different private chat room that's designated

only for fee-base clients or discuss the strategies with fee-base clients on my Skype contact list.

Also, posted below are direct links to information about my

price action trade methodology and

trading plan (there's a difference between the two) that enables me to identify key trading areas in the price action that represent changes in supply/demand and volatility along with being able to exploit these changes via WRB Analysis (wide range body/bar analysis). I'm primarily a day trader because it suits my

personal lifestyle but I do occasionally swing trade and position trade. Simply, my trade method is applicable for position trading, swing trading and day trading.

##TheStrategyLab Chat Room

##TheStrategyLab Chat Room is

free. Members and I use the chat room to post WRB Analysis commentary, real-time trades and to post anything else related to trading. The chat room helps me tremendously in my own trading because I use it to document (journal) general volatility analysis involving WRB Analysis so that I can easily review at a later date my thoughts as I interacted with the markets...info I can not get from my broker statements. Also, this is

not a signal calling chat room where a head trader tells

you when to buy or sell and I do not have the time/energy/resources to manage a signal calling chat room. Access instructions for chat room @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=164 Price Action Analysis via WRB Analysis Tutorials @

http://www.thestrategylab.com/WRBAnalysisTutorials.htm and there's a

free study guide of the WRB Analysis Tutorial Chapters 1, 2 and 3 @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=119&t=718 Trade Signal Strategies via Volatility Trading Report (VTR) @

http://www.thestrategylab.com/VolatilityTrading.htm and there's a

free trade signal strategy @

http://www.thestrategylab.com/tsl/forum/viewforum.php?f=89 so that you can freely test drive one of our price action trade strategies with support (answering your questions)

prior to purchasing the Volatility Trading Report (VTR).

Trading Plan Daily Routine @

http://www.thestrategylab.com/tsl/forum/viewtopic.php?f=246&t=2502 -----------------------------

Market Context Summaries The below summaries by

Bloomberg,

CNNMoney,

Reuters and

Yahoo! Finance helps me to do a quick review of the fundamentals,

FED/

ECB/

BOE/

IMF actions or any important global economic events (e.g.

Eurozone,

MarketWatch.com) that had an impact on today's price action in many trading instruments I monitor during the trading day. Simply, I'm a strong believer that key market events causes key changes in supply/demand and volatility resulting in

trade opportunities (swing points and strong continuation price actions) that reach profit targets. Thus, I pay attention to these key market events, intermarket analysis (e.g. Forex EurUsd, EuroFX 6E futures, Gold GC futures, Light Crude Oil (WTI) CL & Brent Oil futures, Eurex DAX futures, Euronext FTSE100 futures, Emini ES futures, Emini TF futures, Treasury ZB futures and U.S. Dollar Index futures) while using WRB Analysis from one trade to the next trade to give me the

market context for price action trading before the appearance of my

technical analysis trade signals. Therefore, I maintain these

archives to allow me to understand what was happening on any given trading day

in the past involving key market events to help better understand my trade decisions (day trading, swing trading, position trading)...something I can

not get from my broker statements alone. Further, most financial websites remove (delete) their archives after a few years to make room for new content. Therefore, I maintain my own archives of the news content so that I have it available for me when financial websites no longer archives their content.

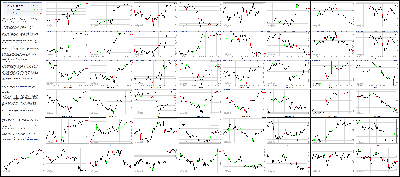

Attachment:

092414-Key-Price-Action-Markets.png [ 1.2 MiB | Viewed 290 times ]

092414-Key-Price-Action-Markets.png [ 1.2 MiB | Viewed 290 times ]

click on the above image to view today's price action of key markets Yahoo! Finance 4:15 pm: [BRIEFING.COM] The stock market ended the midweek session on an upbeat note despite enduring a shaky start to the day. The S&P 500 rose 0.8% with nine sectors posting gains, while the Nasdaq Composite (+1.0%) outperformed.

Equity indices spent the initial 90 minutes of action near their flat lines with the S&P 500 briefly pressured to its 50-day moving average (1976.58) by the early weakness in the energy sector (+0.04%). The growth-sensitive group was down in excess of 1.0% in the early going, but charged into positive territory during afternoon action. Crude oil went along for the afternoon ride, climbing 1.6% to $93.03/bbl.

The test of the 50-day moving average invited dip buyers into the fold, while the relative strength of high-beta areas like biotechnology and chipmakers emboldened their efforts. Furthermore, a well-timed report from the Wall Street Journal indicating China may replace the People's Bank of China Governor Zhou with someone more dovish provided an added measure of support.

The health care sector (+1.7%) seized the lead at the start and held its ground throughout the day to pad its September advance to 2.4%. Biotechnology fueled the rally with the iShares Nasdaq Biotechnology ETF (IBB 279.29, +7.67) climbing 2.8% to a fresh record high.

Conversely, the surge in biotech gave a boost to the Nasdaq, which ended ahead of the broader market even as the top-weighted index component-Apple (AAPL 101.73, -0.91)-spent the day in the red. Chipmakers picked up some of the slack with the PHLX Semiconductor Index climbing 1.2%. Micron (MU 32.22, +1.02) was a notable outperformer amid reports the company has discussed a potential joint venture with Advanced Semiconductor (ASX 6.02, 0.00).

Elsewhere, the consumer discretionary sector (+1.0%) finished among the leaders despite underperforming early. However, homebuilders were unable to participate following a disappointing quarterly report from KB Home (KBH 16.07, -0.90). The stock lost 5.3% and pressured its peers in the early going, but the group was able to trim its losses after a better than expected New Home Sales report crossed the wires (504K; Briefing.com consensus 435K). The iShares Dow Jones US Home Construction ETF (ITB 23.15, -0.05) settled lower by 0.2%.

Treasuries attempted to turn positive just ahead of the housing data, but were rebuffed. The 10-yr note spent the entire day in the red, ending near the lows with its yield up four basis points at 2.56%.

Today's session was met with above-average participation with more than 730 million shares changing hands at the NYSE.

Economic data included New Home Sales and the MBA Mortgage Index:

New home sales jumped 18.0% in August to 504,000 from an upwardly revised 427,000 (from 412,000), while the Briefing.com consensus expected an increase to 435,000

That was the first time that new home sales surpassed 500,000 since May 2008, and the increase was in-line with the spike in the September NAHB home builder index, which reached its highest point since November 2005

With the exception of the Midwest region, which was flat, sales growth was extremely strong across the U.S. That included a 50.0% increase in sales in the West and a 29.2% increase in the Northeast.

The weekly MBA Mortgage Index fell 4.1% to follow last week's 7.9% spike

Tomorrow, weekly Initial Claims (Briefing.com consensus 300K) and Durable Orders for August (consensus -16.3%) will be released at 8:30 ET.

Nasdaq Composite +9.1% YTD

S&P 500 +8.1% YTD

Dow Jones Industrial Average +3.8% YTD

Russell 2000 -3.2% YTD

3:30 pm: [BRIEFING.COM] Dec gold spent most of today's session chopping around in negative territory while the dollar index strengthened to four year highs. The yellow metal touched a session high of $1224.60 per ounce in mid-morning action but quickly retreated back into the red. It traded as low as $1216.20 per ounce and eventually settled with a 0.2% loss at $19.60 per ounce.

Dec silver also traded in the red, slipping as low as $17.51 per ounce in morning action. Unable to gain momentum, it settled with a 0.5% loss at $17.69 per ounce. The metal touched new four year lows earlier this week.

Nov crude oil extended yesterday's gains as it rose on the stockpile report released this morning. The EIA reported that for the week ending Sep 19, crude oil inventories had a draw of 4.273 mln barrels when consensus called for a build of 0.4-0.8 mln barrels. The energy component traded as low as $91.12 per barrel in early morning pit trade but gained steam in afternoon action. It touched a session high of $92.95 per barrel moments before settling with a 1.4% gain at $92.86 per barrel.

Nov natural gas trended higher after lifting from a session low of $3.86 per MMBtu in morning action. It eventually settled at its session high of $3.97 per MMBtu, or 2.6% higher.

3:00 pm: [BRIEFING.COM] The S&P 500 trades higher by 0.8% with one hour remaining in the session. The benchmark index spent the early part of the session near its flat line, but was able to stage a turnaround just north of its 50-day moving average (1977) before finding resistance at the 20-day average (1997.86).

Elsewhere, the Russell 2000 (+0.9%) trades in line with the benchmark index, but the small-cap average is roughly 20 points below closely-watched levels like its 50- and 200-day moving averages. Given its current standing, the index trades near early August levels.

Also of note, Treasuries have slid to lows, pushing the 10-yr yield up to 2.57% (+4 bps).

2:30 pm: [BRIEFING.COM] Not much change in the major averages as they continue hovering near their best levels of the day. Today's economic data was limited to just two releases, which will also be the case tomorrow.

Weekly Initial Claims (Briefing.com consensus 300K) and the August Durable Orders report (consensus -16.3%) will both be released at 8:30 ET.

A quiet week of data will wrap up on Friday with the third estimate of Q2 GDP (consensus 4.6%) and the final release of the Michigan Sentiment survey for September (expected 85.0).

2:00 pm: [BRIEFING.COM] The S&P 500 (+0.6%) has inched up to a fresh session high as the quiet afternoon continues. The health care sector (+1.5%) remains in the lead with the iShares Nasdaq Biotechnology ETF (IBB 278.81, +7.19) now trading at its all-time high.

Elsewhere among influential groups, the discretionary sector (+0.8%) outperforms, while financials (+0.4%) and industrials (+0.4%) lag. The industrial sector has been weighed down by defense contractors in recent days. Today, the PHLX Defense Index trades up 0.3% after reclaiming its 50-day moving average.

Meanwhile, transport stocks have been able to keep pace with the S&P 500. The Dow Jones Transportation Average is higher by 0.6%.

1:25 pm: [BRIEFING.COM] On Tuesday the stock market tried to rebound early. It failed and selling efforts picked up. Today there was an attempt to drive the stock market down early. It failed and buying efforts picked up.

The notable point about today's early retreat is that it was stopped just above the S&P 500's 50-day moving average. The hold of that important technical support area ignited some buy-the-dip interest that began to feed on itself as short-covering activity kicked in.

The major indices are currently sitting near their best levels of the session, supported by broad-based gains and recent remarks from Chicago Fed President Evans who said the Fed should be "exceptionally patient in adjusting the stance of US monetary policy... even to the point of allowing a modest overshooting of our inflation target."

Separately, the $35 billion 5-yr note auction was met with tepid demand. It drew a high yield of 1.80% on a 2.56 bid-to-cover ratio versus the prior 12-auction average of 2.73. The benchmark 10-yr note didn't move much after the auction results as it remains down five ticks for the day with its yield at 2.54%.

1:00 pm: [BRIEFING.COM] The stock market holds a midday gain with the key indices hovering near their best levels of the session. The S&P 500 trades higher by 0.4% with eight sectors in the green, while the Nasdaq Composite (+0.6%) displays relative strength.

Equity indices spent the first 90 minutes of the session near their flat lines with the relative weakness of the energy sector (-1.0%) fueling a brief dip into the red. The sector has been pressured by continued dollar strength, which has impeded earnings prospects of multinational energy names like Chevron (CVX 121.22, -1.84) and ExxonMobil (XOM 95.14, -0.89). Including today's loss, the energy space is down 6.9% so far in September.

However, the underperformance of energy has been masked by relative strength in other influential areas like consumer discretionary (+0.4%), technology (+0.3%), and health care (+1.3%). In addition, a report from the Wall Street Journal indicating China may replace the People's Bank of China Governor Zhou with someone more dovish provided another measure of support.

Most notably, the health care sector has held the lead since the start with a significant boost from biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 277.18, +5.56) trades up 2.1% near its all-time high registered on September 2 (278.78).

Furthermore, the outperformance of biotech has led to the relative strength of the Nasdaq Composite (+0.6%). Chipmakers have also chipped in as evidenced by a 0.8% gain for the PHLX Semiconductor Index. As for top-weighted tech names, Google (GOOGL 597.60, +6.42) and Microsoft (MSFT 46.79, +0.23) outperform, while the largest Nasdaq component by weight-Apple (AAPL 101.78, -0.86)-sits in the red.

Treasuries hover near their overnight lows after failing to turn positive during the past two hours. The 10-yr yield is higher by one basis point at 2.54%.

Economic data included New Home Sales and the MBA Mortgage Index:

New home sales jumped 18.0% in August to 504,000 from an upwardly revised 427,000 (from 412,000), while the Briefing.com consensus expected an increase to 435,000

That was the first time that new home sales surpassed 500,000 since May 2008, and the increase was in-line with the spike in the September NAHB home builder index, which reached its highest point since November 2005

With the exception of the Midwest region, which was flat, sales growth was extremely strong across the U.S. That included a 50.0% increase in sales in the West and a 29.2% increase in the Northeast

The weekly MBA Mortgage Index fell 4.1% to follow last week's 7.9% spike

12:30 pm: [BRIEFING.COM] The S&P 500 has spent the past hour in a sideways drift just below its best level of the session.

The health care sector (+1.3%) spiked in the early going and has maintained its lead with significant help from biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 277.54, +5.92), which trades higher by 2.2%, has approached its record high from September 2 (278.78).

Outside of health care, the consumer staples sector (+1.1%) is the only other group with a gain of 1.0% or more. Meanwhile, the remaining countercyclical sectors-telecom services (+0.2%) and utilities (-0.1%)-trail the broader market.

Elsewhere, Treasuries have returned to their lowest levels of the day with the 10-yr yield now up two basis points at 2.54%.

12:00 pm: [BRIEFING.COM] Equity indices remain bid with the S&P 500 (+0.5%) trading within two points of its session high.

At this juncture, three of six cyclical sectors trade in-line or ahead of the broader market, while the other three have struggled to keep up. Interestingly, the consumer discretionary sector (+0.5%) is showing relative strength after being among the early laggards.

In part, the early weakness stemmed from a disappointing quarterly report from KB Home (KBH 15.77, -1.20). The stock has tumbled 7.1%, while the iShares Dow Jones US Home Construction ETF (ITB 23.02, -0.18) saw a brief spike to its flat line following today's better than expected New Home Sales report for August. The ETF has since returned into the middle of its range and currently trades lower by 0.8%.

Furthermore, retail stocks have overshadowed the losses among homebuilders. The SPDR S&P Retail ETF (XRT 86.68, +0.50) trades up 0.6%.

11:30 am: [BRIEFING.COM] The major averages have climbed to new highs with the Nasdaq Composite (+0.5%) and Russell 2000 (+0.5%) pacing the rally. High-beta names have contributed to the outperformance of the two indices.

The tech-heavy Nasdaq has drawn strength from chipmakers (PHLX SOX Index +0.8%) and biotechnology (IBB +1.6%), while influential tech names like Google (GOOGL 596.10, +4.92), Oracle (ORCL 39.04, +0.21), and Microsoft (MSFT 46.77, +0.21) have also contributed to the advance. However, the top-weighted Nasdaq component-Apple (AAPL 102.04, -0.60)-has yet to climb out of the red. The stock trades down 0.6% amid reports the newest iPhone may be prone to bending.

With stocks on highs, participants have reduced some of their hedges, sending the CBOE Volatility Index (VIX 13.98, -0.95) below the 14.00% mark.

10:55 am: [BRIEFING.COM] Equity indices have climbed off their lows and they currently trade near their opening levels.

The weakest sector of the day-energy (-1.0%)-remains at the bottom of the leaderboard despite a recent spike in crude oil. The energy component trades up 0.4% at $91.85/bbl even with the Dollar Index (+0.4%; 85.00) showing notable strength. Conversely, the stronger dollar has pressured multinational energy companies like Philips 66 (PSX 82.21, -1.05) and Valero (VLO 45.90, -1.23).

On the upside, the health care sector (+0.8%) shares the lead with consumer staples (+0.8%). Of the two, health care has been boosted by biotechnology. The iShares Nasdaq Biotechnology ETF (IBB 275.69, +4.07) trades higher by 1.5%.

Elsewhere, Treasuries remain in the red after a failed attempt at turning positive. The 10-yr yield is higher by one basis point at 2.53%.

10:35 am: [BRIEFING.COM] Precious metals are trading lower this morning while the dollar index adds to gains.

Dec gold touched a session low of $1216.80 moments after equity markets opened and is now down 0.1% at $1220.70.

Dec silver traded as low as $17.51 earlier in the session and is currently 0.8% lower at $17.64.

Nov crude oil pulled back from its session high of $91.79 and brushed a session low of $91.12. It rose slightly on inventory data that showed a draw of 4.273 mln barrels when a build of 0.4-0.8 mln barrels was anticipated. It is currently down 0.1% at $91.51.

Nov natural gas pulled back from its session high of $3.89 and briefly chopped around just below the unchanged line. It is currently trading flat at $3.87.

10:05 am: [BRIEFING.COM] The S&P 500 has surrendered its opening gain amid continued weakness in the energy sector (-1.0%) and recent weakness in cyclical groups like financials (unch), industrials (-0.1%), and technology (-0.1%).

New home sales in August hit an annualized rate of 504,000, which was up from the revised July rate of 427,000 (from 412,000), and better than the rate of 435,000 that had been broadly expected by the Briefing.com consensus.

9:40 am: [BRIEFING.COM] Equity indices climbed out of the gate despite the early weakness in the energy sector (-0.8%). However, the growth-sensitive sector is the only laggard of note, while seven of the remaining nine groups hold gains.

The S&P 500 trades higher by 0.1% with the health care sector (+0.6%) providing early leadership. Biotechnology has factored into the advance with the iShares Nasdaq Biotechnology ETF (IBB 274.25, +2.63) up 1.0%.

Elsewhere, heavily-weighted consumer discretionary (+0.3%) and financials (+0.2%) have also displayed early strength.

Treasuries have extended their losses, pushing the 10-yr yield up to 2.54%.

9:13 am: [BRIEFING.COM] S&P futures vs fair value: +0.60. Nasdaq futures vs fair value: +2.50. The stock market is on track for a flat open as futures on the S&P 500 trade within a point of fair value after surrendering their modest gains. The benchmark index will enter the midweek session little changed after giving up 1.4% over the past two days.

Despite the flat indication, homebuilder shares are expected to display early weakness after KB Home (KBH 15.72, -1.25) reported disappointing earnings. The stock holds a pre-market loss of 7.4%, while peers PulteGroup (PHM 18.00, -0.41) and DR Horton (DHI 20.89, -0.39) are both down near 2.0%.

The industry group could be on the move once again with the New Home Sales report for August (Briefing.com consensus 435K) set to cross the wires at 10:00 ET.

Elsewhere on the earnings front, Accenture (ACN 77.60, -2.00) is indicated to open lower by 2.5% after missing earnings estimates.

Treasuries have spent the entire night in the red and they continue holding modest losses at this time with the 10-yr yield up one basis point at 2.54%.

9:04 am: [BRIEFING.COM] S&P futures vs fair value: -0.30. Nasdaq futures vs fair value: +1.00. The S&P 500 futures trade within a point of fair value.

Markets ended mixed across Asia. The Reserve Bank of Australia warned of an overheating housing market. Elsewhere, the Japanese yen strengthened after Prime Minister Shinzo Abe said he would like to see caution in assessing the impact of recent yen weakness on local economies. The dollar/yen pair fell about 30 pips to the 108.50 area, but has reclaimed that loss.

In economic data:

Japan's Manufacturing PMI slipped to 51.7 from 52.4 (expected 52.5)

Australia's CB Leading Index came in at 0.5% (previous 0.2%)

New Zealand's trade surplus expanded to $2.02 billion from $1.29 billion (expected surplus of $1.22 billion)

------

Japan's Nikkei shed 0.2% to continue backtracking from its best levels of the year. Heavyweight Softbank continued to reel following the Alibaba IPO as shares gave up another 3.5%, and are now down 11.4% since September 19.

Hong Kong's Hang Seng added 0.4%, ticking up from two-month lows. However, casino names were unable to gain traction as Sands China fell 1.6% and Galaxy Entertainment lost 1.5%.

China's Shanghai Composite gained 1.5% to finish at its best level since March 2013. Brokerage names led the advance as a surge in the number of new trading accounts caused a limit up, 10%, spike.

India's Sensex slipped 0.1% off record highs. Financials lagged as State Bank of India and ICICI Bank gave up 2.7% and 1.4%, respectively.

Major European indices trade mostly higher with Italy's MIB (+0.9%) in the lead. The euro slumped following the disappointing Ifo Index from Germany. The single currency hovers near 1.2825 against the dollar after trading near 1.2860 ahead of the report.

Economic data was limited:

Germany's Ifo Business Climate Index fell to 104.7 from 106.3 (expected 105.7) as Current Assessment ticked down to 110.5 from 111.1 (consensus 110.2) and Business Expectations slipped to 99.3 from 101.7 (expected 101.2)

Italy's Consumer Confidence ticked up to 102.0 from 101.9 (consensus 101.5)

Norway's Unemployment Rate ticked up to 3.4% from 3.3% (expected 3.3%)

------

Great Britain's FTSE is higher by 0.1% with miners showing strength for the second consecutive day. Fresnillo and Rio Tinto sport respective gains of 2.4% and 1.3%. Financials lag with Aberdeen Asset Management down 0.7% and Old Mutual lower by 1.1%.

Germany's DAX trades up 0.2% with Merck KGaA in the lead. The stock trades higher by 3.0%. On the flip side, K+S has tumbled 3.9%. Exporters also lag with Daimler and Volkswagen down 0.3% and 0.7%, respectively.

In France, the CAC has added 0.6%. Oil services providers Technip and Total outperform with respective gains of 2.6% and 1.9%. Airbus Group is the weakest performer, down 1.1%.

Italy's MIB trades higher by 0.9%. Telecom Italia and ENI are among the leaders with gains close to 2.0% apiece.

8:29 am: [BRIEFING.COM] S&P futures vs fair value: +2.60. Nasdaq futures vs fair value: +7.00. The S&P 500 futures continue drifting near their best levels of the morning. If the current gain holds, the benchmark index will be able to make a small dent in its week-to-date loss after surrendering 1.4% over the past two sessions.

The dollar index, meanwhile, is on track to enter the equity session at its best level of the morning (+0.2% to 84.79). The greenback has charged higher overnight at the expense of the euro and the Swiss franc, while the dollar/yen pair is little changed near 108.75. Including today's advance, the Dollar Index is higher by 2.4% this month and up 4.3% since the start of August.

8:00 am: [BRIEFING.COM] S&P futures vs fair value: +2.30. Nasdaq futures vs fair value: +5.70. U.S. equity futures trade modestly higher amid cautious action overseas. The S&P 500 futures hover two points above fair value after spending the entire night in positive territory. The overnight session was relatively quiet with the dollar index inching up to continue its recent strength. The Index is higher by 0.1% today and up 2.4% so far in September.

On the economic front, the weekly MBA Mortgage Index fell 4.1% to follow last week's 7.9% jump, while the New Home Sales report for August (Briefing.com consensus 435K) will cross the wires at 10:00 ET.

Treasuries hold slim losses with the 10-yr yield up one basis point at 2.54%.

In U.S. corporate news of note:

Accenture (ACN 77.51, -2.09): -2.6% after missing bottom-line estimates on better than expected revenue. The company lowered its guidance, but hiked its dividend 10%.

Bed Bath & Beyond (BBBY 66.76, +4.07): +6.5% following its better than expected results and above-consensus Q4 guidance.

Newmont Mining (NEM 24.20, +0.21): +0.9% after updating its production outlook for the year.

Reviewing overnight developments:

Asian markets ended mixed. Hong Kong's Hang Seng +0.4%, China's Shanghai Composite +1.5%, and Japan's Nikkei -0.2%.

In economic data:

Japan's Manufacturing PMI slipped to 51.7 from 52.4 (expected 52.5)

Australia's CB Leading Index came in at 0.5% (previous 0.2%)

New Zealand's trade surplus expanded to $2.02 billion from $1.29 billion (expected surplus of $1.22 billion)

In news:

The Japanese yen strengthened after Prime Minister Shinzo Abe said he would like to see caution in assessing the impact of recent yen weakness on local economies. The dollar/yen pair fell about 30 pips to the 108.50 area, but has since reclaimed the bulk of that loss.

Major European indices trade mostly higher. Germany's DAX +0.1%, France's CAC +0.5%, and Great Britain's FTSE is flat. Elsewhere, Italy's MIB +1.2% and Spain's IBEX +0.1%.

Economic data was limited:

Germany's Ifo Business Climate Index fell to 104.7 from 106.3 (expected 105.7) as Current Assessment ticked down to 110.5 from 111.1 (consensus 110.2) and Business Expectations slipped to 99.3 from 101.7 (expected 101.2)

Italy's Consumer Confidence ticked up to 102.0 from 101.9 (consensus 101.5)

Norway's Unemployment Rate ticked up to 3.4% from 3.3% (expected 3.3%)

Among news of note:

The euro slumped following the disappointing Ifo Index from Germany. The single currency hovers near 1.2835 against the dollar after trading near 1.2860 ahead of the report.

6:19 am: [BRIEFING.COM] S&P futures vs fair value: +1.00. Nasdaq futures vs fair value: +2.00.

6:19 am: [BRIEFING.COM] Nikkei...16,167.45...-38.50...-0.20%. Hang Seng...23,921.61...+84.50...+0.40%.

6:19 am: [BRIEFING.COM] FTSE...6,660.82...-15.20...-0.20%. DAX...9,577.63...-17.40...-0.20%.

Treasuries Drop as U.S. Sells $35 Billion in 5-Year Notes By Cordell Eddings Sep 24, 2014 5:07 PM ET

Treasuries fell for the first time in five days as the U.S. received the lowest demand at a five-year note auction this year with investors speculating the Federal Reserve is moving closer to raising interest rates.

The $35 billion sale’s bid-to-cover ratio, which gauges demand by comparing total bids with the amount of securities offered, was 2.56, the lowest since December and versus an average of 2.75 for the past 10 sales. The Fed’s 22 primary dealers were left with 41 percent of the notes, the most since January. Government securities headed for the steepest monthly loss this year after central-bank officials raised their median forecast for borrowing costs.

“The weak auction is reflecting a market that realizes that we are at a crossroads -- the Fed seems on course to raise rates,” said Carl Lantz, head of interest-rate strategy in New York at Credit Suisse Group AG, which as a primary dealer is obligated to bid at U.S. auctions. “The market is finally starting to trade with that in mind, and it’s clear that time isn’t on your side anymore.”

The benchmark Treasury 10-year yield rose four basis points, or 0.04 percentage point, to 2.57 percent as of 5 p.m. New York time after dropping nine basis points the previous four days, according to Bloomberg Bond Trader prices. The 2.375 percent note maturing in August 2024 fell 10/32, or $3.13 per $1,000 face value, to 98 11/32.

Current five-year note yields gained four basis points to 1.79 percent.

5-Year SaleToday’s auction was rated a “two” on a scale of one through five, with one being failed, by six of the Fed’s dealers. The securities yielded 1.8 percent, the highest since May 2011 and the same as the forecast in a Bloomberg News survey of six primary dealers.

“It was a fairly weak auction that left dealers having to take down a lot,” said Jason Rogan, managing director of U.S. government trading at Guggenheim Securities, a New York-based brokerage for institutional investors.

Indirect bidders, an investor class that includes foreign central banks, purchased 50.3 percent of the notes, compared with an average of 47.1 percent for the past 10 sales.

Direct bidders, non-primary-dealer investors that place their bids directly with the Treasury, bought 8.8 percent of the notes, the least since July 2013 and versus an average of 14.1 percent for the past 10 auctions.

Notes ‘Punished’Five-year notes have returned 1.7 percent this year, versus a gain of 3.5 percent by the broad Treasuries market, according to Bank of America Merrill Lynch indexes. The five-year securities lost 2.4 percent in 2013, while Treasuries overall fell 3.4 percent.

“The five-year note has been punished because of the change of tone at the Fed,” said Aaron Kohli, an interest-rate strategist in New York at BNP Paribas, another primary dealer. “The fear is that the Federal Open Market Committee will be much more aggressive once they start. And, if you believe they will act, the five-year note will suffer the most.”

Fed policy makers meeting on Sept. 16-17 boosted their median estimate for the benchmark interest rate, which banks charge each other on overnight loans, for the end of 2015 to 1.375 percent, compared with 1.125 percent in June.

Policy makers have also said they may end the central bank’s purchases of Treasury and mortgage debt in October, concluding the program known as quantitative easing the Fed has used to support the economy.

Fed DebateEven so, officials are giving conflicting opinions on the future path of interests rates.

Speaking at an event in Cheyenne, Wyoming, yesterday, Kansas City Fed President Esther George said now is the time to start normalizing rates. Fed Bank of New York President William Dudley argued on Sept. 22 at the Bloomberg Markets Most Influential Summit in New York for “patience” on interest-rate increases, cautioning that “if the dollar were to strengthen a lot, it would have consequences for growth.”

The risk of tighter Fed monetary policy has helped the dollar appreciate this quarter against all 16 of its major peers tracked by Bloomberg. That’s transformed losses into gains for foreign holders of U.S. Treasuries, who own $6 trillion worth.

“If you have a positive view on the U.S. dollar, you may buy bonds to take advantage of that,” said Allan von Mehren, chief analyst at Danske Bank A/S in Copenhagen. “We are moving closer to beginning rate normalization and the market is still softly priced for that.”

Monthly DeclineTreasuries have fallen 0.8 percent this month through yesterday, set for the biggest decline since December, Bloomberg World Bond Indexes (BUSY) show. They have returned 3.7 percent this year, compared with 6.1 percent for investment-grade corporate bonds and 5 percent for mortgage-backed securities, the data show.

At yesterday’s sale of two-year notes, indirect bidders, a class of investors that includes foreign central banks, purchased 40.9 percent of the notes, matching the most since November 2011.

The U.S. will sell $29 billion of seven-year fixed-rate securities tomorrow.

The Treasury also sold $13 billion of two-year floating-rate notes today at a high discount margin of 0.041 percent, compared to 0.055 percent last month. The securities drew bids for 4.45 times the amount available, versus 4.38 last month and a 4.73 average over the eight offerings of the notes since they were introduced in January.

To contact the reporter on this story: Cordell Eddings in New York at

ceddings@bloomberg.netTo contact the editors responsible for this story: Dave Liedtka at

dliedtka@bloomberg.net Kenneth Pringle, Greg Storey

Special thanks to Bloomberg, CNNMoney, Reuters and Yahoo! Finance for their market summaries.

Best Regards,

M.A. Perry

Trader and Founder of

WRB Analysis (wide range body/bar analysis)

@ http://twitter.com/wrbtrader

@ http://twitter.com/wrbtrader  @ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com

@ http://stocktwits.com/wrbtraderhttp://www.thestrategylab.com Phone: +1 708 572-4885

Business Hours: 8am - 5pm est (Mon - Fri)

Skype Messenger: kebec2002

questions@thestrategylab.com Go Back To TheStrategyLab.com Homepage